Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

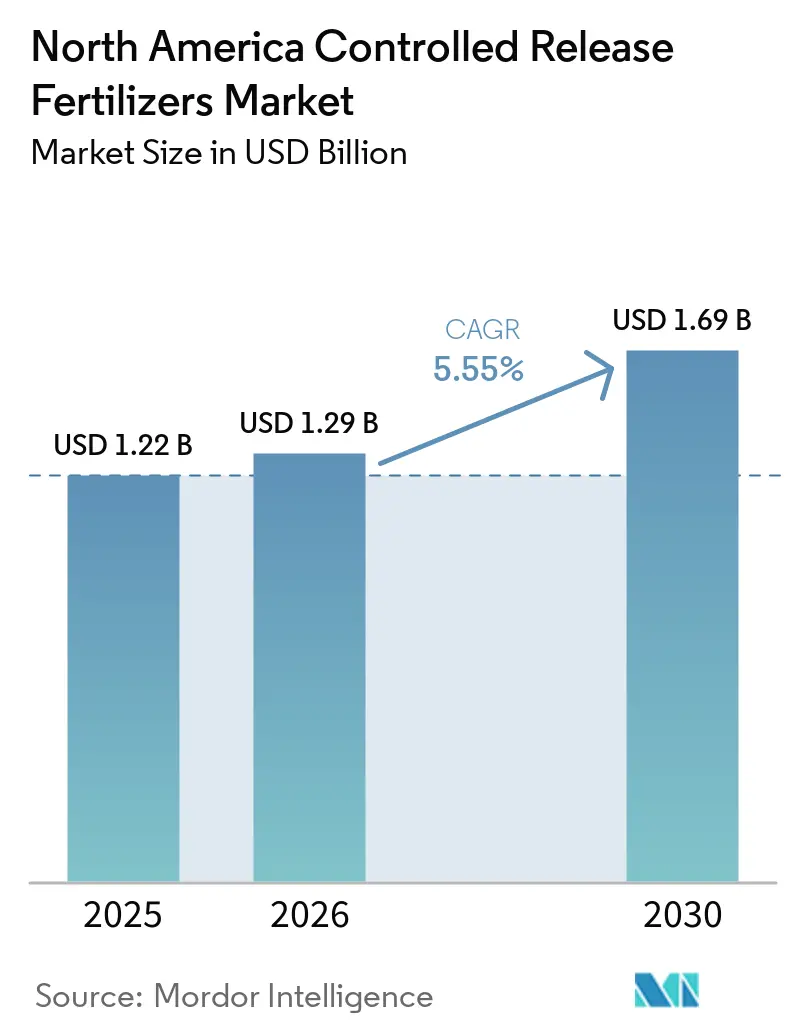

| Base Year Market Size (2025) | USD 1.22 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2030) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

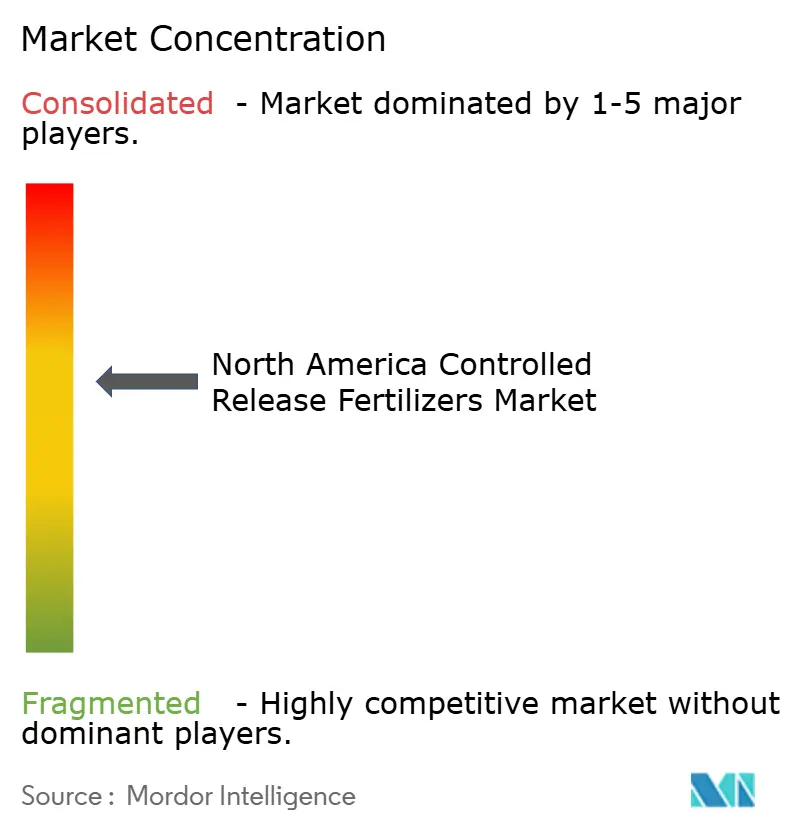

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Controlled Release Fertilizers Market Analysis by Mordor Intelligence

The North America controlled release fertilizers market size is projected to expand from USD 1.22 billion in 2025 and USD 1.29 billion in 2026 to USD 1.29 billion by 2031, registering a CAGR of 5.55% between 2026 and 2031. The North America controlled release fertilizer market is moving beyond niche use because growers now face tighter nutrient runoff rules, higher labor costs, and stronger sustainability checks from buyers and lenders. Precision application tools are making single-pass nutrition programs more practical, which improves the fit between controlled release fertilizer products and day-to-day crop management needs. At the same time, new domestic fertilizer capacity in the United States is improving upstream supply conditions, which should gradually reduce the cost pressure that has limited the broader adoption of the North America controlled release fertilizer market. Demand is also becoming more durable in intensive production systems where nutrient timing, labor efficiency, and leaching control matter as much as yield. Growth still faces some caution because polymer-coated products remain more expensive than conventional materials, and environmental scrutiny around polymer shells could reshape product development priorities over time.

Key Report Takeaways

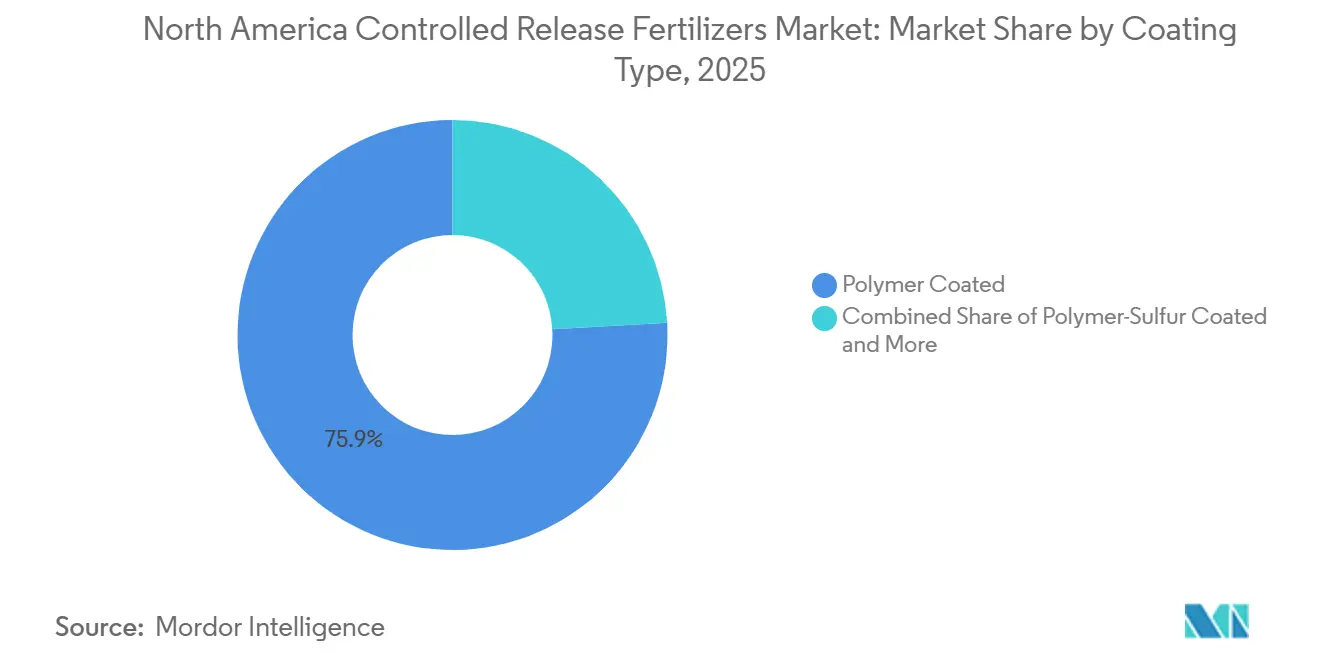

- By coating type, polymer-coated formulations accounted for 75.9% of the North America controlled release fertilizers market size in 2025 and were also the fastest-growing segment, projected to register a CAGR of 7.6% during 2026–2031.

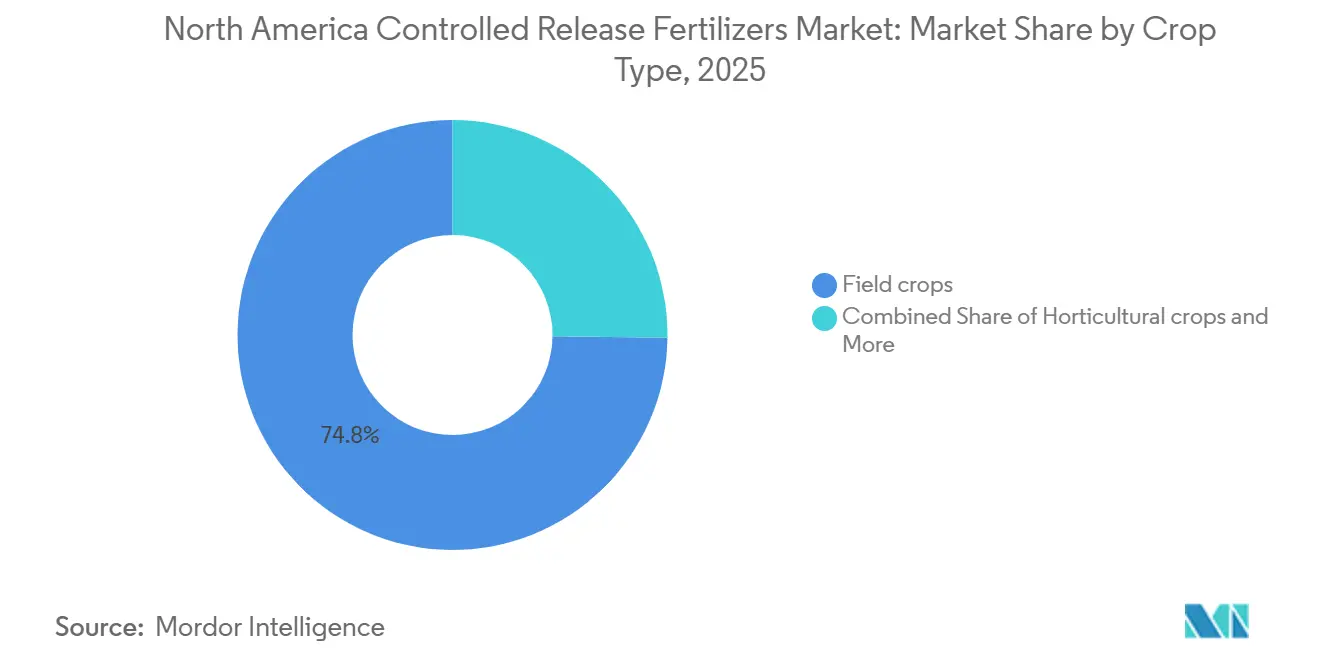

- By crop type, field crops held 74.8% of the North America controlled release fertilizers market share in 2025, while horticultural crops are projected to be the fastest-growing segment, registering a CAGR of 7.8% during 2026–2031.

- By geography, the United States accounted for the largest share of the North America controlled release fertilizers market, representing 70.5% in 2025, while Canada is projected to be the fastest-growing geography, registering a CAGR of 8.4% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Controlled Release Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision agriculture and fertigation adoption | +2.1% | United States and Canada, and Canadian Prairie provinces | Medium term (2-4 years) |

| Nutrient-runoff compliance pressure | +1.8% | Strongest in the Great Lakes Basin, and Gulf Coast states | Short term (≤ 2 years) |

| Field-crop nitrogen-use efficiency needs | +1.5% | United States Corn Belt states | Medium term (2-4 years) |

| Protected horticulture expansion | +1.2% | Canada, especially Ontario, and Texas | Medium term (2-4 years) |

| United States Department of Agriculture backed domestic capacity build | +0.8% | United States, with Canada border regions | Long term (≥ 4 years) |

| Biodegradable coating innovation | +0.9% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision Agriculture and Fertigation Adoption

The North America controlled release fertilizer market is growing due to the increased use of variable-rate technology and integrated nutrient management practices on commercial farms. In the United States, variable-rate technology is extensively applied to cropland, highlighting that many growers already operate within systems requiring precise nutrient placement. This approach reduces the number of fertilizer applications, thereby lowering field costs. Similarly, Canadian farms have adopted variable-rate input application and are already utilizing slow-release fertilizers, demonstrating a strong technical foundation for the wider adoption of controlled release fertilizers. A single application of controlled release fertilizer can align with zone-based nutrient prescriptions, reducing the need for multiple field passes. With ongoing labor shortages and high equipment ownership costs, the North America controlled release fertilizer market is supported by solutions that enhance operational efficiency while maintaining agronomic effectiveness.

Nutrient-Runoff Compliance Pressure

The North America controlled release fertilizer market is also supported by a more stringent regulatory framework for nutrient runoff and water quality. The United States Environmental Protection Agency has continued to support nutrient-reduction efforts in impaired watersheds. This includes a USD 3.7 million grant package announced for June 2025, aimed at organizations in Michigan and Ohio working within the Western Lake Erie Basin[1]Source: United States Environmental Protection Agency, “What Is Nutrient Pollution?,” United States Environmental Protection Agency, epa.gov. This type of basin-level support demonstrates how nutrient management is becoming an integral part of broader water-quality action plans, particularly in sensitive or impaired watersheds. Similar policy support exists in Canada, including Quebec programs that support the adoption of polymer-coated urea through sustainable agriculture initiatives. These regulatory and policy developments continue strengthening long-term demand for controlled release fertilizers across North America.

Field-Crop Nitrogen-Use Efficiency Needs

The North America controlled release fertilizers market is closely linked to the need for improved nitrogen-use efficiency in large-scale field crops. In 2025, corn-planted acreage in the United States reached 95.2 million acres, presenting significant demand potential even with moderate adoption of controlled release fertilizers. A 2025 study by the University of Florida Institute of Food and Agricultural Sciences found that a 100-acre snapbean trial reduced total nitrogen application by approximately 2,500 pounds (1,134 kg) while maintaining yields comparable to those under conventional fertilization methods[2]Source: Taite Miller, Robert Hochmuth, Rajkaranbir Singh, Lakesh Sharma, Tyler Pittman, and Mark Warren, “Use of Controlled-Release Nitrogen in Snapbean Production in the Suwannee Valley,” Ask IFAS, ask.ifas.ufl.edu. These findings emphasize the commercial value of controlled release fertilizers in North America for improving nutrient-use efficiency and reducing excessive fertilizer use. Combined with rising input costs and increasing sustainability pressures, these performance benefits continue to support demand growth in row-crop production systems.

Protected Horticulture Expansion

Protected cultivation systems are driving a stable demand for the North America controlled release fertilizer market, as greenhouse, nursery, and enclosed-production operators focus on nutrient precision, labor efficiency, and minimizing leaching risks. Controlled release fertilizers offer consistent nutrient-release patterns and reduce the need for frequent applications during extended crop cycles, making them particularly suitable for peat- and coco-based growing systems. Industry participants, such as Berger, noted in 2025 that commercial greenhouse operators are increasingly adopting controlled release fertilizers to enhance consistency in horticultural production systems. These benefits continue to support greater adoption across vegetables, fruits, nursery crops, and ornamental plants, where crop quality and substrate management are essential. As greenhouse and protected-cultivation systems expand in Canada and specific regions of the United States, the North America controlled release fertilizer market is anticipated to experience sustained demand in high-value, performance-oriented crop segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus conventional fertilizers | -1.5% | Great Plains and Canadian Prairies | Short term (≤ 2 years) |

| Dealer and grower application-learning gap | -0.8% | United States non-Corn Belt regions | Medium term (2-4 years) |

| Microplastic scrutiny of polymer shells | -0.7% | North America, with sustainability-led procurement channels | Long term (≥ 4 years) |

| Highly cyclical raw-material prices | -0.6% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Price Versus Conventional Fertilizers

The clearest commercial barrier in the North America controlled release fertilizer market remains the price premium of coated products over conventional nitrogen materials. That premium reflects both coating cost and the added manufacturing complexity needed to deliver more predictable nutrient release. For large grain farms, especially in lower-margin cropping systems, the decision often depends on whether the product can show a clear multi-season return rather than a one-season saving. A University of Florida Institute of Food and Agricultural Sciences study published in February 2025 identified high material costs as the main barrier to wider field-crop use, even though local cost-share programs can soften the burden in some cases. Until price gaps narrow further, the North America controlled release fertilizer market will continue to expand fastest where nutrient control, compliance, or labor savings are valuable enough to offset the initial cost difference.

Dealer And Grower Application-Learning Gap

The North America controlled release fertilizer market also faces a training issue because product performance depends on proper selection, placement, storage, and timing. Dealers and agronomists need to explain how release behavior changes with temperature, soil moisture, and coating thickness, which is more complex than selling standard granular fertilizer. This learning gap is uneven across the region, and it is most visible outside the best-developed row-crop distribution corridors, where field support is thinner. Research presented at the International Conference in 2025 on Precision Agriculture showed that precision agriculture penetration in Mexico remained low across several practical measures, including farm-level soil testing and the use of humidity sensors, indicating that the technical infrastructure for advanced nutrient products is still limited in many areas. Unless dealer education catches up with portfolio expansion, the North America controlled release fertilizer market will continue to leave some demand unrealized, even where the agronomic fit is strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Type: Polymer Encapsulation Anchors Market

Polymer-coated formulations accounted for the largest North America controlled release fertilizers market share by coating type, representing 75.9% of the market in 2025. That lead reflects broad acceptance across row crops, protected horticulture, and managed turf, where predictable release behavior is valued more than the lowest upfront input cost. The segment has also benefited from long commercial use in corn and turf systems, which has built confidence around application methods and crop response. Mature supply chains and compatibility with standard blending and spreading equipment have further strengthened adoption across the North America controlled release fertilizer industry. This installed base gives polymer-coated products a clear advantage over sulfur-based and niche coating alternatives when growers want consistency at a commercial scale.

Polymer-coated formulations are the fastest-growing coating type, with a CAGR of 7.6% projected from 2026 to 2031, demonstrating that this technology continues to gain traction rather than losing momentum. Pursell Agri-Tech and Wastech Group entered into a joint venture agreement in 2025 to establish a controlled release fertilizer polymer coating facility in Malaysia. The reported capital expenditure for the project exceeded RM80 million (approximately USD18 million). This facility is projected to serve Southeast Asian markets utilizing Pursell’s coating technology. Polymer-sulfur coated and sulfur coated products still matter in more cost-sensitive settings because they provide a lower-cost path into enhanced efficiency use. Other coated technologies remain relevant in specialty niches, but they do not yet challenge the scale or growth profile of the polymer coated core within the North America controlled release fertilizer market.

By Crop Type: Horticulture Accelerates as Field Crops Provide Volume Base

Field crops accounted for the largest North America controlled release fertilizers market size by crop type, representing 74.8% of the market in 2025. This position stems from the sheer scale of cereal and oilseed production in the region, especially in corn-heavy systems, where nitrogen management directly impacts profitability and compliance exposure. The United States corn planted area reached 95.2 million acres in 2025, underscoring why even modest controlled release fertilizer penetration in field crops can shift regional demand materially. Oilseeds, pulses, and cotton remain smaller users, but they create useful expansion pockets where nutrient access and application efficiency matter in variable soil conditions.

Horticultural crops are the fastest-growing crop type, with a 7.8% CAGR from 2026 to 2031, and this growth is tied to crop systems in which nutrient precision directly affects quality, labor use, and substrate condition. Greenhouse vegetables, fruits, nurseries, and ornamentals are especially receptive to long-season production because it benefits from fewer fertilizer interventions and steadier nutrient release. Berger described this operating logic in 2025, noting the value of controlled release fertilizers in peat-substrate and coco-based greenhouse systems, where consistent crop feeding and lower labor demand are important. Orchard and vineyard systems on the United States Pacific Coast also present a clear fit because single-application programs support perennial nutrition planning and water management discipline. The result is a North America-controlled release fertilizer market in which field crops supply the volume base, while horticulture keeps lifting the premium and growth profile.

Geography Analysis

The United States held 70.5% of the North America controlled release fertilizer market share in 2025. This made it the largest geographic contributor by a wide margin. This position was supported by its large corn acreage, a mature precision agriculture ecosystem, and an active nutrient runoff policy framework. Demand is concentrated across major Corn Belt states such as Iowa, Illinois, Indiana, Nebraska, and Ohio, where nitrogen-intensive production overlaps with watershed management pressures and strong agronomic service networks. In June 2025, the United States Environmental Protection Agency awarded USD 3.7 million to organizations in Michigan and Ohio to support nutrient-management improvements in the Western Lake Erie Basin. This reinforced the role of fertilizer efficiency in regional water-quality programs.

Canada is projected to be the fastest-growing geography with an 8.4% CAGR from 2026 to 2031. This growth is supported by greenhouse expansion, provincial nutrient-efficiency programs, and growing acceptance of reduced-frequency fertilizer programs. Quebec’s support for sustainable agriculture, including polymer-coated urea, helps lower adoption barriers for growers. Provincial technical guidance recognizes slow-release and high-efficiency fertilizers within 4R nutrient management approaches. These factors support demand for controlled release fertilizer in Canada, particularly in greenhouse, horticulture, and precision field-crop systems.

Mexico remains smaller in market value but offers selective opportunities in high-value horticulture, export-oriented farming, managed landscapes, and distributor-led agronomy programs. Adoption is narrower than in the United States and Canada because technical service coverage is uneven, and cost sensitivity remains higher across many farm segments. Precision agriculture research also indicates that Mexico’s digital and diagnostic infrastructure is less developed in several regions. This slows wider adoption outside specialized production clusters.

Competitive Landscape

The North America controlled release fertilizer market is moderately concentrated in 2025, with a small group of multinational manufacturers holding clear advantages in coating chemistry, upstream sourcing, and distribution scale. Nutrien Ltd., ICL Group Ltd., New Mountain Capital (Florikan), Grupa Azoty S.A. (Compo Expert), and Haifa Group all operate from strong product or channel positions. In March 2026, The J.R. Simplot Company has completed and inaugurated an upgraded fertilizer storage facility in Rupert, Idaho. This facility includes heated flooring systems and advanced dry and liquid storage infrastructure. It represents a multi-year investment aimed at modernizing controlled-release fertilizer distribution infrastructure in a significant agricultural region of the Pacific Northwest. The North America controlled release fertilizer market, therefore, rewards both scale and technical specialization. That balance keeps rivalry active without turning the field into a highly fragmented commodity landscape.

New entrants and smaller players can achieve success by targeting niche markets with specialized products. Companies should prioritize developing region-specific solutions tailored to local soil conditions and crop requirements. The increasingly stringent regulatory environment, particularly concerning environmental protection and fertilizer efficiency standards, underscores the importance of compliance capabilities as a key success factor. Establishing strong distribution partnerships and providing technical support services to farmers are becoming essential for market penetration and growth. Additionally, the adoption of smart release fertilizers and precision fertilizer technologies is anticipated to influence market dynamics by delivering customized solutions for specific agricultural needs.

Success in this market increasingly relies on companies' ability to create environmentally sustainable products while ensuring cost efficiency. Leading market players are concentrating on developing advanced coating technologies that enhance nutrient release control and offer environmental advantages. Additionally, companies are investing in digital platforms and precision agriculture solutions to expand their product portfolios and deliver integrated solutions to farmers. Establishing strong partnerships with agricultural research institutions and engaging in government sustainability initiatives has become essential for sustaining a competitive edge. Pursell Agri-Tech, LLC reinforced its technology-led approach in November 2025 through a joint venture with Wastech Group to build a new polymer coating facility in Malaysia, demonstrating that North America know-how can also be scaled through international licensing and manufacturing partnerships[3]Source: Pursell Agri-Tech, “Pursell Agri-Tech and Wastech Group Hold Signing Ceremony for Strategic Joint Venture,” Pursell Agri-Tech, fertilizer.com. Overall, the North America-controlled release fertilizer market is likely to see share shifts driven more by technical differentiation and service depth than by simple price competition alone.

North America Controlled Release Fertilizers Industry Leaders

Grupa Azoty S.A. (Compo Expert)

Haifa Group

ICL Group Ltd

New Mountain Capital (Florikan)

Nutrien Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The J.R. Simplot Company has completed and inaugurated an upgraded fertilizer storage facility in Rupert, Idaho. This facility includes heated flooring systems and advanced dry and liquid storage infrastructure. It represents a multi-year investment to modernize the controlled-release fertilizer distribution infrastructure in a significant agricultural region of the Pacific Northwest.

- November 2025: Pursell Agri-Tech and Wastech Group entered into a joint venture agreement in 2025 to establish a controlled release fertilizer polymer coating facility in Malaysia. The reported capital expenditure for the project exceeded RM80 million (approximately USD18 million). This facility is projected to serve Southeast Asian markets utilizing Pursell’s coating technology.

- May 2025: The University of Florida Institute of Food and Agricultural Sciences documented a commercial-scale controlled-release fertilizer trial on a 100-acre snapbean farm in Trenton, Florida, in which controlled-release fertilizer reduced total nitrogen input by 2,500 pounds (1,134 kg) compared with conventional fertilization, while achieving yields equivalent to 232 bushels per acre.

North America Controlled Release Fertilizers Market Report Scope

Controlled Release Fertilizers (CRFs) are granules coated with semi-permeable materials that gradually release nutrients in response to soil temperature. They match plant nutritional needs over an extended period to maximize growth while significantly reducing environmental leaching.

The North America Controlled Release Fertilizer Market Report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, Sulfur Coated, and Other Coated Technologies), Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and Geography (Canada, Mexico, United States, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Coating Type

| Polymer Coated | Polyurethane and resin-coated |

| Biodegradable polymer-coated | |

| Polymer-Sulfur Coated | |

| Sulfur Coated | |

| Other Coated Technologies |

Crop Type

| Field Crops | Cereals and Grains |

| Oilseeds and Pulses | |

| Cotton and Other Fiber Crops | |

| Horticultural Crops | Fruits |

| Vegetables | |

| Orchard and Vineyard Crops | |

| Turf and Ornamental | Golf and Sports Turf |

| Professional Landscaping | |

| Nursery and Greenhouse Ornamentals |

Geography

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Coating Type | Polymer Coated | Polyurethane and resin-coated |

| Biodegradable polymer-coated | ||

| Polymer-Sulfur Coated | ||

| Sulfur Coated | ||

| Other Coated Technologies | ||

| Crop Type | Field Crops | Cereals and Grains |

| Oilseeds and Pulses | ||

| Cotton and Other Fiber Crops | ||

| Horticultural Crops | Fruits | |

| Vegetables | ||

| Orchard and Vineyard Crops | ||

| Turf and Ornamental | Golf and Sports Turf | |

| Professional Landscaping | ||

| Nursery and Greenhouse Ornamentals | ||

| Geography | Canada | |

| Mexico | ||

| United States | ||

| Rest of North America | ||

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Urea & Complex

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms