Chromatography Reagents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

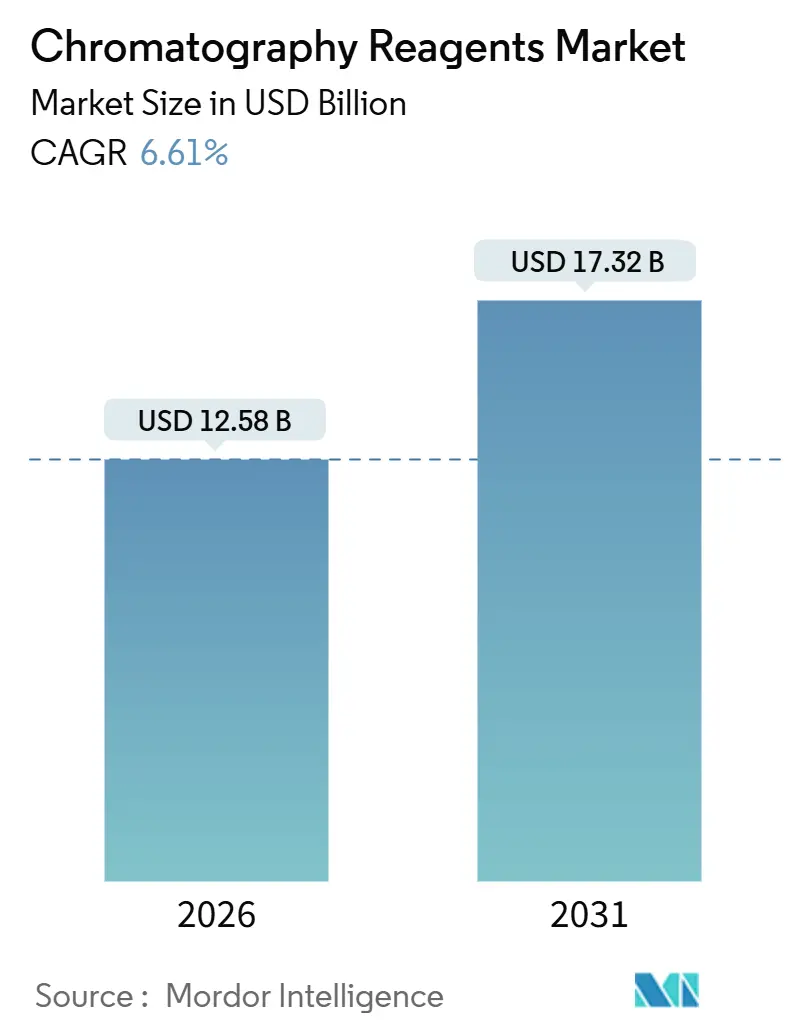

| Market Size (2026) | USD 12.58 Billion |

| Market Size (2031) | USD 17.32 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

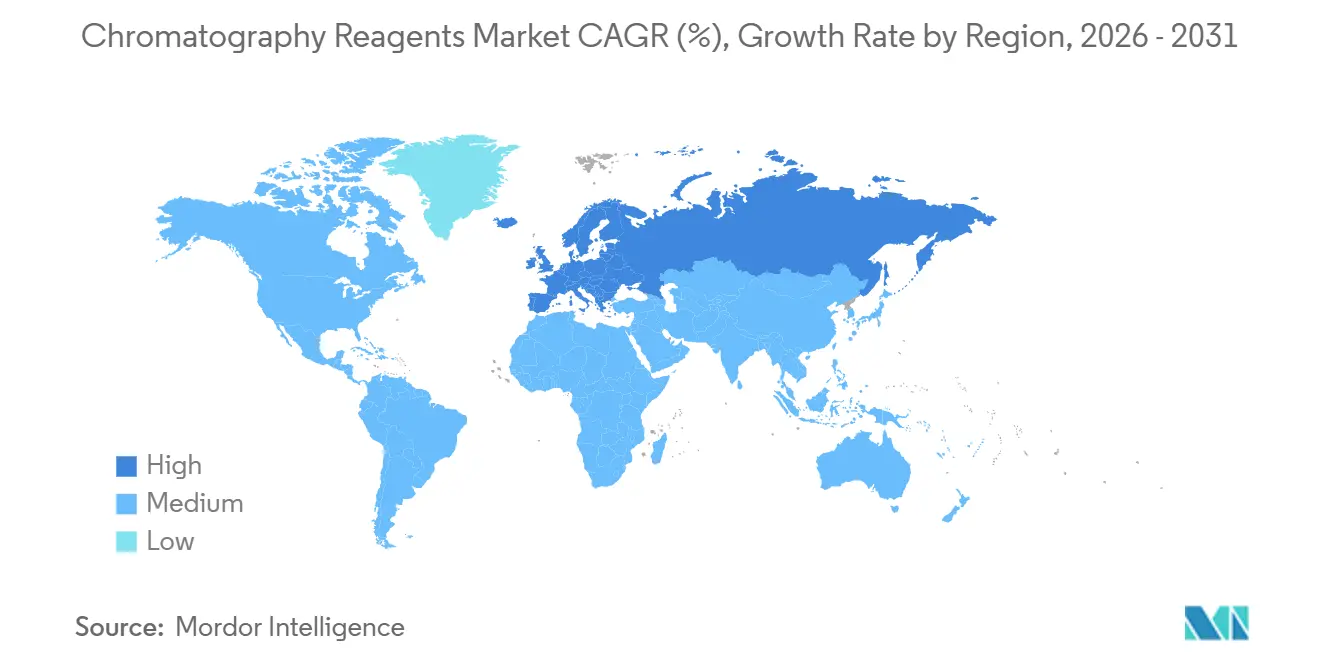

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromatography Reagents Market Analysis by Mordor Intelligence

The Chromatography Reagents Market size is estimated at USD 12.58 billion in 2026, and is expected to reach USD 17.32 billion by 2031, at a CAGR of 6.61% during the forecast period (2026-2031). Pharmaceutical manufacturers are accelerating the shift toward continuous, single-use bioprocess platforms, which require ultra-low-metal solvents and pre-sterilized buffer kits that support mass-spectrometry detection limits below 1 ppb. Food-safety and environmental regulations—most notably stricter PFAS limits in drinking water—are propelling adoption of hydrophilic interaction LC protocols that consume more specialty reagents than traditional reversed-phase workflows. Demand is also expanding as European pesticide directives force laboratories to run two-dimensional GC-MS screens that double solvent and derivatization use per sample. Competitive dynamics remain shaped by instrument vendors that bundle proprietary reagent kits with LC-MS systems, even as specialty chemical suppliers gain share by guaranteeing sub-5 ppb metal content at lower prices.

Key Report Takeaways

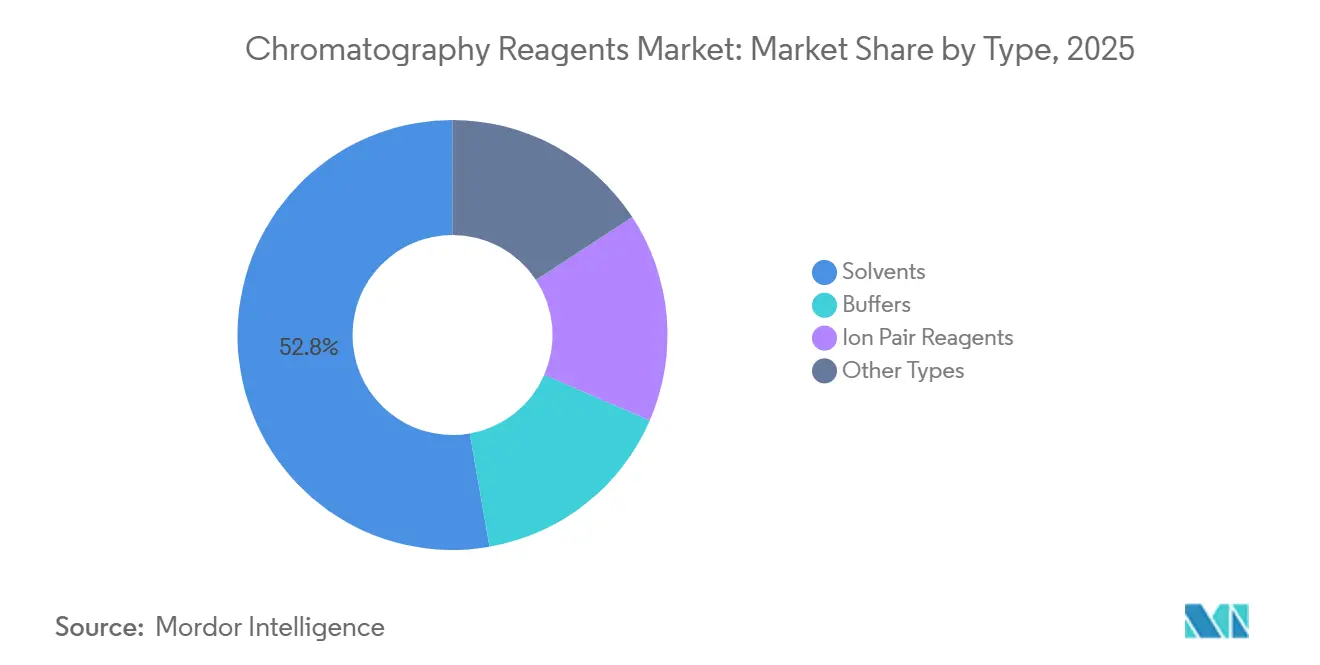

- By type, solvents led with 52.75% revenue share in 2025, while ion pair reagents are projected to expand at a 6.75% CAGR through 2031.

- By physical state of mobile phase, liquid chromatography reagents accounted for 82.56% of 2025 sales, whereas gas chromatography reagents are advancing at a 7.20% CAGR to 2031.

- By technology, affinity exchange captured a 50.75% share in 2025 and is growing at a 7.48% CAGR over the forecast horizon.

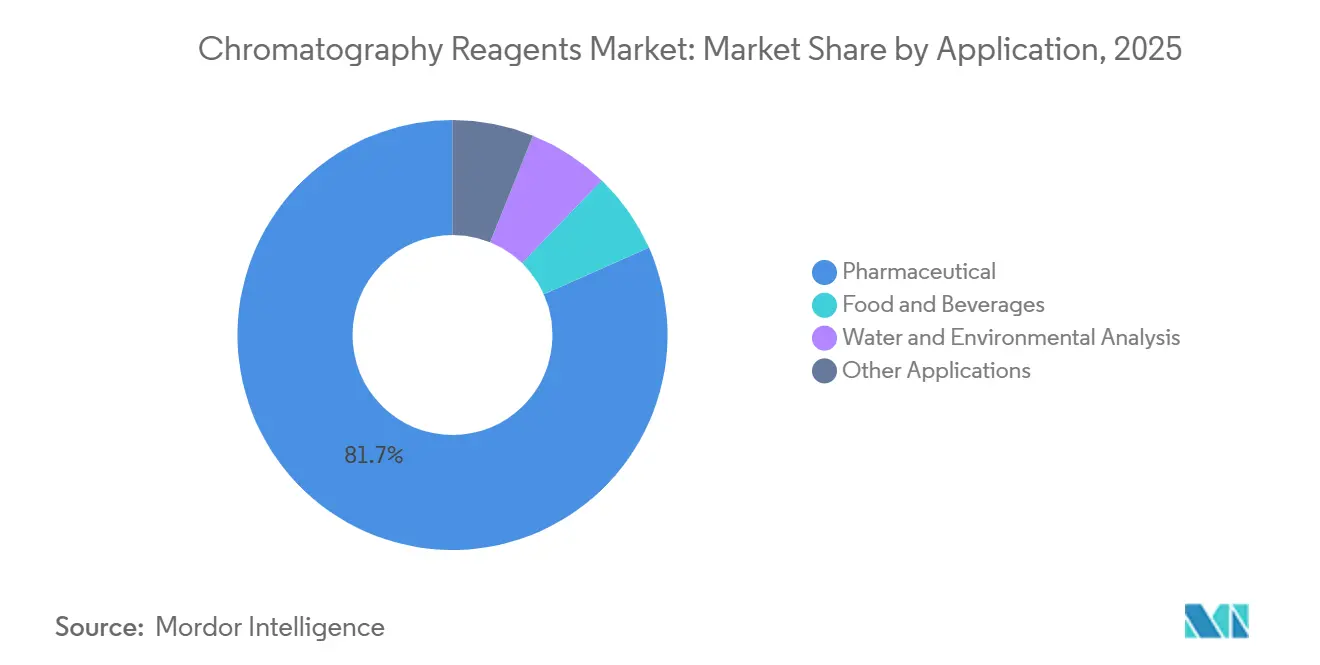

- By application, pharmaceutical workflows commanded an 81.67% share in 2025 and are set to expand at a 6.97% CAGR to 2031.

- By geography, North America held a 46.82% share in 2025, while Europe is forecast to post the fastest 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chromatography Reagents Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from pharmaceutical and biotech manufacturing | +1.8% | Global, concentrated in North America, Europe, and APAC hubs (Singapore, South Korea) | Medium term (2-4 years) |

| Expanding research and development budgets in biotechnology and life-science institutes | +1.3% | North America and EU, with emerging impact in China and India | Long term (≥ 4 years) |

| Stricter global food-safety and environmental-testing regulations | +1.2% | EU (pesticide residues), North America (PFAS), APAC (food export compliance) | Short term (≤ 2 years) |

| Shift to MS-coupled HILIC methods requiring ultra-low-metal reagents | +0.9% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Continuous single-use bioprocessing boosting buffer and single-shot solutions | +1.1% | North America, EU, and APAC biomanufacturing clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Pharmaceutical and Biotech Manufacturing

Between 2024 and 2025, global CDMOs expanded their single-use bioreactor capacity. Each batch requires capture and polishing buffers, resulting in a buffer-to-product ratio and ensuring consistent reagent demand. While the disposable column format streamlines the process by eliminating the need for cleaning validation, it also increases per-batch reagent costs, as these columns are typically discarded after a limited number of cycles. Furthermore, new FDA guidelines on continuous biologics manufacturing mandate that QC labs conduct chromatography assays frequently, leading to a significant increase in solvent throughput compared to traditional batch releases. In the Asia-Pacific region, CDMOs are rapidly expanding their capacities. Notably, South Korea and India have made substantial investments in chromatography-enabled suites during 2024-2025, bolstering the global presence of the chromatography reagents market. These strategic expansions are pivotal in supporting the anticipated growth of overall revenue.

Expanding Research and Development Budgets in Biotechnology and Life-Science Institutes

In 2025, global funding for life-science research and development reached significant levels. Notably, programs in proteomics and metabolomics are consuming a substantial share of LC-MS solvents, buffers, and standards. As universities transition from manual HPLC benches to round-the-clock automated UHPLC platforms, reagent consumption per instrument has surged. Horizon Europe, with an eye on the future, allocated funds for molecular medicine initiatives through 2025. A key stipulation was the use of standardized chromatography methods with certified solvents, further bolstering the chromatography reagents market. In a notable move, China's science foundation amplified its analytical-chemistry grants in 2025. Many of these projects are pivoting towards greener mobile phases, which, paradoxically, is driving a short-term spike in reagent purchases for method validation. Meanwhile, private biotech startups are increasingly turning to CROs for method development. These CROs, while securing volume discounts, are also prioritizing suppliers that offer just-in-time deliveries, a strategy aimed at minimizing inventory carrying costs.

Stricter Global Food-Safety and Environmental-Testing Regulations

Utilities in North America are set to increase their annual LC-MS/MS analyses, a move prompted by the U.S. EPA's 2024 rule designating six PFAS compounds as hazardous[1]U.S. Environmental Protection Agency, “PFAS Rule,” epa.gov . Each analysis utilizes a methanol-acetonitrile blend, leading to a rise in solvent demand. Meanwhile, the EU's 2025 tightening of MRLs for 23 pesticides under its Farm-to-Fork plan has pushed food importers to implement multi-residue GC-MS and LC-MS protocols, which depend on derivatization reagents and matrix-matched standards. In Japan, the positive-list legislation on seafood drug residues mandates the use of ion-pairing reagents, specifically heptafluorobutyric acid, further amplifying regional demand. Collectively, these regulatory measures bolster the upward trajectory of the chromatography reagents market.

Shift to MS-Coupled HILIC Methods Requiring Ultra-Low-Metal Reagents

Benchtop triple-quadrupole LC-MS systems have seen increased installations, effectively displacing traditional optical detectors. HILIC separations demand solvents with minimal metal content. In response, suppliers rolled out acetonitrile and ammonium formate certified for ultra-low metal levels, but at a premium over standard LC-grade products. Each batch of oligonucleotide drugs requires high-grade acetonitrile and ammonium acetate, highlighting the therapeutic RNA pipeline as a significant growth opportunity. The ICH Q3D(R2) guideline, coming into effect in 2024, has tightened elemental impurity limits for inhaled drugs. This mandates a universal validation process to ensure chromatography solvents remain metal-free. Collectively, these dynamics are propelling a niche yet swiftly growing segment within the chromatography reagents market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of high-purity reagents and volatile raw-material pricing | -0.7% | Global, acute in price-sensitive APAC and South America markets | Short term (≤ 2 years) |

| Persistent acetonitrile supply shocks and price volatility | -0.9% | Global, most severe in North America and Europe due to high LC-MS adoption | Medium term (2-4 years) |

| Solvent-reduction/green-chemistry workflows lowering per-sample volumes | -0.5% | EU and North America, driven by sustainability mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of High-Purity Reagents and Volatile Raw-Material Pricing

In 2025, LC-MS-grade acetonitrile commanded significantly higher prices than its technical-grade counterpart. This premium pricing is largely due to stringent producer requirements, mandating sub-1 ppb elemental contamination levels. Pricing fluctuations in raw materials are not merely incidental; they are deeply rooted in the production process. Acetonitrile is predominantly a by-product of propylene-based acrylonitrile production, making its pricing susceptible to the inherent volatilities of the petrochemical market. In 2024, disruptions caused by hurricanes led to a reduction in output from the U.S. Gulf Coast. This shortfall compelled distributors to ration their allocations, nudging smaller laboratories to pivot towards methanol as a substitute. However, this switch came with a trade-off: longer run times[2]Alexandra Aiken, “Acetonitrile Shortage Disrupts Chromatography Labs,” cen.acs.org.

Persistent Acetonitrile Supply Shocks and Price Volatility

In 2024, an explosion at a Jiangsu plant significantly reduced capacity. This incident sent spot prices soaring, doubling the levels seen in 2023. In response, QC labs scrambled to install solvent-recycling systems to safeguard their supply. Meanwhile, European labs have stockpiled inventories for extended periods, a move that has tied up their working capital and escalated storage costs. Despite the challenges, no regulatory body has designated acetonitrile as a strategic chemical, leaving buyers to shoulder the entire procurement risk. While some vendors advocate for supercritical fluid chromatography—an approach that utilizes carbon dioxide and can reduce acetonitrile usage—its adoption remains limited. This limited uptake is attributed to challenges in method portability and the steep capital investment required.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ion Pair Reagents Gain Traction in Peptide Analytics

Ion pair reagents recorded a 6.75% CAGR outlook to 2031, outpacing the broader chromatography reagents market size, as peptide and oligonucleotide pipelines grow. Solvents still dominate revenue and captured a 52.75% chromatography reagents market share in 2025, but per-analysis volumes are slipping as gradient optimization and narrow-bore columns shorten equilibration times.

As single-use bioprocessing prioritizes lot-to-lot consistency, the demand for pre-formulated GMP buffers remains robust. Suppliers are setting themselves apart by offering just-in-time delivery and consignment stock programs, alleviating the working-capital pressures faced by CDMOs. While volatile ion-pairing agents facilitate MS-compatible separations, they necessitate corrosion-resistant titanium flow paths. This requirement carves out a distinct growth trajectory within the chromatography reagents market.

By Physical State of Mobile Phase: GC Reagents Surge on Environmental Mandates

Gas chromatography reagents are set for a 7.20% CAGR to 2031, the fastest among physical-state segments, helped by EU and U.S. rules expanding pesticide and VOC screening that depend on two-dimensional GC-MS workflows. Liquid chromatography reagents retained 82.56% of 2025 revenue, anchored by pharmaceutical QC and bioprocess PAT applications.

In 2024, regulators revised the Industrial Emissions Directive, reducing VOC discharge limits. This move necessitated real-time GC monitoring, which now demands carrier gases and calibration standards at significantly higher rates than historical norms. While SFC reagents occupy a niche, they offer a substantial reduction in solvents. This aligns with sustainability mandates, even if they lack widespread recognition in pharmacopeias. The growing adoption of GCxGC in flavor and fragrance analytics is driving up the demand for derivatization chemicals and ultra-high-purity helium, further diversifying the physical phases of the chromatography reagents market.

By Technology: Affinity Exchange Dominates Biologic Purification

Affinity exchange maintained a 50.75% revenue share in 2025 and is forecast at a 7.48% CAGR, driven by protein A resins that reach 99% purity in a single step. Ion exchange remains critical as a polishing technique, but commoditized strong anion exchangers dilute revenue even as volumes stay high.

South Korean and Chinese biosimilar producers are offering significant discounts, putting pressure on Protein A resin prices. However, established Western suppliers maintain an advantage during regulatory audits, thanks to concerns over ligand leaching. Mixed-mode resins are costly but provide a notable boost in productivity. This allows facilities to increase protein load without a breakthrough, a benefit that Contract Development and Manufacturing Organizations (CDMOs) leverage to optimize capacity utilization. The market for chromatography reagents in AAV gene-therapy purification is rapidly expanding. SEC and salt-tolerant ion exchangers are adept at managing complex viral vectors, underscoring a trend towards technology diversification.

By Application: Pharmaceutical Segment Drives Volume and Innovation

Pharmaceutical workflows generated 81.67% of 2025 revenue and are on track for a 6.97% CAGR. This growth mirrors biologics' substantial stake in drug approvals, which typically demand three to five chromatography steps per campaign. Meanwhile, food and beverage testing is gaining momentum. This surge follows major retailers, such as Walmart, expanding their pesticide screening lists to encompass more compounds, thereby increasing the volume of multi-residue methods.

In California, water-quality mandates set PFAS notification levels at a stringent threshold. This regulation necessitates monthly LC-MS/MS assays, each consuming a considerable amount of solvents. Such demands are propelling the market for chromatography reagents. Additionally, clinical labs conducting metabolic screens for newborns are increasingly turning to GC derivatization kits, highlighting a niche yet growing segment. While pharmaceuticals drive the chromatography reagents market, these diverse applications ensure a robust consumption base.

Geography Analysis

North America accounted for 46.82% of 2025, driven by robust demand. The U.S., housing a significant portion of the world's biologics capacity, enforces stringent cGMP regulations, emphasizing the need for traceable and validated reagents. Regional CDMOs are increasingly adopting pre-formulated buffers, streamlining batch processes, and enhancing solvent and buffer throughput. Canada's cannabis testing regulations, expanded in 2024, now account for additional monthly chromatography runs, heavily utilizing derivatization reagents and LC-MS solvents. Meanwhile, Mexico is emerging as a prominent near-shoring hub, evidenced by a rise in its API exports to the U.S. in 2025, subsequently driving up demand for HPLC solvents.

Europe is projected to grow the fastest at an 8.21% CAGR through 2031. This momentum is largely attributed to revisions by the EMA, which halved the permissible limits on elemental impurities. These changes have mandated a widespread shift to ultra-low-metal solvents across the industry, bolstering the market size for chromatography reagents. In Germany, the Fraunhofer Institute has initiated pilot continuous chromatography facilities, utilizing custom buffers monthly during their optimization phase. The UK's MHRA is championing single-use technology in cell therapies, leading to increased buffer volumes. Concurrently, Sweden's KEMI is urging labs to phase out halogenated solvents by 2028, driving a shift towards ethanol-water systems.

The Asia-Pacific region showcases a mixed landscape. In 2025, China's NMPA greenlit new biologics plants, contributing additional single-use bioreactor capacity and subsequently boosting demand for chromatography reagents. Japan's pharmacopoeia has begun endorsing UHPLC across several monographs. While the transition from 4.6 mm to 2.1 mm columns has achieved a significant reduction in solvent volume per run, the overall solvent volumes remain consistent due to increased sample throughput. South Korea's industry giants, Samsung Biologics and Celltrion, have collectively augmented their biosimilar capacity through 2025, leading to heightened orders for protein A resin. Singapore, on the other hand, has witnessed an uptick in biopharma output, with chromatography consumables constituting a notable portion of production costs. This diverse regional activity underscores the long-term robustness of the chromatography reagents market.

Regulatory Landscape

Chromatography reagents are governed primarily as chemical substances, with market access and ongoing compliance shaped by chemical-registration frameworks and analytical-grade specifications. In the European Union, REACH (Regulation (EC) No 1907/2006, consolidated as of December 2024) drives registration and data requirements for substances manufactured or imported at or above 1 tonne per year, shaping documentation, testing depth, and supply continuity for solvent and reagent portfolios sold into EU laboratories and GMP environments.

Across end-use testing, method and quality requirements reinforce demand for consistent, traceable reagent performance. In the United States, EPA requirements under 40 CFR Part 158 for pesticide registration data underpin residue and environmental screening workflows that rely on chromatography reagents, while laboratory-grade quality benchmarks are anchored by standards such as ASTM D1193-24 for reagent water and ISO reagent specifications (for example, ISO 6353 series). For cross-border trade, Harmonized Tariff Schedule (HTS) classifications published by the USITC (2026) also affect operations, as accurate HS documentation reduces customs friction for analytical instruments and associated supply chains serving chromatography labs.

Value Chain Analysis

The value chain starts with upstream feedstocks and specialty inputs, including petrochemical derivatives for key solvents (acetonitrile and methanol), high-purity inorganic salts for buffers, and niche materials such as silica-based media, affinity ligands, and certified reference materials. Manufacturing is split between high-volume solvent production and precision formulation, filtration, and packaging steps needed for LC-MS and GMP-grade reagents, including controlled contamination (metals and particulates), batch traceability, and specialized packaging (for example, amber glass and inert-atmosphere handling).

Downstream distribution covers direct supply programs to pharma and biomanufacturing accounts, specialty distributors supporting routine analytical labs, and made-to-order, method-specific offerings for CROs and CDMOs that prioritize just-in-time delivery and lot consistency. The chain is exposed to single-source vulnerabilities in some high-value components, including affinity ligands and bead matrices, and to long lead times for certified standards. Larger integrated suppliers also differentiate by bundling columns, kits, and digital replenishment tools to reduce stockout risk for high-throughput QC operations.

Competitive Landscape

The chromatography reagents market is moderately consolidated. The top five suppliers' dominance leaves opportunities for specialty chemical producers and regional distributors. While vendors vie for competitive pricing and swift delivery, commodity solvent margins remain stable. In contrast, ultra-low-metal and MS-grade lines enjoy a premium, a testament to suppliers' certification of sub-1 ppb contamination, traceable to NIST standards. A burgeoning opportunity exists in turnkey buffer kits tailored for gene-therapy purification. Here, the intricate processes and heightened regulatory scrutiny lean towards the appeal of ready-to-use solutions. Incumbents leverage digital supply-chain tools for differentiation. Vendors with predictive re-ordering platforms are particularly sought after by high-throughput labs, where stockouts pose significant risks. Patent filings highlight the industry's innovative pulse, with applications for alkali-stable protein A ligands and multimodal resin chemistries. The entry barriers in this market are formidable. Reagents destined for GMP environments must adhere to stringent pharmacopeial specifications and quality systems, often necessitating an investment in compliant facilities.

Chromatography Reagents Industry Leaders

Thermo Fisher Scientific Inc.

Merck KGaA

Agilent Technologies Inc.

Waters Corporation

Avantor Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An increasingly visible whitespace centers on bioprocessing-grade chromatography inputs that reduce preparation time while meeting regulated QC expectations. This includes pre-formulated buffer kits, MS-compatible ion-pairing systems, and resins designed for quicker column readiness, reflecting the shift toward more standardized and repeatable downstream operations in pharma manufacturing.

Capacity localization and portfolio consolidation are also creating procurement opportunities for labs and biomanufacturers managing supply volatility in critical consumables. In April 2026, DuPont introduced AmberChrom XT SL chromatography resins positioned to simplify biopharmaceutical workflows by eliminating resin hydration steps during column packing. Welch Materials inaugurated a chromatography packing material production base in January 2026 in Nanjing, China, with stated capacity targets of 190,000 chromatographic columns and 30 tons of purification materials per year to support regional availability for high-throughput users. Separately, Merck (MilliporeSigma) completed the acquisition of the JSR Life Sciences chromatography business in April 2026, adding Amsphere Protein A resins and related capabilities, which expands integrated downstream supply options for monoclonal antibody and other biologics purification programs.

Recent Industry Developments

- July 2026: Agilent expanded its Altura portfolio by adding inert size exclusion and PLRP-S columns tailored for biotherapeutic analysis. The update supports workflows that require improved inertness and robustness for complex biomolecules, reinforcing bundled solutions where columns and method packages drive repeatability in regulated labs.

- May 2026: Agilent launched a Multi-Attribute Method (MAM) solution aimed at helping pharmaceutical and biopharmaceutical QC laboratories implement LC/HRMS in regulated environments. By packaging a standardized approach for MAM adoption, the launch increases pull-through for compatible high-purity mobile phases, buffers, and other chromatography reagents used in routine release and characterization testing.

- April 2026: Merck (MilliporeSigma) completed its acquisition of JSR Life Sciences chromatography business, adding Amsphere Protein A resins and related downstream purification capabilities to its life science portfolio. The transaction deepens vertical offerings in biologics purification, supporting integrated supply of chromatography consumables and associated reagents for CDMOs and biomanufacturers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned from chromatography reagents sold for separation and analysis workflows, across common chromatography techniques, and across end users like labs and production environments.

Scope exclusions: chromatography instruments, columns, resins, software, and service or maintenance revenues are not counted as part of this market.

Segmentation Overview

- By Type

- Buffers

- Ion Pair Reagents

- Solvents

- Other Types

- By Physical State of Mobile Phase

- Gas Chromatography Reagents

- Liquid Chromatography Reagents

- Super-Critical Fluid Chromatography Reagents

- By Technology

- Ion Exchange

- Affinity Exchange

- Size Exclusion

- Hydrophobic Interaction

- Mixed-Mode

- Other Technologies

- By Application

- Pharmaceutical

- Food and Beverages

- Water and Environmental Analysis

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand context and to avoid guessing on what is already observable in public data. Sources included the US FDA database for drug approvals (as a proxy for downstream chromatography usage in pharma pipelines), the NIH and PubMed ecosystem to gauge chromatography-intensive research activity, and CDC and WHO statistics that indicate testing volumes and disease monitoring priorities.

To translate the context into sizing inputs, we also reviewed USITC and UN Comtrade trade statistics for relevant chemical categories, and OECD and World Bank indicators for country-level lab and manufacturing capacity signals. Documents from scientific and chromatography-focused associations were used to understand method adoption and quality practices. Company annual reports, investor presentations, and credible press were included to capture pricing actions and mix shifts. Where needed, paid subscriptions already used internally were referenced for company financials, patent signals, and shipment-level trade visibility. These desk sources are illustrative and not exhaustive, and many other public references were used for validation and clarification.

Primary Interviews and Surveys

Primary work was completed through expert interviews and structured surveys with reagent manufacturers, distributors, lab procurement teams, and chromatography users in pharma, biotech, food testing, and environmental labs. These conversations were used to confirm what is purchased as a chromatography reagent versus a consumable accessory, to understand typical pack sizes and buying frequency, and to stress-test pricing and mix assumptions across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | APAC: 51% |

| Mid tier: 52% | Functional/Unit leaders: 25% | EMEA: 31% |

| Smaller Players: 16% | Managers: 59% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was first reconstructed using a top-down build that links chromatography reagent demand to the active installed base and usage intensity in chromatography workflows, and then cross-checks were applied using selective bottom-up approximations. In practice, we start from country and region level indicators that reflect analytical testing and bio-manufacturing activity, and then apply penetration and usage assumptions to arrive at value.

Key model inputs included, for example, pharma and biopharma R&D intensity, biologics and small-molecule manufacturing scale, lab testing throughput in food and environmental labs, growth in chromatography use in quality control, and observed pricing and mix changes between buffers, solvents, and other reagent types. Assumptions that are not consistently visible in public sources, such as replacement cycles, method-specific consumption, and discounting practices, were tightened through interviews and then applied in a repeatable way across geographies.

For forecasting, scenario analysis was used, supported by short trend models on stable drivers like R&D and testing growth, and then moderated by expert views on adoption speed and price progression. Where bottom-up checks had gaps, such as missing revenue splits for smaller entities, conservative proxy shares were applied based on peer sets and distribution-channel checks, and then totals were rebalanced back to the top-down demand pool.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the numbers do not rely on any single data stream. Totals were compared against independent signals such as trade movement trends, reported lab spending priorities, and observed shifts in chromatography usage by application, and large variances were investigated before sign-off.

A second analyst review was used to test the logic, the math, and the narrative consistency, followed by targeted re-contacts when an assumption drove an outlier result. Reports are refreshed annually, with interim updates triggered by material events that can affect pricing, supply, or demand. Before delivery, a fresh review pass is done so clients receive the most current view possible.

Mordor Intelligence's Chromatography Reagents Market Size Compared With Other Published Estimates

Different published market sizes for chromatography reagents often do not match because the scope lines are drawn differently, and because the conversion from lab activity into dollars depends on pricing and mix assumptions. The year used as the anchor, the included end uses, and how regional currency and inflation are handled can also shift results.

Chromatography columns and instruments sit outside Mordor Intelligence's scope in this report, which keeps the value focused on reagent revenues even when suppliers sell bundled solutions. Other gaps usually come from including a wider set of lab chemicals beyond chromatography-specific reagents, applying faster price growth without checking distributor discounting, or using older base-year splits that have not been refreshed after mix changes between solvents, buffers, and specialty reagents.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.58 B (2026) | |

| Global Consultancy A | USD 7.30 B (2024) | Uses an earlier anchor year and a narrower conversion from chromatography activity into reagent spend, and the excerpt does not clarify whether method-specific consumption rates and discounting were primary-validated. |

| Industry Publisher B | USD 6.81 B (2024) | Runs on a different study window and base year, and typically applies a broad product framing where some adjacent lab chemical spending can be blended unless reagent-only boundaries are explicitly enforced. |

The spread in values is mainly explained by what is counted as a reagent, and by the base year and pricing path used to turn usage into revenue. By keeping the scope tied to reagent sales and by aligning assumptions to observed demand signals and interview checks, the estimate stays traceable to clear drivers and can be repeated when the inputs are updated.

Key Questions Answered in the Report

How large is the chromatography reagents market?

The market generated USD 12.58 billion in 2026 and is on track to hit USD 17.32 billion by 2031, registering a CAGR of 6.61%.

Which segment contributes the most to chromatography reagent revenue?

Solvents dominated 2025 revenue with a 52.75% share, reflecting their ubiquity across all chromatographic modes.

Which region is growing fastest for reagent demand?

Europe is forecast to register the quickest 8.21% CAGR through 2031 as new impurity limits drive adoption of ultra-low-metal solvents.

What is driving the switch to ultra-low-metal reagents?

Mass-spectrometry detection and tighter elemental-impurity guidelines require solvents certified below 1 ppb total metals to avoid ion suppression.

How are supply shocks affecting acetonitrile pricing?

Production disruptions in 2024 doubled spot prices and led labs to install recycling systems or substitute methanol, highlighting continued volatility.

Which technology segment shows the highest growth?

Affinity exchange reagents, led by protein A resins for monoclonal antibodies, are projected to grow at a 7.48% CAGR to 2031.

Page last updated on: