North America Pharmaceutical Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

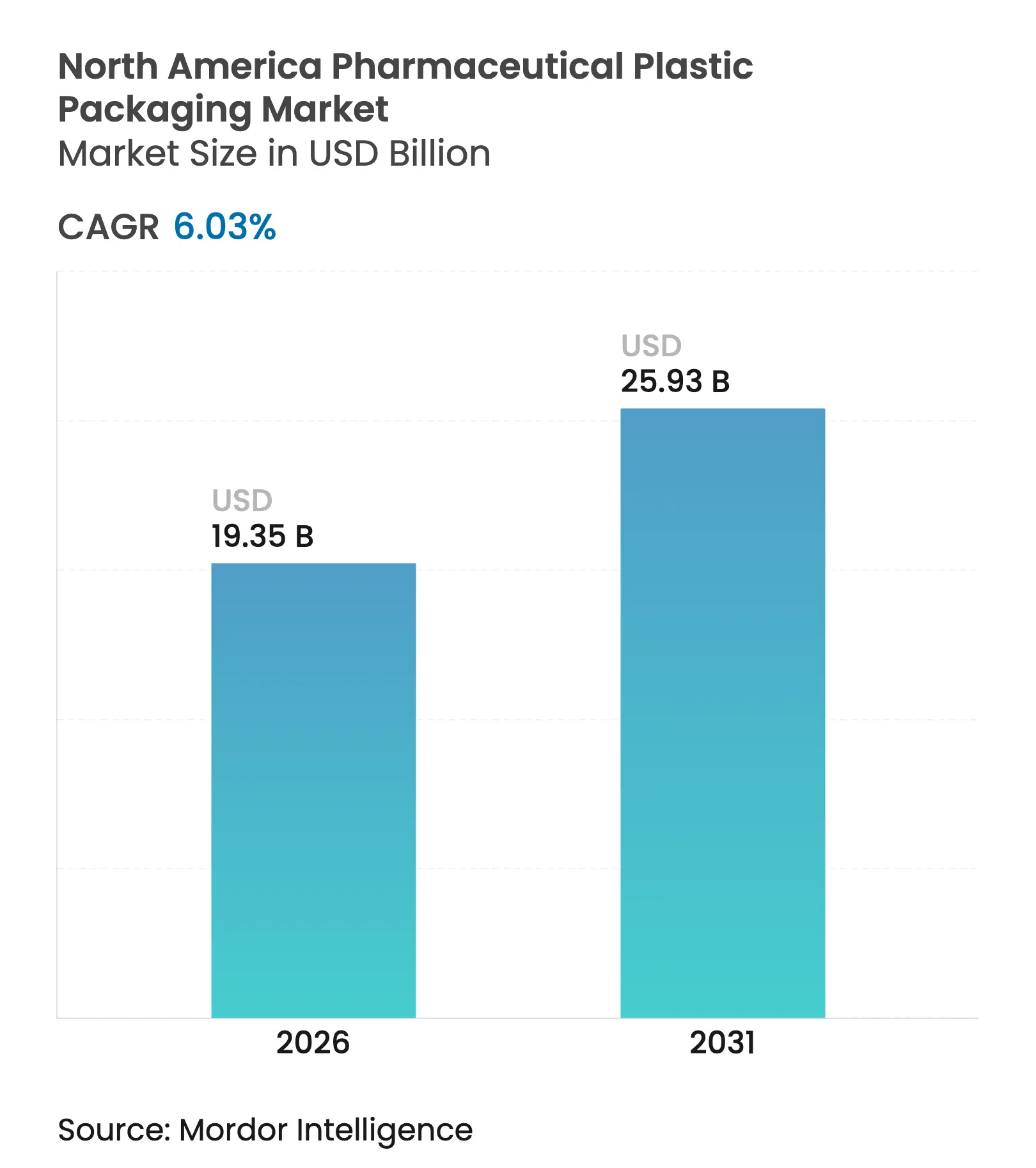

| Market Size (2026) | USD 19.35 Billion |

| Market Size (2031) | USD 25.93 Billion |

| Growth Rate (2026 - 2031) | 6.03 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Pharmaceutical Plastic Packaging Market Analysis by Mordor Intelligence

The North America Pharmaceutical Plastic Packaging Market size was valued at USD 18.25 billion in 2025 and estimated to grow from USD 19.35 billion in 2026 to reach USD 25.93 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). A decisive shift from glass to lightweight plastics, coupled with firm child-resistant closure rules and the spread of home-care therapies, is steering growth. Biologic drug developers are accelerating demand for sterile, ready-to-fill plastic systems that lower contamination risk and simplify cold-chain logistics. Expanded reimbursement for self-administration devices is generating fresh opportunities for nasal, inhalation, and autoinjector formats. Meanwhile, sustainability mandates are nudging producers toward post-consumer recycled (PCR) and bio-based resins, even as supply shortages for medical-grade rPET and HDPE increase sourcing complexity. Moderate industry fragmentation continues, yet the Amcor–Berry Global merger signals an era of scale-driven R&D investments and more pronounced competitive boundaries.

Key Report Takeaways

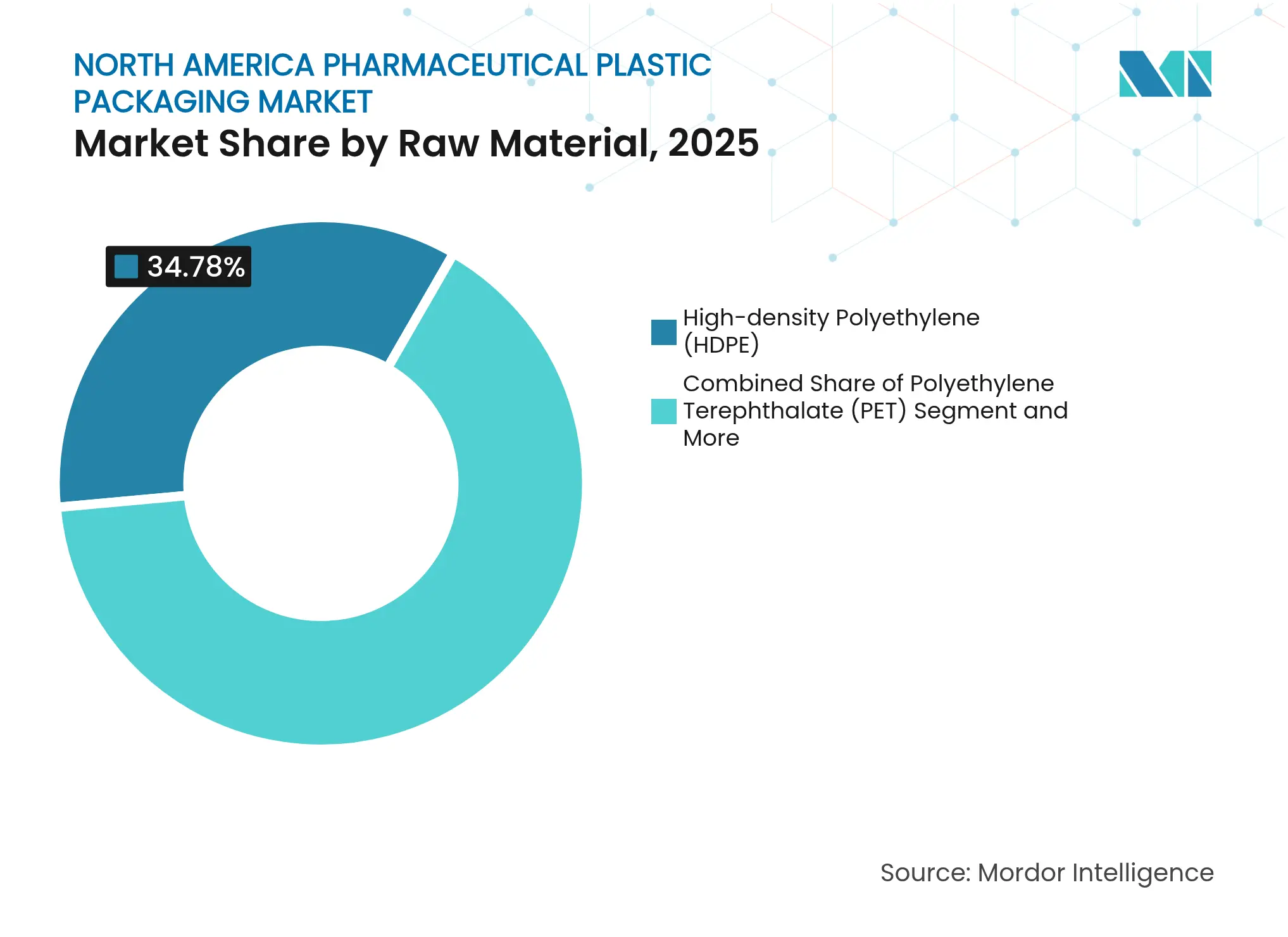

- By raw material, HDPE led with 34.78% of the North America pharmaceutical plastic packaging market share in 2025, while PET is projected to post the fastest 7.47% CAGR through 2031.

- By product type, liquid bottles captured 39.72% of revenue in 2025; nasal spray devices are forecast to grow at 7.26% CAGR to 2031.

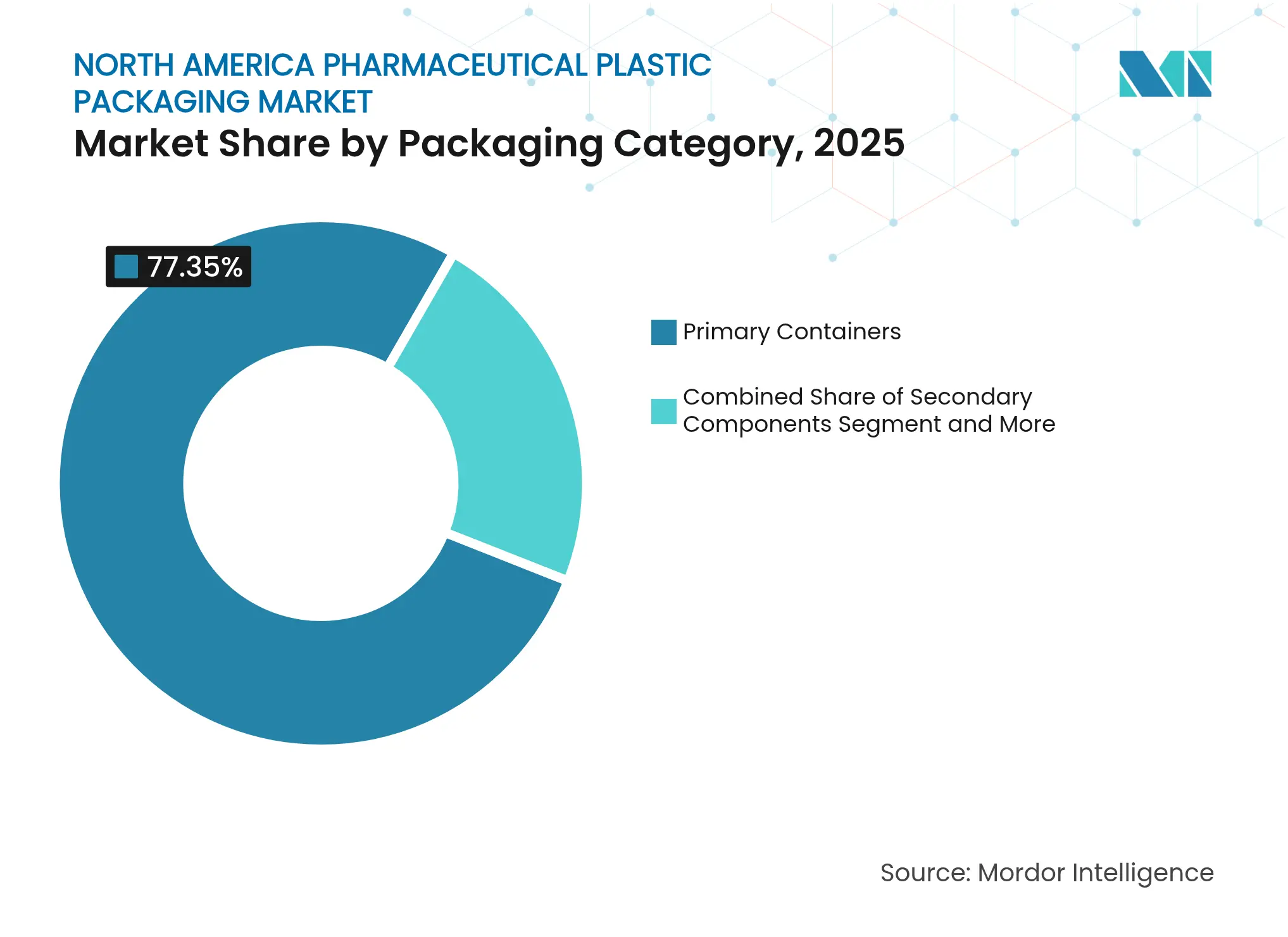

- By packaging category, primary containers held 77.35% revenue in 2025, yet secondary components are expected to expand at 7.79% CAGR.

- By drug-delivery route, oral formats commanded 44.02% share of the North America pharmaceutical plastic packaging market size in 2025; nasal/inhalation packaging is rising at 7.61% CAGR.

- By end-user, branded pharmaceutical companies generated 39.54% of demand in 2025, whereas CDMOs exhibited the highest 7.74% CAGR.

- By country, the United States accounted for 75.88% of 2025 revenue, while Canada is projected to advance at 7.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Pharmaceutical Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Demand for child-resistant closures in pediatric Rx drugs Demand for child-resistant closures in pediatric Rx drugs | +0.8% | North America, with strongest impact in United States | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:North America, with strongest impact in United States | Impact Timeline:Short term (≤ 2 years) |

Shift from glass to lightweight, shatter-proof plastics Shift from glass to lightweight, shatter-proof plastics | +1.2% | Global, with early adoption in North America | Medium term (2-4 years) | |||

Surge in sterile, ready-to-fill formats for biologics Surge in sterile, ready-to-fill formats for biologics | +1.4% | North America and EU, spill-over to emerging markets | Medium term (2-4 years) | |||

Growth of home-care/self-administration therapies Growth of home-care/self-administration therapies | +0.9% | North America, with expansion to developed markets | Long term (≥ 4 years) | |||

Adoption of PCR and bio-based resins to meet ESG targets Adoption of PCR and bio-based resins to meet ESG targets | +0.7% | North America and EU, driven by regulatory mandates | Long term (≥ 4 years) | |||

Expansion of digital-printed smart packs for anti-counterfeit Expansion of digital-printed smart packs for anti-counterfeit | +0.6% | Global, with North America leading implementation | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Sterile, Ready-to-Fill Formats for Biologics

Biologic manufacturers increasingly favor pre-sterilized plastic packaging that shortens filling lines and protects high-value actives throughout cold-chain movement. Regulatory pathways for biologics have streamlined in the United States, propelling demand for systems such as Thermo Fisher’s Fill Finish Solution, which maximizes drug recovery and ensures helium-tested bag integrity. [1]Thermo Fisher Scientific, “Fill Finish Solution – US,” thermofisher.com West Pharmaceutical Services’ Ready Pack™ kits add value for early-stage programs by eliminating on-site sterilization steps and minimizing waste. Rapid uptake of these platforms is trimming time-to-market for temperature-sensitive therapies and reinforcing the competitiveness of the North America pharmaceutical plastic packaging market.

Shift from Glass to Lightweight, Shatter-Proof Plastics

Weight savings of up to 60% versus glass translate into lower freight emissions and fewer breakage-related recalls. Polypropylene vials produced via blow-fill-seal technology now replace glass in large-volume parenterals, improving chemical resistance and reducing particulate risk. Drug Plastics reports growing customer migration to plastic bottles for both cost and safety gains. [2]Drug Plastics & Glass Co., “Glass Bottles vs Plastic Bottles – Lower Cost Gives Plastic the Advantage,” drugplastics.com The North America pharmaceutical plastic packaging market is therefore positioned to capitalize on lower logistics costs and enhanced patient safety profiles.

Growth of Home-Care/Self-Administration Therapies

Post-pandemic consumer comfort with at-home treatment, paired with the fast growth of GLP-1 drugs, is reshaping packaging design. Sharp Packaging has expanded capacity for oral thin films and personalized packs that aid dosing outside clinics. BD’s Neopak™ XSi™ syringe reduces subvisible particle counts, supporting safe self-injection. User-friendly formats strengthen therapy adherence and lift volumes within the North America pharmaceutical plastic packaging market.

Adoption of PCR and Bio-Based Resins to Meet ESG Targets

Regulators now require recycled content, yet medical-grade rPET and HDPE remain scarce, adding price premiums of 20-30%. Innovations such as UPM’s wood-based plastic bottle show the feasibility of sustainable solutions that meet pharmaceutical purity standards. Avient’s Mevopur™ bio-based compounds cut carbon footprints up to 85%. Such material progress is essential for the long-term competitiveness of the North America pharmaceutical plastic packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

API/plastic incompatibilities API/plastic incompatibilities | -0.9% | Concentrated in U.S. biotech hubs | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Concentrated in U.S. biotech hubs | Impact Timeline:Medium term (2-4 years) |

Complex U.S.–Canada EPR mandates Complex U.S.–Canada EPR mandates | -0.7% | Varies by province and state | Short term (≤ 2 years) | |||

Shortage of medical-grade rPET/HDPE Shortage of medical-grade rPET/HDPE | -1.1% | North America and EU | Medium term (2-4 years) | |||

Inflation-driven resin price volatility Inflation-driven resin price volatility | -0.8% | Global, with acute North American impact | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

API/Plastic Chemical Incompatibilities in Novel Drugs

Highly active biologics and emerging modalities such as mRNA vaccines display sensitivity to common polymer additives, complicating container selection. Revisions to USP <661.1> and <661.2> underscore tougher extractables standards. Small biotech firms face six-to-twelve-month launch delays when compatibility data are insufficient, tempering growth in the North America pharmaceutical plastic packaging market.

Shortage of Medical-Grade rPET/HDPE Supply Chains

Robust demand from beverage brands and new statutory recycled-content targets strain limited purification streams. Medical-grade rPET trades at premiums that jeopardize margins for generic drug makers. Dual-sourcing strategies elevate inventory costs and slow progress toward circular-economy goals in the North America pharmaceutical plastic packaging market.

Segment Analysis

By Raw Material: PET Challenges HDPE Dominance

HDPE contributed 34.78% of revenue in 2025, owing to chemical inertia and affordability. PET, bolstered by 7.47% CAGR, is favored for transparency and high moisture-barrier performance. The North America pharmaceutical plastic packaging market benefits as PET’s recyclability supports ESG scorecards. Polypropylene remains indispensable for high-temperature sterilization, whereas LDPE satisfies flexible dropper needs. Premium cyclic olefin copolymers address low-extractables requirements in biologics. The nascent PCR stream shows rapid but supply-constrained uptake, reflecting EPR deadlines in Canada.

Emerging grades of bio-based PET could further accelerate PET adoption. Suppliers emphasize migration-tested masterbatches to keep extractables within USP limits. Price differentials between virgin and recycled PET narrowed during 2025, improving project ROIs. Strategic procurement alliances are increasingly common as drug firms secure long-term capacity for food-contact-grade rPET. HDPE converters respond with lightweighting innovations and tethered cap solutions to retain volumes within the North America pharmaceutical plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Nasal Devices Outpace Legacy Formats

Liquid bottles delivered 39.72% of 2025 sales, reflecting steady prescription and OTC cough remedies. However, nasal spray devices are advancing at 7.26% CAGR, capturing allergy, migraine, and rescue-therapy launches. Enhanced metered-dose accuracy, combined with patient aversion to needles, spurs adoption. Prefillable syringes and cartridges capture self-injecting diabetics and GLP-1 users. Vials and ampoules stay relevant for hospital injectables, though polypropylene formats steadily displace glass to cut breakage. Closures and lids integrate RFID-enabled seals that aid Drug Supply Chain Security Act compliance.

Demand for ophthalmic droppers benefits from aging demographics and dry-eye formulation growth. Unit-dose pouches support hospital compounding and reduce microbial contamination risk. Producers add multi-layer coatings to prevent oxygen ingress in peroxide-sensitive drugs. With regulatory appetite for serialized smart packs intensifying, product-type diversification will keep the North America pharmaceutical plastic packaging market on a robust upward track.

By Packaging Category: Secondary Components Drive Future Value

Primary containers delivered 77.35% of the 2025 turnover and anchor regulatory filings. Nonetheless, secondary components will rise 7.79% CAGR on the back of tamper-evidence and track-and-trace rules. Child-resistant and senior-friendly caps see double-digit innovation investment as demographics shift. Smart closures embedding time-temperature indicators emerge as value-added differentiators.

Producers of tertiary shippers integrate phase-change materials to extend cold-chain windows for biologics. IoT-enabled pallets provide real-time location and vibration alerts, mitigating loss events. Software-defined serialization platforms transform carton and case printing lines, supplying granular visibility across the North America pharmaceutical plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Drug-Delivery Route: Nasal/Inhalation Rising

Oral formats held 44.02% of demand in 2025, yet pipeline emphasis on neuro-psychiatric and emergency nasal sprays lifts the inhalation segment at 7.61% CAGR. Auto-injector-ready parenteral kits address home-administered GLP-1 and oncology biologics. Ophthalmic packaging evolves with preservative-free valves, while transdermal patches gain prominence in pain and hormone therapy markets.

The nasal upswing benefits polypropylene and COC suppliers designing barrier reservoirs that support propellant-free formulations. Meanwhile, growth in advanced parenteral devices prompts partnerships between polymer makers and autoinjector OEMs. Such alignment ensures the North America pharmaceutical plastic packaging market retains technological leadership.

By End-user: CDMOs Gain Share

Branded pharma accounted for 39.54% of purchases in 2025, prioritizing premium features and short lead times. CDMOs, expanding at 7.74% CAGR, absorb outsourced development and secondary packaging jobs as drug owners safeguard focus on R&D pipelines. Catalent and PCI Services upscale sterile filling and late-stage customization suites to capture this outsourcing wave.

Generic manufacturers counter margin pressure through high-speed, fully automated bottling lines. Biotech innovators, especially in cell and gene therapy, demand cryo-compatible containers that maintain viability at −196 °C. This segmented mix fosters resilient, service-oriented growth across the North America pharmaceutical plastic packaging market.

Geography Analysis

The United States generated 75.88% of 2025 revenue, underpinned by FDA mandates and USD 160 billion in domestic manufacturing outlays scheduled for 2025. Facility expansions by Eli Lilly and Novo Nordisk intensify demand for injectable packaging lines. High adoption of serialization software following DSCSA deadlines cements local converter relationships and accelerates digital-print investments.

Canada, projected at 7.68% CAGR, incentivizes recycled-content inclusion through province-level regulations that penalize non-compliant packs. Logistics leaders like UPS bolster cross-border cold-chain capacity via the Andlauer acquisition, easing biologics distribution hurdles. Rising investment in advanced resin supply channels positions Canada as a strategic sustainability test bed.

Mexico delivers emerging-market upside, buoyed by 5.5% annual growth in packaging machinery imports and a 29.3% share for plastics in its materials mix. Near-shoring trends draw U.S. pharma brands to Mexican fill-finish sites, spurring demand for PCR-ready resin allocations. Harmonization of technical standards with U.S. regulations lowers compliance friction, positioning Mexico as an efficient extension of the North America pharmaceutical plastic packaging market footprint.

Competitive Landscape

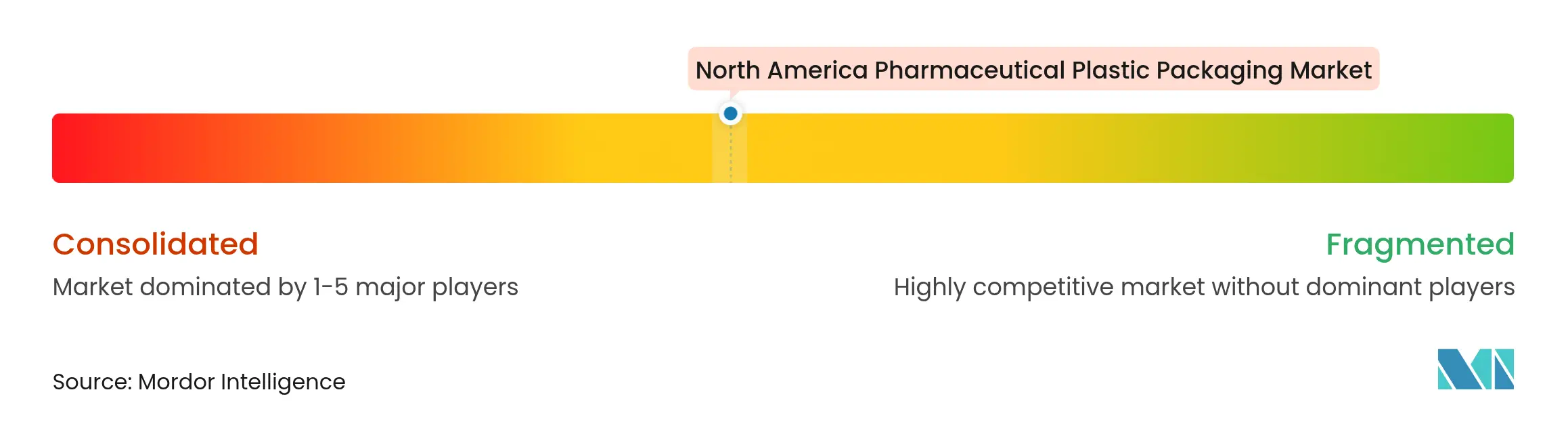

Market Concentration

The North America pharmaceutical plastic packaging market remains moderately fragmented, yet consolidation is accelerating. The 2025 Amcor–Berry Global merger forms a USD 3 billion cash-flow powerhouse aiming for USD 650 million in synergies. Scale advantages facilitate capital-intensive barrier-film research and expedite commercial rollout of PCR blends.

Gerresheimer’s USD 180 million Georgia expansion adds 18,000 m² of cleanroom capacity for inhalers and autoinjectors, deepening local supply resilience. AptarGroup continues to leverage proprietary nasal-spray valve designs, while West Pharmaceutical Services invests in data-rich elastomer seals for combination devices. Start-ups focusing on printed electronics for smart closures attract venture funding, illustrating technology galvanization across the North America pharmaceutical plastic packaging industry.

Competitive differentiation shifts from pure cost toward sustainability credentials, regulatory literacy, and digital-traceability offerings. Patent filings in automated admixture systems and RFID-enabled lids underscore the strategic value of heightened drug integrity. Market entrants capable of pairing primary containers with real-time data capture stand to win contracts as pharma clients prioritize supply-chain transparency.

North America Pharmaceutical Plastic Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor plc closed its all-stock combination with Berry Global, targeting USD 650 million in annual synergies by FY28.

- February 2025: Avient showcased Mevopur™ bio-based polymer solutions containing up to 100% bio-based content.

- January 2025: SCHOTT Pharma reported EUR 899 million in FY 2023 sales, with high-value solutions at 48% of revenue.

- January 2025: Gerresheimer AG began an 18,000 m² expansion of its Peachtree City, Georgia site, investing USD 180 million to add inhaler and autoinjector capacity.

- December 2024: TricorBraun agreed to acquire Veritiv’s Rigid Containers Business, broadening rigid pharmaceutical packaging options.

- October 2024: UPM, SELENIS, and BORMIOLI PHARMA launched the first pharma bottle partially made of wood-based plastics.

- October 2024: Nutra-Med, backed by GenNx360, acquired Legacy Pharma Solutions to strengthen bottling and blistering services.

Table of Contents for North America Pharmaceutical Plastic Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Demand for child-resistant closures in pediatric Rx drugs

- 4.2.2Shift from glass to lightweight, shatter-proof plastics

- 4.2.3Surge in sterile, ready-to-fill formats for biologics

- 4.2.4Growth of home-care/self-administration therapies

- 4.2.5Adoption of PCR and bio-based resins to meet ESG targets

- 4.2.6Expansion of digital-printed smart packs for anti-counterfeit

- 4.3Market Restraints

- 4.3.1API/plastic chemical incompatibilities in novel drugs

- 4.3.2Complex U.S.–Canada EPR and recycling mandates

- 4.3.3Shortage of medical-grade rPET/HDPE supply chain

- 4.3.4Inflation-driven resin price volatility

- 4.4Industry Value Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Industry Attractiveness – Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Impact of Macroeconomic Factors on the Market

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1By Raw Material

- 5.1.1Polypropylene (PP)

- 5.1.2Polyethylene Terephthalate (PET)

- 5.1.3High-density Polyethylene (HDPE)

- 5.1.4Low-density Polyethylene (LDPE)

- 5.1.5Cyclic Olefin Copolymer (COC)

- 5.1.6Post-consumer Recycled (PCR) Plastics

- 5.2By Product Type

- 5.2.1Bottles – Solid-oral

- 5.2.2Bottles – Liquid

- 5.2.3Vials and Ampoules

- 5.2.4Prefillable Syringes and Cartridges

- 5.2.5Nasal Spray Devices

- 5.2.6Dropper and Ophthalmic Containers

- 5.2.7Pouches and Sachets

- 5.2.8Closures and Lids

- 5.3By Packaging Category

- 5.3.1Primary Containers

- 5.3.2Secondary Components (closures, liners)

- 5.3.3Tertiary and Protective Systems

- 5.4By Drug-delivery Route

- 5.4.1Oral

- 5.4.2Parenteral

- 5.4.3Ophthalmic

- 5.4.4Nasal/Inhalation

- 5.4.5Topical/Transdermal

- 5.5By End-user

- 5.5.1Branded Pharma

- 5.5.2Generic Pharma

- 5.5.3Biotech and Cell-/Gene-therapy Firms

- 5.5.4Contract Development and Manufacturing Orgs (CDMOs)

- 5.6By Country

- 5.6.1United States

- 5.6.2Canada

- 5.6.3Mexico

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Amcor PLC

- 6.4.2Berry Global Group Inc.

- 6.4.3Gerresheimer AG

- 6.4.4AptarGroup Inc.

- 6.4.5West Pharmaceutical Services Inc.

- 6.4.6Silgan Holdings Inc.

- 6.4.7Nipro Corporation

- 6.4.8Schott Pharma AG & Co. KG

- 6.4.9SGD Pharma SAS

- 6.4.10Stevanato Group S.p.A.

- 6.4.11Comar LLC

- 6.4.12Tekni-Plex Inc.

- 6.4.13Drug Plastics & Glass Company Inc.

- 6.4.14Pretium Packaging LLC

- 6.4.15Bormioli Pharma S.p.A.

- 6.4.16Alpha Packaging Inc.

- 6.4.17Placon Corporation

- 6.4.18Alpla Werke Alwin Lehner GmbH

- 6.4.19Huhtamaki Oyj

- 6.4.20CCL Industries Inc.

- 6.4.21Wipak Oy

- 6.4.22Romaco Pharmatechnik GmbH

- 6.4.23Plastipak Holdings Inc.

- 6.4.24PakTech LLC

- 6.4.25Catalent Pharma Solutions

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1White-Space and Unmet-Need Assessment

North America Pharmaceutical Plastic Packaging Market Report Scope

Plastic is a favored choice for pharmaceutical packaging due to its applicability, durability, flexibility, and sustainability. In pharmaceutical packaging, plastic bottles are crafted from various materials, such as polyvinyl chloride, polyethylene, polypropylene, and polystyrene. The industry prioritizes transparent, lightweight, and durable plastics for storage and marketing. Beyond bottles, plastics play a pivotal role in packaging blister packs, sachets, prefilled syringes, inhalers, parenteral solution pouches, and more.

The North America Pharmaceutical Plastic Packaging market is segmented by raw material (polypropylene, polyethylene terephthalate, low-density polyethylene, high-density polyethylene, and other raw materials), product type (solid containers, dropper bottles, nasal spray bottles, liquid bottles, oral care, pouches, vials and ampoules, cartridges, syringes, caps and closures, and other products types), and country (United States and Canada). the market sizes and forecasts are provided in terms of value (USD) for all the above segments.