Automated Case Erectors And Sealers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

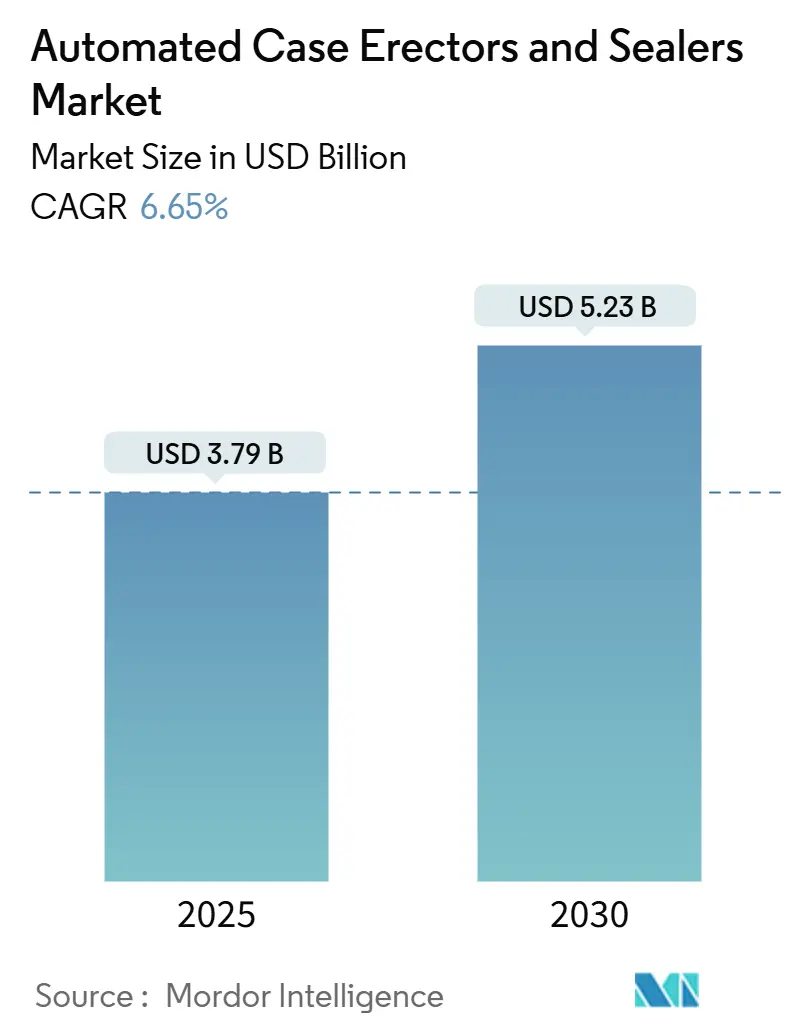

| Market Size (2025) | USD 3.79 Billion |

| Market Size (2030) | USD 5.23 Billion |

| Growth Rate (2025 - 2030) | 6.65% CAGR |

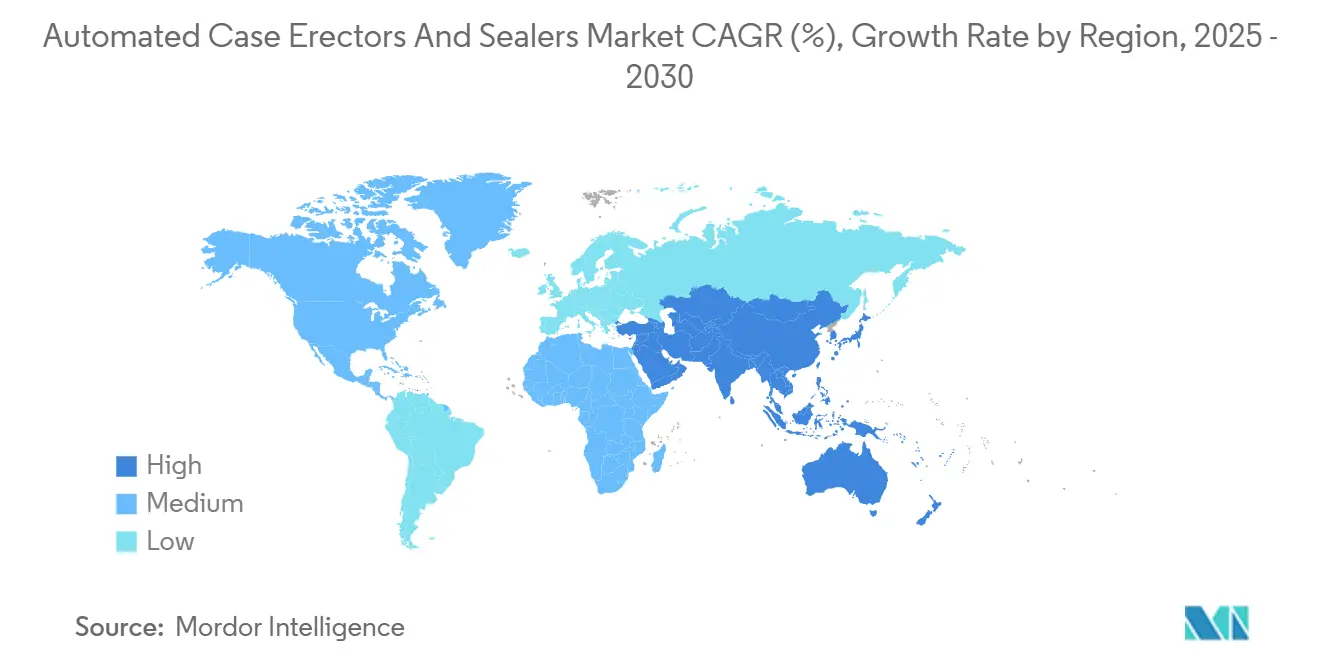

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Case Erectors And Sealers Market Analysis by Mordor Intelligence

The automated case erectors and sealers market size is valued at USD 3.79 billion in 2025 and is projected to reach USD 5.23 billion by 2030, delivering a 6.65% CAGR. Widespread labor shortages, rising e-commerce volumes, and stricter food and pharmaceutical regulations keep automation at the top of plant-level investment lists. Manufacturers increasingly favor equipment with Industry 4.0 connectivity that allows real-time performance tracking and predictive maintenance, while energy-efficient drives support decarbonization targets. Systems capable of quick changeovers gain traction as fulfillment centers handle mixed product portfolios, and financing packages designed for mid-market companies dilute capital-expenditure barriers. Competitive intensity grows as suppliers combine mechanical expertise with software, vision, and data-analytics capabilities to protect margins in a moderately fragmented field.

Key Report Takeaways

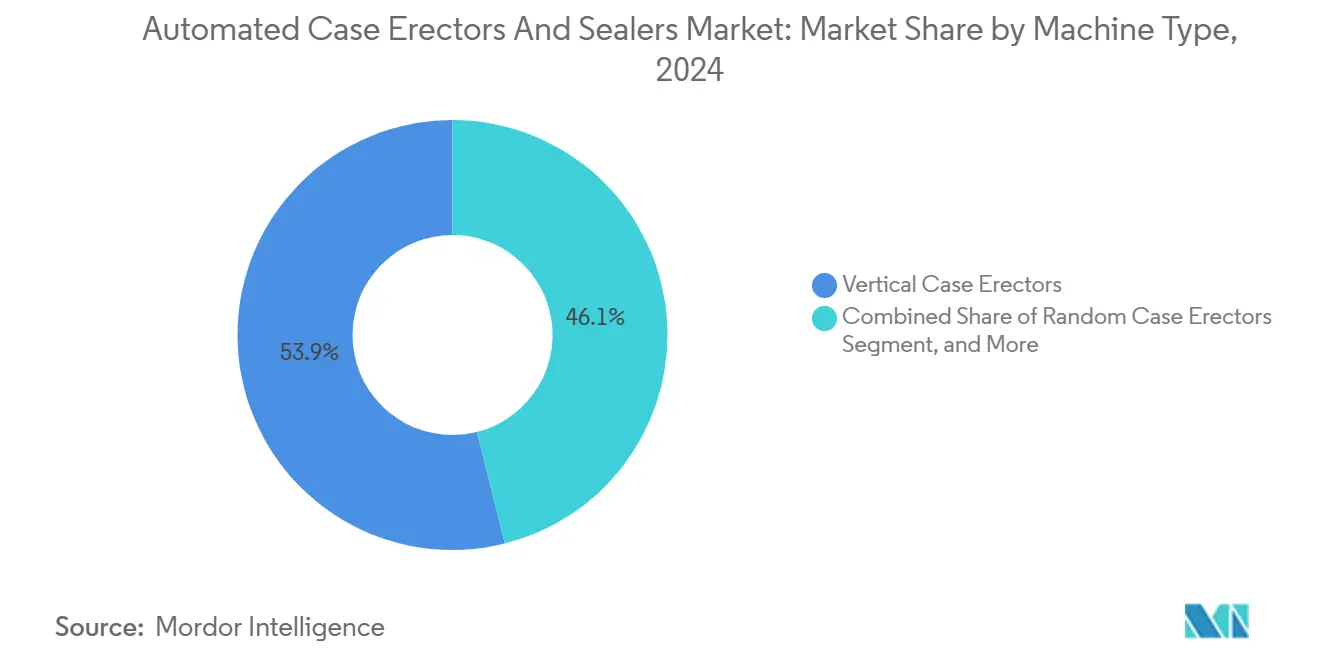

- By machine type, vertical case erectors captured 53.91% of the automated case erectors and sealers market share in 2024.

- By automation level, the automated case erectors and sealers market size for semi-automatic systems is projected to grow at a 7.28% CAGR between 2025-2030.

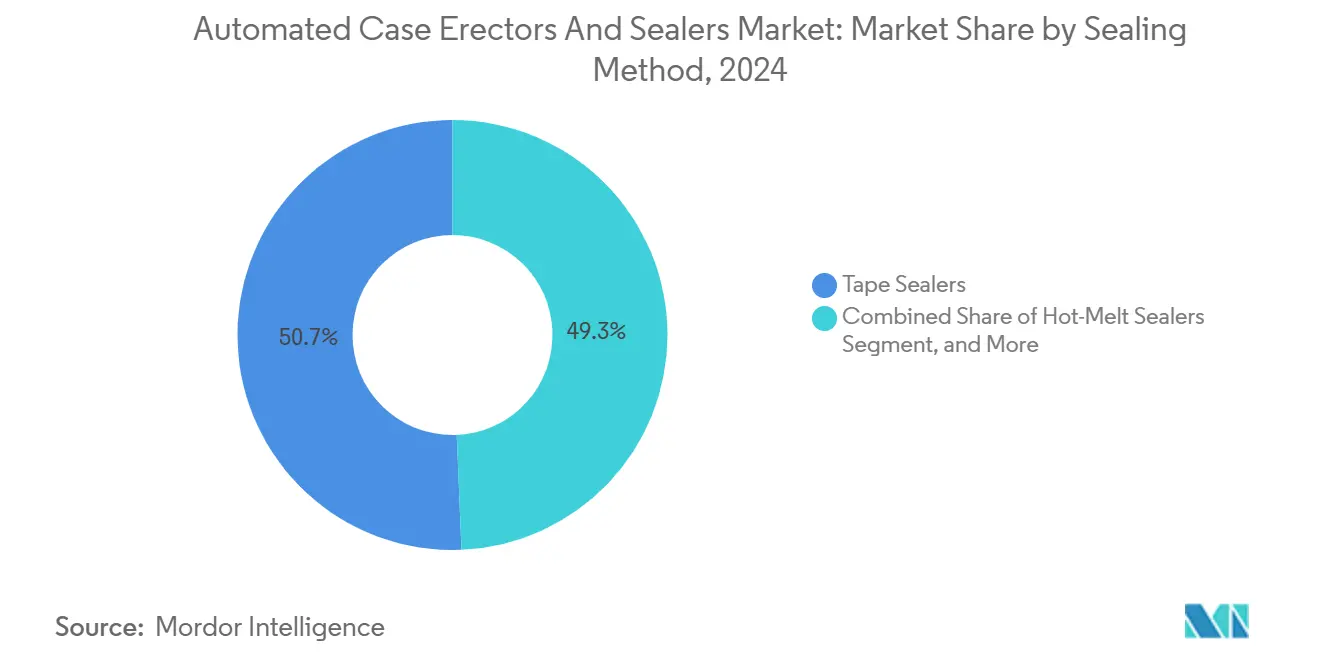

- By sealing type, tape sealing systems captured 50.67% of the automated case erectors and sealers market share in 2024.

- By end-user, the automated case erectors and sealers market size for pharmaceutical applications is projected to grow at an 8.56% CAGR between 2025-2030.

- By geography, North America captured 37.21% of the automated case erectors and sealers market share in 2024.

Global Automated Case Erectors And Sealers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent labor shortages in packaging plants | +1.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Surge in e-commerce parcel volumes | +0.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Food and pharma safety regulations mandating automated end-of-line | +1.1% | Global, stricter in developed markets | Long term (≥ 4 years) |

| Adoption of Industry 4.0 for OEE and predictive maintenance | +0.9% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Retailer mandates for shelf-ready cases with zero glue squeeze-out | +0.7% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| ROI-driven shift to centralized vacuum / low-energy drives | +0.6% | Global, early adopters in energy-conscious regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Labor Shortages Drive Packaging Automation Investment

Packaging departments continue to wrestle with unfilled operator positions, forcing management to automate end-of-line tasks to secure output levels.[1]Bureau of Labor Statistics, “Occupational Employment and Wage Statistics – Packaging and Filling Machine Operators and Tenders,” bls.gov Vacancy rates stay stubbornly high as experienced workers retire and younger talent favors service roles. Automated case erectors and sealers market users cite predictable throughput and lower overtime expenses as key payback variables. Plants in the United States, Germany, and Canada accelerate funding approvals when overtime exceeds budget ceilings. Vendors respond with user-friendly HMIs and remote diagnostics that minimize specialized staffing requirements, further reinforcing the transition toward intelligent equipment.

E-commerce Surge Reshapes Case Handling Requirements

Online retail leaders continue to post double-digit parcel growth, increasing the mix of box sizes in every shift.[2]Amazon.com Inc., “Form 10-K Annual Report 2024,” sec.gov Fulfillment centers install random case erectors that read barcodes or vision cues to auto-adjust in seconds, a feature impractical for manual processes. Seasonal peaks magnify the need for rapid scale-up without proportional labor additions. Semi-automatic machines with quick-swap magazines become popular in mid-volume hubs, allowing one operator to supervise multiple lines. Consequently, the automated case erectors and sealers market records a sustained uptick in orders tied directly to holiday volume forecasts.

Regulatory Mandates Accelerate Automated End-of-Line Adoption

Tighter contamination-control guidance from the FDA and similar agencies positions automation as the default compliance route. Case erectors integrate in-line code verification and seal-integrity sensors, while sealers log critical parameters for audit trails. Pharmaceutical producers embrace fully enclosed hot-melt systems to prevent particulate ingress, and premium food brands replicate pharma-grade packaging to reassure consumers. Regulations transform automation from discretionary spending into a prerequisite for market access, anchoring long-term demand in the automated case erectors and sealers market.

Industry 4.0 Integration Transforms Packaging Operations

Roughly one-third of new installations arrive Industry 4.0-ready, streaming machine data to MES and cloud dashboards. Predictive algorithms alert maintenance crews to component fatigue, cutting unplanned downtime and raising OEE scores. The data layer facilitates cross-line synchronization, enabling the collective optimization of cycle times for erecting, filling, and sealing units. Energy dashboards compare drive consumption across shifts, helping plants fund low-energy vacuum pumps and servo upgrades. These digital gains strengthen the business case for automation well beyond reduced headcount.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for SMEs | -0.9% | Global, acute in developing markets | Short term (≤ 2 years) |

| Integration complexity with legacy lines | -0.7% | North America and Europe with established infrastructure | Medium term (2-4 years) |

| Corrugated board supply volatility post-2025 EU carbon border tax | -0.4% | Europe core, indirect global impact | Short term (≤ 2 years) |

| Cyber-security compliance costs for connected machinery | -0.3% | Global, stricter in regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Barriers Constrain SME Adoption

Entry-level systems cost between USD 150,000 and USD 300,000, a commitment many smaller plants defer until financing aligns.[3]Equipment Leasing and Finance Association, “2024 Survey of Equipment Finance Activity,” elfaonline.org Leasing and as-a-service models are emerging but often cover only hardware, leaving buyers to absorb integration, training, and maintenance. In Latin America and Southeast Asia, currency fluctuations raise effective USD pricing, pushing payback periods beyond acceptable thresholds. As a result, semi-automatic solutions represent a bridge for mid-tier firms that cannot yet justify fully automatic equipment in the automated case erectors and sealers market.

Legacy System Integration Creates Technical Complexity

Facilities running mixed-vintage conveyors and proprietary PLCs face unexpected retrofits when adding modern erectors and sealers. Control engineers must map disparate protocols or install middleware, delaying line-start dates. Physical footprints also clash; older lines often lack the straight conveyor runs new machines require for optimal blank feeding. These hurdles inflate project budgets and can erode internal support for multi-phase automation roadmaps, dampening the speed of adoption for the automated case erectors and sealers industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Vertical Systems Dominate While Random Erectors Accelerate

Vertical units accounted for 53.91% of global revenue in 2024, thanks to their high-speed, high-repeatability design, which is tailored to uniform product flows. The automated case erectors and sealers market size for vertical machines supports stable investments in food and beverage plants that batch similar SKUs for extended runs. Random units, growing at 8.74% CAGR, answer e-commerce demand for dimensional agility. As fulfillment algorithms dynamically select box sizes, random erectors shave downtime by eliminating manual adjustments, enlarging their addressable base.

The segment faces incremental competition from horizontal units designed for tight footprints and frequent brand changeovers. Demonstrations in 2024 recorded 30% quicker changeovers compared to legacy vertical models, allowing brand owners to refresh promotions without lengthy shutdowns. Uniform erectors remain crucial in the pharmaceutical industry, where validated case geometry ensures regulatory compliance. Together, these trends keep the automated case erectors and sealers market engaged in a continuous cycle of speed, flexibility, and validation upgrades.

By Automation Level: Full Automation Leads Despite Semi-Automatic Growth

Fully automatic lines owned 62.15% share in 2024, reflecting mature adoption among multinational producers focused on 24-hour throughput. Plants justify higher capital spend through lower labor fractions and integration with downstream robots. However, semi-automatic machines are leading the automated case erectors and sealers market with a 7.28% CAGR. They allow operators to toggle between manual feed and automatic discharge, ideal for variable-run plants, thereby balancing labor availability with output goals.

Procurement managers carefully weigh utilization rates; sections with seasonal peaks often combine semi-automatic units with labor redeployment plans. Surveys conducted in 2024 revealed that 43% of buyers primarily selected semi-automatic machines for hybrid labor-automation models. As financing solutions improve, a portion of this installed base may upgrade to fully automatic units, supporting long-term expansion for the automated case erectors and sealers industry.

By Sealing Method: Tape Systems Lead While Hot-Melt Gains Traction

Tape sealers captured 50.67% of the revenue in 2024, thanks to their broad material compatibility and economical consumable pricing. They fit both corrugated varieties and recycled substrates, giving procurement teams contract flexibility. Hot-melt units, growing at a 7.61% CAGR, meet stringent integrity demands in the pharma cold chain and premium food exports. Producers cite superior peel strength and tamper-evident features as reasons to pay the adhesive premium, especially when single-digit reject reductions offset the costs of consumables.

Hybrid systems that deploy both tape and hot-melt in sequence emerged in 2024 trials, achieving 99.8% integrity compared to 97.2% for single-method options. Equipment makers now position hybrids for high-value SKUs with long transit cycles. As substrates and coatings evolve, the choice of sealing technology will remain a crucial specification variable in the automated case erectors and sealers market.

By End-Use Industry: Food Dominates While Pharmaceutical Accelerates

Food and beverage held a 40.76% share in 2024 on the back of standardized box sizes and long production runs that justify full automation. The sector continues to prioritize wash-down-ready stainless steel frames and IP65-rated electronics that can withstand bottle rinses and sugar dust. Pharmaceutical lines post the highest 8.56% CAGR thanks to serialization mandates and sterility protocols that virtually preclude manual packing. Audit-ready data logs embedded in case erectors simplify validation, transforming equipment selection into a compliance-driven process.

Outside these two, consumer goods and industrial components adopt flexible automation to manage SKU proliferation. Logistics hubs position automated erectors near pick zones, reducing conveyor travel and packing labor. Collectively, these multiple demand nodes reinforce the robust outlook for the automated case erectors and sealers market.

Geography Analysis

North America retained 37.21% revenue share in 2024, underpinned by extensive installed manufacturing capacity and access to skilled automation integrators. Surveyed plants indicate that 42% plan to upgrade end-of-line equipment within two years, thereby sustaining near-term demand. Mexico’s newly opened assembly sites integrate Industry 4.0-ready erectors at inception, aligning with USMCA clauses on advanced manufacturing know-how. Canada leverages automation to address labor gaps in meat processing and sterile drug packaging, further anchoring regional demand.

The Asia-Pacific region delivers the fastest growth, with a 7.89% CAGR, as labor cost arbitrage narrows and governments subsidize smart-factory conversions. China’s 14th Five-Year Plan lists intelligent packaging among priority equipment classes, unlocking provincial grants for local buyers. Japanese OEMs are pioneering integrated vision modules that differentiate their domestic offerings, while Southeast Asian nations are attracting contract manufacturing that expects the same level of automation density seen in Western facilities. Regional suppliers expand service footprints to support first-time buyers, cementing penetration gains in the automated case erectors and sealers market.

Europe is growing steadily on the strength of environmental regulations and energy-efficiency targets embedded in the Green Deal. German plants lead retrofit activity, replacing pneumatic actuation with servo drives to cut compressed-air demand. Nordic food processors specify equipment with life-cycle energy ratings, dovetailing with regional decarbonization pacts. United Kingdom firms hedge post-Brexit customs risks by automating to offset tariff-related cost pressures. Interconnected market forces continue to drive capital toward advanced end-of-line systems.

Competitive Landscape

The automated case erectors and sealers market exhibits moderate fragmentation, with suppliers clustering into three capability bands: full-line integrators, niche machine specialists, and software-focused entrants. Market leaders amplify differentiation through patented adaptive algorithms that automatically tune blank pickup or seal-ram velocity to carton weight changes. Strategic acquisitions accelerate portfolio breadth, exemplified by ITW Hartness's acquisition of a European automation firm to enter servo-driven random erecting niches.

Technology integration sits at the epicenter of competition. Vendors embed AI modules that predict adhesive-nozzle fouling before output falters, and they pair them with cloud dashboards for multi-site benchmarking. Energy-efficient drives become table stakes as plants report electricity as their second-largest utility line item. Service models also evolve; providers now bundle uptime guarantees and operator-skill assessments into multiyear contracts, fostering lock-in.

Regional expansion strategies intensify. U.S. manufacturers open assembly plants in Mexico to achieve tariff neutrality, while European brands license technology to Asian partners to comply with local content requirements. Mid-size disruptors adopt modular architectures allowing bolt-on functions from vision inspection to pallet labeling, chasing mid-tier buyers seeking phased automation. These dynamics collectively shape a competitive field where hardware prowess and software sophistication carry equal weight.

Automated Case Erectors And Sealers Industry Leaders

A B-C Packaging Machine Corporation

AFA Systems Inc.

Berran Industrial Group, Inc.

BestPack Packaging Systems

BluePrint Automation (BPA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Lantech announced USD 25 million investment in energy-efficient hot-melt sealing R&D for pharma applications.

- August 2024: ITW Hartness acquired a European packaging automation specialist for USD 180 million, expanding geographic reach and servo technology depth.

- July 2024: Premier Tech launched a fully automatic erector series featuring AI-driven predictive maintenance and throughput optimization.

- June 2024: Combi Packaging Systems received FDA approval for a sterility-focused case sealer with real-time monitoring.

Global Automated Case Erectors And Sealers Market Report Scope

| Uniform Case Erectors |

| Random Case Erectors |

| Vertical Case Erectors |

| Horizontal Case Erectors |

| Fully Automatic |

| Semi-Automatic |

| Tape Sealers |

| Hot-Melt Sealers |

| Hybrid / Combination Sealers |

| Food and Beverage |

| Pharmaceutical |

| Consumer Goods |

| E-commerce and Logistics |

| Industrial Manufacturing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Uniform Case Erectors | ||

| Random Case Erectors | |||

| Vertical Case Erectors | |||

| Horizontal Case Erectors | |||

| By Automation Level | Fully Automatic | ||

| Semi-Automatic | |||

| By Sealing Method | Tape Sealers | ||

| Hot-Melt Sealers | |||

| Hybrid / Combination Sealers | |||

| By End-use Industry | Food and Beverage | ||

| Pharmaceutical | |||

| Consumer Goods | |||

| E-commerce and Logistics | |||

| Industrial Manufacturing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the automated case erectors and sealers market in 2025?

The market stands at USD 3.79 billion in 2025 and is projected to reach USD 5.23 billion by 2030, reflecting a 6.65% CAGR.

Which machine type contributes most to revenue?

Vertical case erectors lead with 53.91% of 2024 global revenue due to their reliability in high-volume production.

What is the fastest-growing geographic region?

Asia-Pacific posts the highest regional CAGR at 7.89% through 2030 on the back of rising labor costs and smart-factory incentives.

Why are hot-melt sealers gaining traction?

Hot-melt systems deliver stronger, tamper-evident seals required in pharmaceutical and premium food applications, driving a 7.61% CAGR.

What restrains adoption among small and medium manufacturers?

Capital expenditure remains the primary barrier, with entry-level systems costing USD 150,000-300,000 and limited financing flexibility.

Page last updated on: