Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

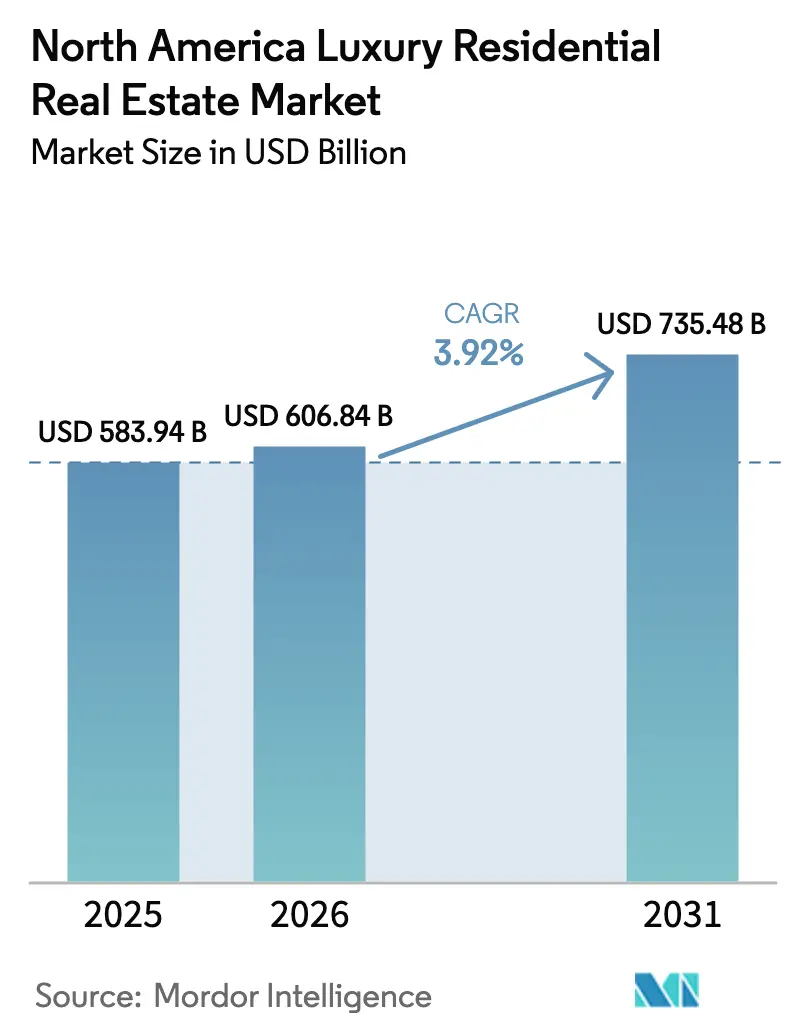

| Base Year Market Size (2025) | USD 583.94 Billion |

| Market Size (2026) | USD 606.84 Billion |

| Market Size (2031) | USD 735.48 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

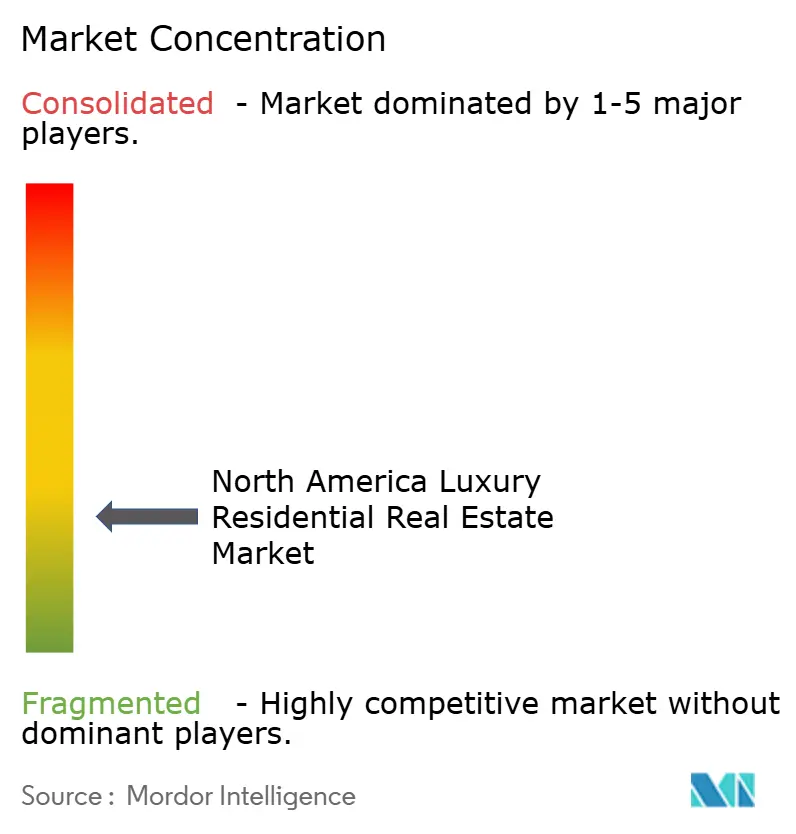

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The North America Luxury Residential Real Estate Market size was valued at USD 583.94 billion in 2025 and estimated to grow from USD 606.84 billion in 2026 to reach USD 735.48 billion by 2031, at a CAGR of 3.92% during the forecast period (2026-2031). Growing millionaire migration, tokenized ownership pilots, and a reallocation of institutional capital from offices to high-end housing are reshaping competitive dynamics. Fractionalization lowers the minimum ticket size, broadening the buyer base and adding liquidity. Sunbelt inflows have pushed prime home prices in Miami, Austin, and Las Vegas to record highs, while zero-income-tax policies reinforce the shift. At the same time, ESG mandates are steering developers toward WELL- and LEED-certified schemes that command pricing premiums and support longer-term value preservation.

Key Report Takeaways

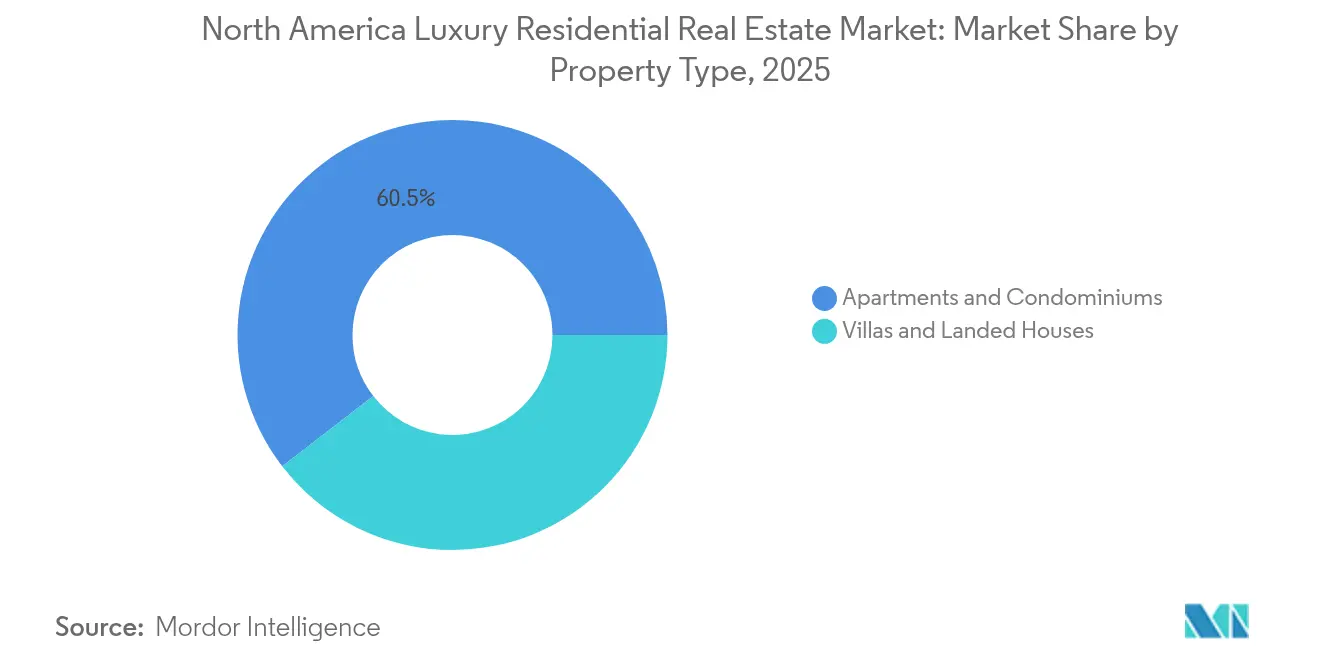

- By property type, apartments and condominiums led with a 60.45% North America luxury residential real estate market share in 2025, while villas and landed houses deliver the fastest 4.05% CAGR to 2031.

- By business model, the sales segment held 69.20% of the North America luxury residential real estate market size in 2025; rentals are expanding at a 4.12% CAGR through 2031.

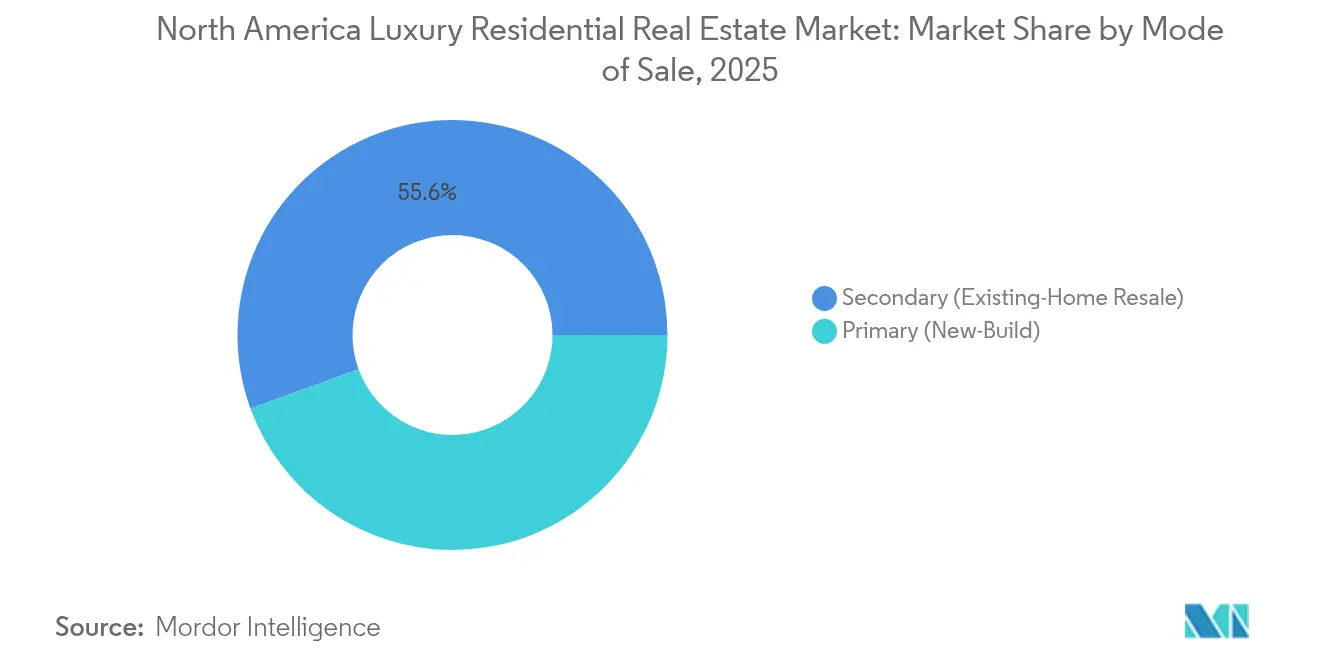

- By mode of sale, secondary transactions accounted for 55.55% of the North America luxury residential real estate market in 2025, whereas primary developments recorded a 4.18% CAGR.

- By geography, the United States dominated with 78.60% revenue share in 2025; Mexico posts the swiftest 4.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-income-tax Sunbelt migration | +1.2% | Florida, Texas, Nevada; spillover to Mexico | Short term (≤ 2 years) |

| Geopolitical capital flight of UHNWIs | +0.9% | US and Canadian gateway metros | Medium term (2-4 years) |

| Tokenized luxury pipelines unlocking fractional ownership | +0.8% | US & Canada gateway cities | Medium term (2-4 years) |

| Post-pandemic estate expansions | +0.6% | US suburban luxury belts | Short term (≤ 2 years) |

| Institutional ESG mandates pushing WELL Platinum supply | +0.5% | Urban cores in US & Canada | Long term (≥ 4 years) |

| Luxury build-to-rent resorts for digital nomads | +0.4% | US coasts & ski markets, Canadian resorts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

USD 1 trillion tokenized luxury pipelines unlocking fractional ownership

Blockchain-enabled tokenization is lowering entry barriers by splitting prime residences into digital shares that can be traded without conventional escrow delays. Deloitte highlights that a single Canadian tower raised USD 300 million through token sales, demonstrating institutional appetite for the model. Smart contracts automate dividend distribution and compliance checks, cutting middle-agent costs. The St. Regis Aspen precedent further eases regulatory concerns, and North American securities watchdogs are drafting sandbox frameworks expected to go live within three years. Taken together, tokenization increases velocity of capital and broadens participation in the North America luxury residential real estate market.

Surging demand for zero-income-tax Sunbelt states

Florida captured 29,771 high-income households averaging USD 907,013 in adjusted gross income during the latest filing year. Texas and Nevada post similar trends, propelled by corporate relocations such as Citadel’s headquarters move to Miami. Over six hundred USD 10 million-plus closings in South Florida last year underscore structural rather than seasonal demand. Builders respond with turnkey condos offering marina berths and private wellness suites, inflating land prices yet sustaining absorption. The pattern accelerates cross-border interest in Mexican resort towns, reinforcing the North America luxury residential real estate market’s Sunbelt bias[1]Ryan Sherrill, “Domestic Migration Flows by Income Group,” Internal Revenue Service Statistics of Income, irs.gov.

Geopolitical capital flight of UHNWIs from LATAM & APAC

Henley & Partners forecasts 142,000 high-net-worth relocations in 2025, an all-time peak, with 7,500 heading to the US and 3,200 to Canada. Vancouver benefits from its Asian diaspora base, while New York and Los Angeles remain safe-haven hubs despite tax headwinds. Multiple-property purchases are common, lifting transaction volumes in both primary and secondary brackets. This inflow underpins steady demand even during equity-market swings, cementing the North America luxury residential real estate market as a global wealth reservoir.

Institutional ESG mandates accelerating WELL Platinum projects

WELL-certified inventory is still under 9% of global certified floor area, signalling room to scale. Hines pledges net-zero operational carbon across its USD 62.16 billion portfolio and delivered New York’s greenest residential tower last year. Oxford Properties embeds decarbonisation plans in more than half of its USD 62.16 billion assets, channelling capital toward heat-pump systems, biophilic design, and low-carbon concrete. Energy-efficient homes cut operating costs 20-30%, supporting price resilience and broadening the investor pool for the North America luxury residential real estate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proposed mansion & vacancy taxes | -0.7% | Select US metros; Vancouver, Toronto, Honolulu | Short term (≤ 2 years) |

| Equity-market volatility cutting stock-option buys | -0.6% | US tech hubs; Canadian finance centers | Short term (≤ 2 years) |

| Supply crunch in imported bespoke finishes | -0.5% | North America with global inputs | Medium term (2-4 years) |

| Escalating WELL/LEED compliance costs | -0.3% | Urban luxury corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proposed mansion & vacancy taxes in major metros

In Los Angeles, a new tax called Measure ULA, aimed at property sales over USD 5 million, led to a steep 68% drop in those sales within a year. The tax only managed to raise USD 215 million, which was much lower than expected. On the other hand, Honolulu is considering a 3% tax on vacant homes, which could bring in up to USD 306 million in revenue. Investors may route capital toward lower-tax jurisdictions, dampening short-run price momentum in affected nodes of the North America luxury residential real estate market.

Supply crunch in imported bespoke finishes

Italian marble waste surpasses 70% of quarried volume, inflating extraction and logistics costs. Steel prices leapt 11.2% last year, while lumber tariffs added USD 3,000 to each multifamily unit. Smart-glass capacity remains limited to a handful of plants globally, stretching lead times for curtain-wall residences. Developers either accept margin compression or raise asking prices, tempering absorption in parts of the North America luxury residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Condominiums command urban dominance while villas accelerate suburban sprawl

Apartments and condominiums held a 60.45% slice of the North America luxury residential real estate market in 2025, propelled by demand for lock-and-leave convenience, shared security, and amenity-rich towers. Vista Pointe on New Jersey’s Gold Coast exemplifies the model with 73 glass-wrapped units, an infinity pool, and a 24-hour concierge. Institutional buyers back such schemes for stable rental yields, reinforcing pipeline depth. Secondary resales remain active, especially for branded residences that preserve service standards over time. At the opposite end, villas and landed houses outpace at a 4.05% CAGR as clients seek acreage for wellness pavilions and multigenerational living.

Estate lots in Palm Beach, Scottsdale, and Muskoka now feature accessory dwelling units and tech-integrated spas, lifting replacement costs and resale potential. Developers pivot with gated communities offering curated landscaping and private docks, blending privacy with community governance. This mix enables villas to capture lifestyle-centric spending, a tailwind for the overall North America luxury residential real estate market expansion.

By Business Model: Sales supremacy meets rental agility

Sales transactions comprised 69.20% of the North America luxury residential real estate market in 2025, reflecting the asset-preservation instinct of UHNWIs and family offices. Trophy purchases hedge inflation and provide inter-generational wealth storage, keeping turnover healthy even when rates rise. Meanwhile, rentals log a 4.12% CAGR as flexibility gains favour. Build-to-rent resorts in Jackson Hole and Whistler furnish five-star services without ownership burdens, an attractive set-up for globe-trotters.

Developers secure long-dated credit lines and structure lease programs with hospitality operators, aligning cash flows with investor demands. Younger millionaires rotate between tech hubs and leisure hotspots, sustaining occupancy. Rental platforms also test blockchain-driven security-deposit models that speed check-in and reduce friction. Both channels coexist, broadening the audience for the North America luxury residential real estate market.

By Mode of Sale: Secondary maturity versus primary innovation

Secondary deals represented 55.55% of transactions in 2025, confirming ample legacy stock across high-end zip codes. Historic co-ops on Central Park West and 1990s-era penthouses in Toronto trade at premiums when retrofit with smart-home upgrades. Familiar neighbourhood brands, school districts, and cultural institutions anchor liquidity.

Primary developments, however, move ahead at a 4.18% CAGR, often wrapped in global hotel brands that deliver food-and-beverage, yacht-charter concierge, and medical partnerships. Waldorf Astoria Residences Pompano Beach, scheduled for a 2027 handover, sold 60% of its inventory within nine months. ESG-ready design gives new builds an edge as investors prioritise carbon footprints. The dual-track structure enriches choice within the North America luxury residential real estate market.

Geography Analysis

The United States captured 78.60% of the North America luxury residential real estate market in 2025, underscored by concentrated domestic wealth and policy incentives in zero-income-tax states. Florida, Texas, and Nevada led net in-migration, with Miami alone adding nearly 600 USD 10 million-plus trades over 12 months. Capital flight from Latin America solidified demand in Coral Gables and Brickell, while tech relocations energised Austin’s lakefront enclaves. Builders responded with branded towers offering valet boat slips and private seaplane docks, amplifying price resilience even as borrowing costs climbed.

Canada benefits from 3,200 millionaire entries a year under its immigration investor programs. Vancouver’s west side fetches premium valuations, buoyed by Chinese and South Asian communities seeking education and stability. Toronto’s Yorkville corridor posts record condo launches, although proposed vacancy levies add caution. Developers offset regulatory drag by targeting Toronto-born diaspora now working in US tech hubs, yet retaining familial ties. This cross-border capital circulation strengthens the integrated fabric of the North America luxury residential real estate market.

Mexico registers the fastest 4.08% CAGR to 2031, driven by currency arbitrage and proximity to US buyers. Los Cabos, Punta Mita, and Tulum attract retirees and remote executives who split time between US headquarters and coastal sanctuaries. Developers bundle property stewardship, medical concierge, and remote-work infrastructure, easing ownership complexities. Joint-venture financing with US private equity accelerates construction pipelines, underlining Mexico’s strategic role in the broader North America luxury residential real estate market.

Competitive Landscape

The North America Luxury Residential Real Estate Market is fragmented, with no single brokerage or developer controlling more than a single-digit share across the continent. Regional specialists such as Sotheby’s International Realty, Coldwell Banker Global Luxury, and Howard Hughes compete on local knowledge, while technology-enabled entrants seek scale. Compass completed a series of acquisitions, including Washington Fine Properties and @properties, lifting agent count past 50,000 and annual closed volume to USD 127 billion. The playbook blends brand retention with data-driven marketing, setting a precedent for platform consolidation inside the North America luxury residential real estate market.

Private-equity funds pivot toward high-end housing as office yields compress. KKR deployed USD 2.1 billion for an 18-property multifamily set spanning California, Florida, and Texas, signaling a belief in luxury-adjacent rental stability. VICI Properties and Eldridge invested USD 300 million in One Beverly Hills, uniting the Aman flag with retail and gardens that meet WELL benchmarks. These moves indicate rising institutional appetite and intensify rivalry for prime land parcels.

Disruptors introduce blockchain escrow, AI-driven valuation and fractional-share trading platforms. Early pilots, while small, highlight potential fee compression for legacy agents. Established firms counter by pairing white-glove service with tech enhancements such as virtual-reality tours and predictive pricing dashboards. This innovation cycle preserves market fluidity and ensures healthy competitiveness across the North America luxury residential real estate market.

North America Luxury Residential Real Estate Industry Leaders

Toll Brothers City Living

Lennar Corp (CalAtlantic Luxury)

Howard Hughes Corp

Related Companies

Extell Development

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: VICI Properties, Cain International and Eldridge injected USD 300 million into One Beverly Hills, anchoring the first West Coast Aman hotel and luxury residences slated for late 2027 completion. The capital also funds a Beverly Hilton refresh and 8 acres of botanical gardens, reinforcing Los Angeles’ ultra-prime pipeline.

- April 2025: Compass entered advanced talks to acquire HomeServices of America, a brokerage with 50,000-plus agents and USD 127 billion 2023 volume. The deal would vault Compass to the top of the U.S. rankings while folding Berkshire Hathaway HomeServices into its tech-driven platform.

- February 2025: Compass bought Washington Fine Properties, adding USD 43 billion in historic DC-area sales and the region’s highest average transaction size. WFP retains its brand while gaining Compass marketing, AI pricing and referral tools.

- January 2025: Quad-C divested @properties and Christie’s International Real Estate to Compass after the duo posted a 250% revenue surge and 20 new offices. The move widens Compass’ global reach to nearly 50 countries under the Christie’s flag.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the North American luxury residential real estate market as all newly built or existing detached or attached dwellings whose listing or transaction prices sit within the top-tier brackets of each metro and typically start around USD 1 million, yet often range far higher when prime location, large floorplate, branded interior finish, or historic provenance justify premiums. We therefore capture sales and rentals of apartments, condominiums, villas, and landed houses that cater to high-net-worth and ultra-high-net-worth buyers.

Scope exclusion: mixed-use towers in which residential units form a minor share of total built-up area are not included.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Business Model

- Sales

- Rentals

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing-Home Resale)

- By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed luxury brokers across coastal U.S. metros, Canadian institutional landlords, bespoke builders in Texas and Florida, and mortgage underwriters specializing in jumbo loans. These conversations tested preliminary demand drivers, typical absorption rates, and average selling price (ASP) trajectories, letting us refine assumptions that raw desk data cannot reveal by itself.

Desk Research

We began with land-registry transfers, U.S. Census Bureau Building Permits, Statistics Canada housing starts, Mexico's RUV issuance tallies, and wealth distribution tables from the IRS and CRA because these datasets outline the potential unit pool and capital base. Macroeconomic indicators from BEA and Banco de México, secondary-market indices such as the Case-Shiller High-Tier 20-City composite, and Institute for Luxury Home Marketing monthly thresholds helped benchmark price bands. To enrich competitive context, our analysts extracted developer disclosures and Form 10-K filings, while paid platforms like D&B Hoovers and Dow Jones Factiva supplied company-level revenue clues. The sources mentioned are illustrative; many other public and paid references supported validation and clarifications.

Market-Sizing & Forecasting

We applied a top-down rebuild of aggregate transaction value by overlaying median luxury thresholds onto county-level deed counts, which are then adjusted for cash-only share and secondary-home prevalence. Bottom-up cross-checks sampled ASP and unit deliveries from ten marquee developers flag outliers and close gaps. Key variables inside our multivariate regression forecast include: 1) annual change in North American millionaire households, 2) luxury building permits, 3) prime mortgage spread versus conforming rates, 4) LEED/WELL-certified luxury starts, and 5) foreign capital inflows tracked through FINTRAC disclosures. Scenario analysis around monetary-policy paths provides upside and downside bands.

Data Validation & Update Cycle

Every draft model passes peer review where variance against external indices and prior-year deeds is stressed. Material deviations trigger re-contacts with market participants. Reports update annually; should tax, zoning, or macro shocks emerge, an interim refresh is issued and the analyst rechecks figures before client release.

Why Our North America Luxury Residential Real Estate Baseline Earns Trust

Published estimates diverge because firms pick different threshold prices, transaction inclusions, and refresh cadences.

Key gap drivers center on whether resales are net or gross, if rentals are capitalized into value, and how cash-buyer premiums are handled. Mordor employs metro-specific threshold tracking and refreshes annually, whereas some publishers freeze assumptions for several years or convert units with universal ASP mark-ups.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 583.94 B (2025) | Mordor Intelligence | - |

| USD 276.51 B (2024) | Regional Consultancy A | Excludes high-value resales and applies a uniform 3-bedroom proxy for all units |

| ~USD 500 B (2023) | Trade Journal B | Mixes residential with limited mixed-use stock and uses fixed 2021 FX rates |

The comparison shows figures swing widely when threshold choice or unit coverage shifts. By anchoring values to verifiable deeds, wealth data, and annually refreshed ASP curves, Mordor delivers a balanced baseline that decision-makers can retrace and stress-test with confidence.

Key Questions Answered in the Report

What is the current size of the North America luxury residential real estate market?

The market is valued at USD 606.84 billion in 2026 and is forecast to reach USD 735.48 billion by 2031.

Which property type dominates the market?

Apartments and condominiums command 60.45% share, reflecting urban buyers’ preference for amenity-rich, low-maintenance living.

Why are zero-income-tax states important for luxury housing growth?

States such as Florida and Texas attract high-income migrants, increasing prime-home demand and supporting above-average price appreciation.

How does ESG influence new luxury developments?

Institutional investors prioritise WELL and LEED certifications, pushing developers to integrate energy efficiency and health-focused design to secure funding and pricing premiums.

What role does tokenization play in the sector?

Tokenization fractionalises ownership, lowers entry costs and enhances liquidity, drawing new capital pools into luxury real estate.

Which geography is the fastest-growing?

Mexico posts a 4.08% CAGR through 2031, buoyed by US wealth spillover, currency advantages and luxury resort expansion.

Page last updated on: