North America Shrink And Stretch Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

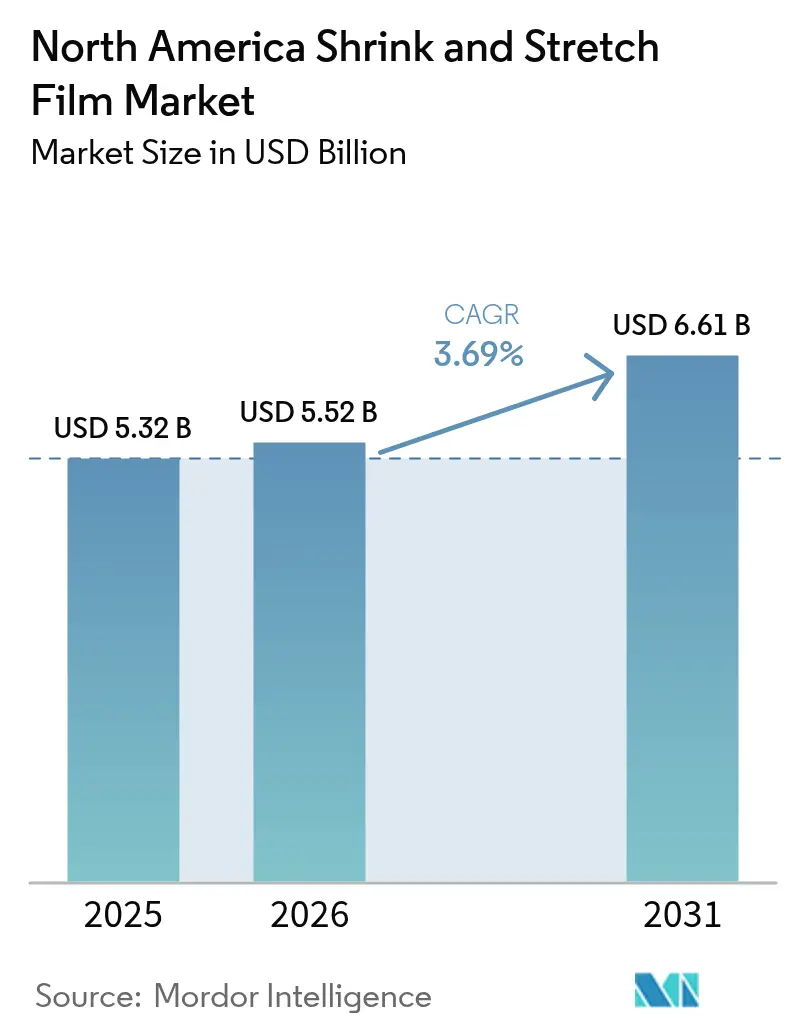

| Base Year Market Size (2025) | USD 5.32 Billion |

| Market Size (2026) | USD 5.52 Billion |

| Market Size (2031) | USD 6.61 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

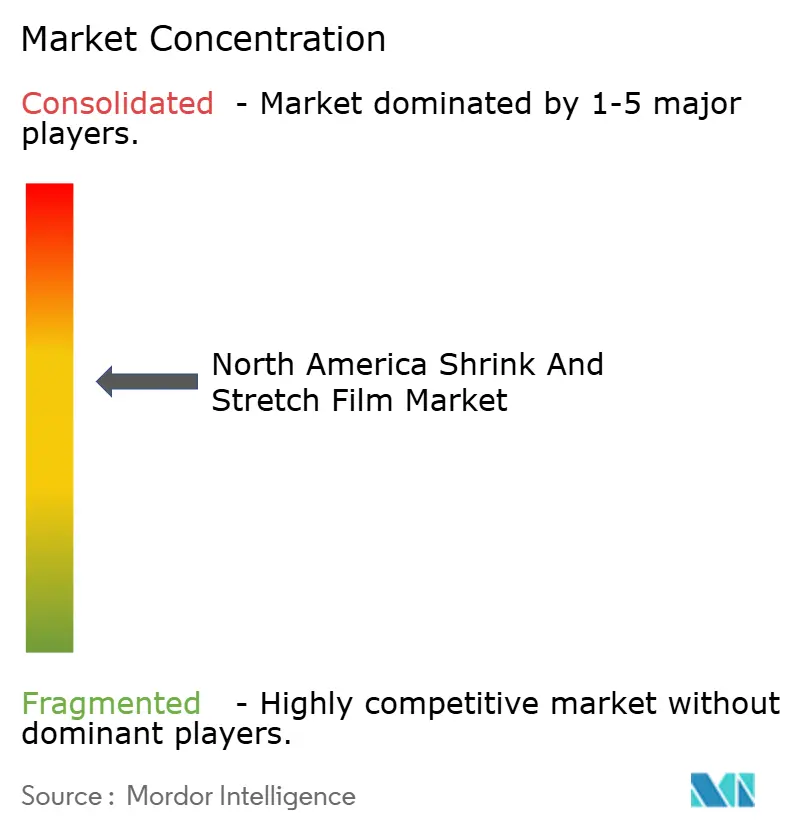

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Shrink And Stretch Film Market Analysis by Mordor Intelligence

The North America shrink and stretch film market size is expected to grow from USD 5.32 billion in 2025 to USD 5.52 billion in 2026 and is forecast to reach USD 6.61 billion by 2031 at 3.69% CAGR over 2026-2031. Growth reflects the region’s gradual market maturation yet underscores resilient demand as fulfillment centers, food processors, and industrial shippers modernize packaging lines. Demand benefits from warehouse automation that favors machine-grade films tuned for high-speed palletizers, the steady expansion of processed and frozen foods, and regulatory shifts that push converters toward recycled or bio-based resins. Consolidation among large film producers supports pricing power, while near-shoring into Mexico raises cross-border pallet flows that require reliable load-containment solutions. At the same time, cost pressures from volatile resin prices and an uneven patchwork of single-use plastic rules compel converters to innovate with downgauged, mono-material, and post-consumer-recycled (PCR) films that comply with emerging fee structures.

Key Report Takeaways

- By product type, stretch wraps accounted for 51.35% of the North America shrink and stretch film market share in 2025, whereas stretch hoods are advancing at a 3.74% CAGR through 2031.

- By material, LLDPE captured 62.35% of the North America shrink and stretch film market share in 2025, whereas recycled & bio-based PE is advancing at a 3.99% CAGR through 2031.

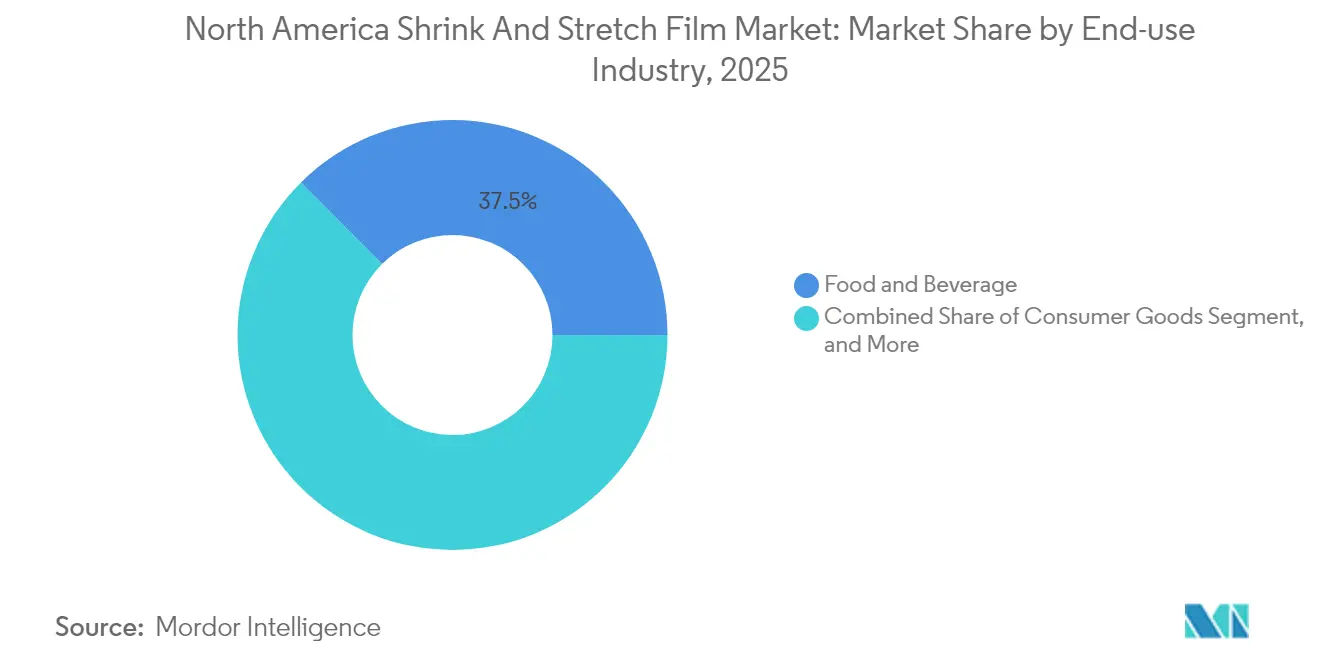

- By end-use industry, food & beverage held 37.45% of the North America shrink and stretch film market share in 2025, whereas e-commerce fulfillment centers are advancing at a 3.78% CAGR through 2031.

- By packaging application, pallet unitization captured 51.28% of the North America shrink and stretch film market share in 2025, whereas tamper-evident sleeve labeling is advancing at a 3.92% CAGR through 2031.

- By country, the United States dominated the North America shrink and stretch film market with a 77.55% share in 2025, whereas its market is advancing at a 3.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Shrink And Stretch Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment boom raises pallet-wrap usage | +0.8% | United States and Canada | Medium term (2-4 years) |

| Growth of processed and frozen foods | +0.6% | United States and Canada | Long term (≥ 4 years) |

| Warehouse automation prefers stretch hoods | +0.5% | United States and Canada | Medium term (2-4 years) |

| Tamper-evident regulations | +0.4% | United States and Canada | Short term (≤ 2 years) |

| Mexico near-shoring boosts cross-border traffic | +0.3% | United States primarily | Medium term (2-4 years) |

| Cannabis cold-chain demands downgauged film | +0.2% | United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment Boom Raises Pallet-Wrap Usage

Robust online retail expansion continues to transform the North America shrink and stretch film market, with fulfillment campuses demanding machine-grade stretch films that deliver repeatable performance at 60-plus pallets per hour. Amazon’s plan for 15 new U.S. and Canadian centers and Walmart’s USD 4.2 billion logistics upgrade highlight how automated stretch hoods now outperform spiral wraps for mixed-SKU pallet loads.[1]Packaging Dive reported ten manufacturers expanding North American rPET and film capacity to meet sustainability mandates PACKAGINGDIVE.COM. Converters able to fine-tune seven-layer formulations onsite win contracts by helping operators cut film waste and downtime. Load-stability requirements also favor puncture-resistant films that maintain clarity for barcode scanning. Regional film plants near Midwestern and Southwestern warehouse corridors shorten lead times and mitigate freight surcharges, strengthening competitive positions.

Growth of Processed and Frozen Foods Drives Retail Shrink Film

Accelerating demand for convenience meals sustained an 8.2% rise in U.S. frozen food sales during 2024, lifting orders for retail shrink sleeves that tolerate cold-chain temperature swings. Beverage bottlers likewise adopt tamper-evident bands to satisfy FDA guidance, pushing converters toward multilayer sleeves with perforated tear strips. Product-launch velocity compels labels to integrate wash-off inks, as seen in Klöckner Pentaplast’s SmartCycle sleeves that remain attached during PET reclamation. These developments reinforce the North America shrink and stretch film market’s stability even amid sustainability scrutiny, because recyclable barrier structures now address retailer mandates without sacrificing shelf life.

Warehouse Automation Prefers Stretch Hoods for Load Stability

Distribution hubs retrofitted with automated storage and retrieval systems specify stretch hoods that achieve up to 120 wrapped pallets per hour, quadrupling output versus manual spiral-wrap methods. The technology’s 360-degree tension and uniform cling sharply reduce product damage, a critical KPI for parcel carriers such as FedEx and UPS. As capital budgets migrate toward automation, film demand tilts toward thicker, multi-layer hoods offering superior tear resistance and optical clarity. Film makers with in-house testing lines simulate high-speed hooding to validate resin blends, cementing supply agreements that lock in multi-year volume commitments within the North America shrink and stretch film market.

Tamper-Evident Regulations in Pharma and Beverages

Revised FDA rules effective 2024 mandate overt breach indicators for over-the-counter drugs, accelerating adoption of shrink sleeves with perforated tabs and holographic seals. Cannabis edibles sold in 23 regulated U.S. states must pair child-resistant closures with tamper-evident wraps, broadening niche consumption. Premium spirits and craft brewers voluntarily deploy shrink bands to underscore authenticity, fueling demand for printed, heat-shrinkable films that accommodate complex container shapes. Suppliers capitalize by embedding covert security inks within five-layer structures that resist counterfeiting. The resulting value-added sales uplift the North America shrink and stretch film market even as volume growth moderates in commoditized wrap categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polyethylene and PVC resin prices | -0.7% | United States and Canada | Short term (≤ 2 years) |

| Stringent single-use-plastic legislation | -0.5% | United States and Canada | Medium term (2-4 years) |

| PCR supply shortage limits film output | -0.4% | United States and Canada | Long term (≥ 4 years) |

| Patent litigation delays advanced films | -0.3% | United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyethylene and PVC Resin Prices

North American spot polyethylene values swung 40% during 2024 amid feedstock outages and shipping bottlenecks, squeezing converter margins that hinge on thin unit economics. PVC resin spiked 35% year-over-year, eroding the competitiveness of high-clarity shrink sleeves. Large vertically integrated players hedge inventory with forward contracts, but smaller converters struggle to pass through surcharges promptly, eroding working-capital positions. These unpredictable inputs slow capital spending on new extrusion lines, tempering near-term expansion of the North America shrink and stretch film market.

Stringent Single-Use-Plastic Legislation in U.S. States and Canada

Thirteen U.S. states now restrict PFAS in food packaging, while California imposes 100 ppm organofluorine caps that challenge coated films[2]Keller and Heckman LLP, “FDA Announces FCNs for 35 PFAS Are No Longer Effective,” packaginglaw.com Colorado, Minnesota, and Oregon have enacted extended producer responsibility programs with eco-modulated fees that penalize non-recyclable laminates, lifting compliance costs by double digits. Canada’s Federal Plastics Registry begins in September 2025, requiring resin producers and converters to disclose volumes, foreshadowing national levies. Navigating divergent rules forces converters to reformulate product lines and maintain parallel SKUs, raising complexity and dampening scale benefits within the North America shrink and stretch film market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stretch Wraps Retain Leadership, Hoods Accelerate

Stretch wraps secured 51.35% of the North America shrink and stretch film market share in 2025, underscoring their entrenched use for pallet load containment in conventional warehouses. The North America shrink and stretch film market size tied to stretch wraps is forecast to edge forward at roughly 3.08% CAGR through 2031 as downgauging and automation sustain baseline demand. Parallelly, stretch hoods record a stronger 3.74% CAGR as robotic palletizers require uniform tension and film breathability. Sigma Plastics Group’s 2024 purchase of Stalwart’s stretch-film assets bolsters supply depth and signals strategic concentration around high-run SKUs. Sleeve labels and bags segments confront greater sustainability headwinds yet find respite in tamper-evident and recyclable PET-compatible innovations.

Adoption curves demonstrate that high-volume distributors justify hood capital expenditures once yearly pallet throughput exceeds 300,000. Hoods deliver superior puncture resistance that minimizes rewrap labor, although higher unit film cost restricts penetration among small to mid-sized shippers. Sleeve label buyers increasingly specify wash-off coatings that meet bottle-to-bottle PET guidelines, pushing converters toward solvent-free gravure inks. As state fees escalate, interest grows in compostable cellulosic shrink bags for specialty meat processors, adding differentiated avenues to the North America shrink and stretch film market.

By Material: LLDPE Dominates, Recycled Resin Gains Momentum

LLDPE retained a 62.35% share during 2025 as its high elongation and tear strength suit machine wraps for 1-ton pallets. Recycled and bio-based resins, however, are advancing at a 3.99% CAGR, the fastest among material options, aided by Nova Chemicals securing FDA food-contact clearance for 35% PCR LLDPE blends. The North America shrink and stretch film market size attributable to PCR grades remains modest yet enjoys premium pricing that offsets throughput de-rates during extrusion.

PVC’s optical clarity maintains relevance for high-shrink sleeve labels on contoured beverage containers, though its chlorine content draws regulatory scrutiny and hinders landfill diversion. PET shrink films anchor premium pharmaceuticals that demand scuff resistance and oxygen barrier, justifying their cost profile. The imminent PFAS phase-outs push research toward fluorine-free friction reducers, while post-industrial scrap recycling loops gain traction among integrated converters striving to meet 25% recycled-content pledges by 2027.

By End-Use Industry: E-Commerce Surges Past Logistics Baseline

Food and beverage processors consumed 37.45% of film tonnage in 2025, validating the North America shrink and stretch film market’s reliance on staples such as frozen entrées and multipack beverages. Nonetheless, e-commerce fulfillment centers are projected to record the steepest 3.78% CAGR through 2031, with Amazon, Target, and third-party logistics players retrofitting depots with orbital wrappers that demand consistent film roll geometry. Pharmaceutical and nutraceutical packagers elevate demand for tamper-evident shrink bands with forensic overt and covert markers, while cannabis cultivators uptake cold-chain films engineered for −20 °C storage.

Retailers’ 15% packaging-reduction goals accelerate downgauging across consumer goods bundles, nudging line speeds higher and necessitating more robust cling additives. Industrial producers of construction materials keep steady consumption rates, but rising steel and lumber exports to Mexico bolster cross-border wrap shipments that now account for 7% of regional film demand. Together, these factors diversify revenue streams within the North America shrink and stretch film market.

By Packaging Application: Pallet Unitization Prevails, Security Sleeves Climb

Pallet unitization represented 51.28% of overall volume in 2025, reaffirming stretch wrap’s ubiquity across inbound supply networks. The North America shrink and stretch film market size tied to pallet unitization is projected to add roughly USD 592 million by 2031 as automated guided vehicles necessitate tight load containment. Tamper-evident sleeve labeling, posting a 3.92% CAGR, benefits from OTC drug compliance deadlines and beverage brand protection against counterfeit refills. Multipack collation film faces headwinds from paper overwrap substitution, yet heat-shrink bundles remain favored for high-speed canning lines where moisture resistance prevails.

Sleeve-label growth leans heavily on recyclable PET structures, with Klöckner Pentaplast’s SmartCycle platform enabling in-process bottle recycling without delabeling. Secondary retail packaging notices a pivot to mono-material PE films that align with store drop-off recycling infrastructure. Collectively, these shifts broaden application diversity, underpinning sustainable gains for the North America shrink and stretch film market.

Geography Analysis

The United States accounted for 77.55% of revenue in 2025, underscoring its outsized warehousing footprint, dominant processed-food sector, and central role in e-commerce logistics. Capital outlays by Amazon and Walmart, alongside 50 new regional cold-storage projects, drive incremental machine-grade stretch demand that lifts the North America shrink and stretch film market. State-specific PFAS bans in California, New York, and New Hampshire complicate product formulation, prompting larger converters to operate multi-resin extrusion hubs that supply tailored SKUs.

Canada, albeit smaller, posts a comparable 3.85% CAGR thanks to strong grocery consolidation and rapidly scaling online retail in Ontario, British Columbia, and Quebec. Federal mandatory plastics reporting scheduled for September 2025 introduces cross-enterprise data infrastructure costs but also encourages PCR commitments that spur investment in reclaim capacity. Provincial extended producer responsibility schemes incentivize mono-material films, and converters offering low-density blends with ≥30% PCR content win retailer buy-ins.

Mexico’s near-shoring upturn indirectly supports the North America shrink and stretch film market, as U.S. exporters ship higher pallet volumes southbound under USMCA provisions. Although Mexico purchases most film domestically, increased cross-border trade elevates demand for load containment and humidity-resistant hoods on northbound electronics and automotive components. Harmonized customs processing times shorten lead cycles, supporting just-in-time stretch film replenishment programs executed by integrated distributors.

Competitive Landscape

Market concentration remains moderate, with Sealed Air, Amcor, and Sigma Plastics Group commanding sizable yet not dominant shares. Sealed Air’s USD 1.2 billion Liquibox acquisition enhances vertical integration from resin to liquid packaging equipment, deepening technical service reach.[3]Sealed Air Corporation, “Sealed Air completes acquisition of Liquibox,” sealedair.com Amcor’s pending USD 8.43 billion merger with Berry Global signals the pursuit of scale synergies in raw-material procurement and a broader sustainable film portfolio. Patent litigation over seven-layer cling technology, as seen in Stretch Cling Film Holdings v. Inteplast Group, injects uncertainty into advanced film rollouts, which could curtail innovation pacing among smaller outfits.

Strategically, leading firms differentiate via PCR incorporation, PFAS-free coating systems, and on-press downgauging analytics that help customers cut film weight by up to 15%. Sigma Plastics Group’s purchase of Stalwart’s wrap assets in 2024 exemplifies selective consolidation to fill product-line gaps and extend geographic reach. Regional converters counterbalance through agile, low-volume custom runs and localized technical support, particularly for Canadian cannabis shippers who require compliant yet odor-barrier films. Overall, customer stickiness hinges on joint process optimization as supply chains digitize and sustainability scorecards sway procurement.

Looking ahead, automation-ready stretch hoods and recyclable barrier sleeves remain white-space opportunities, particularly as Amazon, UPS, and national grocers configure next-generation distribution hubs. Converters able to validate 35-50% PCR content without throughput penalties will capture share under state eco-fee frameworks, advancing their standing in the North America shrink and stretch film market.

North America Shrink And Stretch Film Industry Leaders

Sigma Plastics Group LLC

Amcor Group GmbH

Sealed Air Corporation

Klöckner Pentaplast Group

Coveris Holdings S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Packaging Dive reported ten manufacturers expanding North American rPET and film capacity to meet sustainability mandates.

- January 2025: Klöckner Pentaplast introduced SmartCycle PET-compatible shrink sleeves that recycle seamlessly with bottles .

- January 2025: FDA confirmed that 35 PFAS food-contact notifications are no longer effective, tightening compliance windows .

- October 2024: Klöckner Pentaplast unveiled two recyclable barrier flow-wrap films capable of 75% weight reduction versus legacy solutions.

North America Shrink And Stretch Film Market Report Scope

The scope of the study characterizes the shrink and stretch film market based on the raw materials, including LDPE, LLDPE, PVC, PET, and other materials used across various end-use industries such as food, beverages, pharmaceuticals, consumer, industrial, and other end-use industries across the two countries. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period.

The North American shrink and stretch film market is segmented by product type (hoods, wraps, and sleeve labels), material (low-density polyethylene (LDPE) and linear low-density polyethylene (LLDPE), polyvinyl chloride (PVC), and polyethylene terephthalate (PET), and other materials), end-use industry (food and beverage, consumer goods, pharmaceutical, industrial, and other end-use industries), and country (United States and Canada). The report offers market sizes and forecasts in terms of value (USD) for all the above-mentioned segments.

| Hoods |

| Wraps (Machine and Hand) |

| Sleeve Labels |

| Bags and Pouches |

| LDPE |

| LLDPE |

| PVC |

| PET |

| Recycled and Bio-based Resins |

| Food and Beverage |

| Consumer Goods |

| Pharmaceutical and Healthcare |

| Industrial and Logistics |

| E-commerce Fulfilment Centers |

| Pallet Unitization |

| Bundling and Multipack |

| Tamper-evident Sleeve Labeling |

| Secondary Retail Packaging |

| United States |

| Canada |

| Mexico |

| By Product Type | Hoods |

| Wraps (Machine and Hand) | |

| Sleeve Labels | |

| Bags and Pouches | |

| By Material | LDPE |

| LLDPE | |

| PVC | |

| PET | |

| Recycled and Bio-based Resins | |

| By End-use Industry | Food and Beverage |

| Consumer Goods | |

| Pharmaceutical and Healthcare | |

| Industrial and Logistics | |

| E-commerce Fulfilment Centers | |

| By Packaging Application | Pallet Unitization |

| Bundling and Multipack | |

| Tamper-evident Sleeve Labeling | |

| Secondary Retail Packaging | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America shrink and stretch film market in 2026?

It reached USD 5.52 billion and is projected to grow 3.69% annually to 2031.

Which end-use segment is expanding fastest?

E-commerce fulfillment centers, supported by warehouse automation, are pacing at a 3.78% CAGR.

What material holds the largest share today?

LLDPE dominates with 62.35% volume thanks to its balance of stretch and puncture resistance.

How are regulations influencing product development?

State PFAS bans and extended producer responsibility programs are steering converters toward PCR and PFAS-free mono-material films.

Which application shows the strongest growth?

Tamper-evident sleeve labeling, driven by FDA and beverage brand security needs, is climbing at 3.92% CAGR.

Who are the leading companies?

Sealed Air, Amcor, and Sigma Plastics Group top the field, with ongoing consolidation shaping competitive dynamics.

Page last updated on: