Lidding Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.59 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

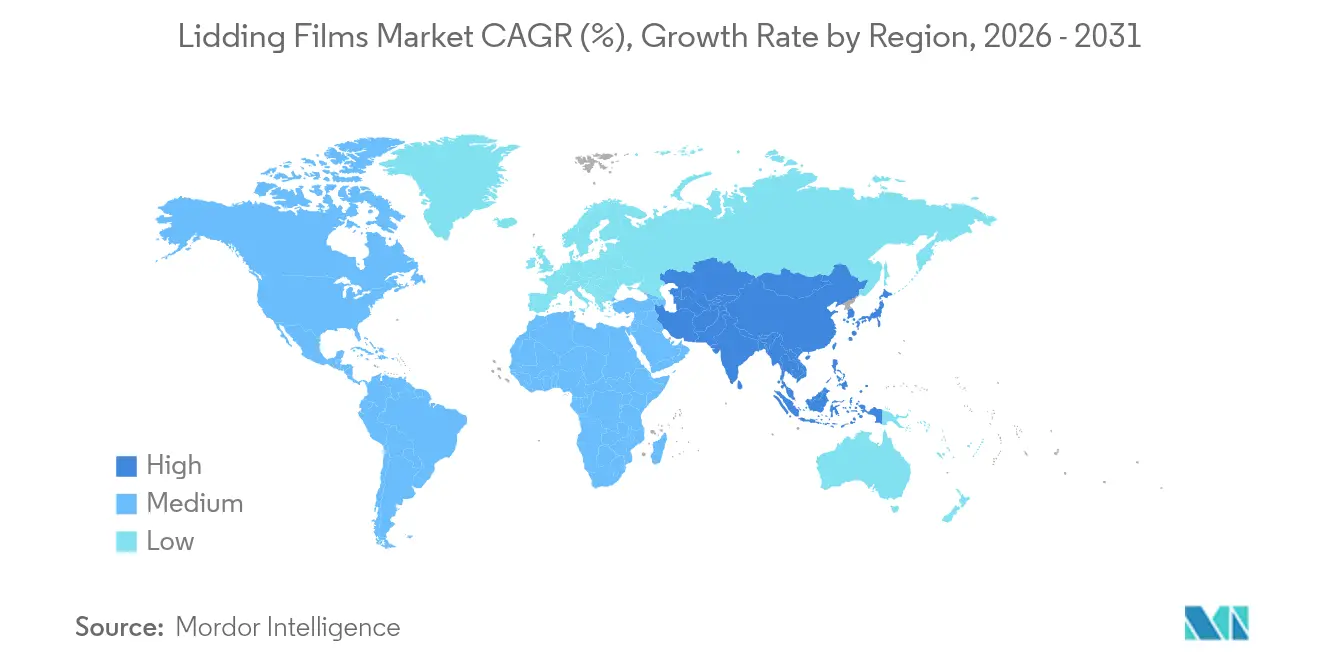

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

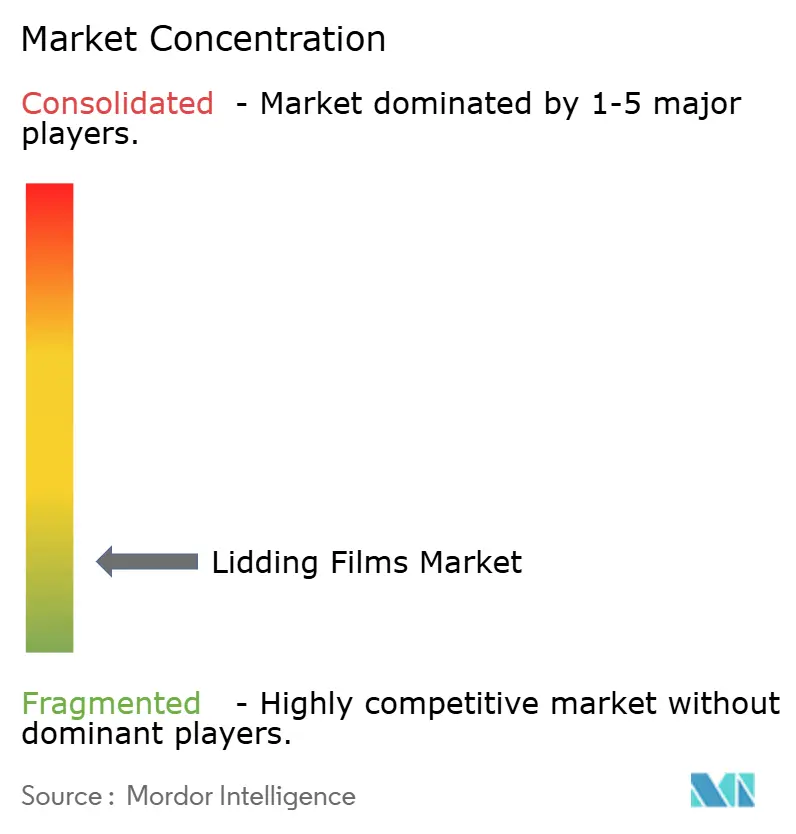

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lidding Films Market Analysis by Mordor Intelligence

The global lidding films market size was valued at USD 4.39 billion in 2025 and estimated to grow from USD 4.59 billion in 2026 to reach USD 5.76 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031). Growing demand for convenience food, tougher sustainability mandates, and the rapid scale-up of meal-kit and e-grocery channels are reshaping performance requirements. Brand owners now specify high-barrier, mono-material structures that extend shelf life while remaining compatible with curbside or closed-loop recycling. Pharmaceutical and personal-care packagers adopt similar platforms to meet tamper-evidence rules and patient-friendly opening forces. Material innovation concentrates on heat-resistant polyethylene terephthalate (PET) and emerging polypropylene (PP) formulations that incorporate post-consumer recycled content without sacrificing seal integrity. Together these factors keep equipment utilization high, encourage investments in advanced coating lines, and sustain steady price realization across regional markets.

Key Report Takeaways

- By product type, high-barrier films accounted for 36.10% revenue in 2025; specialty & biodegradable films are projected to grow at an 8.12% CAGR to 2031.

- By material, PET held 33.85% of 2025 revenue, whereas PP is poised for the fastest 7.48% CAGR over the forecast period.

- By seal type, peelable solutions commanded 47.12% of 2025 revenue, while resealable designs are advancing at a 8.74% CAGR.

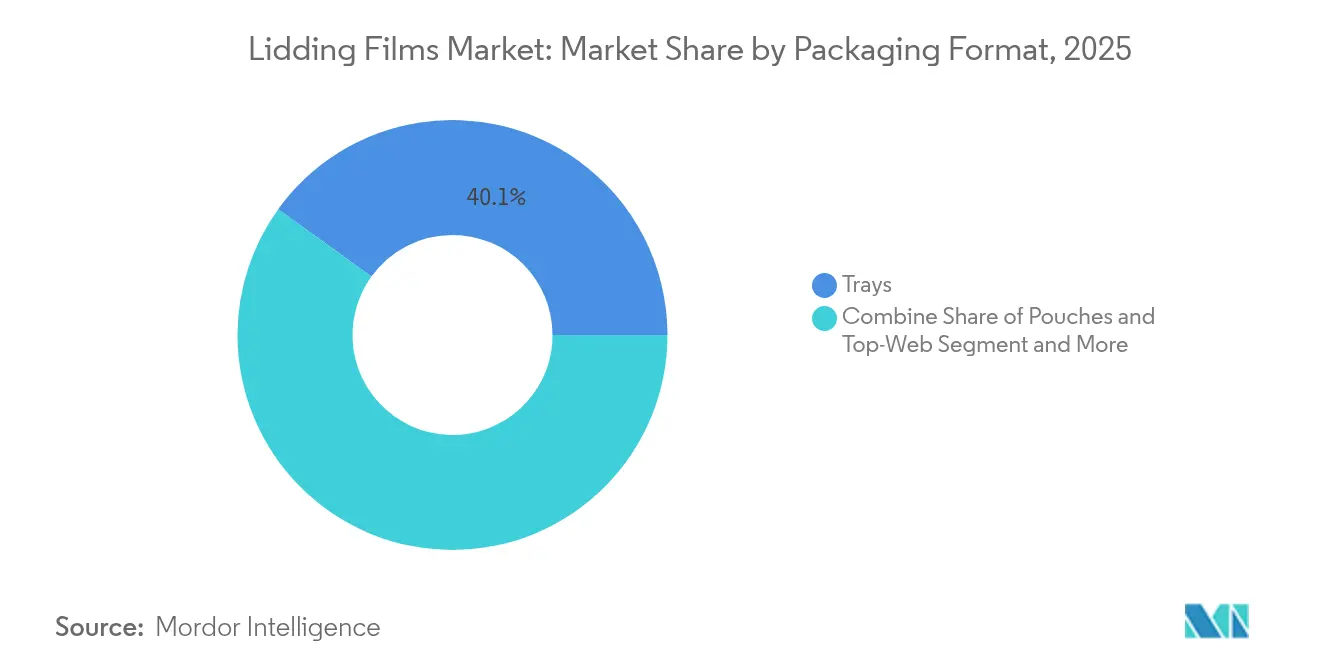

- By packaging format, trays captured 40.05% of 2025 revenue; pouches and top-web formats are on track for an 7.98% CAGR.

- By end-use industry, food applications represented 61.05% of the 2025 total, yet pharmaceutical demand is projected to post a 6.08% CAGR to 2031.

- By geography, Europe led with 30.12% of lidding films market share in 2025 while Asia-Pacific is set to expand at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Lidding Films Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in ready-to-eat and convenience food consumption | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Boom in e-commerce grocery fulfillment | +0.8% | APAC core, spill-over to North America & Europe | Short term (≤ 2 years) |

| Shift to high-barrier and MAP packaging | +0.9% | Global, led by Europe & North America | Long term (≥ 4 years) |

| Meal-kit brands' adoption of peel-and-reseal films | +0.4% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Monomaterial mandates and plastic taxes | +0.7% | Europe & North America, expanding globally | Long term (≥ 4 years) |

| In-line digital printing for late-stage customization | +0.3% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in ready-to-eat and convenience food consumption

Demand for dual-ovenable trays and bowls lifts specifications for heat-resistant PET that retains clarity at 95 °C while still delivering sub-1 cc/m²/day oxygen transmission. Brands also request anti-fog coatings so shoppers can see product quality on shelf. Portion-control formats stimulate investment in precision perforation to enable clean separation without damaging adjacent seals. Established suppliers capitalize on these technical hurdles to defend margins, whereas smaller converters struggle with the capital intensity of multilayer lamination and inline coating lines. As a result, the lidding films market continues to favor participants with deep material-science capabilities and broad application engineering support.

Boom in e-commerce grocery fulfillment

Online grocery channels expose packages to multiple handling cycles and 48- to 72-hour temperature swings. High-barrier lids with enhanced puncture resistance therefore gain traction among seafood, fresh-cut produce, and ready-meal SKUs. [1]Sealed Air Corporation, “Lid Films | FlexLok,” sealedair.com Resealable lids enable consumers to return unused ingredients, reducing food waste and raising brand loyalty. Digital printing on demand lets retailers localize compliance data and seasonal graphics without holding excess inventory. These attributes push film makers to add digital presses and fast-change slitting assets, tilting competitive advantage toward vertically integrated players.

Shift to high-barrier and MAP packaging

Meat and cheese processors deploy modified-atmosphere lines that require lidding films with oxygen rates below 1 cc/m²/day, extending shelf life by three to five days. EVOH-based or metallized structures dominate today, but research into plant-based coatings aims to replicate barrier levels while easing recycling constraints. The complexity of gas-flushing operations and region-specific labeling drives customers to global suppliers able to certify performance across regulatory regimes. Longer shelf life also supports retailers’ shrink-reduction targets, reinforcing demand for premium structures.

Meal-kit brands’ adoption of peel-and-reseal films

Meal-kit operators seek user-friendly openings and reclosures that withstand multi-day storage. Controlled-peel adhesives permit effortless removal without fiber tear yet reseal reliably after partial use. Brands further request variable-data printing for recipe-specific cooking steps, a capability that rewards converters with late-stage digital print modules. Premium price tolerance within the segment lets film makers recoup investments in specialized adhesive chemistries and surface-energy control technologies.

Restraints Impact Analysis of Lidding Films Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock volatility | -0.6% | Global, acute in regions dependent on imports | Short term (≤ 2 years) |

| Recycling restrictions on multilayer laminates | -0.4% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Seal-failure issues on high-speed retort lines | -0.3% | Global, concentrated in high-volume food processing | Medium term (2-4 years) |

| Shortage of high-clarity r-PET resin | -0.2% | North America & Europe, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Petrochemical feedstock volatility

Crude-linked PTA and MEG contracts saw double-digit swings during 2024, lifting European PET resin to EUR 1,150 per ton (USD 1,265 per ton). Polyolefin prices mirrored natural-gas shifts, moving 5-6 cents per pound quarterly Plastics Technology. Smaller converters without hedging tools resort to shorter customer contracts, eroding loyalty and compressing margins when costs spike. Volatility also deters capital expenditure as CFOs weigh uncertain payback periods, moderating near-term additions to lidding film capacity.

Recycling restrictions on multilayer laminates

EU rules class many polyester/olefin combinations as non-recyclable, triggering plastic taxes that can reach EUR 800 per ton. Film makers must either migrate to mono-material designs or fund access to emerging chemical recycling. Both paths require high R&D spend and potential requalification of food-contact compliance—a burden heavier for regional independents lacking dedicated laboratories. [2]UPM Raflatac, “PPWR Plastic Packaging Recyclability,” upmraflatac.com Brands hesitant to pay for next-generation barriers delay full-scale conversions, tempering overall growth of the lidding films market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Lidding Films Market Segment Analysis

By Product Type:

Biodegradable Films Drive InnovationHigh-barrier formats captured 36.10% of 2025 revenue, cementing their role in fresh protein and dairy packs where oxygen rates below 1 cc/m²/day remain critical. Specialty and biodegradable grades, though smaller today, headline the fastest 8.12% CAGR as retailers pledge landfill-free packaging. The lidding films market size for biodegradable offerings is therefore projected to widen rapidly alongside compostable coffee capsule lids. Dual-ovenable structures ride microwave-ready meal popularity, while classic peelable lids stay essential for yogurt and produce tubs.

The switch to plant-based barriers such as Lactips’ plastic-free coating shows how performance parity and recyclability can coexist. Amcor’s fully PP retort pouch further illustrates progress, reporting up to 60% lower carbon footprint relative to foil alternatives. As these solutions achieve scale, the lidding films market share of legacy multilayer laminates is likely to erode, hastening investment in new extrusion and coating assets.

By Material Type:

Polypropylene Gains MomentumPET retained 33.85% of 2025 demand thanks to clarity and mature recovery streams. PP, however, is advancing at a 7.48% CAGR as converters master heat-resistant homopolymers that survive 95 °C retort while blending up to 90% recycled content; Mechanical-recycling alliances promise 30% cost savings and steadier quality, paving the way for wider PP adoption. Polyethylene secures niches needing aggressive chemical resistance, whereas PVC steadily exits food contact use amid regulatory scrutiny.

The lidding films market size attributed to PP is expected to narrow the gap with PET by 2031 as sorting-tech upgrades and digital watermarks improve reclaim purity. Early movers building dedicated PP-recycle loops enjoy stronger customer pull as brand owners aim to publicize circularity milestones.

By Seal Type:

Resealable Solutions AcceleratePeelable lids represented 47.12% of 2025 turnover, favored for dairy cups and produce where consumers demand effortless opening. Resealable designs, however, are pacing a 8.74% CAGR, enabled by controlled-adhesion chemistries that keep oxygen ingress low after first use. Permanent heat seals dominate pharma and nutraceutical SKUs requiring tamper evidence, while cold-seal options address temperature-sensitive treats such as chocolate.

Advanced airborne-ultrasound scanners now embed on converting lines to ensure defect-free seals, reducing complaint rates and reinforcing confidence in light-gauge lids. Given rising single-serve snack culture, the lidding films market share of resealable formats is projected to climb further, especially in e-commerce packs where multiple handlings raise spillage risk.

By Packaging Format:

Pouches Gain TractionRigid trays still held 40.05% revenue in 2025, valued for on-shelf merchandising of meat and ready meals. Yet pouches and top-web applications are on an 7.98% CAGR path, driven by 30–40% material savings, flat-pack shipping efficiency, and fill-and-seal speeds reaching 200 units per minute Coveris. Cups and tubs grow steadily in desserts and dips where stackability matters, while jars and bottles defend premium categories through tactile appeal.

Retailers pressing for source-reduction reward pouch adopters, reinforcing demand for PE or PP mono-material laminates. As lidding films integrate digital print embellishments for brand storytelling, pouches become a canvas for short-run promotions, accelerating their share within the lidding films market.

By End-Use Industry:

Pharmaceutical Growth AcceleratesFood accounted for 61.05% of 2025 revenue, reflecting wide adoption in fresh produce, dairy, and ready meals. Tight migration limits and tamper-evidence standards elevate technical requirements, positioning high-barrier PP and polyamide lids as preferred substrates.

Japan’s positive-list regulation effective June 2025 heightens compliance hurdles, favoring global suppliers with validated analytical support. As healthcare markets look for child-resistant yet senior-friendly openings, specialty seal designs emerge, adding profitable niches within the overall lidding films market.

Geography Analysis

Europe Lidding Films Market

Europe dominated the 2025 landscape with 30.12% revenue, aided by advanced recycling infrastructure and binding targets that require 30% recycled content in PET packs by 2030.. Germany’s updated food-contact rules and the EU-wide ban on PFAS in food packaging effective December 2024 compel rapid material reformulation. Mondi’s EUR 200 million recycled containerboard project in Italy exemplifies strategic investment aligned with circular-economy goals. Large converters leverage premium-price acceptance to roll out mono-material high-barrier lids and secure long-term retail contracts across the region.

APAC Lidding Films Market

Asia-Pacific delivers the fastest 7.12% CAGR as urbanization, rising disposable incomes, and expanding pharma capacity in China and India lift flexible-pack use. India’s flexible packaging turnover hit USD 49 billion in 2023 and is tracking double-digit gains through 2027. China’s modernized food-contact framework mandates extensive documentation, favoring international suppliers with compliance muscle. Japan’s positive-list enforcement from June 2025 sets strict additive limits, again advantaging firms with robust test datasets. Although cost competitiveness remains a regional draw, navigating fragmented regulations requires dedicated legal and technical teams.

North America Lidding Films Market

North America posts steady growth as e-commerce and meal-kit distribution extend cold-chain distance. State-level extended producer responsibility laws such as California SB 343 will restrict recyclability claims from October 2026, nudging brands toward mono-material lids and verified reclaim content. Sealed Air’s pivot to fiber-based solutions under its 2024 reorganization reflects broadening substrate options while retaining performance. Converters add digital printing and automation to support personalized packaging trends, ensuring the lidding films market in the region remains innovative and resilient.

Competitive Landscape

The lidding films industry features fragmented , with top players pursuing acquisitions and R&D to scale sustainable offerings. Amcor finalized its all-stock merger with Berry Global in April 2025, targeting USD 650 million in synergies and broadening its heat-resistant mono-PP portfolio. Mondi followed with a EUR 200 million upgrade to recycled containerboard capacity in Italy, strengthening supply-chain security for European e-commerce customers. Sealed Air reorganized verticals and added fiber solutions, complementing its FlexLok high-barrier lids.

Technology differentiation intensifies as suppliers integrate airborne-ultrasound seal inspection, smart freshness sensors, and inline inkjet lines. Partnerships with chemical recyclers help close material loops, while plant-based barrier specialists provide acquisition targets for cash-rich multinationals. Smaller firms compete in niche biomedical, high-clarity, or compostable segments but face rising capex and compliance thresholds. The aggregated share of the top five converters is estimated near 55%, underscoring a balanced yet consolidating field.

Lidding Films Industry Leaders

Mondi Plc

Amcor PLC

ProAmpac LLC

Huhtamaki Oyj

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Lidding Films Market Companies Covered in this Report

- Amcor plc

- Mondi plc

- Constantia Flexibles

- Winpak Ltd.

- Sealed Air Corp.

- Huhtamaki Oyj

- ProAmpac LLC

- Sonoco Products Co.

- Toray Plastics (America) Inc.

- DuPont Teijin Films

- Clondalkin Group

- Jindal Poly Films Ltd.

- Uflex Ltd.

- Schur Flexibles Group

- Südpack Verpackungen GmbH

- Coveris Holdings

- Sigma Plastics Group

- Toppan Inc.

- TCL Packaging

Recent Industry Developments in Lidding Films Market

- May 2025: Mondi started commercial production on a EUR 200 million recycled-containerboard line in Duino, Italy, adding 420 kilotonnes of sustainable substrate capacity for lidding film converters targeting closed-loop trays.

- April 2025: Amcor completed its all-stock combination with Berry Global, expecting USD 650 million synergies by FY28.

- April 2025: ProAmpac debuted its latest fiber-based and recyclable lidding film solutions at SPC Impact 2025, underscoring commitments to mono-material formats that meet new EPR and recycled-content targets.

- March 2025: Innovia Films commissioned a PVC-free coating line in the United Kingdom, enabling solvent-less, high-clarity over-laminates suitable for peel-and-reseal applications in food and personal-care packaging.

Lidding Films Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the lidding films market as all ready-to-apply mono- or multilayer flexible webs that seal rigid packs, trays, cups, tubs, and similar containers through heat, pressure, or cold-seal adhesives, thereby safeguarding and displaying the packed product. We include plastic, aluminum, and paper-based lids sold to converters and end-of-line packers across food, beverage, pharmaceutical, and personal care applications, as described by Mordor Intelligence analysts.

Scope Exclusions: Films used purely as stretch or shrink overwraps and captive lids manufactured for in-house consumption are not covered.

Segments Covered in This Report

- By Product Type

- Dual-Ovenable Films

- High-Barrier Films

- Specialty/Biodegradable Films

- Peelable Lidding Films

- Other Product Types

- By Material Type

- Polyethylene Terephthalate (PET)

- Polypropylene (PP)

- Polyethylene (PE)

- Polyvinyl Chloride (PVC)

- Polyamide

- Other Material Types

- By Seal Type

- Peelable

- Resealable

- Permanent Heat Seal

- Cold Seal and Self-Adhesive

- By Packaging Format

- Trays

- Cups and Tubs

- Pouches and Top-Web

- Jars and Bottles

- Other Packaging Format

- By End-Use Industry

- Food

- Beverage

- Pharmaceutical

- Personal Care and Cosmetics

- Other End-use Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed converters, tray thermoformers, chilled-meal brands, and procurement managers across North America, Europe, and Asia Pacific. Their insights on run-rate line utilization, barrier-film adoption, and regional ASP dispersion allowed us to reconcile secondary indicators, validate assumed scrap rates, and fine-tune volume splits.

Desk Research

We started by aggregating production, trade, and consumption signals from tier-1 public sources such as UN Comtrade export codes for flexible packaging, Eurostat plastics packaging waste statistics, the US Census Quarterly Plastics Products Survey, and trade-association briefs from the Flexible Packaging Association and AMERIPEN. Patent abstracts from Questel and company financials accessed via D&B Hoovers helped us benchmark converter capacities, while Dow Jones Factiva news feeds traced new line expansions and M&A that shift market share.

Annual reports, 10-Ks, and investor decks from leading film extruders provided average selling price (ASP) direction, which we cross-checked with customs unit-value data. These inputs laid the factual backbone; yet many other open, subscription, and pay-as-you-go sources were also reviewed to round out figures and narrative.

Market-Sizing & Forecasting

A top-down model uses global flexible-packaging output and import-export reconciliations to approximate the demand pool, which is then sense-checked through sampled ASP × volume roll-ups for key suppliers. We layer in market fingerprints, MAP tray penetration, protein meal production, barrier-film share shift, resin price pass-through, and regional convenience-food growth to build scenario cells. A multivariate regression with ARIMA overlays projects the 2025-2030 trajectory, while bottom-up supplier checks close gaps in under-reported regions.

Data Validation & Update Cycle

We triangulate every output against shipment trends, converter order books, and resin demand signals; anomalies trigger an analyst peer review before sign-off. Reports refresh annually, and interim updates follow material events such as capacity additions or regulatory shifts, ensuring clients always receive Mordor's latest view.

How Mordor Intelligence's Lidding Films Market Size Compares to Other Published Estimates

Published figures often diverge because publishers pick different scope boundaries, pricing ladders, or refresh cadences. We acknowledge these inevitable gaps upfront.

Key gap drivers include plastic-only coverage by some firms, inclusion of overwraps by others, and limited geographic focus in a few regional studies. Mordor's disciplined scope, full material coverage, and yearly refresh minimize such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.39 B (2025) | Mordor Intelligence | - |

| USD 3.29 B (2024) | Global Consultancy A | Counts plastics only; omits aluminum and paper lids |

| USD 4.61 B (2024) | Industry Aggregator B | Adds easy-peel overwraps and internal transfer values |

| USD 1.78 B (2023) | Regional Consultancy C | Focuses on food trays within limited Asian markets |

Taken together, the table shows why our balanced, transparent baseline, anchored to clear scope choices and repeatable steps, offers decision-makers the most dependable starting point for strategy and investment.

Key Questions Answered in the Report

What is the current size of the lidding films market?

The lidding films market size reached USD 4.59 billion in 2026 and is projected to climb to USD 5.76 billion by 2031 at a 4.62% CAGR.

Which region leads the lidding films market?

Europe commands the largest 30.12% share, supported by advanced recycling infrastructure and strict circular-economy mandates.

Which product segment is growing the fastest?

Specialty and biodegradable films are the fastest, increasing at an 8.12% CAGR as brands target compostable and mono-material solutions.

Why is polypropylene gaining popularity in lidding films?

Polypropylene offers superior heat resistance, can incorporate high recycled content, and aligns with emerging mono-material recycling streams.

How are e-commerce trends influencing lidding film design?

E-grocery and meal-kit services push demand for high-barrier, puncture-resistant, and resealable lids that endure multiple handling cycles and extended cold-chain transit.

What sustainability regulations most affect lidding film producers?

The EU Packaging and Packaging Waste Regulation, state-level extended producer responsibility laws in the United States, and Japan’s positive-list system collectively drive a shift toward recyclable mono-material structures and higher recycled content.

Page last updated on: