Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

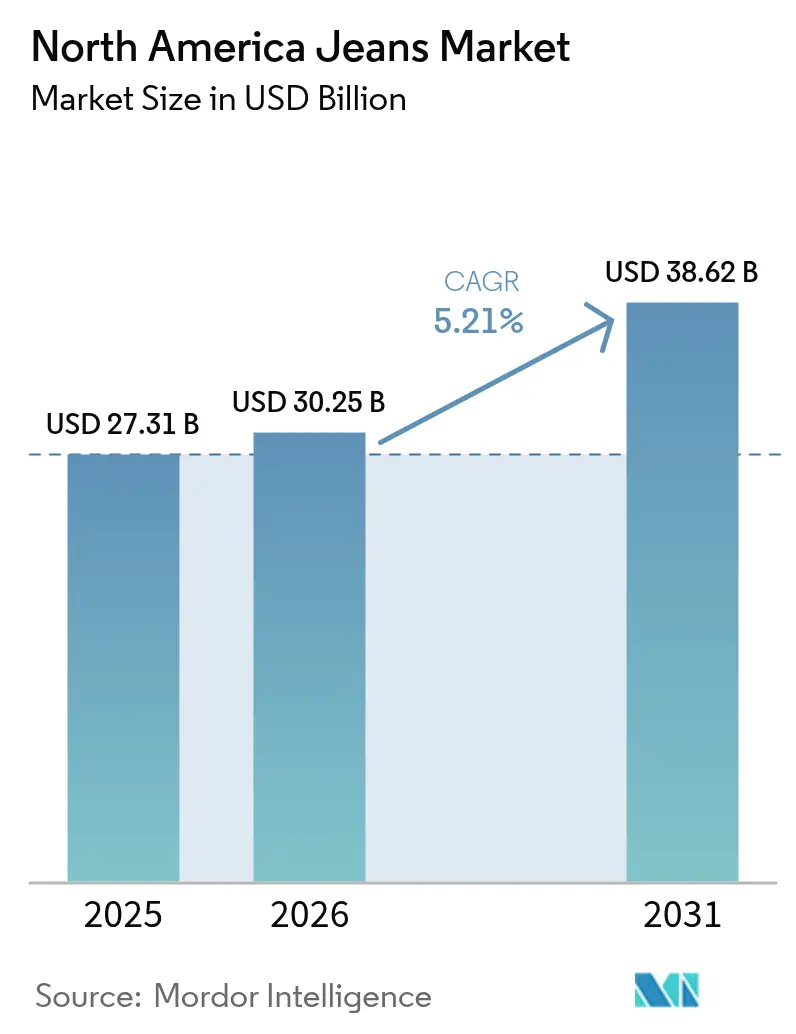

| Base Year Market Size (2025) | USD 27.31 Billion |

| Market Size (2026) | USD 30.25 Billion |

| Market Size (2031) | USD 38.62 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

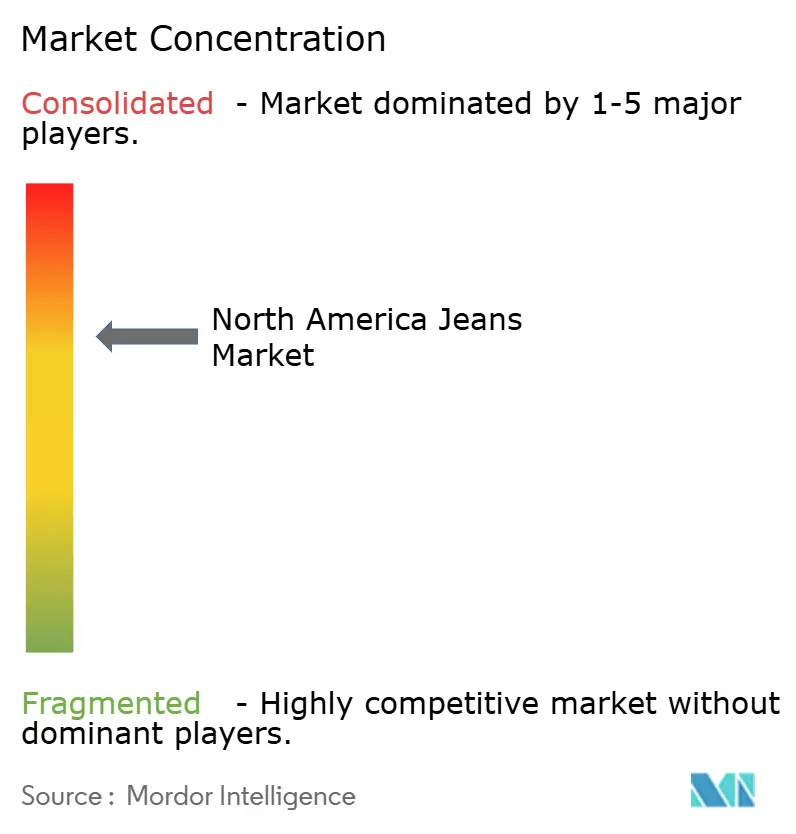

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Jeans Market Analysis by Mordor Intelligence

By 2031, the North American jeans market size is expected to grow significantly, increasing from USD 27.31 billion in 2025 and USD 30.25 billion in 2026 to USD 38.62 billion, reflecting a robust 5.21% CAGR during the forecast period of 2026 to 2031. The evolving dynamics of casual office dress codes, the growing emphasis on sustainability, and the shift from mass production to personalized offerings are fundamentally transforming the competitive landscape. Strategic collaborations with celebrities are driving higher average selling prices, while the adoption of AI-powered fit tools is improving online sales conversion rates. Additionally, nearshoring initiatives are keeping sewing operations in Mexico active, enabling U.S. brands to comply with USMCA regulations effectively. However, challenges such as volatile cotton prices, increasing water-treatment costs, and uncertainties surrounding tariffs are exerting pressure on profit margins. Despite these hurdles, companies investing in recycled fibers and circular resale models are positioning themselves for long-term relevance, provided they have the financial capacity to support this transition.

Key Report Takeaways

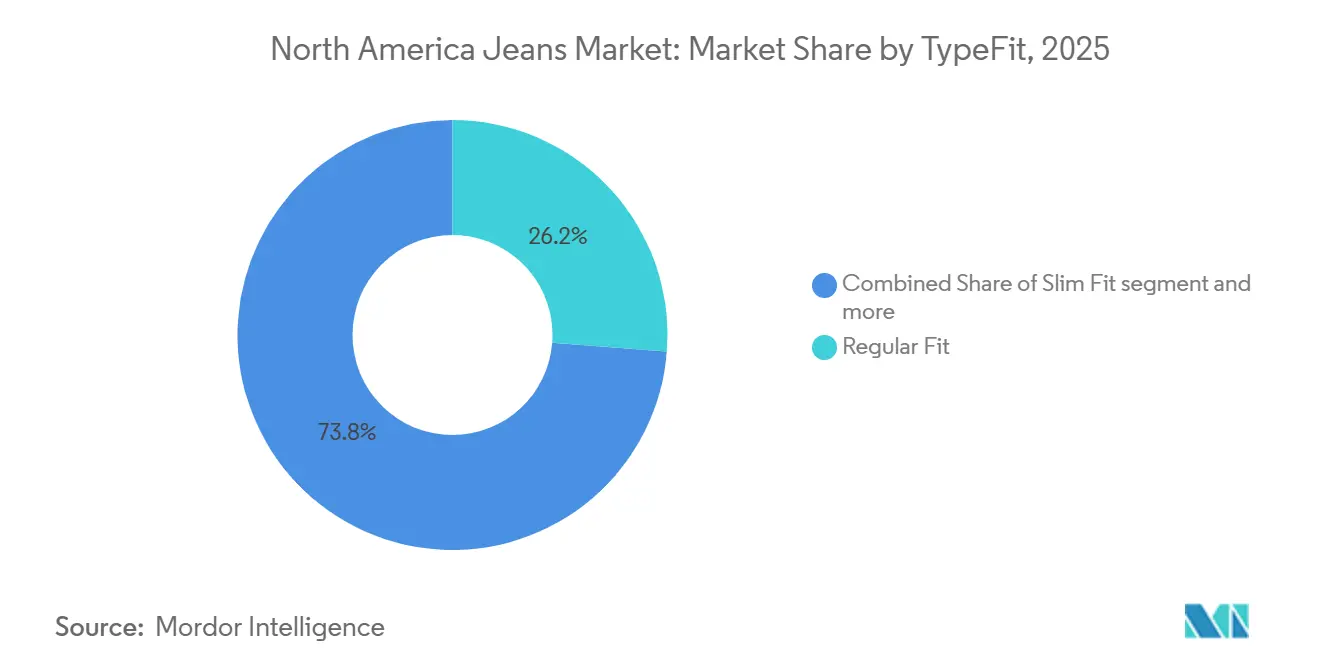

- By type/fit, regular fit led with a 26.48% 2025 share, while slim fit is forecast to expand at a 7.28% CAGR through 2031.

- By end user, women captured 58.28% of the 2025 North America jeans market share, and children’s jeans are expected to grow at a 6.78% CAGR between 2026 and 2031.

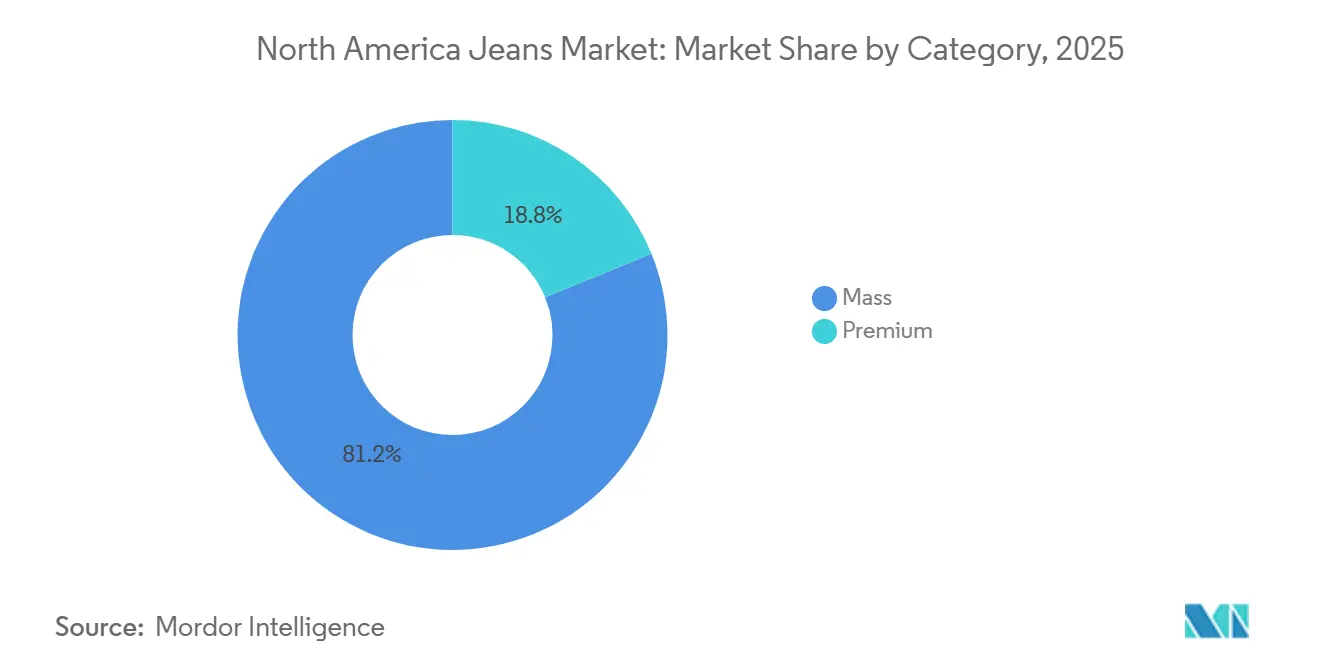

- By category, mass-market options held 81.16% share in 2025, whereas the premium tier is positioned for a 6.13% CAGR to 2031.

- By distribution channel, online retail accounted for 40.11% of 2025 revenue and is projected to rise at a 5.85% CAGR through 2031.

- By Geography, the United States commanded 79.62% of regional demand in 2025, while Mexico is set to register the fastest 5.58% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Jeans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fashion-Forward Fabric Innovations (Stretch, Bio-Based Blends) | +0.8% | United States, Canada, with adoption spill-over to Mexico manufacturing hubs | Medium term (2-4 years) |

| Rise Of Circular Resale And Rental Denim Platforms | +0.5% | United States (urban centers), Canada (Toronto, Vancouver) | Long term (≥ 4 years) |

| Limited-Edition Celebrity/Brand Collaborations | +0.6% | United States (primary), Canada (secondary), Mexico (emerging) | Short term (≤ 2 years) |

| AI-Driven Fit-Personalization And Virtual Try-On | +0.7% | United States, Canada, with technology infrastructure concentrated in major metros | Medium term (2-4 years) |

| Work-Leisure Dress Codes Expanding Denim Occasions | +0.9% | United States, Canada (post-pandemic casualization), Mexico (corporate sectors in Monterrey, Mexico City) | Short term (≤ 2 years) |

| Regulatory Push For Recycled Cotton And Clean Dyes | +0.4% | California, Massachusetts (United States), with compliance influence extending to suppliers in Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fashion-Forward Fabric Innovations Drive Margin Expansion

Brands are increasingly adopting bio-based stretch technologies and sustainable fiber blends to redefine denim's value proposition. This approach enables them to achieve premium pricing while adhering to environmental mandates. For example, Qira, a corn-derived stretch fiber, acts as a sustainable substitute for petroleum-based spandex. Likewise, COREVA provides a plastic-free stretch solution. These advancements are being incorporated into collections by brands aiming to enhance their sustainability credentials without compromising the comfort that has driven stretch denim's popularity over the past decade. Additionally, finishing innovations such as ozone treatment, laser distressing, and enzymatic bleaching are cutting water usage by up to 90% per garment compared to traditional stone-washing methods. Jeanologia reported saving 13 million cubic meters of water across client operations in 2019, a figure that has grown as brands face increasing investor scrutiny over Scope 3 emissions. The takeaway is clear: fabric innovation has evolved from a niche strategy to a competitive necessity. Retailers now prioritize suppliers who can provide verifiable documentation on traceability and environmental impact reductions, ensuring compliance with regulatory standards and meeting the ESG criteria of institutional investors.

Circular Resale And Rental Platforms Extend Product Lifecycles

Denim is shifting from a linear consumption model to a circular economy framework, with resale and rental models unlocking value across multiple ownership cycles. Levi's SecondHand platform, introduced in 2020 and now expanded across North America, enables consumers to exchange used jeans for store credit. The company refurbishes these jeans and resells them at prices 30-50% lower than new ones, appealing to price-sensitive consumers while reducing landfill waste. Urban markets are experiencing growth in rental services, particularly for event wear and capsule wardrobes. This trend is especially prominent among Gen Z consumers, who favor access over ownership and view rentals as a sustainable choice. The viability of this model depends on efficient reverse logistics and quality-control systems that can evaluate, clean, and restock inventory at scale. These capabilities generally give established players with existing distribution networks an edge over pure-play startups. Regulatory support is also emerging: California's SB 707, set to take effect in 2026, requires brands to fund end-of-life collection and recycling programs, according to the California Legislative Information[1]Source: California Legislative Information, “AB 405 and SB 707,” leginfo.legislature.ca.gov. This regulation not only supports the infrastructure for circular models but also has the potential to decouple revenue growth from virgin material consumption, redefining competitive advantages in a resource-constrained future.

Limited-Edition Celebrity Collaborations Amplify Brand Differentiation

Celebrity and influencer partnerships are functioning as demand-generation engines, converting social media reach into measurable sales velocity and enabling brands to test new aesthetics with lower inventory risk. Beyoncé's multi-chapter collaboration with Levi's, including the January 2025 CÉCRED Chapter Two launch, leveraged her 300 million Instagram followers to drive traffic to both physical and digital channels, with Levi's reporting a 9% year-over-year increase in direct-to-consumer revenue in Q3 2024. Wrangler's partnership with country artist Lainey Wilson taps into a demographic, rural and suburban consumers aged 25-54, that skews older and more brand-loyal than coastal urban markets, allowing Kontoor to sustain Wrangler's 7% revenue growth in Q3 2024 even as competitor brands targeting Gen Z faced margin pressure. Dolly Parton's "Joleans" line with Good American and Lucky Brand's collaboration with influencer Addison Rae illustrate how brands are segmenting partnerships by audience psychographics rather than raw follower counts. The short-term impact is concentrated in the United States, where celebrity culture and social commerce infrastructure are most developed, but the model is diffusing to Canada and Mexico as digital payment systems and influencer ecosystems mature.

AI-Driven Fit Personalization Reduces Return Friction

Virtual try-on and AI-powered fit recommendation tools are addressing denim's highest operational cost in e-commerce: return rates that can exceed 30% for online apparel purchases. The North America virtual try-on technology market reached USD 9.59 billion in 2024 and is projected to grow at 26% CAGR through 2029, with apparel, and specifically bottoms, which include jeans, representing a primary use case due to fit variability across brands and body types. Technologies such as 3D body scanning, machine learning algorithms trained on return data, and augmented reality overlays are being integrated into mobile apps, with smartphones and tablets accounting for the majority of virtual try-on sessions due to their ubiquity and camera capabilities. The medium-term impact will be most pronounced in the United States and Canada, where e-commerce penetration is highest, and consumers have demonstrated willingness to adopt digital shopping tools, but tariff-driven supply constraints on 3D scanning hardware could slow deployment if trade tensions escalate.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cotton-Price Volatility From Climate Shocks | -0.6% | United States (domestic production), Mexico (import dependence), Canada (fully import-dependent) | Short term (≤ 2 years) |

| Water-Usage And ESG Compliance Cost Escalation | -0.5% | United States (California, Texas manufacturing), Mexico (water-scarce regions: Baja California, Coahuila) | Medium term (2-4 years) |

| Substitution By Athleisure Bottoms | -0.7% | United States, Canada (urban markets, younger demographics) | Medium term (2-4 years) |

| Tariff And Trade-Tension Exposure On Imported Denim | -0.4% | United States (imports from Asia), Mexico (input tariffs), Canada (re-export constraints) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cotton-Price Volatility Compresses Manufacturer Margins

Raw material cost instability is eroding profitability for vertically integrated producers and forcing brands to choose between absorbing input inflation or passing costs to price-sensitive consumers. United States Department of Agriculture forecasts for the 2025/26 crop year project U.S. output at 14.5 million bales with farm prices at USD 0.62 per pound, up from USD 0.58 in the prior year, tightening supply for North American mills that have historically relied on domestic fiber[2]Source: United States Department of Agriculture, “Cotton Outlook 2025/26,” usda.gov. Mexico's textile sector, which sources approximately 70% of its cotton from imports, faces additional exposure to currency fluctuations and freight cost volatility, with CANAINTEX reporting a USD 4.28 billion trade deficit for January-November 2024 as input costs outpaced export revenue growth. Brands with long-term supply contracts and futures hedging programs—such as Levi's and VF Corporation—are better insulated than smaller players operating on spot markets, creating a competitive advantage for scale. The short-term impact is most acute in the United States and Mexico, where domestic production and import dependence, respectively, create direct exposure to price swings, while Canada's fully import-dependent model offers some buffering through diversified sourcing.

Water-Usage Compliance Raises Capital Intensity

Regulatory mandates and investor pressure are forcing manufacturers to invest in water recycling and treatment infrastructure, increasing the fixed-cost base and disadvantaging smaller operators. Levi's 2030 Water Action Strategy targets a 50% reduction in water use across its supply chain versus 2018 baselines, having already achieved 27% through closed-loop systems that recycle up to 100% of process water, yet textile engineers estimate such systems can triple or quadruple treatment costs relative to conventional finishing. Hogan Lovells notes that compliance with California's Corporate Sustainability Due Diligence Directive (CSDDD) and related frameworks can entail fines up to 5% of annual turnover for non-compliance, incentivizing preemptive investment but straining working capital for mid-tier brands. The medium-term impact is concentrated in water-scarce manufacturing regions, California's Central Valley, Texas, and northern Mexico, where capital availability and regulatory enforcement will determine which facilities remain viable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type/Fit: Slim Fit Gains Share As Casualization Favors Tailored Aesthetics

Between 2026 and 2031, slim fit denim is set to grow at a robust 7.28% CAGR, outpacing the broader market. This trend underscores a shift in consumer preferences towards silhouettes that seamlessly blend comfort with a tailored look, especially in hybrid work settings. In 2025, regular fit denim commanded a 26.48% market share, thanks to its widespread appeal across diverse age groups and body types. However, its growth is slowing as younger consumers lean towards more intentional styles. Once the reigning champion of the 2010s, skinny fit denim is now witnessing a deceleration in growth as fashion trends pivot away from ultra-slim looks. Yet, it continues to enjoy a dedicated following among women aged 18-34. Bootcut and flared styles are making a comeback, riding the wave of Y2K-inspired fashion, especially among women.

Brands like Good American and Madewell are leading the charge, reintroducing wider-leg silhouettes to stand out in a market dominated by slim and skinny options. The "others" category, which includes relaxed, boyfriend, and wide-leg fits, is gaining traction. These designs cater to consumers prioritizing comfort, especially in light of post-pandemic body changes and the oversized fashion trend. A survey by Kontoor reveals that 39% of respondents anticipate wearing jeans to the office, highlighting the evolving fit preferences driven by the need for versatility between professional and casual settings. The swift rise of slim fit denim underscores its dual appeal: it's tailored enough for business-casual offices yet comfortable for all-day wear.

By End User: Kids/Children Segment Accelerates On Millennial Parent Demand

Driven by millennial and Gen Z parents prioritizing durability, ethical sourcing, and size inclusivity, the kids/children segment is set to expand at a 6.78% CAGR from 2026 to 2031. In 2025, women held a dominant 58.28% share of the end-user market, a testament to their higher per-capita denim ownership and the broader style variety available. Brands now cater to diverse body types and fashion preferences, offering multiple fits, rises, and washes. While men's denim constitutes about 35% of the market and is experiencing slower growth, it enjoys advantages like longer replacement cycles and premium pricing. Brands such as AG Adriano Goldschmied and 7 For All Mankind command prices between USD 200 and 300 per unit. The kids/children segment's robust performance is buoyed by several factors: millennials in suburban and exurban markets are seeing rising birth rates, there's a noticeable uptick in household budget allocations for children's apparel, and brands like Gap and H&M are broadening their kids' denim lines.

These expansions now feature sustainable fabrics and adjustable waistbands, enhancing the garment's lifespan. Statistics Canada highlighted a 10.7% year-over-year surge in children's clothing sales for November 2025, with both boys' and girls' categories enjoying double-digit growth[3]Source: Statistics Canada, “Retail Commodity Survey November 2025,” 150.statcan.gc.ca. This data underscores an accelerating momentum in the segment, rather than a plateau. The strategic takeaway for brands is clear: by investing in kids' denim, they can cultivate loyalty with parents, paving the way for future purchases for themselves and shaping their children's brand preferences as they transition into teen and adult markets.

By Category: Premium Tier Outpaces Mass On Collaboration And Sustainability Premiums

Premium jeans are forecast to grow at 6.13% CAGR during 2026-2031, outpacing the mass segment's 5.21% expansion as consumers trade up for differentiated products that signal sustainability credentials and cultural relevance. Mass-market offerings held 81.16% of category share in 2025, reflecting the dominance of value-oriented retailers such as Walmart, Target, and Old Navy, which compete on price and convenience rather than brand storytelling. The premium segment's acceleration is being driven by limited-edition collaborations, such as Levi's x Beyoncé and Diesel's artist partnerships, that convert social media engagement into pricing power, allowing brands to charge USD 150-300 per unit versus USD 40-80 for mass equivalents. Sustainability is functioning as a premium justification: brands such as Everlane and Madewell are marketing their use of organic cotton, recycled fibers, and transparent supply chains to justify price premiums of 30-50% over conventional denim, with consumers in coastal urban markets demonstrating willingness to pay for products aligned with their environmental values.

H&M's Denim United collection, which incorporates recycled cotton and is positioned at a mid-premium price point, illustrates how mass retailers are attempting to capture premium demand without alienating their core value-seeking base. The mass segment's slower growth does not imply decline, its scale and distribution advantages remain formidable, but the premium tier's momentum suggests that differentiation through storytelling, sustainability, and scarcity is becoming a viable path to margin expansion in a category historically characterized by commoditization.

By Distribution Channel: Online Retail Sustains Lead Despite E-Commerce Headwinds

In 2025, online retail channels captured a 40.11% share of the distribution market. Projections indicate a 5.85% CAGR growth from 2026 to 2031, solidifying their status as the fastest-growing channel, even as e-commerce growth rates temper from their pandemic highs. Specialty stores, encompassing mono-brand boutiques and denim-centric retailers like Buckle and Denim & Supply, may be witnessing a slowdown in growth. However, they remain pivotal for premium brands, leveraging in-store service and fit expertise to validate their elevated price points. Supermarkets and hypermarkets, accounting for roughly 15% of the distribution landscape, are ceding ground. Consumers are increasingly turning to online platforms for routine apparel purchases, drawn by the allure of a wider selection and the convenience of home delivery. Other channels, such as department stores and off-price retailers like TJ Maxx, are finding stability after pandemic-induced declines. Yet, they grapple with structural challenges, evident as foot traffic lingers below 2019 benchmarks. The growth of online retail is buoyed by investments in virtual try-on technology, particularly in North America.

Data from Statistics Canada highlighted a 10.7% year-over-year surge in Canadian clothing retail sales for November 2025. Both online and brick-and-mortar channels played a role, but e-commerce's slice of the total retail pie saw a slight dip, falling from 6.1% in May to 5.9% in June 2025. This trend underscores the rising prominence of omnichannel strategies: consumers are increasingly researching online before making in-store purchases, and vice versa. Consequently, brands that adeptly weave together digital discovery, virtual fitting tools, and versatile fulfillment options are reaping the distribution rewards, overshadowing those that focus on a singular channel.

Geography Analysis

In 2025, the United States accounted for 79.62% of regional revenue. High per capita apparel spending, strong adoption of direct-to-consumer models, and a rich portfolio of heritage brands position the U.S. as the foundation of North America's denim jeans market. Although growth has slowed due to athleisure gaining a share of casual wear, sustainability legislation and AI-powered shopping tools have maintained denim's relevance. Nearshoring has enabled U.S. designers to launch capsule collections with a ten-day lead time, significantly faster than the six-week delay associated with sourcing from Asia, enhancing their competitive agility.

Mexico is projected to be the fastest-growing region, with a 5.58% CAGR through 2031. Nuevo León, Baja California, and Querétaro are attracting investments due to the Decreto Nearshoring decree, which provides an 89% immediate deduction on new fixed assets and a 25% bonus for worker training. While CANAINTEX recorded a USD 4.28 billion textile deficit in 2024, supportive policies and USMCA tariff benefits have positioned Mexico as a key assembly hub for U.S. and Canadian brands rather than a primary demand driver.

Canada contributes significantly to regional revenue. In November 2025, clothing sales increased by 10.7% year-on-year, with women’s categories rising by 13.5%. High e-commerce penetration and a strong consumer focus on ethical sourcing have driven initiatives like Levi’s SecondHand. However, reliance on imports exposes retailers to freight cost fluctuations and the impact of U.S.–China tariffs. While remote work has reduced overall wardrobe spending, relaxed dress codes have stabilized demand, demonstrating the North American jeans market's ability to thrive when brands meet Canadian expectations for transparency.

Competitive Landscape

Market concentration in North America's jeans sector is moderate. Levi Strauss, Kontoor Brands, and PVH command a significant share, yet their dominance is tempered by the rise of direct-to-consumer entrants and resale platforms, resulting in a mid-range concentration score of 5. In Q3 2024, Levi's direct channels saw a 9% uptick, bolstered by the CÉCRED collaboration. Wrangler's revenue climbed 7%, thanks to strategic tie-ins with Lainey Wilson. Conversely, Calvin Klein denim from PVH experienced a 10% dip, underscoring that a storied heritage doesn't always equate to growth.

Technology is the key differentiator. Walmart's body-scan tool bridges the fit gap traditionally held by specialists. Meanwhile, SMX's molecular markers ensure recycled content meets California's 2028 wastewater compliance standards. Brands that can authenticate their material's origin stand to gain USMCA benefits, sidestepping Mexico's tariffs on Asian fabrics. Fast Retailing and Uniqlo are making inroads in U.S. metropolitan areas, pushing high-quality basics that pose a challenge to mid-tier brands. Urban millennials are gravitating towards Everlane and Bonobos, drawn by their commitment to transparency.

Circular business models are further splintering market shares. Levi's SecondHand initiative, alongside emerging rental start-ups, is appealing to both price-sensitive and environmentally-conscious consumers. Mastering refurbishment logistics and app-centric merchandising is becoming essential. The industry's evolution in North America is marked by a pivot from traditional scale economics to a focus on agility, regulatory compliance, and data-centric personalization, heralding a new era of competitive advantage.

North America Jeans Industry Leaders

Kontoor Brands, Inc.

The Gap Inc

PVH Corp.

American Eagle Outfitters Inc.

Levi Strauss & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Wrangler introduced its first women's riding jeans reinforced with Dyneema, the world's strongest fiber, 15 times stronger than steel and lightweight enough to float on water, available in Skylar High Rise Relaxed and Rodeo High Rise Boot styles.

- August 2025: Levi Strauss & Co. debuted "The Denim Cowboy," the final chapter of its Levi’s REIIMAGINE campaign in partnership with Beyoncé, featuring pieces like the Western Crystal ‘90s Shrunken Trucker and 501 Curve jeans from the BEYONCÉ x LEVI’S collection.

- March 2025: Good American, debuted at Macy’s in 36 stores for Spring 2025, expanding to 79 stores by Fall 2025, to bring its inclusive, premium denim and ready-to-wear to millions more customers nationwide.

- March 2025: Levi's unveiled its Linen + Denim collection for Spring/Summer 2025, merging lightweight linen with stretch denim for enhanced breathability. The lineup spans men and women's jeans, shorts, jumpsuits, and tops, all adorned in fresh seasonal washes.

North America Jeans Market Report Scope

Jeans are trousers or pants that are made from denim or dungaree cloth.

The scope of the report includes segmentation by the end user, category, distribution channel, and geography. By end user, the market is segmented into men, women, and children. By category, the market is segmented into mass and premium. The market is segmented based on the distribution channel into specialty stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. By geography, the study provides key insights into the United States, Canada, Mexico, and the Rest of North America. The report offers the market size in value terms in USD for all the abovementioned segments.

By Type/Fit

| Regular Fit |

| Slim Fit |

| Skinny Fit |

| Boocut |

| Flared |

| Others |

By End User

| Men |

| Women |

| Children/Kids |

By Category

| Mass |

| Premium |

Distribution Channel

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type/Fit | Regular Fit |

| Slim Fit | |

| Skinny Fit | |

| Boocut | |

| Flared | |

| Others | |

| By End User | Men |

| Women | |

| Children/Kids | |

| By Category | Mass |

| Premium | |

| Distribution Channel | Specialty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the projected value of the North America jeans market by 2031?

The North America jeans market size is forecast to reach USD 38.62 billion by 2031.

Which fit style is growing the fastest in the region?

Slim fit jeans are projected to rise at a 7.28% CAGR between 2026-2031.

Why is Mexico’s growth outpacing the United States?

Nearshoring investments and USMCA tariff advantages support a 5.58% CAGR for Mexico through 2031.

Which segment is expected to add the most new customers?

The kids/children segment expands at 6.78% CAGR as millennial parents buy durable, ethically sourced denim.

Page last updated on: