Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.19 Billion |

| Market Size (2031) | USD 13.52 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

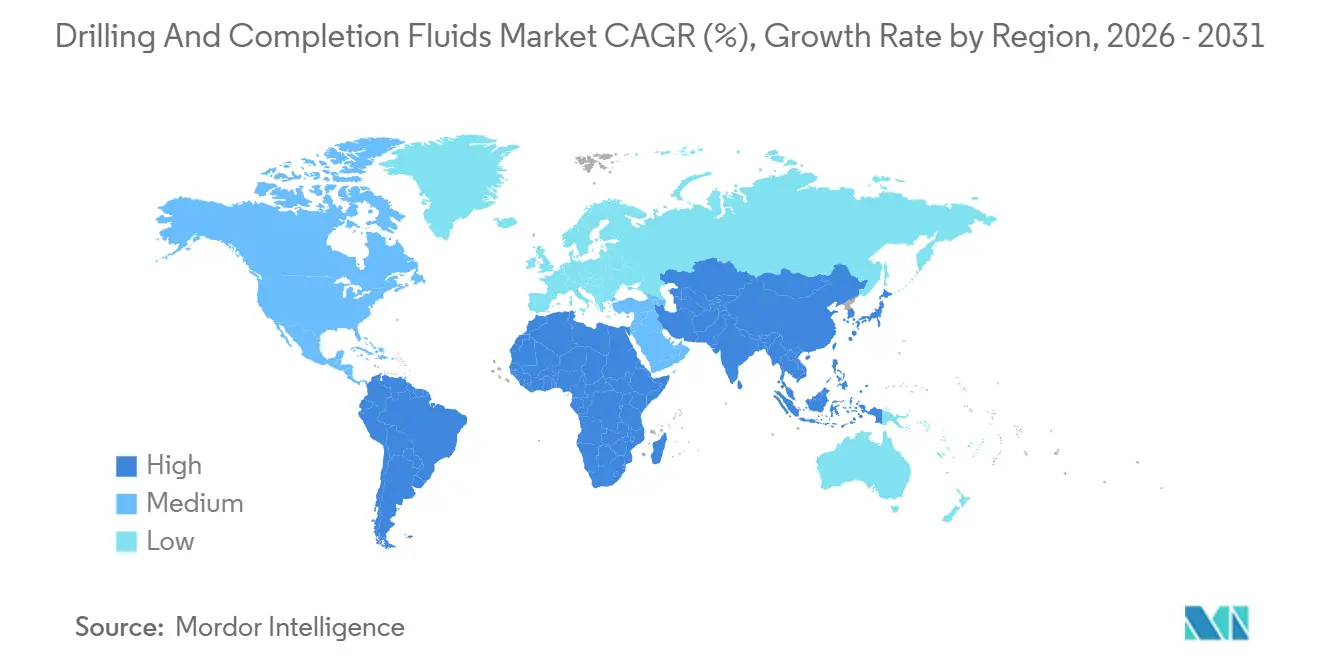

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drilling And Completion Fluids Market Analysis by Mordor Intelligence

The Drilling And Completion Fluids Market size is expected to grow from USD 10.73 billion in 2025 to USD 11.19 billion in 2026 and is forecast to reach USD 13.52 billion by 2031 at 3.85% CAGR over 2026-2031.

Intensifying deep-water work, unconventional reservoir expansion, and stricter environmental rules are steering demand away from undifferentiated mud toward engineered fluid systems tailored for equivalent circulating density (ECD) windows, shale inhibition, and real-time rheology control. Water-based formulations still dominate high-volume onshore wells, yet synthetic systems are winning share in high-pressure, high-temperature (HPHT) offshore holes where discharge limits and wellbore stability both matter. Digital optimization platforms that automate additive dosing and predict fluid behavior are tightening the link between fluid performance and drilling efficiency, allowing service companies to defend margins through outcome-based contracts. At the same time, procurement strategies are shifting as national oil companies and independents outsource integrated fluid management to preserve capital for core exploration and production.

Key Report Takeaways

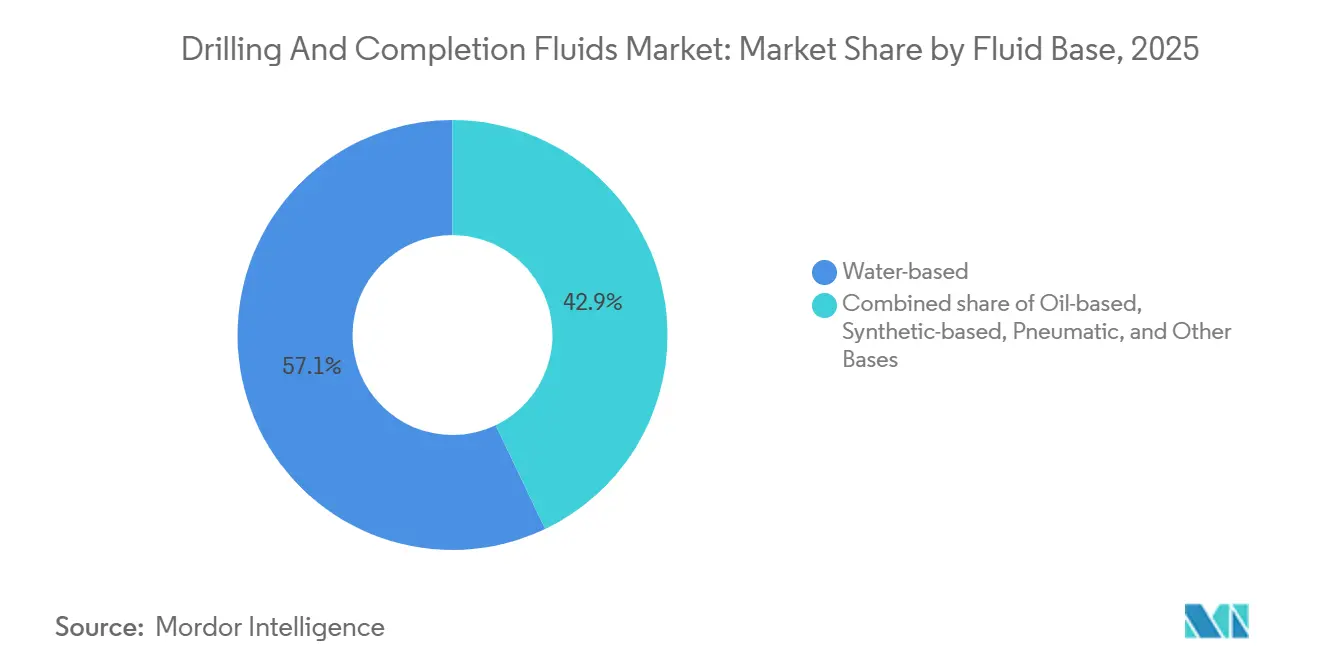

- By fluid base, water-based systems led with 57.1% revenue share in 2025; synthetic-based systems are poised to expand at a 5.8% CAGR through 2031.

- By drilling stage, drilling fluids accounted for 70.5% of the drilling and completion fluids market share in 2025, while completion and work-over fluids are projected to register a 4.9% CAGR to 2031.

- By well type, conventional wells held 64.9% of the drilling and completion fluids market size in 2025, whereas unconventional reservoirs are forecast to grow at a 5.5% CAGR.

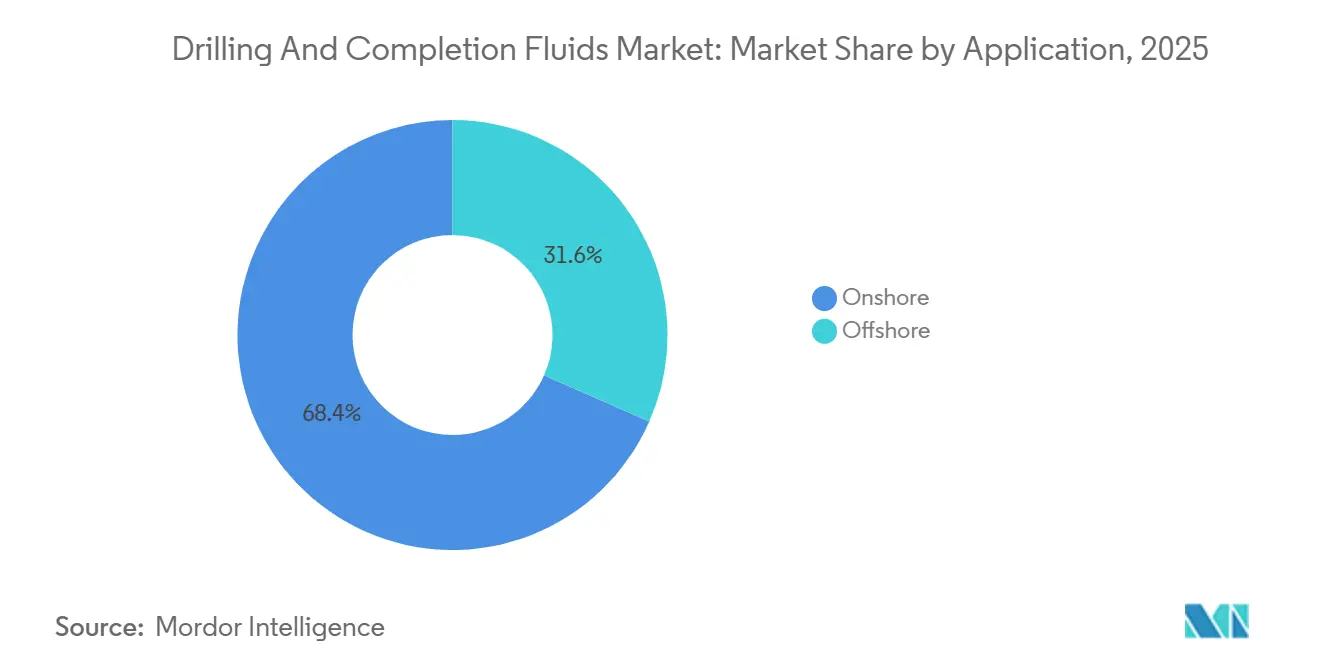

- By application, onshore operations represented 68.4% of 2025 volume, yet offshore activities are set to rise at a 5.1% CAGR through 2031.

- By geography, North America captured 37.7% of 2025 revenue, while Asia-Pacific is expected to clock the fastest 5.7% CAGR to 2031.

- Schlumberger’s M-I SWACO, Halliburton, and Baker Hughes collectively controlled about 55%–60% of the global share in 2025, underscoring a moderately concentrated competitive landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Drilling And Completion Fluids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising deep-water and ultra-deep-water drilling campaigns | 1.2% | Global, concentrated in Gulf of Mexico, Brazil pre-salt, West Africa, Southeast Asia | Medium term (2-4 years) |

| Expansion of unconventional (shale & tight) reservoirs | 1.5% | North America core, spillover to Argentina Vaca Muerta, China Sichuan Basin | Long term (≥ 4 years) |

| Environmental push toward low-toxicity, water-based and synthetic fluids | 0.9% | Europe (North Sea), North America offshore, Asia-Pacific coastal zones | Short term (≤ 2 years) |

| Digitally enabled drilling fluid optimization & real-time rheology control | 0.7% | Global, early adoption in North America shale, Middle East NOC projects | Medium term (2-4 years) |

| Circular-economy models for recycling and re-conditioning spent mud | 0.4% | North America onshore, Europe, Middle East with water scarcity concerns | Medium term (2-4 years) |

| National oil company (NOC) localization programs driving regional fluid manufacturing | 0.6% | Middle East (Saudi Arabia, UAE, Qatar), Asia-Pacific (China, India), Latin America (Brazil, Mexico) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Deep-Water And Ultra-Deep-Water Campaigns Reshape Fluid Specifications

Deep-water wells consume 3,000-5,000 barrels of fluid each and impose HPHT conditions that demand synthetic muds blended with cesium formate brines to achieve ECDs above 18 lb/gal, as seen in Petrobras’ pre-salt programs, where reservoir pressure reaches 15,000 psi.[1]Petrobras Investor Relations, “2025 Operational Results,” petrobras.com Equinor’s Johan Castberg Arctic project showed synthetic systems trimmed non-productive time by 18% under discharge bans on diesel-based mud. TotalEnergies adopted internal-olefin synthetic fluids on Mero 4 to satisfy Brazilian cuttings rules while maintaining shale inhibition.[2]TotalEnergies SE, “Mero 4 Development Update,” totalenergies.com These high-spec wells elevate per-well fluid value and concentrate demand in fewer, but more lucrative, offshore campaigns. Rapid rig mobilization to Namibia and Suriname is expected to reinforce this pattern through the forecast period.

Unconventional Reservoir Expansion Drives Friction-Reducer And Clay-Stabilizer Demand

Extended-reach laterals exceeding 12,000 ft in the Permian Basin rely on polyacrylamide friction reducers to cut pump pressure and torque.[3]U.S. Energy Information Administration, “Drilling Productivity Report,” eia.gov Argentina’s Vaca Muerta uses potassium-chloride muds with encapsulating polymers that lowered wellbore-instability incidents by 22% versus bentonite systems. CNPC achieved 15% faster footage in Ordos tight sand by adding nano-silica sealants that kept fluid loss below 5 mL/30 min.[4]China National Petroleum Corporation, “Annual Report 2025,” cnpc.com.cn These chemistry upgrades also appear in completion fluids, where viscosity breakers and surfactants improve proppant transport and recovery factors.

Environmental Regulations Accelerate Synthetic And Water-Based Fluid Adoption

The UK Offshore Chemicals Regulations now require ≥60% biodegradation in 28 days, eliminating diesel muds from new permits. Norway pushed water-based or synthetic fluids to 89% of wells drilled in 2025 by avoiding the shipment of oil-contaminated cuttings. BOEM rules in the Gulf of Mexico cap polycyclic aromatic hydrocarbons in synthetic bases at 0.1%, forcing reformulation of legacy systems. OSPAR and Brazil’s CONAMA Resolution 393 create region-specific standards, compelling suppliers to run parallel product lines and raising compliance costs that filter through to pricing.

Digital Optimization Platforms Enable Real-Time Fluid Adjustments

Schlumberger’s OPTIDRILL linked downhole sensors with machine learning to cut stuck-pipe events by 31% on Gulf of Mexico wells in 2025. Halliburton’s BaraLogix paired rheology and drilling mechanics to slice drilling time by 14% on Jafurah Basin gas wells. Baker Hughes’ Leucipa spectroscopy system reduced manual mud checks by 70% and additive waste by 18% across six offshore rigs. Such platforms shift competition toward integrated service delivery, rewarding vendors that combine chemistry, sensors, and analytics in a single contract.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil price cycles delaying drilling budgets | -1.1% | Global, acute in North America shale, Latin America, Africa | Short term (≤ 2 years) |

| Stringent discharge regulations on oil-based mud cuttings | -0.6% | Europe (North Sea), North America offshore, Brazil, Southeast Asia | Medium term (2-4 years) |

| Supply chain tightness of specialty polymer & barite additives | -0.5% | Global, acute impact in Asia-Pacific and Europe dependent on Chinese barite exports | Short term (≤ 2 years) |

| Rising adoption of managed-pressure drilling that lowers fluid volumes | -0.3% | North America shale, Middle East HPHT wells, offshore deep-water applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oil Price Volatility Compresses Upstream Capital Allocation

Brent averaged USD 78/bbl in 2025, down from USD 84/bbl in 2024, prompting several Permian independents to park 9% of rigs and defer completions until prices exceed USD 80/bbl, as noted by ConocoPhillips in its Q3 2025 call. The IEA reported upstream capex remaining 15% below 2019 real-terms levels, with discretionary drilling projects bearing the sharpest cuts. West Africa’s active rig count slipped 11% after Angolan and Nigerian programs were postponed under fiscal stress, directly trimming fluid orders. Because fluids make up only 4%-7% of well cost, they are among the first line items downgraded or canceled when operators retrench.

Discharge Regulations Force Costly Fluid Substitutions

EU Marine Strategy revisions obligate member states to achieve “good environmental status” by 2030, forcing a shift from oil-based to synthetic mud even where costs rise USD 150,000-USD 300,000 per well. Chevron’s North Sea unit spent an extra USD 4.2 million on synthetic alternatives across 14 wells in 2025, slicing margins in maturing fields. Brazil’s IBAMA rejected three pre-salt permits in 2025 that proposed oil-based fluids within 50 km of marine reserves, causing six-month project delays. Region-specific mandates fragment the drilling and completion fluids market and inhibit economies of scale in manufacturing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Base: Synthetic Systems Gain Offshore Share

Synthetic-based fluids captured a growing offshore share and are projected to register a 5.8% CAGR to 2031, outpacing the overall drilling and completion fluids market. Water-based products held 57.1% of 2025 revenue, favored in onshore shale where they undercut synthetic prices by 40%-50%. Oil-based muds are retreating as regulators tighten cuttings rules, while pneumatic fluids stay niche at <3% volume. Internal-olefin systems, such as Baker Hughes' SYN-TEQ, handled 350 °F bottom-hole temperatures in Gulf of Mexico lower tertiary wells during 2025. Emerging nano-formulations like Schlumberger's RHELIANT improved lubricity by 24% on Middle East extended-reach wells. These advances underscore how specification-driven demand is concentrating value in premium fluid categories.

Water-based technology also evolves: Halliburton's Baracarb blend attained shale inhibition parity with oil-based muds across 18% of North America's land footage while eliminating disposal fees. Cost-optimized polymer packages allow land operators to trim dilution rates without sacrificing ROP, supporting continued dominance in high-activity basins. Overall, escalating offshore HPHT projects ensure synthetic fluids remain the growth engine of the drilling and completion fluids market, even as water-based systems anchor volume and offer a sustainability narrative that resonates with regulators.

By Drilling Stage: Completion Fluids Command Premium Pricing

Drilling fluids retained 70.5% of 2025 demand, yet completion and work-over fluids are positioned for a faster 4.9% CAGR as reservoir contact quality eclipses pure drilling speed in operator priorities. Formate-based brines used by Occidental in Wolfcamp completions lifted initial production 11%, justifying 30%-40% higher barrel pricing. Multi-stage hydraulic fracturing intensifies density-control requirements, making premium brines and fiber-laden systems indispensable for fracture geometry management. Weatherford’s Frac-Pac fluids enabled real-time fracture mapping on 230 wells in 2025, reinforcing the trend toward integrated fluid-frac workflows.

Drilling fluid innovation nevertheless continues: Newpark’s Evolution biodegradable polymer system cut dilution 19% on Gulf Coast shale wells, lowering total fluid cost despite higher additive unit prices. Blurring lines between drilling and completion workflows encourages long-term, single-provider contracts that bundle both fluid phases, reinforcing the value of holistic fluid engineering throughout the well life cycle.

By Well Type: Unconventional Wells Drive Fluid Innovation

Conventional wells still represented 64.9% of the drilling and completion fluids market size in 2025, but unconventional wells will grow faster at a 5.5% CAGR to 2031. Lateral lengths above 10,000 ft require specialized rheology and cuttings transport; EOG used encapsulating polymers to reduce ECD by 0.4 lb/gal and safely extend Delaware Basin laterals. Saudi Aramco’s Jafurah project introduced potassium-formate fluids to manage HP gas zones while stabilizing Jurassic shales. These complex chemistries generate higher average revenue per well, underpinning fluid spending despite fewer overall holes drilled compared with legacy vertical programs.

Conventional wells remain important in offshore shelf and mature onshore basins where standardized programs curb NPT. Service providers must therefore maintain distinct cost-focused lines for conventional markets and high-spec, additive-rich blends for unconventional work, preventing any single supplier from dominating both segments under a single business model.

By Application: Offshore Demands High-Spec Fluids

Onshore drilling accounted for 68.4% of 2025 volume, but offshore wells are forecast to post a 5.1% CAGR, claiming a larger slice of the drilling and completion fluids market by value. Transocean’s ultra-deepwater rigs required synthetic muds with cesium formate weighting to hit 19.5 lb/gal ECD for Miocene targets. These HPHT demands, plus logistics of pre-mixing and vessel shipping, add a 25%-35% cost premium per barrel relative to onshore.

Onshore fluid innovation turns on circular-economy models: Devon recycled 85% of drilling mud in the Anadarko Basin, saving 1.2 million bbl of freshwater and USD 180,000 per well. Supply-chain efficiency and ESG credentials alike support cost-focused water-based systems in land operations, ensuring balanced growth between the two applications.

Geography Analysis

North America’s market size advantage is anchored in the Permian Basin, but emerging tight-oil plays in Canada and Alaska also deploy digital fluid systems to cut well costs and emissions. Asia-Pacific’s localization surge signals a shift toward shorter supply chains, compelling Western service companies either to build plants or cede share. Europe’s fluid demand is increasingly synthetic; 89% of 2025 Norwegian wells used water-based or synthetic formulations under stricter discharge rules. South America’s pre-salt wells carry some of the highest fluid spend per hole worldwide, explaining sustained vendor investment in Brazilian blending hubs. The Middle East continues to pay premiums for HP high-H₂S completion brines that preserve carbonate reservoir integrity. Africa’s outlook will hinge on fiscal reforms that can reignite shelved exploration in Angola and Nigeria; without them, fluid demand risks under-performance relative to other frontier basins.

Regulatory Landscape

Offshore discharge compliance remains a key determinant of drilling and completion fluid selection, particularly in mature basins with enforceable discharge and toxicity thresholds. In the United States, the EPA regulates offshore discharges in the Gulf of America through the NPDES General Permit GMG290000, which sets limits for parameters including oil and grease and requires toxicity controls for well treatment, completion, and workover (TCW) fluids (including an acute Whole Effluent Toxicity framework with LC50 performance thresholds). In January 2026, the EPA proposed a modification to GMG290000 that would extend the compliance deadline for acute WET testing for TCW fluids from May 11, 2025, to May 11, 2028, easing near-term testing and reporting burdens while maintaining the broader direction toward lower-toxicity formulations.

Well control and operational integrity rules also shape fluid program design and documentation. In US federal offshore operations, BSEE requirements under 30 CFR Part 250 include expectations around maintaining well control and managing drilling fluid programs (including routine inventory and monitoring practices tied to safe operations). In February 2026, BSEE published a proposed rule to revise provisions linked to the 2023 Blowout Preventer Systems and Well Control Rule, clarifying submittal requirements and timeframes for failure data and analysis, which affects how operators and service providers document well control performance alongside fluid management in offshore campaigns.

Value Chain Analysis

The value chain spans upstream raw materials and specialty additives through blending, onsite engineering, and end-of-well waste handling. Key inputs include base fluids and brines, polymers, lubricants, and weighting agents sourced from specialized chemical suppliers, while global and regional service providers formulate and deliver complete fluid systems and integrated fluid management at the rig site. Increasingly, performance differentiation is created at the formulation and engineering layers, where real-time measurement, dosing, and control platforms are bundled into contracts to reduce non-productive time and additive waste.

Manufacturing and logistics are organized around regionalized mixing and supply infrastructure to manage lead times, offshore mobilization, and local content requirements. Operators and service companies rely on micro-plants and blending hubs positioned near major offshore and onshore activity corridors (for example, around established offshore deployment nodes such as Port Fourchon, Rio de Janeiro, and Stavanger), with last-mile delivery and onsite technicians coordinating inventory, solids control, and fluid conditioning. Product and supply-chain decisions are increasingly tied to compliance and lifecycle handling, including formulations that reduce hazardous constituents and completion fluids tailored for deepwater and high-pressure wells, as reflected by new high-density, zinc-reduced completion fluid introductions targeted at deepwater deployments.

Competitive Landscape

Schlumberger’s M-I SWACO, Halliburton, and Baker Hughes captured roughly 55%-60% of global share in 2025, reflecting stronghold positions in offshore and HPHT wells where integrated chemistry, mud engineering, and waste management are vital. These firms leverage proprietary digital suites, OPTIDRILL, BaraLogix, and Leucipa, to lock in long-term contracts that bundle performance guarantees. Regional challengers such as CES Energy Solutions and Newpark Resources exploit cost-advantaged sourcing and pad-drilling logistics in Western Canada and the U.S. shale patch, often pricing contracts on penetration-rate metrics rather than per-barrel volumes.

Strategic moves underline the shifting battlefield: Halliburton bought Al Wusta Drilling Fluids for USD 95 million to deepen Middle East localization, while Schlumberger committed USD 180 million to a Jubail plant that trims Saudi lead times by 30%. Baker Hughes’ graphene-oxide HydraGlyde launch illustrates how nano-additives create performance “white space” for premium pricing. Patent filings concentrate on nano-particle dispersion, biodegradable surfactants, and AI-driven rheology control, signaling that intellectual property and data analytics will decide future competitive advantage as much as chemical supply chains.

Drilling And Completion Fluids Industry Leaders

Schlumberger Limited

Halliburton Company

Baker Hughes Company

Weatherford International plc

Newpark Resources Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Deepwater and ultra-deepwater project execution continues to open opportunities for premium synthetic and high-density completion fluid systems, alongside integrated well construction offerings that bundle drilling, fluids, and digital workflows. Named contract activity provides a visible pull-through for suppliers that can deliver chemistry plus infrastructure: in July 2026, Halliburton was awarded integrated drilling and completions contracts for the GranMorgu deepwater development offshore Suriname, including upgrades to liquid mud and cement plant infrastructure, reinforcing demand for localized blending, reliable additive supply, and high-spec fluid execution in frontier offshore hubs. In May 2026, Baker Hughes announced an extension and expansion of an integrated well construction contract with Petrobras across Brazils Santos Basin, underscoring how operator procurement is consolidating around integrated packages where fluid performance and well construction efficiency are managed together.

Environmental constraints and discharge rules continue to create whitespace for lower-toxicity and more biodegradable additive systems that preserve HPHT performance. Active 2026 research on biodegradable additives sourced from biomass and on advanced nanomaterials (for example, graphene-oxide based multifunctional materials and chitosan-derived nanocomposites) signals a technology pipeline aimed at improving filtration control and thermal stability in water-based muds, which supports product roadmaps for suppliers targeting regulated offshore basins and water-scarce onshore regions. Digitalization also remains a commercialization pathway, as closed-loop and sensor-informed workflows in completions and fluids management broaden the addressable service scope beyond per-barrel chemistry into outcome-linked, automated fluid and fracture execution.

Recent Industry Developments

- May 2026: Weatherford was awarded a deepwater integrated completions contract by Esso Exploration & Production Nigeria Ltd (an ExxonMobil affiliate) for offshore Nigeria. The award expands Weatherfords footprint in deepwater completions where fluids and completion system execution are procured together, supporting bundled offerings that combine completion hardware with specialized fluids and onsite services.

- November 2025: Drilling Specialties, in collaboration with Chevron Phillips Chemical, launched NanoSlide drilling fluid lubricant using a multiphase formulation based on micronized graphene and polyalphaolefins. The introduction targets high-friction, challenging drilling environments where lubricant performance can translate into lower torque, reduced wear, and tighter wellbore stability windows.

- September 2024: SCF Partners completed the acquisition of the Newpark Fluids Systems business from Newpark Resources. The transaction reshaped ownership of a major fluids and integrated fluid management platform, influencing competitive dynamics and capital allocation for product development and regional expansion.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues earned from drilling fluids and completion and work-over fluids used during well drilling, casing and cementing support, and well completion, across onshore and offshore oil and gas activity worldwide.

Scope exclusions: It excludes drilling equipment and solids-control hardware, and it also excludes pure oilfield services revenue that is not tied to fluids supply and related additives.

Segmentation Overview

- By Fluid Base

- Water-based

- Oil-based

- Synthetic-based

- Pneumatic (air, mist, foam)

- Other Bases (ester, glycol, nano-fluids)

- By Drilling Stage

- Drilling Fluids

- Completion and Work-over Fluids

- By Well Type

- Conventional

- Unconventional

- By Application

- Onshore

- Offshore

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Norway

- Russia

- Ukraine

- Rest of Europe

- Asia-Pacific

- China

- India

- ASEAN Countries

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Nigeria

- Algeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base activity picture and to set boundaries around what counts as fluids revenue versus nearby oilfield spend. We relied on public and official sources such as the EIA for drilling and production context, the International Energy Agency for upstream outlook signals, OPEC publications for supply and investment direction, and Baker Hughes rig count releases for near-term activity shifts.

To turn activity into demand drivers, we also reviewed sources such as USGS publications where relevant for basin context, peer-reviewed SPE papers for typical fluid system usage patterns, and customs or trade statistics where additives and key materials show visible cross-border movement. Company filings, investor presentations, and credible industry press were used to sanity-check pricing commentary and product mix changes. Where needed, paid subscriptions for company financials, patent lookups, and shipment-level trade intelligence were used selectively to fill gaps. These examples are not exhaustive, and many other public sources were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys across fluid formulators, additive suppliers, distributors, and end users, so assumptions could be corrected where public indicators were too broad. Since this is a global market, views were balanced across major producing regions. Follow-up questions were used to confirm what changed in pricing, fluid mix, and offshore versus onshore demand before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 39% | EMEA: 32% |

| Smaller Players: 21% | Managers: 46% | Americas: 25% |

Market-Sizing & Forecasting

Sizing started with a top-down build where drilling activity and completion intensity were translated into a demand pool by region, then priced using typical fluid system mixes. In practice, this meant tying the model to indicators such as active rig counts, footage drilled and well counts, the share of horizontal and unconventional wells, offshore project timing, and the split of water-based versus oil-based and synthetic systems, which then drive different consumption and pricing patterns.

Those totals were corroborated using selective bottom-up approximations, such as rolling up a sample of supplier revenues, using channel checks to validate average selling prices, and stress-testing volume assumptions against what field experts see in day-to-day operations. Where coverage gaps existed, they were filled using conservative ranges and then narrowed through interview feedback, so the final number remains reproducible with clearly explained steps.

For forecasting, scenario analysis was used, anchored on expected upstream spending and drilling activity outlooks. The model was adjusted for likely pricing movement in key additives and for changes in fluid system selection driven by regulations and well complexity. Assumptions were reviewed region by region, and the final forecast was kept consistent with the direction of the input drivers rather than forcing a smooth curve.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals, including rig activity trends, regional drilling cycles, and published upstream outlook updates, so the market path matches what operators and suppliers can explain. When a segment result looked out of line, the inputs were re-opened, and respondents were re-contacted to confirm whether the issue came from mix, price timing, or a boundary assumption.

Before sign-off, the model goes through multiple analyst reviews, and variance checks are run across regions and fluid systems to confirm that shares and implied prices remain realistic. Reports are refreshed annually, and interim updates are done when material events occur, such as sharp commodity price swings or major changes in drilling activity. Right before delivery, a fresh review pass is completed so clients receive the most current view available.

Mordor Intelligence's Global Drilling and Completion Fluids Market Market Sizing Compared With Other Published Estimates

Published market sizes for drilling and completion fluids can differ even when the market name looks the same, since the year used for pricing, currency conversion timing, and what gets counted as completion and work-over revenue are not handled uniformly.

In our work, the main spread typically comes from when average selling prices are refreshed during the year and how quickly those updates are validated against rig activity and well mix shifts. This is why currency timing and quarterly price checks matter in the final number, a discipline applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.73 B (2025) | |

| Industry Publisher A | USD 10.30 B (2025) | Uses a broader long-range outlook with a single-year pricing assumption and limited visibility on mid-year additive price resets, which can understate the realized 2025 average price in regions with fast activity changes. |

| Global Publisher B | USD 10.51 B (2025) | Leans on a base-year snapshot and may treat work-over fluids and certain completion-related additives differently by application, which shifts the counted revenue between drilling and completion buckets. |

Looking at the three values together, the difference is mostly explained by price timing and what is counted inside completion and work-over fluids, rather than a disagreement on demand direction. By keeping the activity drivers visible and re-checking implied prices against interview feedback, the resulting market size stays traceable to clear steps that can be repeated each refresh.

Key Questions Answered in the Report

How large is the drilling and completion fluids market in 2026?

The market stands at USD 11.19 billion in 2026 and is forecasted to reach USD 13.52 billion by 2031.

Which fluid base is growing fastest?

Synthetic-based systems are projected to advance at a 5.8% CAGR through 2031, driven by HPHT offshore wells and tightening discharge limits.

Why are completion fluids priced higher than drilling fluids?

Completion fluids must be solids-free and formation-compatible to protect reservoir contact, which raises additive complexity and commands 30%-40% higher barrel pricing.

What impact do digital platforms have on fluid demand?

Real-time rheology and automated dosing reduce non-productive time and additive waste, allowing suppliers to bundle higher-margin services without shrinking overall fluid value.

Which region is expected to grow fastest?

Asia-Pacific is set to post a 5.7% CAGR through 2031 as China, India, and ASEAN nations localize fluid supply and intensify offshore and unconventional drilling.

Who are the leading suppliers?

Schlumberger's M-I SWACO, Halliburton, and Baker Hughes hold a combined 55%-60% share, followed by regional specialists such as CES Energy Solutions and Newpark Resources.

Page last updated on: