Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

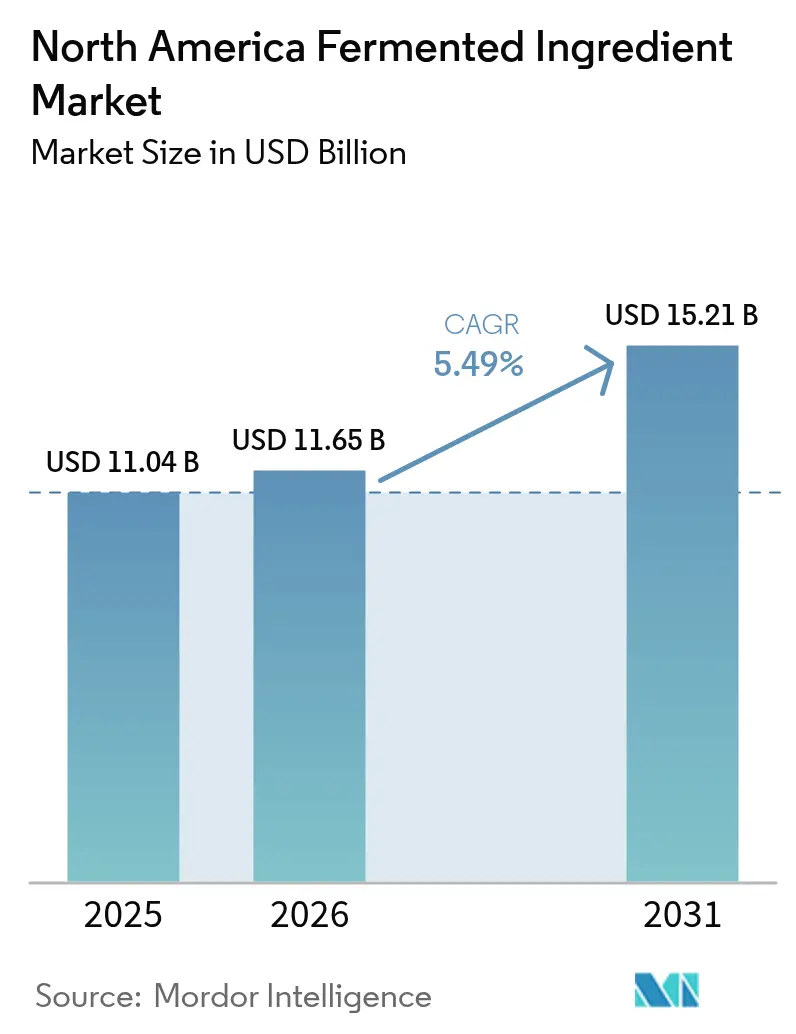

| Base Year Market Size (2025) | USD 11.04 Billion |

| Market Size (2026) | USD 11.65 Billion |

| Market Size (2031) | USD 15.21 Billion |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Fermented Ingredient Market Analysis by Mordor Intelligence

The North America fermented ingredient market size is expected to grow from USD 11.04 billion in 2025 to USD 11.65 billion in 2026 and is forecast to reach USD 15.21 billion by 2031 at 5.49% CAGR over 2026-2031. This growth trajectory reflects the region's pivot toward bio-based manufacturing platforms that can deliver functional ingredients without the environmental footprint of petrochemical synthesis. Clean-label mandates from major retailers and the pharmaceutical sector's search for supply-chain resilience are converging to elevate fermentation from a niche process to a strategic imperative. The United States commands 75.82% of regional revenue in 2024, anchored by decades of corn-ethanol infrastructure and a dense network of contract manufacturing organizations serving both food and pharmaceutical clients[1]Source: USDA Foreign Agricultural Service, "Why Do Ag Exports Matter to U.S. Farmers and the U.S. Economy?", fas.usda.gov. Nearshoring of food-processing capacity into Mexico, alongside public funding of USD 125 million for bio-manufacturing research in the United States, positions the region at the forefront of scale-up activity. Headline risks remain tied to capital intensity, feedstock-price volatility, and the 18–36-month approval window for novel ingredients, yet incumbent players rely on established corn-ethanol infrastructure and proven microbial strains to mitigate these frictions.

Key Report Takeaways

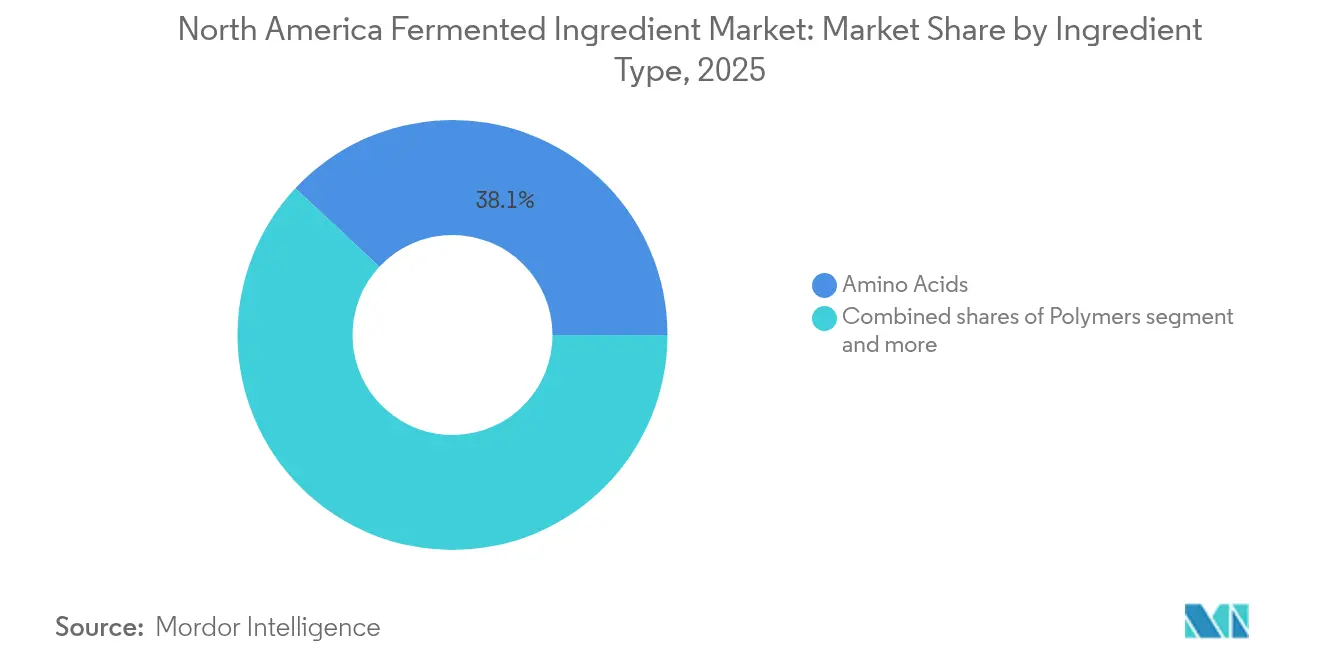

- By ingredient type, amino acids captured 38.05% revenue in 2025, while Polymers are projected to record a 6.61% CAGR to 2031.

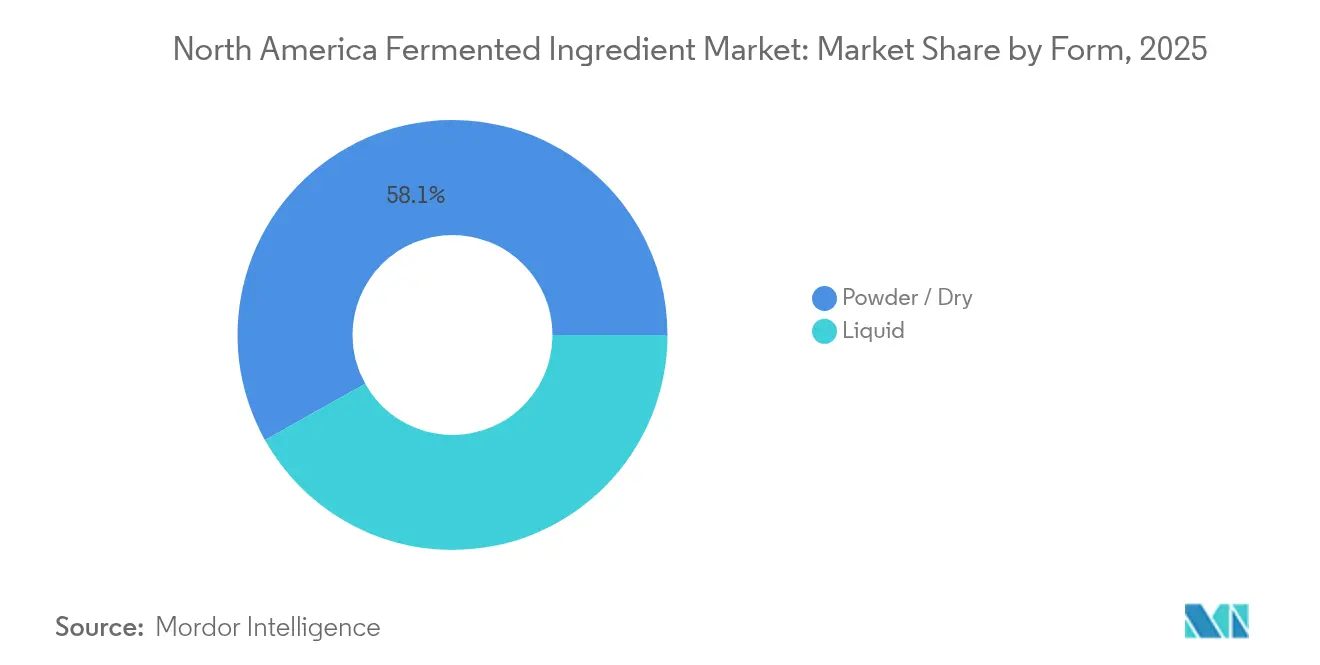

- By form, powder/dry formats held 58.12% revenue in 2025; Liquid formats are forecast to grow at a 5.92% CAGR through 2031.

- By application, food and beverages commanded 36.58% revenue in 2025, whereas Pharmaceuticals are set to expand at a 7.52% CAGR to 2031.

- By geography, the United States retained 75.10% revenue in 2025; Mexico is expected to post the fastest 6.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Fermented Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional foods offering health benefits | +1.8% | United States, Canada, with spillover to Mexico | Medium term (2-4 years) |

| Increased application of fermented acids and enzymes in the food and beverage industry | +1.5% | United States, Mexico | Short term (≤ 2 years) |

| Clean-label trends boosting the adoption of fermentation ingredients | +1.6% | United States, Canada | Medium term (2-4 years) |

| Growing pharmaceutical reliance on bio-based fermentation APIs | +2.1% | United States, with early gains in North Carolina, Kentucky, Illinois | Long term (≥ 4 years) |

| Expanding use of probiotics in personal care formulations | +0.9% | United States, Canada | Long term (≥ 4 years) |

| Enhanced shelf life through fermentation-derived preservatives | +1.2% | North America-wide, strongest in United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Functional Foods Offering Health Benefits

Consumer willingness to pay premiums for fortified and functional foods is reshaping ingredient procurement strategies across North America. Fermentation-derived amino acids, vitamins, and probiotics deliver bioavailability profiles that synthetic analogs struggle to match, making them preferred choices for sports nutrition, infant formula, and senior wellness categories. Ajinomoto's Iowa facility produces feed-grade tryptophan and L-tyrosine via precision fermentation, targeting livestock nutrition and human dietary supplements with identical molecular structures. The U.S. Food and Drug Administration's Generally Recognized as Safe framework under 21 CFR Parts 170, 172, 173, 174, and 184 provides a streamlined pathway for fermentation ingredients, reducing time-to-market compared to novel chemical entities[2]Source: U.S. Food and Drug Administration, "Generally Recognized as Safe (GRAS)", fda.gov. This regulatory clarity, combined with rising awareness of gut-health benefits, is driving double-digit growth in probiotic-fortified yogurts, beverages, and snack bars. The convergence of clean-label mandates and functional-food trends suggests sustained momentum through 2030, particularly as aging demographics in the United States and Canada prioritize preventive nutrition.

Increased Application of Fermented Acids and Enzymes in the Food and Beverage Industry

Organic acids and industrial enzymes are displacing synthetic preservatives and chemical catalysts in food processing, driven by retailer clean-label scorecards and consumer skepticism of E-numbers. Cargill and ADM supply citric acid derived from Aspergillus niger fermentation for beverage acidulation, flavor enhancement, and mineral chelation, with U.S. consumption reaching 96 million kg annually [3]Source: U.S. Environmental Protection Agency, "U.S. Environmental Protection Agency", epa.gov. Solugen's Marshall, Minnesota, facility produces glucaric acid and other organic acids at 120,000 metric tons per year using enzymatic oxidation, targeting applications in detergents, de-icers, and food preservation. Novozymes' Avantec enzyme portfolio, including Extenda, Liquozyme, and Frontia Prime, enables corn ethanol producers to boost yields by 2 to 3 percentage points, translating to millions of gallons of additional output from existing feedstock. The U.S. ethanol sector produced 15.8 billion gallons in 2024, underpinning steady demand for alpha-amylases, glucoamylases, and proteases.

Clean-Label Trends Boosting the Adoption of Fermentation Ingredients

Retailer mandates and consumer activism are forcing food manufacturers to replace synthetic additives with recognizable, pronounceable ingredients. Fermentation-derived components satisfy these criteria while delivering equivalent or superior functionality. The USDA's National Bioengineered Food Disclosure Standard under 7 CFR Part 66 requires labeling of genetically engineered organisms, but fermentation ingredients produced by modified microbes often qualify for exemptions if the final product contains no detectable recombinant DNA. This regulatory nuance has enabled precision-fermentation startups to market dairy proteins, egg whites, and collagen as "animal-free" without triggering bioengineered labels, appealing to flexitarian consumers. Imagindairy received FDA GRAS affirmation in January 2024 for whey protein produced via engineered yeast, positioning the ingredient for use in infant formula and sports nutrition. Lesaffre's acquisition of DSM-Firmenich's yeast extract business in June 2024 for an undisclosed sum reflects consolidation around natural flavor and umami platforms that replace monosodium glutamate and hydrolyzed vegetable proteins. As major retailers tighten acceptable-ingredient lists, fermentation platforms that can deliver clean-label functionality at scale will command pricing power.

Growing Pharmaceutical Reliance on Bio-Based Fermentation APIs

Supply-chain disruptions during 2020-2023 exposed North American pharmaceutical manufacturers' dependence on Asian active pharmaceutical ingredient suppliers, prompting a strategic pivot toward domestic fermentation capacity. AbbVie's North Chicago facility operates 3,000 cubic meters of microbial fermentation capacity for antibiotic and immunosuppressant APIs, representing one of the largest biomanufacturing footprints in the region. Sandoz maintains penicillin fermentation lines at its Lexington, Kentucky site, one of the few remaining U.S. sources for beta-lactam antibiotics amid chronic shortages flagged by the FDA. The agency's 2024 shortage list includes penicillin G and amoxicillin, underscoring the fragility of antibiotic supply chains and the strategic value of domestic fermentation assets. Contract development and manufacturing organizations are retrofitting mammalian-cell suites with microbial fermentation trains to serve biotech clients seeking alternatives to chemical synthesis for complex molecules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs associated with specialized fermentation infrastructure | -1.4% | United States, Canada | Short term (≤ 2 years) |

| Lengthy regulatory approval processes are delaying product launches | -1.1% | United States, with spillover to Canada and Mexico | Medium term (2-4 years) |

| Competition from alternative non-fermented functional ingredients | -0.8% | North America-wide | Medium term (2-4 years) |

| Complexities arising from a fragmented starter culture supply chain | -0.6% | United States, Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Costs Associated with Specialized Fermentation Infrastructure

Capital expenditure for pharmaceutical-grade fermentation facilities routinely exceeds USD 100 million, encompassing stainless-steel bioreactors, clean-in-place systems, and chromatography columns that meet FDA current Good Manufacturing Practice standards. The collapse of the ADM-LG Chem joint venture in July 2024, intended to produce lactic acid and polylactic acid at a U.S. site, illustrates how construction-cost inflation and feedstock-price volatility can render projects uneconomical. Smaller entrants face additional hurdles securing debt financing, as lenders view fermentation assets as illiquid and difficult to repurpose if a product fails regulatory approval. Corbion's commissioning of a vinegar plant in Montgomery, Alabama, in 2024 required multi-year planning and integration with existing acetic acid supply chains, a complexity that deters opportunistic investment. Energy costs for sterilization, aeration, and temperature control can represent 20 to 30% of operating expenses, making fermentation less competitive in regions with high electricity tariffs. These barriers favor incumbents with amortized assets and integrated feedstock supply, limiting the pace at which new capacity enters the market and constraining supply elasticity.

Lengthy Regulatory Approval Processes Delaying Product Launches

FDA's GRAS self-determination pathway permits manufacturers to market fermentation ingredients without pre-market approval, but voluntary GRAS notices, which confer greater legal certainty, require 18 to 36 months of toxicology studies, manufacturing documentation, and agency review. Health Canada's alignment with FDA standards streamlines cross-border approvals, yet divergent labeling requirements and bilingual documentation add compliance costs. Mexico's COFEPRIS has accelerated review timelines for food additives to support the country's expanding food-processing sector, but inconsistent enforcement and limited technical staff create unpredictability. The FDA's 2024 guidance on fermentation-derived biologics introduced new expectations for host-organism characterization and adventitious-agent testing, extending development cycles by 6 to 12 months. These delays erode first-mover advantages and increase the risk that competitors will introduce substitute ingredients before a fermentation product reaches commercialization, dampening investor enthusiasm for novel platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Amino Acids Lead, Polymers Accelerate

Amino Acids commanded 38.05% of ingredient-type revenue in 2025, reflecting entrenched demand from animal feed, sports nutrition, and pharmaceutical compounding. Ajinomoto's Iowa facility produces L-tyrosine and tryptopan via precision fermentation, targeting livestock producers seeking alternatives to synthetic methionine and lysine. DSM-Firmenich supplies feed-grade amino acids across North America, leveraging fermentation processes that deliver higher purity and lower environmental impact than chemical synthesis. Polymers, however, are forecast to grow at 6.61% through 2031 as brands substitute fossil-derived thickeners with xanthan gum, gellan gum, and experimental polyhydroxyalkanoates. Organic Acids capture share in beverage acidulation and preservation, with Cargill and ADM supplying citric acid derived from Aspergillus niger fermentation. Vitamins remain a steady contributor, anchored by BASF's riboflavin production via Ashbya gossypii and DSM-Firmenich's B12 fermentation, both targeting fortification of breakfast cereals, infant formula, and dietary supplements.

Industrial Enzymes serve corn ethanol, brewing, and baking applications, with Novozymes' Avantec portfolio enabling yield gains of 2 to 3 percentage points in ethanol production. Probiotics and Starter Cultures address dairy fermentation, functional foods, and animal feed, with Novonesis (formed from the January 2024 merger of Novozymes and Chr. Hansen) holding a dominant market share in lactic acid bacteria strains. Antibiotics represent a smaller segment, constrained by the offshoring of penicillin and cephalosporin production to Asia, though Sandoz's Lexington, Kentucky, facility remains a strategic domestic source. The "Others" category encompasses yeast and microbial cultures for brewing and baking, with Lesaffre's Milwaukee and Cedar Rapids facilities supplying baker's yeast and brewer's yeast across the region.

By Form: Liquid Gains on Beverage Formulation Needs

Powder and Dry formats held 58.12% of form-based revenue in 2025, driven by shelf-stability, lower shipping costs, and compatibility with dry-blending operations in bakery, confectionery, and supplement manufacturing. Liquid ingredients, however, are forecast to grow at 5.92% through 2031 as beverage formulators prioritize ready-to-dose enzyme and probiotic slurries that eliminate reconstitution steps and reduce batch-to-batch variability. Novonesis supplies liquid alpha-amylases and glucoamylases to corn ethanol producers, where direct injection into mash tanks improves mixing efficiency and reduces enzyme degradation. DuPont's liquid probiotic cultures for yogurt and kefir production offer faster fermentation kinetics than freeze-dried alternatives, shortening production cycles and improving texture consistency. Liquid organic acids, particularly citric and lactic acid, dominate beverage acidulation, with Cargill and ADM supplying concentrated solutions that integrate seamlessly into continuous-flow processing lines.

Powder formats retain advantages in applications requiring long shelf life or ambient storage, such as animal feed enzymes, bakery improvers, and dietary supplement tablets. Spray-drying and freeze-drying technologies enable manufacturers to stabilize heat-sensitive probiotics and enzymes, though these processes add 15 to 25% to production costs compared to liquid formats. The U.S. ethanol sector's preference for liquid enzymes, driven by the need for rapid hydrolysis in high-throughput fermentation, anchors demand for liquid formats, while export-oriented ingredient suppliers favor powder to minimize freight costs and simplify customs clearance. As beverage brands invest in aseptic processing lines that can handle liquid ingredient streams without intermediate drying steps, the cost premium for liquid formats is narrowing, accelerating adoption in high-volume applications.

By Application: Pharmaceuticals Outpace Food and Beverages

Food and Beverages claimed 36.58% of application revenue in 2025, reflecting the sector's scale and diversity of fermentation ingredients, from enzymes in baking and brewing to organic acids in soft drinks and probiotics in dairy. Pharmaceuticals, however, are forecast to grow at 7.52% through 2031 as contract development and manufacturing organizations retrofit fermentation suites to produce bio-identical APIs and reduce reliance on Asian supply chains. AbbVie's North Chicago facility operates 3,000 cubic meters of microbial fermentation capacity for antibiotic and immunosuppressant APIs, representing a strategic asset amid chronic shortages of penicillin G and amoxicillin flagged by the FDA. Sandoz's Lexington, Kentucky, penicillin lines serve hospital formularies and generic drug manufacturers, underscoring the pharmaceutical sector's willingness to pay premiums for supply-chain security.

Animal Feed applications leverage enzymes, amino acids, and probiotics to improve feed conversion ratios and gut health in poultry, swine, and ruminants. Novozymes' Ronozyme portfolio and Alltech's Allzyme SSF deliver phytase and xylanase activities that liberate phosphorus and energy from plant-based feeds, reducing reliance on inorganic phosphates. Cosmetics and Personal Care represent a nascent but fast-growing application, with brands incorporating probiotic lysates and fermentation-derived peptides into skincare formulations targeting microbiome balance. FDA guidance clarifies that live topical probiotics require pre-market approval as drugs, steering formulators toward heat-killed or lysed probiotic ingredients that qualify as cosmetics. Biofuel applications, dominated by corn ethanol, consume industrial enzymes at scale, with the U.S. producing 15.8 billion gallons in 2024 under the EPA's Renewable Fuel Standard mandate , according to the U.S. Environmental Protection Agency. Other Applications span industrial biotechnology, including bio-based chemicals and materials, where fermentation-derived building blocks compete with petrochemical incumbents on sustainability metrics rather than cost.

Geography Analysis

The United States captured 75.10% of regional revenue in 2025, anchored by a mature corn-ethanol sector that produced 15.8 billion gallons and consumed billions of dollars of industrial enzymes and yeast annually. The country's dense network of contract development and manufacturing organizations, concentrated in North Carolina, Illinois, and Kentucky, serves both pharmaceutical and food clients, offering fermentation capacity that ranges from 50-liter pilot scale to 3,000-cubic-meter commercial production. FDA's Generally Recognized as Safe framework under 21 CFR provides regulatory clarity that accelerates ingredient approvals, while the USDA's National Bioengineered Food Disclosure Standard under 7 CFR Part 66 creates labeling predictability for fermentation-derived products.

Mexico is forecast to grow at 6.37% through 2031, the fastest geographic CAGR, driven by nearshoring of food-processing capacity and bilateral trade flows with the United States exceeding USD 79 billion in 2024. COFEPRIS, Mexico's regulatory authority, has accelerated review timelines for food additives to support sectoral growth, though inconsistent enforcement and limited technical staff create compliance uncertainty for multinational suppliers. U.S. ingredient exporters view Mexico as a strategic growth market, leveraging USMCA provisions that eliminate tariffs on fermentation-derived enzymes, organic acids, and vitamins.

Canada represents a smaller but stable market, with Health Canada's alignment with the FDA on GRAS determinations streamlining cross-border ingredient approvals. Biofeed Technology, a Canadian animal feed enzyme supplier, markets Fullzyme products domestically and exports to the United States, illustrating the integrated nature of North American supply chains. The rest of North America, comprising Central American and Caribbean nations, remains a minor contributor, constrained by limited food-processing infrastructure and reliance on ingredient imports from the United States and Mexico.

Regulatory Landscape

In the United States, fermented ingredients used in food are primarily governed through the U.S. Food and Drug Administration (FDA) framework for food additives and Generally Recognized as Safe (GRAS) substances under 21 CFR Part 170, with additional provisions across Title 21 depending on the ingredient class (for example, enzyme preparations and other direct food substances). For fermentation-derived ingredients, FDA submissions and supporting dossiers commonly emphasize microorganism identity and safety, the fermentation and downstream processing description, and controls that demonstrate purity and the absence of harmful residues. This structure creates a relatively defined path for established fermentation ingredient categories, although novel uses and novel production strains still require substantial data packages.

Canada regulates many newer fermentation-derived ingredients through Health Canada oversight for novel foods under the Food and Drug Regulations (notably Division 28), which requires mandatory pre-market notification when an ingredient lacks a history of safe use or is produced via a new process. Health Canada also publishes determinations that certain products are non-novel, and it maintains guidance that is frequently used for probiotic microorganisms in food, along with compliance pathways relevant to supplemented foods (Division 29). Across North America, commercialization planning is closely tied to selecting the appropriate pathway early (GRAS, food additive petition, or novel food submission) and aligning labeling and documentation requirements for cross-border supply.

Value Chain Analysis

The value chain starts with upstream feedstocks (corn-derived dextrose and other carbohydrate streams, plus emerging agricultural and industrial side streams) and specialized inputs such as production strains, nutrients, and processing aids. Core manufacturing includes strain development and scale-up, fermentation operations (batch or continuous), and downstream recovery and purification (for example, filtration and concentration) to meet food- or pharma-grade specifications. A mix of large integrated producers and specialists participate in North America, including fermentation platform suppliers such as Biospringer (Lesaffre) and Jungbunzlauer, and custom fermentation and flavor specialists such as BioSource Flavors and Jeneil Biotech.

Downstream, fermented ingredients flow through blenders, formulators, and distributors into end users across food and beverages, dietary supplements, animal nutrition, and adjacent applications. Compliance and quality management shape manufacturing and distribution practices, including current good manufacturing expectations and, for certain categories, additional FDA requirements for acidified foods (21 CFR Part 114) where applicable to finished products. Bottlenecks commonly surface at the scale-up and validation stages (process stability, contamination control, and reproducibility), which strengthens the role of pilot-to-commercial partners and makes regional capacity additions relevant, including Jungbunzlauer's September 2024 investment in a Canadian xanthan gum facility to reduce import dependence and anchor supply closer to regional feedstock sources.

Competitive Landscape

The North America fermentation ingredients market exhibits moderate concentration, as multinational ingredient houses such as Novonesis, DSM-Firmenich, Cargill, and DuPont coexist with specialized fermentation startups targeting high-margin niches. Novonesis, formed from the January 2024 merger of Novozymes and Chr. Hansen commands a dominant share in industrial enzymes and probiotic starter cultures, leveraging a portfolio of more than 1,000 microbial strains and a North American manufacturing footprint that includes facilities in the United States and Canada.

Cargill and ADM hold leading positions in organic acids and amino acids, benefiting from vertical integration into corn wet-milling and access to low-cost dextrose feedstock. Strategy patterns emphasize acquisitions of complementary fermentation platforms, as evidenced by Lesaffre's October 2024 acquisition of a 70% stake in Biorigin and its June 2024 purchase of DSM-Firmenich's yeast extract business, consolidating the company's position in natural flavors and umami ingredients. Opportunities center on precision-fermented dairy proteins, rare organic acids, and bio-based polymers, where startups such as Imagindairy (whey protein) and Solugen (glucaric acid) are securing FDA GRAS affirmations and scaling production.

Emerging disruptors leverage synthetic biology and machine learning to accelerate strain development, compressing timelines from 3 to 5 years to 12 to 18 months. The collapse of high-profile joint ventures such as the ADM-LG Chem lactic acid project in July 2024 demonstrates that capital intensity and feedstock-price volatility remain formidable barriers, favoring incumbents with amortized assets and integrated supply chains. Technology deployment focuses on continuous fermentation, which reduces batch turnaround times and improves asset utilization, and on downstream purification innovations such as membrane filtration and simulated moving-bed chromatography that lower cost-of-goods by 15 to 25%. As pharmaceutical and food clients prioritize supply-chain resilience, contract manufacturers with dual-use fermentation capacity, capable of producing both food-grade and pharmaceutical-grade ingredients, are capturing share by offering flexibility and shorter lead times.

North America Fermented Ingredient Industry Leaders

-

BASF SE

-

Döhler GmbH

-

DSM-Firmenich

-

DuPont

-

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercialization whitespace is most visible where fermentation platforms deliver ingredients that reduce reliance on conventional animal or petrochemical supply chains, while meeting clean-label and functionality requirements. Precision-fermented proteins and postbiotic ingredients are moving from regulatory clearance into broader commercialization routes, supported by partnerships that link startups with established processors and distributors. For example, ADM and The Every Company announced a July 2026 collaboration to scale OvoPro precision-fermented egg white protein at ADM's Clinton, Iowa facility, showing how incumbent processing infrastructure is being used to expand supply availability for novel fermented proteins.

Capacity buildouts and applied scale-up infrastructure also support opportunities in probiotics, yeast derivatives, and other high-value fermented ingredients where stability, segregation, and consistent quality influence purchasing decisions. Vidya opened a 28,750-square-foot probiotic manufacturing facility in Bunnell, Florida in April 2026 with separated production for spore-forming and non-spore-forming lines, pointing to manufacturing designs that protect strain integrity and streamline compliance. In parallel, mid-scale scale-up resources are expanding, including the University of Illinois plan to grow its Integrated Bioprocessing Research Laboratory (IBRL) footprint from 40,000 to 75,000 square feet, which strengthens the bridge between bench development and contract manufacturing for food innovators and ingredient companies working through GRAS and novel-food engagement pathways.

Recent Industry Developments

- July 2026: ADM and The Every Company announced a partnership to scale production of OvoPro precision-fermented egg white protein at ADM's facility in Clinton, Iowa. The partnership connects a precision-fermentation protein developer with a large-scale processor to translate demand signals into commercial volumes. It also reflects a broader pattern of using existing Midwest fermentation and processing infrastructure to shorten the path from validation to supply agreements.

- July 2025: Meridian Biotech announced a USD 40 million facility in Franklin County, Kentucky, aimed at repurposing bourbon distillery byproducts into alternative proteins. The project highlights feedstock diversification and circular-economy sourcing models within North American fermentation supply chains. It also broadens regional manufacturing options beyond traditional corn-sugar inputs by monetizing consistent industrial side streams.

- September 2024: Jungbunzlauer announced a USD 200 million investment to build a xanthan gum manufacturing facility in Port Colborne, Ontario. The facility supports Canada for greater local production of a key fermentation-derived polymer used across food and beverage formulations. It also improves supply security by reducing reliance on imports and leveraging regional corn-based inputs for fermentation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America fermented ingredient market covers ingredients produced through microbial fermentation and sold for use in food and beverage formulations across the region, measured in revenue terms for the defined geography.

Scope exclusions: Excludes retail sales of finished fermented foods and beverages and counts only ingredient value, not downstream branded product value.

Segmentation Overview

-

By Ingredient Type

- Amino Acids

- Organic Acids

- Vitamins

- Industrial Enzymes

- Probiotics / Starter Cultures

- Polymers

- Antibiotics

- Others

-

By Form

- Liquid

- Dry / Powder

-

By Application

- Food and Beverages

- Pharmaceuticals

- Animal Feed

- Cosmetics and Personal Care

- Biofuel

- Other Applications

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

To set the fact base, we start with public and official sources that help anchor the ingredients demand pool and trade flows. Common references include USDA data and outlooks, Statistics Canada releases, the US International Trade Commission database, UN Comtrade, and US FDA materials that clarify ingredient use and labeling context.

Next, we cross-check manufacturer disclosures such as annual reports, investor decks, and product literature to understand where fermentation-derived inputs are used and how pricing tends to move. Import and export shipment level data is also used selectively to spot directional changes in cross-border movements for relevant ingredient categories. The source list above is illustrative only, and many additional references were used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that are usually fuzzy in public data, such as typical contract pricing behavior, application mix shifts, and how much fermentation output is consumed locally versus traded. We spoke with a spread of ingredient manufacturers, distributors, and downstream formulators across the United States, Canada, and Mexico so that the model reflects practical purchasing patterns and not just published statistics.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | |

| Mid tier: 59% | Functional/Unit leaders: 30% | |

| Smaller Players: 15% | Managers: 55% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where food and beverage manufacturing activity and related ingredient consumption signals are translated into an addressable fermented-ingredient revenue pool for North America, and then adjusted to match observed trade and price realities. To keep the totals honest, we corroborate the outcome with selective bottom-up approximations, such as sampled ASP ranges by ingredient families multiplied by indicative volume bands shared during interviews, followed by distributor channel checks.

Inputs that matter for this market include fermentation-derived ingredient penetration in key processed food categories, pricing movement for widely used fermented inputs (for example, organic acids and enzymes), import and export trends for relevant HS-linked ingredients, plant utilization and expansion announcements, and the split between food versus beverage usage. When data is missing for smaller niches, gaps are handled through proxying from adjacent ingredient families and then normalized through expert feedback so the final totals do not get overstated.

For forecasting, scenario analysis is used around variables that can change quickly, such as clean label reformulation pace, capacity additions, and price pass-through timing. These scenarios are then blended into a base case after the assumptions are reviewed with primary respondents for what seems realistic in the next five years.

Data Validation & Update Cycle

Before numbers are finalized, we run multiple checks so the market size does not rely on a single dataset or one strong assumption. Outputs are compared against independent signals such as trade direction, known capacity movements, and the implied spend per unit of food manufacturing activity, and then outliers are investigated before sign-off.

A second analyst review is completed to confirm definitions, unit consistency, and currency treatment, and we re-contact sources when a key assumption shows unusual variance. The report is refreshed annually, and interim updates are made when major events materially change pricing, capacity, or demand. Right before delivery, a final review pass is done so clients receive the most current view available.

Mordor Intelligence's North America Fermented Ingredient Market Size Compared With Other Published Estimates

Published market sizes for fermented ingredients in North America can vary quite a bit, even when the topic name looks similar. The biggest drivers are usually what is counted as an ingredient versus a finished product, which applications are included, the pricing basis used, and how fresh the base year assumptions are.

The main gap comes from whether adjacent fermentation outputs and downstream product value are folded into the total, where Mordor Intelligence counts only ingredient-level revenue for North America and keeps pricing tied to interview-validated ranges that are refreshed to the stated base year rather than extended from older averages.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.04 B (2025) | |

| Trade Publisher A | USD 11.14 B (2024) | Uses a different base year and a longer-dated growth curve, and the scope language suggests broader inclusion across fermentation-derived categories, which can shift totals when pricing is not rechecked for the updated year. |

| Global Consultancy B | USD 4.85 B (2025) | Likely applies a narrower product set or end-use filter, and it may exclude several high-volume fermented ingredient families, which pulls the 2025 total down even if the regional definition stays similar. |

The spread in the table is mainly explained by scope control and base year pricing treatment, not by a single forecasting formula. When the model is tied to clear ingredient-only revenue, checked against trade and capacity signals, and then aligned with interview feedback on price and mix, the result is easier to trace and repeat across updates.

Key Questions Answered in the Report

What is the forecast value of the North America Fermentation Ingredients Market by 2031?

The market is projected to reach USD 15.21 billion by 2031.

Which ingredient type leads revenue share in North America?

Amino Acids led with 38.05% revenue share in 2025.

Which application segment is expected to grow fastest?

Pharmaceuticals are set to expand at a 7.52% CAGR between 2026 and 2031.

Why are liquid fermentation ingredients gaining traction?

Beverage and ethanol processors prefer ready-to-dose slurries that remove reconstitution steps and improve process efficiency.

Page last updated on: