Offshore Drilling Rigs Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 39.26 Billion |

| Market Size (2031) | USD 45.87 Billion |

| Growth Rate (2026 - 2031) | 3.16% CAGR |

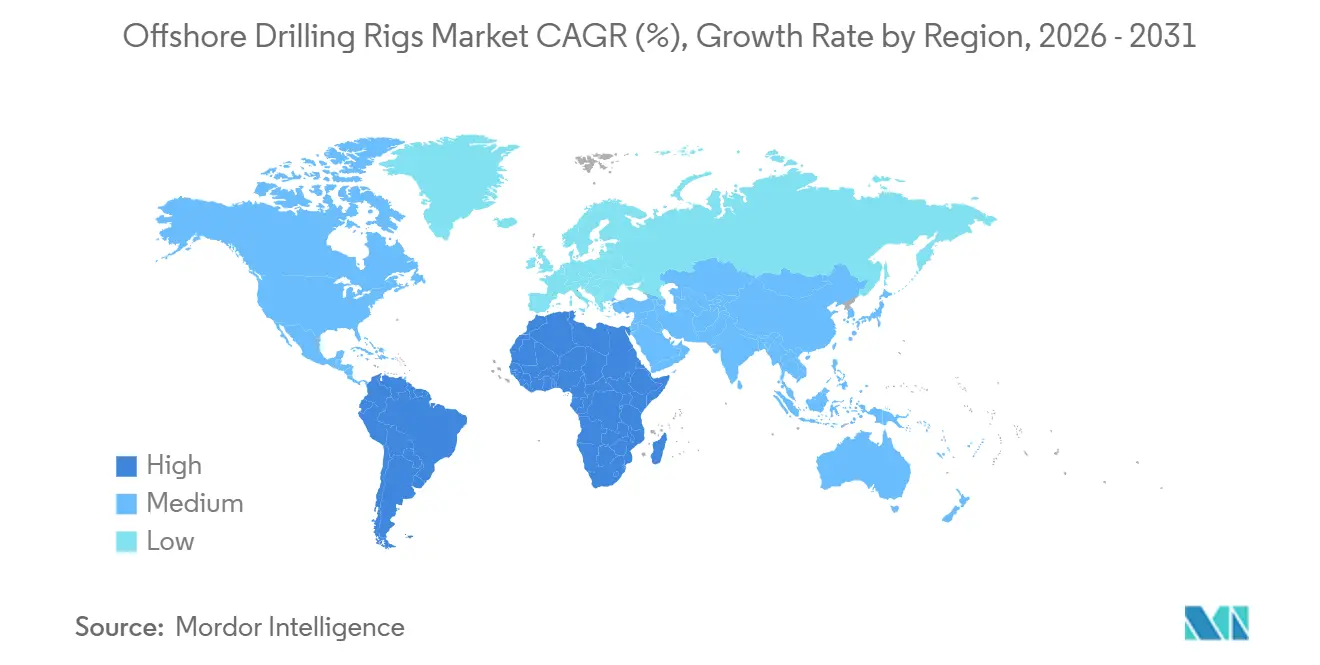

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

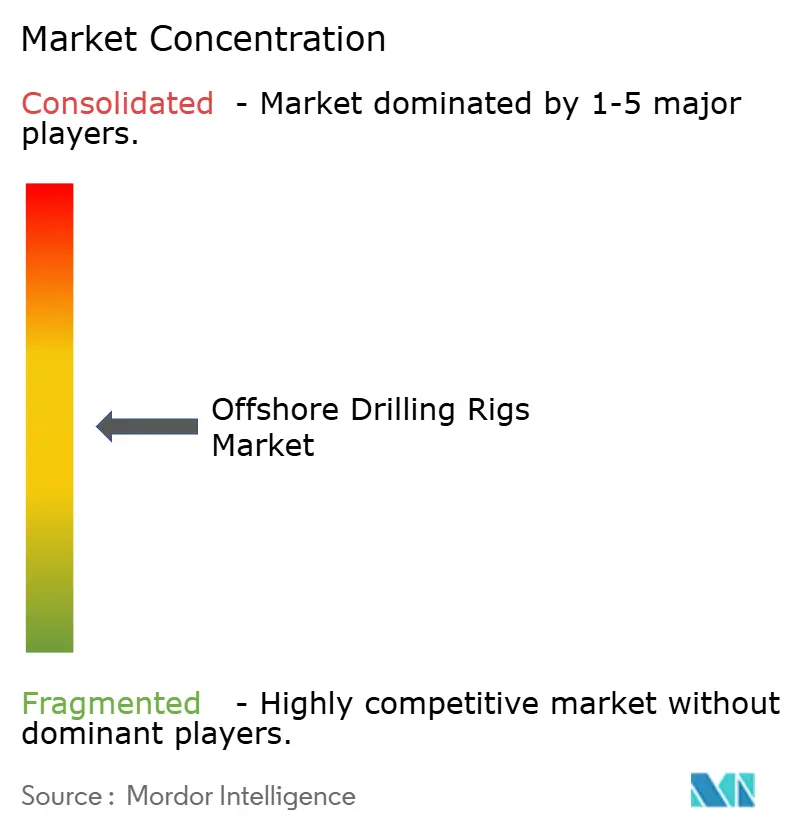

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore Drilling Rigs Market Analysis by Mordor Intelligence

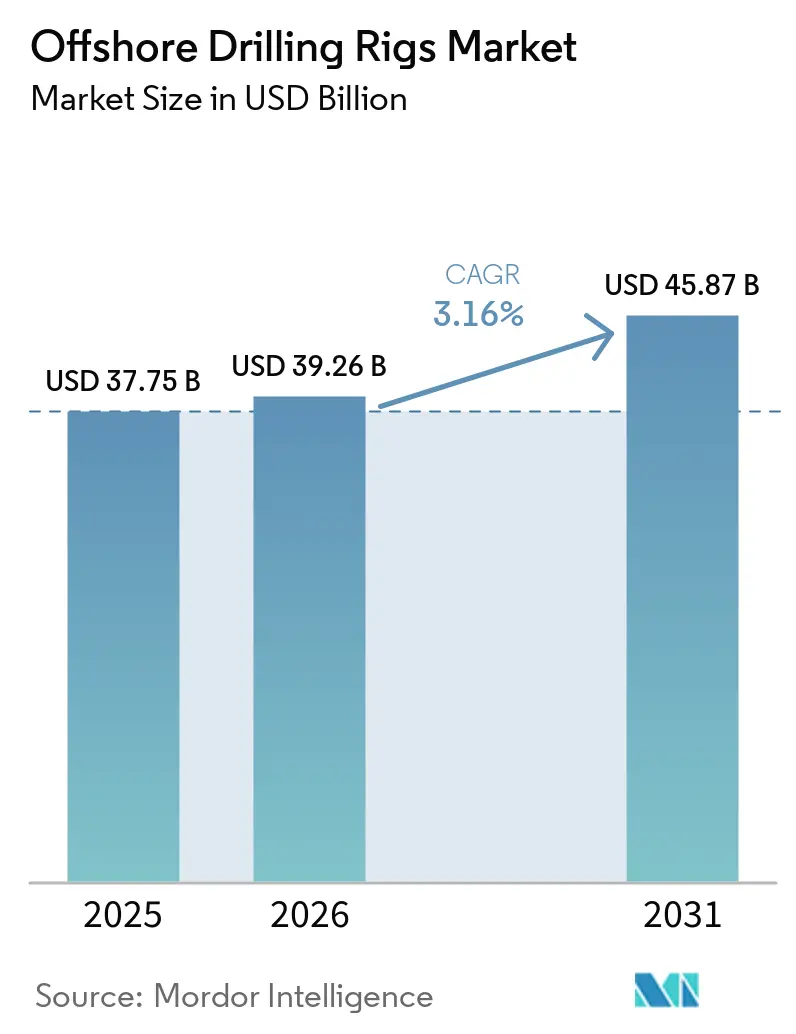

The Offshore Drilling Rigs Market size is expected to grow from USD 37.75 billion in 2025 to USD 39.26 billion in 2026 and is forecast to reach USD 45.87 billion by 2031 at 3.16% CAGR over 2026-2031.

This market size outlook underscores a disciplined capital-allocation cycle in which contractors favor backlog visibility and higher utilization rather than speculative newbuild programs. Higher-specification rigs, especially seventh-generation drillships, continue to command premium day rates because they enable operators to reach ultra-deep targets that hold multi-billion-barrel reserves. Day-rate recovery is strongest in ultra-deepwater, yet shallow-water jack-ups remain the workhorse of mature basins where low break-evens preserve drilling activity even under price volatility. Regional demand pivots around Asia-Pacific, where national oil companies deploy jack-ups to secure domestic supply, and South America and Africa, where ultra-deepwater discoveries reshape production portfolios. Technology adoption, ranging from automated drilling control to hybrid power systems, is emerging as a critical lever for cost optimization and emissions compliance.

Key Report Takeaways

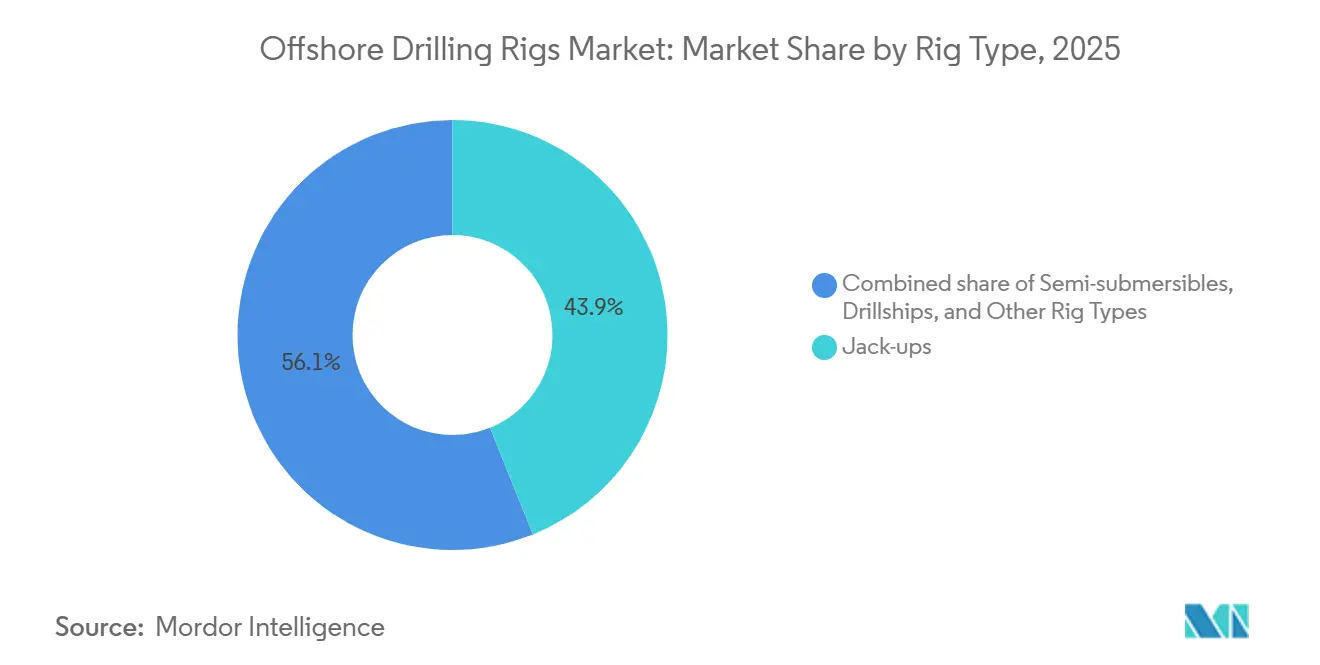

- By rig type, jack-ups led with 43.9% of offshore drilling rigs market share in 2025, while drillships posted the fastest 7.2% CAGR through 2031.

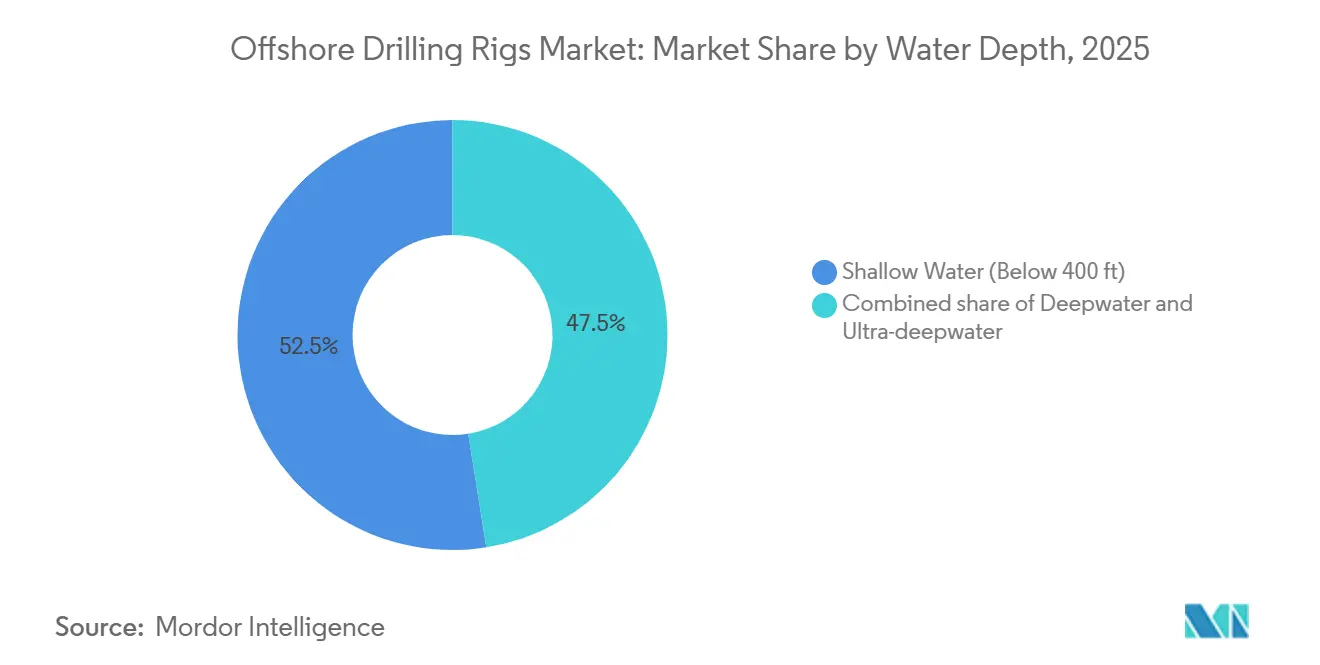

- By water depth, shallow-water projects accounted for 52.5% of the offshore drilling rigs market size in 2025, yet ultra-deepwater campaigns are set to expand at a 9.8% CAGR between 2026-2031.

- By geography, Asia-Pacific captured 37.6% revenue in 2025 and is outpacing peers with a 4.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Offshore Drilling Rigs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global energy demand | +0.8% | Global, with pronounced effect in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Exploration of untapped offshore reserves | +0.6% | South America (Brazil, Guyana), Africa (Namibia, Angola), Asia-Pacific | Long term (≥ 4 years) |

| Rising deep- & ultra-deepwater discoveries in South America & Africa | +0.9% | South America (Brazil, Guyana), Africa (Namibia, Angola, Mozambique) | Long term (≥ 4 years) |

| Decommissioning backlog driving rig-repurposing demand | +0.3% | North America (Gulf of Mexico), Europe (North Sea), with spillover to Asia-Pacific | Medium term (2-4 years) |

| Emergence of offshore carbon-storage & geothermal drilling | +0.4% | Europe (Norway, UK, Netherlands), North America, with early adoption in Australia | Long term (≥ 4 years) |

| Accessibility of stranded gas via FLNG developments | +0.5% | Asia-Pacific (Australia, Malaysia, Indonesia), Africa (Mozambique, Mauritania/Senegal) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Energy Demand

Oil and gas are expected to retain a combined 52% share of the global energy mix through 2030, creating a durable baseload for offshore drilling campaigns.[1] International Energy Agency, “World Energy Outlook 2025,” iea.org ADNOC Drilling plans to grow its fleet to 125 rigs by 2028 to help the UAE hit 5 million bpd production capacity, illustrating how national oil companies backstop demand.[2]ADNOC Drilling, “Fleet Expansion Announcement,” adnocdrillingir.ae India’s ONGC is extending jack-up charters in the Krishna-Godavari basin to preserve output from aging wells, reinforcing the shallow-water importance in energy-hungry emerging economies. Petrobras secured 12 drillships for pre-salt operations, signaling that state-backed operators can sustain drilling through price cycles.[3]Petrobras, “Pre-Salt Drilling Program Update,” investidorpetrobras.com.br This bifurcation, OECD efficiency versus non-OECD expansion, results in a two-tier demand pattern where jack-ups cater to incremental volumes in Asia while premium floaters chase frontier deepwater barrels.

Exploration of Untapped Offshore Reserves

Namibia’s Orange Basin holds an estimated 10 billion barrels of recoverable resources, with TotalEnergies and Shell collectively deploying four drillships during 2024-2025. Guyana’s Stabroek block surpassed 11 billion barrels discovered, requiring a continuous fleet of six drillships to sustain its ramp-up past 640,000 bpd. These successes are lowering perceived risk and supporting well costs above USD 100 million when success probabilities rise. Angola’s USD 6 billion Kaminho project will use two drillships over four years, highlighting the willingness to fund frontier deepwater when breakevens sit near USD 35 per barrel. Modern drillships capable of 10,000-foot water depths and 20,000-psi HPHT ratings thus form the growth engine of the offshore drilling rigs market.

Rising Deep- & Ultra-Deepwater Discoveries in South America & Africa

Brazil’s Atapu and Sépia fields reached a combined 500,000 bpd in 2025, underpinned by eight active drillships in up to 7,000-foot waters. Mozambique’s Coral Sul FLNG now exports gas from a 450 billion-cubic-meter resource, with more floating LNG trains planned. Namibia’s momentum signals that South America and Africa will collectively account for 40% of ultra-deepwater rig demand by 2026. The commercial viability of these plays has lowered pre-salt breakevens to USD 35 per barrel, rivaling onshore Middle East assets and making ultra-deepwater a mainstream portfolio component. Drillship utilization has therefore climbed above 90%, underpinning day rates near USD 500,000 for leading-edge units.

Decommissioning Backlog Driving Rig-Repurposing Demand

The North Sea faces a GBP 20 billion (USD 25 billion) decommissioning liability, opening multi-year contracts for jack-ups and heavy-lift vessels. The Gulf of Mexico holds 3,800 idle wells, prompting new bonding rules that accelerate plug-and-abandon work. Semi-submersibles are being retrofitted for CCS injection, exemplified by Equinor’s Northern Lights project that sequesters 1.5 million t of CO₂ annually. The retrofit niche extends asset life while addressing emissions mandates, allowing contractors to diversify revenue streams beyond hydrocarbon extraction. As regulators tighten removal deadlines, a steady pipeline of end-of-life wells supports baseline demand for adaptable rigs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns & stricter ESG regulation | -0.5% | Global, with stringent enforcement in Europe and North America | Short term (≤ 2 years) |

| Crude-oil price volatility impacting CAPEX cycles | -0.7% | Global, with acute sensitivity in North America and Europe | Short term (≤ 2 years) |

| Subsea tiebacks reducing demand for new exploration wells | -0.4% | North America (Gulf of Mexico), South America (Brazil), Europe (North Sea) | Medium term (2-4 years) |

| Supply-chain bottlenecks for ultra-deepwater equipment | -0.3% | Global, with pronounced impact in South America, Africa, and Asia-Pacific ultra-deepwater projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns & Stricter ESG Regulation

From 2025, the EU’s Emissions Trading System extends to offshore vessels, adding up to USD 10 million per year in carbon costs for rigs lacking abatement technology. The U.S. EPA also tightened drilling-fluid discharge norms, increasing equipment spend by 15-20%. These mandates prompted Transocean to cold-stack three legacy semi-subs that were uneconomical to upgrade. Contractors with hybrid power packs and real-time emissions monitoring now enjoy bidding advantages as operators integrate ESG metrics into sourcing. Norway’s Petroleum Safety Authority has introduced continuous methane monitoring requirements, adding further compliance layers for North Sea rigs.

Crude-Oil Price Volatility Impacting CAPEX Cycles

Brent oscillated between USD 70-90 per barrel during 2024-2025, leading majors to defer 15 offshore FIDs worth USD 40 billion. Independent E&Ps cut offshore drilling spend by 12% in 2025, instead favoring short-cycle shale. Saudi Aramco released eight jack-ups in 2024 amid revised production targets, demonstrating even state players’ responsiveness to OPEC+ quotas. Although national oil companies continue multiyear programs, the investment stop-start among independents injects scheduling uncertainty for contractors and complicates fleet-planning decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rig Type: Drillships Lead Growth Despite Jack-Up Dominance

Jack-ups controlled 43.9% of the offshore drilling rigs market share in 2025, supported by high utilization in the Persian Gulf, Southeast Asia, and the Gulf of Mexico. In contrast, drillships are forecast to post a 7.2% CAGR through 2031, pushing the offshore drilling rigs market size for this segment to an expected USD 18 billion by the end-year window. Premium units fetch USD 500,000 per day when equipped for 20,000-psi HPHT wells, such as Transocean’s Deepwater Atlas, which began a three-year Equinor contract in 2025.[4]Equinor, “Deepwater Atlas Contract,” equinor.com Semi-submersibles filled mid-water campaigns with 78% utilization in 2025, largely for appraisal work in West Africa and the Far North Sea. The continuing retirement of vintage rigs concentrates demand on high-specification assets, promoting stronger pricing power for contractors that modernize their fleets.

The offshore drilling rigs market trajectory underscores a pivot toward fleet standardization and digital enablement. Samsung Heavy Industries delivered two newbuild drillships in 2024-2025 that immediately entered Petrobras’ pre-salt pool, evidencing thin slack in the premium floater segment. Conversely, jack-up oversupply in Southeast Asia pressured Borr Drilling to redeploy four units to the Middle East in 2025, chasing rates 25% higher than in Thailand. Global jack-up utilization was 82% in late 2025 versus 91% for floaters, confirming that shallow-water capacity is absorbing the demand upswing more slowly than deepwater.

By Water Depth: Ultra-Deepwater Outpaces Shallow

Shallow-water programs contributed 52.5% of 2025 revenue, yet the ultra-deepwater segment is set to outgrow it at a 9.8% CAGR. That trajectory would lift ultra-deepwater’s offshore drilling rigs market size past USD 20 billion by 2031. Anchor, Chevron’s 20,000-psi Gulf of Mexico development, became the first HPHT field in 5,000-foot water, showcasing technical advances that unlock extreme regimes. Deepwater projects between 400 and 5,000 feet are transitioning toward subsea tiebacks to existing hubs, reducing new-well counts but extending rig campaigns via workovers. Shell’s Whale field connected fifteen wells to a legacy platform through a 27-mile flowline, cutting capital intensity by 30%.

Ultra-deepwater’s rapid growth is anchored in reserve quality. Petrobras’ Bacalhau field, which hit first oil in 2024 and is forecast to plateau at 220,000 bpd, equals 10% of Brazil’s offshore output. Namibia’s Venus appraisal results could yield a multi-train FPSO development that sustains four drillships through 2030. Across these plays, well productivity offsets higher rig-day economics, resulting in a durable demand channel that compensates for the more mature shallow-water landscape.

Geography Analysis

Asia-Pacific retained 37.6% revenue in 2025 thanks to Thailand, Vietnam, and India, and remains the fastest-growing region at 4.1% CAGR through 2031. PTTEP awarded three jack-up contracts in 2025 to extend life in the Gulf of Thailand, while PetroVietnam kept five rigs active on Bach Ho and Cuu Long, compensating for territorial constraints that slow frontier exploration. India’s ONGC extended multiple jack-ups to guard against import dependence, backing the government’s 1 million bpd domestic output goal by 2030. China’s CNOOC deployed six floaters to South China Sea gas fields to feed the Greater Bay Area’s industrial demand, while Woodside advances the Scarborough gas tieback that could enter final investment decision in 2026.

North America showed divergent trends. The U.S. Gulf of Mexico focused on subsea tieback projects, flattening rig demand, whereas Mexico’s Pemex secured three jack-up contracts in 2024-2025 to stabilize 1.8 million bpd output. South America remained dominated by Brazil and Guyana. Petrobras operated twelve drillships to hold production above 3 million bpd, while Guyana’s Stabroek block kept six floaters busy across development and exploration wells. Trinidad’s shallow-water gas wells support Atlantic LNG throughput, sustaining moderate jack-up utilization.

Europe’s activity centered on Norway, where Equinor deployed digital twins on Johan Sverdrup to shave 15% off non-productive time. The UK Continental Shelf prioritized decommissioning, letting four jack-ups work well-abandonment campaigns. The Middle East maintained high shallow-water intensity: ADNOC Drilling’s 125-rig program underpins a 5 million bpd target, Qatar’s North Field East gas expansion required six jack-ups in 2025, and Saudi Aramco’s rig count fluctuated with OPEC+ output ceilings. Africa’s ultra-deepwater frontier surged, led by Namibia and Angola. TotalEnergies’ Kaminho development and Nigeria’s Bonga Southwest appraisal reinforced the continent’s longer-term rig demand profile.

Competitive Landscape

The five largest contractors, Transocean, Valaris, Seadrill, Noble, and ADNOC Drilling, controlled 55% of premium-rig capacity in 2025, illustrating moderate consolidation. Competitive strategy diverges by asset class. International contractors lock in three- to five-year charters on seventh-generation floaters, assuring backlog to justify reactivations or selective newbuild orders. Regional players such as Shelf Drilling and COSL pursue one- to two-year jack-up deals to sustain utilization, accepting lower pricing in oversupplied basins. Equinor’s Northern Lights CCS contract highlights a new niche for semi-submersibles repurposed as CO₂ injectors, a model that blends decommissioning and climate-infrastructure demand.

Technology leadership is an emerging differentiator. NOV’s NOVOS automation suite achieved 20% non-productive-time reduction across twelve rigs by 2025, helping operators meet emissions targets. Cognite’s real-time digital twin partnership with Aker BP cut Valhall well delivery by 18%, validating data-driven drilling as a cost lever. Supply-chain consolidation also matters: Seatrium, formed by the Keppel-Sembcorp merger, delivered four newbuild units in 2024-2025, increasing negotiating leverage with component suppliers and offering integrated life-cycle services.

Regulatory compliance shapes contract awards: European majors embed ISO 14001 certification and emissions metrics into tender scoring, benefiting contractors that adopt hybrid power packages, SCR systems, and closed-loop mud handling. IMCA’s updated 2024 blowout-preventer integrity standards raise entry barriers, advantaging larger contractors that can fund real-time monitoring retrofits. The competitive landscape, therefore, rewards scale, technological sophistication, and ESG readiness over pure fleet size.

Offshore Drilling Rigs Industry Leaders

Seadrill Ltd

Transocean Ltd

Valaris Ltd

Noble Corporation plc

Shelf Drilling Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ventura Offshore secured a contract extension from Petrobras for the drillship Carolina. This extension added approximately USD 29 million to Ventura’s backlog.

- April 2026: ExxonMobil, together with Energean and Helleniq Energy, signed a drilling contract with Stena Drilling for offshore gas exploration in the Ionian Sea off Greece. The campaign is expected to begin in 2027 using a high-spec offshore drilling vessel.

- February 2026: Transocean announced a USD 5.8 billion all-stock acquisition of Valaris in February 2026. The combined company will operate a fleet of 73 offshore rigs, including ultra-deepwater drillships, semisubmersibles, and jackups, strengthening its global offshore drilling position.

- January 2026: Borr Drilling secured its first jackup rig contracts of 2026, including new drilling campaigns in the Gulf of Mexico and U.S. offshore markets. The contracts extend utilization for rigs such as Odin and provide optional work into 2027.

Global Offshore Drilling Rigs Market Report Scope

Offshore drilling rigs, or offshore platforms or drilling units, are structures used for drilling and extracting oil and gas reserves from beneath the seabed in offshore locations. These rigs are specifically designed to operate in various water depths, ranging from shallow to ultra-deepwater.

The market is segmented into rig type, water depths, and geography segments in the Offshore Drilling Rigs Market. By rig types, the market is segmented into jack-ups, semisubmersibles, drill ships, and other types. The market is segmented by water depth into shallow water, deepwater, and ultra-deepwater. The report also covers the market size and forecasts for the offshore drilling rigs market across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Jack-ups |

| Semi-submersibles |

| Drillships |

| Other Rig Types (Tender, Barges, Modu conversions) |

| Shallow Water (Below 400 ft) |

| Deepwater (400 to 5,000 ft) |

| Ultra-deepwater (Above 5,000 ft) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Trinidad and Tobago | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| Angola | |

| Namibia | |

| Rest of Middle East and Africa |

| By Rig Type | Jack-ups | |

| Semi-submersibles | ||

| Drillships | ||

| Other Rig Types (Tender, Barges, Modu conversions) | ||

| By Water Depth | Shallow Water (Below 400 ft) | |

| Deepwater (400 to 5,000 ft) | ||

| Ultra-deepwater (Above 5,000 ft) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Trinidad and Tobago | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| Angola | ||

| Namibia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global spending on offshore drilling rigs be by 2031?

The offshore drilling rigs market is forecast to reach USD 45.87 billion by 2031 due to disciplined fleet utilization and ultra-deepwater project sanctions.

Which rig type is posting the fastest growth?

Drillships lead growth at a 7.2% CAGR because frontier discoveries in Brazil, Guyana, and Namibia require seventh-generation floaters.

Why is ultra-deepwater activity accelerating?

Massive pre-salt and frontier finds offer low-breakeven, high-volume reserves that justify premium day rates and support 9.8% CAGR for ultra-deepwater campaigns.

How are ESG rules affecting offshore drilling costs?

EU carbon pricing and stricter U.S. discharge limits are adding up to USD 10 million per year for non-compliant rigs, incentivizing hybrid power and closed-loop systems.

Which region accounts for the largest market share today?

Asia-Pacific commands 37.6% share, driven by energy-security programs in Thailand, Vietnam, India, and China that sustain jack-up utilization.

Page last updated on: