North America Quinoa Seeds Market Analysis by Mordor Intelligence

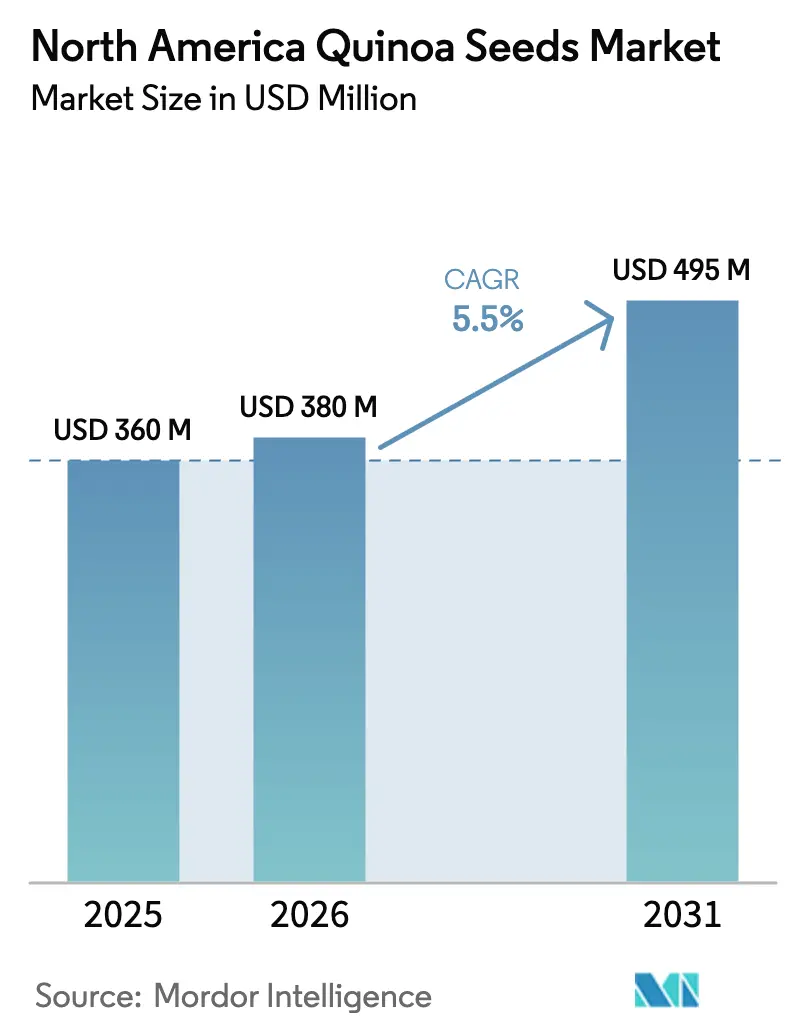

The North America quinoa seeds market size was valued at USD 360.0 million in 2025 and estimated to grow from USD 380.0 million in 2026 to reach USD 495.0 million by 2031, at a CAGR of 5.5% during the forecast period (2026-2031). A widening consumer base for gluten-free and high-protein grains underpins demand, while acreage gains in Colorado, Washington, Oregon, Saskatchewan, and Alberta signal a gradual supply response. Imports from Peru and Bolivia remain pivotal because specialized cleaning and desaponification assets are scarce in the Pacific Northwest and Prairie provinces. Currency swings within the United States–Mexico–Canada Agreement (USMCA) zone reshape sourcing decisions each season, and government programs such as the United States Department of Agriculture Specialty Crop Block Grant continue to lower entry barriers for new growers. Improved agronomic practices and varietal adaptation for North American climates are gradually narrowing quinoa’s yield gap versus imported supply, supporting better price competitiveness.

Key Report Takeaways

By geography, the United States held 72% of the North America quinoa seeds market share in 2025, while Mexico is projected to grow at a 7.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Quinoa Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for gluten-free, high-protein grains | +1.2% | United States and Canada, urban clusters | Medium term (2-4 years) |

| Expansion of domestic quinoa acreage in United States and Canada | +0.9% | Colorado, Washington, Oregon, Saskatchewan, and Alberta | Long term (≥ 4 years) |

| Government incentives for climate-smart specialty crops | +0.7% | United States and Canada | Short term (≤ 2 years) |

| Import-tariff volatility favoring local production | +0.6% | United States, Canada, and Mexico | Short term (≤ 2 years) |

| Rapid growth of online bulk-grain marketplaces | +0.5% | United States and Canada | Short term (≤ 2 years) |

| Precision-ag breeding raises yields and seed quality | +0.2% | University research stations in the United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Gluten-Free, High-Protein Grains

Urban consumers across North America are channeling grocery spending toward ancient grains that combine gluten-free positioning with complete amino acid profiles. Quinoa’s 14-18% protein content and lysine richness support premium pricing in ready-to-eat meals, protein bars, and bakery mixes. United States gluten-free sales kept a double-digit trajectory through 2025, boosted by celiac diagnoses and lifestyle adopters who value gut-health and allergen transparency. The food-service sector echoes this pull, inserting quinoa into salad bars and grain bowls that create steady, year-round demand. Together, these outlets help domestic growers compete with Andean imports, even though production costs remain two to three times higher than wheat or oats [1]Source: World Health Organization, “Gluten-Free Diets and Celiac Disease,” WHO, who.int.

Expansion of Domestic Quinoa Acreage in United States and Canada

Specialty-crop growers in semi-arid zones are pivoting toward quinoa as a higher-margin substitute for wheat and barley. Cold-tolerant lines from Colorado State University and Washington State University enable plantings above 40° N latitude, and Agriculture and Agri-Food Canada backs Prairie trials where long daylight hours drive photosynthesis [3]Source: Colorado State University, “Cold-Tolerant Quinoa Varieties Released,” CSU Extension, colostate.edu. United States Department of Agriculture Specialty Crop Block Grant funds of USD 72.9 million in fiscal 2025 underwrote variety evaluation, soil-health work, and market access projects.

Government Incentives for Climate-Smart Specialty Crops

Federal and provincial programs reward crops that sequester carbon, improve soil structure, and reduce reliance on synthetic inputs. Quinoa aligns well, due to its deep taproot and suitability for reduced-till systems. United States Department of Agriculture (USDA) climate-smart commodity grants and Agriculture and Agri-Food Canada (AAFC) cost-share schemes for organic transition support grower adoption, although the three-year organic certification window strains cash flow. The result is a two-tier supply base, with capital-rich farms capturing subsidies while smaller operators struggle.

Rapid Growth of Online Bulk-Grain Marketplaces

Digital platforms specializing in organic and ancient grains now connect small growers with artisan bakers, meal-kit services, and health retailers. Aggregated supply, real-time pricing, and split-shipment logistics shrink order minimums, letting niche buyers bypass conventional elevators that lack quinoa-dedicated lines. Growers capture varietal premiums by selling red, black, and tri-color quinoa separately rather than blending them. The surge in direct-to-consumer sales during 2024-2025 strengthens this channel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited processing capacity in Prairie and Pacific Northwest | −0.8% | Saskatchewan, Alberta, Washington, and Oregon | Medium term (2-4 years) |

| High production costs vs. mainstream grains | −0.6% | All United States and Canadian quinoa zones | Long term (≥ 4 years) |

| Climate variability and pest pressure | −0.7% | Pacific Northwest, Colorado, and Prairie provinces | Short term (≤ 2 years) |

| Narrow genetic base and Intellectual Property (IP) constraints on elite seed | −0.5% | Breeding programs throughout North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Processing Capacity in Prairie and Pacific Northwest

The absence of dedicated quinoa cleaning and desaponification facilities requires growers to transport raw seeds over long distances, leading to higher freight costs and increased risk of moisture damage. Conventional grain elevators prioritize wheat, barley, and canola, leaving quinoa to compete for off-season slots or surrender organic premiums through co-mingling. Capital spending on specialized lines lags because processors want multi-year supply contracts that growers hesitate to sign amid price swings, especially in Saskatchewan, Alberta, Washington, and Oregon.

Climate Variability and Pest Pressure

Peronospora variabilis outbreaks in Washington and Oregon cut yields by up to 50% during wet springs, undermining profitability. Spores survive on residue and spread by wind, complicating rotations and pushing growers toward fungicides that conflict with organic goals. Unpredictable rainfall shifts sowing windows, while late-season heat triggers premature flowering. Elevated crop-insurance premiums and absence of extension support deter acreage expansion in high-risk zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

The United States anchors the North America quinoa seeds market with 72% value share in 2025, due to its large consumer base, dense natural-foods retail network, and broad food-service penetration. Domestic output remains concentrated in Colorado, Washington, Oregon, and California, where cold-tolerant lines reduce season-length risk. United States Department of Agriculture Specialty Crop Block Grant funds in 2025 strengthen local trials and supply-chain upgrades, yet the strong United States dollar keeps imported products competitive [2].Source: United States Department of Agriculture, Economic Research Service, “Specialty Crop Production Costs and Returns 2025,” USDA, ers.usda.gov Growth through 2031 will be moderate as processing capacity constraints offset relentless consumer demand for gluten-free and high-protein foods.

Canada commands a smaller but steady share, with acreage clustered in Saskatchewan and Alberta. Agriculture and Agri-Food Canada (AAFC) cost-share funding supports organic transitions and on-farm trials, while long summer daylight hours aid photosynthesis. Frost risk and limited cleaning infrastructure remain hurdles. Exports to Japan and South Korea offer price premiums tied to traceability, and domestic demand rises in metro centers such as Toronto and Vancouver.

Mexico is the fastest-growing geography, set for a 7.4% CAGR to 2031. A 23.4% Mexican peso depreciation in 2024 locked in cost advantages for Andean imports but also stirred interest among Mexican processors in local sourcing to hedge exchange risk. Manufacturers in Monterrey and Guadalajara blend quinoa into tortillas, cereals, and snack bars, appealing to middle-class consumers who link the grain with premium nutrition and indigenous heritage. Future momentum depends on building domestic processing assets and stable seed supply as phytosanitary checks and currency shifts complicate imports.

Competitive Landscape

The North America Quinoa Seeds Market exhibits fragmented competition. Employee-owned Bob’s Red Mill retains strong brand equity and direct-to-consumer reach in quinoa-based ingredients, while diversified grain platform Ardent Mills continues to scale through vertical integration. Seed specialists such as Territorial Seed Company and Adaptive Seeds focus on varietal innovation for organic growers, guarding niche footholds outside heavy processing.

Investment white-space centers on processing hubs in Washington, Oregon, Saskatchewan, and Alberta. Facilities equipped for cleaning, color sorting, and desaponification could capture toll-processing revenue and secure long-term contracts with growers anxious to avoid cross-contamination. Online bulk-grain marketplaces disrupt legacy distribution by directly connecting growers to artisan bakers, meal-kit firms, and natural-foods retailers. Precision-agriculture tools lower production risk, and genomic platforms accelerate trait stacking for disease tolerance.

United States–Mexico–Canada Agreement (USMCA) tariff-free treatment of quinoa enables seamless regional trade, but exchange-rate shifts and phytosanitary protocols favor processors that maintain dual sourcing from North American growers and Andean exporters. Strategic seed-manufacturer partnerships with food companies are emerging, delivering proprietary varieties optimized for extrusion snacks or gluten-free baking mixes. Consolidation will continue to advance as larger entities purchase regional mills and seed firms, while niche operators defend positions through varietal uniqueness, sustainability certifications, and direct-to-consumer storytelling.

Recent Industry Developments

- May 2025: Meli, a new gluten-free beer made entirely from quinoa, has been launched, providing a wellness-focused alternative within the craft beer market. It is available in select stores across Massachusetts and online, catering to health-conscious consumers seeking gluten-free options beyond traditional food products.

- December 2024: United States researchers developed a genetic test to quickly detect downy mildew in quinoa seeds and leaves, helping improve disease management and support resistant crop varieties.

- March 2024: NIUKE Foods introduced a quinoa-derived plant milk (QMILQ) as part of its vegan product range. Promoted as the first quinoa milk in the United States, the product combines quinoa with plant proteins and vitamins, targeting the expanding dairy alternatives market.

North America Quinoa Seeds Market Report Scope

Quinoa is a cereal crop primarily cultivated for its edible seeds, which are naturally gluten-free, high in protein, and a good source of dietary fiber. The North America Quinoa Seeds Market report is segmented by geography into the United States, Canada, and Mexico. The report includes production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), wholesale price trend analysis and forecasts, regulatory framework, list of key players, logistics and infrastructure, and seasonality analysis. Market forecasts are provided in terms of value (USD) and volume (metric tons).

By Geography

| United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis |

| By Geography | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

Key Questions Answered in the Report

What is the current value of the North America quinoa seed market?

The market is valued at USD 380 million in 2026 and is forecast to reach USD 495 million by 2031.

Which country holds the largest share of North American quinoa demand?

The United States controls 72% of regional market value, driven by its sizable consumer base and extensive retail and food-service networks.

What is the fastest-growing geography for quinoa in North America?

Mexico is projected to expand at a 7.4% CAGR through 2031 as rising middle-class incomes and urbanization boost demand for functional grains.

Why are imports still critical to North America quinoa supply?

Limited domestic cleaning and de-saponification capacity, combined with favorable currency moves, keeps imports from Peru and Bolivia cost-competitive.

Page last updated on: