Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

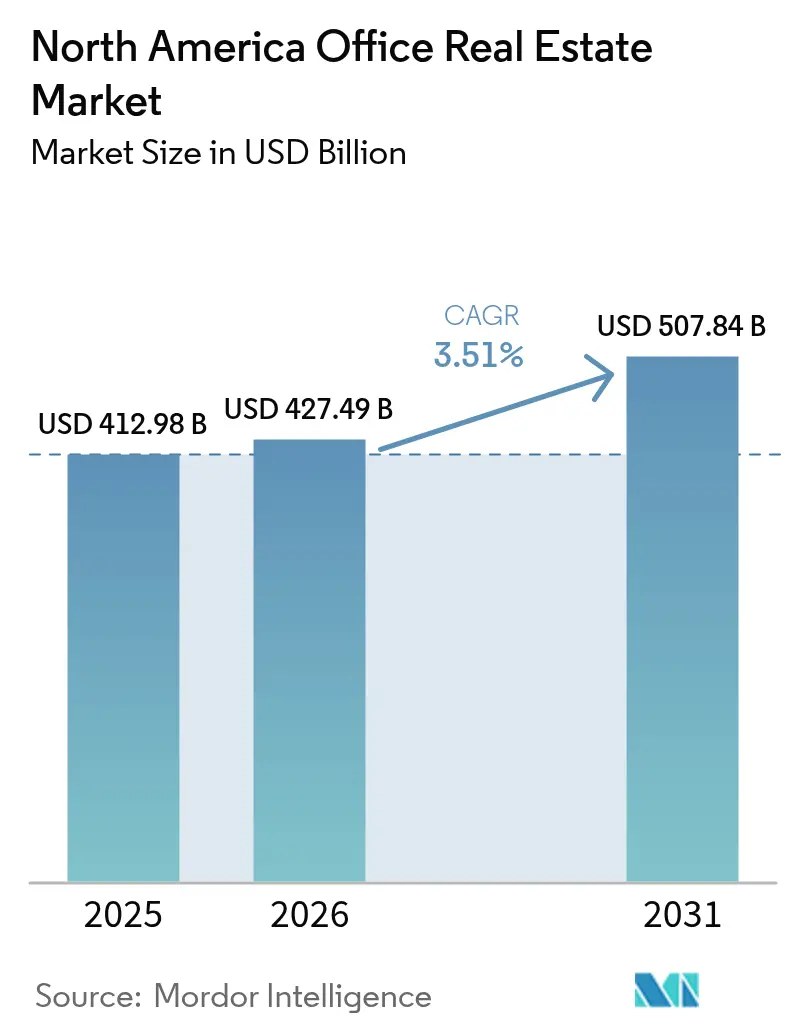

| Base Year Market Size (2025) | USD 412.98 Billion |

| Market Size (2026) | USD 427.49 Billion |

| Market Size (2031) | USD 507.84 Billion |

| Growth Rate (2026 - 2031) | 3.51% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Office Real Estate Market Analysis by Mordor Intelligence

The North America Office Real Estate Market size in 2026 is estimated at USD 427.49 billion, growing from 2025 value of USD 412.98 billion with 2031 projections showing USD 507.84 billion, growing at 3.51% CAGR over 2026-2031. Demand is splitting sharply between premium workplaces and aging commodity space as tighter return-to-office mandates intersect with durable hybrid work adoption. Grade A buildings capture flight-to-quality leasing, while large volumes of Grade B/C stock face conversion to residential or data-center uses. Investor appetite is re-emerging for distressed trophies after rate cuts, yet refinancing headwinds remain acute for highly levered secondary assets. Nearshoring is steering fresh capital into Mexican growth corridors, and municipal “green overlay” incentives are accelerating adaptive reuse in U.S. gateway cities. Overall, the North America office real estate market is becoming a two-track arena defined by amenity-rich, energy-efficient space on one side and rapidly obsolescing stock on the other.

Key Report Takeaways

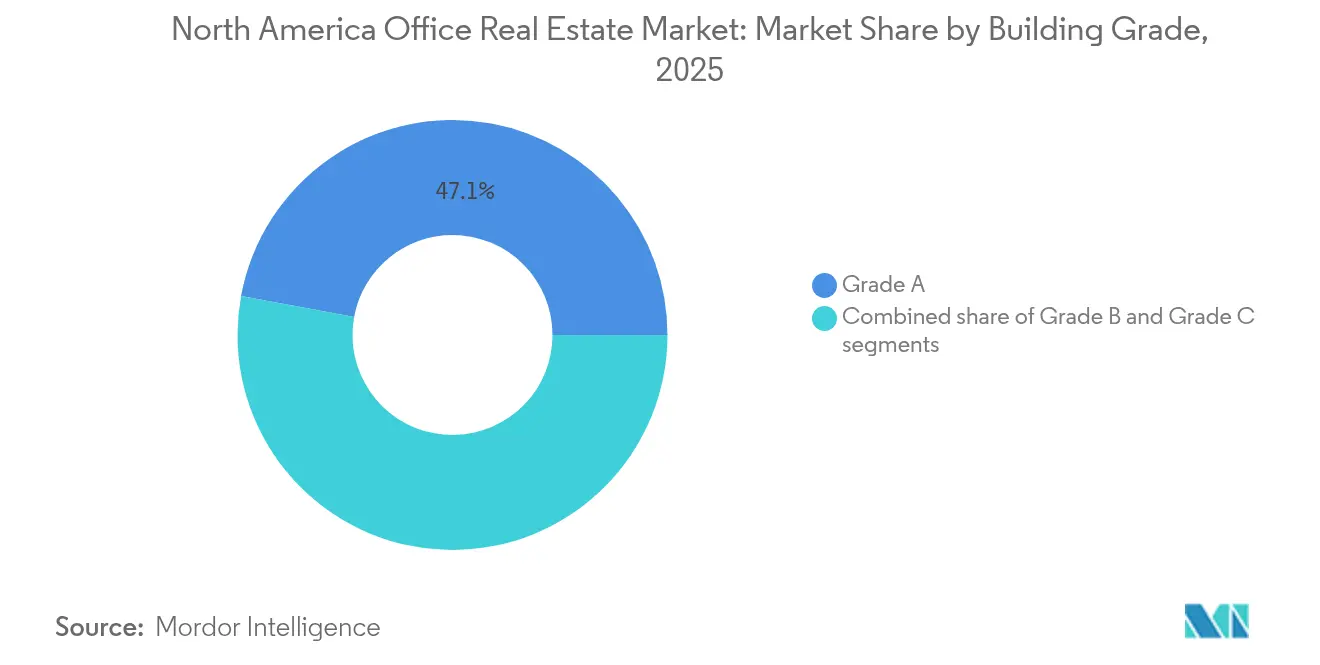

- By building grade, Grade A assets commanded 47.10% of the North America office real estate market share in 2025, and this segment is expanding at a 3.85% CAGR through 2031.

- By transaction type, rentals represented 77.40% of total activity in 2025, while sales are the fastest-growing segment at a 3.95% CAGR to 2031.

- By end use, information technology held a 27.95% share of the North America office real estate market size in 2025 and is forecast to increase at a 4.05% CAGR during 2026-2031.

- By country, the United States retained 89.65% share of 2025 revenue, whereas Mexico is set to post the highest 4.32% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Return-to-office mandates lifting premium-grade leasing demand | +0.8% | United States & Canada | Short term (≤ 2 years) |

| Record capital availability for opportunistic office buys post-rate cuts | +0.6% | North America | Medium term (2-4 years) |

| Flight-to-quality trend favoring energy-efficient, amenity-rich buildings | +0.5% | Global / U.S. gateways | Long term (≥ 4 years) |

| AI model-training loads driving conversion of Grade B/C stock to edge data centers | +0.4% | U.S. data-center hubs | Medium term (2-4 years) |

| Municipal “green-overlay” zoning incentives fast-tracking office-to-residential conversions | +0.3% | U.S. urban cores | Long term (≥ 4 years) |

| Rise of private-credit funds offering bridge-to-core financing for distressed assets | +0.2% | North America secondary markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Return-to-office mandates lifting premium leasing

Large employers such as Amazon, Starbucks, and IBM reinstated four-to-five-day attendance rules in 2024, pushing 75% of U.S. white-collar staff under set office-presence targets. Tenants now concentrate on best-in-class towers where high-spec ventilation, wellness certifications, and vibrant amenities help justify commutes. The 100 biggest leases averaged 288,834 sq ft, up 8% year on year, with 68% structured as renewals to lock cost certainty. Financial-services occupiers dominated Manhattan’s high-rent deals, securing 64% of leases above USD 100 psf and nearly tripling contracts above USD 200 psf. Employers with set attendance policies report lower turnover versus fully remote peers, reinforcing premium-space demand signals.

Capital surge for opportunistic office buys post-rate cuts

Easing monetary policy has revived deal pipelines for well-capitalized investors. Private-credit giants alone amassed more than USD 40 billion earmarked for bridge-to-core office debt, led by KKR’s USD 42 billion pipeline. Assets in distress trade at 30-70% below replacement cost, especially in secondary U.S. metros where local banks pulled back lending. Monarch Capital Partners deployed USD 3.6 billion into opportunistic plays by April 2024, benefiting from a USD 929 billion commercial mortgage maturity wall through 2025. REITs added USD 84.7 billion of fresh equity in 2024 to hunt similar bargains.

Flight-to-quality toward green amenity-rich buildings

Hybrid norms leave commodity space struggling, yet prime towers recorded positive 49 million sq ft net absorption between 2020-2024 while non-prime lost 170 million sq ft. Effective rents for Class A+/A rose 5.2% since 2023 and now command 84% premiums over B/C stock. Upcoming regulations such as New York’s Local Law 97, which levies USD 268 per-ton carbon fees from 2025, heighten owner urgency to decarbonize[1]New York City Mayor’s Office of Climate & Environmental Justice, “Climate Mobilization Act: Local Law 97,” NYC Accelerator, accelerator.nyc.

AI-driven upgrades converting Grade B/C offices to edge data centers

Soaring AI training loads require low-latency compute close to users. Vacant offices with solid power feeds and fiber routes are prime conversion candidates, reducing delivery time versus ground-up builds. Prologis has repurposed warehouse shells into data-ready space outside Chicago, spotlighting power access as the key determinant. Edge retrofits simultaneously relieve oversupply in under-performing submarkets and feed surging data-center demand, with investors arbitraging location and electrical capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent hybrid-work adoption reducing net absorption | -0.9% | North America (tech-heavy metros) | Long term (≥ 4 years) |

| Elevated refinancing wall & tightened bank-lending standards | -0.7% | United States & Canada | Short term (≤ 2 years) |

| Generative-AI workplace-planning tools optimizing space use, cutting footprints | -0.4% | Global (early tech & finance adopters) | Medium term (2-4 years) |

| Local energy-performance mandates penalizing older assets | -0.3% | U.S. major metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistently hybrid work cutting net absorption

Hybrid work stabilized at 80% adoption even as mandates intensified, with actual U.S. office utilization averaging only 38% of capacity in 2024. Organizations reduced seat counts by 15% per head, targeting 25% smaller footprints via sharing ratios above 1.5:1. Vacancy climbed to 19% by Q1 2025, the highest since the early 1990s[2]U.S. Government Accountability Office, “Commercial Real Estate: Trends, Risks, and Federal Monitoring Efforts,” GAO, gao.gov. Nearly half of surveyed employees would quit rather than return full-time, valuing flexibility at an 8% pay uplift. These shifts permanently depress absorption of generic space, tilting demand toward fewer, higher-quality locations.

Refinancing wall amid tighter bank lending

More than USD 1.2 trillion of U.S. commercial mortgages will mature by 2025, with offices forming 17% of the load. Regional banks, which hold 75% of these loans, curtailed new originations as deposit flight and higher funding costs squeezed balance sheets. Office CMBS delinquency rose to 5.07% by early 2024, and only 10% of maturing loans were paid off at term. Borrowers confront conservative loan-to-value hurdles and fresh equity requirements that many cannot meet, triggering loan extensions and discounted trades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium towers dominate a bifurcated landscape

Grade A space captured 47.10% of the North America office real estate market share in 2025 and continues to lead absorption trends as tenants consolidate into modern, tech-enabled environments. Prime towers posted positive leasing of 49 million sq ft versus a 170 million sq ft loss in non-prime categories. Average asking rents in Grade A exceed lower classes by 84%, reflecting superior amenities and ESG credentials. Financial services firms signed 64% of USD 100-plus rents in Manhattan, further tightening supply at the top end.

Competitive gaps will widen through the decade. The fastest-growing slice—ultra-prime, ESG-certified assets—should track a 3.85% CAGR, underpinned by carbon-penalty regimes such as Local Law 97 that elevate compliant stock values. Vacancy inside Toronto’s AAA cluster, for instance, rests at 7.2% against citywide 18%. Investments in smart-building tech, wellness amenities, and on-site power resilience will cement pricing power for landlords in this tier, while older buildings head toward conversion or repricing.

By Transaction Type: Rentals prevail, but opportunistic sales accelerate

Rental contracts accounted for 77.40% of 2025 volume, signaling corporations’ preference for flexibility while they refine hybrid policies. Lease renewals dominated big-ticket activity, representing 68% of top-100 deals, as occupiers locked favorable terms without relocation disruption. The North America office real estate market size tied to leasing should expand modestly as tenants prioritize smaller but higher-quality footprints.

Sales transactions, although a smaller share, register the highest 3.95% CAGR over 2026-2031, propelled by discounted buying opportunities and cheaper debt post-rate cuts. Private-credit funds and equity REITs are mobilizing record capital to recapitalize properties unable to refinance. Notable moves include Office Properties Income Trust swapping 2025 notes for new 8% 2030 paper to shore up liquidity. Municipal conversion incentives are also spawning new deal flow outside the rent-versus-buy dichotomy, adding complexity to capital-allocation decisions.

By End Use: Tech sector reshapes demand physics

Information technology commanded 27.95% of 2025 leasing and embodies the fastest 4.05% CAGR to 2031, CBRE. Tech occupiers continue signing large leases—29 of the top 100 in 2024—yet they also spearhead AI-driven efficiency that spurs edge-data-center retrofits. Roughly 43% of enterprises now deploy AI for space-management analytics, tightening utilization metrics. The North America office real estate market size tied to IT will therefore split between conventional workspace and high-power data infrastructure inside urban shells.

Financial-services tenants remain pivotal. They dominate luxury leasing and are urgently chasing green-certified locations to satisfy Scope 3 targets, benefiting owners of LEED-Platinum towers. Professional-services firms maintain hybrid-friendly footprints with elevated collaboration areas, whereas life-science and energy players seek specialized build-outs resistant to commoditization. This diversification insulates landlords with mixed-use portfolios from sector-specific shocks.

Geography Analysis

The United States maintained 89.65% of 2025 spending in the North America office real estate market, buoyed by dense corporate clusters and an escalating return-to-office push. Manhattan continued to outperform: 28 leases surpassed USD 200 psf in 2024, nearly three times 2023’s volume. Yet recovery is uneven; Sun Belt metros such as Miami logged rent growth, while San Francisco values slid 18% amid persistent tech-sector remote work. Regulatory levers like New York City’s 467-m tax break and Local Law 97 shape asset repositioning economics, and a USD 929 billion refinancing wall looms over secondary U.S. markets.

Canada represents the second-largest slice of the North America office real estate market. Toronto recorded 650,000 sq ft positive absorption in 2024—its first yearly gain since 2019—yet overall national vacancy touched 18.3%. Construction sits at 20-year lows, signaling a supply pause while conversions accelerate. Calgary’s incentive plan aims to retire 6 million sq ft of surplus offices by 2031, offering a blueprint other Canadian cities may emulate.

Mexico is the fastest-growing geography, tracking a 4.32% CAGR through 2031 as nearshoring fuels record USD 36 billion FDI in 2023. Office demand in Monterrey, Guadalajara and Mexico City rides on manufacturing back-office needs and rising cross-border trade, which hit USD 286 billion with Texas alone in 2022. Northern industrial corridors show sub-2% vacancy after a new-build wave, and airport expansions reinforce the growth narrative. Persistent issues around water and security require risk-adjusted underwriting, but policy incentives and strategic location keep Mexico on investors’ radar.

Competitive Landscape

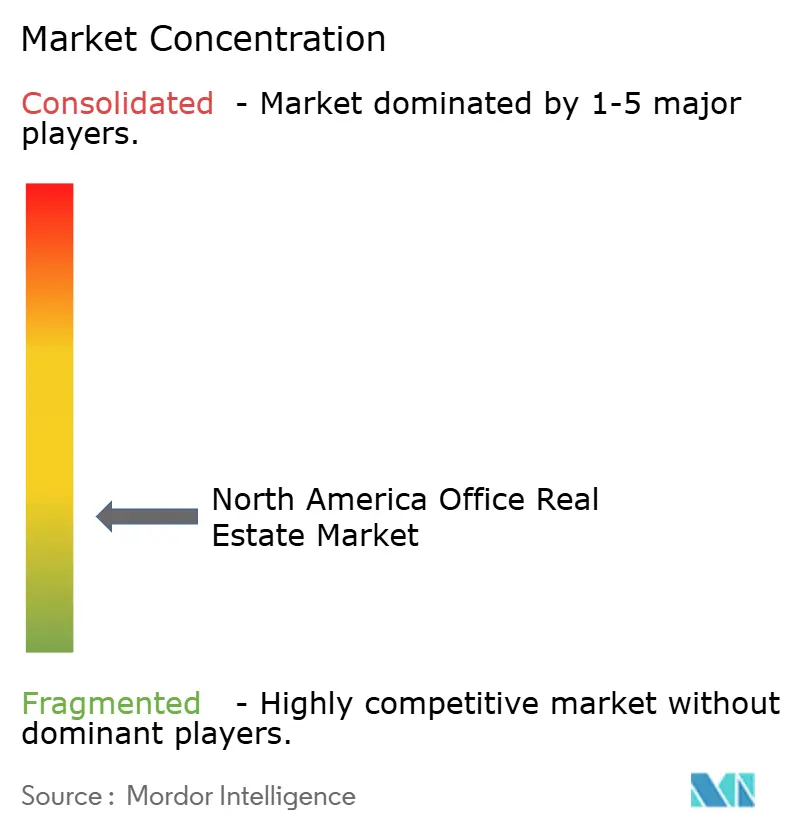

The North America office real estate market displays low concentration, yet market power is tilting toward institutional landlords able to fund retrofits and source inexpensive capital. Public REITs raised USD 84.7 billion in 2024 to acquire distressed stock, recycle out of non-core assets, and green-upgrade core holdings. Boston Properties reported 5.6 million sq ft of new leases even as it recognized USD 341 million in impairments, illustrating the bifurcation between trophy and secondary assets.

Technology implementation is becoming a critical differentiator. CBRE, Jones Lang LaSalle IP, and Cushman & Wakefield deploy AI-driven platforms for predictive maintenance and space planning, cutting operating expenses and improving tenant satisfaction. Landlords embracing smart-building upgrades secure longer lease terms from corporate occupiers aiming to enhance employee experience metrics. Adaptive-reuse leadership is also emerging: Brookfield and Hines are partnering with municipalities on office-to-residential conversions that tap local tax abatements.

Private-credit funds such as KKR are disintermediating traditional banks, supplying bridge-to-core financing at attractive spreads but tighter covenants. Their willingness to underwrite complex capital stacks gives well-capitalized buyers an edge in distressed auctions. Smaller owners lacking scale or ESG cap-ex capacity are increasingly forced into joint ventures or sales, ratcheting competitive intensity for prime assets in gateway cities.

North America Office Real Estate Industry Leaders

Hines

Brookfield Asset Management

BXP Inc.

SL Green Realty Corp.

Vornado Realty Trust

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: San Francisco enacted a Downtown Revitalization Financing District covering 1,200 offices eligible for conversion into approximately 4,400 homes.

- April 2025: CBRE Group posted USD 8.9 billion Q1 2025 revenue, up 12% YOY; U.S. office leasing rose 38%.

- March 2025: JLL logged 212 Manhattan leases above USD 100 psf in 2024, totaling 9.8 million sq ft; 28 exceeded USD 200 psf.

- February 2025: Office Properties Income Trust offered private exchanges into new 8% notes due 2030 worth up to USD 175 million.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America office real estate market as the aggregated annual transaction value of purpose-built office buildings, completed, under construction, or undergoing adaptive reuse, across the United States, Canada, and Mexico. Transactions include rental contracts, strata sales, and portfolio acquisitions in Grade A, B, and C stock.

Scope exclusion: assets primarily configured for logistics, data-center, or retail use after conversion are omitted from our baseline.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifescience, Energy, Legal)

- By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview REIT finance heads, corporate real-estate managers, construction contractors, and municipal assessors spanning gateway metros and high-growth secondary cities. These conversations validate headline rents, discount rates, and emerging retrofit costs, while short online surveys with occupiers test assumptions on hybrid-work driven space reduction.

Desk Research

We begin by mining open data from sources such as the U.S. Census Bureau, Statistics Canada, Mexico's INEGI, the Bureau of Labor Statistics, and Building Owners & Managers Association briefs, which reveal inventory, vacancy, and cost benchmarks. Industry white papers and quarterly office pulse reports issued by leading brokerages supplement construction pipelines, absorption swings, and grade-wise asking rents. Paid datasets, including company financials from D&B Hoovers and news archives on Dow Jones Factiva, help us reconcile deal values and cross-border capital flows. This list is indicative; many other publicly available releases and proprietary feeds inform our evidence base.

Market-Sizing & Forecasting

We anchor a top-down model that rebuilds market value from national building stock, average effective rent, and gross leasing volume, which are then adjusted for vacancy drift and sub-lease shadow space. Select bottom-up checks, REIT revenue roll-ups, sampled Grade A sales, and typical Class B cap-rate differentials tighten the totals. Key variables include quarterly net absorption, vacancy spreads between grades, construction starts, refinance maturities, average sale price per square foot, and GDP momentum. A multivariate regression blended with ARIMA captures cyclical drivers and structural shifts, before scenario filters from expert panels fine-tune the five-year view. Gaps where granular data are scarce (e.g. private building trades in tertiary cities) are bridged using peer-confirmed vacancy-to-rent elasticities.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst inspection, and senior sign-off. Models are refreshed annually; mid-cycle updates trigger on material events such as policy shocks or rate moves. A pre-delivery sense-check ensures clients always receive the freshest calibrated numbers.

Why Mordor's North America Office Real Estate Baseline Commands Reliability

Published estimates often diverge because firms select dissimilar property scopes, assume varied vacancy recovery curves, or freeze their exchange rates for longer than market reality allows.

Key gap drivers include: some publishers fold mixed-use towers into office totals, others model an aggressive hybrid-work contraction, and a few rely on list rents without vacancy discounts. Our scope stays office-only, our vacancy glidepath mirrors verified leasing data, and our annual refresh cadence curbs currency and inflation drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 412.98 B (2025) | Mordor Intelligence | - |

| USD 409.8 B (2024) | Global Consultancy A | Static FX conversion and older rent series |

| USD 1,050 B (2023) | Trade Journal B | Includes mixed-use and owner-occupied corporate campuses |

| USD 486 B (2024) | Industry Association C | Applies aggressive vacancy rebound, limited Canadian coverage |

In short, our disciplined property definition, transparent variable selection, and timely refreshes give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current North America office real estate market size?

The market is valued at about USD 427.49 billion in 2026 and is projected to reach USD 507.84 billion by 2031.

Which building grade leads leasing demand?

Grade A assets hold a 47.10% 2025 share and remain the prime target for occupiers seeking energy-efficient, amenity-rich space.

How significant is hybrid work in shaping demand?

Hybrid work models remain in use at 80% of firms, limiting average utilization to 38% of capacity and pressuring commodity offices.

Why are opportunistic investors active now?

Rate cuts and a USD 1.2 trillion refinancing wall have created discounted buying opportunities, with private-credit funds ready to deploy substantial capital.

Which geography is growing fastest?

Mexico is set to post a 4.32% CAGR through 2031 as nearshoring attracts record foreign direct investment and boosts office requirements.

What municipal policies affect office conversions?

Programs such as New York City’s 467-m tax incentive and Washington D.C.’s “Office to Anything” tax freeze are accelerating office-to-residential transformations to mitigate vacancy.

Page last updated on: