Nucleotides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 7.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

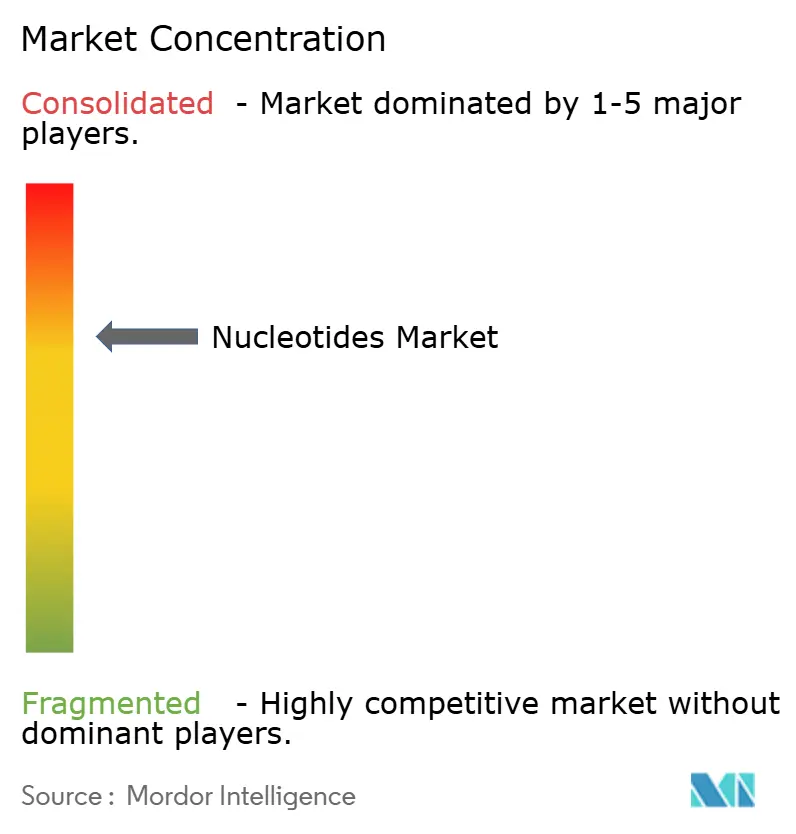

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nucleotides Market Analysis by Mordor Intelligence

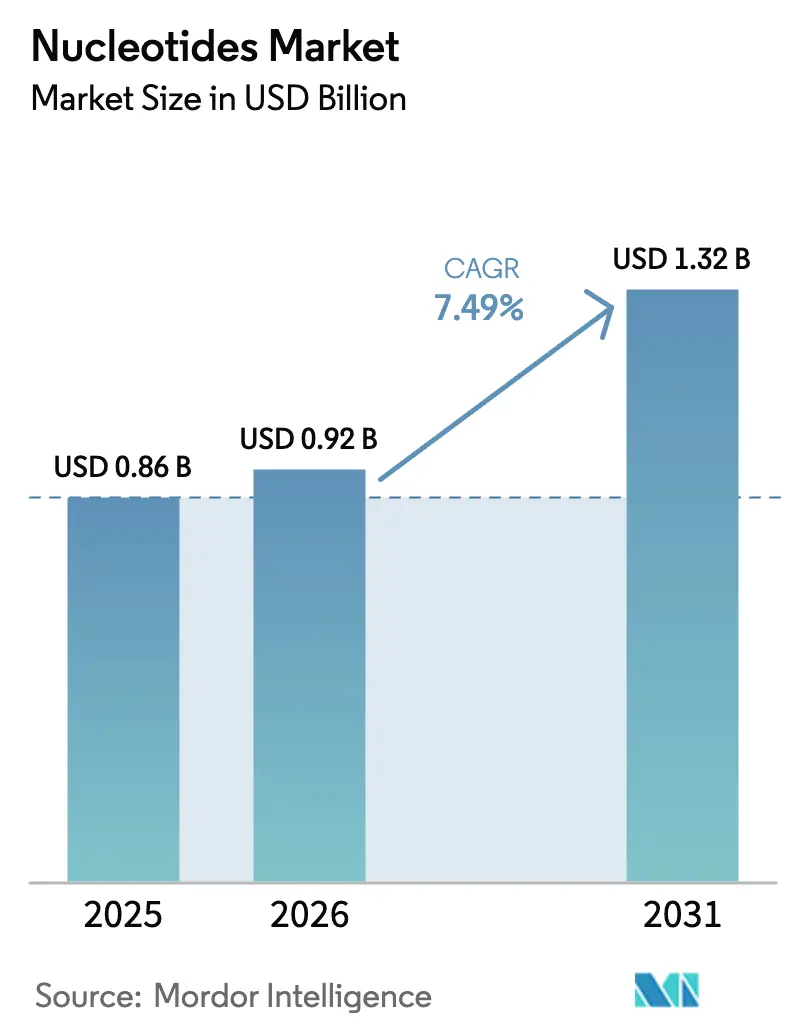

The Nucleotides Market size is expected to grow from USD 0.86 billion in 2025 to USD 0.92 billion in 2026 and is forecast to reach USD 1.32 billion by 2031 at 7.49% CAGR over 2026-2031. This sustained trajectory mirrors strong pull from gene- and cell-therapy pipelines that consume large volumes of GMP-grade building blocks, steady infant-formula fortification mandates in Asia and Europe, and rapid adoption of nucleotide-based feed additives following restrictions on prophylactic antibiotics. Pyrimidine derivatives continue to dominate supply chains because cytidine and uridine support mRNA vaccine production, while precision-fermentation upgrades tighten cost curves for both food- and pharma-grade lines. Consolidation is moderate: the top five producers control about half of installed capacity, yet dozens of specialist CDMOs compete in high-margin oligonucleotides. Commodity corn and sugar price swings, however, inject earnings volatility, and capital-intensive GMP plants constrain new entrants.

Key Report Takeaways

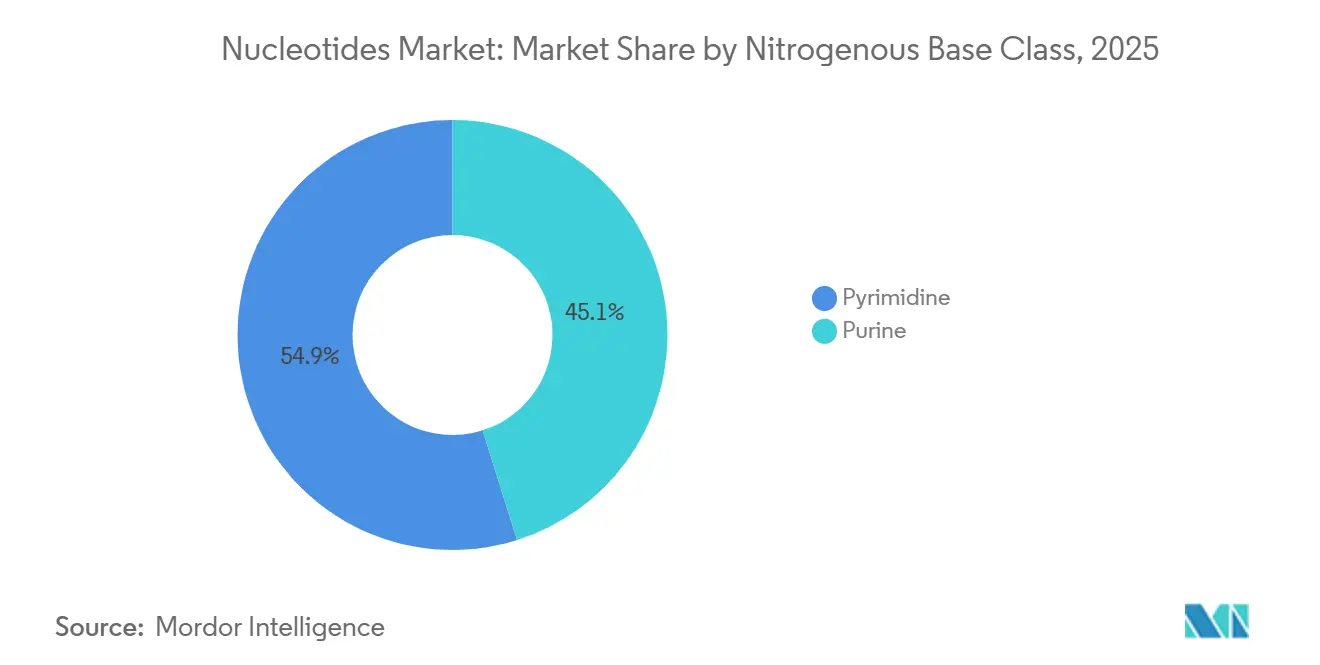

- By nitrogenous base class, pyrimidines captured 54.87% of the nucleotides market share in 2025 and are advancing at 7.96% CAGR through 2031.

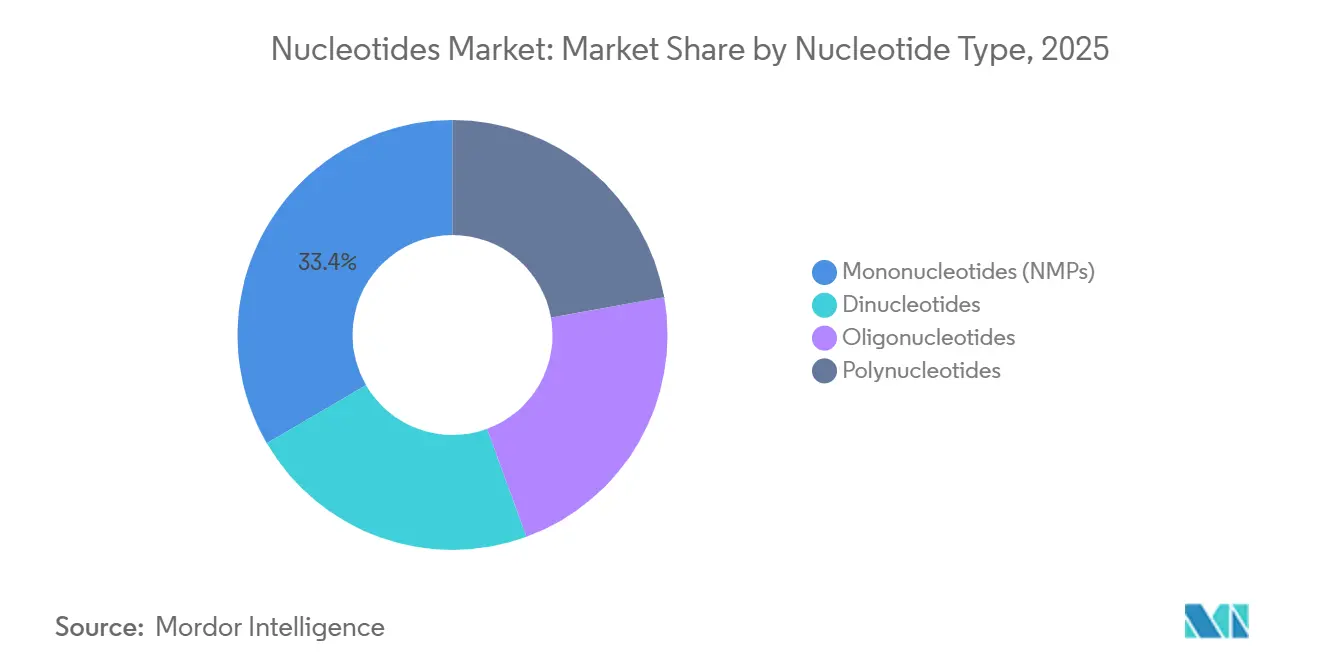

- By nucleotide type, mononucleotides retained 33.40% of the nucleotides market size in 2025, while oligonucleotides are recording an 8.22% CAGR to 2031.

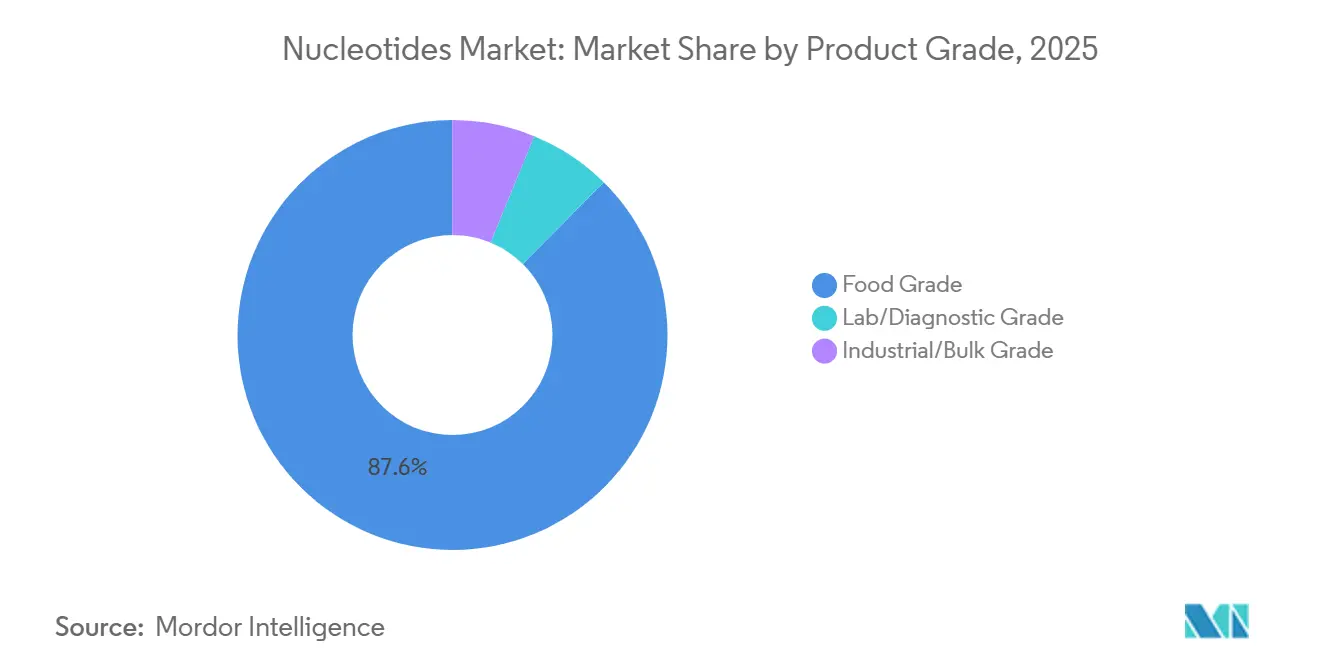

- By product grade, food-grade commanded 87.58% of revenue in 2025 and is advancing at 8.38% CAGR through 2031.

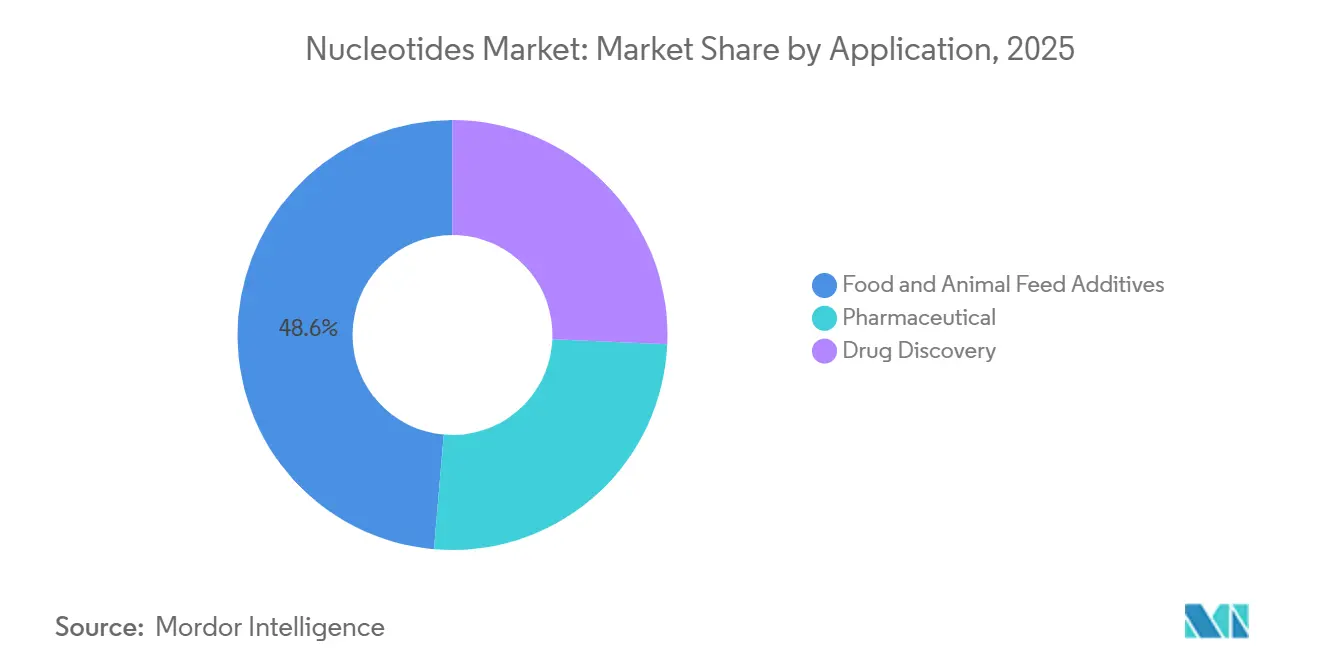

- By application, food and animal-feed additives led with 48.62% share of the nucleotides market size in 2025 and are forecast to post 7.65% CAGR through 2031.

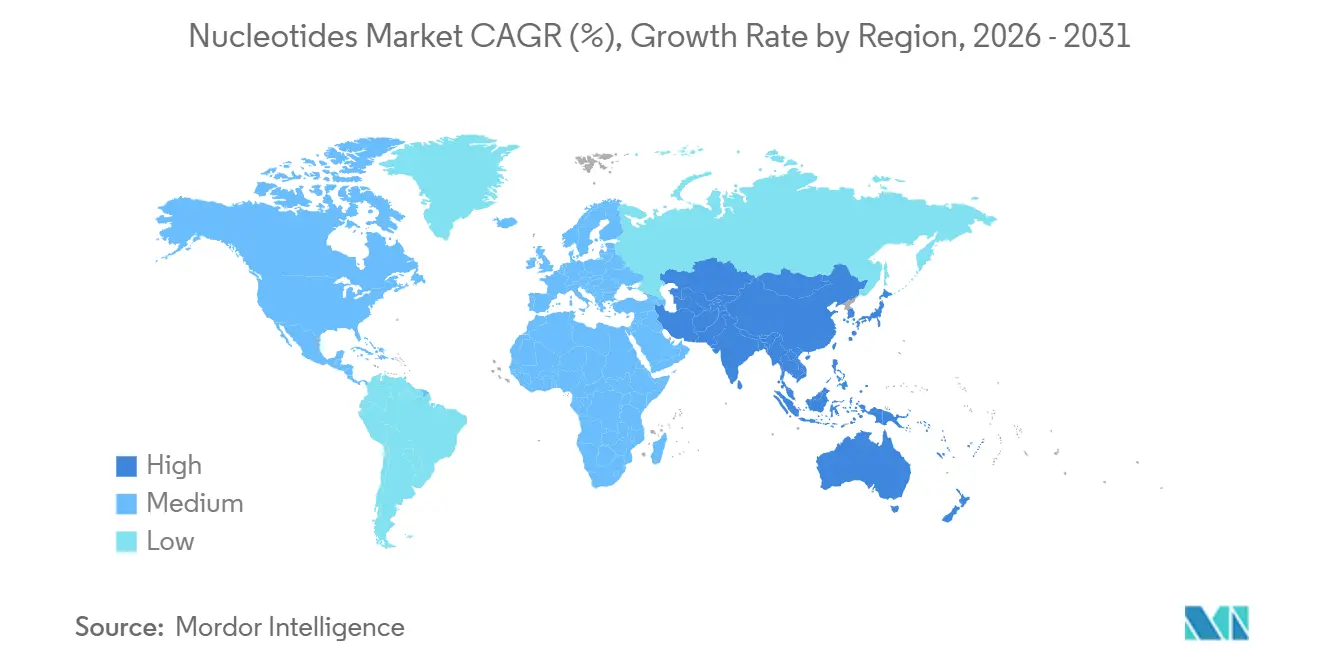

- By geography, Asia-Pacific held 44.71% share of the nucleotides market size in 2025 and is advancing at a 7.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nucleotides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from pharmaceutical and biopharma sectors | +2.1% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Rising adoption in functional infant and medical nutrition | +1.8% | Asia-Pacific core, spillover to Europe and North America | Medium term (2-4 years) |

| Inclusion in livestock and aquaculture feed to replace antibiotics | +1.3% | Europe and Asia-Pacific, emerging in Latin America | Medium term (2-4 years) |

| Rapid growth of oligonucleotide-based gene and cell-therapy pipelines | +1.6% | North America and Europe, early adoption in Japan | Long term (≥ 4 years) |

| Precision fermentation platforms lowering production cost | +1.2% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Pharmaceutical and Biopharma Sectors

Oligonucleotide therapeutics shifted from niche to mainstream after the FDA cleared Casgevy, Itvisma, RIVFLOZA, and TRYNGOLZA in 2024, prompting originators to lock in multi-year supply contracts for high-purity nucleotides. Thermo Fisher expanded a Singapore facility in 2025, injecting 500 kg of annual capacity and offering 2-week turnaround times for antisense and siRNA programs. The American Society of Gene and Cell Therapy counted 1,261 RNA-based therapies in active pipelines, a 22% rise year-over-year, underscoring pervasive demand for cytosine, adenine, guanine, and uracil monomers. Messenger-RNA vaccine plants consumed 12,000 t of nucleotides in 2024 and are switching to continuous processing, which heightens near-term raw-material tightness. Convergence of CRISPR, RNAi, and self-amplifying RNA platforms therefore cements structural pull for GMP-grade inputs that food-grade suppliers cannot match.

Rising Adoption in Functional Infant and Medical Nutrition

Regulators continue to endorse nucleotide fortification in formula. The European Food Safety Authority reaffirmed safe use up to 5 mg/100 kcal in 2024[1]European Food Safety Authority, “Scientific Opinion on Infant Formula Additives,” efsa.europa.eu . China’s National Health Commission mandated nucleotides in follow-on formula for 6- to 12-month infants in 2025, instantly lifting demand by 2,400 t per year. Clean-label brands now insist on fermentation-derived grades; lead times stretched to 20 weeks in early 2026, double 2024 norms, as capacity struggled to certify organic standards. Medical-nutrition firms add nucleotide blends at concentrations two-to-three times infant-formula norms, capturing premium pricing. As regulatory mandates intersect with consumer preference for natural inputs, procurement teams reevaluate supplier rosters in favor of dedicated clean-room fermenters.

Inclusion in Livestock and Aquaculture Feed to Replace Antibiotics

The European Union’s 2022 antibiotic ban catalyzed a shift toward immune-modulating nucleotide additives. Poultry trials adding 0.5–1 kg of nucleotide blend per metric ton of feed cut mortality 8–12% and improved feed conversion up to 5%. China approved six nucleotide feed additives for aquaculture in 2025, supporting shrimp and tilapia farms plagued by disease. Aquaculture is particularly responsive because fish have limited endogenous synthesis pathways. Brazilian integrators are running commercial pilots to secure antibiotic-free export premiums. Although the segment is price-sensitive, its volume stability cushions producers against pharmaceutical demand cycles.

Rapid Growth of Oligonucleotide-Based Gene and Cell-Therapy Pipelines

CRISPR-Cas9 approvals spotlight high per-patient nucleotide usage, with each Casgevy dose requiring roughly 250 g of modified oligos. Vertex disclosed USD 80 million of QC infrastructure spending to safeguard supply chain for the launch. Antisense launches need 5–10 kg of API per program, straining mid-tier CDMO capacity. Japan fast-tracked two oligonucleotide drugs in 2025, adding localized demand that domestic suppliers aim to capture. As the pipeline advances, achieving sub-USD 500 per gram cost for phosphorothioate oligos remains the gating hurdle to broad access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and GMP-compliance costs for new plants | -0.9% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Volatile sugar/corn-based raw material prices | -0.7% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Fermentation-capacity bottlenecks for clean-label infant-formula grade | -0.6% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and GMP-Compliance Costs for New Plants

Building a GMP nucleotide plant demands USD 50–200 million in upfront spending plus stringent validation regimes that raise operating overhead 15–20% versus food-grade lines. BioSpring’s Hamburg expansion took 18 months of inspections before revenue flow, illustrating cash-flow drag. Average utilization hovers near 70% because changeovers and batch-release testing idle equipment, below the 85% threshold needed for robust returns. As a result, smaller CDMOs favor partnerships over greenfield builds, concentrating pharmaceutical-grade supply among a dozen qualified players.

Volatile Sugar/Corn-Based Raw-Material Prices

Glucose feedstocks represent up to half of bulk mononucleotide production costs, yet U.S. corn futures swung 18% during 2025 after weather disruptions in Brazil and the Midwest[2]U.S. Department of Agriculture, “Grain Market Review 2025,” usda.gov . Chinese producers faced a 12% cost spike when drought hit Heilongjiang Province, squeezing margins on long-term fixed contracts. European suppliers hedge sugar but paid 6–8% premiums over spot, eroding competitiveness versus Asian rivals. Alternative carbon sources such as methanol remain at pilot scale and await regulatory clearance for food-grade and pharma-grade use. Until diversification matures, producers remain exposed to commodity cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nitrogenous Base Class: Pyrimidine Dominance Anchored in mRNA Platforms

Pyrimidines accounted for 54.87% of 2025 demand, reflecting the central role of cytidine and uridine in in-vitro transcription for mRNA vaccines and therapeutics. Each conventional mRNA dose uses roughly 1 g of pyrimidines, so vaccine ramp-ups from 2020–2024 locked in multi-year contracts for GMP lots. Self-amplifying RNA formats lower per-dose nucleotide requirements but pipeline growth in gene therapies offsets volume moderation. Purines make up the remaining 45.13% and are especially important in antisense oligos where phosphorothioate-modified adenosine and guanosine enhance stability. Balanced 55:45 pyrimidine-to-purine ratios in infant formula maintain a stable floor for both classes.

In pharmaceutical supply chains, pyrimidines enjoy pricing premiums because GMP lines must mitigate cytidine deamination and uridine oxidation. Thermo Fisher’s 2025 upgrade added dedicated reactors for cytidine triphosphate to address this constraint. Chinese fermentation groups are adding uridine crystallization capacity to capture higher margins, but Western buyers still prefer suppliers with robust impurity profiles validated by EMA norms. As mRNA vaccines diversify into oncology and autoimmune indications, pyrimidine momentum is unlikely to relent.

By Nucleotide Type: Oligonucleotides Lead Growth Amid Therapeutic Momentum

Oligonucleotides are set to expand at 8.22% CAGR through 2031 as 87 late-stage drug candidates advance toward approval. Mononucleotides held 33.40% of the nucleotides market size in 2025, buoyed by infant-formula mandates and growing livestock applications. Dinucleotides remain a flavor-modulating niche tied to savory snacks, while polynucleotides benefit from record NIH RNA-biology funding of USD 3.2 billion for fiscal 2025.

Custom oligo houses such as BioSpring can deliver modified strands in 2 weeks, outpacing legacy four-to-six-week cycles and commanding 25% price premiums. CDMO shortages continue, evidenced by 12-month reservation queues at several U.S. providers, nudging biotech firms to dual-source supply. Process-scale phosphoramidite synthesis still dominates, but enzymatic alternatives could reduce solvent waste, a shift investors track closely.

By Product Grade: Food Grade Dominates but Pharmaceutical Margins Reshape Strategies

Food-grade material contributed 87.58% of revenue in 2025, anchored by long-standing infant-formula inclusion guidelines and antibiotic-free livestock feed. Diagnostic-grade dNTPs and modified nucleotides serve PCR and sequencing kits, markets sustained by 2.5 billion global PCR tests in 2025. Industrial grade intermediates stagnate as users seek higher consistency. Lab/diagnostic grade lots, though small in volume, capture 40-50% gross margins, motivating Asian bulk suppliers to invest in GMP suites. EMA guidance in 2024 mandating full impurity profiling further narrowed the field to 10–12 compliant vendors.

By Application: Feed Additives Lead Share While Pharma Drives Margin

Food and animal additives represented 48.62% of 2025 demand, underpinned by EU antibiotic restrictions and China’s formula mandate. The pharmaceutical segment, despite a lower share, will grow fastest on the back of four FDA approvals and a robust late-stage pipeline; each commercial antisense launch needs up to 10 kg of API. Discovery-phase CRISPR libraries and high-throughput screens form a high-margin niche where customers accept USD 50–200 per gram prices. Ajinomoto signaled it would reallocate 60% of capex to pharma-grade capacity over the next three years to capture this margin arbitrage. Volume will remain anchored in feed and food, but profit pools are migrating toward therapeutic uses.

Geography Analysis

Asia-Pacific owned 44.71% of global demand in 2025 and is projected to expand at 7.91% CAGR to 2031. China alone houses the majority of worldwide fermentation capacity, propelled by oligo therapy trials aligned with the country’s precision-medicine roadmap. South Korea’s CJ CheilJedang leverages continuous fermenters to serve both formula and biotech buyers. India focuses on diagnostic reagents yet domestic infant-formula demand is climbing as urban breastfeeding rates fall.

North America is led by the largest oligonucleotide drug pipeline and premium organic-formula segments. Thermo Fisher’s Singapore plant was built to shorten lead times for U.S. clients and safeguard supply chains against trans-Atlantic disruptions. Canada’s formula regulations specify nucleotide levels 20% above Codex minima, resulting in high per-capita consumption. Mexico’s poultry sector is piloting nucleotide feed blends to secure antibiotic-free certifications for exports.

Europe’s demand is characterized by strict clean-label rules that elongate lead times. EMA traceability guidance favors regional suppliers able to document every step, benefitting BioSpring and French CDMOs. Germany, France, and the U.K. host 38 companies developing oligonucleotide drugs, concentrating GMP raw-material usage. The organic-formula boom lifted nucleotide shortages, driving spot premiums. South America and Middle-East and Africa represent lower demand, yet Brazil’s USD 3 billion annual shrimp disease losses spur nucleotide adoption, and Saudi Arabia’s Vision 2030 includes pharma-input localization that could open new capacity bids.

Competitive Landscape

The nucleotides market remains moderately consolidated. Chinese firms dominate food-grade output due to scale and integrated amino-acid operations that cut unit costs 20-30% below Western peers. Western companies specialize in pharma grades; their GMP certifications, validated analytical suites, and regulatory track record create customer stickiness. Strategic moves focus on vertical integration: Asian suppliers are installing downstream oligo lines, and Western CDMOs are securing upstream monomers via offtake agreements to hedge feedstock risks.

Technology leadership is shifting. Thermo Fisher’s automated synthesis reduced per-gram costs by 25% and trimmed lead times to two weeks, allowing it to capture urgent research orders. Patent filings for modified nucleotides hit 47 in 2025, signaling intensified competition for IP around phosphorothioate and 2'-O-methyl chemistries. Regulatory hurdles remain a moat: EMA’s 2024 impurity-profiling rule shrank the compliant supplier pool to a dozen. Precision-fermentation startups are experimenting with CO₂-derived feedstocks; commercial scale remains several years out, but incumbents monitor these pilots closely.

Nucleotides Industry Leaders

Ajinomoto Co., Inc.

CJ CheilJedang Corp.

Meihua Holdings Group Co., Ltd.

DAESANG

STAR LAKE BIOSCIENCE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ionis Pharmaceuticals, Inc. partner GSK announced positive results from two pivotal Phase 3 studies, B-Well 1 and B-Well 2. These studies evaluated the safety and efficacy of bepirovirsen, an investigational antisense oligonucleotide (ASO) for the treatment of chronic hepatitis B (CHB).

- January 2026: Codexis, Inc. expanded the ECO Synthesis manufacturing platform through evaluation agreement with Axolabs for oligonucleotide therapeutics. The collaboration between Codexis and Axolabs highlighted their shared commitment to advancing high-quality oligonucleotide-based medicines and broadening global access to these therapeutics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global nucleotides market as the value generated from the manufacture and bulk sale of purified mono-, di-, and oligo-nucleotides, whether chemically synthesized or fermentation-derived, that are subsequently supplied to pharmaceutical, nutrition, diagnostics, and livestock-feed formulators. According to Mordor Intelligence, the frame spans food-, lab-, and industrial-grade material traded in solid or liquid form across all major regions.

Scope exclusion: finished medicines, infant formulas, or feed premixes that merely contain nucleotides are outside the monetary base.

Segmentation Overview

- By Nitrogenous Base Class

- Pyrimidine

- Purine

- By Nucleotide Type

- Mononucleotides (NMPs)

- Dinucleotides

- Oligonucleotides

- Polynucleotides

- By Product Grade

- Food Grade

- Lab/Diagnostic Grade

- Industrial/Bulk Grade

- By Application

- Food and Animal Feed Additives

- Pharmaceutical

- Drug Discovery

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with fermentation plant managers, infant-formula R&D scientists, nutraceutical procurement heads, and feed-premix distributors across Asia-Pacific, North America, Europe, and Latin America. These discussions verified utilization rates, average selling prices, and emerging therapeutic use cases, filling data gaps left by desk work and aligning model assumptions with on-ground realities.

Desk Research

We began with trade statistics tagged under HS 2934, FAO livestock protein tables, WHO Essential Nutrition guidelines, and FDA GRAS notices to benchmark demand pools. Industry white papers from the European Federation of Food Science, peer-reviewed articles in Nucleic Acids Research, and patent families scraped via Questel helped clarify technology shifts. Financial cues were drawn from public filings of leading nucleotide producers, while pricing trends came from Dow Jones Factiva news archives and D&B Hoovers company dossiers. These examples illustrate, not exhaust, the secondary sources consulted to ground volumes, prices, and regulatory context.

A second pass focused on country-level production incentives (e.g., China's tax rebates for bio-fermentation parks) and import duties, allowing us to refine regional cost curves. Additional customs databases and national statistics portals were screened to validate cross-border trade flows and remove double counting. Many other public and paid references were also reviewed as needed.

Market-Sizing & Forecasting

A top-down reconstruction starts from global nucleotide output reported by manufacturers and customs agencies, which is then allocated to end-use buckets using surveyed inclusion rates and regional demand indicators. Selective bottom-up checks, such as sampled ASP × volume roll-ups at leading suppliers and channel audits, are applied to stress-test totals. Key variables include installed fermentation capacity expansions in China, median nucleotide load per kilogram of infant formula, mRNA vaccine batch requirements, feed-premix penetration in aquaculture, and lab-grade reagent price erosion. A multivariate regression model, backed by expert consensus, projects each driver to 2030. Scenario analysis covers raw-material price shocks and regulatory swings. Gaps in bottom-up granularity are bridged through ratio imputation anchored to verified historical relationships.

Data Validation & Update Cycle

Outputs pass three-layer checks: variance analysis versus historical series, peer model comparison, and senior-analyst review. We refresh every twelve months, with interim updates triggered by capacity additions, major regulatory changes, or price movements, ensuring clients receive a current, balanced view.

Why Mordor's Nucleotides Baseline Commands Reliability

Published figures often diverge because firms choose different grade mixes, include downstream formulations, or apply dissimilar ASP progressions. By reporting only raw nucleotide revenue and keeping forecast logic transparent, our baseline reduces scope creep and currency noise.

Key gap drivers versus other publishers include: (1) Some aggregate oligonucleotide therapeutics revenue, inflating totals; (2) Others use a uniform global ASP, ignoring Asia's lower ex-works prices; (3) A few rely on historical CAGR extrapolations without reconciling new Chinese capacity or vaccine-linked demand spikes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.85 B (2025) | Mordor Intelligence | - |

| USD 0.93 B (2024) | Global Consultancy A | Includes finished diagnostic kits and applies single ASP for all regions |

| USD 0.76 B (2024) | Industry Intelligence B | Omits lab-grade volumes and uses conservative capacity growth assumptions |

| USD 0.67 B (2024) | Trade Journal C | Forecasts built on straight-line CAGR without primary validation |

The comparison shows that our disciplined scope definition, mixed-method modeling, and annual refresh cadence yield a balanced, reproducible baseline that decision-makers can trust for strategic planning.

Key Questions Answered in the Report

How fast is the nucleotides market expected to grow through 2031?

The market is forecast to post a 7.49% CAGR, taking value from USD 0.92 billion in 2026 to USD 1.32 billion by 2031.

Which nucleotide class leads global demand today?

Pyrimidine derivatives held 54.87% share in 2025 due to heavy use in mRNA vaccine and infant-formula production.

What is driving the surge in pharmaceutical-grade nucleotide consumption?

Four FDA approvals in 2024 validated oligonucleotide therapies and, coupled with 1,261 RNA-based drugs in development, are pulling more GMP-grade supply into biopharma channels.

Why are clean-label nucleotide supplies tight in Europe?

Organic-formula growth, strict EU purity rules, and limited dedicated fermenter capacity have pushed lead times for certified batches to 20 weeks.

Page last updated on: