North America Cotton Seed Treatment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

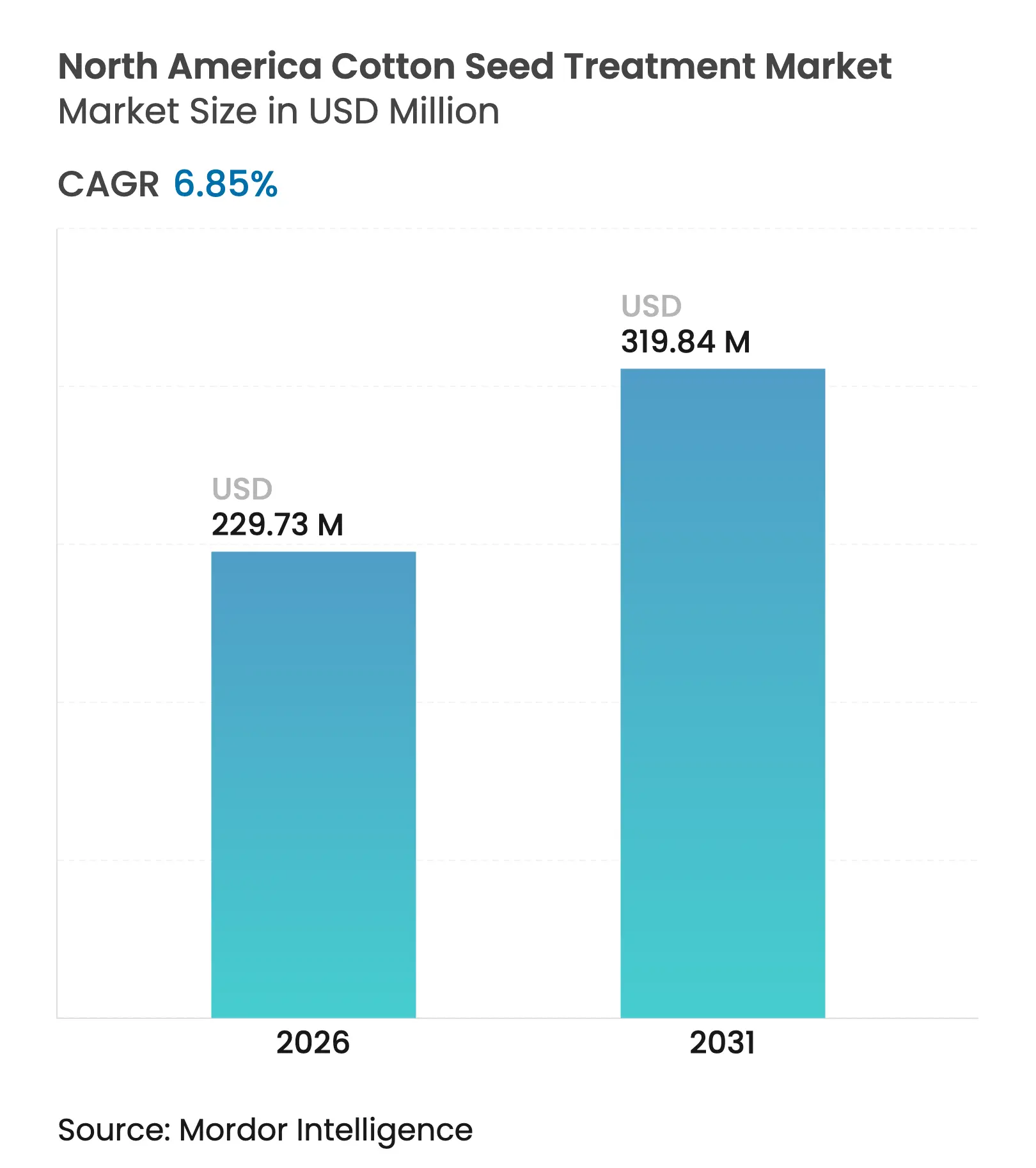

| Market Size (2026) | USD 229.73 Million |

| Market Size (2031) | USD 319.84 Million |

| Growth Rate (2026 - 2031) | 6.85 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Cotton Seed Treatment Market Analysis by Mordor Intelligence

The North America cotton seed treatment market size is expected to grow from USD 215.0 million in 2025 to USD 229.73 million in 2026 and is forecast to reach USD 319.84 million by 2031 at 6.85% CAGR over 2026-2031. Growers continue to shift away from broad-spectrum foliar programs because early-season pest pressure is now more efficiently managed through seed-applied technologies, especially in areas where pink bollworm resistance has rendered aerial sprays ineffective. Liquid flowable concentrates dominate because they meter cleanly through high-speed commercial treaters, while biological actives gain traction as retailers pursue residue-free lint across export channels. Capital-intensive on-farm treating equipment favors large operators in Texas and Georgia, yet cooperative treating hubs in northern Mexico are accelerating regional adoption. Competitive differentiation is concentrated in combination packages that stack synthetic insecticides, biological fungicides, and polymer coatings to delay resistance and cut dust-off during planting.

Key Report Takeaways

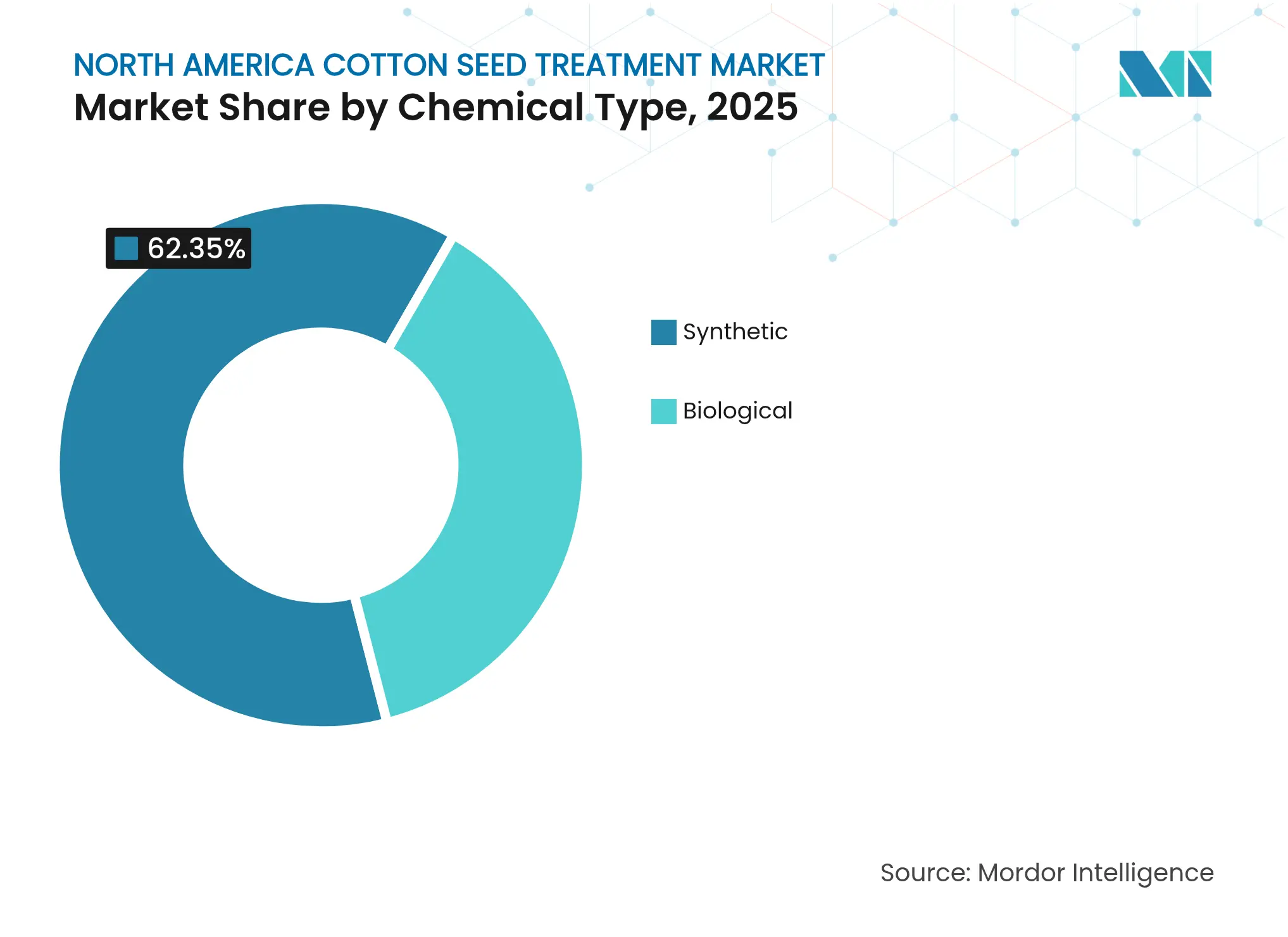

- By chemical type, synthetic formulations captured 62.35% of the North America cotton seed treatment market size in 2025, while biologicals are advancing at an 10.98% CAGR through 2031.

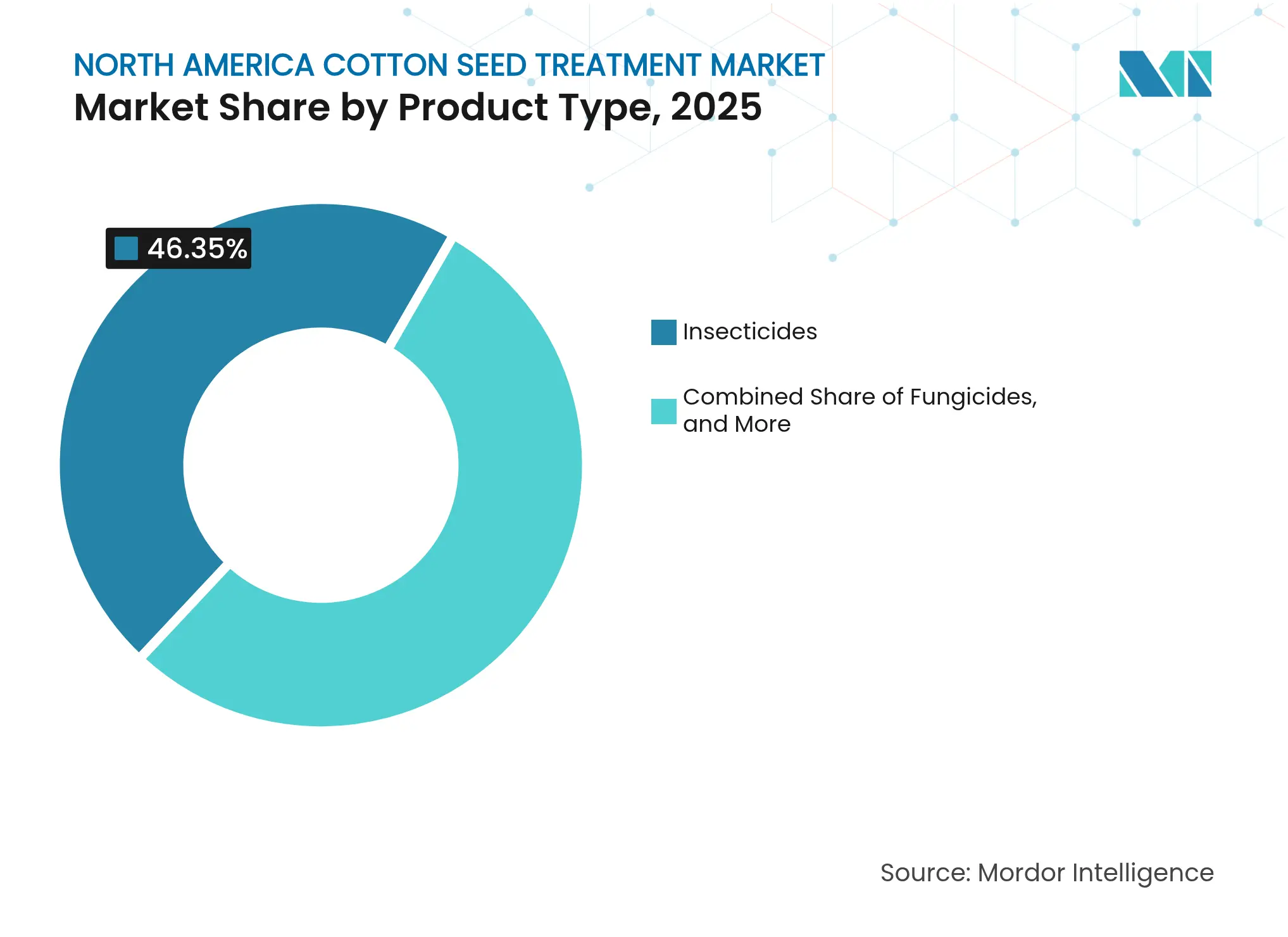

- By product type, insecticides led the North America cotton seed treatment market with 46.35% of the market size in 2025, whereas the fungicides category is forecast to expand at a 9.42% CAGR through 2031.

- By geography, the United States holds the largest 66.25% of the North America cotton seed treatment market share in 2025, and Mexico is projected to grow at an 8.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Cotton Seed Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost–benefit ratio versus soil and foliar spraying High cost–benefit ratio versus soil and foliar spraying | +1.8% | United States, and Mexico | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:United States, and Mexico |

Impact Timeline

:

Medium term (2-4 years)

|

Surging insecticide resistance in pink bollworm and plant bug populations Surging insecticide resistance in pink bollworm and plant bug populations | +1.5% | United States (Texas, Arizona, Georgia) | Short term (≤ 2 years) | |||

Tightening worker-safety rules on aerial pesticide use Tightening worker-safety rules on aerial pesticide use | +1.2% | United States, and Canada | Medium term (2-4 years) | |||

Rapid shift toward biological seed protectants Rapid shift toward biological seed protectants | +1.4% | United States and Mexico | Long term (≥ 4 years) | |||

Plant-back interval waivers boosting pre-season adoption Plant-back interval waivers boosting pre-season adoption | +0.6% | United States (Mid-South, Southeast) | Short term (≤ 2 years) | |||

Edge-of-field water-quality credits for treated seeds Edge-of-field water-quality credits for treated seeds | +0.5% | United States (Mississippi River Basin) | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost-Benefit Ratio Versus Soil and Foliar Spraying

Seed-applied actives deliver up to a 90% reduction in total pesticide use compared to broadcast foliar programs, a cost advantage that becomes decisive when diesel and aerial application labor exceed USD 25 per acre. University trials in Texas documented that a USD 12 per acre seed-treatment investment prevented an average of 3.2 foliar insecticide sprays, saving growers USD 68 per acre in application costs and reducing environmental loading by 85%. The shift is also driven by tightening buffer-zone requirements for aerial spraying near schools and residential areas, which have expanded from 100 feet to 300 feet in California and are under review in other states, effectively removing foliar options for edge-of-field cotton blocks. The trend is accelerating consolidation in the United States cotton belt, with the average farm size in the Mid-South increasing from 1,200 acres in 2020 to 1,650 acres in 2024 [1]Source: United States Department of Agriculture Economic Research Service, “Cotton and Wool Data,” ers.usda.gov .

Surging Insecticide Resistance in Pink Bollworm and Plant Bug Populations

Field-evolved resistance to pyrethroid insecticides has been confirmed in pink bollworm populations in Arizona, Texas, and parts of northern Mexico, rendering foliar sprays ineffective and forcing growers to adopt seed treatments with alternative modes of action, such as diamides and neonicotinoids. The resistance crisis is driving demand for multi-mode seed-treatment packages that combine neonicotinoids, diamides, and biological insecticides in a single coating. Corteva's Lumisena, which pairs a Bt protein with a chemical insecticide, is gaining traction in resistance hotspots, though its premium pricing limits adoption to high-value irrigated acres. Field trials in Georgia showed that seed treatments combining a neonicotinoid with Beauveria reduced thrips populations by 78% at 21 days after planting, compared to 62% for the neonicotinoid alone.

Tightening Worker-Safety Rules on Aerial Pesticide Use

EPA's revised Worker Protection Standard, implemented in 2024, mandates that aerial applicators wear respirators and chemical-resistant suits during mixing and loading operations, adding 15 to 20 minutes per application and increasing labor costs by USD 8 to USD 12 per acre. The regulatory shift is also creating opportunities for biological seed treatments, which carry lower toxicity classifications and shorter restricted-entry intervals. Seed treatments formulated with Trichoderma or Bacillus strains are exempt from many Worker Protection Standard requirements because they pose minimal inhalation or dermal hazards, allowing growers to plant and scout fields without waiting periods. The trend is reinforcing the economic case for seed treatments, as labor availability for aerial application continues to tighten and wage rates for certified applicators rise 6 to 8% annually.

Rapid Shift Toward Biological Seed Protectants

Biological seed treatments, which include microbial inoculants and biochemical elicitors, are projected to expand at an annual rate of 11.3% through 2030, driven by retailer sustainability mandates and consumer demand for residue-free cotton in apparel and home textiles. Major brands such as Nike and H&M have committed to sourcing 100% of their cotton from farms that reduce synthetic pesticide use by 50% by 2030, creating downstream pressure on growers to adopt biological alternatives. The shift is also being driven by supply-chain economics. Fermentation-based biological actives are produced using renewable feedstocks such as molasses and corn steep liquor, insulating formulators from the price volatility that affects petroleum-derived synthetic chemistries. Biological production faces its own constraints, as fermentation capacity for high-demand strains such as Bacillus amyloliquefaciens remains concentrated in a handful of contract manufacturers in India and Brazil, creating lead times of 6 to 9 months for bulk orders. This bottleneck pushed biological active ingredient prices up 18% in 2024, eroding the cost advantage that biologicals once held over synthetics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Low adoption among small growers lacking on-farm application equipment Low adoption among small growers lacking on-farm application equipment | -0.9% | United States Southeast and Mid-South, Mexico | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

United States Southeast and Mid-South, Mexico

|

Impact Timeline

:

Medium term (2-4 years)

|

Perception that stacked Genetically Modified traits reduce need for seed treatments Perception that stacked Genetically Modified traits reduce need for seed treatments | -0.7% | United States (Texas, Mississippi, Arkansas) | Short term (≤ 2 years) | |||

Regulatory scrutiny on neonicotinoid dust-off issues Regulatory scrutiny on neonicotinoid dust-off issues | -0.5% | United States, and Canada | Medium term (2-4 years) | |||

Supply-chain price spikes in biological actives Supply-chain price spikes in biological actives | -0.6% | United States and Mexico | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Low Adoption Among Small Growers Lacking On-Farm Application Equipment

Farms smaller than 500 acres represent 42% of United States cotton acreage but account for only 18% of seed-treatment adoption, a disparity driven by the high capital cost of on-farm seed treaters and the logistical challenges of coordinating custom application services during the narrow planting window. Commercial seed-treatment equipment ranges from USD 40,000 for basic batch treaters to USD 150,000 for continuous-flow systems with polymer-coating capability, with payback periods exceeding 5 years for operations planting fewer than 1,000 acres annually. The gap is creating market opportunities for seed companies that offer pre-treated seed with flexible delivery schedules, though this model shifts the economic benefit upstream and reduces grower control over active ingredient selection and application timing. In Mexico, smallholder cooperatives are addressing the equipment barrier by pooling capital to purchase shared seed treaters, a model that has increased adoption rates from 12% in 2020 to 31% in 2024 in Chihuahua state.

Perception That Stacked Genetically Modified Traits Reduce Need for Seed Treatments

Third-generation Bt cotton varieties, which express multiple Cry proteins targeting lepidopteran pests, have created a perception among growers that additional seed protection is redundant, particularly in regions where pink bollworm populations remain suppressed by area-wide eradication programs. Field surveys in the Mid-South indicate that 34% of acres planted with stacked-trait cotton receive no seed treatment, a practice that leaves early-season thrips and seedling diseases unmanaged and can reduce stand establishment by 12 to 18% in years with cool, wet springs. The economic consequences of skipping seed treatments are often masked by favorable weather or low pest pressure, leading growers to underestimate the insurance value of seed-applied insecticides. Replant rates for untreated stacked-trait cotton averaged 8.2% in Texas during the 2024 season, compared to 2.1% for treated seed, a difference that translates to USD 45 per acre in additional seed and planting costs [2]Source: Texas A&M AgriLife Research, “Replant Economics in Untreated Bt Cotton,” agriliferesearch.tamu.edu .

Segment Analysis

By Chemical Type: Biologicals Gain Despite Synthetic Dominance

Synthetic formulations captured 62.35% of the North America cotton seed treatment market size in 2025, anchored by neonicotinoid insecticides and triazole fungicides that offer predictable efficacy and multi-season shelf stability. Synthetic formulations retain advantages in insecticide applications, where neonicotinoids and diamides deliver systemic protection for 30 to 45 days after planting, a duration that biological insecticides cannot yet replicate due to their limited residual activity and sensitivity to fluctuations in soil temperature and moisture. The cost differential between synthetic and biological treatments narrowed from 35% in 2020 to 18% in 2025, driven by fermentation-capacity expansions in Asia and regulatory costs that now add USD 2 to USD 3 per acre to synthetic formulations through stewardship fees and environmental monitoring requirements .

Biologicals are advancing at an 10.98% CAGR through 2031, as growers respond to retailer sustainability mandates and seek alternatives to neonicotinoids facing regulatory restrictions. The biological surge is concentrated in fungicide applications, where Trichoderma and Bacillus strains now match the performance of synthetic fungicides against Rhizoctonia and Fusarium seedling diseases while carrying lower environmental persistence and shorter restricted-entry intervals. The biological trajectory suggests that by 2030, biologicals could capture 45 to 50% of the fungicide segment while remaining below 25% in insecticides, creating a bifurcated market where chemical origin aligns with pest target rather than grower philosophy.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Insecticides Lead, Nematicides Accelerate

Insecticides led the North America cotton seed treatment market, accounting for 46.35% of the market size in 2025, reflecting the primacy of early-season thrips and aphid management in cotton production systems. Combination products that pair synthetic insecticides with biological fungicides are emerging as a middle path, capturing 12% of 2025 revenue by offering growers the residual protection of synthetics with the sustainability profile of biologicals. Syngenta's Vibrance technology, which combines a synthetic fungicide with a biological seed-treatment enhancer, is gaining traction in Mexico and the United States Southeast, where seedling disease pressure is high and growers are willing to pay a 10 to 15% premium for improved stand establishment.

The fungicides category is forecast to expand at a 9.42% CAGR through 2031, driven by persistent seedling disease pressure in no-till and minimum-tillage systems where crop residue harbors Rhizoctonia and Pythium inoculum. Field trials in Mississippi showed that seed treatments combining a nematicide with a fungicide increased early-season root mass by 22% and final yield by 8% compared to fungicide-only treatments, a performance gain that justifies the USD 18 to USD 24 per acre cost premium. The shift toward multi-active seed treatments is creating formulation challenges, as compatibility issues between neonicotinoids and certain biological fungicides can reduce efficacy or cause phytotoxicity, requiring formulators to invest in polymer-coating technologies that physically separate incompatible actives on the seed surface.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United States generated a 66.25% market share in 2025, driven by large-scale operations in Texas, Georgia, and Mississippi that plant 1,500 to 5,000 acres of cotton annually, allowing for the amortization of seed-treatment equipment costs across multiple crops and seasons. Texas alone accounts for 35% of the United States' cotton acreage and leads in seed-treatment adoption, with 78% of planted acres receiving at least one seed-applied active ingredient in 2025, up from 62% in 2020.

Mexico is projected to grow at an 8.58% CAGR through 2031, the fastest pace in North America, as cotton acreage expands in Chihuahua and Coahuila states and smallholder cooperatives adopt centralized seed-treatment facilities to meet export-quality standards for the United States and Asian textile markets. Mexico's cotton sector is transitioning from subsistence farming to commercial production, with average farm sizes increasing from 80 acres in 2020 to 140 acres in 2025, a scale that justifies investment in shared seed-treatment infrastructure. The country's regulatory environment is less restrictive than that of the United States, with faster approval timelines for new active ingredients and fewer restrictions on neonicotinoid use. This advantage may erode as Mexico harmonizes its pesticide regulations with those of the United States under the United States-Mexico-Canada Agreement.

Canada remains a minor contributor, with cotton acreage limited to experimental plots and niche organic production in British Columbia, though the country's seed-treatment expertise in canola and wheat is creating technology spillovers that could benefit cotton if climate warming expands the crop's viable growing range northward. The Central American countries and Caribbean islands holds significant share in Guatemala and Honduras following years of decline due to pest pressure and low commodity prices. These markets favor low-cost generic insecticides and fungicides over premium biological formulations, though sustainability mandates from European textile importers are beginning to shift demand toward residue-free production systems.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The North America cotton seed treatment market exhibits high concentration, with the top five players including Bayer AG, Syngenta AG, Corteva Agriscience LLC, BASF SE, and FMC Corporation holding significant combined share in 2024, a structure that reflects the capital intensity of biological-strain development, polymer-coating patents, and multi-year supply agreements with seed companies. Bayer, Syngenta, and Corteva dominate through integrated portfolios that span insecticides, fungicides, and biological inoculants, enabling them to offer bundled solutions that lock in grower loyalty and create switching costs for competitors.

Smaller formulators such as Vive Crop Protection and Albaugh are competing on price in the generic insecticide segment, where patent expirations on key neonicotinoids and diamides have opened the market to lower-cost alternatives, though these players lack the R&D budgets to develop proprietary biological strains or advanced polymer coatings. Technology is reshaping competitive dynamics, with firms investing in precision-coating equipment that uses machine vision and real-time feedback to ensure uniform active-ingredient distribution and reduce waste by 10 to 15% compared to conventional batch treaters.

Strategy patterns emphasize vertical integration, with leading firms acquiring fermentation-capacity providers and polymer-technology specialists to secure supply chains and capture margin at multiple value-chain stages. Opportunities are emerging in combination products that pair nematicides with plant-growth regulators, a category that remains underpenetrated despite field trials showing 8 to 12% yield gains when root protection is combined with hormonal optimization of canopy architecture.

North America Cotton Seed Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Syngenta received Environmental Protection Agency (EPA) registration for Tymirium technology, a novel seed-treatment fungicide combining mefentrifluconazole with a biological elicitor, targeting Rhizoctonia and Fusarium seedling diseases in cotton. The product is positioned as a premium alternative to generic metalaxyl formulations and projected to launched commercially in the United States Southeast for the 2026 planting season.

- February 2025: Syngenta AG and Ginkgo Bioworks collaborated to develop a new biological solution. Through this partnership, Ginkgo Bioworks developed and optimized a microbial strain to achieve productivity targets for a secondary metabolite from Syngenta Biologicals' pipeline.

- July 2023: Bayer introduced ThryvOn Technology for commercial use in the United States, a cotton biotech trait system that offers integrated pest protection. The technology provides inherent defense against tarnished plant bugs and thrips species, potentially reducing the need for insecticide applications.

Table of Contents for North America Cotton Seed Treatment Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1High cost benefit ratio versus soil and foliar spraying

- 4.2.2Surging insecticide resistance in pink bollworm and plant bug populations

- 4.2.3Tightening worker-safety rules on aerial pesticide use

- 4.2.4Rapid shift toward biological seed protectants

- 4.2.5Plant-back interval waivers boosting pre-season adoption

- 4.2.6Edge-of-field water-quality credits for treated seeds

- 4.3Market Restraints

- 4.3.1Low adoption among small growers lacking on-farm application equipment

- 4.3.2Perception that stacked Genetically Modified traits reduce need for seed treatments

- 4.3.3Regulatory scrutiny on neonicotinoid dust-off issues

- 4.3.4Supply-chain price spikes in biological actives

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Bargaining Power of Suppliers

- 4.6.2Bargaining Power of Buyers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Chemical Origin

- 5.1.1Synthetic

- 5.1.2Biological

- 5.2By Product Type

- 5.2.1Insecticides

- 5.2.2Fungicides

- 5.2.3Other Product Types

- 5.3By Geography

- 5.3.1United States

- 5.3.2Canada

- 5.3.3Mexico

- 5.3.4Rest of North America

6. COMPETITIVE LANDSCAPE

- 6.1Strategic Moves

- 6.2Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1Bayer CropScience AG

- 6.3.2Syngenta AG

- 6.3.3Corteva Agriscience LLC

- 6.3.4BASF SE

- 6.3.5FMC Corporation

- 6.3.6UPL Limited

- 6.3.7Sumitomo Chemical America Inc.

- 6.3.8Nufarm Ltd.

- 6.3.9Albaugh LLC

- 6.3.10Helena Agri-Enterprises LLC

- 6.3.11Vive Crop Protection Inc.

- 6.3.12Verdesian Life Sciences LLC

- 6.3.13Indigo Ag, Inc.

- 6.3.14Incotec Corporation

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

North America Cotton Seed Treatment Market Report Scope

Seed treatment products are biological, physical, and chemical agents and techniques applied to seeds to protect and improve the establishment of healthy crops. The North America cottonseed market is segmented by Chemical Type (Synthetic, Biological), Product Type (Insecticide, Fungicide, Nematicide, and Other Product Types), and Geography (United States, Canada, Mexico, and the Rest of North America). The report offers market size and forecasts in value (USD) for all the above segments.