North America Feed Lutein And Zeaxanthin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

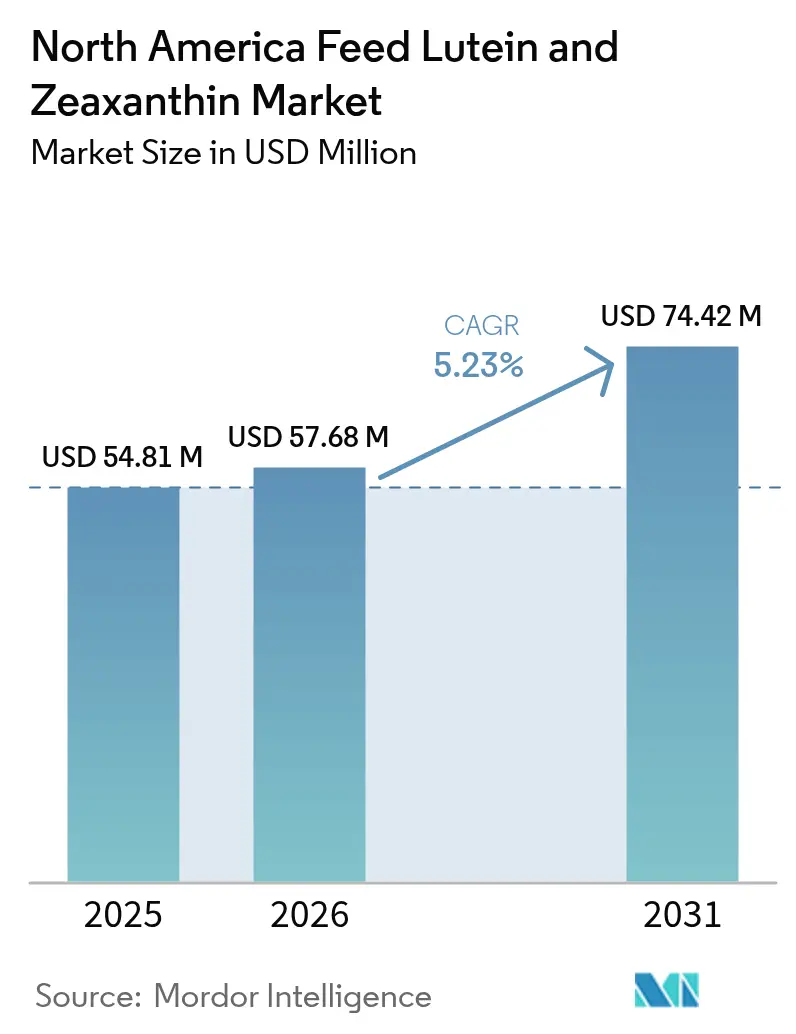

| Base Year Market Size (2025) | USD 54.81 Million |

| Market Size (2026) | USD 57.68 Million |

| Market Size (2031) | USD 74.42 Million |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Feed Lutein And Zeaxanthin Market Analysis by Mordor Intelligence

The North America feed lutein and zeaxanthin market size is expected to grow from USD 54.81 million in 2025 to USD 57.68 million in 2026 and is forecast to reach USD 74.42 million by 2031 at 5.23% CAGR over 2026-2031. The market is evolving due to shifting consumer preferences and demographic changes. With the United States Census Bureau forecasting a population of 417 million by 2060, the demand for animal-based protein products remains strong. The market growth is driven by the increasing demand for naturally pigmented eggs, meat, and farmed fish, supported by organic certification requirements that restrict synthetic additives. The expansion of aquaculture production, particularly in salmon and trout farming, increases the demand for astaxanthin-related xanthophylls. Poultry integrators are enhancing yolk color programs to meet quick-service restaurant requirements. Recent regulatory changes by the Food and Drug Administration and Canadian Food Inspection Agency have increased permitted carotenoid inclusion rates, providing greater formulation flexibility. Marigold cultivation contracts in Mexico and Guatemala ensure consistent lutein supply throughout the year, but raw material price fluctuations continue to pose challenges.

Key Report Takeaways

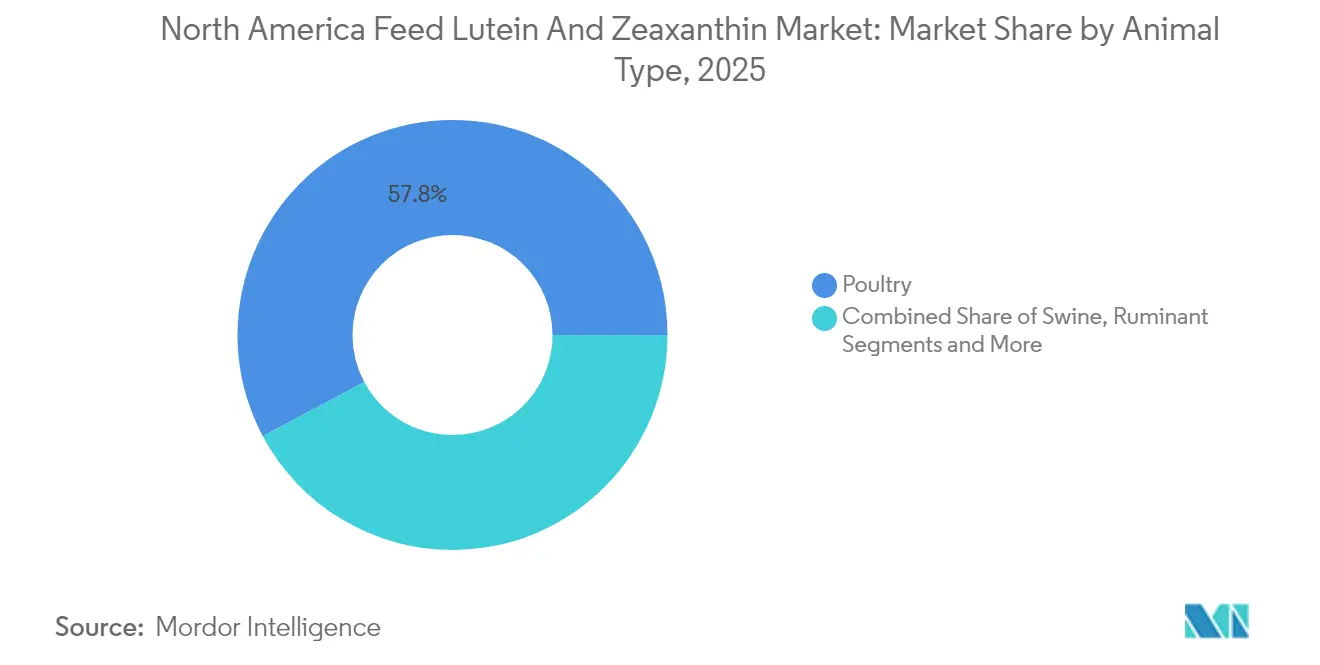

- By animal type, poultry led with 57.80% of the North America feed lutein and zeaxanthin market share in 2025, while aquaculture is forecast to record the fastest 7.69% CAGR through 2031.

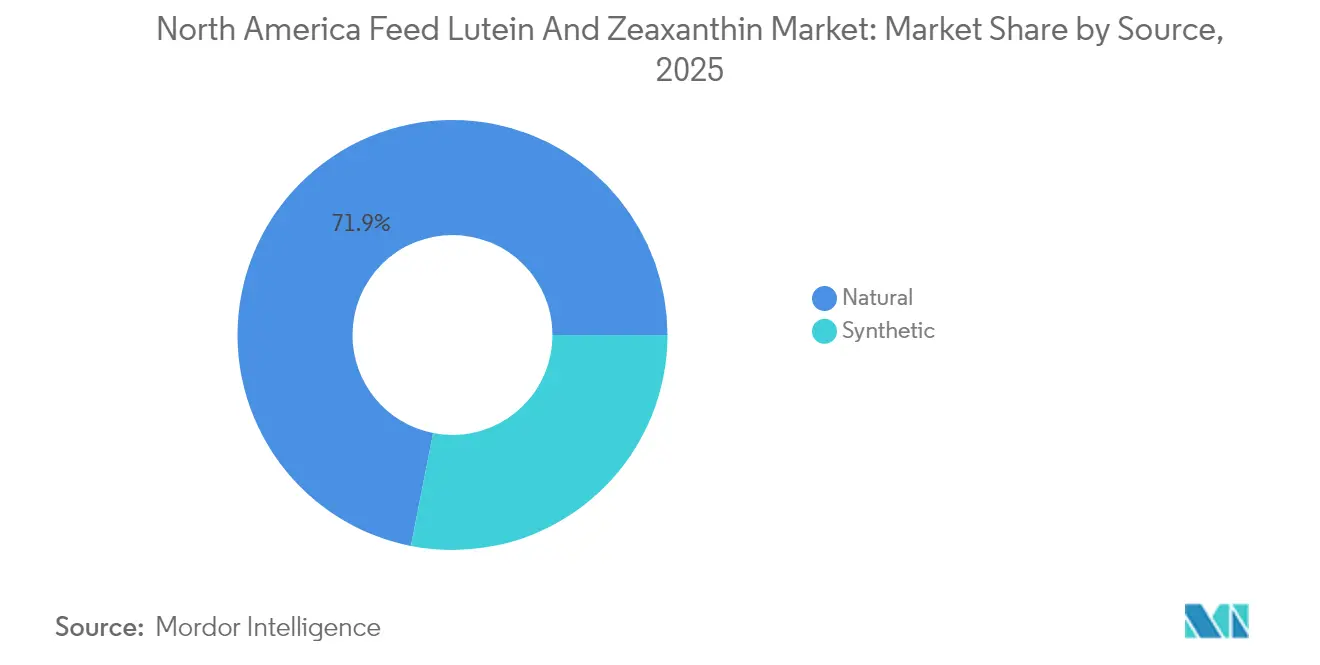

- By source, natural commanded a 71.90% share of the North America feed lutein and zeaxanthin market size in 2025, and is projected to advance at a 7.36% CAGR between 2026-2031.

- By country, the United States held a 61.80% share of the market revenue in 2025, whereas Mexico is set to expand at a 6.13% CAGR to 2031.

- Market concentration is moderate, with the top five companies - DSM-Firmenich AG, BASF SE, Kemin Industries, Inc., EW Nutrition GmbH, and Nutrex NV collectively holding the majority of the market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Feed Lutein And Zeaxanthin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for animal-based protein | +1.2% | United States and Canada | Medium term (2-4 years) |

| Surging demand for natural pigmentation | +0.9% | United States and Canada organic sectors | Long term (≥ 4 years) |

| Expansion of organic-certified egg and meat output | +0.8% | United States and Canada | Long term (≥ 4 years) |

| Technological advances in carotenoids extraction and delivery methods | +0.7% | North America research and development hubs | Medium term (2-4 years) |

| Marigold production contracts lowering supply-chain risk | +0.5% | Mexico and Guatemala supply corridors | Short term (≤ 2 years) |

| Regulatory allowances for higher inclusion caps | +0.4% | United States Food and Drug Administration and Canadian Food Inspection Agency regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Animal-Based Protein

North American protein consumption patterns influence carotenoid demand as livestock producers optimize feed formulations to achieve specific egg yolk color and salmon flesh pigmentation requirements. The United States Department of Agriculture projects growth in per capita consumption of eggs and fish, particularly farmed salmon, where astaxanthin supplementation is necessary for market acceptance. The increasing per-capita egg and fish consumption across the United States and Canada has led feed formulators to adjust lutein, zeaxanthin, and astaxanthin dosing for color consistency[1]Source: “Aquaculture Opportunity Areas,” NOAA.gov. Quick-service restaurant chains require specific yolk color standards, which compel integrators to maintain consistent xanthophyll levels in feed formulations. This requirement has shifted the North America feed lutein and zeaxanthin market toward precision premixes.

Surging Demand for Natural Pigmentation

Consumer preferences for natural ingredients are reshaping carotenoid sourcing strategies as food manufacturers adapt to clean label demands. Natural carotenoids from marigold extract and paprika oleoresin command higher prices but comply with the United States Department of Agriculture (USDA) National Organic Program standards, which restrict synthetic alternatives. The demand for clean-label products increases the use of marigold and paprika-derived pigments despite their premium pricing. United States Department of Agriculture Organic regulations prohibit most synthetic carotenoids, directing poultry and premium aquaculture producers toward natural inputs, despite cost premiums reaching 200% above synthetic options[2]Source: Agricultural Marketing Service, “Organic Livestock Requirements,” USDA.gov. This shift significantly affects premium egg producers, where natural yolk pigmentation supports higher retail prices and organic certification requirements.

Technological Advancement in Carotenoids Extraction and Delivery Methods

Advancements in extraction methods have reduced natural carotenoid production costs while enhancing bioavailability through improved delivery systems. The use of supercritical CO2 extraction eliminates solvent residues and increases carotenoid purity, addressing food safety requirements and lowering processing costs compared to conventional solvent extraction. The application of enzymatic extraction using cellulases and pectinases increases yield from marigold petals and other plant sources, improving the economic viability of natural carotenoid production. Microencapsulation protects carotenoids from oxidation during feed processing and storage, extending product shelf life and minimizing supply chain waste.

Marigold Production Contracts Lowering Supply-Chain Risk

Contract farming of marigolds in Mexico and Guatemala provides stability to North American carotenoid processors' supply chains. These agreements establish minimum prices for farmers and ensure consistent raw material availability for processors, reducing the price volatility that previously limited natural pigment adoption. The long-term contracts also support investments in specialized harvesting and processing equipment, which enhances lutein extraction efficiency from marigold flowers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility | -0.8% | Global inputs into North America | Short term (≤ 2 years) |

| Stringent color uniformity specs from quick-service restaurants | -0.6% | United States and Canada foodservice | Medium term (2-4 years) |

| Stability and shelf-life issues | -0.4% | North America distribution networks | Medium term (2-4 years) |

| Limited farmer awareness outside the poultry segment | -0.3% | Rural aquaculture zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility

Raw material costs for carotenoids experience significant fluctuations due to weather-dependent crop yields and the limited number of suppliers, creating budget uncertainty for feed manufacturers who operate on narrow margins. Marigold flower prices vary by season and respond to climate conditions in major growing regions. Supply disruptions in synthetic carotenoid precursors occur due to chemical plant outages, as evidenced by the BASF Ludwigshafen facility fire in July 2024, which affected vitamin A market availability. The limited number of global carotenoid producers increases price sensitivity when individual facilities face disruptions or capacity limitations.

Stringent Color Uniformity Specs from Quick-Service Restaurants

Foodservice chains require strict color specifications for egg products and salmon portions, necessitating precise dosing of carotenoids in animal feed. These specifications often exceed natural color variation ranges, compelling producers to either combine multiple carotenoid sources or increase inclusion rates to achieve consistent results. Meeting these standards accounts for 2-3% of total feed costs in laying hen operations and up to 20% in salmon feed production. Consumers increasingly prefer natural ingredients, but economic pressures favor the use of synthetic carotenoids for achieving color consistency. The additional quality control testing requirements increase operational costs and create risks of batch rejection due to color non-compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Poultry Maintains Dominance

Poultry accounts for 57.80% of the North American feed lutein and zeaxanthin market share in 2025, and is projected to advance at a 7.34% CAGR between 2026-2031. Layer operations require precise lutein and zeaxanthin supplementation to meet the United States Department of Agriculture Grade AA yolk color standards required by retailers. Commercial broiler producers utilize xanthophyll supplementation to enhance skin coloration, particularly for premium branded products. The poultry segment offers the highest returns for pigment suppliers due to efficient premix distribution systems and established technical support infrastructure.

The aquaculture segment is projected to grow at a 7.69% CAGR through 2031. Salmon and trout farming operations require both astaxanthin and lutein supplementation to achieve specific flesh color characteristics for product differentiation. With pigments comprising up to 20% of total feed costs, producers increasingly adopt microencapsulated forms to minimize feed waste. The expanding shrimp production in Mexico and the Gulf Coast regions provides additional growth opportunities, as processors must maintain consistent shell pigmentation to meet export requirements.

By Source: Natural Pigments Lead but Face Cost Pressure

Natural ingredients account for 71.90% of the North America feed lutein and zeaxanthin market size in 2025 and are projected to grow at a 7.36% CAGR during 2026-2031, driven by regulatory requirements and consumer preference for plant-derived ingredients. Marigold, paprika, and algae serve as primary sources for lutein and zeaxanthin production, with enhanced extraction efficiencies reducing the cost difference compared to synthetic alternatives. Manufacturers leverage organic certification premiums to offset higher raw material costs, while encapsulation technology preserves the stability of natural molecules during the feed pelleting process.

Synthetic sources maintain a cost advantage in conventional feed operations, providing consistent oxidative stability and color uniformity. Their market share decreases as food service chains and retailers increase their clean-label requirements. In response, manufacturers invest in the research and development of solvent-free extraction and enzyme-based processes to increase the efficiency of natural ingredient production.

Geography Analysis

The United States holds 61.80% of the North America feed lutein and zeaxanthin market share in 2025. This dominance stems from the country's position as the second-largest poultry producer globally and its growing coastal salmon aquaculture industry. The Food and Drug Administration's established inclusion thresholds facilitate formulation approvals, though supply chain vulnerabilities emerged during events including BASF's 2024 vitamin precursor disruption.

Canada maintains a smaller but high-value position in the North America feed lutein and zeaxanthin market. The Canadian Food Inspection Agency's 2024 approval of saponified paprika oleoresin provided organic egg producers with additional pigment options. The country's salmon farms in British Columbia and Atlantic provinces use astaxanthin and lutein combinations to meet export standards, despite limited domestic pigment crop production due to climate constraints.

Mexico demonstrates the highest regional growth rate at 6.13% CAGR through 2031, benefiting from continuous marigold production and advancing poultry operations. COFEPRIS (Federal Commission for the Protection against Sanitary Risks) aligns its additive regulations with North American standards, though approval processes remain longer. The Pacific coast shrimp aquaculture industry increases its use of pigment-enhanced feeds to meet Asian market color requirements, driving demand for lutein and zeaxanthin concentrates.

Competitive Landscape

The market shows moderate concentration, with five companies, DSM-Firmenich AG, BASF SE, Kemin Industries, Inc., EW Nutrition GmbH, and Nutrex NV - holding the majority market share in 2024, while still allowing space for niche players. DSM-Firmenich AG maintains the largest market share, with its planned spin-off of the Animal Nutrition and Health division aimed at enhancing strategic focus and shareholder value.

DSM-Firmenich AG and BASF SE maintain competitive advantages through patented microencapsulation technology, extending carotenoid shelf life by 18 months - a significant benefit for distributors operating across large geographical areas. Kemin secures its market position through proprietary marigold varieties grown under long-term contracts in Mexico, ensuring a consistent supply of natural lutein. Smaller market participants compete by developing specialized blends for regional preferences or providing comprehensive technical support services to emerging aquaculture customers.

Recent strategic decisions reflect industry transformation. DSM-Firmenich sold its Feed Enzymes Alliance stake to Novonesis for EUR 1.5 billion (approximately USD 1.6 billion) in February 2025, reallocating resources toward the expansion of carotenoids and vitamins. Kemin introduced PROSIDIUM in March 2025, expanding into biosecurity solutions that complement its existing pigment products. BASF divested its Food and Health Performance Ingredients unit in December 2024 to concentrate on nutrition and feed additives operations, including feed lutein and zeaxanthin.

North America Feed Lutein And Zeaxanthin Industry Leaders

DSM-Firmenich AG

BASF SE

Kemin Industries, Inc.

EW Nutrition GmbH

Nutrex NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Vepinsa conducted a specialized pigmentation course on lutein and zeaxanthin at the National Autonomous University of Mexico (UNAM). The course attracted 20 poultry industry professionals from El Salvador, Ecuador, Colombia, Guatemala, Peru, and Mexico. Participants received technical training at UNAM and visited natural pigment production facilities and distribution centers that supply broiler chickens to the Mexican market.

- January 2024: Kemin Industries, Inc., a manufacturer of feed lutein and zeaxanthin, has introduced its new global tagline, "Compelled by Curiosity." The company uses this tagline worldwide, including the North America, to showcase its focus on innovation, collaboration, and exploration of new possibilities.

North America Feed Lutein And Zeaxanthin Market Report Scope

Lutein or zeaxanthin are yellow carotenoid antioxidants known as macular pigments and are used in animal feed for coloring skin, muscle, feathers, scales, and egg yolk. These are used for various animal types including ruminants, poultry, swine, and aquaculture, among others. The North America feed lutein and zeaxanthin market is segmented by Animal Type (Ruminants, Poultry, Swine, Aquaculture, and Other Animal Types) and Geography (United States, Canada, Mexico, and the Rest of North America). The report offers market size and forecasts in terms of value (USD) for all of the above.

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Other Animal Type (Equine, Camel, etc.) |

| Natural |

| Synthetic |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Animal Type | Poultry |

| Swine | |

| Ruminants | |

| Aquaculture | |

| Other Animal Type (Equine, Camel, etc.) | |

| By Source | Natural |

| Synthetic | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America feed lutein and zeaxanthin market?

The market is valued at USD 57.68 million in 2026.

How fast is the market projected to grow?

It is forecast to expand at a 5.23% CAGR, reaching USD 74.42 million by 2031.

Which animal segment uses the most lutein and zeaxanthin?

Poultry leads with 57.80% market share in 2025 because of stringent yolk color standards.

Why are natural pigments gaining traction?

The United States Depertment of Agriculture Organic rules prohibit most synthetic additives and consumers favor clean-label products, giving natural pigments 71.90% share in 2025.

Which country shows the fastest growth?

Mexico is projected to grow at a 6.13% CAGR through 2031 as aquaculture and modern poultry facilities expand.

Page last updated on: