Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

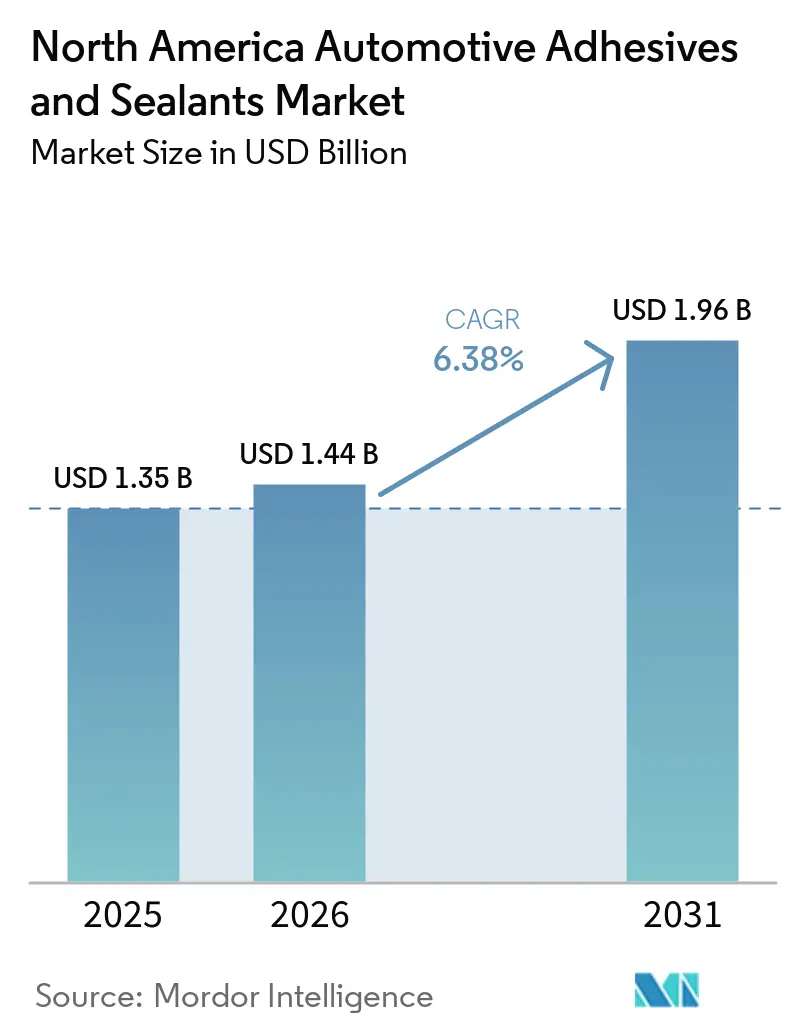

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 1.96 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Adhesives And Sealants Market Analysis by Mordor Intelligence

The North America Automotive Adhesives And Sealants Market size is expected to grow from USD 1.35 billion in 2025 to USD 1.44 billion in 2026 and is forecast to reach USD 1.96 billion by 2031 at 6.38% CAGR over 2026-2031. Demand acceleration reflects a significant shift toward electrified drivetrains, the reshoring of component production under the Inflation Reduction Act (IRA), and lightweighting strategies that replace spot-welds with structural bonds. Automakers are increasingly using crash-resistant epoxies for mixed-material body-in-white designs, while battery gigafactories require thermally conductive silicone gap fillers to manage heat across the planned 500 GWh of cell capacity by 2030. Tier-1 suppliers are localizing adhesive production to comply with the USMCA’s 75% regional value-content rule, boosting the procurement of polyurethane reactive hot-melts and water-borne dispersions that adhere to the U.S. Environmental Protection Agency’s tightened VOC limits. Feedstock volatility continues to pose challenges, with TDI spot prices rising 8.13% in March 2026 following outages in Europe and Asia. Formulators are addressing these issues by passing surcharges through quarterly pricing clauses and investing in bio-based alternatives that achieve up to 60% renewable content.

Key Report Takeaways

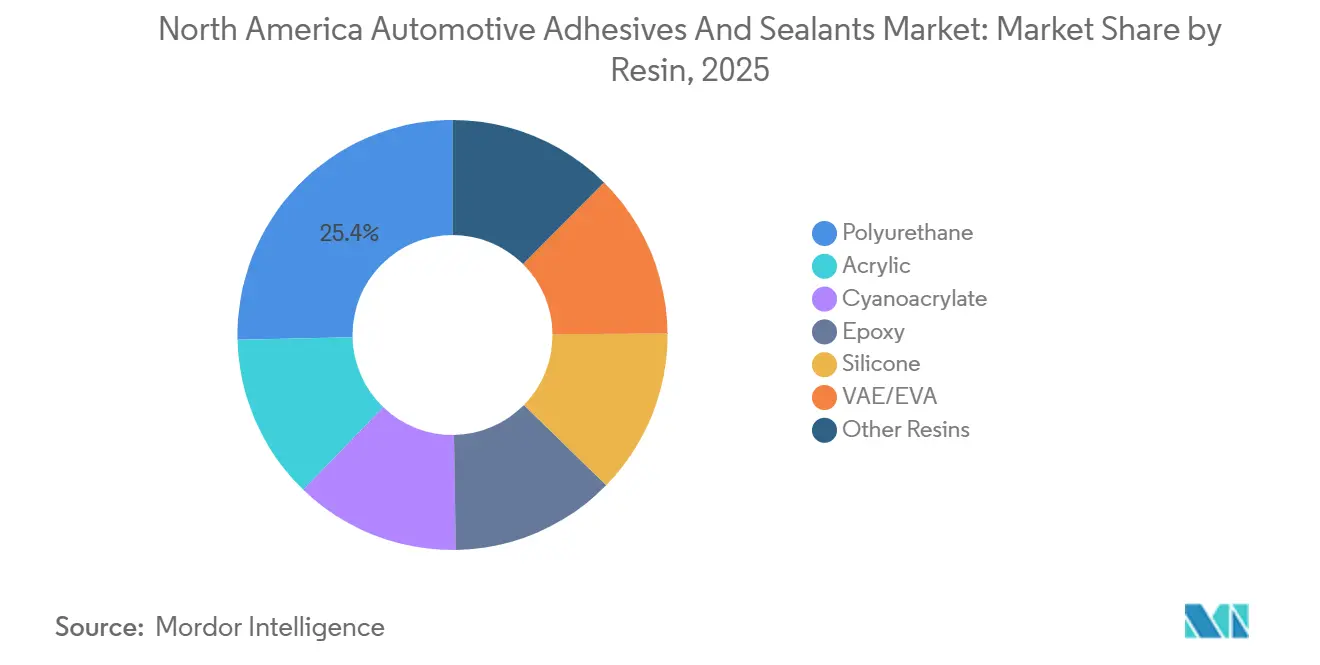

- By resin, polyurethane captured 25.35% of the North America automotive adhesives and sealants market share in 2025, while VAE/EVA resins are on track to record the fastest 6.45% CAGR through 2031.

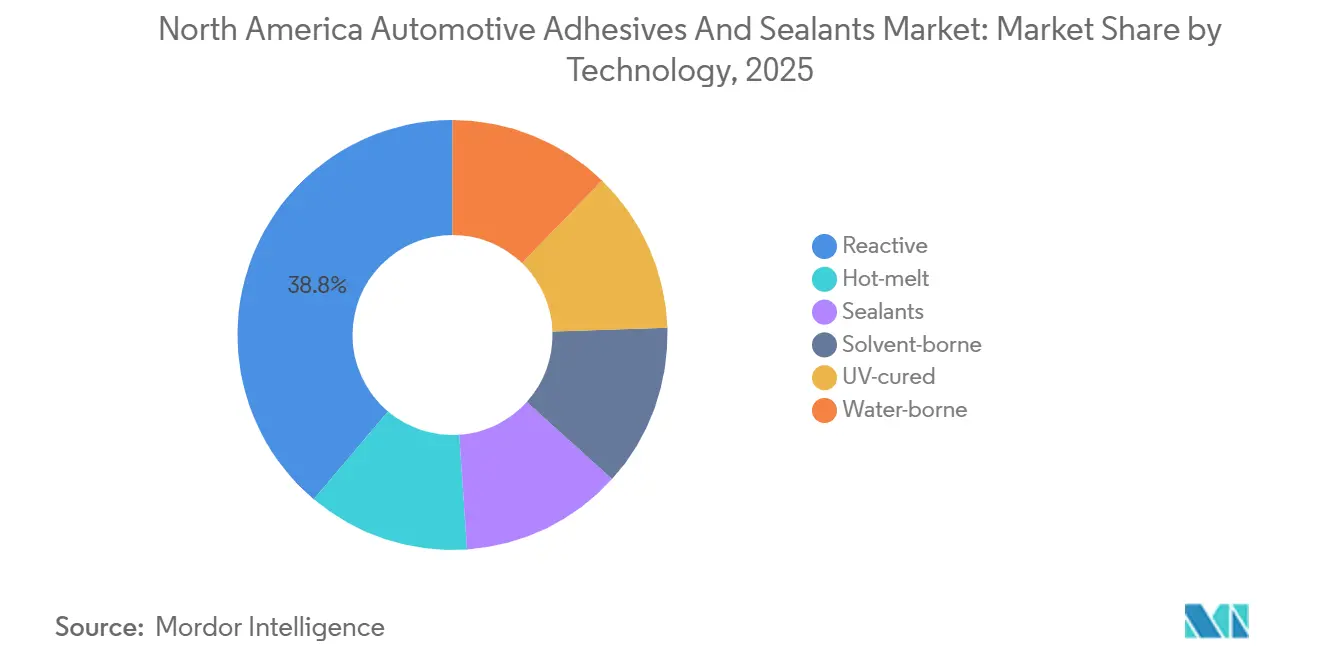

- By technology, reactive led with 38.84% of the North America automotive adhesives and sealants market share in 2025; water-borne is advancing at a 7.20% CAGR through 2031.

- By geography, the United States accounted for 65.34% of the North America automotive adhesives and sealants market share in 2025, whereas Mexico is projected to post the highest 9.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Automotive Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV-specific bonding requirements | +1.8% | United States, Canada, with spillover to Mexico | Medium term (2-4 years) |

| Lightweighting mandates across USMCA | +1.2% | North America (USMCA region-wide) | Long term (≥ 4 years) |

| OEM shift to mixed-material body-in-white | +1.5% | United States, Mexico assembly corridors | Medium term (2-4 years) |

| Rapid growth of battery gigafactories | +1.6% | United States (Kansas, Michigan, Tennessee), Canada (Ontario) | Short term (≤ 2 years) |

| Tier-1 adoption of smart curing lines | +0.9% | United States, Mexico Tier-1 clusters | Medium term (2-4 years) |

| IRA-driven reshoring of supply chains | +1.4% | United States, with secondary benefits to Canada and Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV-Specific Bonding Requirements

Gigafactory investments are redefining adhesive specifications. Panasonic Energy’s Kansas plant requires epoxies with thermal conductivity exceeding 2 W/m·K, while Volkswagen’s Ontario facility has approved silicone thermal interface materials that retain 80% bond strength after 3,000 thermal cycles. Dispensing robots at the Tesla–LG joint venture in Michigan utilize UV-cured chemistries that achieve a tack-free state in under 10 seconds, enabling automation-compatible products that reduce cycle times without compromising dielectric performance. Federal grants worth USD 100 million are supporting R&D into solid-state cell encapsulation, driving demand for flame-retardant adhesives that meet UL 94 V-0 flammability standards.

Lightweighting Mandates Across USMCA

USMCA content rules are accelerating the transition from steel to aluminum and carbon-fiber composites, which cannot be welded. Compliance rates for Mexican-origin vehicles reached 76.1% by July 2025, an increase of 8 percentage points over two years. Ford’s F-150 Lightning and GM’s Silverado EV rely on crash-resistant epoxies to bond aluminum extrusions to steel subframes, with associated surface-preparation primers now contributing an 8–12% increase in adhesive system costs.

OEM Shift to Mixed-Material Body-in-White

Multi-material structures require solutions for bonding dissimilar substrates. DuPont’s BETAMATE 2098 bonds aluminum to CFRP with tensile strength exceeding 30 MPa, while 3M’s impact-resistant acrylic absorbs 40% more energy in IIHS frontal tests compared to traditional epoxies. Adhesives must also accommodate differential thermal expansion; aluminum expands 23 µm/m °C compared to 1 µm/m °C for CFRP. To address this, suppliers are developing adhesives with elongations exceeding 200% to prevent delamination during 180 °C paint-bake cycles.

Rapid Growth of Battery Gigafactories

Stellantis–Samsung SDI’s USD 5.1 billion Indiana plant is expected to consume approximately 1,200 metric tons of thermally conductive materials annually, highlighting a significant increase in volume per site. GM’s Ultium Cells plant in Tennessee specifies silicone gap fillers with 3.5 W/m·K conductivity and thermal resistance below 0.05 °C cm²/W, raising performance standards for polymer matrices. Federal infrastructure funds have allocated 15% of USD 7 billion to adhesives that enable battery packs to meet stringent fire-safety regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material volatility for petro-resins | -1.1% | North America, with acute pressure in United States Gulf Coast clusters | Short term (≤ 2 years) |

| Limited high-temperature recyclability | -0.6% | United States, Canada (battery-recycling hubs) | Long term (≥ 4 years) |

| OSHA scrutiny on isocyanate exposure | -0.7% | United States, with spillover compliance in Canada and Mexico | Medium term (2-4 years) |

| Scale-up risk for bio-based chemistries | -0.4% | North America, concentrated in United States and Canada R&D centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Volatility for Petro-Resins

Unplanned outages at BASF and Wanhua caused TDI spot prices to rise by 8.13% in March 2026, while aniline, a key feedstock, increased by 18% in Q4 2024 due to gas price spikes and higher ocean freight costs. Acrylic monomer supply tightened by 12% in 2025 as Chinese producers reduced output to meet carbon-intensity targets, squeezing margins for North American compounders. While formulators implemented quarterly adjustment clauses, Tier-1 suppliers bound by annual contracts faced USD 40–60 million in margin erosion during 2025.

Limited High-Temperature Recyclability

Thermoset adhesives create challenges for end-of-life disassembly. The European Union’s regulation mandating 95% lithium recovery by 2030 is pressuring suppliers to develop debonding-on-demand chemistries[1]European Commission, “Proposed EU Battery Regulation,” eur-lex.europa.eu. Henkel’s Diels-Alder-based adhesive detaches at 180 °C but requires up to 60 minutes, which is too slow for facilities processing over 1,000 battery packs daily. Magnetically triggered systems from Fraunhofer IFAM release bonds in 15 seconds but add USD 2–3 per kg to costs and are incompatible with ferrous housings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Polyurethane Dominance Challenged by VAE/EVA in Low-Stress Applications

Polyurethane accounted for 25.35% of the 2025 demand in the North America automotive adhesives and sealants market due to its adaptability in structural bonding, NVH damping, and seam sealing. However, VAE/EVA resins are anticipated to grow at a 6.45% CAGR through 2031, as interior-trim manufacturers prioritize low-temperature activation, which reduces oven energy consumption by 30% and supports recycling efforts. Epoxy remains critical for crash-critical joints requiring tensile strength above 25 MPa, while silicone usage is increasing in battery thermal-management applications due to its stability across a temperature range of -40 °C to +150 °C. Acrylics, including cyanoacrylates, are gaining traction in niche rapid-assembly applications, such as sensor brackets, due to their sub-60-second fixture-free curing times. Additionally, "other resins," such as polyimides, command premium margins in thermal-barrier applications.

The growth of VAE/EVA aligns with OEM commitments to increase recycled content, while Henkel’s 60% bio-based polyurethane demonstrates how polyurethanes can meet sustainability goals without compromising lap-shear strength below 5 MPa. Epoxy suppliers are developing toughened grades to address differential expansion in mixed-material joints, and silicone formulators are enhancing dielectric strength beyond 20 kV/mm to meet the requirements of high-voltage battery designs. Cyanoacrylate developers are integrating UV and moisture curing for shadowed areas, expanding their use in automated ADAS module production lines. Overall, resin selection is shifting toward chemistries that balance mechanical performance with reduced energy consumption and improved end-of-life recyclability, reflecting the ongoing transition in the North America automotive adhesives and sealants market.

By Technology: Reactive Technology Lead, Water-Borne Technology Accelerate on VOC Compliance

Reactive technology accounted for 38.84% of the 2025 revenue in the North America automotive adhesives and sealants market, with two-part epoxies and moisture-cure polyurethanes maintaining their dominance due to superior bond strength. Water-borne technology is anticipated to grow at a 7.20% CAGR through 2031, as OEMs aim for LEED certification and seek products with VOC emissions below 50 g/L, significantly lower than the EPA’s 275 g/L limit. Stahl’s RelcaDur platform, launched in 2025, exemplifies this trend by achieving 15 MPa lap-shear strength on steel while reducing VOC emissions by 85%.

Hot-melt adhesives retain their share in polypropylene-rich interiors, where 15-second open times are sufficient. Sealants are experiencing growth due to the increasing number of sensors, windshields, and battery-tray gaskets in EV designs. Solvent-borne adhesives are in structural decline but remain relevant in aftermarket repairs, where fast tack and broad substrate compatibility outweigh environmental concerns. UV-cured adhesives are gaining traction in camera module applications, where 3-second cure times significantly improve production efficiency, creating a premium segment within the North America automotive adhesives and sealants market.

Geography Analysis

The United States generated 65.34% of the 2025 demand, supported by legacy Detroit capacity and increased EV investments in Kansas, Tennessee, and Michigan. January 2026 motor-vehicle shipments reached USD 68.222 billion, highlighting robust output despite inventory adjustments[2]U.S. Census Bureau, “Manufacturers’ Shipments, Inventories, and Orders,” census.gov. IRA Section 45X credits are encouraging supplier co-location, with H.B. Fuller’s Kentucky plant and Sika’s New Jersey expansion adding a combined 20,000 metric tons of annual capacity for structural acrylics and polyurethane hot-melts targeting EV programs. Panasonic Energy’s Kansas gigafactory consumes 800–1,000 metric tons of adhesives annually, focusing on silicone materials that maintain thermal pathways in large-format cylindrical cells.

Canada faces short-term challenges as Honda, Stellantis, and GM streamline assembly operations. However, Volkswagen’s USD 7 billion PowerCo facility in Ontario, scheduled for 2027, is expected to anchor local adhesive supply chains. Federal Zero-Emission Vehicle mandates, requiring 60% EV sales by 2030, are likely to drive demand for gap fillers and structural epoxies as new models enter production.

Mexico is the fastest-growing node, with a projected CAGR of 9.33% through 2031, as nearshoring boosts auto-parts production to USD 113.199 billion and captures 43.18% of U.S. component imports. Tesla’s Nuevo León assembly hub and BMW’s San Luis Potosí plant are localizing adhesive dispensing lines to meet USMCA labor-value thresholds, driving demand for reactive epoxies that perform reliably in high-humidity environments. The 2026 USMCA review is expected to tighten melted-and-poured rules for metals, further promoting adhesive-intensive multi-material designs and supporting market growth in Mexico.

Competitive Landscape

Market concentration is moderate. Major players include Henkel, Sika, H.B. Fuller, 3M, and Dow. Key strategies include proximity to gigafactories and R&D investments in smart-cure chemistries compatible with Industry 4.0 production lines. Henkel’s BONDERITE LineguardX has reduced scrap by up to 22% at Magna and Gestamp plants through closed-loop bead-width control. Sika has expanded its New Jersey facility by 12,000 metric tons to produce aluminum-CFRP acrylics, while H.B. Fuller’s Kentucky site supplies polyurethane reactive hot-melts to Ford’s BlueOval SK complex.

Innovation is focused on thermally reversible bonds for battery disassembly, with Michelin’s BioImpulse targeting 80% bio-content by 2028. Smaller players like Permabond and Dymax are carving out niches in dual-cure cyanoacrylates and UV-cured systems for ADAS modules. Technology adoption and proximity to EV production hubs remain critical factors for securing long-term sourcing agreements in the North America automotive adhesives and sealants market.

North America Automotive Adhesives And Sealants Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: TruArc Partners, a private equity firm specializing in middle-market investments in business services and specialty manufacturing, acquired Matrix Adhesives Group, a North American provider of adhesive and sealant solutions. Matrix Adhesives Group supplied advanced adhesive and sealant solutions, offering a diverse range of products for the automotive industry.

- December 2025: Henkel AG & Co. KGaA introduced Loctite MS 9650, a silane-modified polymer (SMP) adhesive and sealant specifically developed for the automotive industry. It was designed for durable structural bonding in automotive display components and lightweight vehicle assemblies, compatible with various materials, including glass, metal, painted surfaces, and plastics.

North America Automotive Adhesives And Sealants Market Report Scope

Automotive adhesives and sealants play a vital role in contemporary vehicle manufacturing and repair. They are used to bond materials such as metal, plastic, and glass, while also ensuring weatherproofing and structural integrity. By substituting traditional mechanical fasteners, these materials facilitate lightweighting, potentially reducing vehicle weight by up to 25% and enhancing fuel efficiency.

The North America Automotive Adhesives And Sealants Market is segmented into resin, technology, and geography. By resin, the market is segmented into polyurethane, acrylic, cyanoacrylate, epoxy, silicone, VAE/EVA, and other resins. By technology, the market is segmented into reactive, hot-melt, sealants, solvent-borne, UV-cured, and water-borne. The report also covers the market size and forecasts for automotive adhesives and sealants in 3 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin

| Polyurethane |

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Reactive |

| Hot-melt |

| Sealants |

| Solvent-borne |

| UV-cured |

| Water-borne |

By Geography

| United States |

| Canada |

| Mexico |

| By Resin | Polyurethane |

| Acrylic | |

| Cyanoacrylate | |

| Epoxy | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Reactive |

| Hot-melt | |

| Sealants | |

| Solvent-borne | |

| UV-cured | |

| Water-borne | |

| By Geography | United States |

| Canada | |

| Mexico |

Market Definition

- End-user Industry - In the automotive industry, both the OEM and after market adhesive and sealants applications are considered under the scope.

- Product - All adhesive and sealant products used in automotive industry are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, UV Cured Adhesives, and Sealants technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms