North America Solid Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

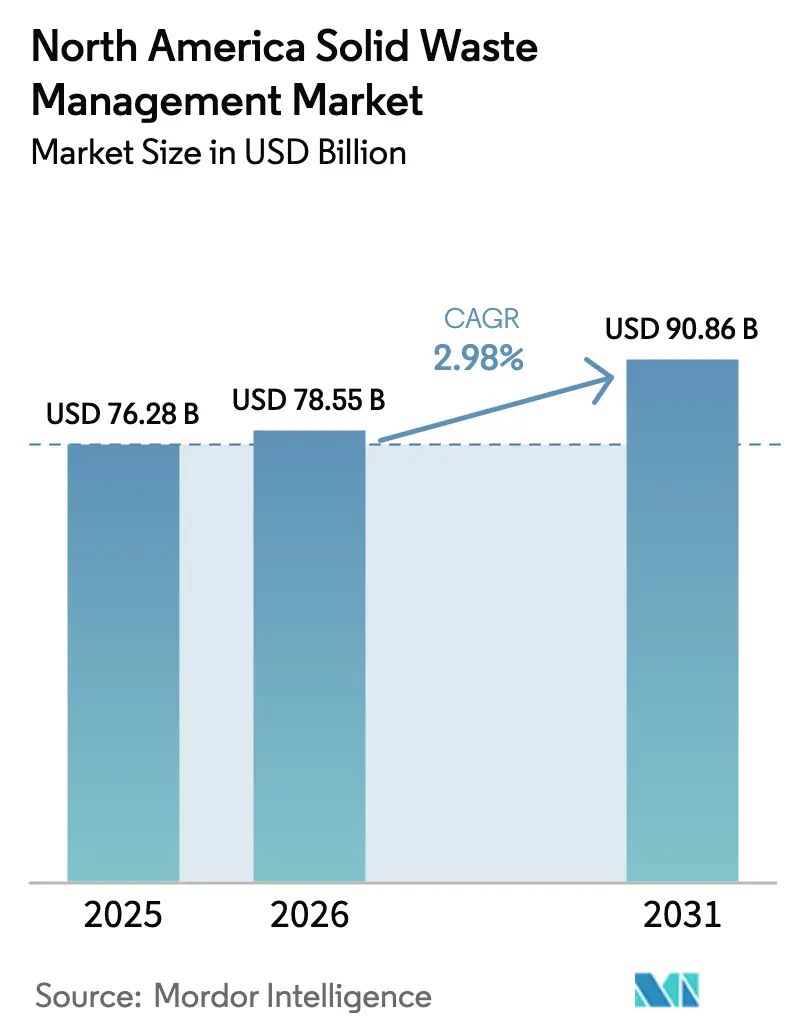

| Base Year Market Size (2025) | USD 76.28 Billion |

| Market Size (2026) | USD 78.55 Billion |

| Market Size (2031) | USD 90.86 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

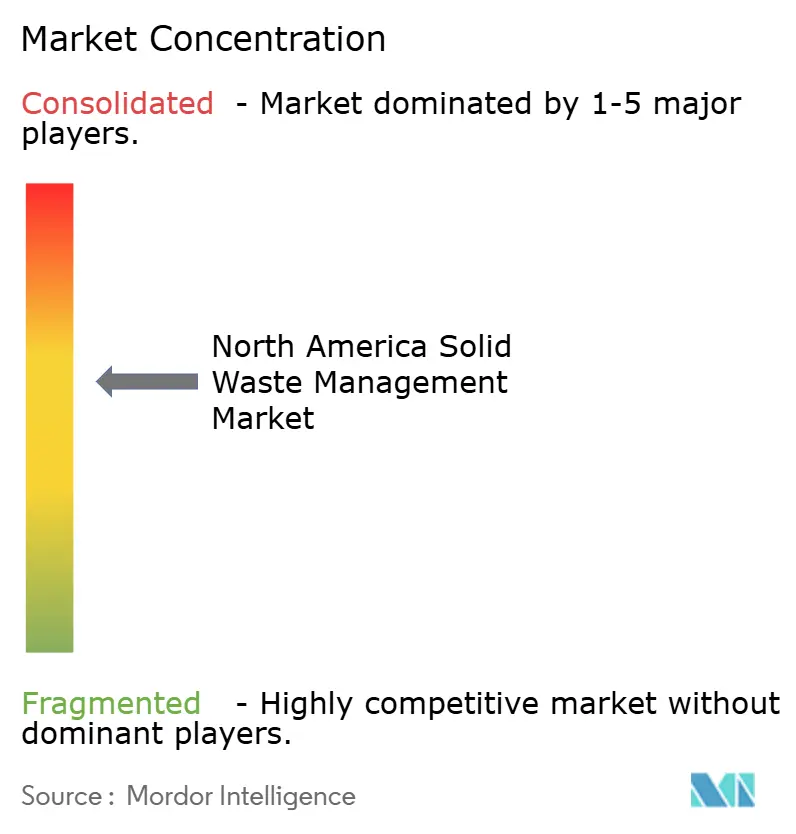

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Solid Waste Management Market Analysis by Mordor Intelligence

The North America Solid Waste Management Market size was valued at USD 76.28 billion in 2025 and estimated to grow from USD 78.55 billion in 2026 to reach USD 90.86 billion by 2031, at a CAGR of 2.98% during the forecast period (2026-2031). Rising landfill-gas–to-renewable-natural-gas (RNG) investments, corporate ESG mandates, and extended producer responsibility (EPR) regulations are shifting growth from pure volume expansion toward higher-margin recycling, energy recovery, and compliance services. Waste-to-energy contracts and closed-loop material recovery now command premium fees that insulate operators from fluctuations in recycled-commodity prices. As a result, the North America solid waste management market is becoming a platform for energy, data, and sustainability services that improve revenue quality even while overall volumes stabilize. Competitive intensity is rising in hazardous waste, healthcare waste, and RNG project finance, where regulatory complexity keeps barriers to entry high.

Key Report Takeaways

- By product type, waste disposal equipment led with 59.85% revenue share in 2025; waste recycling and sorting equipment is projected to expand at a 3.47% CAGR through 2031.

- By waste type, non-hazardous waste held a 77.65% share of the North America solid waste management market size in 2025, while hazardous waste is expected to advance at a 3.22% CAGR to 2031.

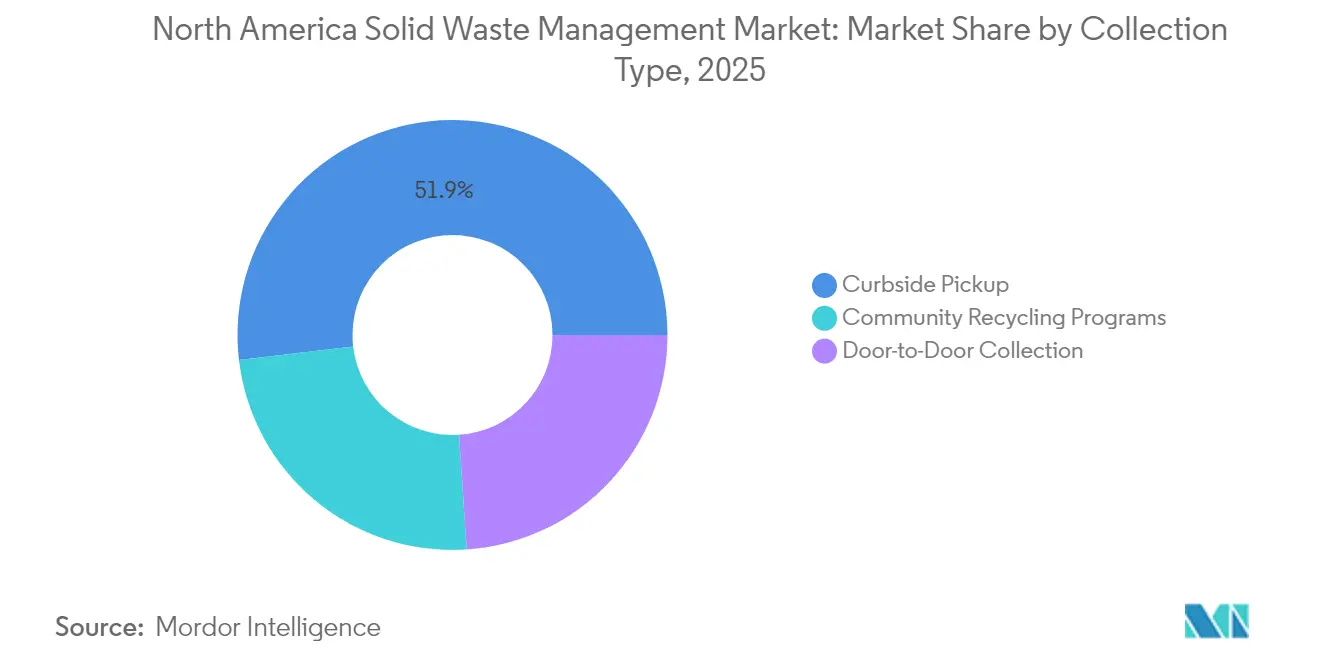

- By collection type, curbside pickup accounted for a 51.85% share of the North America solid waste management market size in 2025, and community recycling programs are projected to progress at a 3.44% CAGR through 2031.

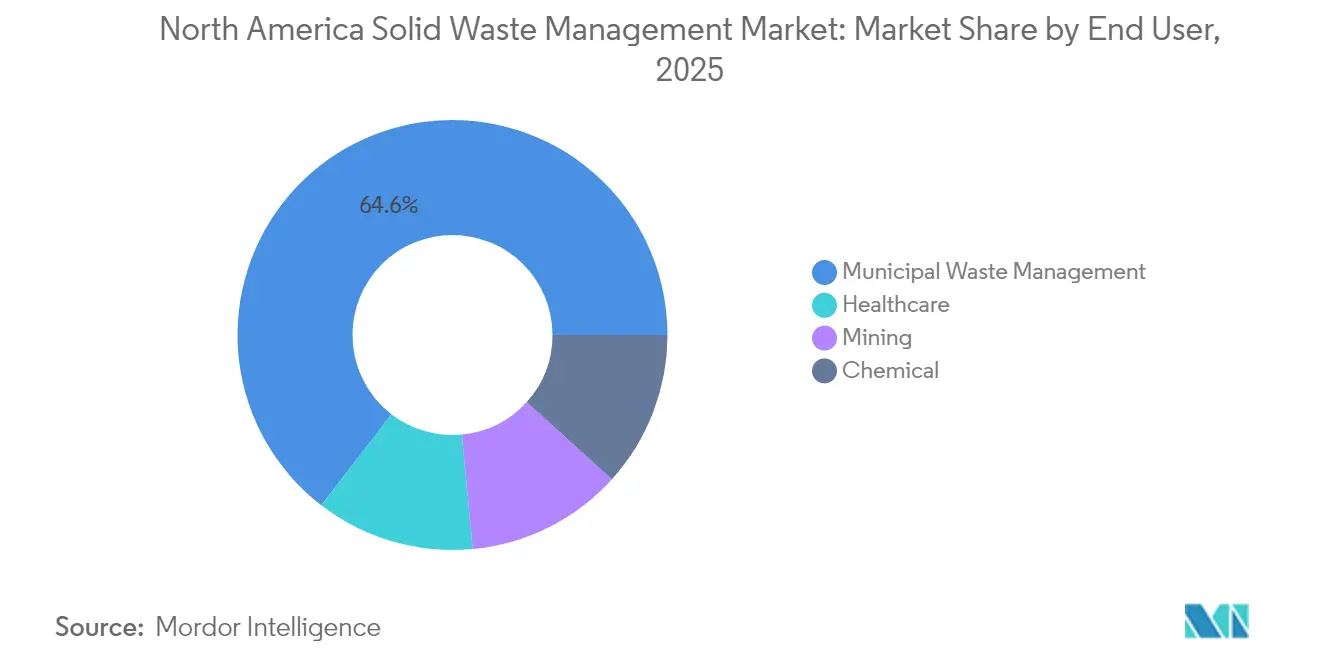

- By end user, municipal services accounted for 64.55% of the North America solid waste management market share in 2025, whereas healthcare waste services were projected to post the highest CAGR of 3.33% until 2031.

- By geography, the United States captured 79.60% revenue share in 2025; Mexico is expected to record the fastest growth at a 3.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Solid Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Circular-economy and recycling mandates accelerate infrastructure investment | +0.8% | United States and Canada, limited Mexico adoption | Medium term (2-4 years) |

| Corporate ESG targets boost demand for closed-loop services | +0.6% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Landfill-gas-to-RNG projects surge under RFS, LCFS and IRA incentives | +0.7% | United States primary, Canada secondary | Long term (≥ 4 years) |

| Ontario landfill-capacity crisis and U.S. export fees trigger regional build-outs | +0.4% | Ontario and Northeast U.S., spillover to adjacent states | Medium term (2-4 years) |

| Smart collection and AI sorting slash OPEX, enable PAYT pricing | +0.5% | North America urban markets, gradual rural penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Circular-Economy and Recycling Mandates Accelerate Infrastructure Investment

EPR statutes, such as California's SB 54 and Canada’s federal single-use plastic ban, obligate producers to finance sorting and processing upgrades, creating predictable fee income for operators in the North American solid waste management market[1]Environment and Climate Change Canada, “Government of Canada Delivers on Commitment to Ban Harmful Single-Use Plastics,” canada.ca. Republic Services has earmarked USD 200 million for optical-sorting retrofits in 2024 that meet contamination thresholds under state rules. Mandatory compliance structures convert recycling from a discretionary expense into an embedded cost of doing business, allowing contracts that guarantee minimum tonnage regardless of resin price cycles. As a result, capital flows toward robotic sorters, chemical recycling, and advanced material recovery facilities are accelerating, positioning the North American solid waste management market for sustained infrastructure build-out.

Corporate ESG Targets Boost Demand for Closed-Loop Services

Fortune 500 procurement programs now require verifiable waste diversion metrics, prompting suppliers to invest in integrated collection, recycling, and reporting solutions. Waste Management’s acquisition of Stericycle gives the combined entity an end-to-end healthcare waste platform that supports pharmaceutical take-back, packaging recovery, and digital tracking. Outcome-based contracts, anchored in diversion and carbon reduction, enable premium pricing and long-term renewals, reinforcing the value-over-volume shift inside the North America solid waste management market.

Landfill-Gas-to-RNG Projects Surge Under RFS, LCFS and IRA Incentives

Federal production tax credits and California LCFS credits combine to generate USD 15–25 per MMBtu for qualifying RNG, transforming landfills from cost centers into profit pools. Private-equity funds are now underwriting landfill acquisitions based on gas potential, reshaping valuation models and driving consolidation momentum across the North America solid waste management market.

Ontario Landfill-Capacity Crisis and U.S. Export Fees Trigger Regional Build-Outs

Ontario faces a 20-year disposal deficit starting in 2028. Waste Connections’ CAD 2.1 billion purchase of Canadian assets positions the firm for premium pricing once regional capacity tightens. Emerging thermal-treatment and waste-to-energy proposals seek to fill the impending gap, injecting fresh capital into the North America solid waste management market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled-commodity price volatility undermines revenue stability | -0.4% | Global, amplified in export-dependent regions | Short term (≤ 2 years) |

| Chronic labor shortages and work stoppages disrupt collection | -0.3% | North America urban centers, acute in Canada | Medium term (2-4 years) |

| CERCLA listing of PFAS heightens landfill liability exposure | -0.2% | United States primary, regulatory spillover expected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recycled-Commodity Price Volatility Undermines Revenue Stability

Mixed-paper prices plunged in 2024, while recycled-polymer values swung 40% quarter-to-quarter, complicating payback models for robotic sorters. Operators now write price-adjustment clauses into municipal contracts, shifting risk to cities that lack hedging tools. This uncertainty delays investment in next-generation recovery technology, tempering near-term revenue growth inside the North America solid waste management market.

Chronic Labor Shortages and Work Stoppages Disrupt Collection

The American Trucking Association estimates a 78,000-driver shortfall in the collection fleet, with annual turnover topping 95% at some firms[2]American Trucking Association, “Driver Shortage Report,” trucking.org . Wage inflation and sporadic work stoppages increase operating costs and service risk, prompting accelerated trials of autonomous side-loading trucks and AI route optimization. Until regulatory frameworks permit commercial deployment, labor scarcity will limit margin expansion in the North America solid waste management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Modernization Drives Recycling Growth

Waste disposal equipment retained a commanding 59.85% share of the North America solid waste management market size in 2025, reflecting entrenched landfill and transfer-station infrastructure across the region. However, revenue growth is shifting toward high-tech recycling and sorting systems, which are projected to post a 3.47% CAGR through 2031, underpinned by EPR mandates and purity standards that manual sorting cannot meet. AI-guided optical scanners now recover 95% of target plastics and metals, unlocking premium offtake pricing and reducing contamination penalties.

The equipment refresh cycle is blurring boundaries between disposal and recovery assets. Autonomous side-loading trucks piloted by Waste Management in Phoenix reduced fuel use by 12% and increased route capacity without requiring additional labor. Smart compactors equipped with Internet-of-Things sensors generate real-time fullness data, triggering dynamic collection schedules that slash empty-run miles and extend container life. Manufacturers increasingly bundle predictive-maintenance analytics with hardware sales, creating sticky service revenues that enrich the North America solid waste management industry’s aftermarket ecosystem.

By Waste Type: Hazardous Streams Command Premium Growth

Non-hazardous streams account for 77.65% of 2025 volume, but hazardous waste revenue is expanding at a 3.22% CAGR as PFAS, pharmaceutical, and semiconductor effluent regulations tighten. The North American solid waste management market size for hazardous materials continues to rise, even as overall tonnage remains modest, due to specialized transport, treatment, and liability-coverage fees that can reach eight times the standard tipping rates. Healthcare and electronics manufacturers now contract with multi-state treatment networks to ensure compliance across jurisdictions, reinforcing the value proposition of integrated players in the North America solid waste management market.

Organic waste, while classified as non-hazardous, is emerging as the feedstock of choice for RNG facilities tied to state Low-Carbon Fuel Standards. Anaerobic digestion units co-located at landfills or dairy farms convert food waste into pipeline-quality gas, diversifying revenue streams. As RNG yields increase, non-hazardous waste contracts are being rewritten to share energy credit proceeds, adding a financial incentive that counterbalances waste-reduction policies within the broader North America solid waste management industry.

By Collection Type: Community Programs Reshape Municipal Services

Curbside pickup accounted for 51.85% of 2025 revenue, yet community recycling programs are forecasted to grow 3.44% annually as suburban and rural municipalities adopt drop-off depots and neighborhood hubs. These decentralized models reduce route mileage and driver hours, resulting in service-cost savings that appeal to cash-strapped local governments. Smart-bin sensors support hybrid scheduling, which pairs baseline weekly pickup with on-demand overflow service, thereby enhancing customer satisfaction while optimizing fleet utilization in the North American solid waste management market.

Pay-as-you-throw (PAYT) billing, enabled by RFID-tagged carts, is encouraging households to limit residual disposal and sort recyclables more diligently. Adoption remains uneven due to upfront technology investment, but early successes are prompting regional consortiums to pool procurement and spread fixed costs, reinforcing the viability of community programs across the North America solid waste management market.

By End User: Healthcare Waste Accelerates Post-Pandemic

Municipal accounts accounted for 64.55% of 2025 revenue, while healthcare clients are expected to drive growth with a 3.33% CAGR through 2031. Aging demographics and the outpatient-care boom lift regulated medical waste volumes, while DEA drug-take-back mandates fuel demand for secure pharmaceutical destruction. Waste Management’s USD 7.2 billion acquisition of Stericycle created the region’s largest integrated healthcare platform, capable of tracking sharps, chemotherapy, and controlled-substance streams from cradle to grave. These capabilities justify premium contract rates and long tenures, raising switching costs within the North America solid waste management market.

Chemical and mining sectors are generating more hazardous by-products as reshoring trends revive domestic production, particularly in battery materials and semiconductor fabs in Texas and Arizona. Operators with multi-jurisdiction treatment footprints capture these accounts, underscoring the competitive advantage of scale. Meanwhile, retailers leverage take-back programs to satisfy ESG scorecards, adding a consumer-facing dimension to demand patterns in the broader North America solid waste management industry.

Geography Analysis

The United States accounts for 79.60% of the 2025 value, reflecting mature infrastructure, favorable RNG incentives, and a dense network of transfer stations that lower logistics costs. Federal production tax credits under the Inflation Reduction Act continue to funnel capital into landfill gas capture and organics digestion, supporting steady expansion even as per-capita waste generation levels off. Growth in the U.S. segment, therefore, hinges on value-added services—such as digital tracking, energy recovery, and ESG reporting—that deepen wallet share within existing accounts, sustaining momentum for the North American solid waste management market.

Canada remains a significant market, though disposal capacity gaps in Ontario force costly exports to U.S. landfills. Provincial EPR schemes and the federal single-use plastic ban are catalyzing investments in chemical recycling and thermal treatment facilities, while cross-border trade friction is spurring domestic solutions. Western provinces benefit from construction debris tied to LNG terminal build-outs, yet also confront landfill methane regulations that resemble U.S. rules, aligning the two markets’ policy trajectories and reinforcing cross-border best-practice sharing in the North America solid waste management market.

Mexico, advancing at a 3.29% CAGR, is the growth frontier as urbanization, industrial corridors, and evolving environmental statutes stimulate private-sector participation. Municipal concessions in Mexico City and Monterrey include waste-to-energy clauses that guarantee feedstock volumes, creating bankable revenue streams for foreign investors. Informal sector competition and uneven enforcement still pose challenges, but ongoing NAFTA supply-chain integration encourages multinationals to replicate U.S. compliance protocols, accelerating professionalization across the North America solid waste management market.

Competitive Landscape

The North America solid waste management market is moderately fragmented. The consolidation has accelerated following Waste Management’s acquisition of Stericycle, as peers have rushed to fortify vertical niches such as healthcare waste, hazardous materials, and recycling MRFs. Strategic partnerships with OEMs and energy firms are proliferating. White-space opportunities reside in PFAS remediation, battery-recycling logistics, and organics processing. Clean Harbors and specialized boutique firms pursue high-margin niche markets for hazardous waste, while municipal agencies issue long-term build-own-operate contracts for food waste digestion. As ESG disclosures become mandatory, investors reward operators that demonstrate quantifiable environmental benefits, reinforcing consolidation around firms with integrated, tech-enabled service portfolios.

North America Solid Waste Management Industry Leaders

Waste Management Inc.

Republic Services

GFL Environmental Inc.

Waste Connections

Clean Harbors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: GFL Environmental acquired Superior Waste Industries in Oklahoma, adding multiple transfer stations and an MSW landfill as part of its USD 900 million 2025 mergers and acquisitions program.

- July 2025: Casella Waste Systems agreed to purchase Mountain State Waste, extending its footprint across West Virginia, Ohio, Pennsylvania, and Kentucky, and adding about USD 30 million in annualized revenue.

North America Solid Waste Management Market Report Scope

Solid waste management is basically the whole process of getting rid of solid waste. It involves collecting waste from different sources, transporting it, treating it, analyzing it, and then disposing of it.

The solid waste management market is segmented by waste type, disposal method, and geography. By waste type, the market is segmented into e-waste, plastic, hazardous, bio-medical, and other waste types; by disposal methods, the market is segmented into landfills, incineration, and recycling; and by region, the market is segmented into the United States, Canada, and Mexico.

The report offers market size and forecasts for the solid waste management market in terms of value (USD) for all the above segments.

| Waste Disposal Equipment |

| Waste Recycling and Sorting Equipment |

| Hazardous Waste |

| Non-hazardous Waste |

| Curbside Pickup |

| Door-to-Door Collection |

| Community Recycling Programs |

| Municipal Waste Management |

| Healthcare |

| Chemical |

| Mining |

| United States |

| Canada |

| Mexico |

| By Product Type | Waste Disposal Equipment |

| Waste Recycling and Sorting Equipment | |

| By Waste Type | Hazardous Waste |

| Non-hazardous Waste | |

| By Collection Type | Curbside Pickup |

| Door-to-Door Collection | |

| Community Recycling Programs | |

| By End User | Municipal Waste Management |

| Healthcare | |

| Chemical | |

| Mining | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America solid waste management market in 2026?

The market stands at USD 78.55 billion in 2026 and is forecast to reach USD 90.86 billion by 2031.

What is the expected CAGR for solid waste management services in North America?

The market is projected to register a 2.98% CAGR during 2026-2031.

Which product category leads revenue in regional waste management?

Waste disposal equipment accounts for 59.85% of 2025 revenue, supported by established landfill and transfer-station infrastructure.

Which waste stream is growing fastest across North America?

Hazardous waste services are projected to post the strongest growth at a 3.22% CAGR due to stricter regulations for PFAS and pharmaceuticals.

Which country is the fastest-growing market within North America?

Mexico is forecast to expand at a 3.29% CAGR through 2031, driven by urbanization and new environmental policies.

What factor is driving investment in landfill gas projects?

Layered incentives under the Inflation Reduction Act, the Renewable Fuel Standard, and the Low Carbon Fuel Standard make RNG yields financially attractive.

Page last updated on: