Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

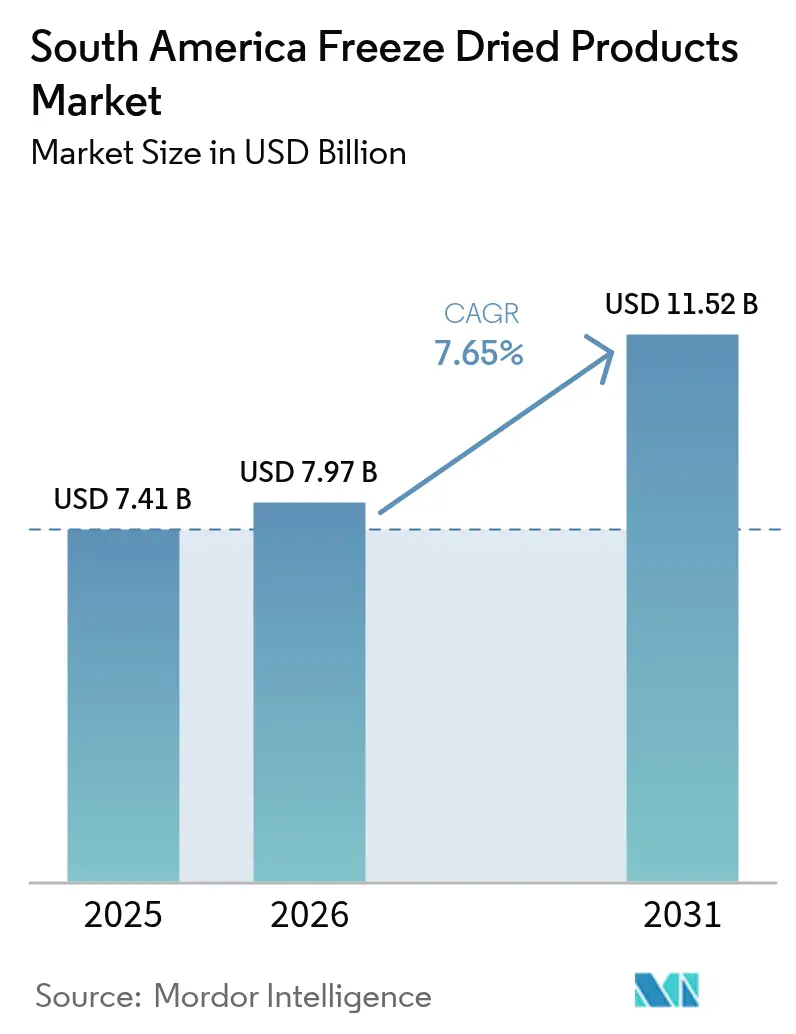

| Base Year Market Size (2025) | USD 7.41 Billion |

| Market Size (2026) | USD 7.97 Billion |

| Market Size (2031) | USD 11.52 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Freeze Dried Products Market Analysis by Mordor Intelligence

The South America Freeze Dried Products Market size is expected to increase from USD 7.41 billion in 2025 to USD 7.97 billion in 2026 and reach USD 11.52 billion by 2031, growing at a CAGR of 7.65% over 2026-2031. Brazil's strong retail expansion, the growth of e-commerce grocery platforms, and institutional programs emphasizing shelf-stable, nutrient-dense products are driving demand. Government-supported crop-valorization initiatives also ensure a reliable supply of fruits, vegetables, and dairy for processors. However, challenges such as energy-intensive production, "ultra-processed" product perceptions, and competition from more affordable frozen or canned alternatives continue to impact margins and adoption rates. Nevertheless, increased investments in microwave-assisted freeze-drying technology, clean-label certifications, and smart packaging are expected to drive the market's next phase of growth.

Key Report Takeaways

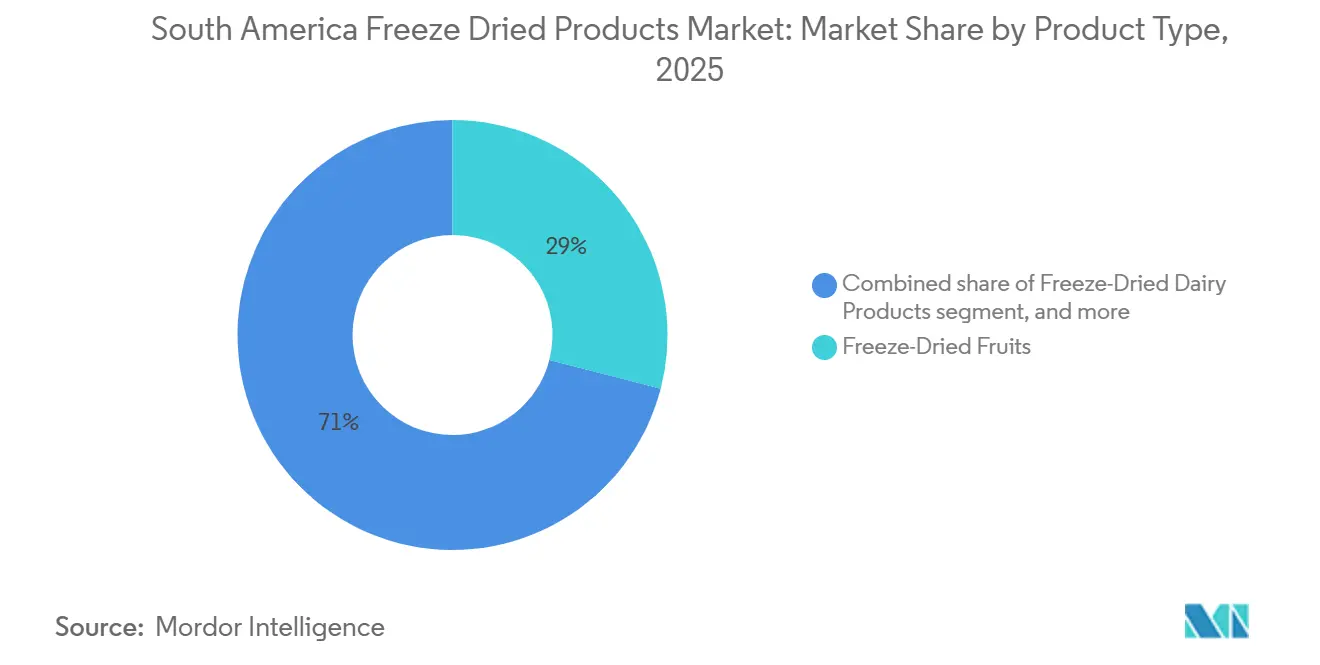

- By product type, freeze-dried fruits led with 29.03% of South America freeze dried products market share in 2025, while freeze-dried dairy is advancing at an 8.67% CAGR through 2031.

- By nature, conventional variants captured 72.57% of South America freeze dried products market size in 2025, while organic lines are projected to expand at a 9.13% CAGR between 2026-2031.

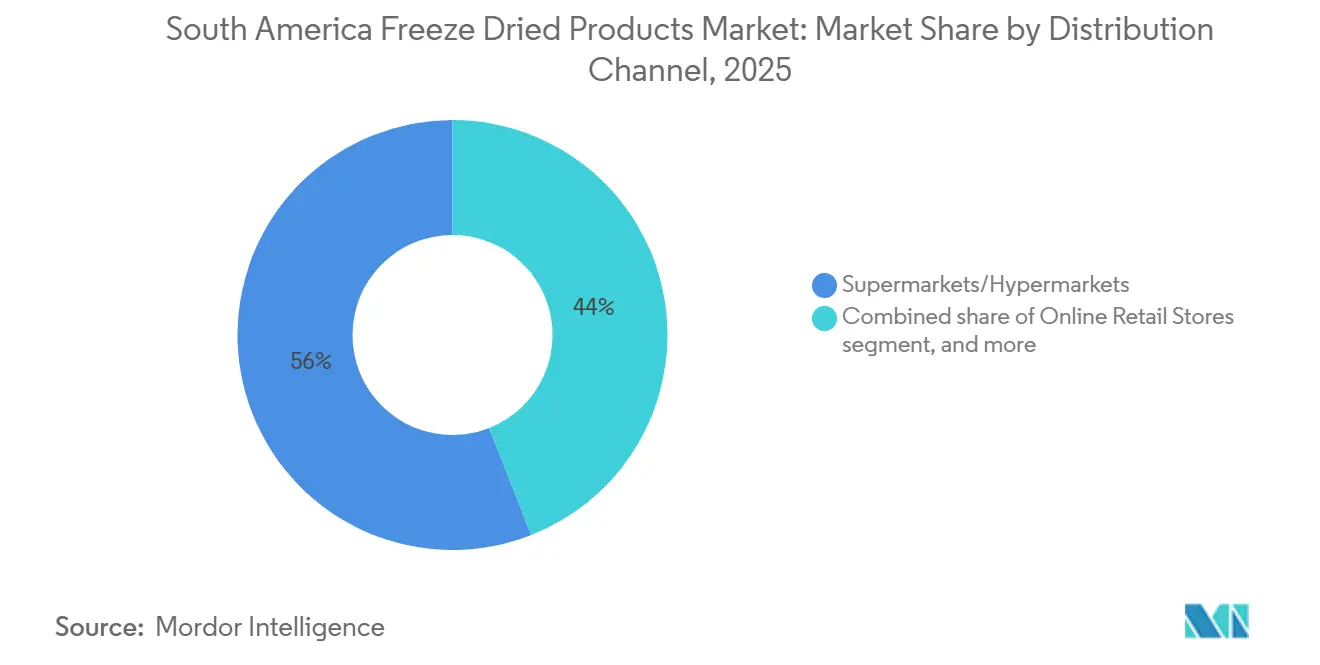

- By distribution channel, supermarkets and hypermarkets controlled 55.97% revenue share in 2025, whereas online retail is poised for 9.27% CAGR growth to 2031.

- By geography, Brazil held 56.69% of the regional total in 2025, while Argentina is forecast to post a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Freeze Dried Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for convenient and nutritious ready-to-eat foods | +1.8% | Brazil, Argentina, Chile urban centers with dual-income households | Medium term (2-4 years) |

| Growing use of freeze-dried inputs in infant and clinical nutrition | +1.5% | Brazil (PNAE school feeding 40M students), Argentina export corridors | Long term (≥4 years) |

| Growing popularity of outdoor activities, camping, and emergency food rations | +1.2% | Chile (Patagonia tourism), Argentina (trekking hubs), Brazil (eco-tourism) | Short term (≤2 years) |

| Preference for clean-label, natural ingredients over additives | +1.4% | Global, with premium segments in São Paulo, Buenos Aires, Santiago | Medium term (2-4 years) |

| Plant-based meal-kit brands incorporating freeze-dried produce | +1.0% | Brazil, Colombia urban millennial cohorts | Medium term (2-4 years) |

| Government-backed programs to valorize climate-impacted crops | +0.9% | Chile (SAG), Bolivia (World Bank project), Peru (superfood initiatives) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising consumer demand for convenient and nutritious ready-to-eat foods

Dual-income households in São Paulo and Buenos Aires are increasingly opting for meal solutions that avoid cold-chain reliance while maintaining nutrient density. Freeze-dried fruits and prepared meals effectively cater to this preference. According to the World Bank, 54% of Brazilian women aged 15 and older participated in the labor force in 2024[1]Source, World Bank, "Labor force participation rate", worldbank.org. Convenience formats are on the rise, with private-label penetration reaching 32% in Colombia and discounter channels gradually taking market share from traditional supermarkets. This evolution in retail channels benefits freeze-dried products, which offer extended shelf life without refrigeration, reducing inventory risks for retailers. In Brazil, trading companies are diversifying their offerings with freeze-dried vegetable mixes and fruit snacks, distinguishing themselves from the growing influx of commodity frozen imports, including a 25% year-on-year increase in the potato category. The combination of urbanization, higher disposable incomes, and retailer demand for low-spoilage inventory is driving this trend. Household savings in Brazil, as a percentage of GDP, increased from 15.5% in 2024 to 16.3% in 2025, according to the Brazilian Institute of Geography and Statistics[2]Source: Brazilian Institute of Geography and Statistics, "Contas Nacionais Trimestrais", ibge.gov.br.

Growing use of freeze-dried inputs in infant and clinical nutrition

Freeze-dried dairy and fruit ingredients align with WHO nutrient-profile models, which set energy-density thresholds, sodium limits, and prohibit added sugars and sweeteners for foods aimed at children aged 6 to 36 months. Brazil's National School Feeding Programme (PNAE), catering to 40 million students, mandates that 30 percent of its procurement comes from family farms. This creates a robust demand for shelf-stable, nutrient-dense inputs, essential for distribution to remote municipalities. Nestlé Health Science, alongside regional formulators, is infusing freeze-dried protein matrices into infant cereals and therapeutic foods. They are capitalizing on water-activity levels below 0.6 to align with Codex Alimentarius standards for Ready-to-Use Therapeutic Foods (RUTF). Thanks to Argentina's SENASA organic certification, freeze-dried dairy powders are now being exported to North American and European clinical-nutrition brands, which prioritize non-GMO and traceable supply chains. Given the stringent regulatory landscape surrounding infant and clinical applications—where safety, traceability, and nutrient retention are paramount—freeze-dried inputs emerge as a strategically vital category.

Growing popularity of outdoor activities, camping, and emergency food rations

Following the pandemic, tourism has recovered in Chile's Patagonia region and Argentina's trekking corridors, driving increased outdoor-recreation spending. This growth has boosted demand for freeze-dried meals, valued for their lightweight and calorie-dense properties. Climate volatility, highlighted by the World Bank's USD 100 million initiative in Bolivia to develop resilient food systems, has raised awareness about emergency preparedness. As a result, the market for long-shelf-life rations has expanded. In Brazil, the eco-tourism industry—focused on the Amazon and Atlantic Forest biomes—has increasingly adopted freeze-dried provisions for multi-day expeditions where refrigeration is not feasible. Companies such as Expedition Foods and regional players like SouthAm Freeze Dry are adapting their product offerings to suit local preferences. By incorporating ingredients like cassava, quinoa, and tropical fruits, they differentiate themselves from North American imports. The segment's short-term impact reflects rapid consumer responses to climate events and the revival of tourism.

Preference for clean-label, natural ingredients over additives

IFOAM Organics International reports that South America encompasses 1.1 million hectares of certified organic farmland. Brazil stands out with more than 20,000 organic producers registered on the SISORG platform, while Argentina's SENASA registry plays a critical role in supporting export-oriented organic supply chains. The freeze-drying process, which removes water without causing heat-induced degradation, is highly compatible with clean-label mandates. These mandates strictly prohibit the inclusion of artificial preservatives, synthetic colors, and artificial flavor enhancers, ensuring product integrity. In premium retail markets such as São Paulo, Buenos Aires, and Santiago, certified-organic freeze-dried fruits achieve price premiums ranging between 20% and 40%. These substantial margins encourage processors to invest in obtaining organic certifications and implementing robust traceability systems. Additionally, the growing health consciousness among South American consumers has led to increased scrutiny of ingredient lists, prompting private-label brands to reformulate their products using more recognizable and natural inputs. The clean-label trend is expected to contribute an additional 1.4 percentage points to the compound annual growth rate (CAGR), with its impact likely to strengthen in the medium term as certification infrastructure continues to develop and mature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs from energy-intensive freeze-drying processes | -1.3% | Brazil, Argentina grid instability and energy tariffs | Short term (≤2 years) |

| Sensitivity to temperature/humidity fluctuations, requiring robust cold-chain logistics | -0.9% | Pan-regional, acute in Amazonian and Andean distribution routes | Medium term (2-4 years) |

| "Ultra-processed food" perception among health-conscious buyers | -0.7% | Urban premium segments in São Paulo, Buenos Aires, Santiago | Medium term (2-4 years) |

| High competition from fresh, frozen, and canned foods | -1.1% | Brazil (frozen potato imports +25% YoY), Argentina, Chile | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High production costs from energy-intensive freeze-drying processes

Microwave-assisted freeze-drying systems are significantly more energy-efficient, consuming 30 to 50 percent less energy compared to conventional systems. This efficiency gap, as quantified by IEEE research, remains largely unaddressed by many processors in South America due to financial limitations. In Brazil, high industrial electricity tariffs exacerbate operational costs, while Argentina's unstable power grid further complicates energy management. These factors collectively compress profit margins, particularly for regional players that lack economies of scale. The freeze-drying process itself is energy-intensive, involving three distinct stages, freezing, primary drying under vacuum, and secondary drying, which require a continuous energy supply over a prolonged period of 12 to 48 hours per batch. This contrasts sharply with the near-instantaneous throughput offered by spray-drying. Processors in Chile and Colombia report that energy expenses account for 25 to 35 percent of their direct manufacturing costs. This substantial cost burden not only restricts their ability to expand production capacity but also necessitates the adoption of premium pricing strategies to maintain profitability.

Sensitivity to temperature/humidity fluctuations, requiring robust cold-chain logistics

When packaging integrity is compromised, freeze-dried products rapidly absorb moisture, emphasizing the critical need for climate-controlled storage and transportation to maintain product quality. In 2024, Brazil's e-commerce retail penetration remains low at 3 percent, reflecting significant deficiencies in last-mile infrastructure. These shortcomings are particularly pronounced in the North and Northeast regions, where inadequate logistics systems increase the risk of spoilage during the final stages of delivery. Similarly, distribution routes in Peru and Bolivia face significant challenges due to extreme temperature variations, which place additional strain on packaging standards. To address these issues, manufacturers rely on foil-laminate pouches equipped with oxygen absorbers, which effectively protect the products but increase unit costs by 10 to 15 percent. Furthermore, the IDB's regional logistics assessments identify cold-chain infrastructure gaps as a persistent structural bottleneck, particularly for products intended for rural and peri-urban markets, where logistical challenges are more pronounced.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Innovations Outpace Traditional Fruit Dominance

In 2025, freeze-dried fruits captured a 29.03% share of South America's freeze-dried products market, equating to an approximate value of USD 2.31 billion. Dominating breakfast cereals and snack mixes are mango, strawberry, pineapple, and apple varieties. This trend is bolstered by Brazil's burgeoning tropical-fruit harvest and Argentina's esteemed berry belts. Additionally, niche fruits like camu camu and açaí are making their way into sports-nutrition products, signaling a shift towards antioxidant-focused marketing. Institutional feeding programs are turning to vegetable cubes of pea, corn, and carrot for their stable bulk needs. Meanwhile, blends of meat and seafood are carving out niches in outdoor recreation and emergency rations, thanks to their protein-rich sachets. Though still in their infancy, prepared meals and pet food are witnessing double-digit growth, attracting the attention of formulators eyeing higher margins.

Among all categories, freeze-dried dairy is set to lead with a projected CAGR of 8.67%. This surge is largely attributed to the WHO's nutrient profile mandates for infant formulas and the Codex's RUTF standards. With their low water-activity, these powders are perfect for remote school-feeding programs, ensuring deliveries remain spoilage-free. Furthermore, organic certification from SENASA paves premium pathways into North America and Europe. In a bid to enhance efficiency, numerous Brazilian dairies are integrating microwave-assisted lines to reduce cycle times. Simultaneously, Argentine cooperatives are turning to solar-hybrid systems as a strategy to counter escalating electricity costs. Given the regulatory compliance advantages and institutional demand, dairy's growth trajectory is poised to significantly bolster South America's freeze-dried products market in the coming years.

By Nature: Organic Certification Accelerates Despite Conventional Dominance

In 2025, conventional variants accounted for a significant 72.57% share of South America's freeze-dried products market. This dominance is driven by extensive contracts with supermarket chains and government feeding programs that prioritize cost efficiency. Established logistics, lower certification costs, and broad retailer familiarity ensure conventional products remain prominent in high-volume aisles. However, regulatory tightening from ANVISA and SENASA is compelling conventional suppliers to improve traceability. This development is prompting gradual quality improvements, reducing the perceived gap with organic labels.

Although organic products represent a smaller segment, they are growing rapidly at a 9.13% CAGR. Supported by SISORG and SENASA registries, along with traceability apps that allow shoppers to scan field-level QR codes, organic products achieve premium mark-ups of 20-40% in metropolitan stores and online boutiques. E-commerce platforms are creating branded microsites for certified fruit snacks and dairy powders, leveraging their extended shelf life to distribute across South America without refrigerated transport. As eco-labels become more mainstream and digital sales channels expand, the growth of the organic segment is expected to further increase the size of South America's freeze-dried products market.

By Distribution Channel: E-Commerce Gains Ground as Supermarkets Retain Scale

In 2025, supermarkets and hypermarkets accounted for 55.97% of South America's freeze-dried products market. Their dominance stems from extensive floor space, effective category management, and growing private-label offerings that enhance profit margins. Discounter chains have launched house-brand freeze-dried fruit pouches, utilizing volume contracts to reduce the price gap with canned fruits. Convenience stores are targeting commuters with single-serve snack tubes, while specialty outdoor retailers provide calorie-dense, foil-packed meals designed for trekkers.

Online retail, although a smaller segment, is expected to grow at a strong 9.27% CAGR. This channel is increasingly focusing on curated assortments of organic and clean-label products. In 2024, Brazil saw 84% of its population engaging with the Internet, bolstering the country's online retail channels, as reported by the International Telecommunication Union (ITU)[3]Source: International Telecommunication Union (ITU), "ICT Indicators Database", itu.int. Brazil's e-grocery sector remains underdeveloped, offering opportunities for subscription services delivering monthly mixed-fruit boxes or pet-food bundles. Digital-native brands are leveraging direct feedback to optimize flavors and introduce limited-edition tropical blends, fostering customer loyalty. Enhanced last-mile delivery networks and the growing adoption of digital wallets are anticipated to drive online sales, redistributing market share within South America's freeze-dried products sector.

Geography Analysis

In 2025, Brazil accounted for 56.69% of the regional revenue, driven by its robust USD 197 billion retail sector, substantial investments in e-commerce, and a government policy mandating that 30% of PNAE (National School Feeding Program) purchases must be sourced from family farms. The country's mango harvests are projected to grow at an annual rate of 2.1% through 2033, ensuring a consistent supply of raw materials for fruit processors. Additionally, EMBRAPA's applied-research laboratories are developing customized drying curves tailored to local mango varieties, enhancing processing efficiency. Although ANVISA's enforcement of compositional transparency has increased compliance costs for producers, it has simultaneously strengthened consumer trust, thereby contributing to the expansion of the freeze-dried products market across South America.

Argentina is experiencing a strong growth trajectory, with a compound annual growth rate (CAGR) of 9.18%. The country is leveraging SENASA certification to position its dairy and berry powders in high-value export markets. In 2023, domestic online grocery sales reached USD 409 million, highlighting a tech-savvy consumer base that is open to trying innovative products such as freeze-dried smoothie boosters and baby-food sachets. Furthermore, INTI's 2024 guidelines on microwave-assisted drying have already prompted three medium-scale processors to submit capital expenditure plans, indicating early signs of momentum that are expected to drive further growth in national production.

Chile, Colombia, Peru, and other South American countries collectively contribute to the remaining share of the regional market. In Chile, an upgrade funded by the Inter-American Development Bank (IDB) and implemented by SAG is modernizing post-harvest processing lines, making them suitable for freeze-drying blueberries and stone fruits targeted at Asian export markets. In Colombia, the 32% penetration of private-label products has encouraged grocery chains to experiment with proprietary freeze-dried vegetable mixes, catering to evolving consumer preferences. Meanwhile, in Peru, producers of quinoa and camu camu are utilizing low-temperature dehydration techniques to preserve heat-sensitive nutrients, ensuring product quality. Additionally, Bolivia and Paraguay are poised to benefit indirectly from World Bank-funded resilience loans, which are being used to develop storage hubs and upgrade power infrastructure. These initiatives aim to gradually integrate smaller growers into larger cross-border supply chains, enhancing their market access and competitiveness.

Regulatory Landscape

Regulatory rules governing freeze-dried foods across South America are shaped by Mercosur and national authorities. Mercosur technical regulations (GMC resolutions) are required to be transposed into member-state law to harmonize safety, labeling, and approvals.

In March 2026, PAHO highlighted broad adoption of front-of-package warning labels across the Americas, including Argentina, Chile, Colombia, Peru, Uruguay, and Brazil. This is increasing scrutiny of sugar, sodium, and saturated fat in snacks, prepared meals, and beverage mixes that use freeze-dried ingredients. Packaging and food-contact requirements are also tightening as Mercosur updates its food-contact regulations. GMC/Res. No 34/2025 requires transposition by June 16, 2026, and revised rules for cellulosic food-contact materials (GMC/Res. No 02/25) accompany product and packaging compliance. Border and export requirements remain tied to SENASA (Argentina) and SENASAG (Bolivia), while a May 2026 Mercosur initiative to accelerate mutual recognition of sanitary and phytosanitary certificates (including development of the SMASF alert platform) supports intra-bloc trade for processed, shelf-stable foods.

Competitive Landscape

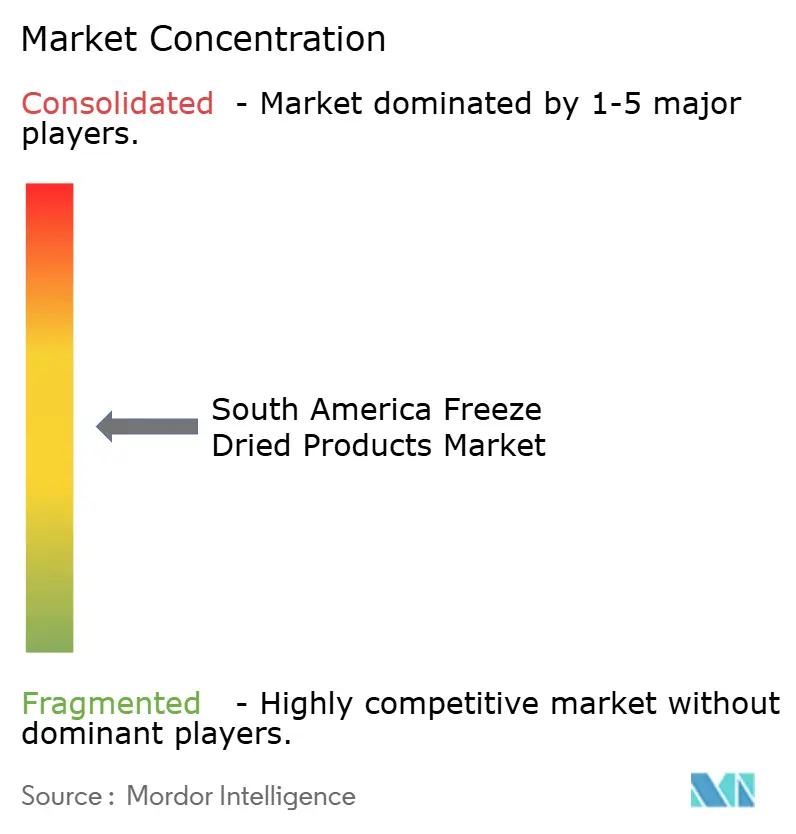

In the South America freeze dried products market, competition is moderately concentrated. Nestlé, Ajinomoto, and Mondelez dominate a significant share of total sales by leveraging their extensive procurement networks and multiproduct plants. Regional players such as SouthAm Freeze Dry, Freeze Point Argentina, and Lam Foods focus on niches by sourcing local fruits and quickly fulfilling private label demands. Technology is transforming the competitive landscape: companies implementing automated tray loaders and real-time moisture analytics have significantly reduced labor costs, improving pricing flexibility. Energy-focused upgrades, like closed-loop chillers, are co-funded by Brazil’s BNDES green credit lines, further widening the gap between leading industry players and smaller competitors.

Channel strategies play a key role in defining market positioning. Multinational corporations drive volumes through major supermarkets, using trade-promotion budgets to secure prime shelf placements. On the other hand, disruptors capitalize on direct-to-consumer subscriptions, collecting valuable first-party data. In the pet food segment, Viscofan-backed Pet Mania targets protein-rich treats, utilizing freeze-drying to enhance both palatability and shelf life. Ingredient distributor Prinova, strengthened by its acquisition of Aplinova, enhances vertical integration by providing faster formulation support to beverage brands. Companies proficient in navigating compliance, particularly with Agência Nacional de Vigilância Sanitária's e-submission portals, gain a competitive advantage by launching new Stock Keeping Units ahead of competitors.

Multilateral institutions are prioritizing sustainability narratives when evaluating tenders for emergency rations. Companies emphasizing lifecycle assessments and demonstrating significant reductions in food waste compared to canned alternatives are gaining procurement advantages. This focus on sustainability aligns with the global trend toward environmentally responsible supply chain practices. Although intellectual-property protections are limited, the South American freeze-dried products market thrives on rapid market entry, reliable supply, and effective cost management. These factors are critical in addressing the urgent demands of emergency ration procurement while ensuring cost efficiency and dependability.

South America Freeze Dried Products Industry Leaders

-

Thrive Life, LLC

-

Asahi Group Holdings, Ltd.

-

OFD Foods, LLC.

-

Ajinomoto Co., Inc.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market Opportunities: In South America, freeze-drying economics remain sensitive to electricity costs and batch times. That dynamic creates room for processors and co-manufacturers that adopt more efficient freezing and dehydration workflows, along with equipment suppliers that can offer automation, remote diagnostics, and real-time drying-phase monitoring to reduce variability and labor intensity.

Brazil-focused applied R&D by SENAI on optimized, more sustainable freeze-drying processes for açaí pulp supports the Amazonian production chain and targets energy and cycle-time bottlenecks. Cold-chain and freezing infrastructure build-outs also support higher-throughput ingredient preparation and export readiness for temperature-sensitive inputs across fruit, dairy, and prepared-meal components. Recent capacity additions include Emergent Cold LatAm's June 2026 blast-freezing tunnels in San Antonio, Chile (over 10,500 tons annual capacity), MBRF's USD 70 million Uruguay expansion in April 2026 (including a 21,000-box capacity tunnel), and KEMOLO's FD-500R delivery to Bolivia in March 2026, which points to a growing installed base for freeze-drying hardware.

Recent Industry Developments

- June 2026: Emergent Cold LatAm commissioned two new blast-freezing tunnels in San Antonio, Chile, adding over 10,500 tons of annual food processing capacity. This expansion strengthens export-oriented cold-chain capability for fruit and prepared-food inputs feeding freeze-dried lines.

- April 2026: MBRF invested USD 70 million to expand its Tacuarembó, Uruguay industrial complex with new freezing infrastructure, including a 21,000-box capacity tunnel. The project broadens regional capacity for high-throughput freeze-drying inputs for fruit, dairy and prepared-meal components.

- April 2025: Nestle launched Nescafe ready-to-drink cold coffee in Brazil. The rollout reinforces product innovation around coffee formats that rely on soluble inputs, supporting premiumization and broader retail experimentation in beverage-led freeze-dried applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of freeze-dried products sold across South America, where moisture is removed under vacuum after freezing to preserve structure and shelf life. The sizing reflects sales across key end markets, using consistent regional coverage and comparable currency treatment.

Scope exclusions: We exclude non-freeze drying methods such as air-dried, spray-dried, drum-dried, and standard dehydrated products, even if they are marketed as dried foods.

Segmentation Overview

-

By Product Type

-

Freeze-Dried Fruits

- Strawberry

- Raspberry

- Pineapple

- Apple

- mango

- Other Fruits

-

Freeze-Dried Vegetables

- Pea

- Corn

- Carrot

- Potato

- Mushroom

- Other Vegetables

- Freeze-Dried Meat and Seafood

- Freeze-Dried Dairy Products

- Freeze-Dried Beverages

- Prepared Meals

- Pet Food

-

Freeze-Dried Fruits

-

By Nature

- Conventional

- Organic

-

Distribution Channel

- Suopermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channel

-

By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the regional demand pool and to anchor assumptions that can be checked in public data. We relied on sources such as UN Comtrade and national customs portals for trade flows, FAOSTAT for agricultural production context, and statistics offices in major countries for food manufacturing and price series. We also reviewed standards and guidance from bodies such as Codex Alimentarius (for food category definitions) and relevant ministries of agriculture and health for labeling and compliance signals.

To translate this into a workable market model, we supplemented the above with company annual reports, investor presentations, and reputable press coverage that discuss capacity changes, product launches, and distribution shifts. In a few places, paid subscriptions were used only for company financials and news screening, plus patent databases to confirm process and packaging activity, which helped us avoid double counting adjacent dried formats. The desk sources named here are illustrative, and many other public references were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually sold as freeze-dried in the region, and how product mix and channel mix are moving in practice. We spoke with manufacturers, ingredient suppliers, distributors, and downstream buyers, then used follow-up checks to confirm pricing logic, penetration assumptions, and realistic growth bounds across South America.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 50% |

| Mid tier: 47% | Functional/Unit leaders: 26% | EMEA: 29% |

| Smaller Players: 16% | Managers: 60% | Americas: 21% |

Market-Sizing & Forecasting

Our sizing starts from a top-down build where production, trade, and consumption signals are used to reconstruct the regional pool of freeze-dried supply, which is then allocated across key product groupings and channels. After that, selective bottom-up approximations were applied, such as sampled price-per-kg by product type multiplied by estimated volumes, plus distributor channel checks, and these checks were used to adjust totals when gaps appeared.

Inputs were chosen because they can be explained and rechecked without relying on hard-to-access datasets. The main drivers included (illustratively) freeze-dried fruit and vegetable availability tied to crop output, import and export movements for shelf-stable ingredients, average selling price progression by category, changes in online retail share for specialty foods, and demand signals from prepared meals and pet food usage. Where volume signals were noisy, we used conservative ranges, then tightened them through interview feedback on conversion yields and pack size mix.

Forecasting was done using scenario analysis supported by simple trend and driver linking, so growth paths remain realistic even when macro conditions change. Assumptions around category growth, pricing, and channel mix were stress-tested in an upside and downside case, and the final forecast kept the middle path that primary respondents described as most likely.

Data Validation & Update Cycle

Validation was handled through multiple checks that look for mismatches between the modeled totals and independent indicators, such as trade directionality, category price movement, and country-level food processing activity. Outliers were reviewed country by country, and when a variance could not be explained by seasonality, one-off stocking, or currency timing, the assumptions were reopened and rechecked through follow-up calls.

Before release, the draft model goes through multi-step analyst review so calculations, definitions, and year alignment stay consistent. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity additions, policy changes that affect cross-border flows, or sharp commodity-driven price swings. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's South America Freeze Dried Product Market Sizing Compared With Other Published Estimates

Published market sizes can look different even when the topic label sounds the same, because the underlying scope and pricing logic are not always aligned. The biggest differences usually come from how strictly the freeze-dried process is defined, whether adjacent dried formats are blended in, which countries are included under South America, and how prices are converted and timed across inflationary periods.

Some estimates appear to expand the definition by blending wider dried and dehydrated product revenue to smooth gaps where freeze-dried volume is harder to observe. In Mordor Intelligence, the count is limited to products explicitly covered under freeze-drying process definitions and then validated using channel mix and category-level price checks before totals are signed off.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.41 B (2025) | |

| Trade Publisher A | USD 7.39 B (2025) | Uses a closely similar regional cut, but the disclosed scope emphasizes fruits and vegetables more heavily, which can shift category weighting and pricing when other freeze-dried types are not modeled in the same detail. |

| Industry Desk Study B | USD 7.94 B (2026) | Reported year is different and the step-up can be driven by timing of price updates and currency conversion assumptions, especially when rapid inflation and retail mix changes are carried into the next-year value. |

Taken together, the spread is mainly explained by scope breadth and year alignment, and not by a single data point. By keeping the product definition tight and then cross-checking value with observable trade, pricing, and channel signals, the final number stays traceable to inputs that can be repeated and audited.

Key Questions Answered in the Report

How big is the South America freeze dried products market today?

It reached USD 7.97 billion in 2026 and is forecast to hit USD 11.52 billion by 2031, reflecting a 7.65% CAGR.

Which product category is growing fastest?

Freeze-dried dairy leads with an 8.67% CAGR, fueled by infant-nutrition and clinical-food reformulations.

Why does Brazil dominate regional sales?

A USD 197 billion retail base, mandated school-feeding purchases, and abundant tropical-fruit supply give Brazil 56.69% share.

Are organic freeze-dried foods gaining traction?

Yes, organic variants are expanding at a 9.13% CAGR as QR-code traceability and premium pricing resonate with urban shoppers.

Page last updated on: