Occupant Classification Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

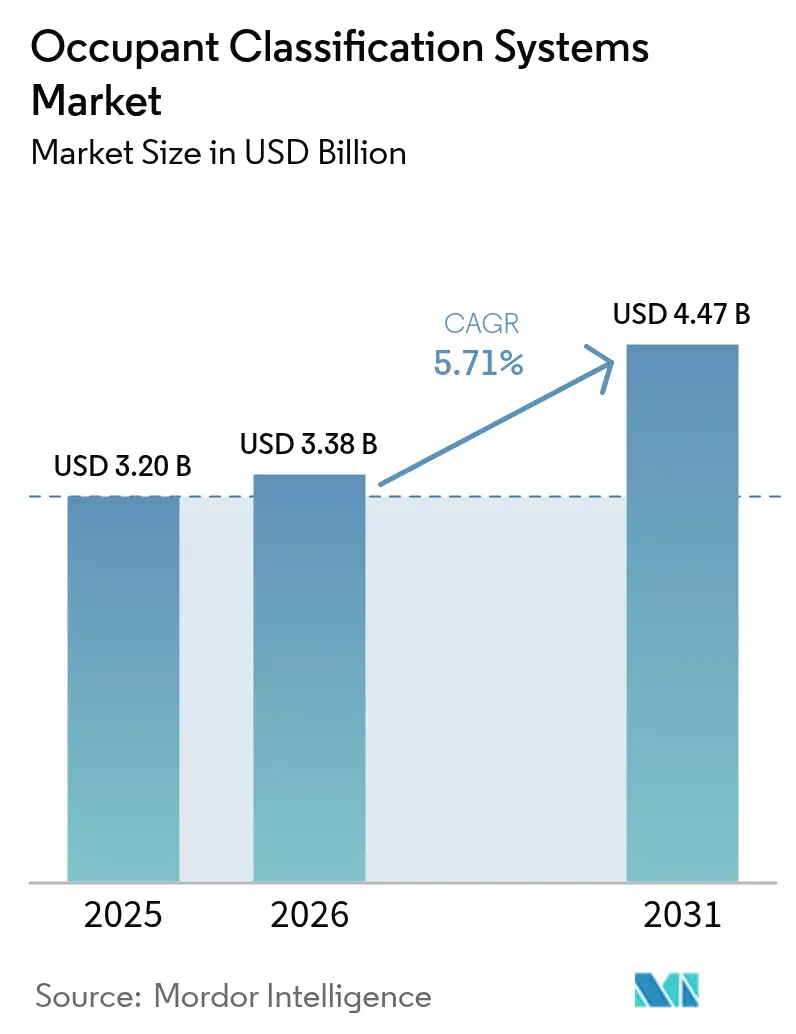

| Market Size (2026) | USD 3.38 Billion |

| Market Size (2031) | USD 4.47 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

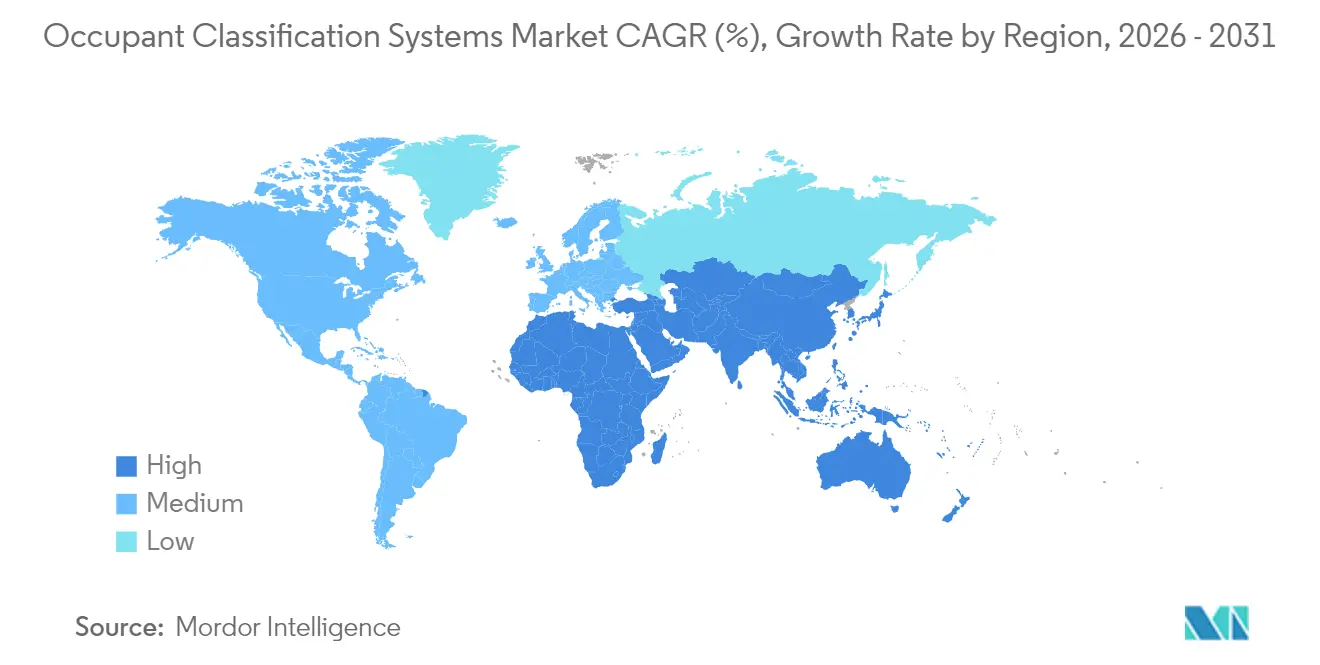

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Occupant Classification Systems Market Analysis by Mordor Intelligence

The occupant classification systems market size was valued at USD 3.2 billion in 2025 and estimated to grow from USD 3.38 billion in 2026 to reach USD 4.47 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031). Demand is accelerating as Euro NCAP’s 2026 protocol and China’s GB 15083-2024 rule tighten requirements for real-time occupant detection, prompting automakers to embed more sophisticated sensing arrays. Suppliers are also benefiting from the migration to software-defined vehicles that support over-the-air safety updates, reducing recall costs while extending system life cycles. Asia-Pacific holds a clear lead because its radar module supply chain enables low-cost integration, while South America records the fastest growth as regional regulators mirror global safety norms. Competitive intensity is rising as Tier 1 suppliers add mmWave radar and AI-enabled domain controllers to established air-bag expertise, aiming to secure long-term platform awards with global OEMs.

Key Report Takeaways

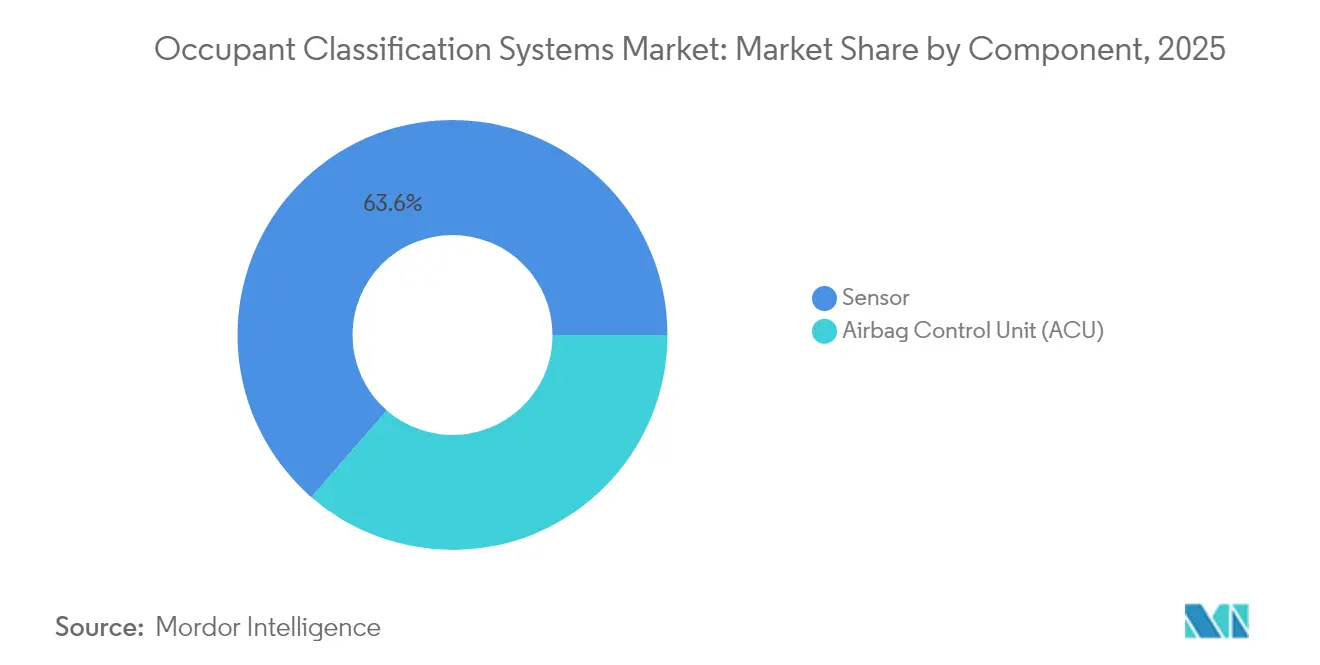

- By component, sensors led with 63.60% revenue share in 2025; airbag control units are expanding at an 8.18% CAGR through 2031.

- By sensor type, pressure sensors held 47.30% of the occupant classification systems market share in 2025, while radar sensors are projected to post a 12.21% CAGR to 2031.

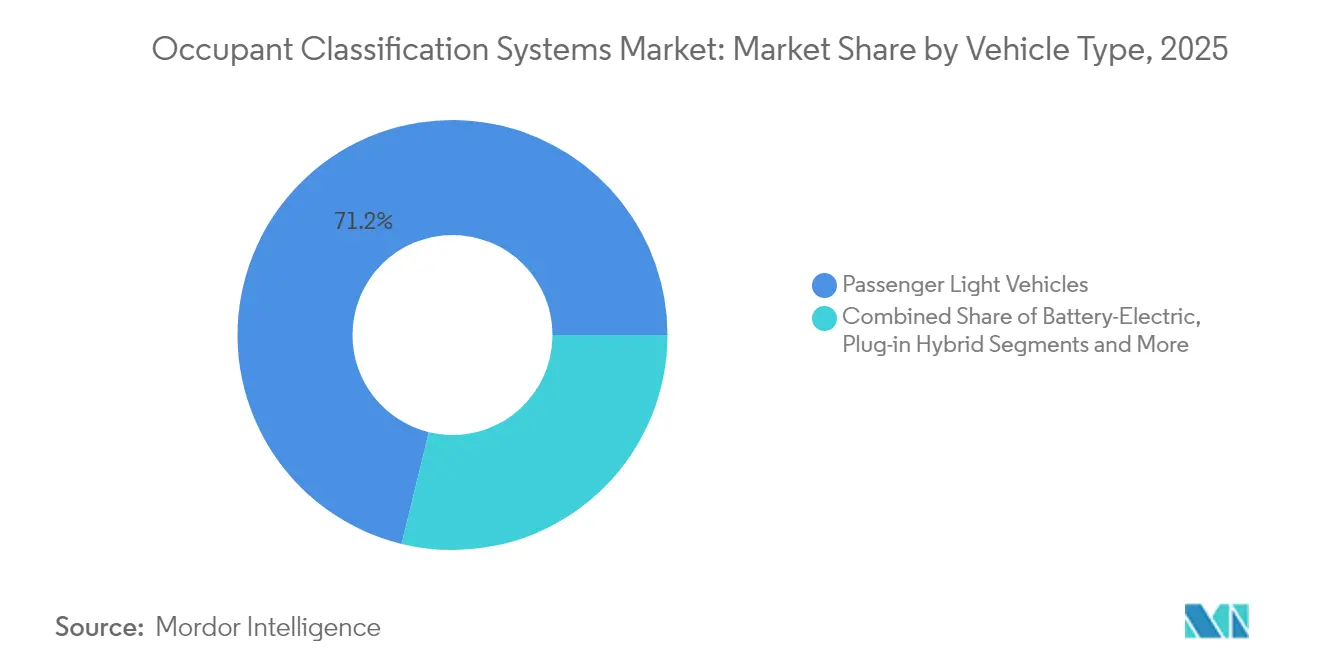

- By vehicle type, passenger light vehicles commanded 71.20% share of the occupant classification systems market size in 2025; battery-electric vehicles are progressing at a 9.94% CAGR to 2031.

- By sales channel, OEM-fitted solutions accounted for 57.30% of the occupant classification systems market in 2025, whereas aftermarket kits exhibit the fastest CAGR at 9.76% through 2031.

- By geography, Asia-Pacific dominated with a 30.60% share in 2025; South America is poised for an 8.48% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Occupant Classification Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Emergence of Low-cost mmWave Radar Modules for In-Cabin Sensing (Asia) | +1.2% | Asia-Pacific, with spillover to North America | Medium term (2-4 years) |

| NCAP 2026 Mandate on Rear-Seat Belt Reminders (US & EU) | +0.9% | North America & EU, with adoption in emerging markets | Short term (≤ 2 years) |

| Rapid Uptake of Smart Curtain-Airbag Architectures in SUVs | +0.7% | Global, with concentration in premium SUV segments | Medium term (2-4 years) |

| Battery-Electric Vehicle (BEV) Skateboard Floors Freeing Space for Embedded OCS | +0.8% | Global, led by China and Europe | Long term (≥ 4 years) |

| China's GB 15083-2024 Crash-Safety Rule Adding Dynamic Weight-Sensing | +0.6% | China, with regulatory spillover to ASEAN | Short term (≤ 2 years) |

| Automaker Shift to Software-Defined Vehicles Enabling Over-the-Air OCS Updates | +0.5% | Global, concentrated in premium segments initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Emergence of low-cost mmWave radar modules

Sixty-gigahertz and 77 GHz chips such as Infineon’s BGT60ATR24C now ship at consumer-grade price points, allowing radar to replace weight mats even in sub-USD 25,000 vehicles. These solid-state devices classify adults, children and empty seats under all lighting and temperature conditions, reducing warranty claims linked to foam hysteresis. Asian OEMs rapidly embed the technology to meet China’s new dynamic weight-sensing rule and to standardize platforms for export markets.[1]Infineon Technologies, “BGT60ATR24C XENSIV Radar MMIC Detects In-Vehicle Occupancy,” infineon.com

NCAP 2026 mandate on rear-seat belt reminders

Euro NCAP and NHTSA now require detection of occupied rear seats combined with audiovisual warnings if belts stay unfastened, compelling automakers to deploy multi-sensor arrays that distinguish toddlers, child seats and luggage. Volume deployment boosts economies of scale for radar and capacitive solutions, lowering per-vehicle system cost by up to 18% based on supplier quotations.

BEV skateboard floors freeing sensor space

Flat battery packs open cabin volume that engineers use for distributed sensor placement, enabling floor-integrated pressure cells and seat-frame radar without comfort trade-offs. Zonal 48 V wiring trims harness weight by 85%, creating headroom for additional occupant-monitoring endpoints.

Shift to software-defined vehicles enabling OTA updates

Central domain controllers now push certified algorithm updates over secure channels, eliminating dealer-based ECU reflashes and enabling quick calibration for demographic diversity. The model aligns with OEM efforts to monetize post-sale features, turning occupant classification performance into an upgradable asset rather than a fixed-point specification.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Seat-Foam Hysteresis Causing Calibration Drift in Weight Sensors | -0.8% | Global, particularly affecting cost-sensitive segments | Medium term (2-4 years) |

| High-GHz Radar Interference with 5G Modules inside EV Cabins | -0.6% | Global, concentrated in premium EV segments | Short term (≤ 2 years) |

| Tariff-Driven Cost Inflation on MEMS Pressure Cells (US-China) | -0.4% | North America, with spillover to global supply chains | Short term (≤ 2 years) |

| Consumer Privacy Concerns over Camera-based Occupancy Analytics | -0.3% | North America & EU, with emerging concerns in Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seat-foam hysteresis causing calibration drift

Hyper-elastic foams deform over time and temperature, shifting baseline weight-sensor output and prompting costly recalibration. A 2022 MDPI study confirmed drift can exceed 6 kg within two years, enough to misclassify small adults as children, forcing migration to radar or advanced packaging structures.

High-GHz radar interference with 5G modules

When multiple 76-77 GHz sensors operate inside quiet EV cabins, overlap with 71-76 GHz telecom bands can raise packet-error rates and corrupt occupancy data streams, particularly in multi-row SUVs. Mitigation requires adaptive waveform management and EMC shielding, adding between USD 4 and USD 7 in bill-of-material cost per vehicle according to Tier 1 quotations.[2]IOPscience, “Compatibility Studies of IMT System and Automotive Radar,” iop.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors anchor system value

Sensors captured 63.60% of 2025 revenue as OEMs relied on multi-modal arrays to fulfill global safety norms. Pressure, capacitive and radar elements together generate the real-time data that air-bag logics demand. Most value accrues to suppliers that can combine hardware stacks with embedded diagnostics to meet ASIL D targets. The airbag control-unit segment is rising at 8.18% CAGR because domain controllers now fuse occupant data with crash algorithms in a single box, trimming harness length and assembly time.

Continental’s ACU Premium platform consolidates restraint logic, enabling OTA calibrations that cut warranty costs by 22% over the vehicle life cycle. Veoneer’s SC3 controller ships in one-fourth of new cars worldwide, reflecting OEM confidence in integrated safety silicon. These examples illustrate how software capability is capturing margin once held solely by discrete sensors within the occupant classification systems market.

By Sensor Type: Radar outpaces legacy mats

Pressure mats retained a 47.30% share in 2025 thanks to low unit cost; yet mmWave radar now posts a 12.21% CAGR as OEMs seek calibration-free accuracy. Capacitive grids address premium interiors where touch surfaces double as HMI, and ultrasonic devices serve compact cabins but face acoustic interference. Dual-mode pressure-plus-radar kits are emerging as a mid-cost solution that leverages existing seat architecture while adding child-presence detection for NCAP scoring.

When comparing lifetime cost, suppliers estimate radar modules lower warranty provisioning by 30% through immunity to foam drift. This risk-reduction advantage underpins radar’s swift share gains within the occupant classification systems market size for new platforms entering production from 2027 onward.

By Vehicle Type: Electrification sets the pace

Passenger light vehicles represented 71.20% of shipments in 2025; still, battery-electric vehicles grow the fastest at 9.94% CAGR through 2031. Skateboard chassis enable flush-mounted floor sensors, and low-noise cabins highlight the comfort benefits of silent solid-state radar. Plug-in hybrids adopt similar architectures but remain transitional. Commercial vans and light trucks increasingly retrofit occupancy kits to satisfy fleet insurance mandates, opening incremental revenue for sensor suppliers.

Tesla’s 2024 decision to add cabin radar demonstrates how BEVs can leapfrog weight mats and set new baselines for global homologation. As electrification spreads, these design freedoms will extend across mainstream segments, reinforcing radar’s trajectory inside the occupant classification systems market.

By Sales Channel: Retrofit demand accelerates

OEM installations dominated with 57.30% share in 2025; nonetheless, aftermarket kits expand at 9.76% CAGR. Fleet operators retrofit older buses and vans to reduce liability, while consumer demand rises where new-car prices outpace income. Standardized CAN and LIN gateways simplify installation, and printed flexible pressure sensors let installers slide mats beneath existing upholstery without seat teardown, a factor that broadens reach in emerging economies.

IDTechEx projects printed-sensor revenue to approach USD 1 billion within the decade on strong retrofit take-up. As feature-on-demand models gain traction, retrofit channels will serve as test beds for software-enabled safety services across the occupant classification systems industry.

Geography Analysis

Asia-Pacific commanded 30.60% of 2025 revenue, driven by China’s dynamic weight-sensing regulation and a deep radar supply chain that compresses component costs. Domestic OEMs already represent 40% of Autoliv’s Chinese sales, evidencing local appetite for advanced restraint technologies. Japan pushes driver-condition monitoring for Level-3 autonomy, and South Korea’s EV incentives stimulate radar adoption, creating a robust regional ecosystem around the occupant classification systems market.

North America and Europe set the regulatory tone. Euro NCAP 2026 and NHTSA’s FMVSS 208 revisions harmonize rear-seat alerts and thus standardize sensor specifications. The EU General Safety Regulation II, live since July 2024, bundles occupant detection with drowsiness alarms, driving multi-sensor rollouts. Privacy-minded consumers in both regions prefer radar over camera analytics, shaping supplier roadmaps and reinforcing demand for non-visual sensing within the occupant classification systems market size.

South America marks the fastest trajectory at 8.48% CAGR, as Brazil and Argentina upgrade safety standards and court OEM investment. Argentina’s 2025 traffic law now references autonomous functions, indirectly encouraging occupant-monitoring integration. While price sensitivity limits camera use, flexible pressure sensors and simplified radar bring compliant packages into mid-range models, widening addressable volume. Middle East and Africa remain nascent, but fleet retrofits in the Gulf leverage aftermarket kits to satisfy insurance discounts, indicating gradual diffusion across the global occupant classification systems market.

Competitive Landscape

Tier 1 suppliers such as Autoliv, Continental, and ZF claim scale advantages from decades of air-bag engineering yet now pivot toward radar and AI software. Continental’s April 2025 launch of the Aumovio brand ahead of its automotive IPO packages sensor fusion, domain control and cybersecurity in a single stack, targeting the occupant classification systems market’s new software value pools. ZF is carving out its LIFETEC passive-safety arm to sharpen focus on high-growth radar occupant detection, acknowledging investor demand for pure-play safety assets.

Automakers also file patents to own core algorithms: a January 2024 U.S. application from Tesla combines weight sensors with radar presence checks to refine air-bag logic. Start-ups pitch data-centric tools; Anyverse trains occupant models on synthetic datasets to sidestep privacy hurdles, courting OEMs that fear regulatory fines. Component consolidation is visible as chip vendors bundle radar front-ends with on-chip AI accelerators, shortening development cycles for Tier 1 integrators.

Strategic moves underscore convergence. Volvo and ZF jointly unveiled adaptive belts that tighten based on real-time occupant mass, blending restraint hardware with sensor feedback. Autoliv partnered with Formula E to showcase electric-vehicle safety tech, elevating brand equity while harvesting track telemetry for algorithm refinement. These initiatives reveal how product leadership now hinges on software extensibility as much as mechanical reliability inside the occupant classification systems market.

Occupant Classification Systems Industry Leaders

ZF Group

Continental AG

Robert Bosch GmbH

Autoliv Inc.

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Volvo unveiled adaptive seatbelt technology co-patented with ZF that utilizes real-time occupant data to adjust restraint systems based on passenger body type and position, representing a significant advancement in personalized safety systems that integrate with occupant classification platforms.

- April 2025: Continental Automotive launched the Aumovio brand during Auto Shanghai 2025, focusing on sensor solutions and assistance systems for software-defined vehicles ahead of the company's planned September 2025 automotive spin-off and IPO, positioning the new entity to compete in advanced occupant monitoring markets.

- April 2025: Autoliv announced a partnership with the ABB FIA Formula E World Championship as Official Mobility Safety Partner, beginning April 2025, to enhance automotive safety awareness and develop safety technologies for electric vehicles, including occupant protection systems.

- January 2025: Anyverse introduced a reliable occupant monitoring AI system built with synthetic data, addressing the challenge of developing robust occupant classification algorithms without compromising passenger privacy through real-world data collection.

Global Occupant Classification Systems Market Report Scope

The study of the occupant classification systems (OCS) market has considered the various offerings from the vendors for sensors and airbag systems, globally. The OCS systems enable the differentiation of passenger seating on the front passenger seat to assist advanced airbag safety systems.

| Airbag Control Unit (ACU) |

| Sensors |

| Pressure Sensors |

| Seat-belt Tension Sensors |

| Strain-Gauge Mat Sensors |

| Capacitive Sensors |

| Ultrasonic Sensors |

| 60 GHz and 77 GHz Radar Sensors |

| Passenger Light Vehicles |

| Battery-Electric Vehicles |

| Plug-in Hybrid Vehicles |

| Commercial Light Trucks and Vans |

| OEM-Fitted Systems |

| Aftermarket and Retrofit Kits |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Airbag Control Unit (ACU) | |

| Sensors | ||

| By Sensor Type | Pressure Sensors | |

| Seat-belt Tension Sensors | ||

| Strain-Gauge Mat Sensors | ||

| Capacitive Sensors | ||

| Ultrasonic Sensors | ||

| 60 GHz and 77 GHz Radar Sensors | ||

| By Vehicle Type | Passenger Light Vehicles | |

| Battery-Electric Vehicles | ||

| Plug-in Hybrid Vehicles | ||

| Commercial Light Trucks and Vans | ||

| By Sales Channel | OEM-Fitted Systems | |

| Aftermarket and Retrofit Kits | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving the occupant classification systems market between 2026 and 2031?

The 5.71% CAGR is fueled by stricter safety mandates such as Euro NCAP 2026, China’s GB 15083-2024, and the shift to software-defined vehicles that allow continuous algorithm upgrades.

Which component contributes the most revenue today?

Sensors contribute 63.60% of 2025 revenue because pressure, capacitive and radar devices provide the raw data that restraint controllers require.

Why are radar sensors gaining share over pressure mats?

Radar avoids calibration drift caused by seat-foam hysteresis and meets new child-presence detection requirements, supporting a 12.21% CAGR through 2031.

Which region will grow the fastest?

South America shows the highest regional CAGR at 8.48% as Brazil and Argentina update safety regulations and attract new vehicle assembly investments.

How are suppliers differentiating in a crowded field?

Tier 1s integrate sensor fusion and OTA-ready domain controllers; for example, Continental’s Aumovio and ZF’s LIFETEC carve-out focus on AI software and vertical integration.

Can existing fleets upgrade to advanced occupant detection?

Yes. Aftermarket kits—expanding at 9.76% CAGR—use printed flexible pressure sensors and standard CAN gateways to retrofit older vehicles with compliant occupant monitoring.

Page last updated on: