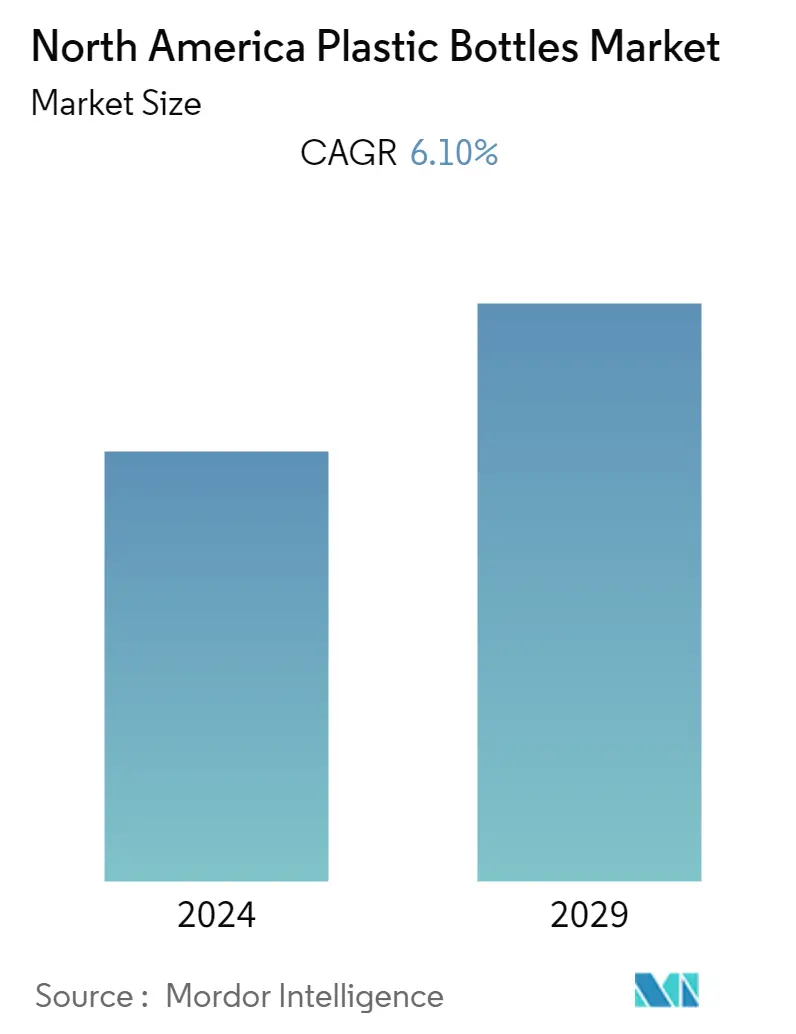

North America Plastic Bottles Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 6.10 % |

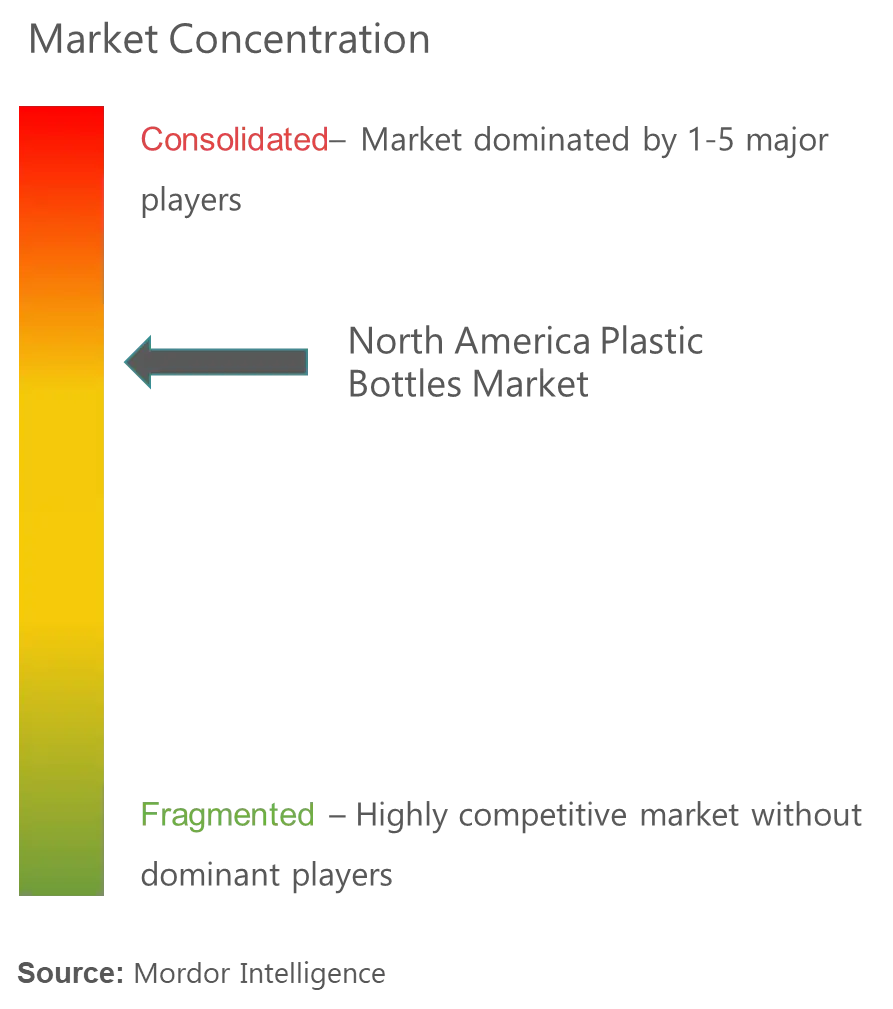

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

North America Plastic Bottles Market Analysis

The North America plastic bottles market was valued at USD 26.70 billion in 2020 and is expected to reach USD 41.56 billion by 2026, registering a CAGR of 6.1% during the forecast period (2021 - 2026). Strong demand for sustainable and convenient packaging solutions among consumers will drive the demand for plastic bottles in North America. According to the Association for Packaging and Processing Technologies (PMMI) 2018 Beverage Report, the North American beverage industry is expected to register a growth of 4.5% during the period 2018-2028.

- The preference for bottled drinks is increasing rapidly, compared to canned beverages, owing to its cost-effectiveness. Additionally, the consumers in the North American region are quickly shifting toward healthy alternatives to beverages, primarily bottled water.

- Energy drink space in the region is booming. This is due to the increasing trend of athleticism, rising concern for health, and shift in dietary patterns due to changing lifestyles. The innovation of new flavors with health benefits is a major driving factor.

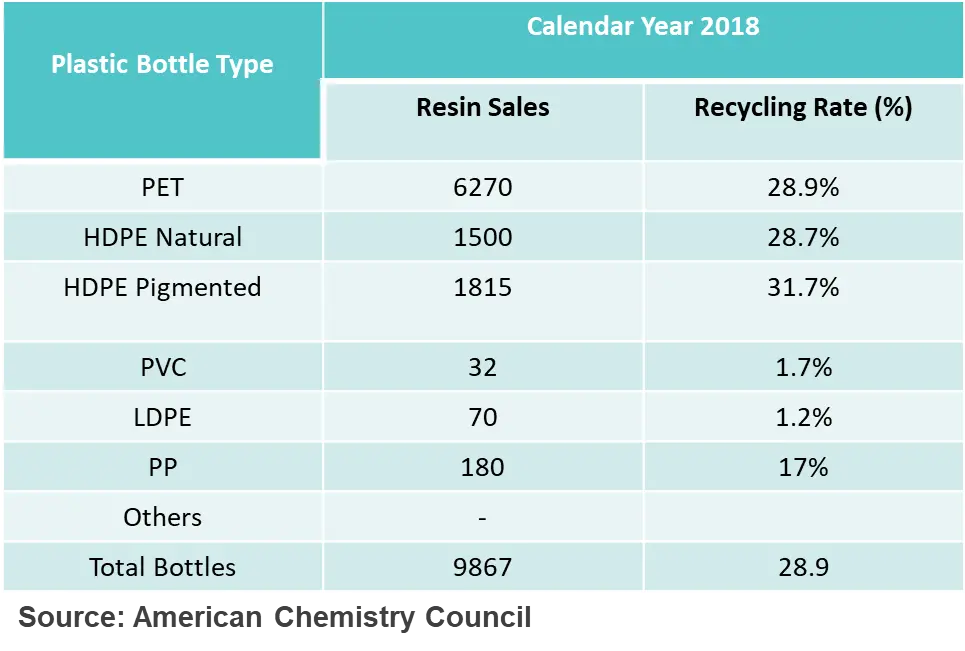

- With the U.S. plastic recycling rate showing no significant growth, the concerns relating to the use of plastic are growing. It has been estimated by Athe ssociation of Plastic Recyclers (APR) and the American Chemistry Council (ACC) that othe verall recycling rate for plastic bottles was 28.9 % compared with 29.3 % in 2017. This is expected to have a negative impact on market growth in the region over the forecast period.

- The spread of covid 19 has not majorly negatively affected the plastic bottle industry in North America. This is because it supports the vital food, beverage ,and pharmaceutical industry, which comes under essential services and won't be discontinued tuntilthe pandemic is over.

North America Plastic Bottles Market Trends

This section covers the major market trends shaping the North America Plastic Bottles Market according to our research experts:

Non-Alcoholic Beverages to Dominate the Market

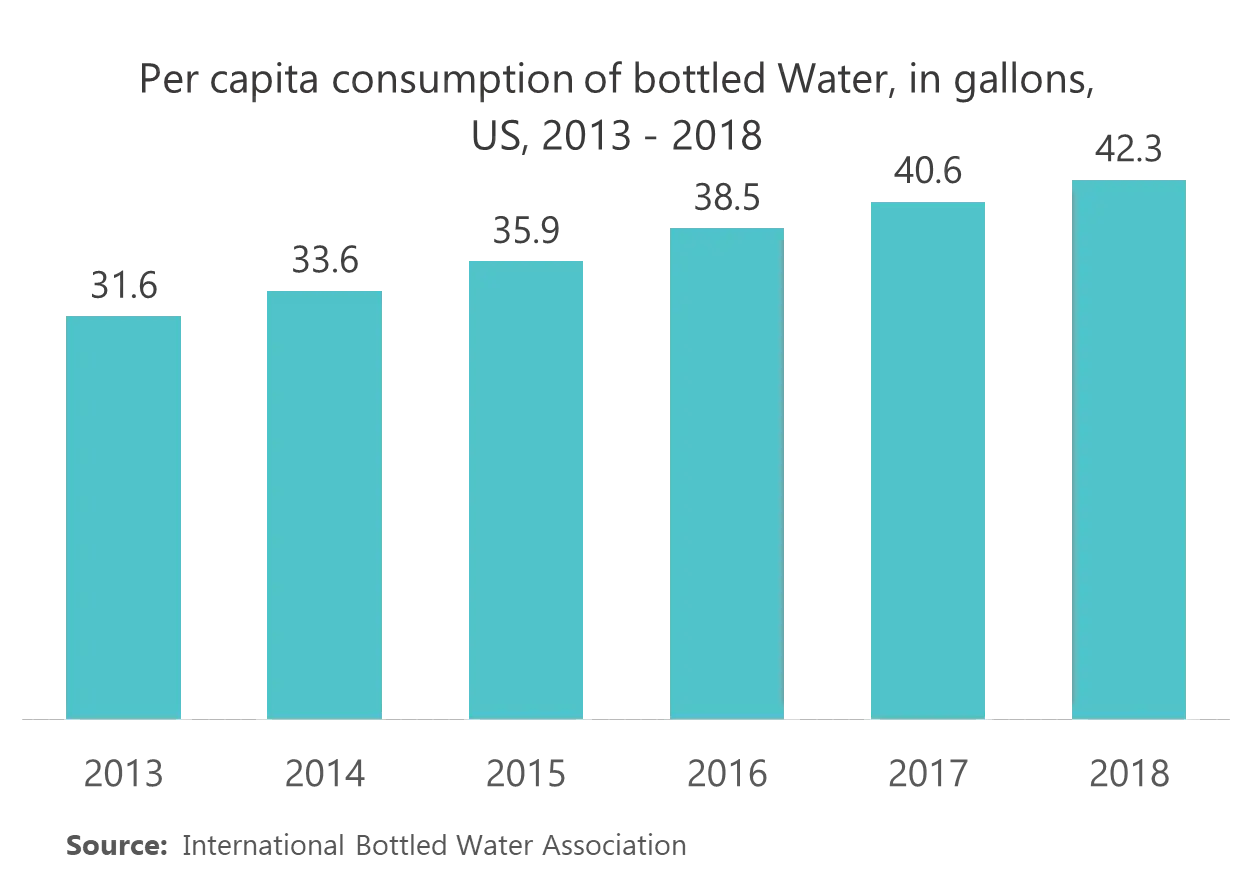

- Soda consumption is decreasing in the U.S. However; bottled water consumption has been increasing. Both products are predominately packaged in plastic bottles. In fact, plastic bottle usage skyrocketed from carbonated soft drinks (CSD) have reached their saturation in the North American region, and companies like Coca-Cola, Pepsi, and Keurig Dr pepper have reported flat sales from their carbonated software division in North America.

- Coca-Cola, in its annual reports for 2018 and 2019, mentioned that the unit volume sales of its CSD were 3.306 billion unit cases in 2018 and 3.44 billion in 2017. The company has claimed to be the most significant player in the North American region, with a market share of 43% in 2018.

- According to PETRA, PET is a clear, strong, and lightweight plastic that is widely used for packaging foods and beverages, especially convenience-sized soft drinks, juices, and water. Virtually all single-serving and 2-liter bottles of carbonated soft drinks and water sold in the U.S. are made from PET.

- As the shift from soda to water progresses, the bottled water industry has worked with recycling advocates to increase recycling rates of water bottles.

- The companies in the region are currently expanding. In 2019, Nestlé Waters North America (NWNA) announced the acquisition of bottled water distributor Watchung Spring Water in the United States.

- Cott Corporation made two significant acquisitions in 2018 and 2019. In 2018, it acquired The Mountain Valley Spring Company for USD 78.5 million from Great Range Capital, and in 2019, it acquired WG America Company and its individual affiliated companies.

PET to Show Significant Market Growth

- PET has been the most predominantly used material for beverage packaging in the region. Moreover, the trend for light-weighted packaging has increasingly driven the demand for PET bottles.

- According to the International Bottled Water Association, the average weight of a half-liter 16.9 ounce PET plastic bottle has declined 48% to 9.89 grams from 2000 to 2014. The drop in weight is the equivalent of 6.2 billion pounds of PET resin since 2000. This decrease has resulted in the manufacture of more number of bottles with the available resin, which has driven its growth.

- Moreover, the PET bottles have also been witnessing demand in the alcoholic beverages market. The wine market is one that has been slow to adopt new forms of packaging. As new concepts in PET gaining substantial grounds in the wine industry, companies are bringing new products into the market.

- For instance, in February 2020, Amcor announced its latest and custom designs at the Wine and Grape Symposium, North America. The company also announced a collaboration with Garçon Wines, a British start-up.

North America Plastic Bottles Industry Overview

The plastic bottles market is highly concentarted in North America, with legacy players such as Amcor, Plastipak and Berry Global occupying the majority market share. These players are mostly involved in acquisitions with a few focusing on product innovations. Some of the recent developments occuring in the market are --

- February 2020 - Amcor in the multivitamin category showcased the development and launch of the PET container that is made from 100% post-consumer recycled content (PCR) resin. The company created the new clear bottle in two sizes, 100 cubic centimeters and 150 cubic centimeters, for Ritual, a health meets technology company that reimagined the multivitamin.

- July 2019 - Berry Global Group, Inc. completed the acquisition of RPC Group, Plc. with an approximate price of USD 6.5 billion. RPC Group is the leading global designer and engineer of the plastic products in packaging and non-packaging markets. The acquisition has helped the growth of Berry's Engineered Materials product portfolio, which is expected to strengthen the Berry's product line.

- March 2019 - Altium Packaging Canada announced that it has acquired Plastique Micron (PMI) and its affiliates, IMBC Blowmolding (2014) and Action Plastic Products, which is a major specialty packaging manufacturer. Altium was focusing on in expansion plans in Canada over the past year and continues to seek opportunities to grow across the country.

North America Plastic Bottles Market Leaders

Alpha Packaging Inc.

Altium Packaging (Loews Corporation)

Gerresheimer AG

Berry Global Inc

Plastipak Holdings Inc.

*Disclaimer: Major Players sorted in no particular order

North America Plastic Bottles Market Report - Table of Contents

-

1. INTRODUCTION

-

1.1 Study Deliverables

-

1.2 Study Assumptions

-

1.3 Scope of the Study

-

-

2. RESEARCH METHODOLOGY

-

3. EXECUTIVE SUMMARY

-

4. MARKET DYNAMICS

-

4.1 Market Overview

-

4.2 Market Drivers

-

4.2.1 Changing Demographic and Lifestyle Factors

-

-

4.3 Market Restraints

-

4.3.1 Fluctuating Raw material (Plastic Resin) prices

-

4.3.2 Growing Environmental Concerns Over the Use of Plastic

-

-

4.4 Value Chain Analysis

-

4.5 Porters Five Force Analysis

-

4.5.1 Threat of New Entrants

-

4.5.2 Bargaining Power of Buyers/Consumers

-

4.5.3 Bargaining Power of Suppliers

-

4.5.4 Threat of Substitute Products

-

4.5.5 Intensity of Competitive Rivalry

-

-

-

5. MARKET SEGMENTATION

-

5.1 By Raw Material

-

5.1.1 PET

-

5.1.2 PP

-

5.1.3 LDPE

-

5.1.4 HDPE

-

5.1.5 Other Raw Materials

-

-

5.2 By End-user Vertical

-

5.2.1 Food

-

5.2.2 Pharmaceuticals

-

5.2.2.1 Solid Containers

-

5.2.2.2 Dropper Bottles

-

5.2.2.3 Nasal Spray Bottles

-

5.2.2.4 Liquid Bottles

-

5.2.2.5 Oral Care

-

5.2.2.6 Other Types

-

-

5.2.3 Cosmetics

-

5.2.4 Household care

-

5.2.5 Other End-user Verticals

-

-

5.3 By Country

-

5.3.1 United States

-

5.3.2 Canada

-

-

-

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

-

6.1.1 Alpha Packaging Inc.

-

6.1.2 Altium Packaging (Loews Corporation)

-

6.1.3 Gerresheimer AG?

-

6.1.4 Graham Packaging Company

-

6.1.5 Berry Global, Inc.

-

6.1.6 Plastipak Holdings Inc.

-

6.1.7 Amcor Plc

-

6.1.8 Comar LLC

-

- *List Not Exhaustive

-

-

7. INVESTMENT ANALYSIS

-

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

North America Plastic Bottles Industry Segmentation

Plastic bottles are generally made up of plastic resins, such as PET, PP, and HDPE, among others. By end-user vertical, the market is divided into beverages, food, pharmaceuticals, cosmetics, household care, among others. Based on the country, the United States and Canada are considered in the scope.

| By Raw Material | |

| PET | |

| PP | |

| LDPE | |

| HDPE | |

| Other Raw Materials |

| By End-user Vertical | ||||||||

| Food | ||||||||

| ||||||||

| Cosmetics | ||||||||

| Household care | ||||||||

| Other End-user Verticals |

| By Country | |

| United States | |

| Canada |

North America Plastic Bottles Market Research FAQs

What is the current North America Plastic Bottles Market size?

The North America Plastic Bottles Market is projected to register a CAGR of 6.10% during the forecast period (2024-2029)

Who are the key players in North America Plastic Bottles Market?

Alpha Packaging Inc., Altium Packaging (Loews Corporation), Gerresheimer AG, Berry Global Inc and Plastipak Holdings Inc. are the major companies operating in the North America Plastic Bottles Market.

What years does this North America Plastic Bottles Market cover?

The report covers the North America Plastic Bottles Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the North America Plastic Bottles Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

North America Plastic Bottles Industry Report

Statistics for the 2024 North America Plastic Bottles market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. North America Plastic Bottles analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.