Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

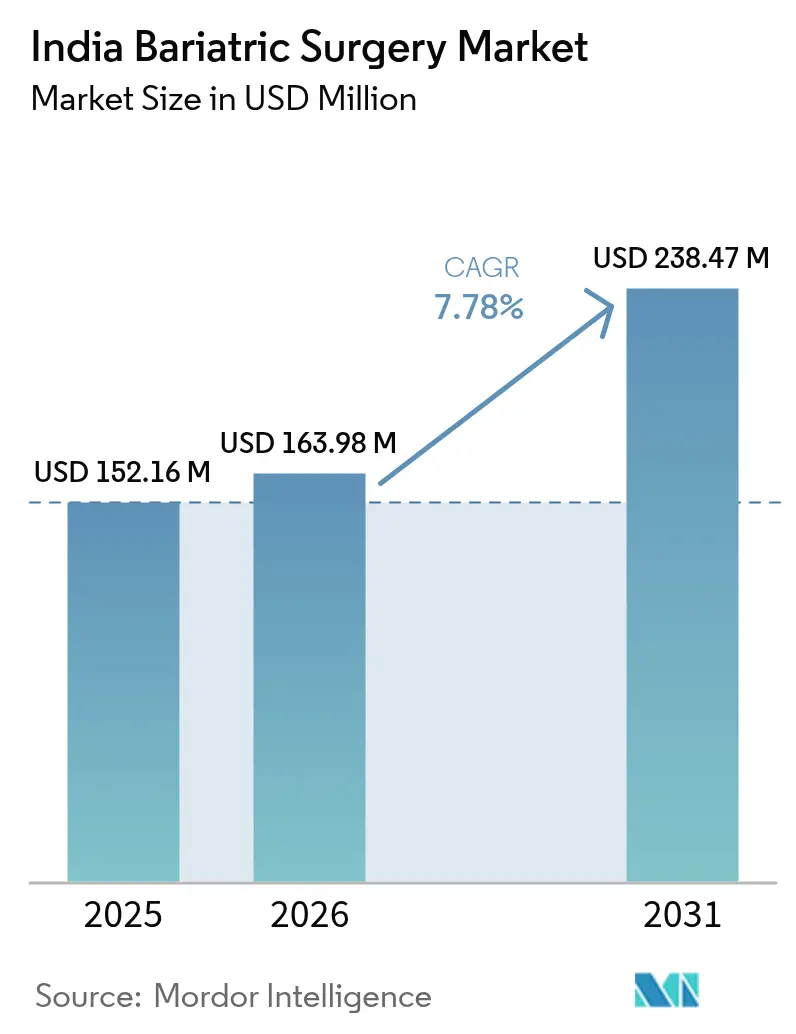

| Base Year Market Size (2025) | USD 152.16 Million |

| Market Size (2026) | USD 163.98 Million |

| Market Size (2031) | USD 238.47 Million |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

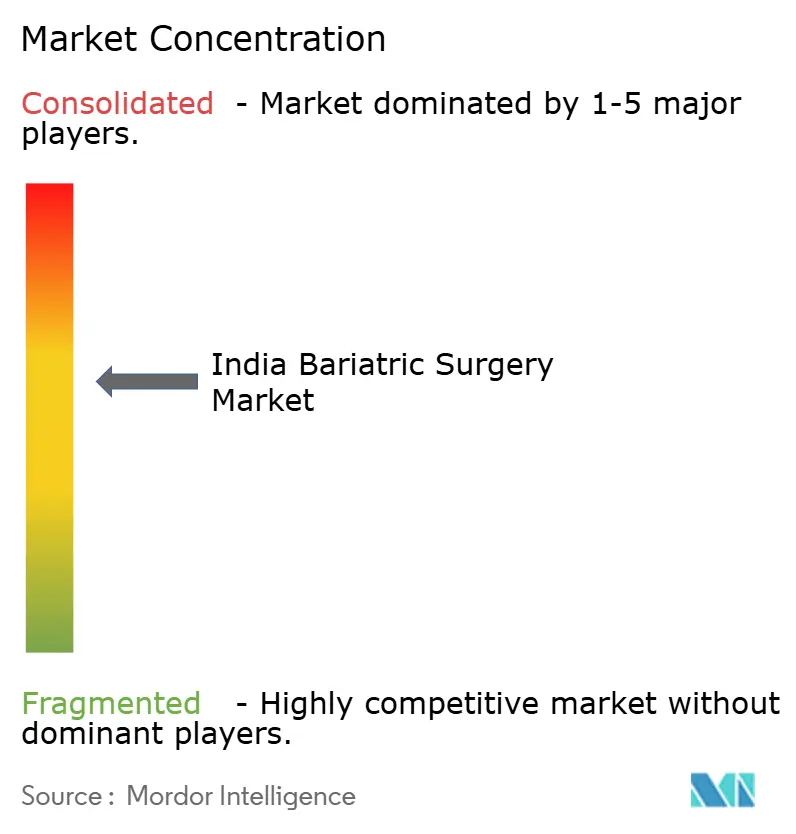

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Bariatric Surgery Market Analysis by Mordor Intelligence

The India bariatric surgery market size was valued at USD 152.16 million in 2025 and estimated to grow from USD 163.98 million in 2026 to reach USD 238.47 million by 2031, at a CAGR of 7.78% during the forecast period (2026-2031). India’s escalating obesity prevalence, rising to 28.6% in large metros, and the parallel surge in Type-2 diabetes are sustaining a stable pipeline of eligible patients. Expanding private-sector medical insurance, led by ICICI Lombard, Star Health, and HDFC ERGO, now reimburses 60-70% of bariatric costs, elevating affordability. Indigenous innovation in low-cost laparoscopic staplers, plus structured surgeon training, cuts capital outlays for hospitals and encourages Tier-2 market penetration. Further momentum comes from medical tourists favoring Tier-2 hubs such as Pune, Ahmedabad, and Kochi, attracted by 40-50% cost savings over Tier-1 cities.

Key Report Takeaways

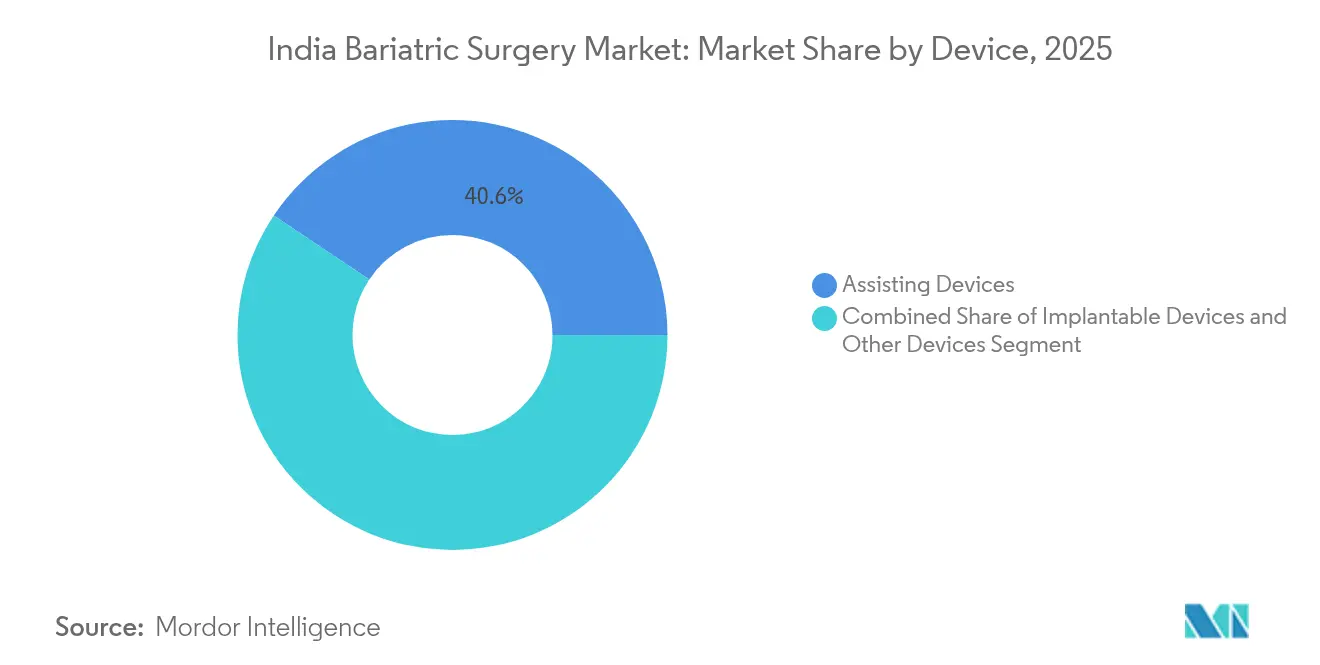

- By device, assisting devices captured 40.62% of the India bariatric surgery market share in 2025. Implantable Devices are projected to record a 8.97% CAGR between 2026-2031.

- By procedure type, restrictive procedures led with 54.02% revenue share in 2025, while endoscopic bariatric therapies are forecast to grow at an 8.18% CAGR through 2031.

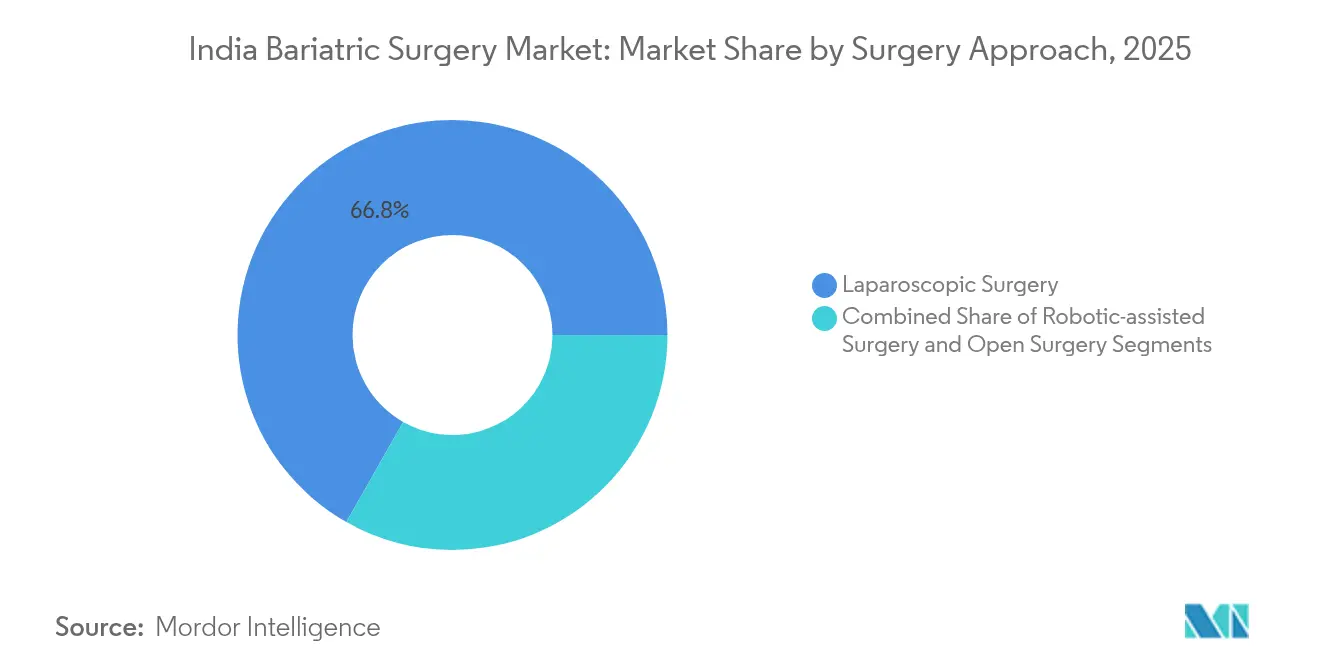

- By surgical approach, laparoscopic techniques accounted for 66.78% of the Indian bariatric surgery market size in 2025, whereas Robotic-assisted surgery is expected to progress at an 8.55% CAGR to 2031.

- By end user, multi-specialty hospitals commanded a 35.02% share of the India bariatric surgery market size in 2025; bariatric surgery centers are expected to expand at a 9.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Bariatric Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban obesity prevalence | +2.8% | Metro & growing Tier-2 cities | Medium term (2-4 years) |

| Rising Type-2 diabetes & cardiovascular risk | +2.1% | Urban & semi-urban India | Long term (≥4 years) |

| Broader insurance coverage | +1.7% | National (early uptake in Mumbai, Delhi, Bangalore) | Short term (≤2 years) |

| Medical-tourism inflows to Tier-2 hubs | +1.2% | Pune, Ahmedabad, Kochi, Hyderabad | Medium term (2-4 years) |

| Indigenous low-cost laparoscopic staplers | +0.4% | Manufacturing hubs in Gujarat & Tamil Nadu | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Obesity Prevalence in Urban India

Urban adults aged 20-39 show obesity levels surpassing 32% in Delhi NCR, creating sustained demand for metabolic surgery. Employers in technology clusters such as Bengaluru, Hyderabad, and Pune increasingly finance bariatric procedures to curb productivity losses. Desk-bound lifestyles accelerated after COVID-19 generate heavier patient backlogs, especially among younger professionals. Wellness policies by Tata Consultancy Services and Infosys reimburse surgery when medical necessity is documented. These corporate benefits cultivate hospital-employer partnerships that funnel insured patients directly to accredited surgical centers.

Increasing Prevalence of Type-2 Diabetes & Cardiovascular Co-morbidities

India recorded 77.2 million Type-2 diabetics in 2024; 65% also meet obesity criteria. The Indian Council of Medical Research now endorses bariatric surgery for BMI > 32.5 kg/m², immediately adding 15 million potential candidates[1]Indian Council of Medical Research, “Consensus Statement on Bariatric Surgery for Type-2 Diabetes,” icmr.gov.in. Sleeve gastrectomy achieves 78% diabetes remission within one year, persuading endocrinologists to refer earlier. Cardiologists observe coronary events in 42% of untreated obese diabetics within five years, reinforcing surgical urgency. Inter-specialty referral boards in leading hospitals standardize patient screening to accelerate procedure volumes.

Expanding Insurance Coverage for Bariatric Procedures

Since 2024, ICICI Lombard, Star Health, and HDFC ERGO reimburse bariatric surgery when BMI and co-morbidity thresholds are met, slashing patient expenditure from USD 4,000-6,000 to USD 1,200-2,000. Ayushman Bharat pilots in Uttar Pradesh and Gujarat could extend eligibility to 500 million residents. Corporate group policies by Wipro and HCL Technologies mirror this shift, widening the insured pool across Tier-2 cities where disposable income is lower but disease burden is high. Streamlined pre-authorization processes reduce wait-times, enabling quicker surgical scheduling.

Surge in Medical Tourism for Metabolic Surgery in Tier-2 Cities

International patients now constitute up to 30% of bariatric volumes at centers in Pune, Ahmedabad, and Kochi[2]Ministry of Tourism, “Medical Tourism in Tier-2 Cities,” tourism.gov.in. Direct flights from Dubai, Singapore, and Colombo cut travel time, while package pricing remains 40-50% below Tier-1 hospitals. Apollo Hospitals in Ahmedabad and Fortis Mohali actively market bundled robotic-surgery packages, exploiting lesser visa processing hurdles. Local governments grant medical visas within 48 hours, encouraging companion travel and extended stay, which boosts ancillary spending on hotels and local transport.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost | -1.8% | National, more pronounced in Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Limited awareness among obese population | -1.2% | Rural and semi-urban areas, lower socioeconomic segments | Long term (≥4 years) |

| Poor post-operative follow-up adherence | -0.8% | National, with larger gaps where continuity of care is limited | Long term (≥4 years) |

| Supply-chain disruptions for CO₂ insufflation cartridges | -0.6% | Nationwide, especially in import-dependent hospital networks | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost

Average bariatric surgery billing remains USD 4,000-6,000, exceeding annual household income for 70% of eligible patients. Device expenditures constitute one-third of the bill, hospital overheads another 40-45%. Although NBFCs such as Bajaj Finserv offer 12-36-month zero-interest EMIs, uptake captures only 15% of cases. Insurance deductibles and waiting periods prolong decision cycles. Progressive price cuts from domestic stapler makers alleviate part of the burden but do not yet offset premium robotic-system fees at leading centers.

Limited Awareness among Obese Population

Just 23% of obese Indians recognize bariatric surgery as a viable intervention. Rural health workers rarely discuss metabolic surgery; stigma persists around “weight-loss operations.” Language barriers hamper digital outreach, with few vernacular explanations of eligibility. Primary-care doctors seldom refer before secondary complications arise, limiting early intervention. Health-tech platforms Practo and 1mg run targeted campaigns, but geographic reach is skewed toward major cities, delaying uptake in peripheral districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device: Assisting Devices Drive Current Demand

Assisting Devices held 40.62% of 2025 revenue, anchored by widespread use of laparoscopic staplers and energy platforms in restrictive procedures. This segment benefits from high procedure counts and disposable device demand cycles, ensuring recurring sales to hospitals. The India Bariatric Surgery market size for assisting solutions is projected to climb at 7.12% CAGR as Tier-2 facilities adopt standardized kits. Johnson & Johnson’s Ethicon retains leadership, yet Meril’s local staplers priced 30% lower build share within public hospitals. Import reliance for CO₂ insufflators exposes supply chains to currency volatility, stimulating interest in domestic alternatives.

Implantable Devices represent the fastest-growing category, with a 8.97% CAGR, fueled by reversible gastric bands and next-generation intragastric balloons. Younger patients favor adjustable solutions, deferring irreversible resections. Medtronic’s banding systems dominate but balloon introductions, including Boston Scientific’s Orbera365, accelerate adoption among BMI 30-35 cohorts following CDSCO clearance. The India Bariatric Surgery market share differential between assisting and implantable products will narrow as payers reimburse less invasive implants under updated coverage tables.

Second-line devices, notably single-use energy scalpels, enjoy rising preference due to infection-control mandates. Disposable harmonic devices manufactured domestically under ISO 13485 promise cost savings, though clinical committees weigh reuse protocols to moderate consumable spend. Hospitals that negotiate bulk long-term contracts secure 15-20% discounts, improving margin capture in package pricing.

By Procedure Type: Restrictive Procedures Dominate Market

Restrictive Procedures accounted for 54.02% of all Indian bariatric cases in 2025, with sleeve gastrectomy alone comprising 70% of activity. Sleeve resection’s shorter operative time and 2-3-day discharge profile resonate with high-volume centers. Cumulative improvements in staple-line reinforcement have trimmed leak rates below 1.5%, reinforcing surgeon confidence. The India Bariatric Surgery market size linked to restrictive methods is forecast to advance at 7.74% CAGR through 2031, aligning with continued insurance acceptance.

Endoscopic Bariatric Therapies register an 8.18% CAGR, catalyzed by Orbera balloon approvals and early adoption of endoscopic sleeve gastroplasty. These minimally invasive options target patients previously hesitant about surgery, enabling ambulatory treatment with same-day discharge. Device makers collaborate with gastroenterology societies to expand accredited training, broadening the practitioner pool. Hospitals differentiate via bundled wellness services, including dietetic counseling, to capture ancillary revenue.

Mal-absorptive techniques, notably BPD/DS, persist in specialized university hospitals because of higher nutritional follow-up demands. Roux-en-Y gastric bypass—straddling restrictive and mal-absorptive attributes—secures diabetic remission in over 80% of Indian patients, steering referrals from endocrinologists. Yet long-term vitamin supplementation protocols temper its volume share.

By Surgery Approach: Laparoscopic Leadership with Robotic Growth

Laparoscopy remains the dominant approach, capturing 66.78% of 2025 procedure volumes due to mature surgeon proficiency and abundant training programs from the Association of Surgeons of India. The India Bariatric Surgery market size tied to laparoscopic kits will continue to rise, albeit at a tempered 6.55% CAGR as conversion to robotic systems gathers pace.

Robotic-assisted surgery is the fastest-growing modality, posting an 8.55% CAGR through 2031. Forty-five da Vinci systems are operational nationwide, mostly in Tier-1 private hospitals pursuing differentiation with overseas payers. Intuitive Surgical’s training alliance with Apollo Hospitals targets 200 surgeon certifications annually. Despite procedure costs 40-50% higher than laparoscopy, data on lower wound infection rates and faster ambulation sway affluent domestic and foreign patients. Government-run tertiary centers in Delhi and Chandigarh have acquired dual-console robots to democratize exposure among surgical residents.

Open surgery usage dwindles, confined to complex revisions and high-risk adhesions. Device vendors no longer prioritize product development for open kits, pivoting R&D resources toward smart staplers compatible with robotic arms. Regulators mandate credentialing for robotic console operators, compelling structured proctoring and minimizing adverse events.

By End-User: Multi-specialty Hospitals Lead Market

Multi-specialty Hospitals supplied 35.02% of device demand in 2025, leveraging integrated ICUs, endocrinology clinics, and radiology. Insurer empanelment favors these large systems because of established risk-management protocols. Package deals with medical-tourism facilitators funnel overseas patients to their robotic suites, boosting higher-margin device consumption.

Bariatric Surgery Centers, often single-specialty facilities, will record the segment-best 9.18% CAGR, propelled by growing prevalence in Tier-2 cities. These centers capitalize on lean staffing structures, allowing 20-30% lower procedure tariffs than metropolitan hospitals. Dedicated marketing emphasizes shorter wait-times and surgeon continuity of care. Accreditation by the National Board for Bariatric Surgery, launched in 2025, will formalize quality standards and amplify patient trust.

Ambulatory Surgical Centers (ASCs) emerge as cost-efficient venues for balloon placements and endoscopic sleeve gastroplasty. Same-day discharge protocols slash bed costs, and simplified credentialing expedites ramp-up in suburban catchments. Device makers bundle endoscopic kits with service contracts tailored to ASC cash-flow constraints, fostering wider adoption.

Regulatory Landscape

Bariatric surgery devices in India are regulated by the Central Drugs Standard Control Organization (CDSCO) under the Drugs and Cosmetics Act, 1940 and the Medical Devices Rules, 2017 (MDR-2017). Device makers supplying bariatric and metabolic procedures must align product licensing to India risk classification (including higher-risk implantables and certain endoluminal/implantable systems), along with quality management requirements and applicable compliance documentation used in CDSCO pathways.

In April 2026, the Ministry of Health and Family Welfare (MoHFW) published draft Medical Devices (Amendment) Rules, 2026 (G.S.R. 270(E)), which included proposals around fee transparency and strengthened sterilization traceability. Separately, MoHFW proposals in 2026 to reduce certain licensing timelines under MDR-2017 (including for Class C and D devices) add a tangible operational lever for manufacturers and importers of high-risk bariatric-related devices seeking faster market access. Clinical practice alignment in bariatric/metabolic care continues to be shaped by Indian professional guidance, including OSSI and the Endocrine Society of India, influencing credentialing norms and procedure adoption within hospitals.

Value Chain Analysis

The value chain spans raw materials and precision components (metals, polymers, coatings), finished-device manufacturing and assembly (including stapling systems, energy platforms, trocars, and endoscopic tools), sterilization and packaging, and then multi-tier distribution to hospitals and specialty centers. On the demand side, multi-specialty hospital systems and bariatric surgery centers act as the primary procurement hubs, typically bundling devices into standardized procedure kits; OEM service capability (for endoscopic/robotic ecosystems and energy platforms) remains a key differentiator in tendering and long-term contracting.

Regulatory and compliance steps under MDR-2017 (CDSCO oversight for higher-risk devices, State Licensing Authorities for lower-risk categories) sit directly on the critical path for time-to-revenue, and hospital credentialing requirements further influence which technologies become routinized. India-focused localization programs, including the Production Linked Incentive (PLI) scheme and the development of Medical Device Parks (such as the YEIDA-linked park), support domestic manufacturing scale-up and reduce dependency on imports for select medtech categories. In the operating-theatre equipment layer supporting bariatric programs, domestic suppliers such as Galaxy India and Surgident India participate in the ecosystem by supplying infrastructure and surgical equipment used by hospitals running bariatric and metabolic surgery services.

Competitive Landscape

The India Bariatric Surgery market demonstrates moderate concentration: the top five vendors captured 55% revenue in 2024. Medtronic leads implantables, propelled by its gastric band franchise and early physician-education investments. Johnson & Johnson’s Ethicon dominates assisting devices, particularly laparoscopic staplers, through wide hospital outreach and local training labs. Boston Scientific capitalizes on the fastest-growing endoscopic balloon arena, aided by Orbera365’s recent approval.

Indigenous suppliers are narrowing the technology gap. Meril Life Sciences unveiled locally made smart staplers in 2025 after acquiring Germany’s Endocon, trimming production costs and achieving CE certification. Staan Bio-Med Engineering earned ISO 13485 for its Ahmedabad plant, unlocking European exports that augment scale and lower domestic unit costs. These firms compete on price, offering 25–30% savings that resonate with government hospitals and cash-pay patients.

Differentiation pivots on distribution reach and multi-procedure portfolios. Vendors bundling energy devices, staplers, and trocars secure exclusive purchasing contracts with high-volume centers, insulating share against single-product rivals. Meanwhile, Intuitive Surgical leverages its da Vinci install base to lock in proprietary robotic staplers, creating a premium sub-segment. Global majors increasingly localize assembly to avoid import duties—Medtronic’s USD 25 million Pune plant exemplifies this strategy, promising 40% cost savings and shorter lead-times.

Strategic alliances intensify. BD partners with Indian contract manufacturers to assemble trocar seals, ensuring supply continuity amid shipping disruptions. Olympus establishes a Bangalore service hub to guarantee 24-hour device uptime for endoscopic suites, a key criterion in hospital tender evaluations. Cross-licensing agreements around reusable instrument sterilization systems may surface as OEMs seek sustainability credentials and cost efficiencies.

India Bariatric Surgery Industry Leaders

Johnson and Johnson

Medtronic PLC

Conmed Corporation

B. Braun SE

Apollo Endosurgery Inc (Boston Scientific)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity sits in faster availability and broader choice of high-risk bariatric and metabolic devices as the MoHFW moves to streamline MDR-2017 processes, including the June 2026 proposal to reduce license timelines for Class C and D devices from 105 days to 90 days. For manufacturers and distributors, this shifts attention to compliance readiness (technical dossiers, quality systems, and traceability) and to building channel coverage beyond Tier-1 private hospitals, where demand is increasingly linked to structured insurance reimbursement and packaged-care pathways.

Service expansion by hospitals is creating new procedural nodes outside the traditional private metro base, opening whitespace for stapling/energy consumables, endoscopy-based bariatric tools, and post-op follow-up solutions. In February 2026, AIIMS Patna introduced bariatric surgery services, signaling government-institution participation in a large eastern catchment; in the same month, Maharaja Yashwantrao Hospital (MYH) in Madhya Pradesh launched bariatric surgery services positioned around affordability for Ayushman cardholders. Private providers are also investing in program depth and capability, including Noble Hospital and Research Centre launching a dedicated obesity and advanced bariatric sciences center in Pune (March 2026), and CARE Hospitals reporting completion of 100 high-risk bariatric surgeries in super-super obese patients (June 2026), reinforcing demand for advanced laparoscopic/robotic infrastructure, specialized devices, and multidisciplinary peri-operative pathways.

Recent Industry Developments

- June 2026: CARE Hospitals reported completing 100 high-risk bariatric surgeries in super-super obese patients (BMI above 60). The milestone underscores growing clinical confidence in managing complex bariatric cases and supports higher-acuity device demand across stapling, energy, and advanced peri-operative monitoring pathways.

- September 2025: Max Healthcare and Medtronic inaugurated the Max-Medtronic Skill Lab at Max Super Specialty Hospital in Saket, New Delhi to train clinicians in minimally invasive surgical techniques. The facility strengthens surgeon training throughput and supports broader standardization of laparoscopic bariatric workflows that drive recurring consumable usage.

- July 2025: SS Innovations announced completion of a robotic telesurgery for weight loss using its SSi Mantra 3 surgical robotic system. The case expands the visibility of India-origin robotic platforms and highlights how connectivity-enabled surgical capability can influence adoption discussions for robotic-assisted bariatric programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers bariatric surgery care delivered in India, including procedure demand and the related surgical devices that are used to perform and support these interventions across eligible patient groups.

Scope exclusions: Cosmetic weight loss treatments without a bariatric procedure, general fitness programs, and non-surgical diet products are excluded from this market sizing.

Segmentation Overview

- By Device

- Assisting Devices

- Suturing Devices

- Closure Devices

- Stapling Devices

- Other Assisting Devices

- Implantable Devices

- Other Devices

- Assisting Devices

- By Procedure Type

- Restrictive Procedures

- Mal-absorptive Procedures (BPD/DS)

- Combination Procedures (Roux-en-Y Gastric Bypass)

- Endoscopic Bariatric Therapies

- By Surgery Approach

- Laparoscopic Surgery

- Robotic-assisted Surgery

- Open Surgery

- By End-User

- Multi-specialty Hospitals

- Bariatric Surgery Centers

- Ambulatory Surgical Centers

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to pin down India-specific demand signals for obesity care, procedure adoption, and hospital capacity. We referenced public health statistics and clinical guidance to keep assumptions aligned with what is typically documented in India, then mapped those signals to what is observable in the bariatric care pathway.

Typical sources included government health and population statistics (such as national survey releases), peer reviewed clinical journals on obesity and metabolic surgery outcomes, professional surgical society publications and registry style updates, medical device regulator notifications and recall notes, and customs or trade data for relevant device categories where it helped. We also reviewed hospital networks, annual reports, and investor presentations to understand capacity additions and service expansion. These examples are illustrative, and additional sources were also used to collect data, validate assumptions, and clarify open questions as the India-specific patient flow and device adoption details came into focus.

Primary Interviews and Surveys

Primary work focused on validating how often bariatric procedures are performed, how approaches are shifting (laparoscopic versus robotic-assisted), and how pricing moves by city tier and hospital type. We spoke with a mix of clinicians, procurement and hospital administrators, and device channel participants so gaps from desk research could be filled, especially around utilization, payer or self-pay dynamics, and what hospitals actually bill per case. Since this is an India-only market, interviews were balanced across major metros and fast-growing tier-2 treatment hubs to reflect where patient flow is expanding.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | |

| Mid tier: 51% | Functional/Unit leaders: 28% | |

| Smaller Players: 17% | Managers: 57% |

Market-Sizing & Forecasting

The core sizing starts with a top-down reconstruction of the addressable surgery pool in India, where obesity burden, treated patient eligibility, and procedure penetration are converted into annual procedure counts, and then translated into value using typical case economics. We then used selective bottom-up checks, such as sampled hospital throughput, average selling price ranges for key device kits, and channel discussions on volumes, and we applied adjustment when a gap showed up between top-down assumptions and observed capacity.

Key inputs that were tracked include obesity prevalence and related comorbidities, bariatric procedure mix (for example, restrictive versus bypass style procedures and endoscopic therapies), surgery approach split (laparoscopic, robotic-assisted, open), average procedure pricing by facility type, and changes in availability of trained surgeons and operating slots. Because pricing and utilization can shift quickly in India, scenario analysis was used for the forecast, and the final path was aligned to what experts consider realistic for adoption, reimbursement comfort, and capacity ramp-ups.

Data Validation & Update Cycle

Outputs were checked against independent signals such as procedure volumes reported by leading centers, changes in operating capacity, and import and procurement direction for surgical devices that typically move with case load. When a number looked inconsistent, we revisited assumptions and triggered follow-up calls to confirm whether the issue was pricing, mix shift, or a one-time capacity jump.

Before sign-off, the model goes through multi-step analyst review so arithmetic, unit logic, and year-on-year movements stay consistent across sections. The report is refreshed annually, and interim updates are made when material events change supply, pricing, or care access. Right before delivery, a final update pass is completed so the view reflects the latest available inputs.

Mordor Intelligence's India Bariatric Surgery Market Size Compared With Other Published Estimates

It is common to see different market values for India bariatric surgery, even when the topic name looks the same. Most gaps come from what is being counted as the market, which year is treated as the base, and whether the model is anchored to procedure demand, device revenue, or a combined care pathway.

By tracking procedure mix, approach split, and India-specific price bands, Mordor Intelligence keeps the estimate tied to observed care delivery and avoids inflating totals by counting broad obesity management spend that does not translate into surgeries.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 163.98 M (2026) | |

| Industry Publisher A | USD 300.00 M (2024) | This estimate appears to lean heavily toward procedure and service revenues and may apply higher average pricing or a wider billed-care definition, which can lift totals versus a model that separates core surgery activity from adjacent obesity care. |

| Advisory Firm B | USD 312.40 M (2026) | The scope described includes follow-up care and counseling services and may assume faster uptake and higher per-case realization across facilities, which can raise the value versus a model that uses tighter surgery-linked device and procedure accounting. |

Taken together, the spread in values is mainly explained by scope boundaries and how pricing and adoption are applied across facility types. Our approach stays traceable to clear levers, including procedure volumes, approach mix, and realistic India pricing ranges, which makes the estimate easier to reproduce and update when new signals emerge.

Key Questions Answered in the Report

How large is the India Bariatric Surgery market in 2026?

The sector is valued at USD 163.98 million in 2026 and is forecast to reach USD 238.47 million by 2031.

What is the expected CAGR for bariatric surgery devices in India?

The market is projected to grow at a 7.78% CAGR over 2026-2031.

Which device category currently dominates sales?

Assisting Devices, led by laparoscopic staplers and energy platforms, held 40.62% revenue share in 2025.

Which geographic areas are witnessing the fastest procedure growth?

Tier-2 cities such as Pune, Ahmedabad, and Kochi are advancing 11-14% annually thanks to medical tourism and lower pricing.

How are insurance changes affecting adoption?

Expanded coverage from major insurers now reimburses 60-70% of costs, lowering patient out-of-pocket spend and accelerating uptake, especially in Tier-2 markets.

Who are the key market leaders?

Medtronic, Johnson & Johnson's Ethicon, and Boston Scientific together captured about 55% of 2024 device revenue.

Page last updated on: