Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

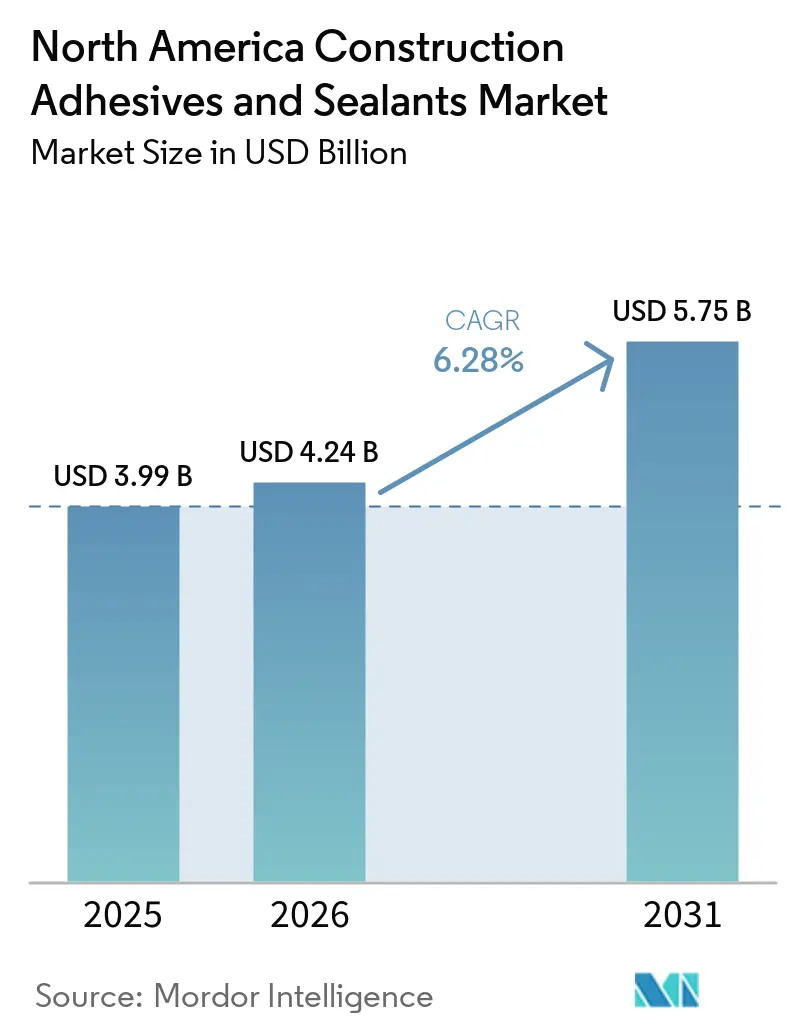

| Base Year Market Size (2025) | USD 3.99 Billion |

| Market Size (2026) | USD 4.24 Billion |

| Market Size (2031) | USD 5.75 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Construction Adhesives And Sealants Market Analysis by Mordor Intelligence

The North America Construction Adhesives And Sealants Market size is expected to increase from USD 3.99 billion in 2025 to USD 4.24 billion in 2026 and reach USD 5.75 billion by 2031, growing at a CAGR of 6.28% over 2026-2031. Rising federal infrastructure outlays, the rapid adoption of modular building methods, and state-level low-VOC regulations are transforming product demand patterns. Contractors are increasingly specifying factory-ready adhesives that cure quickly and bond mixed substrates, while building owners prioritize long-term weather resistance and lower indoor air emissions. Challenges such as raw material price volatility and labor shortages persist, but suppliers with vertically integrated feedstocks and streamlined application systems are gaining market share. Competitive intensity remains high, as no single vendor accounts for more than one-quarter of regional revenue, creating opportunities for specialists focusing on data centers, mass-timber buildings, and bridge rehabilitation.

Key Report Takeaways

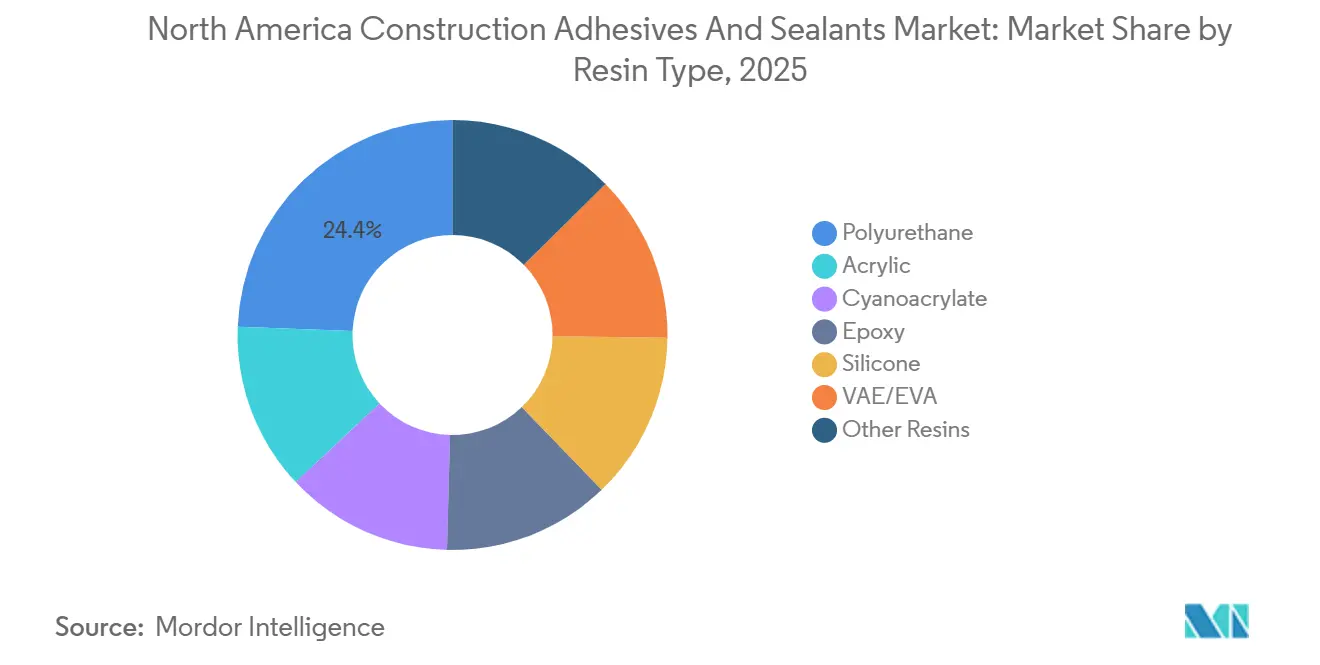

- By resin type, polyurethane captured 24.38% of the North America construction adhesives and sealants market share in 2025, while silicone posted the fastest 6.43% CAGR through 2031.

- By technology, sealants accounted for 42.01% of the North America construction adhesives and sealants market share in 2025; water-borne technology is growing at a 6.43% CAGR through 2031.

- By application, flooring and tiling held 39.83% of the North America construction adhesives and sealants market share in 2025, while infrastructure joints are projected to expand at a 7.18% CAGR through 2031.

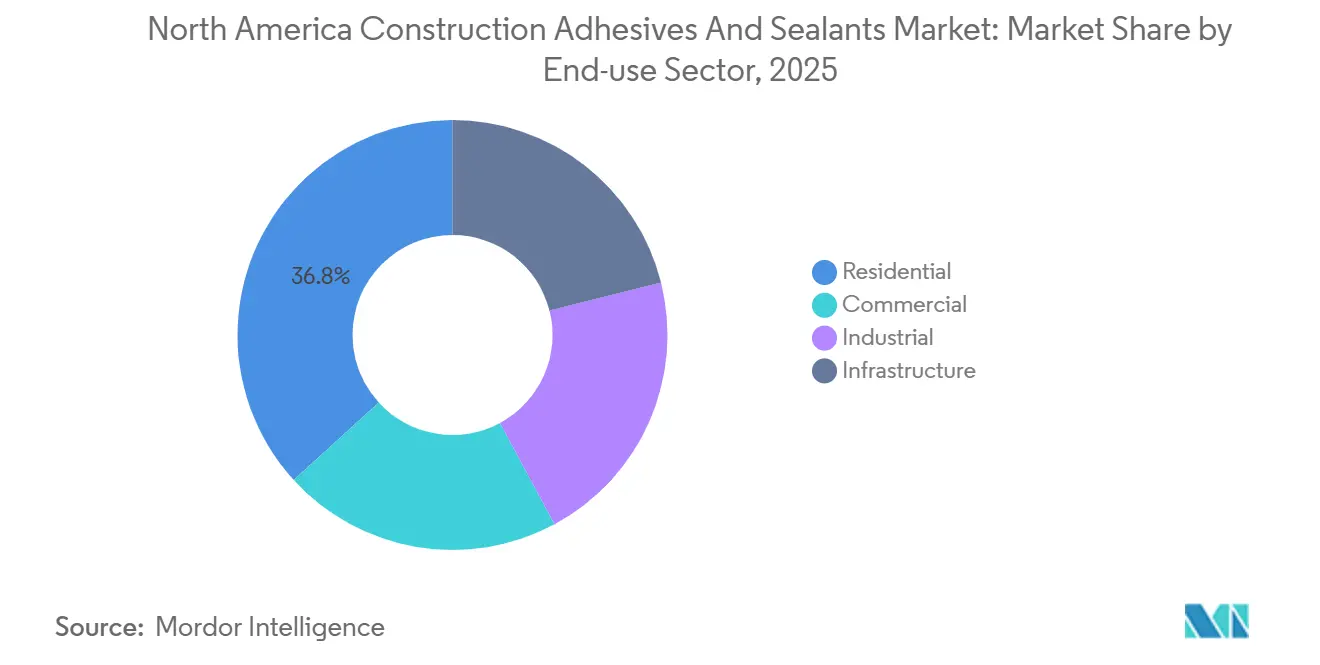

- By end-use sector, residential represented 36.78% of the North America construction adhesives and sealants market share in 2025, yet infrastructure is rising at a 7.23% CAGR through 2031.

- By geography, the United States led with 81.25% of the North America construction adhesives and sealants market share in 2025, whereas Canada is forecast to advance at a 6.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Construction Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for low-VOC construction materials | +1.2% | United States (California, OTC states), Canada | Medium term (2-4 years) |

| Rapid growth of off-site modular construction | +1.5% | United States, Canada | Long term (≥ 4 years) |

| Infrastructure stimulus packages in the U.S. and Canada | +1.8% | United States, Canada | Short term (≤ 2 years) |

| Adhesive formulation innovations enabling mixed-material bonding | +0.9% | North America (concentrated in advanced manufacturing hubs) | Medium term (2-4 years) |

| Rising multi-story timber buildings adoption | +0.6% | United States (West Coast, Northeast), Canada (British Columbia, Ontario) | Long term (≥ 4 years) |

| Widespread reroofing linked to extreme-weather events | +0.8% | United States (Southeast, Gulf Coast), Canada (Atlantic provinces) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Low-VOC Construction Materials

California’s SCAQMD Rule 1168, which limits VOC content to 50-250 g/L, has driven widespread reformulation away from solvent-based chemistries. Similar regulations in Maryland, Massachusetts, Texas, and other OTC states have created a fragmented regulatory environment that benefits suppliers with extensive compliant product portfolios. In March 2025, BASF and Sika introduced Baxxodur EC 151, which reduces VOC emissions by up to 90% and cures at temperatures as low as 5-10 °C. Modified-silane hybrids are gaining market share as they eliminate isocyanate exposure while meeting adhesion requirements. Specifiers are increasingly integrating low-VOC credentials with lifecycle durability, embedding environmental compliance into bid specifications rather than treating it as a regulatory formality.

Rapid Growth of Off-Site Modular Construction

Permanent modular construction reached USD 14.6 billion in 2024, up from USD 4.3 billion a decade earlier, reflecting a shift toward controlled-environment assembly. Factory workflows require adhesives that cure predictably and integrate with robotic dispensers. For instance, SikaWall-3000 Rapid Bond cures within one hour on cross-laminated timber (CLT) production lines, enhancing throughput. Similarly, Kiilto’s Pro SW adhesive reduces CLT bond times by 30%, improving cycle-time efficiency. Since modular units are completed in factories, demand for field-focused slow-cure adhesives is declining, steering the North America construction adhesives and sealants market toward factory-optimized formulations.

Infrastructure Stimulus Packages in the U.S. and Canada

The U.S. Bipartisan Infrastructure Law allocates over USD 480 billion to 60,000 projects, driving demand for bridge, tunnel, and highway sealants capable of tolerating ±60% joint movement[1]U.S. Department of Transportation, “Bipartisan Infrastructure Law Dashboard,” transportation.gov. Canada’s Investing in Canada Infrastructure Program contributes over USD 33 billion, along with more than USD 6 billion in targeted housing funds. Two-part silicone systems, such as Wabo SiliconeSeal, are preferred for their 75-year design life. States with a high number of structurally deficient bridges, including Pennsylvania, Ohio, and Michigan, are experiencing regional demand surges, favoring suppliers with local inventories and DOT-approved products.

Adhesive Formulation Innovations Enabling Mixed-Material Bonding

Modern construction increasingly involves mixed-material envelopes combining steel, engineered wood, FRP, and UHPC, making single-substrate adhesives inadequate. Henkel’s Purform platform reduces diisocyanates while effectively bonding metal, wood, and composites, meeting safety standards without compromising performance. Dow’s bio-based carbon-neutral silicones align with LEED credits and decarbonization goals. Additionally, UV-triggered on-demand curing technologies are being piloted, minimizing waste from expired two-part mixes and setting new benchmarks for process control in the North America construction adhesives and sealants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in petro-derived raw material prices | -0.7% | North America (concentrated in regions with limited feedstock alternatives) | Short term (≤ 2 years) |

| Stricter REACH and TSCA compliance costs | -0.4% | United States, Canada (cross-border trade implications) | Medium term (2-4 years) |

| Skilled-labor shortages for correct sealant application | -0.5% | United States (Southeast, Midwest), Canada | Long term (≥ 4 years) |

| Competition from mechanical fastening alternatives in roofing | -0.3% | United States (commercial roofing segment) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Petro-Derived Raw Material Prices

MDI prices rose by 5.86% in the week ending March 20, 2026, following a spike in benzene feedstock costs, with Covestro and Huntsman announcing price increases of USD 220-260 per ton. Raw materials account for approximately 75% of adhesive production costs, so a 1% price change can impact net income by USD 13.3 million for mid-sized producers. While formulators are exploring bio-based polyols and recycled resins, the requalification process for building codes can take up to two years, leaving smaller firms exposed to margin pressures.

Stricter REACH and TSCA Compliance Costs

TSCA risk evaluations for diisocyanates and phthalates require additional exposure data and investments in closed-loop dispensing systems. REACH authorizations can cost over EUR 500,000 per substance, posing significant challenges for regional suppliers[2]European Chemicals Agency, “REACH Authorization Overview,” echa.europa.eu. Henkel’s 2026 acquisition of ATP Adhesive Systems, a specialist in water-based adhesives, highlights a strategic shift toward inherently compliant product portfolios that mitigate risks associated with future substance bans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Resins Adoption Accelerates on Weathering Superiority

Silicone resins are projected to grow at a CAGR of 6.43% through 2031, as façade engineers value their long-term elasticity under UV exposure and thermal cycling. Polyurethane accounted for 24.38% of the North America construction adhesives and sealants market share in 2025, driven by its use in flooring and spray-foam insulation, though it faces cost challenges due to fluctuating isocyanate feedstock prices. Acrylics are preferred for interior applications where ease of cleanup and cost are prioritized over exterior durability. Epoxies are utilized in heavy-duty flooring and chemical-resistant bonds, with advancements such as low-temperature, low-VOC hardeners like Baxxodur EC 151 ensuring their relevance in cold-climate applications.

Silicone’s weathering advantage is supported by a 40-year outdoor study that demonstrated minimal modulus loss compared to polyurethane or acrylic sealants under cyclic UV, salt fog, and temperature variations. Code officials now include silicone in curtain-wall specifications, and bridge authorities approve two-part silicone joints for 75-year assets. Phenol-resorcinol remains critical for structural mass-timber laminations, while modified-silane hybrids combine silicone’s durability with polyurethane’s adhesion. Suppliers with expertise in multi-resin portfolios are better positioned to address the mixed-material bonding challenges in the North America construction adhesives and sealants market.

By Technology: Water-Borne Technology Gains on Regulatory Tailwinds

Water-borne technology is expected to grow at the highest CAGR of 6.43% through 2031, driven by regulatory measures such as SCAQMD Rule 1168 and OTC model rules, which impose strict VOC limits. Sealants accounted for 42.01% of technology revenue in 2025, with performance demands leading to niche formulations for specific applications like concrete-to-FRP, metal-to-glass, and wood-to-polymer joints.

Solvent-borne products maintain a presence in applications where freeze-thaw cycles or porous substrates challenge water-based alternatives, though their market share continues to decline. Reactive chemistries, including epoxies, polyurethanes, and methacrylates, are used for high-strength structural bonds despite their mixing complexity. Hot-melt adhesives are thriving in factory settings for windows and insulated panels, with Arkema expanding UV acrylic capacity in 2024 to meet modular construction demand. Hybrid technologies that combine water-borne low-VOC benefits with reactive strength are emerging as a key growth area in the North America construction adhesives and sealants market.

By Application: Infrastructure Joints Lead Growth

Infrastructure joints are forecast to grow at a CAGR of 7.18% through 2031, supported by the Bipartisan Infrastructure Law, which targets the replacement of aging bridges and tunnels. Flooring and tiling accounted for 39.83% of revenue in 2025, driven by residential remodeling and the adoption of large-format porcelain tiles. The infrastructure joint segment is expected to grow further as DOT specifications increasingly mandate advanced systems like Mageba’s Tensa Polyflex Advanced PU, which accommodates ±60% movement and resists de-icing salts.

Roofing demand is rising in hurricane-prone regions, where pressure-sensitive tapes are replacing hot asphalt to meet VOC regulations and wind-uplift requirements. Wall-panel systems are shifting toward unitized curtain walls with factory-applied structural silicone glazing, reducing onsite labor and ensuring consistent quality. Suppliers with localized production near major bridge corridors and disaster-prone roofing zones are well-positioned to capitalize on these growth trends.

By End-use Sector: Infrastructure Surpasses Residential Momentum

The infrastructure sector is projected to grow at a CAGR of 7.23% through 2031, supported by USD 480 billion in U.S. stimulus funding and over USD 33 billion in federal commitments in Canada. The residential sector accounted for 36.78% of demand in 2025, but higher mortgage rates are dampening single-family housing starts. The infrastructure segment is expected to expand as long-life, low-maintenance sealants gain traction in bridges, transit tunnels, and water treatment plants.

Commercial conversions of obsolete office spaces into apartments are driving demand for interior adhesives, while industrial megaprojects, such as battery plants and semiconductor facilities, require cleanroom-compatible sealants and high-temperature structural epoxies. Labor shortages are encouraging the use of prefabricated elements, shifting adhesive demand from jobsites to factories and benefiting suppliers with automated production solutions.

Geography Analysis

The United States captured 81.25% of the North America construction adhesives and sealants market revenue in 2025 as the Bipartisan Infrastructure Law funneled capital into highways, bridges, and transit. California’s VOC caps and similar rules in Maryland and Texas accelerate the transition to water-borne and reactive systems. The Southeast posts the largest nonresidential starts because data-center, semiconductor, and renewable-energy projects demand specialty sealants for thermal management and cleanrooms. The West Coast leads mass-timber deployment, exemplified by San Mateo’s 208,000 ft² COB3 office, boosting structural polyurethane and phenol-resorcinol orders.

Canada is the fastest-growing geography at a 6.43% CAGR through 2031, aided by infrastructure and housing funds that exceed USD 40 billion. British Columbia and Ontario pioneer CLT high-rises such as Toronto’s 87,000 ft² TRCA headquarters, raising demand for PRG 320-compliant timber adhesives. Atlantic provinces face frequent reroofing cycles linked to severe storms, stimulating uptake of pressure-sensitive tapes and fully adhered membranes.

In Mexico, nearshoring of automotive and electronics plants spurs industrial adhesive uses, while Arkema’s acquisition of Polímeros Especiales localizes supply. Labor migration across North America tightens skilled applicator availability, further encouraging prefabrication and simplified cartridge systems.

Competitive Landscape

The North America construction adhesives and sealants market remains moderately fragmented. Henkel’s 2026 deals to acquire ATP (EUR 270 million) and Stahl (EUR 2.1 billion) expand water-based tapes and specialty coatings portfolios, aligning with low-VOC mandates. Arkema invested USD 27 million to raise polyester capacity in Massachusetts, securing feedstock for Bostik’s high-performance flooring and roofing lines.

Technology leadership differentiates players: H.B. Fuller’s 4SG warm-edge spacer retains over 93% argon after 10 weather cycles, driving adoption of TPS automated lines. BASF and Sika co-developed Baxxodur EC 151, enabling ultra-low VOC epoxy floors to cure at 5-10 °C. Digital specification tools, such as the Bostik Pro app and BIM objects, deepen architect engagement and cut misapplication risks. Regional specialists carve niches by offering rapid color matches, custom pack sizes, and on-site technical training, advantages hard for global rivals to replicate.

White-space opportunities abound. Data-center construction needs fire-rated cable-penetration sealants and thermally conductive gap fillers. Renewable energy requires blade adhesives with 25-year UV endurance. Vendors that combine global R&D with local service, maintain vertically integrated feedstocks, and invest in automation-friendly products will outpace the broader North America construction adhesives and sealants market.

North America Construction Adhesives And Sealants Industry Leaders

3M

Henkel AG & Co. KGaA

Sika AG

H.B. Fuller Company

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Bostik, Inc., a subsidiary of Arkema, introduced OB1 multi-surface construction sealant and adhesive in the United States. This product is a versatile sealant and adhesive designed to streamline installations by replacing multiple products with one solution.

- September 2025: ATP adhesive systems AG unveiled ATP North America, a new initiative focused on delivering solvent-free adhesive technologies to manufacturers in the United States. The company supported this effort with a USD 70 million investment, establishing its first solvent-free manufacturing facility in Columbia, South Carolina.

North America Construction Adhesives And Sealants Market Report Scope

Construction adhesives and sealants play a critical role in building projects. Adhesives are designed to provide high shear and tensile strength, acting as invisible fasteners that evenly distribute load and stress across bonded surfaces. On the other hand, sealants are formulated to offer high flexibility and accommodate movement, enabling them to stretch and compress as buildings expand or contract due to thermal variations.

The North America Construction Adhesives And Sealants Market is segmented into resin, technology, application, end-use sector, and geography. By resin, the market is segmented into polyurethane, acrylic, cyanoacrylate, epoxy, silicone, VAE/EVA, and other resins. By technology, the market is segmented into sealants, water-borne, solvent-borne, reactive, and hot-melt. By application, the market is segmented into flooring and tiling, roofing, wall panels and facades, insulation and weatherproofing, and infrastructure joints (bridges, tunnels). By end-use sector, the market is segmented into residential, commercial, industrial, and infrastructure. The report also covers the market size and forecasts for construction adhesives and sealants in 3 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Polyurethane |

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Sealants |

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot-melt |

By Application

| Flooring and Tiling |

| Roofing |

| Wall Panels and Facades |

| Insulation and Weatherproofing |

| Infrastructure Joints (bridges, tunnels) |

By End-use Sector

| Residential |

| Commercial |

| Industrial |

| Infrastructure |

By Geography

| United States |

| Canada |

| Mexico |

| By Resin Type | Polyurethane |

| Acrylic | |

| Cyanoacrylate | |

| Epoxy | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Sealants |

| Water-borne | |

| Solvent-borne | |

| Reactive | |

| Hot-melt | |

| By Application | Flooring and Tiling |

| Roofing | |

| Wall Panels and Facades | |

| Insulation and Weatherproofing | |

| Infrastructure Joints (bridges, tunnels) | |

| By End-use Sector | Residential |

| Commercial | |

| Industrial | |

| Infrastructure | |

| By Geography | United States |

| Canada | |

| Mexico |

Market Definition

- End-user Industry - Residential construction, commercial construction, public buildings, industrial buildings and infrastructure projects are considered under the construction industry.

- Product - All adhesive and sealant products used in construction industry are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and Sealants technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms