Ultrasonic Flow Meters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

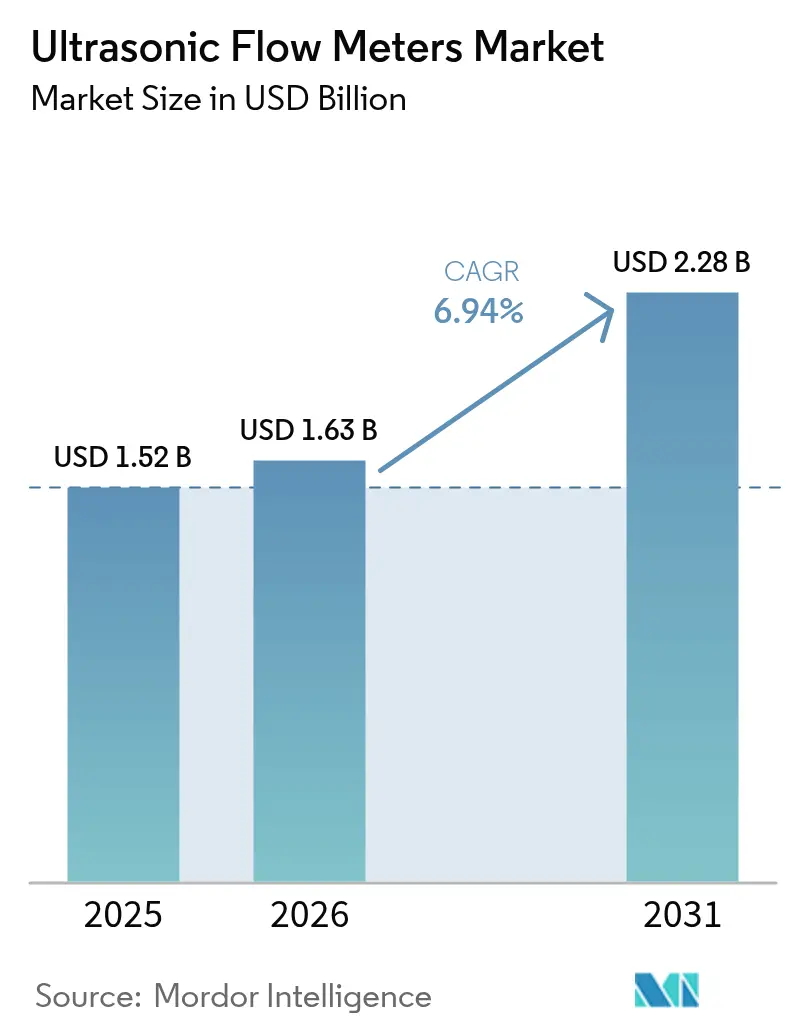

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.28 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

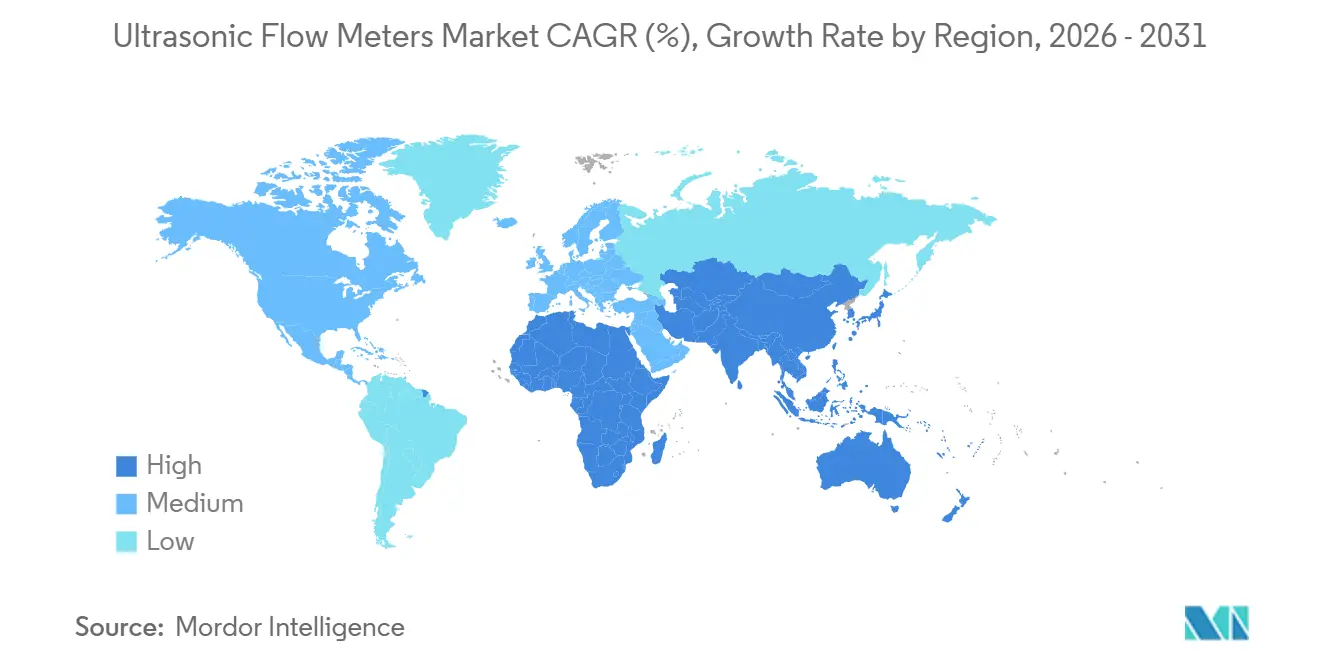

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

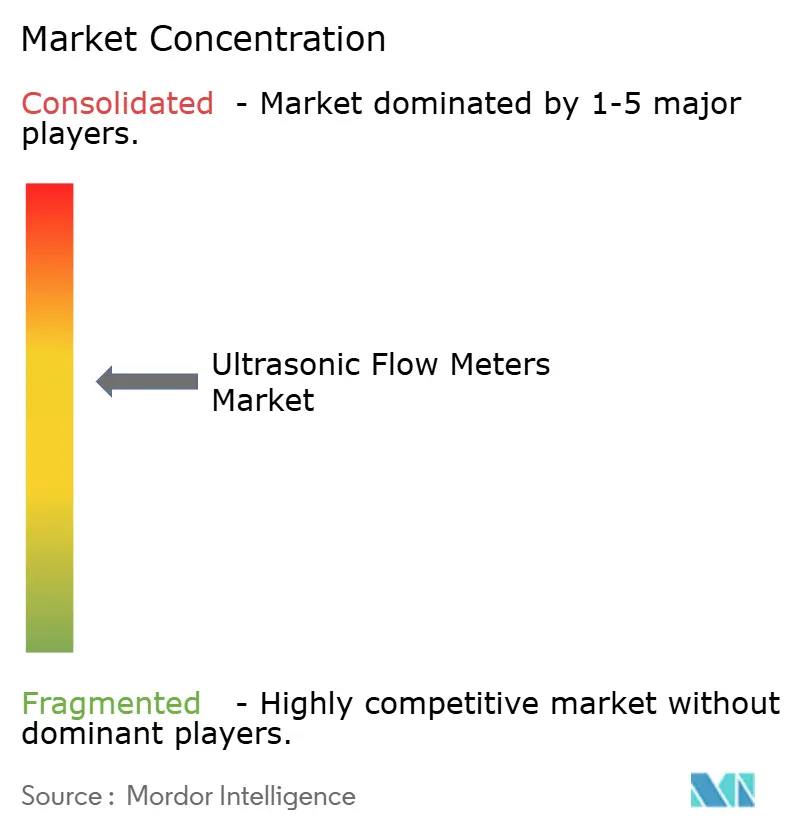

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrasonic Flow Meters Market Analysis by Mordor Intelligence

The ultrasonic flow meters market size was valued at USD 1.52 billion in 2025 and estimated to grow from USD 1.63 billion in 2026 to reach USD 2.28 billion by 2031, at a CAGR of 6.94% during the forecast period (2026-2031). Rising demand for non-invasive retrofit solutions, hydrogen-ready measurement in natural gas grids, and real-time leak detection in water-stressed utilities is accelerating equipment replacement cycles. Clamp-on devices are expanding fastest because they can be installed without hot-work permits or service interruptions, while multipath architectures are becoming the default for custody transfer as operators target ±0.7% fiscal-uncertainty limits. Edge-AI diagnostics embedded in next-generation meters are doubling inspection intervals and cutting unplanned outages by more than one-third, which tightens the total-cost-of-ownership case versus legacy differential-pressure or turbine designs. Parallel policy actions California’s 12-inch main monitoring rule, zero-liquid-discharge mandates in India and China, and the European Union’s stricter Industrial Emissions Directive, are further repositioning ultrasonic technology from a premium option to a baseline compliance tool across energy, water, and chemical sectors.

Key Report Takeaways

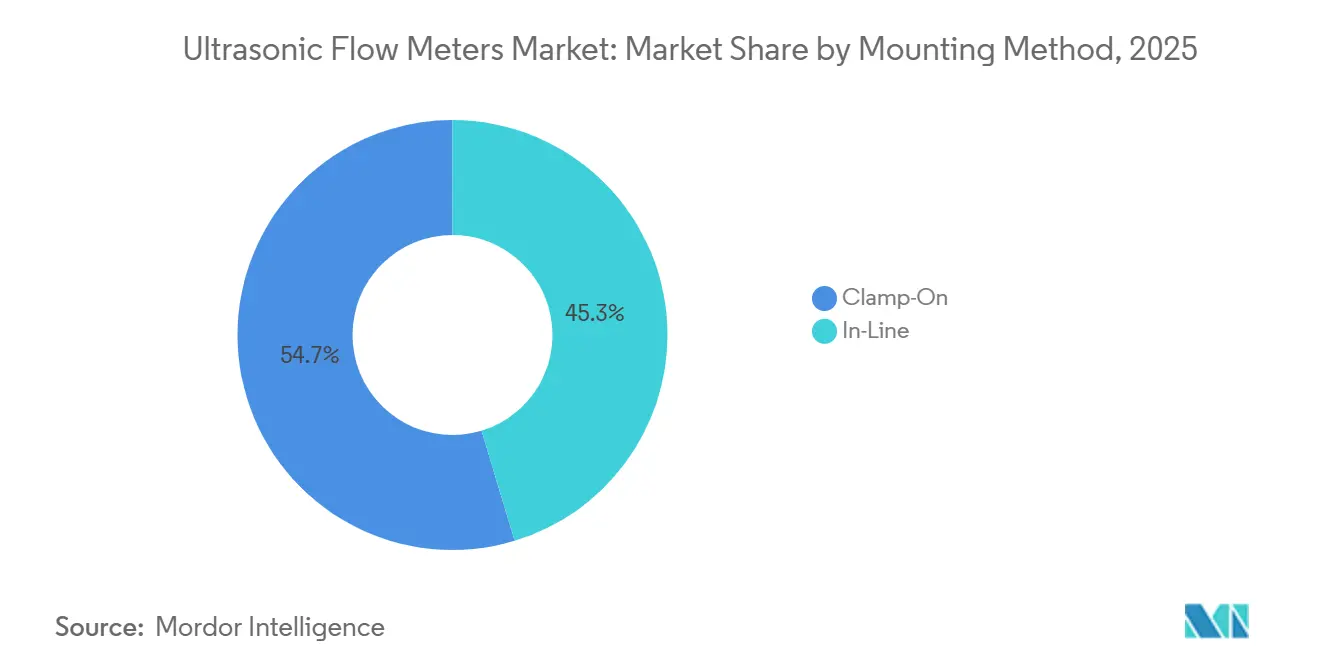

- By mounting method, clamp-on configurations led with 54.67% share in 2025 and are projected to advance at a 7.11% CAGR through 2031.

- By measurement technology, transit-time meters dominated with 63.89% of the ultrasonic flow meters market share in 2025, while hybrid and multipath designs are expected to post the fastest 7.34% CAGR to 2031.

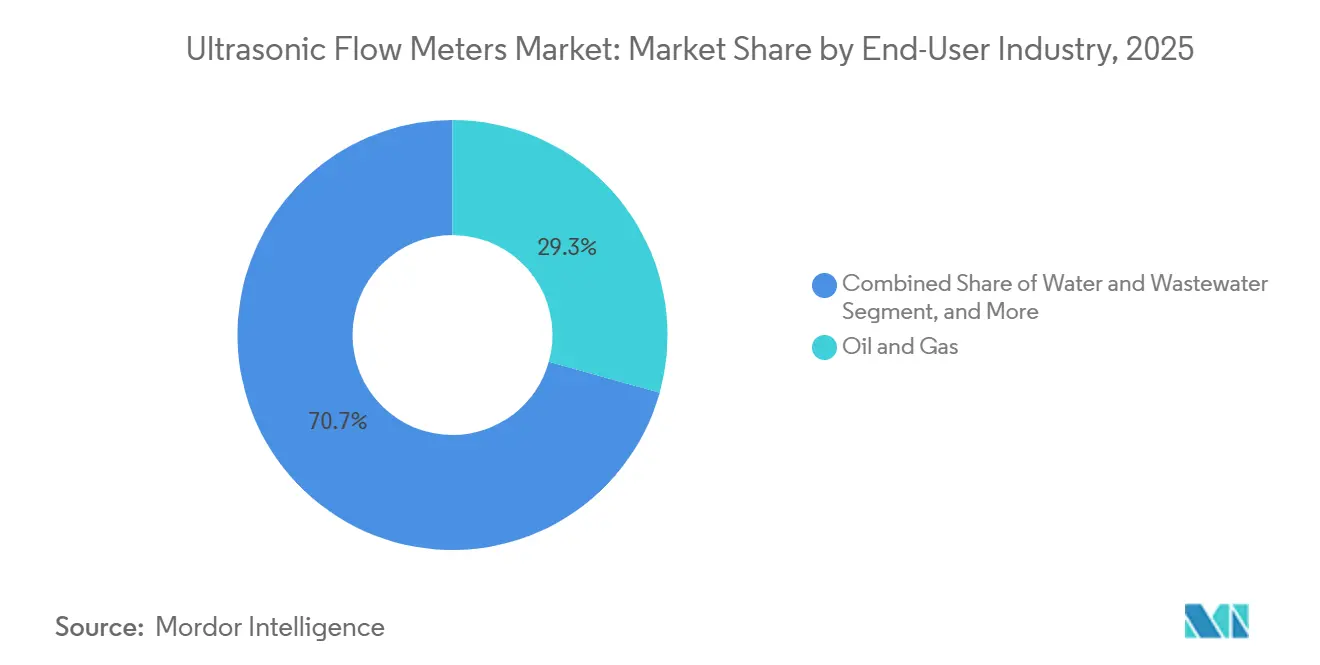

- By end-user industry, oil and gas accounted for the largest 29.32% share in 2025; water and wastewater is set to record the highest 7.92% CAGR over 2026-2031.

- By number of acoustic paths, multipath meters captured a 56.83% of the ultrasonic flow meters market share in 2025 and are forecast to grow at a 7.54% CAGR through 2031.

- By geography, North America commanded 36.91% of the revenue share in 2025, whereas the Asia-Pacific is anticipated to register the fastest 7.96% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultrasonic Flow Meters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift to Custody-Transfer-Grade Ultrasonic Meters in Large-Diameter Gas Pipelines | +1.8% | North America, Europe, Middle East | Medium term (2-4 years) |

| Rapid Retrofit Demand for Non-Invasive Clamp-On Meters in Water-Stress Hotspots | +1.5% | North America (Southwest US), Middle East, Asia-Pacific (India, China) | Short term (≤ 2 years) |

| Hydrogen-Ready Ultrasonic Designs Enable Early-Mover Advantage in Energy Transition | +1.2% | Europe, Asia-Pacific (Japan, South Korea), select North America projects | Long term (≥ 4 years) |

| Edge-AI Self-Diagnostics Cut OPEX for Utilities and Boost Predictive Maintenance Adoption | +0.9% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Mandatory Zero-Liquid-Discharge Policies Push High-Accuracy Flow Control in Chemicals | +0.7% | Asia-Pacific (India, China), Middle East, select EU member states | Short term (≤ 2 years) |

| OEM-Embedded Ultrasonic Transmitters in Smart Pumps Expand Addressable OEM Market | +0.5% | Global, led by Germany, United States, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Custody-Transfer-Grade Ultrasonic Meters in Large-Diameter Gas Pipelines

Interstate and cross-border pipeline operators in North America and Europe are retiring turbine and orifice-plate meters in favor of 4- to 8-path ultrasonic designs that achieve ±0.5% accuracy under the tighter ±0.7% fiscal-uncertainty limit set by the 2024 revision of AGA Report 9.[1]American Gas Association, “AGA Report No. 9: Measurement of Gas by Multipath Ultrasonic Meters,” AGA.ORG Liquefied natural gas terminals have been early adopters because every 0.1% error in a cargo transfer worth more than USD 10 million can spark costly revenue disputes. Operators also favor the technology’s solid-state architecture, which doubles inspection intervals and eliminates pressure-drop energy losses, yielding lifecycle savings that offset its higher purchase price. In 2025, European transmission system operators installed 22% more ultrasonic units on interconnectors to reconcile metering data across national grids that apply different regulatory accounting rules. These moves have turned multipath ultrasonic meters into the default specification for new gas pipeline projects worldwide.

Rapid Retrofit Demand for Non-Invasive Clamp-On Meters in Water-Stress Hotspots

Drought-affected utilities are deploying clamp-on ultrasonic meters to pinpoint non-revenue water without cutting service, a critical advantage where any outage triggers public backlash. California utilities installed more than 3,500 units in 2025 to meet the state mandate for real-time monitoring of mains above 12 inches, completing each installation in under 2 hours and avoiding hot-work permits.[2]California Department of Water Resources, “Urban Water Use Efficiency Regulations,” WATER.CA.GOV Dubai Electricity and Water Authority echoed this approach, installing 1,200 clamp-on meters as part of a USD 180 million leakage-reduction drive that targets 10% savings by 2028. Industrial campuses such as semiconductor fabs and hyperscale data centers mirror the trend because nondisruptive retrofits preserve uptime worth up to USD 100,000 per hour. As battery-powered, cellular-enabled models proliferate, technicians can now conduct temporary flow surveys in remote areas without electrical infrastructure, broadening the addressable market.

Hydrogen-Ready Ultrasonic Designs Enable Early-Mover Advantage in Energy Transition

European and Japanese regulators now insist that new custody-transfer meters maintain ±1.0% accuracy when natural gas pipelines carry up to 20% hydrogen by volume, a threshold that legacy turbine devices cannot meet.[3]FNB Gas, “Technical Guidelines for Hydrogen-Ready Pipeline Metering,” FNB-GAS.DE Ultrasonic meters pass this test because acoustic velocity calculations remain stable across changing gas densities and because hydrogen-resistant transducer materials prevent embrittlement. KROHNE and Endress+Hauser secured early contracts in the Netherlands and Belgium after winning OIML R 137-1 hydrogen certification for their multipath models in late 2024. Japan’s Ministry of Economy, Trade and Industry extended the same requirement to all DN 300 pipelines starting January 2026, creating a captive market for 800-1,000 units annually through 2031. Operators favor buying hydrogen-ready meters now rather than paying three to four times more to retrofit within five years.

Edge-AI Self-Diagnostics Cut OPEX for Utilities and Boost Predictive Maintenance Adoption

Next-generation ultrasonic meters embed machine-learning algorithms that analyze acoustic signal health in real time and flag developing faults up to six weeks before accuracy drifts beyond calibration limits. Emerson’s Rosemount 8800 line reduced unplanned outages by 35% across a dozen North Sea platforms in 2025, saving about USD 2.3 million per site by allowing maintenance to coincide with planned shutdowns. Water utilities use the same diagnostics to identify turbulence hot spots that signal imminent pipe failures, guiding capital spending toward the riskiest mains. Because the analytics reside at the meter head, alerts continue even if the control network is offline, addressing cyber-resilience concerns in critical infrastructure. The resulting OPEX reductions strengthen the return-on-investment case for higher-priced ultrasonic units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial CAPEX vs. Legacy DP/Turbine Meters | -1.1% | Global, acute in South America, Africa, Southeast Asia | Short term (≤ 2 years) |

| Accuracy Drift in Multiphase / Slurry Service Without Advanced Signal Conditioning | -0.6% | Oil and gas upstream, Mining, Pulp and paper | Medium term (2-4 years) |

| Scarcity of Accredited Calibration Labs Above DN 1000 in Emerging Regions | -0.4% | Middle East, Africa, South America, parts of Asia-Pacific | Long term (≥ 4 years) |

| Cyber-Security Concerns over IIoT-Connected Meters in Critical Infrastructure | -0.3% | Global, heightened in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX vs. Legacy DP/Turbine Meters

A custody-transfer-grade 8-path ultrasonic meter for a DN 600 gas line lists at USD 45,000-65,000, roughly 50% more than an equivalent turbine meter, deterring budget-constrained utilities despite lower lifetime costs. Although ultrasonic designs eliminate pressure-drop energy losses worth USD 8,000-12,000 per year and cut maintenance by 60%, many water utilities in South America, Africa, and Southeast Asia cannot finance the higher upfront outlay. A 2025 World Bank survey of 140 utilities in India, Indonesia, and Kenya found 68% citing purchase price as the main adoption barrier, even when donors offered 50% capital subsidies. Chinese and South Korean manufacturers have introduced lower-cost models priced 25% below those of Western incumbents, yet lingering doubts about quality and after-sales support limit their penetration in mission-critical custody-transfer applications. As a result, the premium remains a structural drag on near-term growth in emerging regions.

Accuracy Drift in Multiphase or Slurry Service Without Advanced Signal Conditioning

Standard transit-time ultrasonic meters assume single-phase, homogeneous fluids; once gas void fractions exceed 2 % or solids exceed 5,000 ppm, measurement uncertainty can spike beyond ±5 %. Doppler variants tolerate higher solids but only achieve ±3-5 % accuracy, unacceptable for fiscal metering in upstream oil and gas or mineral-slurry pipelines. Hybrid units with sophisticated signal processors and redundant transducer arrays can correct for scattering and refraction effects, yet they cost 50-80% more than baseline models, curbing uptake in high-value wells and critical process loops. Operators in the Permian Basin and the North Sea reported replacing conventional ultrasonic meters on multiphase flowlines within 18 months due to chronic under-reading that distorted production accounting. Until low-cost, robust signal-conditioning solutions mature, mechanical or Coriolis meters will retain a share of the market in severe-service applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mounting Method: Clamp-On Retrofits Outpace Inline Installations

Clamp-on configurations commanded a 54.67% market share of ultrasonic flow meters in 2025, reflecting sustained preference for tools that eliminate hot-work permits and process shutdowns. Utilities in drought-prone U.S. states can now fit as many as 15 clamp-on meters per day because technicians can couple transducers in less than 2 hours and resume service immediately, a workflow impossible with inline units that require pipe cutting. California’s 12-inch main monitoring rule alone created demand for 4,500-5,500 additional devices, underscoring how policy quickly converts into purchase orders. Petrochemical sites echo the trend, as zero-liquid-discharge retrofits seek non-invasive metering to avoid lost production worth USD 50,000-150,000 per shutdown. The appeal extends to data-center cooling loops and semiconductor fabs, where contamination risk makes external sensors the only acceptable option.

Inline meters, however, remain indispensable for the fiscal hand-off because welded spool pieces ensure long-term positional stability and enable the intricate multipath internals required for ±0.5% custody-transfer accuracy. Midstream operators and LNG terminals purchased 60% of 2025 inline volume, typically specifying 4- to 8-path designs that meet AGA 9 and ISO 17089-1 traceability requirements. Although an inline spool costs more up front, its 25-year service life and self-diagnostics offset the installation premium over time. As a result, the ultrasonic flow meters market size for inline units still expanded in absolute terms, but the growth gap versus clamp-on models widened to almost a full percentage point in 2025. Going forward, edge-AI diagnostics that cut biennial maintenance visits in half may slow clamp-on gains by making permanent spools even more desirable for high-stakes service.

By Measurement Technology: Hybrid Multipath Designs Lead Fiscal Upgrades

Transit-time instruments retained 63.89% of the ultrasonic flow meter market share in 2025, driven by ±0.5% accuracy in clean liquids and gases. Their solid-state architecture eliminates pressure drop energy losses and moving part wear, making them the default choice for water distribution, HVAC balancing, and process utilities. Doppler models carved out an 18% niche in mining, pulp and paper, and municipal sludge lines where suspended solids exceed 5,000 ppm and ±3% precision suffices for process control. Operators appreciate Doppler’s tolerance for entrained bubbles, even though fiscal applications avoid the technology because of its poorer linearity.

Hybrid and multipath meters are the clear growth engine, advancing at a 7.34% CAGR as pipeline operators and chemical terminals respond to the tighter ±0.7% fiscal-uncertainty limit set by the 2024 AGA 9 revision. Redundant acoustic paths distribute measurement across the full cross-section, compensating for swirl and jetting that distort single-path readings. The design’s built-in statistical checks also trigger early fouling alarms, reducing false positives by half and supporting unmanned offshore assets where a helicopter callout costs USD 10,000 or more. As hydrogen blending spreads, multipath variants gain another edge because they maintain accuracy across changing gas densities without recalibration. This performance premium keeps the ultrasonic flow meters market size for hybrid solutions on a steeper trajectory than any other technology class through 2031.

By End-User Industry: Water Utilities Post Fastest Gains Under Leak-Reduction Mandates

Oil and gas remained the largest buyer, accounting for 29.32% of 2025 shipments as interstate pipelines completed migrating from turbine to ultrasonic custody-transfer metering. Purchase volume, however, is shifting downstream to LNG terminals and terminal loading racks where single-phase conditions avoid multiphase drift issues. Water and wastewater utilities are the breakout story, logging a forecast 7.92% CAGR, driven by statewide mandates in California, Texas, and Arizona requiring real-time monitoring of trunk mains. North American utilities alone placed more than 3,500 orders in 2025, while Saudi Arabia’s National Water Company bought 3,200 units for Riyadh and Jeddah leakage-reduction programs.

Chemical and petrochemical operators, representing 22% of demand, continue upgrading effluent lines to meet zero-liquid-discharge rules in India and China that specify ±2% accuracy. Ultrasonic technology’s immunity to fouling and its lack of moving parts give it a lifecycle advantage over mechanical meters that can seize in slurry streams. Industrial users in food, beverage, and HVAC account for another 18%, often choosing embedded sensors supplied with smart pumps that optimize energy use in real time. Collectively, these shifts are expanding the ultrasonic flow meters market faster for compliance-driven applications than for traditional fiscal metering, diversifying vendor revenue across multiple verticals.

By Number of Paths: Multipath Meters Secure Custody-Transfer Premium

Single-path devices still serve routine monitoring in HVAC loops and secondary water mains because they cost 50%-60% less and reach ±1.5%-2.0% accuracy, which suffices when financial settlement is not on the line. They held a 43.17% share in 2025, but their trajectory is flattening as utility managers seek more built-in diagnostics. Multipath designs, by contrast, captured 56.83% of the ultrasonic flow meters market share in 2025 and are projected to grow at a 7.54% CAGR through 2031. Four, six, or eight chords triangulate velocity, smoothing turbulence effects and producing custody-transfer-grade results without external flow conditioners.

Transmission system operators in Europe report a 35% drop in fiscal disputes since adopting multipath devices that audit themselves by comparing each chord’s reading for abnormal deviations. Hydrogen blending adds another tailwind because redundant paths preserve accuracy across density shifts better than single-chord models. Vendors also bundle edge AI that mines multipath data for early signs of fouling, allowing maintenance crews to intervene during planned outages rather than react to failures. These performance gains convince pipeline and refinery engineers that the higher capital outlay delivers a superior net present value, sustaining the larger ultrasonic flow meters market size segment well into the next decade.

Geography Analysis

North America retained the leading 36.91% market share in ultrasonic flow meters in 2025, as interstate gas pipelines completed turbine-to-multipath upgrades and drought-hit states accelerated clamp-on retrofits for leak detection. The United States accounted for roughly three-quarters of regional sales, supported by California’s rule requiring all distribution mains above 12 inches to carry real-time monitors, a measure that alone would require more than 3,500 new units in 2025. LNG export build-outs in British Columbia and Alberta lifted Canadian demand, while Pemex modernization projects accounted for Mexico’s modest contribution. These combined drivers keep the North American ultrasonic flow meters market size on a mid-single-digit growth path through 2031 as replacement cycles and hydrogen-blend pilots add incremental volume.

Europe followed with roughly 28% of 2025 revenue, underpinned by hydrogen-ready pipeline retrofits in Germany, the Netherlands, and Belgium, and by multipath installations at chemical loading terminals mandated under the revised Industrial Emissions Directive effective January 2026. Regional operators favor 4- to 8-path meters that meet both fiscal-accuracy and hydrogen-compatibility guidelines, helping the European ultrasonic flow meters market maintain steady growth despite overall infrastructure maturity. Zero-liquid-discharge rules in Italy, France, and Spain further buoy demand from petrochemical clusters that must install ±2% accurate effluent meters. Together, these policy anchors reduce reliance on greenfield projects and shift spending toward high-specification replacements, thereby lifting average selling prices.

Asia-Pacific is the fastest-growing region, with a projected 7.96% CAGR, driven by India’s and China’s water-conservation and effluent-monitoring mandates, as well as LNG import expansions across Southeast Asia. Japan’s January 2026 order that all new DN 300 pipelines be hydrogen-ready creates a captive market for 800-1,000 units a year, while South Korean and Philippine LNG terminals add custody-transfer demand. The Middle East and Africa together held about 15% of the 2025 share, as Saudi Arabia deployed 3,200 meters in Riyadh and Jeddah leakage programs, though large-diameter calibration capacity gaps still slow uptake above DN 1000. South America accounted for 6% share, anchored by Petrobras pipeline upgrades in Brazil and municipal water projects in São Paulo and Rio de Janeiro, but fiscal constraints limit broader regional roll-outs. Overall, divergent regulatory timelines mean absolute shipments rise fastest in Asia-Pacific, yet North America and Europe continue to command the bulk of high-margin custody-transfer orders.

Competitive Landscape

The ultrasonic flow meters market shows moderate concentration, with Emerson Electric, Endress+Hauser, Siemens, KROHNE, and ABB jointly accounting for about 45-50% of global revenue in 2025. These conglomerates bundle meters with control systems and analytics suites, creating switching costs that lock customers into multi-decade service contracts and support premium pricing. Emerson’s Plantweb and Siemens’ SIMATIC PCS neo ecosystems typify this strategy, delivering double-digit energy and maintenance savings compared with standalone instrumentation.

Strategic investments underscore the race for capacity and technology leadership. Siemens committed EUR 45 million (USD 47.7 million) to enlarge its Karlsruhe plant, raising yearly output to 24,300 multipath units by 2027. Emerson completed its USD 8.2 billion acquisition of NI in September 2025, folding advanced test-and-measurement software into its Rosemount line to bolster edge-AI diagnostics. KROHNE captured early market share in hydrogen after obtaining OIML R 137-1 certification for the OPTISONIC 8300 series and winning a USD 28 million Saudi Aramco order for the Jafurah gas project. These moves reinforce incumbents’ ability to defend their share even as average lot sizes grow and application complexity rises.

Yet competitive pressure is intensifying from specialists and low-cost regional entrants. FLEXIM, SICK, and Bronkhorst together hold nearly a 30% share across the portable clamp-on, compact OEM, and high-temperature niches, leveraging agility that larger rivals often lack. Chinese and South Korean suppliers offer transit-time meters priced 25-30% below Western brands, appealing to price-sensitive water utilities in Southeast Asia, though service support gaps still bar them from bidding for custody-transfer contracts. Meanwhile, pump and valve makers are embedding miniature ultrasonic transmitters at the factory, shifting part of future growth to OEM channels and forcing traditional meter vendors to negotiate component supply deals rather than end-user replacements. Heightened R&D intensity is evident in 47 ultrasonic-related patents filed by Emerson, Endress+Hauser, and Siemens during 2024-2025 that target hydrogen-resistant materials and on-board machine learning.

Ultrasonic Flow Meters Industry Leaders

ABB Ltd.

Baker Hughes Company

Emerson Electric Co.

Endress+Hauser Group Services AG

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Endress+Hauser unveiled the Proline Promass X 500 range featuring hydrogen-ready certification and edge-AI fouling alerts.

- December 2025: Siemens committed EUR 45 million (USD 47.7 million) to expand ultrasonic meter production in Karlsruhe, Germany, targeting an extra 6,300 custody-transfer units per year by 2027.

- October 2025: KROHNE won a USD 28 million order from Saudi Aramco to supply 450 multipath meters for the Jafurah gas project, with deliveries extending through 2027.

- September 2025: Emerson Electric closed its USD 8.2 billion acquisition of NI, integrating advanced test-and-measurement software into its Rosemount portfolio.

Global Ultrasonic Flow Meters Market Report Scope

The Ultrasonic Flow Meters Market Report is Segmented by Mounting Method (Clamp-On, and In-Line), Measurement Technology (Transit-Time, Doppler, Hybrid/Multipath), End-User Industry (Oil and Gas, Water and Wastewater, Chemical and Petrochemical, Industrial, Other End-User Industries), Number of Paths (Single-Path, and Multi-Path), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Clamp-On |

| In-Line |

| Transit-Time |

| Doppler |

| Hybrid / Multipath |

| Oil and Gas |

| Water and Wastewater |

| Chemical and Petrochemical |

| Industrial |

| Other End-User Industries |

| Single-Path |

| Multi-Path |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Mounting Method | Clamp-On | ||

| In-Line | |||

| By Measurement Technology | Transit-Time | ||

| Doppler | |||

| Hybrid / Multipath | |||

| By End-User Industry | Oil and Gas | ||

| Water and Wastewater | |||

| Chemical and Petrochemical | |||

| Industrial | |||

| Other End-User Industries | |||

| By Number of Paths | Single-Path | ||

| Multi-Path | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the ultrasonic flow meters market be by 2031?

The ultrasonic flow meters market size is forecast to reach USD 2.28 billion by 2031, reflecting a 6.94% CAGR over 2026-2031.

Which mounting method is growing the fastest?

Clamp-on devices are projected to expand at 7.11% CAGR because they avoid shutdowns and hot-work permits during retrofit installation.

Why are multipath meters preferred for custody transfer?

Four- to eight-path designs meet the tighter ±0.7% fiscal-uncertainty limits set by AGA 9 and ISO 17089-1, while delivering built-in self-diagnostics.

What role does hydrogen blending play in market growth?

Hydrogen-ready transmission projects in Europe and Japan require meters that maintain accuracy across 0%-20% hydrogen, boosting demand for ultrasonic units certified under ISO 12213-2.

Which region will post the highest growth rate?

Asia-Pacific is projected to grow at 7.96% CAGR through 2031, driven by India’s and China’s zero-liquid-discharge regulations and LNG infrastructure build-outs.

How do edge-AI diagnostics reduce operating costs?

Embedded analytics detect fouling or signal degradation weeks in advance, trimming unplanned shutdowns by up to 35% and doubling maintenance intervals.

Page last updated on: