Cold Insulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

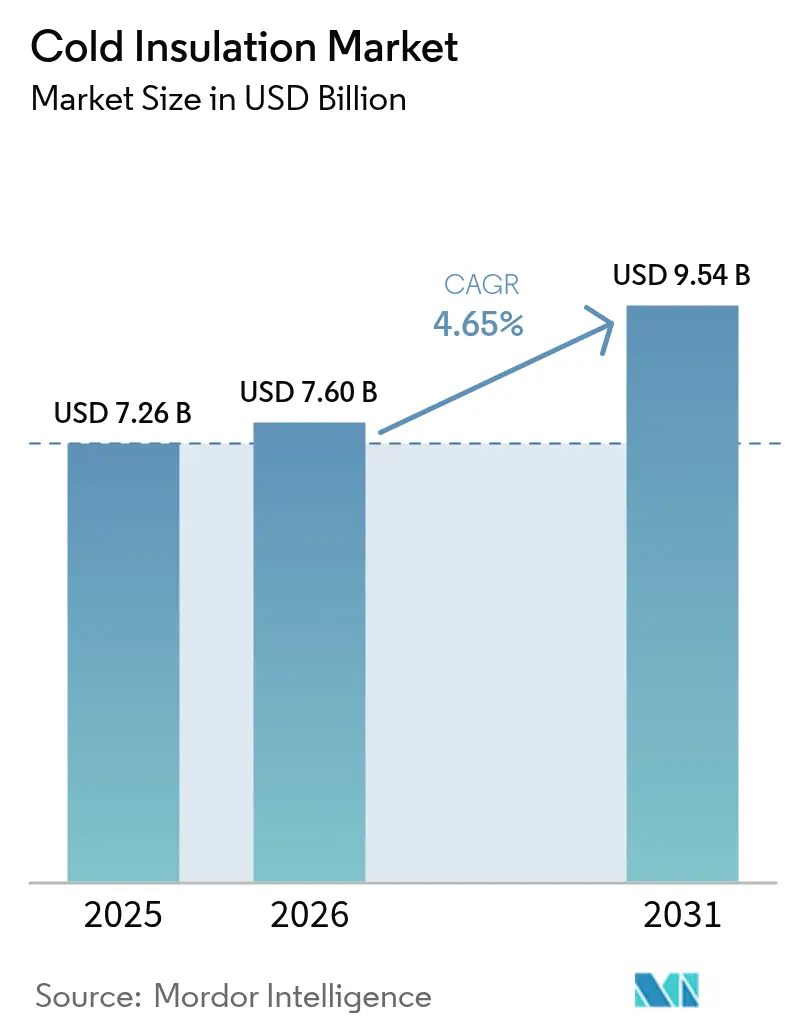

| Market Size (2026) | USD 7.6 Billion |

| Market Size (2031) | USD 9.54 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

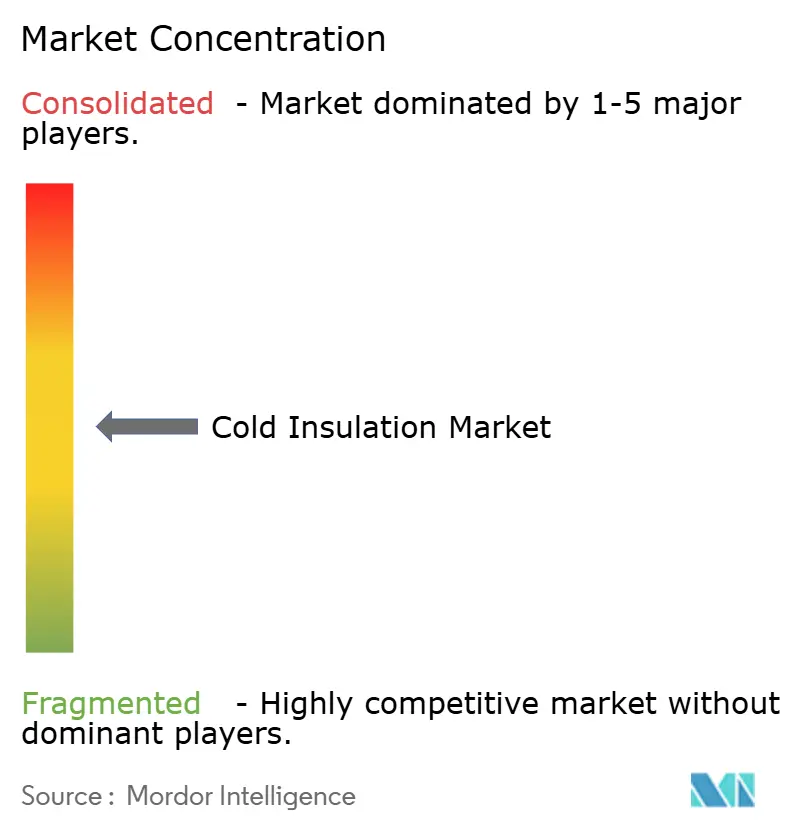

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Insulation Market Analysis by Mordor Intelligence

Cold Insulation market size in 2026 is estimated at USD 7.6 billion, growing from 2025 value of USD 7.26 billion with 2031 projections showing USD 9.54 billion, growing at 4.65% CAGR over 2026-2031. Demand is propelled by liquefied natural gas (LNG) build-outs, stricter energy-efficiency mandates for building retrofits, and wider adoption of temperature-controlled logistics. Technology improvements, particularly phenolic foam’s enhanced fire resistance and aerogel-based composites, allow suppliers to meet tougher performance specifications while easing installation constraints. Regulatory pressure to decarbonize industrial assets keeps R-value requirements moving upward, expanding the addressable scope for high-performance products. Meanwhile, the installer talent gap for advanced systems and volatile diisocyanate costs create periodic margin swings even for leading manufacturers. As capital requirements rise, larger players rely on vertical integration and regional manufacturing footprints to secure feedstocks and shorten delivery cycles, reinforcing high entry barriers across the cold insulation market.

Key Report Takeaways

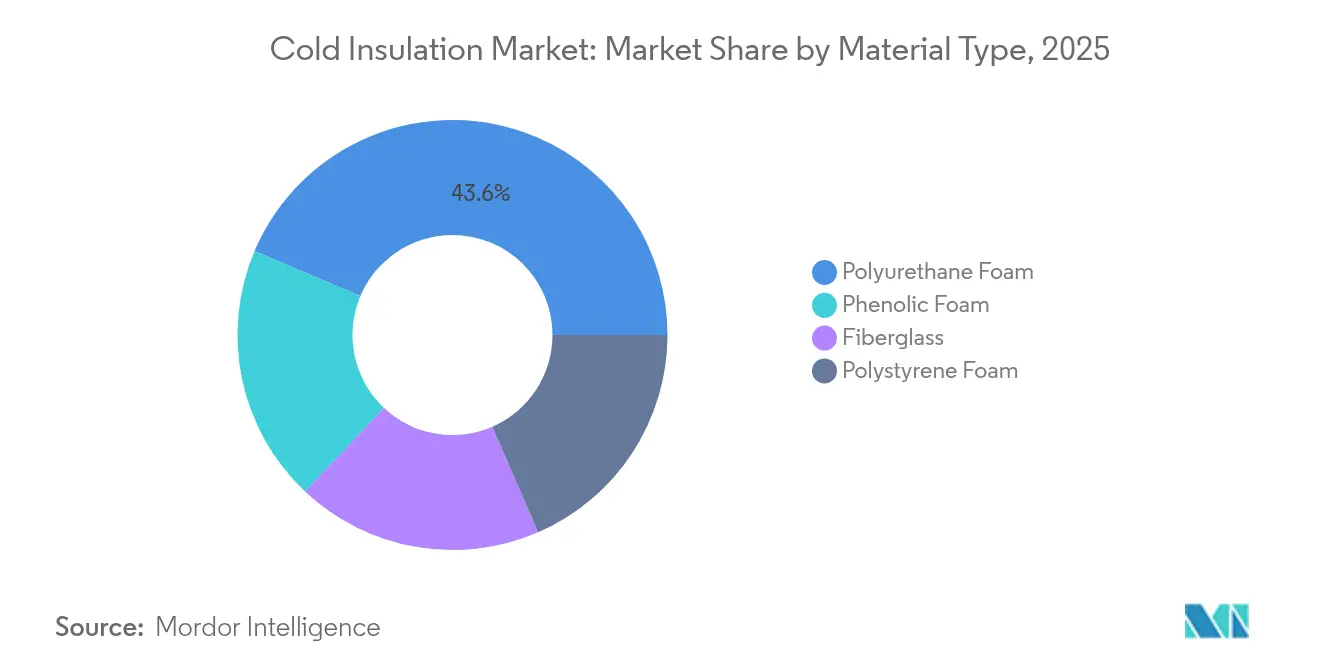

- By material, polyurethane foam held 43.62% of the cold insulation market share in 2025; phenolic foam is growing fastest at a 4.82% CAGR through 2031.

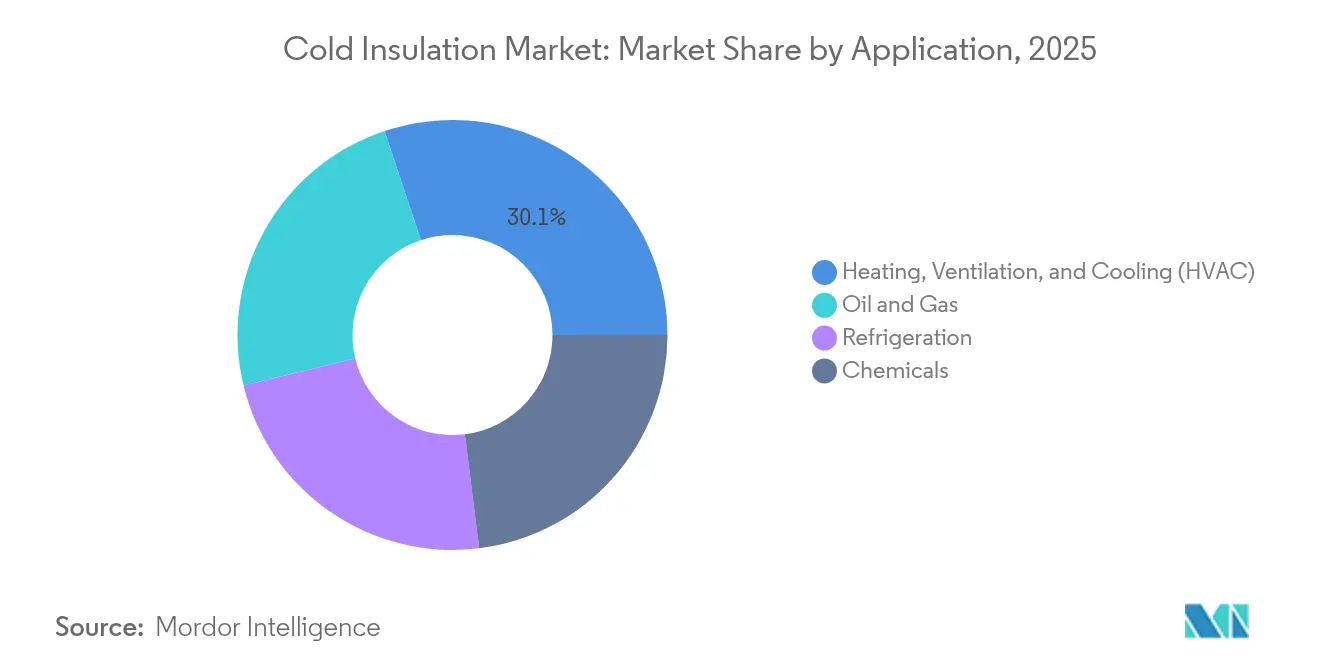

- By application, HVAC accounted for 30.12% of the cold insulation market size in 2025, while oil and gas is expanding at a 5.02% CAGR to 2031.

- By geography, Asia Pacific led with 37.35% revenue in 2025 and posts the highest regional CAGR of 5.4% over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cold Insulation Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for cryogenic insulation (LNG and LH₂ projects) | +1.6% | Global, with concentration in Asia Pacific and North America | Medium term (2-4 years) |

| Growing need for energy-efficiency and Net-Zero retrofits | +0.8% | Europe and North America primarily | Long term (≥ 4 years) |

| Expansion of global cold-chain logistics and e-grocery | +1.2% | Global, led by North America and Asia Pacific | Short term (≤ 2 years) |

| Surge in small-scale LNG bunkering infrastructure | +0.9% | Global maritime routes, concentrated in Europe and Asia | Medium term (2-4 years) |

| Industrial and Infrastructure Growth in Emerging Markets | +0.5% | Asia Pacific, Middle East, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cryogenic Insulation (LNG And LH₂ Projects)

Cryogenic applications require materials that withstand –162 °C for LNG and –253 °C for liquid hydrogen without structural creep or delamination. Composite systems pairing phenolic foam with multilayer barriers are therefore displacing legacy fiberglass, explaining phenolic’s 5.05% growth. In LNG bunkering, insulation integrity safeguards against flash vaporization events that would spike boil-off rates, so ship-to-ship transfer operators specify lower thermal conductivity thresholds. Floating storage and regasification units add complexity because cryogenic CO₂ capture zones demand separate temperature envelopes within the same hull. Suppliers responding with aerogel-reinforced foams gain differentiation while securing early-stage approvals from classification societies. The result is a premium-priced niche that punches above its volume weight yet exerts outsized pull on research and development spending across the cold insulation market.

Growing Need for Energy-Efficiency and Net-Zero Retrofits

EU renovation policy calls for a 3% annual deep-renovation rate, driving EUR 275 billion in yearly spending and tightening U-value ceilings for external walls[1]Buildings Performance Institute Europe, “Report on the evolution of the European regulatory framework for buildings efficiency,” BPIE.EU. Vacuum insulation panels (VIPs) and aerogel sheets solve space-constraint issues in heritage buildings, achieving 35% lower thermal transmittance versus mineral wool while keeping façade thickness unchanged. Retrofit programs such as Energiesprong have validated industrialized over-cladding kits that cut site labor by half, signaling scalable pathways for large housing stocks. Corporate landlords and municipalities consequently rank envelope performance as a top capital-allocation priority, further broadening opportunity for the cold insulation market.

Expansion of Global Cold-Chain Logistics and E-Grocery

E-commerce grocers and pharmaceuticals heighten demand for urban micro-fulfillment hubs that hold –30 °C chambers adjacent to ambient pick stations. Robotics adopted in these sites suffer from condensation-induced sensor faults unless panel joints achieve tight tolerances, making high-density EPS, VIPs, or bio-based polyurethane preferred solutions. Sustainability scorecards add another layer: grocery retailers now request Environmental Product Declarations for facility envelopes, nudging suppliers toward low-embodied-carbon foams that still meet freezer-grade R-values. These intertwined drivers secure a steady pipeline of retrofit and greenfield work for players across the cold insulation industry.

Industrial and Infrastructure Growth in Emerging Markets

India’s Production-Linked Incentive scheme, targeting a 25% manufacturing GDP share by 2025, lifts demand for chilled warehouses supporting vaccine exports and processed foods[2]International Trade Administration, “India Advanced Manufacturing Sector,” TRADE.GOV . Mexico, now the world’s fourth-largest polyurethane consumer, shows how near-shoring bolsters local panel makers supplying appliances and automotive assemblies. Price sensitivity in these markets sustains fiberglass and EPS volumes, yet multinationals still introduce phenolic lines to satisfy export-oriented factories obligated to meet stricter global standards. Over time, maturing building codes and carbon disclosure frameworks are expected to steer procurement toward higher-spec products, lengthening the runway for the cold insulation market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petrochemical raw-material pricing | –0.7% | Global, notably polyurethane producers | Short term (≤ 2 years) |

| Shortage of certified installers for aerogel/VIP systems | –0.4% | North America and Europe | Medium term (2-4 years) |

| Lack of awareness about cold insulation materials | –0.3% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Raw-Material Pricing

With 85% of MDI’s cradle-to-gate global-warming potential linked to feedstock inputs, polyurethane makers face both cost and emissions exposure. Diversification into bio-circular feedstocks partially hedges against price volatility, yet scale remains limited to pilot lines. On the demand side, appliance OEMs often delay procurement during price spikes, producing short-run volume dips that ripple through the cold insulation market. Vertical integration, such as Owens Corning’s resin procurement contracts and Kingspan’s pipeline of local MDI storage tanks, softens but does not eliminate the headwind.

Shortage of Certified Installers for Aerogel/VIP Systems

Vacuum panels lose nearly all R-value once punctured, so site crews must be trained to avoid damage and seal joints precisely. Industry leader Armacell instituted a global certification pathway in 2024 to triple the number of qualified contractors by 2027. Still, capacity lags demand, particularly across U.S. and German retrofit programs, where union labor shortages compound scheduling delays. Installation errors, inflating field failure rates, discourage some building owners despite strong modeled paybacks, muting uptake of high-performance solutions across the cold insulation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyurethane Dominance Faces Phenolic Challenge

The polyurethane segment captured 43.62% of the cold insulation market size in 2025, buoyed by mature supply chains and favourable spray-foam economics. Phenolic foam is expanding at a 4.82% CAGR on the strength of LNG and hydrogen projects demanding low flame-spread and robust cryogenic performance. Bio-based polyurethane variants containing 25% recycled or plant-derived polyols lower embodied-carbon footprints by 43% and help manufacturers win public-sector bids.

Competitive intensity inside polyurethane tightens as producers backward-integrate into diisocyanate synthesis to manage price risk. Owens Corning’s 2025 feedstock sourcing program stabilizes margins while enabling bulk purchasing economies. Meanwhile, Kingspan’s Ukraine campus injects new regional capacity, reducing freight emissions and enhancing supply security for Eastern Europe. These moves reinforce the high threshold for new entrants seeking scale inside the cold insulation market.

By Application: Heating, Ventilation, and Cooling (HVAC) Leadership Challenged by Energy-Sector Growth

Heating, Ventilation, and Cooling (HVAC) held 30.12% the cold insulation market share in 2025, lifted by aggressive renovation targets that specify higher R-values for ducting, chilled-water lines, and rooftop units. Oil and gas is the fastest-rising application at 5.02% CAGR, reflecting LNG liquefaction trains, bunkering modules, and hydrogen storage tanks that require multi-layer cryogenic systems. Cold-chain refrigeration follows closely; demand from e-grocery dark stores and vaccine freezers keeps panel volumes high even when construction cycles soften. Chemical processing plants favour phenolic and cellular-glass solutions where chemical resistance trumps price.

Emerging sub-applications, such as phase-change panels integrated inside HVAC plenum cavities, spawn niche demand for hybrid insulation-plus-energy-storage assemblies. Building owners accept modest cost premiums because load-shifting cuts chiller runtime and peak-demand charges. Taken together, these trends diversify growth vectors beyond traditional building shells, ensuring the cold insulation market remains resilient through macroeconomic swings.

Geography Analysis

Asia Pacific dominated with 37.35% revenue in 2025 and is projected to add a further 5.4% CAGR to 2031, making it both the largest and fastest region. China’s automation-driven cold-chain overhaul, which deploys autonomous forklifts inside –30 °C warehouses, calls for ultra-low-permeability panel joints to maintain humidity control. India’s policy push for a 25% manufacturing GDP share, coupled with fiscal incentives for cold-store construction, attracts polyurethane suppliers setting up local rigid-foam board lines.

North America commands a sizeable slice, supported by federal retrofit tax credits and record LNG export terminal builds along the Gulf Coast. Owens Corning’s new Ohio fiberglass line, slated for 2027, underpins regional supply, while DOE grants accelerate aerogel VIP commercialization that could unlock deeper building retrofits. Europe, though facing sluggish construction output, maintains healthy insulation demand thanks to legally mandated deep-renovation rates. Kingspan and Knauf Insulation expand regional capacity even as energy-price volatility challenges operating margins. Middle East mega-projects such as Qatar’s LNG expansion and Saudi hydrogen hubs apply stringent cryogenic specs that invite aerogel players, while Latin America benefits from refrigeration investments connected to agrifood exports. Collectively, these regional vectors guarantee broad-based opportunity for the cold insulation market.

Competitive Landscape

The cold insulation market is moderately fragmented, yet capital-intensive. Owens Corning, Kingspan, Armacell, and Knauf Insulation headline the tier-one group, combining global brands with vertically integrated feedstock positions. Technology differentiation dominates market-share battles. Aerogel VIPs, non-isocyanate foams, and phase-change-enhanced boards allow suppliers to secure LEED and BREEAM credits for projects chasing tax incentives. Installer certification programs, pioneered by Armacell, further lock in customers by guaranteeing field performance, a competitive moat when contractor scarcity persists.

Cold Insulation Industry Leaders

Owens Corning

Armacell

Aspen Aerogels Inc.

BASF

ROCKWOOL A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kingspan Group announced a EUR 280 million (~USD 328.6 million) investment in a Ukrainian manufacturing campus to meet growing regional demand for high-performance insulation materials including cold insulation.

- October 2024: Carlisle Companies acquired Plasti-Fab for USD 259.5 million, expanding its polystyrene insulation platform across North America.

Global Cold Insulation Market Report Scope

The Cold Insulation Market report includes:

| Polyurethane Foam |

| Fiberglass |

| Polystyrene Foam |

| Phenolic Foam |

| Oil and Gas |

| Chemicals |

| Heating, Ventilation, and Cooling (HVAC) |

| Refrigeration |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Material Type | Polyurethane Foam | |

| Fiberglass | ||

| Polystyrene Foam | ||

| Phenolic Foam | ||

| By Application | Oil and Gas | |

| Chemicals | ||

| Heating, Ventilation, and Cooling (HVAC) | ||

| Refrigeration | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the cold insulation market by 2031?

It is expected to reach USD 9.54 billion, growing at a 4.65% CAGR.

Which region leads the cold insulation market?

Asia Pacific holds 37.35% of revenue and also records the fastest 5.4% CAGR.

Why is phenolic foam gaining share in cold insulation applications?

Superior fire resistance and cryogenic stability make it the preferred choice for LNG and hydrogen projects.

How do volatile diisocyanate prices influence insulation suppliers?

Price swings compress polyurethane margins by up to 25%, pushing producers toward vertical integration and bio-based feedstocks.

What hinders faster adoption of aerogel and vacuum insulation panels?

A shortage of certified installers raises field failure risks, delaying project schedules and limiting uptake.

Page last updated on: