Oilfield Drill Bits Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

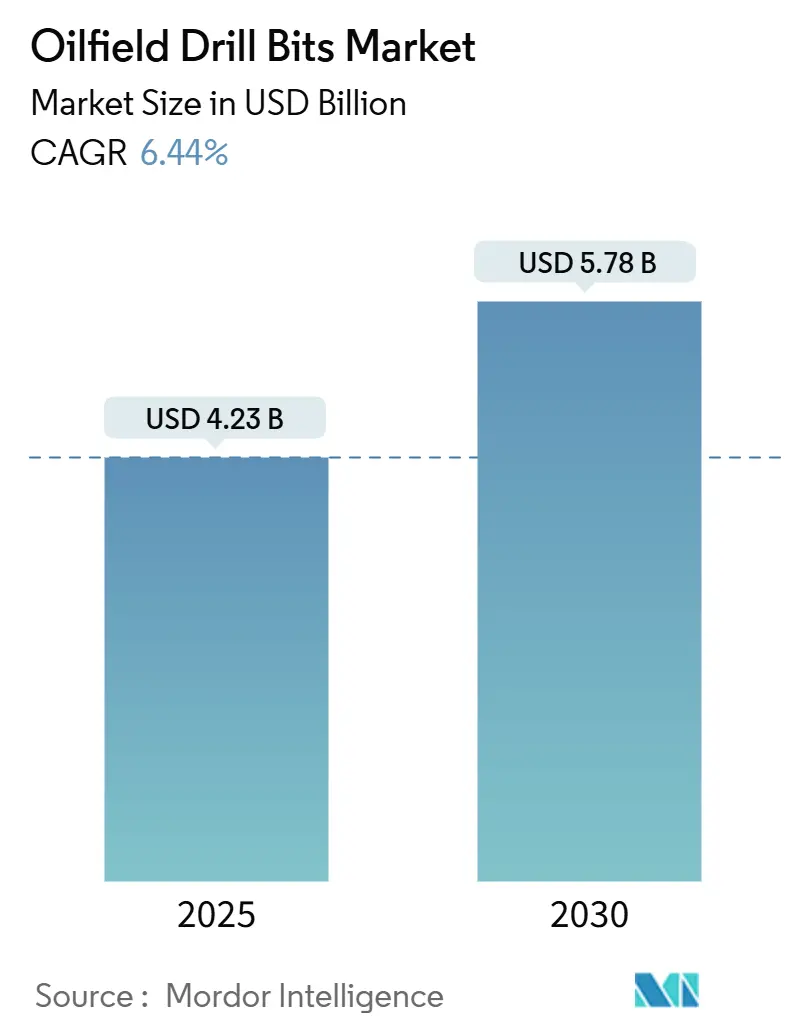

| Market Size (2025) | USD 4.23 Billion |

| Market Size (2030) | USD 5.78 Billion |

| Growth Rate (2025 - 2030) | 6.44% CAGR |

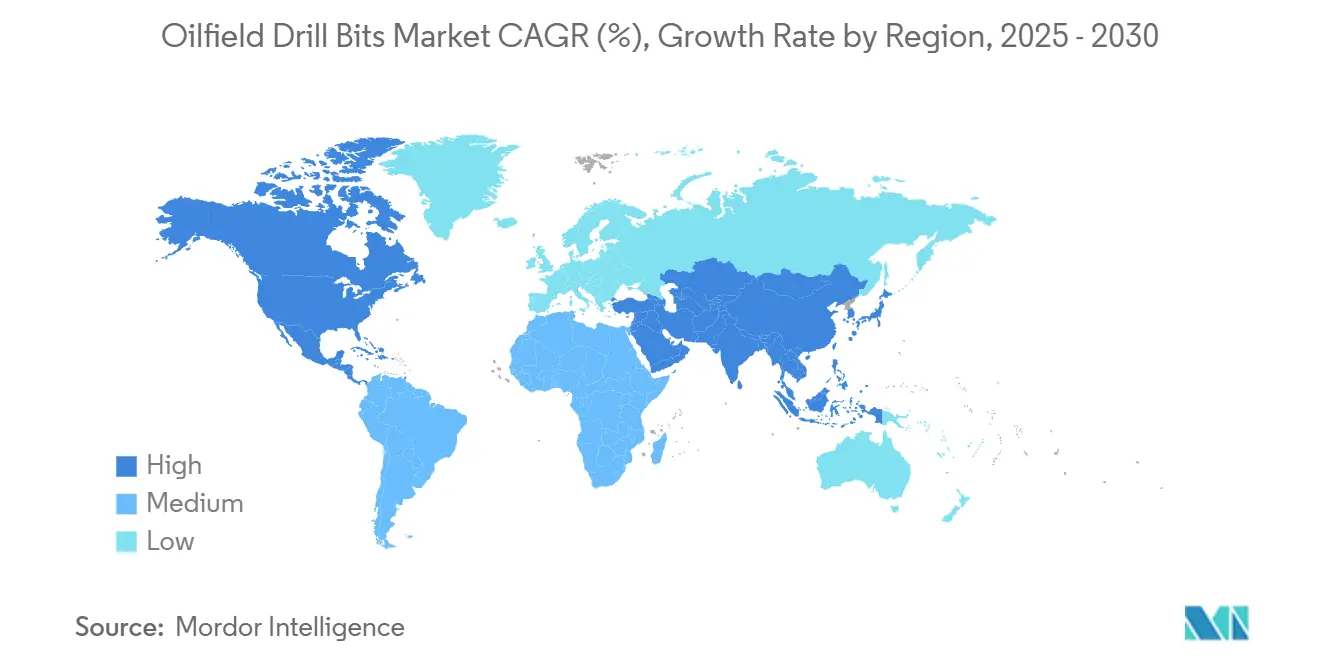

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

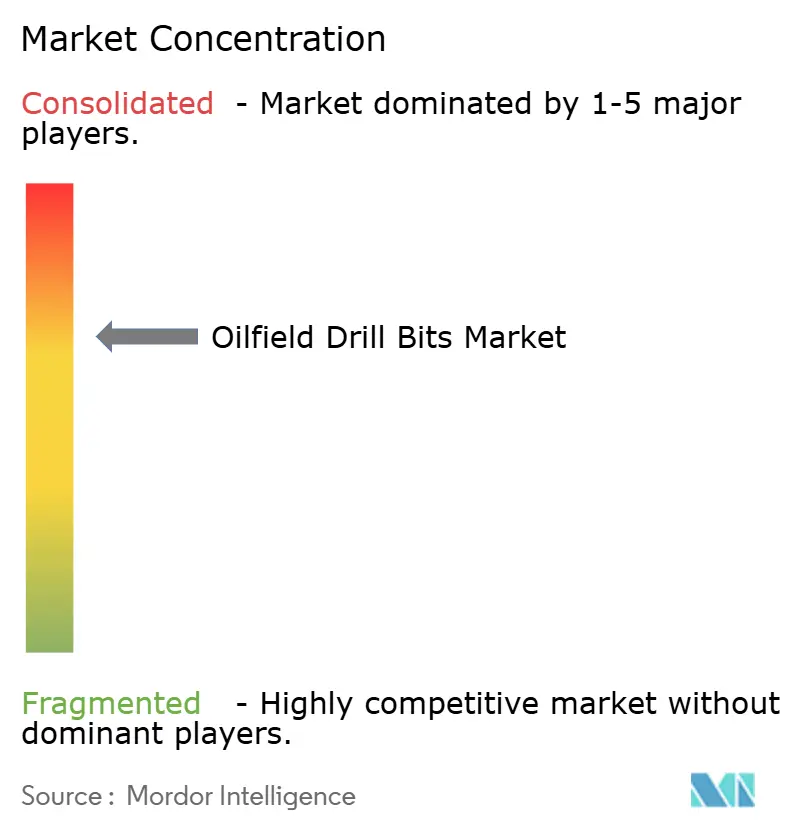

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oilfield Drill Bits Market Analysis by Mordor Intelligence

The Oilfield Drill Bits Market size is estimated at USD 4.23 billion in 2025, and is expected to reach USD 5.78 billion by 2030, at a CAGR of 6.44% during the forecast period (2025-2030).

Solid offshore spending commitments, sustained shale drilling programs, and rapid advances in cutter metallurgy anchor the growth trajectory of the oilfield drill bits market. Operators are prioritizing higher-rate-of-penetration (ROP) tools that shorten drilling cycles, while contractors favor integrated digital platforms that reduce non-productive time. Hybrid bit designs, AI-enabled bit performance analytics, and expanded budgets from national oil companies (NOCs) across the Middle East and Asia-Pacific have emerged as powerful demand catalysts. At the same time, downstream price discipline and the industry’s pivot toward deeper and hotter reservoirs underscore the need for premium drill-bit technologies capable of withstanding extreme environments. Although crude-price volatility, stricter cutting-disposal rules, and the adoption of casing-while-drilling act as headwinds, most producers continue to allocate capital to projects with breakeven economics below projected price floors, thereby preserving order visibility for suppliers across the oilfield drill bits market.[1]U.S. Energy Information Administration, “Short-Term Energy Outlook July 2025,” eia.gov

Key Report Takeaways

- By type, fixed-cutter bits held a 42.6% share of the oilfield drill bits market in 2024, whereas hybrid bits are projected to expand at a 9.0% CAGR through 2030.

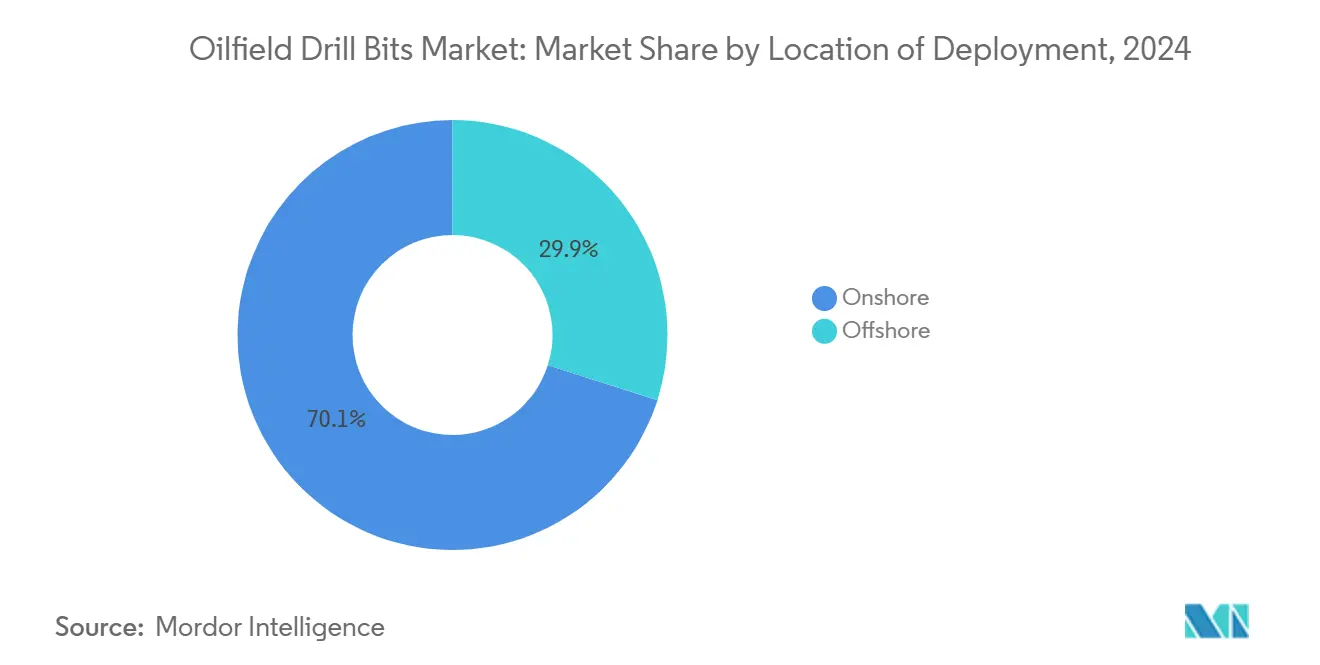

- By location of deployment, onshore drilling accounted for 70.1% of 2024 revenue; offshore applications are expected to grow at an 8.1% CAGR through 2030.

- By application, operators controlled 57.9% of the oilfield drill bits market share in 2024, while drilling contractors showed the fastest CAGR at 7.9% through 2030.

- By geography, North America led with 40.5% of 2024 revenue; Asia-Pacific is forecast to register the highest 8.2% CAGR during 2025-2030.

Global Oilfield Drill Bits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resurgence in offshore deep-water E&P spending | 1.20% | Gulf of Mexico, West Africa, Brazil | Medium term (2-4 years) |

| Shale drilling intensification in North America | 0.90% | Permian, Eagle Ford, Bakken | Short term (≤ 2 years) |

| Advances in PDC-cutter metallurgy boosting ROP | 0.80% | Global | Long term (≥ 4 years) |

| NOC cap-ex rebound in MENA & APAC | 0.70% | Middle East, Asia-Pacific | Medium term (2-4 years) |

| Real-time bit-performance analytics & digital twins | 0.50% | North America, Europe | Long term (≥ 4 years) |

| Geothermal well demand for oilfield-grade bits | 0.30% | North America, Europe, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Resurgence in Offshore Deep-water E&P Spending

Global offshore capital expenditure is projected to exceed USD 300 billion in 2025, led by developments in Asia and the Middle East.[2]Offshore Magazine Editors, “Global Offshore Spending Set to Exceed USD 300 Billion,” offshore-mag.com Shell is expanding its Gulf of Mexico assets, and ExxonMobil has earmarked USD 1.5 billion for Nigerian deep-water work. Deep-water wells require drill bits that can withstand extreme pressures, prompting suppliers like Baker Hughes to introduce enhanced PDC designs with optimized hydraulics. Longer laterals in high-pressure zones magnify bit-life requirements, enabling premium manufacturers to capture higher margins. As fleet utilization tops 80%, service companies find sustainable pricing power, fostering a virtuous investment cycle across the oilfield drill bits market.

Shale Drilling Intensification in North America

Permian Basin output is on track to hit 6.6 million bpd in 2025, up 430,000 bpd from 2023 levels. Productivity gains stem from longer laterals that now exceed 10,000 ft and from advanced fixed-cutter bits that sustain sharpness across mixed lithologies. Newly completed Permian wells delivered 433,000 bpd as of July 2024. HSBC research anticipates U.S. shale growth until 2028, supported by cost-effective drilling of marginal acreage. Such resilience ensures baseline demand for high-performance bits, reinforcing North America’s primacy within the oilfield drill bits market.

Advances in PDC-Cutter Metallurgy Boosting ROP

Next-generation diamond sintering methods have increased cutter abrasion resistance by 270% compared to prior premium grades.[3]OnePetro Technical Papers, “Advances in PDC Cutter Abrasion Resistance,” onepetro.org NOV’s ION+ cutters cut on-bottom time 63% at the FORGE geothermal test site, underscoring crossover potential into high-temperature hydrocarbon wells.[4]Drilling Contractor Staff, “ION+ Cutters Slash Geothermal Drilling Time,” drillingcontractor.org Conical diamond elements accelerated ROP by 200% in hard North Sea formations, validating the economic value of metallurgical innovation for operators. These breakthroughs directly translate into lower drilling cost per foot, spurring technology adoption across every tier of the oilfield drill bits market.

NOC Cap-ex Rebound in MENA & APAC

Saudi offshore spending increased by 22% in 2024 due to expansions of legacy fields. India’s Oilfields Amendment Bill 2024 targets 1,100 offshore wells over five years, encouraging new entrants that favor turnkey drilling packages. China is simultaneously scaling conventional oil, gas, and offshore wind, sustaining broad demand for versatile bit designs. Australia reported a 62% surge in offshore activity, while Malaysia logged 19 discoveries, which increased basin complexity and reinforced the demand for premium tools capable of handling variable pressure regimes. Collectively, these initiatives expand the regional addressable market for oilfield drill bits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility curbing exploration budgets | -1.10% | Global; high impact in North America shale | Short term (≤ 2 years) |

| Casing-while-drilling reducing bit runs per well | -0.80% | North America, North Sea | Medium term (2-4 years) |

| Synthetic-diamond supply chain bottlenecks | -0.40% | Global | Medium term (2-4 years) |

| Stricter cuttings-disposal rules raising costs | -0.30% | North Sea, Gulf of Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Curbing Exploration Budgets

Brent is expected to decline from USD 80/bbl in 2024 to USD 74/bbl in 2025 and USD 66/bbl in 2026. Historically, upstream budgets retreat swiftly when oil averages below USD 70 / bbl, forcing operators to defer marginal prospects. Dallas Fed surveys reveal cautious 2025 capital plans, despite record free cash flow positions. Rystad Energy projects a 2% decline in global upstream investment for 2025, although deep-water spending is expected to rise 3% due to longer-cycle economics. Such mixed signals restrain near-term growth potential in the oilfield drill bits market.

Casing-While-Drilling Reducing Bit Runs Per Well

Tenaris’s iRun Casing system has logged 30 million linear feet across 1,100 U.S. wells, cutting trips and improving cement integrity. Because CwD bits remain in the hole, the number of bits consumed per well falls, shrinking the volume opportunity. North Sea and Gulf of Mexico operators, facing high spread rates, have accelerated the adoption of CwD, intensifying this demand-erosion effect on the oilfield drill bits market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: PDC Technology Keeps the Upper Hand

Fixed-cutter bits accounted for 42.6% of 2024 revenue, driven by the near ubiquity of PDC technology, which powers roughly 70% of global footage drilled. The oilfield drill bits market size for fixed-cutter tools benefits from five decades of incremental cutter and matrix innovation, enabling reliable performance in soft to medium-hard formations. Roller-cone bits remain indispensable in highly abrasive sections where the crushing action outperforms the shearing action. Specialty profiles serve niche tasks such as casing exits and re-entries.

Hybrid bits, which blend roller-cone durability with PDC efficiency, are leading the category with a projected 9.0% CAGR. Baker Hughes’ Kymera series boosts ROP by 24% in interbedded Kuwait formations, trimming 3.5 days per well and showcasing economic value as unconventional plays expand into lithologies that challenge pure PDC or roller cone solutions, hybrid uptake increases. Consequently, suppliers capable of scaling hybrid production stand to capture outsize gains in the oilfield drill bits market.

By Location of Deployment: Offshore Momentum Builds

Onshore operations accounted for 70.1% of 2024 revenue, thanks to shale dominance and low entry costs for land rigs. Competitive day-rate pressures reward bits that deliver faster footage drilled per hour, prompting rapid diffusion of the newest-generation cutters among Permian contractors.

Offshore drilling, although it has a smaller revenue pool, is forecast to grow at an 8.1% CAGR as deep-water breakevens fall below USD 40/bbl and fleet utilization climbs to decade highs. High-temperature, high-pressure (HTHP) wells require robust hydraulics and advanced gauge-protection features, pushing average bit selling prices higher. The resulting mix uplift favors suppliers with offshore-validated product lines, reinforcing premiumization trends across the oilfield drill bits market.

By Application: Contractors Widen Technical Influence

Operators retained 57.9% market share in 2024, leveraging in-house subsurface teams to specify bit programs aligned with reservoir objectives. Long-cycle offshore projects and corporate commitment to safety drive adoption of conservative, field-proven bit designs.

Drilling contractors exhibit the fastest 7.9% CAGR, reflecting a service model where turnkey performance metrics are heavily reliant on bit selection. Contract structures are increasingly tying bonuses to ROP and footage milestones, giving contractors the authority to standardize premium bit portfolios across clients. This purchasing centralization deepens relationships between major contractors and bit suppliers, amplifying the contracting influence within the oilfield drill bits market.

Geography Analysis

North America remained the largest regional contributor, with a 40.5% share in 2024, underpinned by the resiliency of shale drilling and top-tier service infrastructure. U.S. crude output should average 13.7 million bpd in 2025 as the Permian alone contributes 6.6 million bpd, reinforcing baseline procurement for premium cutters. Canadian oil-sands and emerging shale targets sustain demand for hard-rock, appropriately designed bits that can handle stick-slip tendencies and high formation temperatures. The mature services ecosystem accelerates field validation of new bit concepts, shortening commercialization cycles in the oilfield drill bits market.

The Asia-Pacific region is poised to be the fastest-growing region, with an 8.2% CAGR. China’s concerted offshore program and India’s forthcoming 1,100 offshore wells generate a broad spectrum of lithological challenges, from soft deltaic sediments to hard carbonate shelves. Australia’s 62% rise in offshore activity, alongside Malaysia’s 19 discoveries, reflects the expanding breadth of exploration across basin types. Government support packages encourage domestic hydrocarbon development, creating a favorable demand backdrop for suppliers able to localize support services.

Europe’s North Sea is continuing to transition from greenfield expansion to brownfield optimization, channeling bit demand toward erosion-resistant cutters suitable for re-entry and plug-and-abandon work. Stringent environmental policies have elevated interest in water-based mud-compatible bits that resist chemical degradation. The Middle East and Africa benefit from NOC-led offshore investments, notably Saudi Arabia’s 22% cap-ex uplift, while South America’s outlook hinges on Brazil’s pre-salt and Argentina’s Vaca Muerta, both requiring high torque-rated bits capable of stable performance in thick pay sections. Such geographic heterogeneity compels suppliers to maintain versatile portfolios in the oilfield drill bits market.

Competitive Landscape

Market leadership rests with vertically integrated service majors—SLB, Baker Hughes, and Halliburton—that couple proprietary cutter technology with digital performance platforms. SLB’s 2025 acquisition of ChampionX’s MegaDiamond unit secures PDC supply and embeds advanced materials expertise into its design workflow. Halliburton’s LOGIX automation, covering 12 million ft drilled, evidences the performance gains achievable when bit design and downhole parameter control converge.

Mid-tier specialists such as NOV and Varel focus on differentiated cutter geometries and fast customization cycles. NOV’s Phoenix series, featuring ION+ cutters, has demonstrated 63% time savings on geothermal pilots, highlighting cross-sector applicability.

Consolidation among drillers (e.g., Noble’s purchase of Diamond Offshore) reshapes procurement routes, granting larger contractors the leverage to negotiate multi-year bit supply agreements that emphasize total well cost metrics over unit pricing. Simultaneously, rising geothermal investment is attracting new entrants that adapt oilfield-grade bits for renewable applications, further broadening the competitive landscape of the oilfield drill bits market.

Oilfield Drill Bits Industry Leaders

Schlumberger Limited

Baker Hughes Company

Halliburton Company

National Oilwell Varco

Varel Energy Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tenaris announced that its iRun Casing system has exceeded 30 million feet of installed casing across 1,100 U.S. wells, underscoring the growth of CwD and its implications for bit consumption.

- April 2025: Halliburton and Nabors completed the first fully autonomous rotary and slide drilling sequence in Oman using LOGIX and SmartROS, marking a milestone in closed-loop drilling.

- April 2025: Baker Hughes introduced Hummingbird all-electric cementing units and SureCONTROL Plus valves to cut emissions and maintenance costs in onshore and offshore well construction.

- April 2025: SLB debuted its EWC electric well-control technology and secured a North Sea FEED contract for a custom BOP control system, reinforcing the trend towards electrification.

Global Oilfield Drill Bits Market Report Scope

| Roller-Cone Bits |

| Fixed-Cutter Bits |

| Hybrid Bits |

| Specialty Bits (Core, Reaming) |

| Onshore |

| Offshore |

| Oil and Gas Operators |

| Oilfield Service Companies |

| Drilling Contractors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Roller-Cone Bits | |

| Fixed-Cutter Bits | ||

| Hybrid Bits | ||

| Specialty Bits (Core, Reaming) | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Application | Oil and Gas Operators | |

| Oilfield Service Companies | ||

| Drilling Contractors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected 2030 value of the oilfield drill bits market?

The market is forecast to reach USD 5.78 billion by 2030, expanding at a 6.44% CAGR.

Which bit type currently dominates global drilling programs?

Fixed-cutter bits leveraging PDC technology accounted for 42.6% of 2024 revenue, making them the dominant category.

Why are hybrid drill bits gaining traction?

Hybrid designs combine PDC cutters with roller-cone elements, delivering up to 24% higher ROP in mixed formations and are projected to grow at a 9.0% CAGR.

Which region is expected to see the fastest market growth?

Asia-Pacific is set to rise at an 8.2% CAGR through 2030, driven by offshore expansion and rising domestic energy demand.

How is digital technology influencing bit performance?

AI-enabled platforms such as Halliburton’s LOGIX and SLB’s Neuro geosteering optimize drilling parameters in real time, achieving up to 30% ROP gains and reducing unplanned trips.

What impact does casing-while-drilling have on bit demand?

CwD reduces the number of required bit runs per well, lowering overall bit consumption but increasing demand for specialized drillable bits.

Page last updated on: