North America Bariatric Surgery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 1.11 Billion |

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Bariatric Surgery Devices Market Analysis by Mordor Intelligence

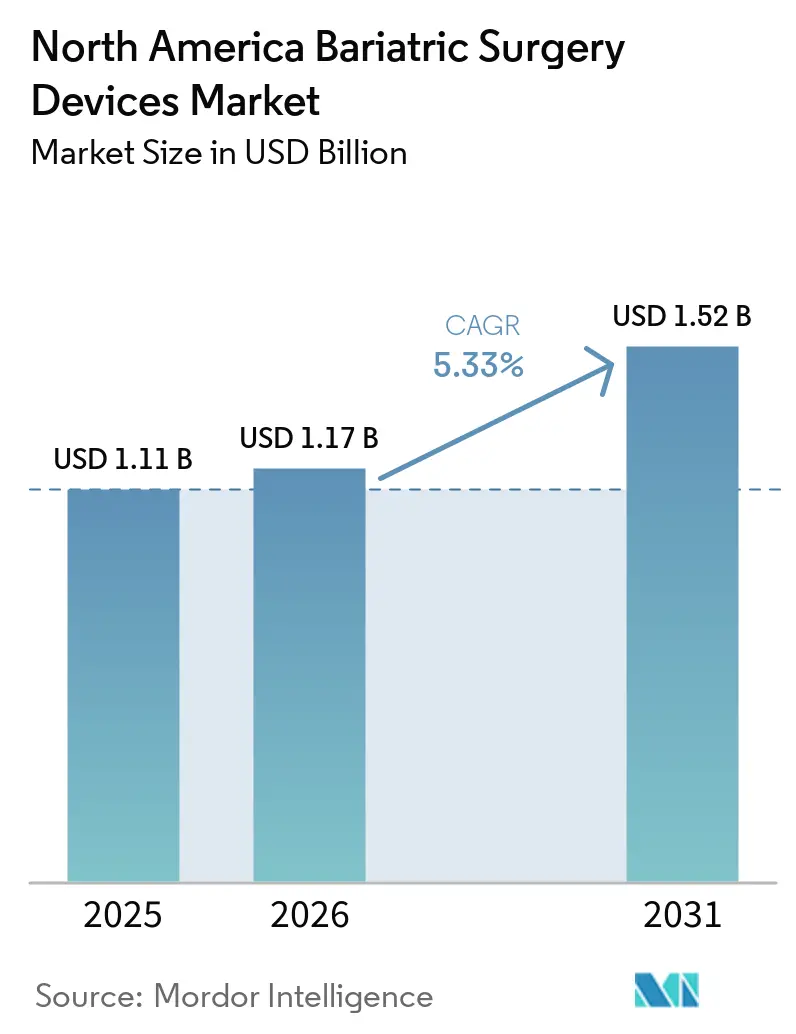

The North America Bariatric Surgery Devices Market size is expected to grow from USD 1.11 billion in 2025 to USD 1.17 billion in 2026 and is forecast to reach USD 1.52 billion by 2031 at 5.33% CAGR over 2026-2031.

Sleeve gastrectomy keeps bariatric volumes resilient even as GLP-1 drugs gain traction, while rapid uptake of robotic platforms supports device revenues. Parallel growth in adolescent approvals, employer subsidies, and AI-guided instrumentation strengthens procedure pipelines. Hospitals still perform most operations, yet outpatient migration boosts ambulatory surgical center (ASC) activity. Persistent workforce shortages and high capital-equipment costs temper overall momentum, but favorable long-term cardiovascular data maintains strong clinical endorsement for surgery.

Key Report Takeaways

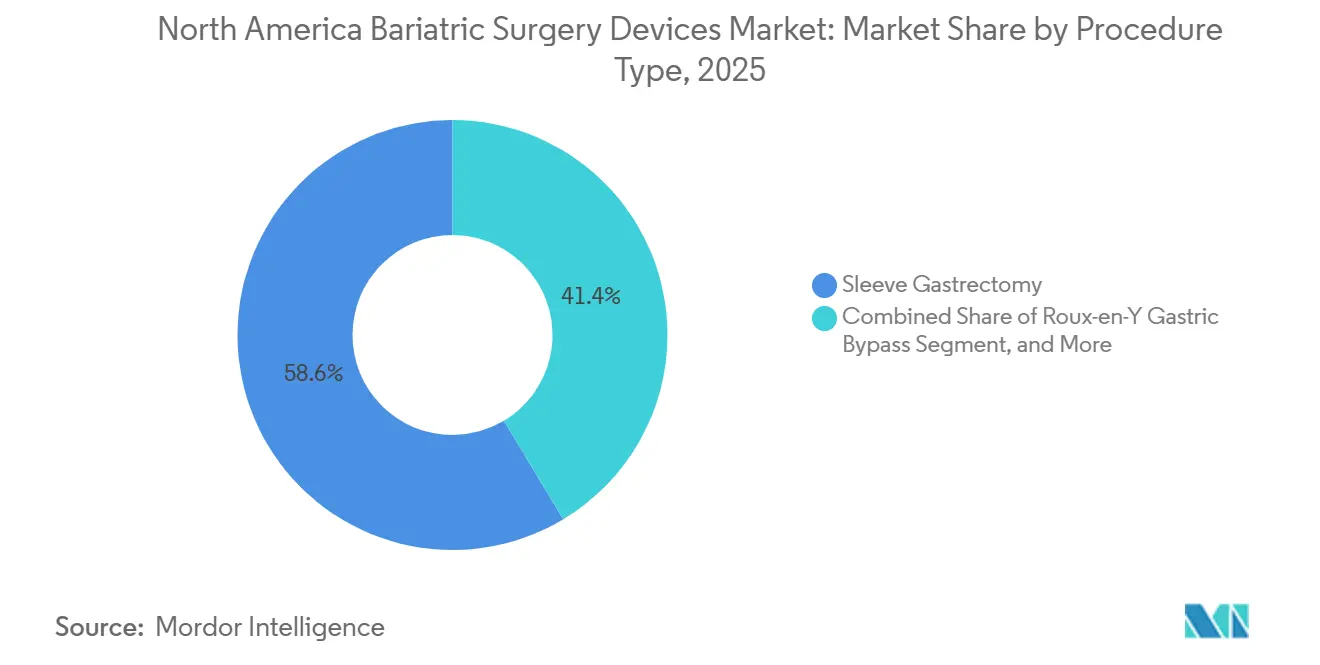

- By procedure type, sleeve gastrectomy led with 58.62% of the North America bariatric surgery devices market share in 2025. Intragastric balloons are projected to command the fastest 5.63% CAGR through 2031 within the procedure portfolio.

- By device type, assisting devices accounted for 65.72% share of the North America bariatric surgery devices market size in 2025. Implantable devices are advancing at a 5.88% CAGR between 2026 and 2031.

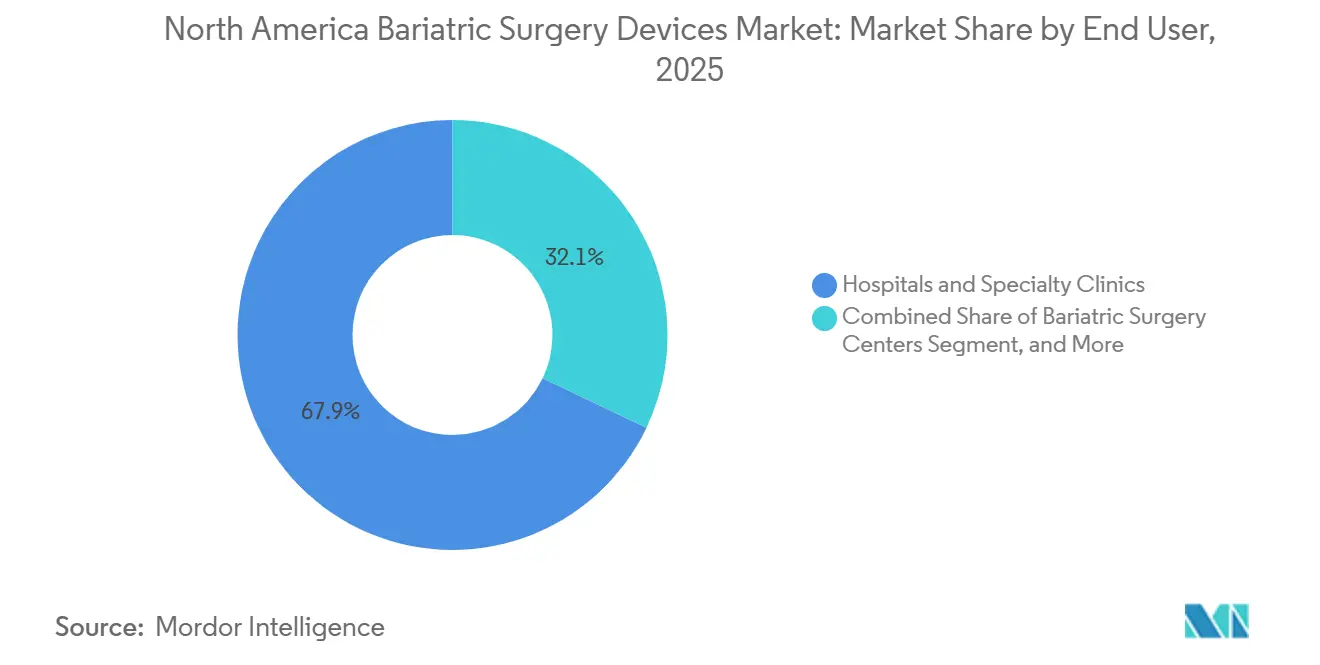

- By end user, hospitals and specialty clinics held 67.95% of total revenue in 2025, whereas ASCs recorded the highest 5.72% CAGR outlook.

- By country, the United States captured 91.84% of regional revenue in 2025 and is forecast to expand at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Bariatric Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in adolescent obesity surgery approvals | +1.2% | United States, with spillover to Canada | Medium term (2-4 years) |

| Wider reimbursement for robotic bariatric procedures | +0.8% | United States primarily, limited Canada coverage | Short term (≤ 2 years) |

| Growing medical tourism flows for metabolic surgery | +0.6% | US-Mexico border regions, concentrated in Tijuana | Long term (≥ 4 years) |

| Entry of AI-guided stapling & suturing systems | +0.9% | North America, led by high-volume centers | Medium term (2-4 years) |

| Corporate wellness programs subsidising surgery costs | +0.7% | United States corporate sector | Short term (≤ 2 years) |

| Long-term cardiovascular outcome data boosting clinical acceptance | +1.1% | North America, with stronger impact in US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Adolescent Obesity Surgery Approvals

FDA clearance of Wegovy for 12-to-17-year-olds, coupled with 2023 pediatric guidelines, has raised adolescent surgical volumes by 15% between 2021 and 2023.[1]U.S. Food and Drug Administration, “FDA Approves New Indication for Weight Management Drug in Pediatric Patients,” FDA.GOV Teen-targeted data showing sustained 20% BMI reduction over 10 years cements early intervention as a credible path. Sleeve gastrectomy represents 86% of these cases because its single-anastomosis technique yields lower leak risk and shorter operative times. Insurers increasingly treat severe adolescent obesity as a metabolic disease rather than a lifestyle issue, widening coverage. Early surgery extends lifetime comorbidity savings, counterbalancing adult volumes eroded by GLP-1 usage.

Wider Reimbursement for Robotic Bariatric Procedures

Medicare’s 2025 payment of USD 19,458 for complex bariatric cases incentivizes robotic adoption that minimizes complications.[2]Centers for Medicare & Medicaid Services, “CY 2025 Medicare Hospital Outpatient Prospective Payment System Final Rule,” CMS.GOV Robots already assist 30% of regional bariatric operations, and eight-year registry data indicate lower revisional morbidity than laparoscopy. Commercial plans are dropping pre-authorizations at accredited centers, accelerating hospital capital-budget approvals despite inflation. Robotic staplers such as SureForm deliver 100% firing accuracy, reducing leak litigation exposure and validating premium device outlays.

Growing Medical Tourism Flows for Metabolic Surgery

Tijuana facilities offering accredited packages at up to 70% cost savings attract U.S. self-pay patients. Employer wellness benefits sometimes include travel stipends, creating a structured pipeline that offsets domestic capacity bottlenecks. Joint Commission International accreditation among Mexican centers further legitimizes cross-border care.

Entry of AI-Guided Stapling & Suturing Systems

Real-time tissue analytics embedded in robotic platforms standardize staple-line creation and forecast leak risk. Early adopters report steeper learning-curve compression for new surgeons, partially alleviating the predicted 10,000-surgeon shortfall by 2036. As algorithms mature, vendors bundle AI software with hardware, shifting revenue models toward recurring analytics fees and locking in long-term customer relationships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uptake of GLP-1 drugs delaying surgery decisions | -1.8% | United States primarily, limited Canada impact | Short term (≤ 2 years) |

| Shortage of bariatric-trained surgical workforce | -0.9% | North America, acute in rural areas | Long term (≥ 4 years) |

| High device cost amid inflation-driven cap-ex freezes | -0.6% | United States and Canada healthcare systems | Medium term (2-4 years) |

| Litigation risk over staple line leaks | -0.4% | United States legal environment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uptake of GLP-1 Drugs Delaying Surgery Decisions

GLP-1 prescriptions rose 132.6% from 2022-2023, coinciding with a 25.6% fall in surgeries among non-diabetic patients. Planned Medicare coverage for obesity drugs in 2026 may deepen deferrals. Nonetheless, concerns about lifelong drug cost and variable weight maintenance preserve a sizable surgical pipeline.

Shortage of Bariatric-Trained Surgical Workforce

One-quarter of practicing surgeons are over 65, threatening a supply gap even as demand rises. Accreditation requires minimum annual volumes that some rural surgeons cannot achieve, concentrating expertise in urban centers and lengthening wait times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Sleeve Gastrectomy Dominance Amid Balloon Innovation

Sleeve gastrectomy captured 58.62% of 2025 revenue, representing the largest slice of the North America bariatric surgery devices market. Intragastric balloons, while accounting for a smaller base, are forecast at a 5.63% CAGR, the swiftest among procedure options. Sleeve popularity stems from single-row staple construction and preserved pyloric function, which lowers nutrient malabsorption concerns. Balloons align with payers favoring stepwise obesity care and with patients desiring reversible options, positioning the modality as an effective bridge to definitive intervention if needed.

Roux-en-Y gastric bypass remains second in volume for severe diabetes owing to superior metabolic outcomes, though complexity limits its growth. Adjustable bands have receded because of high revision rates. Hybrid methods such as SADI-S find traction in super-obese cohorts. Endoscopic sleeve gastroplasty blurs the medical-surgical divide, yet long-term durability evidence is still maturing.

By Device Type: Assisting Devices Lead While Implantables Accelerate

Assisting devices held 65.72% of the North America bariatric surgery devices market size in 2025, safeguarded by their necessity in every minimally invasive case. Continued refinement of staplers and energy platforms attracts premium pricing that hospitals justify through reduced leak and bleed rates. AI-enabled firing logic exemplifies device-driven outcome gains.

Implantable devices grow at 5.88% CAGR as swallowable balloons and neuromodulation systems expand the candidate pool. The Allurion Balloon’s procedure-less design lowers facility needs and improves patient throughput. Gastric electrical stimulators investigating satiety induction present future upside, provided long-term efficacy materializes.

By End User: Hospital Dominance Challenged by ASC Growth

Hospitals and specialty clinics delivered 67.95% of sector revenue in 2025 owing to comprehensive infrastructure and payer mandates that steer complex cases to accredited centers. Despite this dominance, ASCs are scaling at a 5.72% CAGR, enabled by enhanced-recovery protocols that discharge sleeve patients the same day. Physician ownership models and lower overhead improve cost competitiveness.

ASC capacity is most suited to sleeves, which now compose 86% of outpatient bariatric volumes. Larger systems deploy hub-and-spoke models where high-risk candidates remain inpatient while qualifying patients shift to ASC satellites, balancing cost with safety. Dedicated bariatric centers leverage concierge service and bundled self-pay packages, covering a niche yet profitable segment.

Geography Analysis

The United States commanded 91.84% of 2025 revenue in the North America bariatric surgery devices market and is on track for a 6.05% CAGR through 2031. ASC proliferation, employer subsidies, and widening adolescent indications underpin momentum. Medicare’s prospective drug-and-surgery combination policies could expand candidacy by optimizing pre-operative weight loss, ultimately supporting both modalities.

Canada contributes a smaller share but operates a publicly funded, highly standardized network of 11 centers in Ontario, British Columbia, and Quebec. Wait times average 9-12 months, encouraging some private-pay outflow to U.S. or Mexican facilities. Federal and provincial bodies continue to evaluate robotic funding frameworks, which could close technology gaps with American peers and bolster local capacity.

Mexico’s influence arises chiefly from inbound U.S. medical tourists. Accredited Tijuana clinics market cost-effective packages that include postoperative telehealth with U.S. dietitians. The Mexican peso differential and shorter insurer approval cycles sustain cross-border flow. Joint-venture discussions between Mexican providers and U.S. ASCs aim to institutionalize referral pathways and broaden payer acceptance.

Competitive Landscape

The North America bariatric surgery devices market exhibits moderate concentration. Medtronic, Johnson & Johnson (Ethicon), and Boston Scientific collectively represent more than half of annual device placements, leveraging scale, service contracts, and broad portfolios. Intuitive Surgical’s da Vinci platform anchors 30% of procedures, forcing rivals to develop robot-compatible instrumentation or pursue alliances. KARL STORZ’s 2024 acquisition of Asensus Surgical adds the forthcoming LUNA system to its lineup, intensifying robotic competition.

Disruptors target less invasive niches. Allurion Technologies promotes a swallowable balloon that bypasses endoscopy requirements, though recent revenue slippage highlights commercialization challenges. Fractyl Health’s Revita procedure seeks post-GLP-1 weight-maintenance coverage and could create a synergistic surgical-endoscopic continuum. Device makers increasingly embed AI analytics that turn staplers and sealers into data generators, shifting value toward software and postoperative decision support.

Hospital groups negotiate multi-year, volume-based contracts that bundle capital equipment, consumables, and service training, fortifying incumbent positions. Yet ASCs’ rise empowers surgeons to influence purchasing, fostering small-volume opportunities for emerging vendors with differentiated economics. Overall, innovation centers on reducing complications to shield providers from litigation and to justify premium reimbursements in a value-based landscape.

North America Bariatric Surgery Devices Industry Leaders

Medtronic

Olympus Corporation

Conmed Corporation

B. Braun SE

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Olympus received FDA 510(k) clearance for the POWERSEAL Open Extended Jaw Sealer/Divider. This expands the advanced 5mm sealing and dividing portfolio indicated for use in bariatric surgery.

- June 2025: Fractyl Health and Bariendo signed a letter of intent to scale the Revita endoscopic procedure nationally.

- April 2025: Nitinotes announced upcoming clinical presentations of the EndoZip system at ESGE Days 2025.

North America Bariatric Surgery Devices Market Report Scope

As per the scope of the report, bariatric surgery or weight loss surgery is used as one of the major treatment procedures for treating obesity. It is generally the last option for patients who have failed in an attempt to lose weight by several other means. During this procedure, the size of the stomach is reduced by either removing some parts of the stomach or using a gastric band.

The North America bariatric surgery devices market is segmented by procedure type, device type, patient age group, and country. By procedure type, the market is segmented into sleeve gastrectomy, Roux-en-Y gastric bypass, adjustable gastric banding, biliopancreatic diversion with duodenal switch, one anastomosis gastric bypass, endoscopic sleeve gastroplasty, and other procedures. By device type, the market is segmented into assisting devices and implantable devices. By end user, the market is segmented into hospitals & specialty clinics, bariatric surgery centers, ambulatory surgical centers, and others. By patient age group, the market is segmented into adolescents, adults, and geriatrics. By country, the market is segmented into United States, Canada, and Mexico. The report offers the value (in USD million) for the above segments.

| Sleeve Gastrectomy |

| Roux-en-Y Gastric Bypass |

| Adjustable Gastric Banding |

| Biliopancreatic Diversion with Duodenal Switch |

| One Anastomosis Gastric Bypass |

| Endoscopic Sleeve Gastroplasty |

| Other Procedures |

| Assisting Devices | Suturing Device |

| Closure Device | |

| Stapling Device | |

| Trocars | |

| Other Assisting Devices | |

| Implantable Devices | Gastric Bands |

| Electrical Stimulation Devices | |

| Gastric Balloons | |

| Gastric Emptying | |

| Other Devices |

| Hospitals & Specialty Clinics |

| Bariatric Surgery Centers |

| Ambulatory Surgical Centers |

| Others |

| Adolescents (12–17) |

| Adults (18–64) |

| Geriatric (≥65) |

| United States |

| Canada |

| Mexico |

| By Procedure Type | Sleeve Gastrectomy | |

| Roux-en-Y Gastric Bypass | ||

| Adjustable Gastric Banding | ||

| Biliopancreatic Diversion with Duodenal Switch | ||

| One Anastomosis Gastric Bypass | ||

| Endoscopic Sleeve Gastroplasty | ||

| Other Procedures | ||

| By Device Type | Assisting Devices | Suturing Device |

| Closure Device | ||

| Stapling Device | ||

| Trocars | ||

| Other Assisting Devices | ||

| Implantable Devices | Gastric Bands | |

| Electrical Stimulation Devices | ||

| Gastric Balloons | ||

| Gastric Emptying | ||

| Other Devices | ||

| By End User | Hospitals & Specialty Clinics | |

| Bariatric Surgery Centers | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Patient Age Group | Adolescents (12–17) | |

| Adults (18–64) | ||

| Geriatric (≥65) | ||

| Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the market value of the North America bariatric surgery devices market in 2031?

The North America bariatric surgery devices market size is forecast to reach USD 1.52 billion by 2031.

Which procedure currently accounts for the most surgeries across the region?

Sleeve gastrectomy leads with 58.62% of 2025 revenue.

How quickly is the outpatient setting expanding for bariatric operations?

Ambulatory surgical centers are projected to grow at a 5.72% CAGR through 2031.

How have GLP-1 drugs affected surgical volumes?

Rapid GLP-1 adoption has delayed some surgeries, trimming non-diabetic volumes by 25.6% in 2023.

Which technology trend is shaping recent device purchases?

Robotic and AI-guided stapling systems dominate capital investment because they cut complication rates and litigation risk.

Page last updated on: