North America Decorative And Illuminated Mirror Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

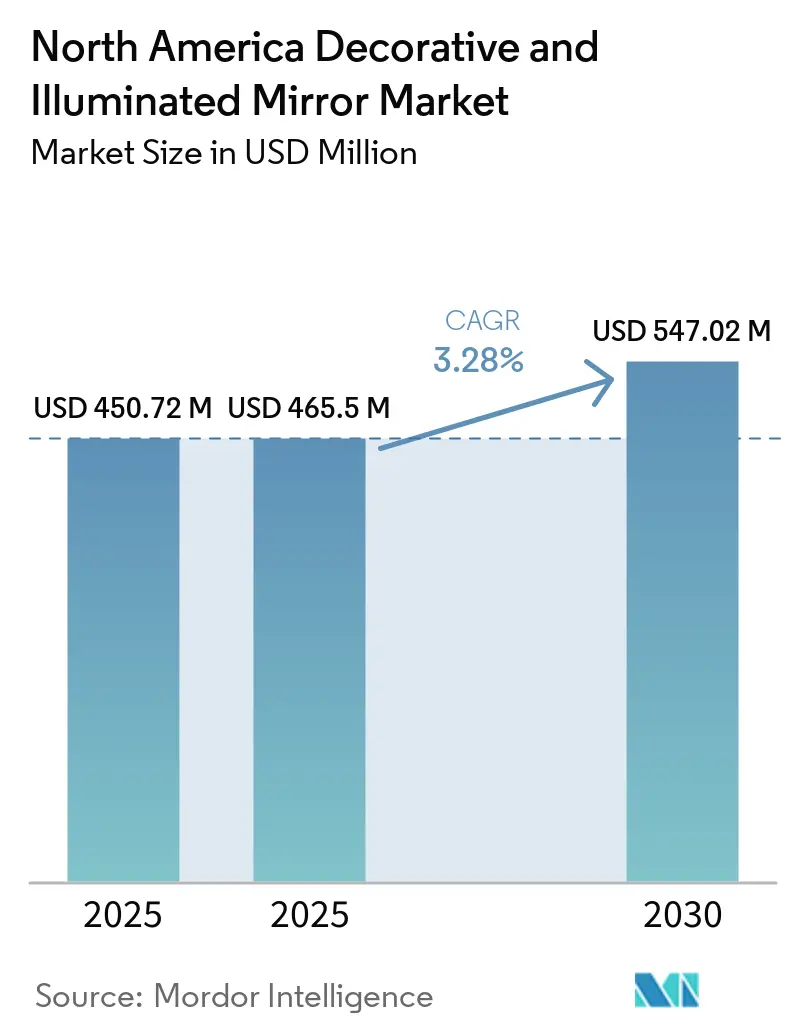

| Base Year Market Size (2025) | USD 450.72 Million |

| Market Size (2025) | USD 465.5 Million |

| Market Size (2030) | USD 547.02 Million |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Decorative And Illuminated Mirror Market Analysis by Mordor Intelligence

The North America illuminated bathroom mirror market size is projected to expand from USD 450.72 million in 2025 and USD 465.50 million in 2026 to USD 547.02 million by 2031, registering a CAGR of 3.28% between 2026 and 2031. Elevated material costs continue to challenge suppliers and installers, with metal window prices up 20.3% year-over-year in February 2026 and flat glass manufacturing costs 6.5% higher, yet premium demand is holding as spec-grade, high-CRI LED mirrors win buyers who want code-compliant performance and durable construction. New energy codes are also reshaping product roadmaps in the North America illuminated bathroom mirror market, since California’s Title 24 rules, effective January 2026, require 90+ CRI, tight flicker thresholds, and continuous dimming, which retire older fluorescent and low-CRI options from remodel and new-build specifications[1]California Energy Commission, “2025 Building Energy Efficiency Standards,” California Energy Commission, energy.ca.gov. Renovation and conversion cycles in hospitality are embedding illuminated mirrors into wellness-driven bathroom programs that target higher room rates and guest satisfaction, lifting specification density across upper-upscale and luxury properties. E-commerce’s steady gains at major home centers, combined with AI-driven configurators and guided selling, are improving product discovery and attachment rates for backlit and front-lit mirrors across both DIY and Pro buyers. Taken together, building-code momentum, hospitality refurbishments, and better digital selling tools are poised to keep specification-grade models on a steady growth path, even as commodity SKUs face tighter margins due to structural input-cost inflation in North America.

Key Report Takeaways

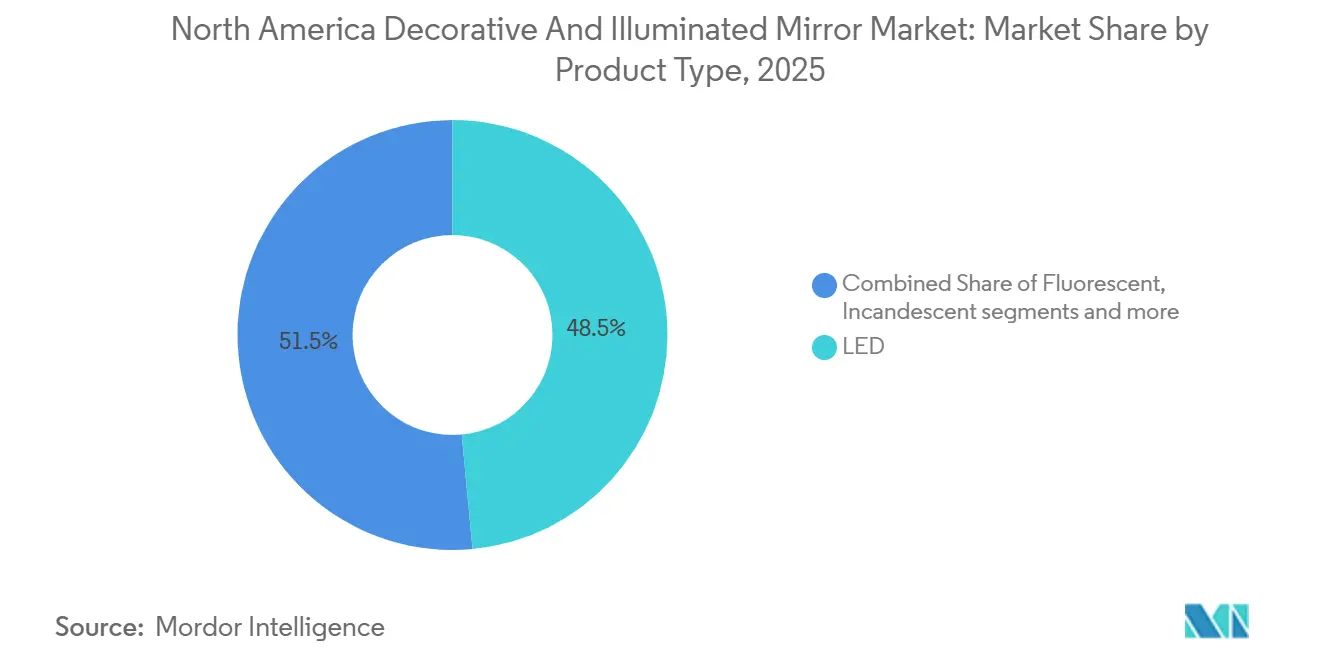

- By product type, LED accounted for 48.52% of revenue in the 2025 North America Decorative and Illuminated Mirror Market, and hybrid lighting systems are projected to expand at a 4.25% CAGR through 2031.

- By application, residential accounted for 62.58% share in the 2025 North America Decorative and Illuminated Mirror Market, and commercial deployments are forecast to grow at a 5.31% CAGR through 2031.

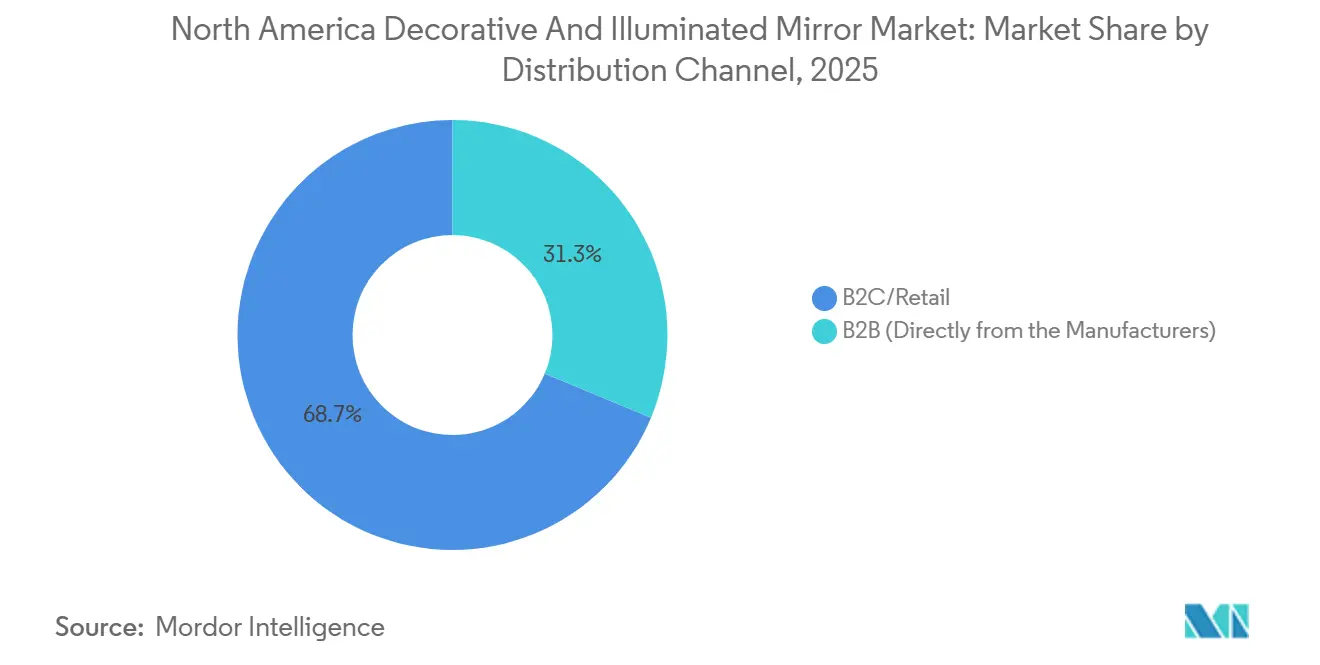

- By distribution channel, B2C retail held 68.72% share in 2025, and B2B direct sales to contractors and developers are expected to grow at a 4.71% CAGR through 2031.

- By geography, the United States captured 84.52% of revenue in 2025, and Mexico is projected to post a 6.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Decorative And Illuminated Mirror Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remodeling Upturn Supports Bathroom Upgrades | 0.90% | United States metro markets and Canadian urban centers; strongest in Sun Belt states and Greater Toronto Area | Medium term (2-4 years) |

| LED Dominance In Homes Drives Illuminated Mirror Demand | 1.00% | United States and Canada nationwide; particularly strong in California, Texas, New York, and British Columbia | Long term (≥ 4 years) |

| Hospitality Wellness Design Adopting Backlit/Front-Lit Mirrors | 0.50% | United States hospitality corridors (New York, Las Vegas, Miami, Los Angeles); emerging in Canadian resort destinations | Medium term (2-4 years) |

| Strong E-Commerce Penetration In Home & Living Boosts Online Mirror Sales | 0.70% | United States and Canada; accelerated by Amazon, Wayfair, and Home Depot digital platforms | Short term (≤ 2 years) |

| Customization & Personalization Demand | 0.50% | United States premium segments (coastal metros, affluent suburbs); growing in Canadian tier-1 cities | Medium term (2-4 years) |

| Multifunctional Space Optimization in Modern Homes | 0.60% | United States urban markets (New York, San Francisco, Seattle); Canadian condos in Toronto, Vancouver, Montreal | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LED Dominance In Homes Drives Illuminated Mirror Demand

Adoption of LED lighting in United States homes has reached mainstream levels, with 51% of renovating homeowners purchasing light fixtures in 2024 and 13% selecting smart variants, which are lifting attachment rates for integrated, high-CRI illuminated mirrors in bathroom upgrades. New launches are addressing fine-tuned grooming requirements and design control, illustrated by Robern’s Instinct Mirror, which supports on-mirror color temperature and brightness control across a 2700K to 5600K range, auto-off timers, and integrated defoggers, while IKEA’s FAXÄLVEN series targets mid-market buyers with smart-home pairing and value-led price points. California’s Title 24 sets performance thresholds that make high-CRI, low-flicker LED sources the practical baseline for new construction and major remodels, lifting quality expectations within the North America illuminated bathroom mirror market. Seniors are also increasing spending on better task lighting, with median bathroom remodel outlays rising to USD 15,300 in 2024, further supporting integrated-mirror installations designed for consistent color rendering and safer daily routines. Electrical compliance is reinforcing this structural shift, as installers avoid non-NRTL-listed products and local authorities will not approve final occupancy without compliant labeling, factors that favor UL- or ETL-listed LED mirrors in both residential and commercial projects.

Remodeling Upturn Supports Bathroom Upgrades

Remodeling activity remains resilient in early 2026, supported by a record outlook for owner-occupied improvement spending and steady bathroom project demand, which keeps the North America illuminated bathroom mirror market on a growth track even as affordability weighs on mid-market buyers. The mix is bifurcating: high-end bathroom spending for large primary baths rose to USD 70,000 in 2024, while median spending trended lower, signaling that affluent cohorts are prioritizing specification-rich mirrors with dimming, defogging, and tunable-white features. New product families such as Robern’s Presence Cabinet highlight how integrated storage and lighting can meet this specification standard by combining tunable task lighting, power access, and moisture resistance in a single assembly. Value-focused consumers continue to participate through direct-to-consumer options like IKEA’s lighted mirrors that pair with smart-home hubs and align to budget ceilings, which sustains baseline unit sales even when big-ticket remodel interest softens[2]IKEA, “FAXÄLVEN Mirror with Built-in Lighting,” IKEA, ikea.com. Installation methods are also responding to price sensitivity, with plug-and-play designs that reduce labor costs for DIY-friendly buyers. At the same time, hardwired units remain the standard for projects that must meet code or hospitality brand requirements.

Hospitality Wellness Design: Adopting Backlit/Front-Lit Mirrors

Hotel owners are using illuminated mirrors to elevate the guest experience during widespread renovation waves, as seen in the United States pipeline, where conversions and refurbishments reached a record 2,118 projects in Q4 2025, pushing specification density for backlit and front-lit mirrors across premium flags. Major properties have already implemented these upgrades, including MGM Grand Las Vegas, with 4,212 rooms remodeled by December 2025, and Hilton Los Angeles Airport, with a USD 50 million renovation scheduled for completion before global sports events in mid-2026, each selecting illuminated mirror packages as standard room features. High-profile developments like the USD 1.3 billion Gaylord Pacific Resort demonstrate how large-scale projects coordinate global material sourcing while aligning bathroom fixtures to domestic electrical codes and inspection requirements. Product innovation is also expanding the category’s role, with Séura’s Smart TV Mirrors integrating display and lighting functions to blend grooming, entertainment, and wellness, which opens a new tier of feature sets for upper-upscale suites and spa environments[3]Séura, “Séura Introduces Next Generation Smart TV Mirrors,” Séura, seura.com. These hospitality trends support the North America illuminated bathroom mirror market by making illuminated solutions part of brand standards and guest-experience narratives in premium segments.

Strong E-Commerce Penetration In Home & Living Boosts Online Mirror Sales

E-commerce penetration has increased at leading home-improvement retailers, with Home Depot reporting online sales at 15.5% of net sales in 1Q25 and Lowe’s noting a 9.5% lift in online performance in Q4 2024, driven by AI-enabled assistants that double conversion rates versus non-assisted sessions. Configurators are improving the path to purchase for illuminated mirrors by letting buyers choose sizes, finishes, color temperatures, and add-ons such as defoggers and magnification zones, which aligns product selection with exact bathroom layouts and aesthetic needs. Government data showed steady growth for nonstore retailers in spring 2025, signaling resilience in online channels even as discretionary categories face mixed demand. B2B e-commerce capabilities are seeing positive traction as well, with Lowe’s Pro Extended Aisle and AI-enabled Pro Companion improving complex order handling and job-specific recommendations for contractors that purchase mirror packages alongside other bath fixtures. This shift continues to shape the North America illuminated bathroom mirror market as showrooms pivot toward design consultation. digital platforms take on an expanding share of assortment display and configuration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Input Costs In Flat Glass And Metals Pressure Pricing And Margins | -0.6% | United States and Canada; acute in energy-intensive manufacturing regions and import-dependent supply chains | Short term (≤ 2 years) |

| Installation And Electrical Compliance Complexity For Hardwired Mirrors Raises TCO | -0.4% | United States markets subject to NEC (National Electrical Code); Canadian provinces with CSA standards enforcement | Medium term (2-4 years) |

| Supply-Chain Reliability And Warranty-Return Risks In Hospitality Projects | -0.2% | United States hospitality markets; cross-border procurement affecting Canadian hotel chains | Short term (≤ 2 years) |

| Remodeling Softness/Uncertainty Can Delay Discretionary Purchases | -0.5% | United States housing-sensitive markets; Canadian exposure tied to mortgage-rate volatility and construction cycles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Input Costs in Flat Glass and Metals Pressure Pricing and Margins

Producer price data show sustained cost escalation across construction inputs, with flat glass manufacturing up 6.5% year-over-year in February 2026 and metal windows up 20.3%, which is putting pressure on finished goods pricing for mirror manufacturers and channel partners. Aluminum mill shapes rose 33% year-over-year in January 2026, and copper increased 15.7%, compounding the effect of tariffs on steel, aluminum, and copper products imposed in 2024 and pushing manufacturers to revisit bills of materials and pricing strategies. Broader market indicators point to persistent inflation in building inputs through 2025, adding difficulty for contractors who face shrinking windows for locked-in subcontractor pricing and pass-through clauses. Suppliers report that domestic glass producers raised prices in early 2026 and that import substitution offers limited relief due to similar tariff exposure, which puts further near-term pressure on margin profiles in the North America illuminated bathroom mirror market. Industry associations note that building material prices remain materially above pre-pandemic levels, reducing project affordability and increasing the risk of cancellation when budgets cannot absorb contingency buffers[4]National Association of Home Builders, “Building Material Price Growth,” National Association of Home Builders, nahb.org.

Installation And Electrical Compliance Complexity for Hardwired Mirrors Raise TCO

Hardwired illuminated mirrors often require certified fixtures, NEC-compliant installation, and sometimes new or dedicated circuits, which add labor and materials to the unit price and raise the total cost of ownership relative to plug-and-play models. Installers generally reject non-NRTL-marked devices, and inspectors require UL, ETL, or CSA labeling before issuing approvals, which extends timelines and imposes rework risk when submittals or samples do not meet local code requirements. California’s current standards add documentation and inspection steps for luminaires and recessed downlights, including dimming and airtightness criteria, which increases administrative overhead on top of installation requirements. This compliance environment is particularly evident in large hospitality projects that coordinate international supply while meeting local inspection requirements, a dynamic that underscores the value of pre-approved, domestically certified mirror assemblies for schedule certainty. Supply variability since 2025 has also led contractors to add clauses around force majeure and material delays, which shifts timing risk into contracts and elevates the reward for suppliers that can guarantee lead times on compliant mirrors in the North America illuminated bathroom mirror market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Systems Challenge LED’s Efficacy Lock-In

LED held 48.52% of the North America illuminated bathroom mirror market share in 2025 as the default choice for new builds and renovations that seek energy savings, tunable color, and higher CRI for everyday grooming tasks. Hybrid lighting systems that combine ambient LED with dedicated task sources are projected to expand at a 4.25% CAGR between 2026 and 2031 as buyers in professional grooming and medical aesthetics demand very high color accuracy and modality switching within the same mirror assembly. This performance tier is evolving with cross-over products like Séura’s Smart TV Mirrors that integrate 4K displays with illuminated grooming functions for premium suites and spa environments. Regulatory standards are also shifting product mix as Title 24 and ENERGY STAR benchmarks eliminate low-efficacy solutions and promote JA8-compliant LED implementations that meet flicker and CRI thresholds, reinforcing the LED baseline for most home upgrades. For buyers that value installation speed and intuitive control, configurable LED mirrors with on-device dimming, selectable CCT, and defoggers are filling the gap between basic commodity mirrors and the premium custom segment in the North America illuminated bathroom mirror market.

Manufacturers continue to refine efficacy and control to balance cost and performance at each price tier in the North America illuminated bathroom mirror industry. Kohler’s Verdera line illustrates the cost-per-lumen advantage that keeps LED in the lead for residential adoption, while ENERGY STAR-certified downlights showcase how standardized performance targets improve whole-bathroom lighting coordination with mirrors. Hybrid configurations are gaining traction where project specifications require elevated CRI and multiple lighting modes, and they can be priced at a premium due to the added engineering and control complexity. Brands are integrating tunable color and task lighting zones that operate independently, giving users the ability to switch from warm ambient light to cool, high-output task light for grooming accuracy without adding extra fixtures. As code and buyer expectations converge around LED’s efficiency, niche commercial applications and top-of-market residential projects are likely to sustain hybrid growth while most households continue to select integrated LED units for practical value in the North America illuminated bathroom mirror market.

By Application: Commercial Renovations Outpace Residential New Builds

Residential accounted for 62.58% of the North America illuminated bathroom mirror market share in 2025 as homeowners continued to prioritize bathroom projects and high-end remodels expanded their feature sets to include integrated mirrors with tunable light and defogging features. Commercial deployments are forecast to grow at a 5.31% CAGR from 2026 to 2031 due to a record conversion and renovation cycle in hotels, which positions illuminated mirrors as part of standard bathroom packages rather than optional amenities. Brand programs at flagship properties emphasize guest wellness and grooming accuracy, reflected in examples such as MGM Grand’s completed room renovations and Hilton Los Angeles Airport’s renovation schedule that brings updated bathrooms and illuminated mirrors into every refreshed room. Bulk procurement, value engineering, and bundled contracting models help large commercial buyers manage cost inflation by packaging mirrors, lighting, and plumbing into integrated bids, an approach visible in multi-thousand-room hospitality projects.

Household demand remains steady as older homeowners increase remodel budgets and younger cohorts select value-focused solutions, which together sustain volumes in the North America illuminated bathroom mirror market. Premium remodels continue to seek larger mirror formats, precise dimming, and high-CRI output to ensure accurate color rendering for daily routines, which supports the premium tier’s features and finishes. At the same time, median-spend renovators are selecting direct-to-consumer options that balance UL listing and IP ratings with smart-home connectivity at accessible price points. Canada’s 2025 housing starts total and the pipeline of multifamily units support a baseline of residential demand for specification-compliant mirror packages in new condos and apartments that aim to differentiate with lighting and finish upgrades. These dynamics keep residential volumes high, while the commercial side leads growth as conversion-heavy hospitality refurbishments apply illuminated mirrors as an element of experiential bathroom design in the North America illuminated bathroom mirror industry.

By Distribution Channel: B2B Direct Gains on Contractor E-Procurement

B2C retail controlled 68.72% of channel share in 2025, supported by higher online penetration at home centers and robust search-to-cart conversion for lighted mirrors that feature clear specifications and compatible dimming guidance. B2B direct is projected to be the fastest grower at a 4.71% CAGR through 2031 as contractors embrace AI-supported procurement and extended digital aisles that streamline configuration, quoting, and bulk ordering for bathroom programs in the North America illuminated bathroom mirror market. Suppliers are enabling this shift with online configurators and spec tools that let Pros set size, finish, and color temperature and then generate job-ready SKUs with documentation for submittals and inspections. Showrooms are adapting by focusing on layout planning and material coordination rather than stocking broad assortments, while retailer promotions steer traffic toward exclusive SKUs that reduce channel conflict and control pricing.

Nonstore retail growth during 2025 supports the broader online shift, while furniture and home furnishings stores grow at a similar pace, indicating that consumers remain willing to transact online for bath fixtures that have clear specifications and dependable delivery timelines. B2B buyers cite scheduling certainty and allocation guarantees as core reasons to centralize purchasing with manufacturers and national retailers, since material volatility has challenged fixed-price windows and contributed to project delays in 2025. As AI-driven tools and extended assortments mature, the North America illuminated bathroom mirror industry continues to shift toward platforms that compress the path from selection to installation, reduce rework risk, and improve documentation readiness for inspections. These changes benefit B2B direct and integrated retail ecosystems, while multi-brand stores focus on design advisory roles to sustain relevance in the North America illuminated bathroom mirror market.

Geography Analysis

The United States captured 84.52% of 2025 revenue, reflecting the depth of its remodel and hospitality cycles, with bathroom projects matching kitchen projects at 24% of homeowner activity in 2024 and high-end spend for large primary baths rising to USD 70,000. The national hotel pipeline reached an all-time high in Q4 2025, and conversions plus renovations set a record, which helps standardize illuminated mirrors as default bathroom fixtures across premium flags in the North America illuminated bathroom mirror market. California’s Title 24 code mandates CRI, flicker, and dimming performance that aligns with integrated LED mirrors and narrows options to certified solutions for new construction and major remodels. Domestic capacity additions by major bath brands shorten lead times and reduce exposure to international freight variability, which can improve product availability and delivery reliability for specification-driven projects. Even with these supports, consumer confidence in big-ticket remodeling remains sensitive to mortgage rates and material costs, which shape the mix between premium and value offerings in the North America illuminated bathroom mirror market.

Canada’s 2025 housing starts increased from 2024 levels, with multiple-unit projects accounting for a large share of new units in high-density markets, which supports baseline demand for specification-ready bathroom mirrors in new condos and apartments. A new ceramics manufacturing facility in Québec marks a strategic local-for-local investment that reduces transport emissions and shortens supply lines for North American projects that include lighted mirrors as part of their bath programs. Canadian installers apply similar certification expectations to United Staes counterparts under CSA standards, reinforcing the value of UL- or ETL-listed assemblies regardless of province. Provincial starts data indicate steady demand in Ontario and Quebec, while British Columbia softens in early 2026, a pattern that aligns with interest rate sensitivity and local housing policy. These regional dynamics sustain unit demand patterns, with mid-market projects favoring value-led integrated mirrors and premium urban projects specifying high-CRI tunable models in the North America illuminated bathroom mirror market.

Mexico is the fastest-growing country in this scope as new housing registrations surged and a national plan targets up to 400,000 homes in 2026, which expands the addressable base for future upgrades, even if many social-interest units initially specify basic mirrors. Housing prices rose in 2025, especially in coastal destinations, which drives premium bathroom fixture selection in resort and second-home developments that cater to international buyers and urban professionals. Broader public investment supports construction employment and creates spillover demand for housing, where illuminated mirrors can be used as differentiation features in mid-tier projects as incomes rise, improving the long-run prospects for the North America illuminated bathroom mirror market. Structural backlogs and affordability gaps still constrain near-term premium adoption, which keeps value-led offerings critical for unit growth until incomes and credit availability expand. Over time, as supply improves and incomes stabilize, upgrade cycles should lift attachment rates for better-performing mirror assemblies that meet international safety and performance standards in the North America illuminated bathroom mirror market.

Competitive Landscape

The North America illuminated bathroom mirror market features a balanced mix of established bath brands and mass-market retailers, with differentiation anchored in certification, design integration, and delivery reliability. Large incumbents are localizing parts of their supply chains to reduce transit risk and improve service levels, illustrated by new United States manufacturing facilities that support plumbing and bathing lines linked to mirror programs. European entrants are also investing in North American capacity to serve regional demand and sustainability goals by eliminating long-distance freight, which aligns with buyer preferences for shorter lead times and consistent quality. Code compliance remains a key differentiator as UL- and ETL-marked mirrors move through approval processes more predictably, reducing inspection risk and favoring brands that maintain up-to-date listings across product families. On the mass-market side, direct-to-consumer channels emphasize quick-ship models with clear specifications and smart-home compatibility, offering value-led solutions that still satisfy safety and performance standards.

Product roadmaps increasingly incorporate tunable lighting, defogging, and integrated storage with power access to meet higher expectations in both premium residential and hospitality segments of the North America illuminated bathroom mirror market. Robern’s modular systems demonstrate how cabinet lighting and mirror lighting can coordinate to deliver consistent facial illumination and intuitive control through on-mirror interfaces, which streamlines installation and use. Cross-category innovations like Séura’s Smart TV Mirrors open a new feature space that combines backlighting with entertainment and environmental control, expanding the set of use cases in premium bathroom and spa installations. Retailers continue to upgrade their digital buying support for Pros through extended assortments and AI-driven assistance, which improves conversion and supports larger project baskets that often include illuminated mirrors, lighting, and plumbing fixtures purchased together. These channel and product shifts help brands defend share across value tiers within the North America illuminated bathroom mirror market as price pressure persists due to metals and glass inflation.

Certification parity between UL and ETL under NRTL recognition has leveled the field for code acceptance, though architect familiarity sometimes leads to a preference for UL on specifications and ETL on value-engineered alternatives due to approval speed and cost. Brands that maintain broad and current certifications across mirror families reduce project risk and gain an advantage during design reviews and inspections, which shortens time to closeout and improves owner satisfaction in the North America illuminated bathroom mirror market. In this environment, marketing narratives that focus on specification clarity, safety labeling, and proven installation workflows can be more persuasive than purely aesthetic claims. As code requirements tighten and supply chains localize, leaders are likely to be those who combine reliable compliance with flexible configuration and consistent lead times supported by domestic capacity. These tools and investments protect share in segments where illuminated mirrors are now part of baseline expectations for bathroom quality, durability, and guest experience across North America.

North America Decorative And Illuminated Mirror Industry Leaders

Electric Mirror

Robern (Kohler)

Séura

OVE Decors

Krugg Reflections

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Duravit officially opened its first North American manufacturing facility in Matane, Canada, a CAD 90 million investment spanning 35,000 square meters with capacity to produce 450,000 sanitary ceramics annually for the North American market.

- September 2025: Robern launched the Instinct Mirror, an illuminated mirror serving as both primary reflection and light source with customizable color temperature and output via on-mirror touch control, built-in defogging technology, and an auto-off timer to save electricity.

- August 2025: TOTO opened a USD 224 million state-of-the-art manufacturing facility in Morrow, Georgia, increasing United States luxury one-piece toilet production capacity by 150% (approximately 300,000 units annually) and bringing total Americas capacity to 1 million units across Morrow, Lakewood, and Mexico plants.

- April 2025: Robern introduced the Presence Cabinet, a frameless medicine cabinet available in multiple shapes, featuring perimeter lighting and On-Mirror TUN Technology, integrated interior lighting, built-in electrical outlets with USB ports, storage solutions, and moisture-resistant construction.

North America Decorative And Illuminated Mirror Market Report Scope

Illuminated mirrors are a type of home accessory. Unlike ordinary mirrors, the illuminated mirror reflects the face. Light is generated within the mirror itself.

The North American decorative and illuminated mirror market is segmented into type, application, distribution channel, and geography. The market is segmented by type into LED technology, fluorescent, and incandescent. The market is segmented by application into bathrooms, bedrooms, and hallways. By distribution channel, the market is segmented into online and offline. The market is segmented by geography into the United States, Canada, Mexico, and the Rest of North America. The report offers market size and forecasts for the North American decorative and illuminated mirror market in value (USD) for all the above segments.

| LED |

| Fluorescent |

| Incandescent |

| Hybrid Lighting Systems |

| Residential |

| Commercial |

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (Directly from the Manufacturers) |

| United States |

| Canada |

| By Product Type | LED | |

| Fluorescent | ||

| Incandescent | ||

| Hybrid Lighting Systems | ||

| By Application | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (Directly from the Manufacturers) | ||

| By Geography | United States | |

| Canada | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the North America illuminated bathroom mirror market?

The North America illuminated bathroom mirror market size is USD 465.50 million in 2026 and is projected to reach USD 547.02 million by 2031 at a 3.28% CAGR from 2026 to 2031.

Which application will grow fastest through 2031 in North America?

Commercial deployments, supported by record hotel conversions and renovations, are projected to grow at a 5.31% CAGR through 2031.

Which product type leads in the North America illuminated bathroom mirror market?

LED models lead with 48.52% share in 2025, while hybrid systems post the fastest growth at a 4.25% CAGR to 2031.

How are codes and standards affecting product selection?

California’s Title 24 mandates high-CRI, low-flicker, dimmable LED sources for permanently installed luminaires in 2026, which pushes integrated LED mirrors into baseline specifications.

What distribution channels are gaining traction among contractors?

B2B direct is gaining with a 4.71% CAGR outlook through 2031 as AI-enabled procurement tools and extended digital assortments streamline job-specific ordering.

Page last updated on: