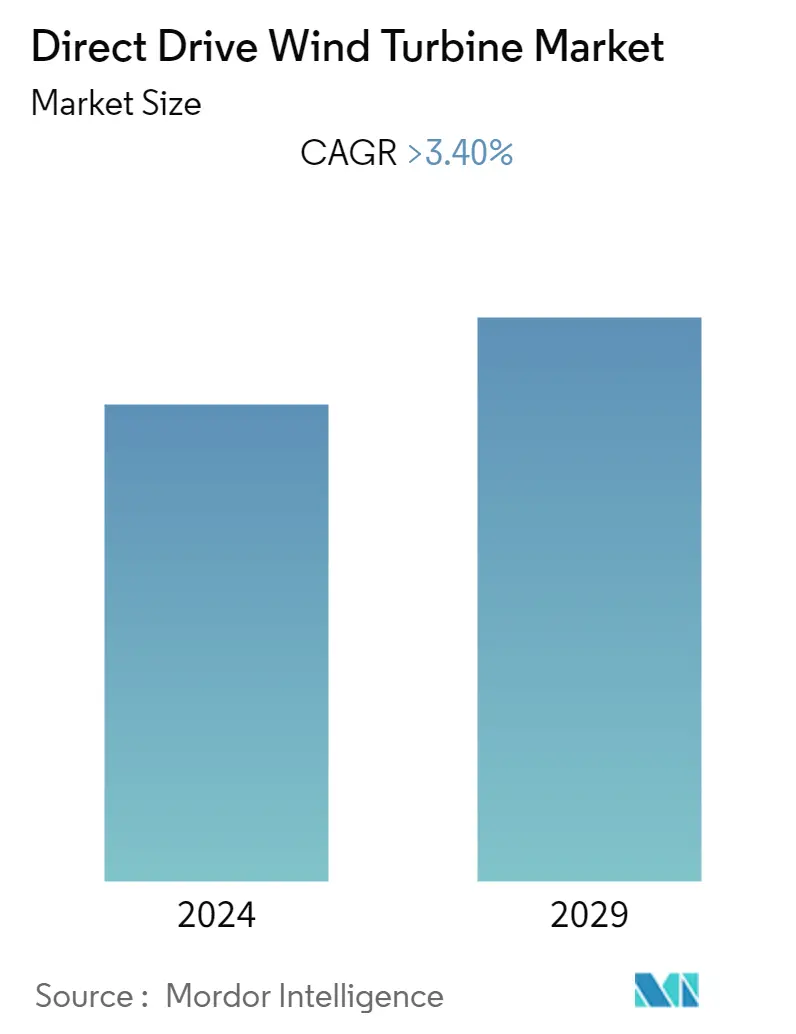

Direct Drive Wind Turbine Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | > 3.40 % |

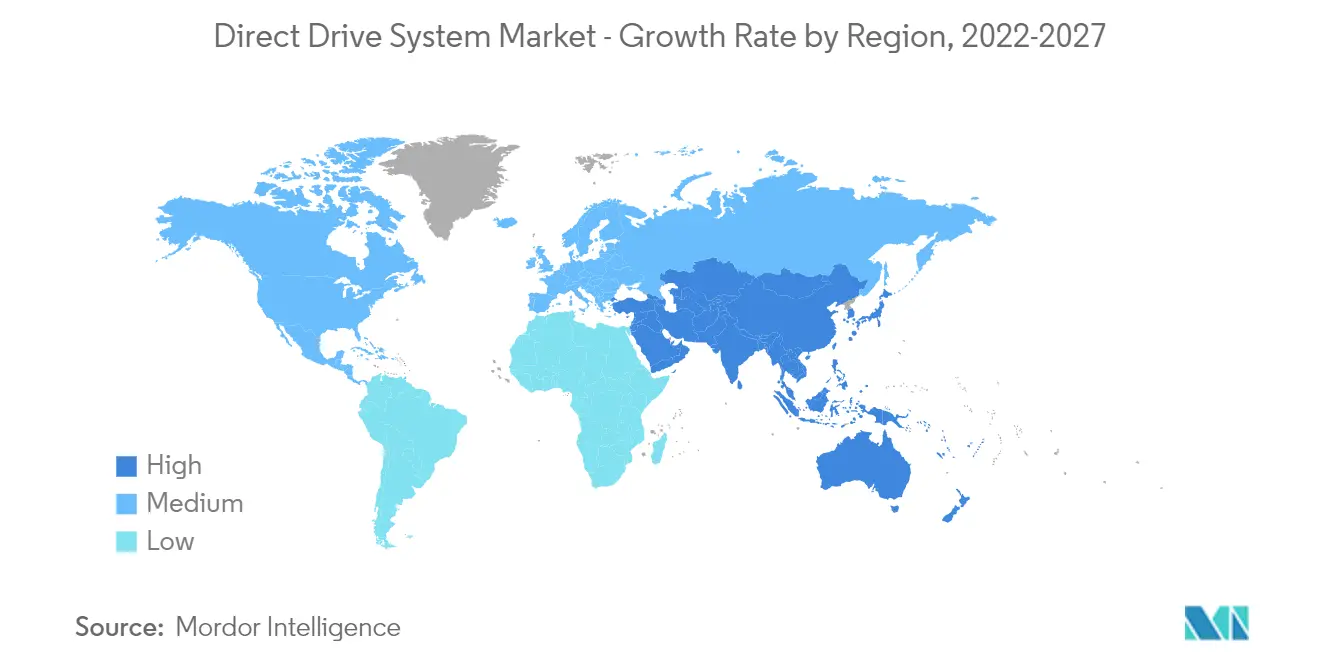

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

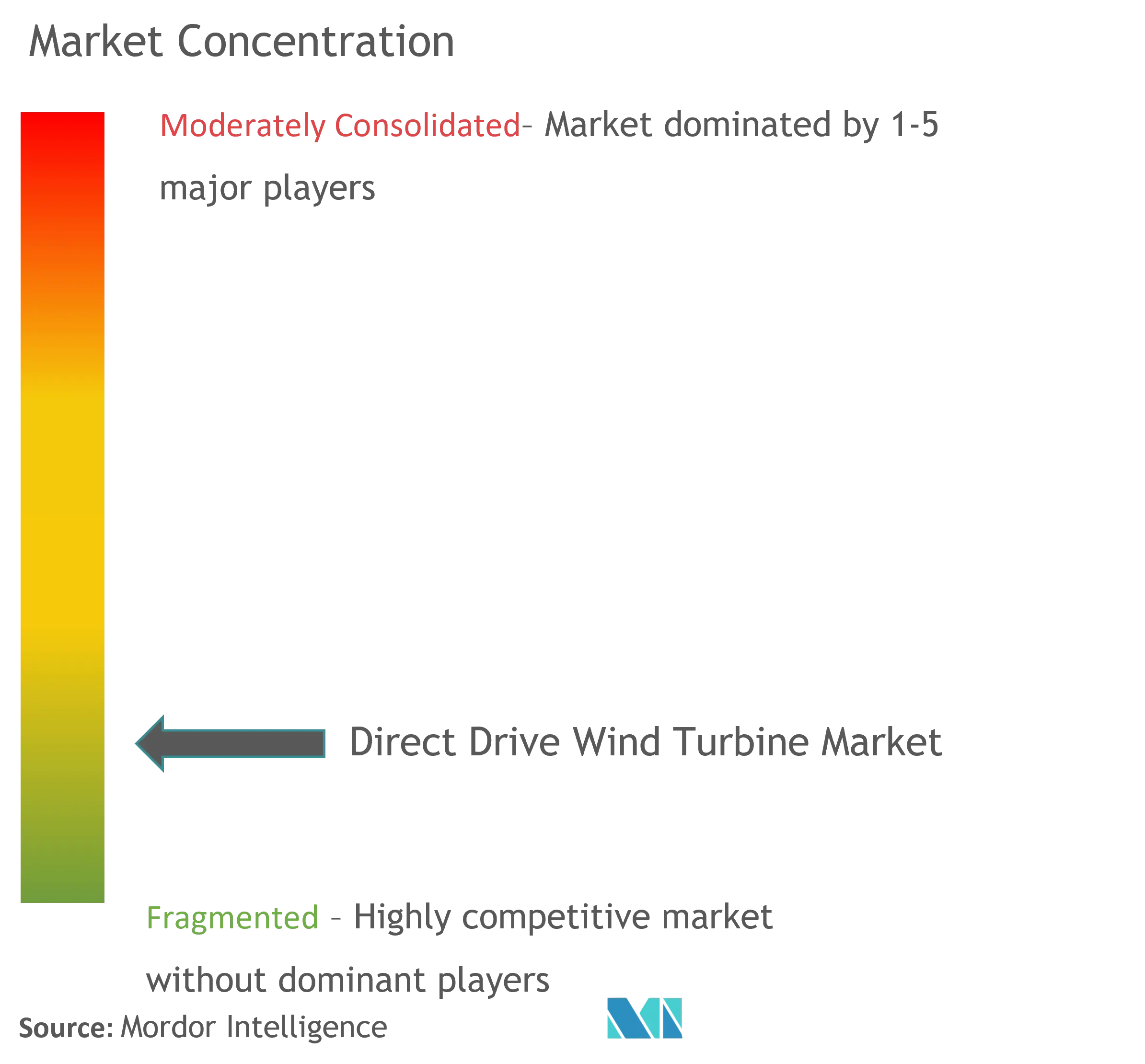

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Direct Drive Wind Turbine Market Analysis

The direct drive wind turbine market is anticipated to register a CAGR of more than 3.4% during the forecast period. In 2020, the COVID-19 outbreak had a moderate impact on the market due to the stringent lockdown protocols imposed by governments worldwide, leading to a delay in the production of direct drive wind turbines. Favorable government policies to adopt clean energy may boost the demand for direct drive wind turbines during the forecast period. The leading wind power plant players have started adopting direct drive systems from the traditional gearbox system due to turbines. Direct drive systems are lighter and more cost-efficient than traditional wind turbines. They do not contain a gearbox, which reduces their weight and eliminates the maintenance problems related to the gearbox. However, the initial capital investment required for a wind power plant is slightly higher compared to the other renewable and non-renewable energy markets. This factor, in turn, is expected to hinder the growth of the market in the coming years.

- Technological advancements, such as increased capacity (1 MW - 3 MW direct drive system) wind turbines, floating wind turbines, and 3D printing, have cut down offshore wind power's overall cost drastically, opening new offshore locations that may drive the wind turbine direct-drive systems market during the forecast period.

- Moreover, the integration of innovative technology in wind turbine direct drive systems will enable advanced condition monitoring and predictive maintenance, resulting in increased efficiency and reduced operational and maintenance costs, which may create a significant opportunity for the market in the future.

- Asia-Pacific is one of the largest growing markets for direct drive wind turbines. As per the Global Wind Energy Council (GWEC), Asia-Pacific has the largest installed wind energy capacity, accounting for around 60% of the global new wind installed capacity in 2020.

Direct Drive Wind Turbine Market Trends

This section covers the major market trends shaping the Direct Drive Wind Turbine Market according to our research experts:

Offshore Segment to Witness Growth for Turbine Capacity of 1 MW – 3 MW

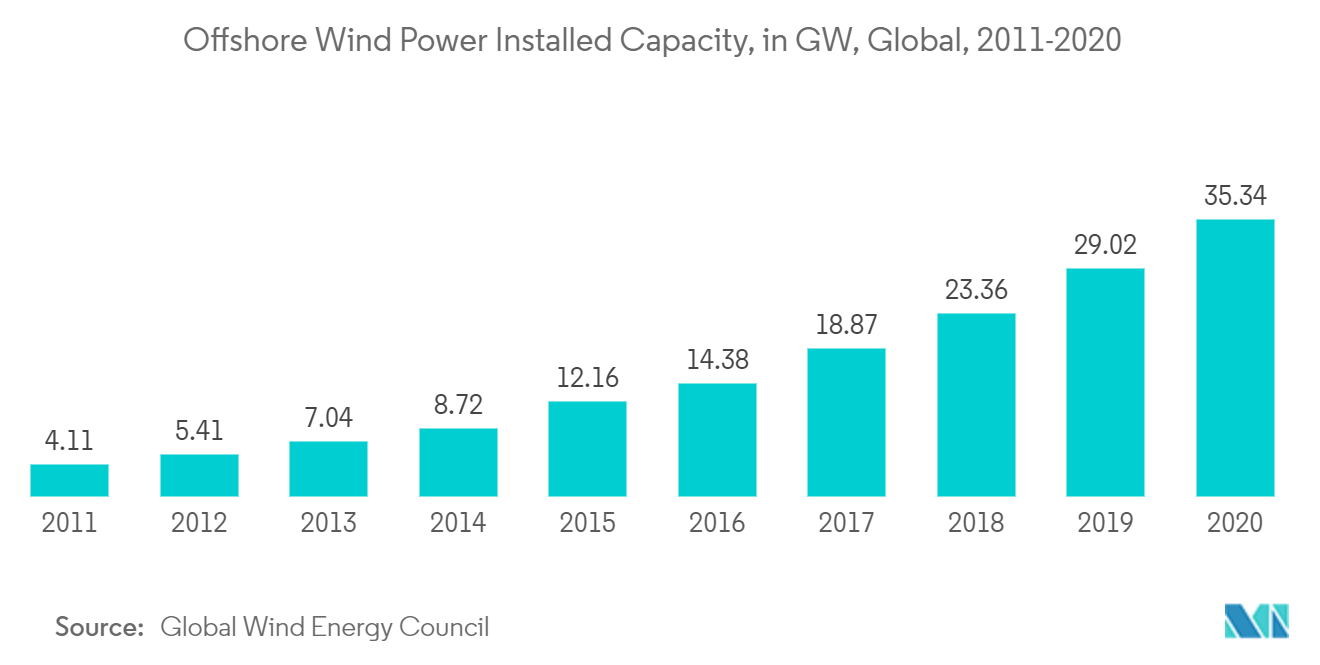

- In 2020, total offshore wind installed capacity surpassed the 35 GW mark, accounting for around 4.8% of the total wind capacity. By 2025, the share of the new offshore installation is expected to exceed 10%, and the total installed base is expected to reach 100 GW, majorly installed with a direct drive system of 1 MW - 3 MW.

- The global offshore market witnessed significant new installations of around 6 GW in 2020. China accounted for almost half of the new installations, propelling the direct drive wind turbine market.

- The offshore wind annual installations are likely to quintuple by 2025 from 6.1 GW in 2020. In total, around 70 GW of new offshore wind capacity is projected to be added worldwide between 2021 and 2025. Further, the global demand for wind turbine direct drive systems in the offshore sector is increasing significantly.

- The wind turbine direct-drive systems are much more robust, efficient, and costlier, as the wind speed in offshore regions is higher. Hence, the growth of the offshore wind energy sector is expected to have a significant impact on the market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The installed wind capacity in Asia-Pacific increased to 346.69 GW in 2020 from 291.08 GW in 2019. China's installed capacity primarily dominates the increasing wind capacity.

- According to IRENA, Asia-Pacific may become the world's dominant wind market, accounting for more than 50% of onshore and 60% of offshore wind installations by 2050. Asia's onshore wind capacity is expected to grow from 336 GW in 2020 to over 2,600 GW by 2050.

- Furthermore, the region attracts significant investments from countries like China and India and emerging countries like Taiwan's wind sector. Chinese manufacturers comprise nearly 95% of the overall wind power market. The government policy and incentives have made China a favorable hotspot for investment. In 2020, the country accounted for over 55% of the new onshore global wind installed capacity.

- In addition, India holds the fourth-largest wind power installed capacity globally. These projects are majorly spread in the northern, southern, and western parts of the country. The government has set a target of 60 GW by 2022. The number of projects during the next two years is expected to increase drastically.

- This factor, in turn, is expected to present Asia-Pacific as an excellent business destination for players involved in the wind turbine direct drive systems business during the forecast period.

Direct Drive Wind Turbine Industry Overview

The direct drive wind turbine market is moderately fragmented. The key players in the market include ABB Ltd, Voith GmbH, Avantis Energy Group, Goldwind Science & Technology Co. Ltd, and Emergya Wind Technologies BV.

Direct Drive Wind Turbine Market Leaders

ABB Ltd

Voith GmbH

Avantis Energy Group

Goldwind Science & Technology Co. Ltd

Emergya Wind Technologies BV

*Disclaimer: Major Players sorted in no particular order

Direct Drive Wind Turbine Market News

- In December 2021, Siemens Gamesa received an order from Orsted for a German offshore wind power project to supply 23 Siemens Gamesa 11.0-200 direct drive offshore wind turbines. The scope of the order includes a five-year service agreement. This order may enhance the company's presence in the German offshore wind industry.

Direct Drive Wind Turbine Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Forecast in USD billion, till 2027

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.2 Restraints

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Capacity

5.1.1 Less than 1 MW

5.1.2 1 MW - 3 MW

5.1.3 Greater than 3 MW

5.2 Geography

5.2.1 North America

5.2.2 Europe

5.2.3 Asia-Pacific

5.2.4 South America

5.2.5 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 ABB Ltd

6.3.2 Siemens Gamesa Renewable Energy SA

6.3.3 Rockwell Automation Inc

6.3.4 Bachmann electronic GmbH

6.3.5 Avantis Energy Group

6.3.6 Goldwind Science & Technology Co. Ltd

6.3.7 Emergya Wind Technologies BV

6.3.8 Northern Power System

6.3.9 Enercon GmbH

6.3.10 M. Torres Olvega Industrial

6.3.11 ReGen Powertech Pvt. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Direct Drive Wind Turbine Industry Segmentation

The scope of the direct drive wind turbine market includes:

| Capacity | |

| Less than 1 MW | |

| 1 MW - 3 MW | |

| Greater than 3 MW |

| Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle-East and Africa |

Direct Drive Wind Turbine Market Research FAQs

What is the current Direct Drive Wind Turbine Market size?

The Direct Drive Wind Turbine Market is projected to register a CAGR of greater than 3.40% during the forecast period (2024-2029)

Who are the key players in Direct Drive Wind Turbine Market?

ABB Ltd, Voith GmbH , Avantis Energy Group , Goldwind Science & Technology Co. Ltd and Emergya Wind Technologies BV are the major companies operating in the Direct Drive Wind Turbine Market.

Which is the fastest growing region in Direct Drive Wind Turbine Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Direct Drive Wind Turbine Market?

In 2024, the Asia Pacific accounts for the largest market share in Direct Drive Wind Turbine Market.

What years does this Direct Drive Wind Turbine Market cover?

The report covers the Direct Drive Wind Turbine Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Direct Drive Wind Turbine Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Direct Drive Wind Turbine Industry Report

Statistics for the 2024 Direct Drive Wind Turbine market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Direct Drive Wind Turbine analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.