Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

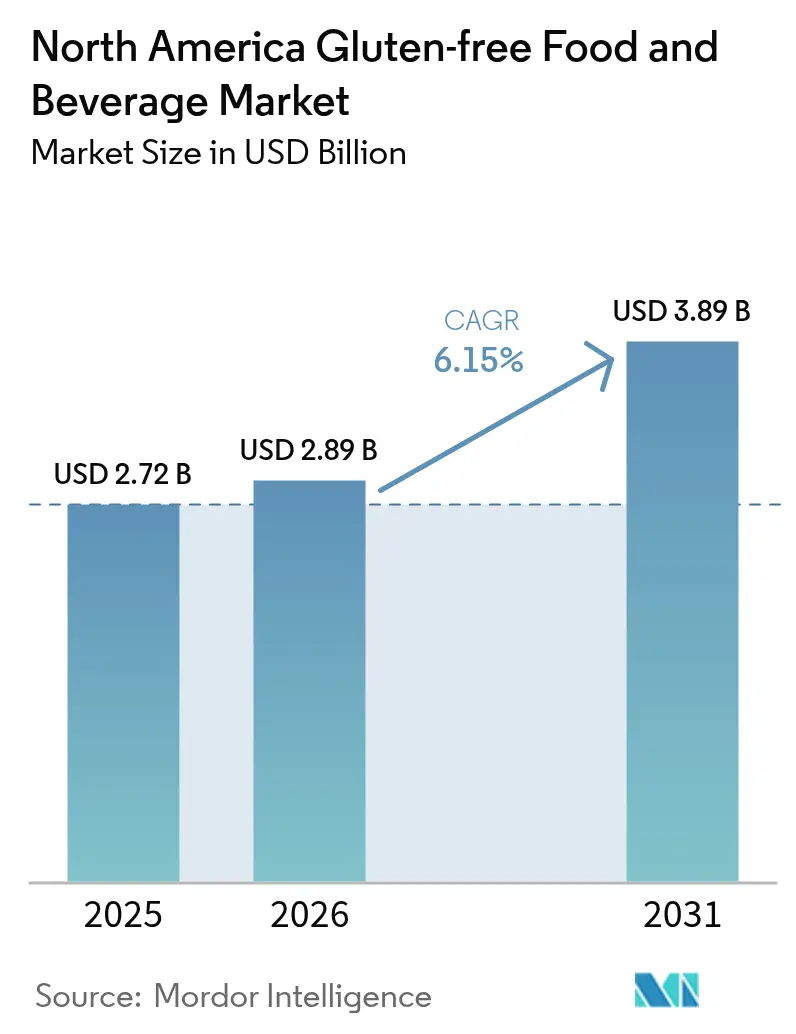

| Base Year Market Size (2025) | USD 2.72 Billion |

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 3.89 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

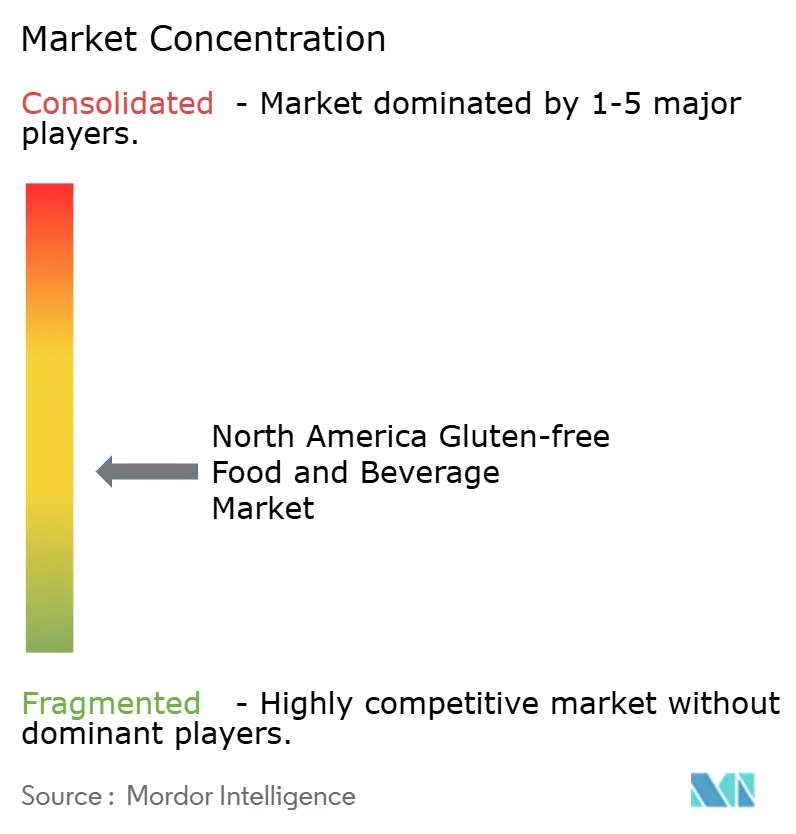

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Gluten-free Food and Beverage Market Analysis by Mordor Intelligence

The North America Gluten-Free Food and Beverages market size is expected to grow from USD 2.72 billion in 2025 to USD 2.89 billion in 2026 and is forecast to reach USD 3.89 billion by 2031 at 6.15% CAGR over 2026-2031. Steady demand for gluten-free products arises from a consistent base of diagnosed celiac patients and a larger group of lifestyle adopters who associate gluten avoidance with overall wellness. Mainstream retailers have integrated gluten-free products into their regular shelves, normalizing the category and reducing its historical price premiums. Innovations in ingredients, especially hydrocolloids, enzymes, and blends of ancient grains, have bridged the taste gap with wheat products while emphasizing a clean-label approach. These advancements have not only improved product quality but also expanded the appeal of gluten-free options to a broader consumer base. Visibility and distribution have been bolstered by e-commerce subscription models, partnerships with esports snacks, and mandates for corporate wellness catering, which have made gluten-free products more accessible and convenient for consumers. The competitive landscape remains moderately fragmented, and despite the entry of private labels, price sensitivity limits penetration among lower-income households, highlighting the need for cost-effective solutions to drive further adoption.

Key Report Takeaways

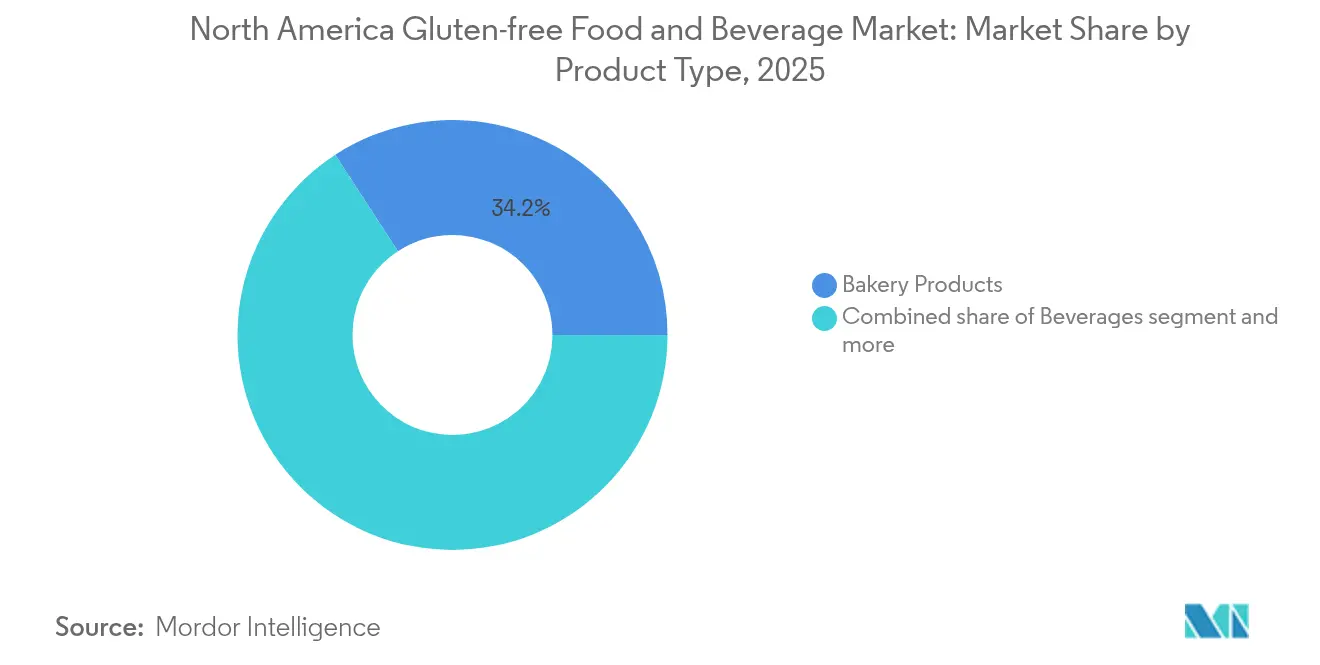

- By product type, Bakery Products led with 34.18% revenue share in 2025, while Beverages are forecast to expand at an 8.59% CAGR between 2026 and 2031.

- By source, plant-based formulations captured 52.22% of 2025 revenue and are projected to advance at a 7.28% CAGR through 2031.

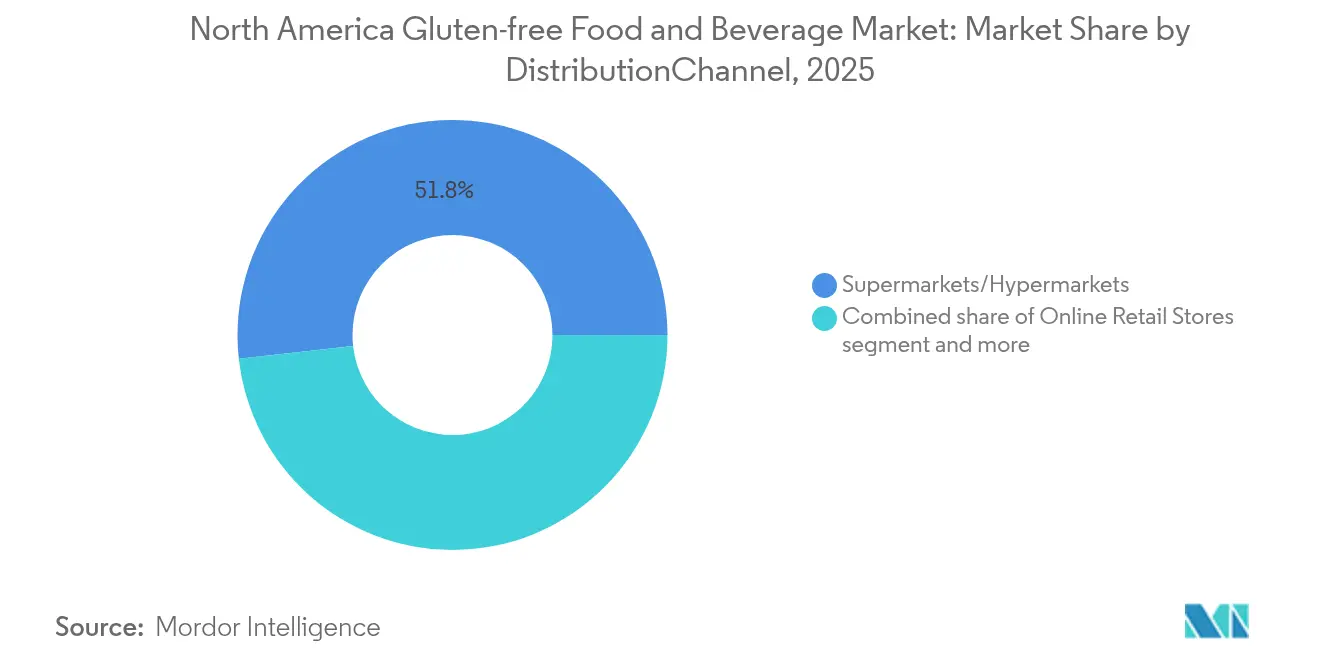

- By distribution channel, Supermarkets and Hypermarkets retained 51.76% of 2025 sales, whereas Online Retail Stores are set to grow at a 6.61% CAGR to 2031.

- By geography, the United States contributed 81.12% of 2025 value; Mexico represents the fastest riser with a 7.69% CAGR expected over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Gluten-free Food and Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosed celiac and gluten-sensitive population | +1.2% | United States, Canada (highest prevalence); Mexico (emerging awareness) | Medium term (2-4 years) |

| Mainstream "better-for-you" positioning in retail | +0.9% | United States, Canada (mature markets); Mexico (urban centers) | Short term (≤ 2 years) |

| Shelf expansion across mass grocery chains | +0.8% | United States (Walmart, Kroger); Canada (Loblaw); Mexico (Soriana, Chedraui) | Short term (≤ 2 years) |

| Ingredient and process innovations improving organoleptics | +1.0% | United States, Canada (research and development hubs); spillover to Mexico | Medium term (2-4 years) |

| Esports and gaming snacks adopting gluten-free formats | +0.4% | United States (primary gaming market); Canada (secondary) | Long term (≥ 4 years) |

| Corporate wellness catering mandates | +0.5% | United States, Canada (corporate wellness programs); limited Mexico adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising diagnosed celiac and gluten-sensitive population

About 1 in 133 North Americans grapple with celiac disease. In contrast, an estimated 6% of U.S. adults experience non-celiac gluten sensitivity, broadening the consumer base and driving demand for gluten-free products[1]Source: Celiac Disease Foundation, " What is Celiac Disease?",celiac.org . Notably, pediatric diagnoses are outpacing adult ones, prompting schools and daycares to offer gluten-free options. This trend not only normalizes early-age consumption but also fosters long-term adoption of gluten-free diets. Regulatory clarity plays a pivotal role in supporting market growth; the FDA's definition of gluten at less than 20 ppm aligns with Health Canada's standards, providing manufacturers with legal certainty and ensuring product consistency. While demand driven by medical necessity remains consistent, the influx of lifestyle adopters leads to a higher churn rate, as these consumers often switch between dietary trends. This dynamic pushes brands to prioritize innovation and develop diverse product offerings to retain customers. Together, these elements not only fuel consistent growth but also diversify demand across various age groups, creating opportunities for market expansion.

Mainstream “better-for-you” positioning in retail

Thirty percent of U.S. shoppers are now cutting back on gluten, even without a formal diagnosis, signaling that gluten-free has become a staple in the wellness decision-making process. Retail giants like Walmart and Kroger have rolled out private-label gluten-free products, pricing them up to 25% lower than established brands. This pricing strategy pressures mid-tier brands to stand out through certifications or unique functional ingredients. As clean-label preferences gain traction, there's a noticeable shift in formulations, moving away from additives like modified starch to more natural binders such as chia and psyllium. This trend, where health-conscious choices converge, has elevated gluten-free products into a premium subcategory, garnering loyalty from affluent consumers. Yet, nutritionists are raising eyebrows at the blanket avoidance of gluten, introducing a wave of skepticism among consumers. Brands now face the challenge of addressing this skepticism head-on, emphasizing the importance of transparent communication.

Shelf expansion across mass grocery chains

In 2024, U.S. supermarkets increased the average linear shelf space for gluten-free items by 12%, signaling retailer confidence in their sell-through rates and the growing consumer demand for such products[2]Source: United States Census, " Monthly Retail Trade",census.gov. While urban flagship stores now allocate entire aisles to these items, rural outlets tend to group them within a single bay, reflecting demographic and purchasing power differences between urban and rural areas. In a strategic move, Kroger replaced its slower-selling conventional pasta with gluten-free options during its 2024 shelf reset, boosting the category's sales velocity and aligning with evolving consumer preferences. Similarly, in Canada, Loblaw expanded its President’s Choice portfolio, adding over 200 SKUs to capitalize on the gluten-free trend and strengthen its competitive positioning in the market. In Mexico, chains like Soriana and Chedraui are testing dedicated bays for gluten-free products in upscale neighborhoods to cater to affluent consumers. However, these chains face a challenge: the shorter shelf life of gluten-free items increases rotation risk, necessitating careful inventory oversight and efficient supply chain management to minimize waste and ensure product availability.

Ingredient and process innovations improving organoleptics

Large incumbents are patenting starch-modification and enzyme treatments, addressing past texture issues and raising entry barriers for smaller competitors. These advancements allow larger players to maintain a competitive edge by offering improved product quality and consistency. Industrial-scale fermentation with sourdough cultures enhances elasticity and flavor complexity, while also reducing the need for additives, making products more appealing to health-conscious consumers. Ancient grains, such as quinoa and teff, boost nutrient density and marketing allure due to their perceived health benefits and unique flavors. However, their supply is sensitive to pricing, especially as climate events in South America and East Africa tighten harvests, leading to potential supply chain disruptions. While enzyme technologies show promise in reducing residual gluten to undetectable levels, outdated labeling rules introduce commercial uncertainties, complicating market positioning for gluten-free products. As a result, continuous research and development is crucial for brands aiming to match wheat-based products in quality and performance while justifying premium pricing to consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus conventional alternatives | -0.8% | United States, Canada (price-sensitive segments); Mexico (broader impact) | Short term (≤ 2 years) |

| Manufacturing cross-contamination risks | -0.5% | United States, Canada (stringent enforcement); Mexico (emerging standards) | Medium term (2-4 years) |

| Climate-driven scarcity of specialty GF grains | -0.6% | Global sourcing impact; Mexico (domestic production challenges) | Long term (≥ 4 years) |

| Labelling grey-zone for "gluten-reduced" claims | -0.3% | United States, Canada (regulatory ambiguity); Mexico (limited awareness) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium price versus conventional alternatives

In 2024, gluten-free bread commanded an average price of USD 6.50 per loaf, significantly outpacing wheat bread's USD 2.50 price tag[3]Source: Unitedc States Department of Agriculture,"Food Price Outlook, 2025 and 2026" , usda.gov . This price disparity poses challenges for mid-income consumers considering the switch. While private-label launches have narrowed this price gap, even a 1.5-time premium remains a deterrent for many, especially during economic downturns when gluten-free is often seen as a luxury. In Mexico, where minimum wages hover below USD 15 per day, gluten-free products remain largely out of reach for all but the upper-income brackets. Economic challenges in 2024 highlighted this sensitivity, with category growth decelerating as inflation tightened household budgets, as noted by. Consequently, manufacturers find themselves at a crossroads: should they reduce prices to expand their consumer base or maintain margins at the risk of slower unit growth.

Manufacturing cross-contamination risks

Brands using shared lines risk gluten traces surpassing the 20 ppm threshold, which can lead to non-compliance with regulatory standards and potential health risks for consumers with gluten sensitivities. While the FDA leans on post-market surveillance to monitor compliance, Health Canada intensifies compliance scrutiny through audits, pushing companies to adopt third-party certifications that ensure gluten levels dip below 10 ppm. These certifications not only help meet regulatory requirements but also build consumer trust. Although dedicated gluten-free plants effectively address these concerns by eliminating cross-contamination risks, they demand hefty investments and long-term planning. A case in point is General Mills' USD 50 million expansion in Iowa, which introduced proprietary milling and packaging lines to enhance gluten-free production capabilities. Recalls can inflict severe reputational damage and financial losses; a 2024 incident saw a mid-tier bakery brand's quarterly revenue plummet by 40%, underscoring the heightened risks for smaller entities that may lack the resources to recover quickly. Consequently, rigorous certification and testing have become essential for market entry, serving as a critical differentiator in an increasingly competitive market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverages Accelerate, Bakery Anchors Volume

In 2025, bakery products dominated North America's gluten-free food and beverage market, claiming a 34.18% share of the market's value. This dominance is rooted in years of refining gluten-free flour systems to mimic wheat's elasticity, allowing celiac and gluten-sensitive consumers to enjoy familiar bread, pastries, and cakes. These advancements have been pivotal in addressing the challenges of replicating the texture and structure of traditional baked goods without gluten. While innovations in hydrocolloids and enzyme technologies have enhanced crumb structure and mouthfeel, the surge in popularity of low-carb and keto diets has tempered growth. Nevertheless, the deep-seated presence of bread and bakery items in Western diets, bolstered by the rise of private-label brands and extensive retail distribution, ensures bakery products remain central to gluten-free shopping. Additionally, the availability of gluten-free bakery options across mainstream retail channels has made these products more accessible, further solidifying their market position.

Meanwhile, the beverage segment is on a rapid ascent, projected to grow at an 8.59% CAGR. Brands are crafting functional drinks using gluten-free bases like oats, sorghum, millet, and rice, catering to consumers' desires for digestive comfort and clean labels. These beverages adhere to the same 20 ppm gluten threshold as foods, bolstering trust among gluten-sensitive individuals. With energy drinks, functional waters, and craft beers made from gluten-free grains, consumption spans from sports events to social gatherings. The segment's growth is also driven by the increasing consumer preference for beverages that combine health benefits with allergen-free claims, making them suitable for a broader audience. As the trend for functional hydration merges with allergen-free and "free-from" labels, beverages are poised to seize a larger slice of North America's gluten-free market, even as bakery products maintain their lead.

By Source: Plant Dominates, Animal Retains Loyalist Niche

In 2025, plant-based formulations dominated North America's gluten-free food and beverage market, accounting for 52.22% of the revenue. Shoppers increasingly gravitate towards products that are both gluten-free and devoid of animal-derived ingredients. These plant-based offerings, bolstered by ingredients like pea protein, chickpea flour, and ancient grains, craft recipes that prioritize performance nutrition without compromising on taste. While regulatory frameworks equate plant and animal sources, plant-based SKUs leverage added claims such as vegan, non-GMO, and organic, justifying their premium pricing. Concerns over livestock production's environmental impact further sway perceptions towards plant inputs, despite ongoing challenges in replicating taste and texture in applications like cheese.

Plant-based products are not only leading but also the fastest-growing segment. The market for plant-based SKUs in North America's gluten-free food and beverages sector is set to expand at a 7.28% CAGR, mirroring the momentum of the broader plant-forward and flexitarian movement. This surge is bolstered by a growing appetite for cleaner labels and multifunctional products that cater to allergen avoidance, ethical considerations, and sustainability. While animal-derived gluten-free options, such as dairy yogurts and deli meats, are witnessing a more tempered growth, they hold significance for consumers prioritizing muscle maintenance, keto diets, and traditional protein formats. Furthermore, hybrid products that meld plant and animal ingredients are emerging, optimizing texture, amino acid profiles, and cost, underscoring a shift where functionality is gaining precedence over ideological purity in product innovation.

By Distribution Channel: Online Scales, Stores Remain Primary

In 2025, supermarkets and hypermarkets led North America's gluten-free food and beverage market, accounting for 51.76% of the revenue. Shoppers prioritize in-person label checks, texture assessments, and freshness evaluations. Major chains, through omnichannel strategies like curbside pickups and digital gluten-free filters, merge the tactile assurance of physical shopping with online ease, curbing the shift towards e-commerce. While specialist health-food outlets serve as initial discovery hubs, they're increasingly overshadowed by mass retailers offering similar products at more competitive prices. Institutional channels, spanning schools, hospitals, and corporate cafeterias, bolster this trend, consistently delivering volume amidst rising wellness and allergen-free initiatives.

Online retail emerges as the fastest-growing channel, projected to surge at a 6.61% CAGR. Subscription boxes, direct-to-consumer brands, and algorithmic recommendations spotlight niche gluten-free products, many of which might remain unseen on physical shelves. The U.S. leads this growth, buoyed by established logistics networks facilitating two-day or same-day deliveries, easing the process for repeat pantry buys. While these platforms shine with long-shelf-life items, they grapple with preservative-free baked goods, which are prone to staling during transit. Convenience stores further enrich the market landscape, bridging online and supermarket offerings by providing single-serve, on-the-go gluten-free snacks, catering to both commuters and gamers.

Geography Analysis

In 2025, the U.S. accounted for a dominant 81.12% of the market revenue, driven by FDA's clear labeling, a vast distribution network, and a cultural perception linking gluten-free products to holistic wellness. With penetration among diagnosed celiac patients nearing its peak, any further growth hinges on retaining lifestyle users, a group that can be sensitive to price fluctuations during economic downturns. Major retailers are placing gluten-free items in mainstream aisles, fostering habitual purchases without the stigma of being in a 'special-diet' section. Research and development hubs in Minneapolis, Chicago, and the Pacific Northwest are not only pushing the boundaries of product formulations but also setting benchmarks that neighboring markets look up to.

Mexico, though smaller in size, is witnessing the fastest growth at a 7.69% CAGR. This surge is supported by COFEPRIS aligning its regulations with international Codex standards, increasing urban incomes, and a heightened awareness among physicians regarding diagnostics. However, affordability poses a significant challenge, confining the adoption of gluten-free products primarily to affluent households in Mexico City and Monterrey. While local reformulations using corn and amaranth present a culturally resonant and cost-effective solution, they necessitate a commitment to consumer education. Additionally, imports grapple with tariffs and logistics costs, inflating retail prices and prompting multinationals to consider near-shoring their production.

Canada enjoys a strategic advantage with its regulatory alignment to the U.S., facilitating smooth cross-border supply chains and consistent quality standards. Retail giant Loblaw, with its vertically integrated approach, boasts over 200 gluten-free SKUs, all competitively priced against imports. Canadians spend more per capita on natural and organic foods than their U.S. counterparts, positioning gluten-free products as an integral part of a broader health-focused diet. While population constraints limit the overall market volume, a higher willingness to pay allows for premium product positioning. Other North American nations capture only a minor market share, hindered by lower income levels, a fragmented retail landscape, and reduced diagnostic rates. However, tourist hotspots in the Caribbean have carved out a niche demand, particularly within the hospitality sector.

Competitive Landscape

In North America, the gluten-free food and beverage market showcases a moderate fragmentation. Here, multinational food giants harness their scale and distribution prowess to dominate shelf space. In contrast, agile specialty brands carve out niche segments, emphasizing allergen-free certifications, transparent sourcing, and direct-to-consumer channels. Heavyweights like General Mills, Nestlé, Kellogg, and PepsiCo bolster their market presence by introducing gluten-free variants of their well-established franchises think Cheerios, DiGiorno, Rice Krispies, and Tostitos. This strategy not only eases consumer trials but also capitalizes on decades of brand equity. These industry stalwarts pour significant investments into dedicated production lines and secure third-party certifications, a move aimed at mitigating cross-contamination risks.

This capital-intensive approach poses challenges for smaller entrants. Meanwhile, specialty brands such as Bob's Red Mill, Enjoy Life, and Amy's Kitchen carve out their niche by emphasizing allergen-free products steering clear of the top 8 allergens, gluten included and maintaining transparent supply chains. This resonates deeply with health-conscious consumers wary of industrial food processing. The competitive landscape is evolving: larger entities vie on price and distribution, while boutique brands emphasize purity and origin. This dynamic creates a 'barbell' market, squeezing mid-tier brands from both ends.

There's untapped potential in the realm of functional gluten-free foods think protein bars, meal replacements, and sports nutrition. Here, manufacturers can amplify health claims (like high protein, low sugar, or keto-friendly) to command premium pricing and draw in health-focused consumers. The esports and gaming snack arena is a budding niche. Brands can forge connections with younger audiences through sponsorships and hands-on marketing. However, they must navigate formulation hurdles, ensuring portability and bold flavors, which demand research and development investment. Technology is rapidly reshaping the landscape: enzyme treatments that render gluten undetectable, fermentation methods enhancing texture and flavor, and AI-driven tools fine-tuning ingredient blends for cost-effectiveness and nutrition are emerging as key differentiators. Yet, navigating regulatory waters poses challenges. The FDA's gluten-free labeling mandate, alongside Health Canada's stringent standards, necessitates thorough testing and documentation. This often sidelines startups, who lean on third-party labs, in favor of established players boasting in-house quality assurance teams.

North America Gluten-free Food and Beverage Industry Leaders

-

Hain Celestial Group, Inc

-

Pepsico Inc.

-

Amy's Kitchen, Inc.

-

Unilever PLC

-

Neslte SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Whoa Dough rolled out its "Two Count Cookie Dough Snack Packs" in three enticing flavors at Grocery Outlet stores. With sights set on expanding to over 2,500 locations, these packs are plant-based and free from gluten, dairy, soy, and eggs. Verified as non-GMO, they deliver a delightful cookie dough experience with 4-5g of protein per bar and under 10g of sugar.

- October 2025: Ready protein bars made their nationwide debut, spotlighting the exclusive "Iced Oatmeal Cookie" flavor. They hit shelves in over 640 Vitamin Shoppe and Super Supplements stores, along with a presence on vitaminshoppe.com. Each bar packs 15g of protein, 7g of fiber, and 6g of whole grains. Proudly gluten-free and non-GMO, they steer clear of artificial sweeteners and sugar alcohols, catering to those seeking clean nutrition for active lifestyles.

- July 2025: Eshbal Functional Food Inc. made headlines with its acquisition of Gluten Free Nation. This strategic move bolsters Eshbal's North American offerings, adding GF Nation's diverse range of sweet and savory products, including breads, muffins, pound cakes, and cookies. These items are already making waves, being sold through major platforms like Walmart.com and Kroger across 49 states.

- March 2024: Tirlán introduced its "Truly Gluten Free" oat drinks to the U.S. market. Crafted from Irish gluten-free oats sourced from 110 farms within an 80-mile radius of the Portlaoise mill, the lineup features both a classic oat drink and a barista variant. These oat milk products boast stringent seed-to-bottle management, ensuring no gluten contamination. They also proudly present a verified low carbon footprint of 207-232kg CO2e/t and a zero-waste commitment, with milling byproducts redirected to animal feed or composting.

North America Gluten-free Food and Beverage Market Report Scope

The North American gluten-free food and beverage market is segmented by product type and geography. On the basis of product type, the market is segmented into beverages, bread products, cookies and snacks, condiments, seasonings, and spreads, dairy/dairy substitutes, meat/meat substitutes, and other gluten-free products. Based on geography, the report covers the North American region, which includes the United States, Mexico, Canada, and Rest of North America.

Product Type

| Bakery Products | Breads and Cakes |

| Cookies and Biscuits | |

| Other Bakery Products | |

| Snacks and RTE Products | |

| Beverages | |

| Condiments, Seasonings and Spreads | |

| Dairy and Dairy Substitutes | |

| meat and Meat Substitutes | |

| Other Gluten-free Products |

By Source

| Plant-based |

| Animal-Based |

Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialist Retailers |

| Online Retail Stores |

| Other Distribution Channels |

Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Product Type | Bakery Products | Breads and Cakes |

| Cookies and Biscuits | ||

| Other Bakery Products | ||

| Snacks and RTE Products | ||

| Beverages | ||

| Condiments, Seasonings and Spreads | ||

| Dairy and Dairy Substitutes | ||

| meat and Meat Substitutes | ||

| Other Gluten-free Products | ||

| By Source | Plant-based | |

| Animal-Based | ||

| Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialist Retailers | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America |

Key Questions Answered in the Report

How big is the North America Gluten Free Food and Beverages market in 2026?

The market is valued at USD 2.89 billion in 2026 with a 6.15% CAGR forecast to 2031.

Which product type is growing fastest?

Beverages are expected to record the quickest expansion at an 8.59% CAGR through 2031 as brands reformulate with gluten-free grains.

What share do plant-based formulations hold?

Plant-based recipes accounted for 52.22% of 2025 revenue and are advancing at a 7.28% CAGR, outpacing animal-based counterparts.

Which sales channel leads distribution?

Supermarkets and Hypermarkets hold 51.76% of revenue, although Online Retail Stores are the fastest-growing at a 6.61% CAGR.

Page last updated on: