North America ATV And UTV Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

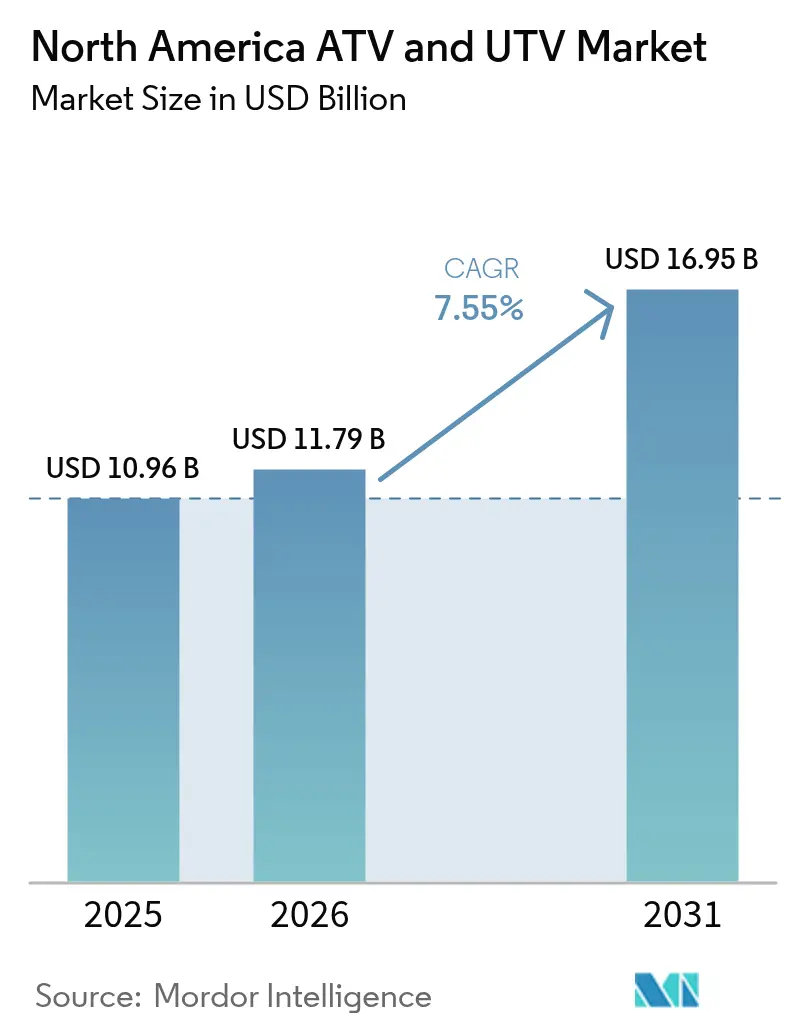

| Base Year Market Size (2025) | USD 10.96 Billion |

| Market Size (2026) | USD 11.79 Billion |

| Market Size (2031) | USD 16.95 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

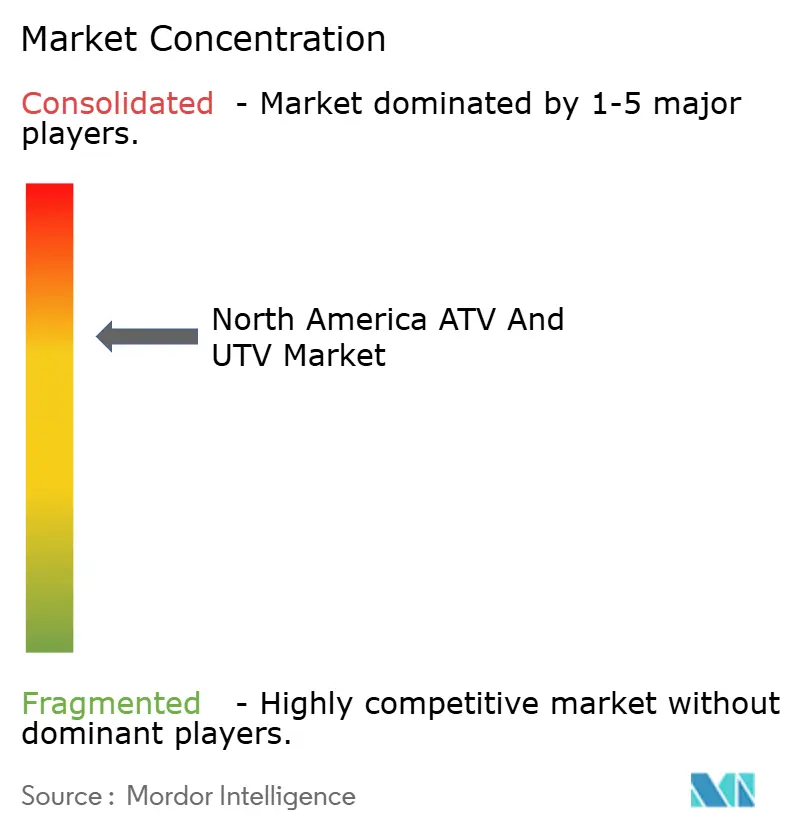

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America ATV And UTV Market Analysis by Mordor Intelligence

The North America ATV and UTV market size in 2026 is estimated at USD 11.79 billion, growing from 2025 value of USD 10.96 billion with 2031 projections showing USD 16.95 billion, growing at 7.55% CAGR over 2026-2031. Robust demand is rooted in recreational trail expansion, precision-farming uptake, and ongoing military procurement, while OEM design roadmaps emphasize electrified drivetrains and digitally controlled safety systems. Persistent growth of utility terrain vehicles (UTVs) safeguards revenue stability as these platforms now integrate factory-installed telematics, autonomous-ready wire-harnesses, and modular cargo solutions that lower the total cost of ownership for farms and public agencies. Electric side-by-sides gain traction in noise-sensitive tourism zones and conservation areas. Yet, gasoline powertrains remain dominant among price-sensitive segments because of their lower upfront cost and established refueling infrastructure. Competitive intensity has heightened after Textron divested Arctic Cat and Polaris confronted retail decline in Q3 2024, prompting aggressive model refreshes, dealer incentive programs, and localization of component supply chains.

Key Report Takeaways

- By vehicle type, utility terrain vehicles captured 71.18% of the North America ATV and UTV market share in 2025 and are advancing at a 7.66% CAGR to 2031.

- By propulsion, gasoline platforms accounted for 62.67% of the North America ATV and UTV market size in 2025, while electric models recorded the fastest 7.62% CAGR through 2031.

- By end-use, recreation and sports retained 72.85% of the North America ATV and UTV market size in 2025, whereas military and government demand is growing at a 7.6% CAGR.

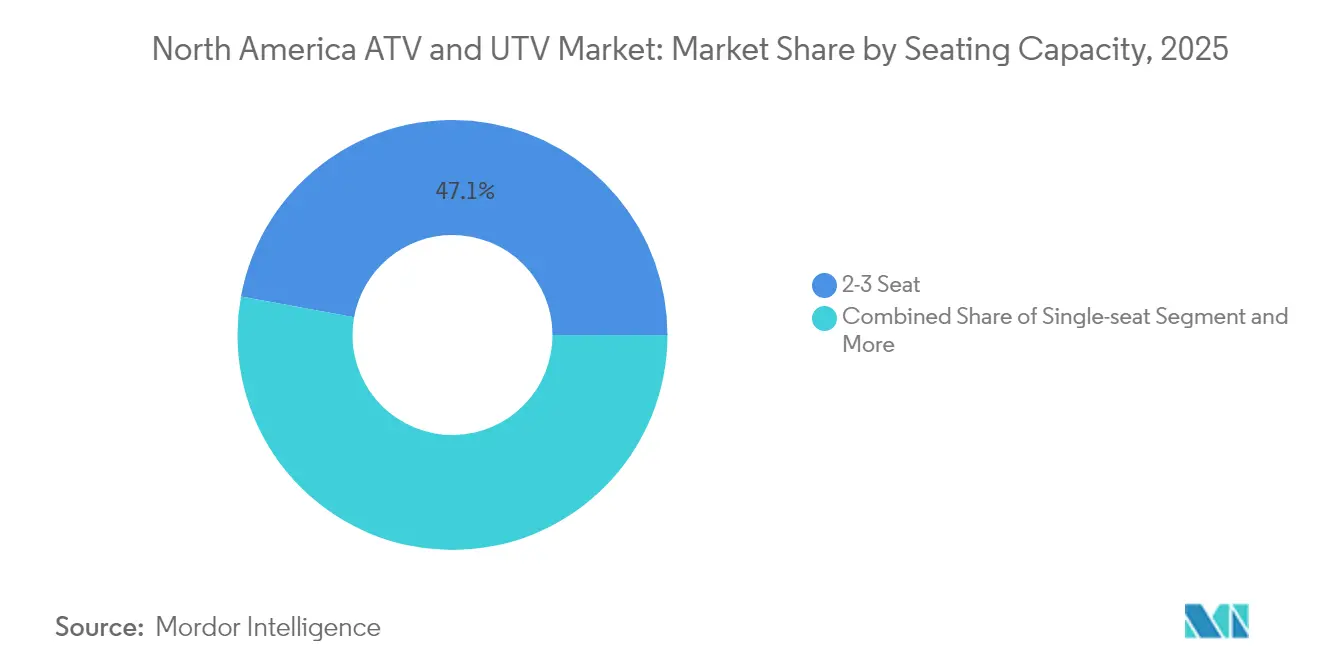

- By seating, two-to-three-seat designs held 47.14% of the North America ATV and UTV market size in 2025, yet four-to-six-seat layouts are expanding at a 7.58% CAGR.

- By drive configuration, four-wheel drive retained 60.72% of the North America ATV and UTV market size in 2025, and intelligent all-wheel drive systems are accelerating at a 7.67% CAGR.

- By country, the United States led with a 90.87% of the North America ATV and UTV market size in 2025, while Mexico is forecast to post the highest 7.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America ATV And UTV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Agricultural Mechanisation Needs | +1.8% | US Midwest, Canadian Prairies, Mexico agricultural regions | Long term (≥ 4 years) |

| Rising Recreational and Motorsports Activities | +1.2% | North America, with strongest gains in US and Canada | Medium term (2-4 years) |

| Silent Electric Sxs Demand | +1.1% | US conservation areas, Canadian wilderness regions | Medium term (2-4 years) |

| Technological Advances | +0.9% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Trail-Tourism Incentive Programs | +0.8% | US Western states, Canadian provinces, Mexico tourism zones | Short term (≤ 2 years) |

| Rural Broadband-Enabled Fleet Connectivity | +0.7% | US rural areas, expanding to Canada and Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Agricultural Mechanization Needs

Machine-learning-based crop-scouting attachments mounted on UTVs deliver 15-20% yield gains by combining multispectral imaging and AI vision analytics that flag nutrient deficiencies in real time[1]“AI-Driven Crop Scouting Trials,” United States Department of Agriculture, usda.gov. Farmers cite durability as their prime purchase criterion, pushing OEMs to reinforce cargo beds to withstand 450 kg hay bale loads. Precision guidance kits with sub-meter GPS accuracy now ship as dealer-installed options, automating spraying and soil sampling on irregular fields. Safety enhancements remain critical because agriculture accounts for three-fifth of work-related ATV fatalities, prompting roll-over detection systems that cut engine power within 200 ms of sensor activation. Autonomous prototypes undergoing pilot trials in Iowa operate follow-me modes behind combines, reducing hired-hand costs during peak harvest. Such innovations position UTVs as integral field assets rather than discretionary purchases, supporting long-run demand for the North America ATV and UTV market.

Rising Recreational & Motorsports Activities

ATV trail mileage funded by state tourism boards keeps expanding, exemplified by Pennsylvania’s Regional Trail Connector that now links 1,200 miles of mixed-use routes to local lodging hubs. Rental fleets report annual profits topping USD 85,000 as guided tour operators bundle equipment hire, trail permits, and safety gear in weekend packages. Wisconsin’s statutory update allowing ATVs and UTVs on designated county roads bolsters ride-in/ride-out tourism, lifting rural hospitality revenue. Equipment OEMs co-sponsor festivals such as Utah’s 2025 Paiute Trail Jamboree to showcase new models and collect real-time performance data through telematics. As a result, the North America ATV and UTV market captures significant global ATV demand, underpinning sustained aftermarket parts and apparel sales.

Silent Electric SxS Demand in Conservation & Hunting

Wildlife agencies in Michigan deploy HuntVe’s Game Changer—a 1,200 lb payload, 25-mile-range electric UTV—to access habitat restoration zones where engine noise disturbs nesting birds[2]“Electric Vehicle Pilot for Wildlife Areas,” Michigan Department of Natural Resources, michigan.gov . Conservation NGOs lease similar platforms for invasive-species removal, citing zero tailpipe emissions and minimal soil compaction as key benefits. Outfitters report higher client satisfaction on silent dawn safaris because game animals remain less skittish, increasing photographic success rates. OEMs respond with camouflage body panels, low-speed crawl modes, and 3-kW auxiliary power sockets that run spotlight arrays or research sensors without idling engines. Public-land administrators along the Colorado Plateau now stipulate decibel thresholds below 70 dBA, effectively steering procurement toward electric. This confluence of ecological regulation and user preference lifts premium-priced electric units, enlarging value pools within the North America ATV and UTV market.

Technological Advances in Suspension & Safety

Fox Live-Valve electronic dampers adapt compression within 20 ms, limiting body roll on rutted forestry roads and minimizing operator fatigue during eight-hour shifts[3]“Live-Valve Technology White Paper,” Fox Factory Holding Corp., ridefox.com . Can-Am’s Smart-Shox package blends inertial measurement data with throttle position to maintain tire contact patch, improving braking distances on loose gravel by over one-tenth. Polaris embeds an over-the-air firmware architecture that pushes traction-control updates via 4G LTE modules, keeping vehicles compliant with evolving ANSI/SVIA 1-2023 standards. Battery-electric drivetrains such as the RANGER XP Kinetic integrate regenerative braking that delivers 140 hp peak while enabling one-pedal control for operators with limited experience. Military integrators retrofit lidar-based collision avoidance on the same platforms, illustrating civil-defense technology spillover that accelerates feature adoption cycles for the North America ATV and UTV market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Purchase and Maintenance Costs | -1.5% | Global, with strongest impact in price-sensitive segments | Short term (≤ 2 years) |

| Lithium Supply-Chain Volatility | -1.2% | Global, affecting electric vehicle adoption rates | Long term (≥ 4 years) |

| Emission and Noise Regulation Tightening | -0.8% | California, northeastern US states, expanding to federal level | Medium term (2-4 years) |

| Land-Owner Liability Litigation | -0.6% | US rural areas, Canadian provinces with recreational access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Purchase & Maintenance Costs

Premium UTV stickers now eclipse USD 30,000 with the 2025 Polaris RANGER XP Kinetic topping USD 37,499 in fully optioned trim. For commercial fleet owners, high insurance costs and parts inventory tie up working capital because driveline, suspension, and battery modules remain brand-specific. Electric models promise more than one-fifth lower running costs over five years, yet limited dealership service capability prolongs downtime when high-voltage components fail. Financing complexities emerge for small farms that manage seasonal cash flows; lenders often require 20% down payments and collateral beyond the vehicle. Price pressure delays replacement cycles, muting short-term unit sales despite robust long-term fundamentals for the North America ATV and UTV market.

Lithium Supply-Chain Volatility

Benchmark forecasts show lithium demand rising fivefold by 2030, but the United States currently refines less than 5% of battery-grade material. Spot prices exceeded USD 21/kg in early 2025, inflating battery pack costs by 18% and eroding OEM margins on entry-level electric ATVs. New Inflation Reduction Act content rules stipulate four-fifths of North American–sourced critical minerals by 2027, forcing manufacturers to negotiate long-term offtake deals with junior miners in Nevada and Quebec. Supply-demand gaps risk production throttling; a projected 46% deficit could constrain 50,000 planned electric vehicle units in 2027, predominantly affecting growth segments of the North America ATV and UTV market. In response, companies like BRP are funding closed-loop recycling pilots to reclaim cobalt and nickel from warranty-return battery packs, cushioning exposure to upstream volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: UTV Versatility Sustains Leadership

Utility terrain vehicles commanded 71.18% of the North America ATV and UTV market share in 2025 and growing at a 7.66% CAGR, underscoring their multi-purpose appeal across construction, emergency response, and back-country tourism. This dominance-reinforcing scale advantages for cargo-bed liners, cab enclosures, and hydraulic lift kits suppliers. The North America ATV and UTV market size allocated to multi-purpose UTV configurations is set to grow exponentially by 2031, supported by dealer-installed telematics that standardize fleet monitoring for municipalities. Sport-oriented UTV models such as Yamaha’s Wolverine RMAX4 1000 help manufacturers defend high-margin niches while showcasing suspension technology transferable to work-focused trims.

All-terrain vehicles maintain niche relevance where single-rider agility, lower curb weight, and narrower track widths matter, particularly on trail systems mandating sub-50-inch vehicles. OEM roadmaps reveal six new ATV variants for 2025, integrating ride-by-wire throttles, blind-spot radar, and factory-installed winches to protect share against rapidly advancing UTVs. Regulatory alignment of ATV rollover standards with UTV occupant-protection protocols could blur historic category boundaries, with future models sharing chassis components and power electronics. Consequently, platform modularity is poised to reduce development cycles, sustaining innovation cadence while tempering bill-of-materials inflation across the North America ATV and UTV market.

By Propulsion/Fuel Type: Electrification Accelerates

Gasoline engines held 62.67% of the North America ATV and UTV market share in 2025. Yet, electrified drivetrains are advancing at a 7.62% CAGR, reflecting tightening emission caps and user preference for low-noise operation. Honda’s expansion in North Carolina earmarks battery packs and final vehicle assembly capacity, signaling mainstream adoption. The North America ATV and UTV market size attributable to electric units is projected to grow drastically by 2031, assuming pack prices decline. Meanwhile, diesel remains confined to heavy-duty ranch and forestry applications where high-torque hauling supersedes energy-density constraints.

Hybrid range-extended concepts such as HuntVe’s Switchback illustrate transitional architectures: a 72-V lithium pack supplies 40 km silent range before a 708 cc gasoline engine engages. Policymakers in California already mandate stage-V-equivalent off-road emission limits, hastening fleet electrification among public agencies. Yet mass-market electric penetration awaits infrastructure build-out of 240-V Level-2 chargers across trailheads and farmsteads, a requirement now tackled by cooperative utility-dealer programs in Midwestern states. Until such grid upgrades materialize, gasoline will sustain its majority hold on unit volumes within the North America ATV and UTV market.

By End-use Industry: Defense Drives Future Growth

Recreation and sports contributed 72.85% of the North America ATV and UTV market share in 2025, reflecting consumer appetite for outdoor adventure across a network of 100,000-plus miles of permitted trails. Defense procurement budgets deliver the fastest 7.6% CAGR through 2031 as armed forces adapt commercial off-the-shelf chassis for tactical autonomous missions. Polaris Government & Defense has booked over half a billion in cumulative U.S. contracts since 2003, and the latest indefinite-delivery vehicle award covers spare parts, training, and life-cycle support.

Agriculture and forestry represent a steady adoption curve where autonomous spot-spraying modules cut herbicide spend by quarter. Growth is further enhanced by rural broadband build-outs, enabling cloud-based fleet analytics, a cornerstone of multi-farmer equipment cooperatives. Industrial and construction firms account for under 5% of present demand but deploy UTVs with dump-box conversions and fire-suppression kits on remote mining sites. Search-and-rescue agencies leverage stretcher-ready rear decks and thermal-camera masts, transforming the North America ATV and UTV market into an essential element of public-safety infrastructure.

By Seating/Capacity: Crew Transport Takes Center Stage

Two-to-three-seat machines represent 47.14% of the North America ATV and UTV market share in 2025, balancing compact dimensions with adequate crew transport for fence repair, irrigation checks, and small-group tourism. OEMs offer factory quick-detach rear seats that convert to extended flatbeds within five minutes, improving asset utilization. Single-seat platforms retain a foothold in sports racing circuits and precision orchard spraying, where narrow rows dictate sub-1.2-m widths. Safety design evolves in tandem; multi-passenger builds now feature pretensioned three-point belts and adjustable-height grab handles, elevating perceived quality while boosting average selling prices across the North America ATV and UTV market.

Four-to-six-seat formats expanded at a 7.58% CAGR in 2025-2026 as families and work crews favor shared rides over solo operation. Model launches such as Kawasaki’s 2025 RIDGE Crew XR HVAC Limited showcase 5-passenger cabins with automotive-grade climate control, 116 hp output, and 2,500 lb towing capacity, bridging lifestyle and utility expectations. For hunting outfitters, multi-row seating increases party throughput per guide, elevating revenue density per trail permit.

By Drive Type: Intelligent Drivetrains Gain Share

Four-wheel drive maintained 60.72% of the North America ATV and UTV market share in 2025, owing to proven reliability and lower cost relative to fully active systems. However, all-wheel drive (AWD) platforms integrating electronically controlled differentials are set to grow at a 7.67% CAGR, propelled by demand from novice riders who value point-and-shoot traction over manual lock engagement. Can-Am’s Smart-Lok allows automatic torque biasing based on throttle, steering angle, and gyroscopic inputs, enabling confident rock-crawling without driver intervention.

Terrain-mode selectors synchronize engine mapping, ABS, and suspension damping, lowering technical barriers for commercial operators with seasonal staff turnover. Two-wheel drive remains relevant in flat agricultural plains where purchase price outweighs terrain complexity, but its share erodes steadily. The shift to intelligent drivetrains dovetails with autonomous frameworks, as shared sensor suites facilitate lane-centering and geofencing, further embedding software value capture inside the North America ATV and UTV market.

Geography Analysis

The United States dominated 2025 revenue with a 90.87% of the North America ATV and UTV market share in 2025, bolstered by millions of acres of managed trail systems, robust military spending, and dealer networks spanning 2,300 storefronts. Yet unit volumes plateaued in 2024 when Polaris reported a retail contraction, signaling maturity in core recreation sub-segments. Federal regulators intensified oversight after a more than one-fifth rise in child fatalities. New ANSI/SVIA 1-2023 mandates, effective from January 2025, require speed-limiting youth keys, steering-column crush zones, and mandatory rollover warnings. OEMs reacted by channeling more resources into premium trims and service-based revenue, including subscription data analytics that predict maintenance events with 85% accuracy.

Canada contributes modest but steady growth, with provinces such as British Columbia and Alberta extending ATV trails by one-tenth from 2023–2025 to capitalize on adventure tourism. Prairie farms integrate UTVs into mixed-fleet telematics alongside tractors and combines, enabling cross-asset route optimization that trims diesel consumption by 7%. Harmonized safety regulations facilitate cross-border vehicle homologation, allowing U.S. dealers near the border to service Canadian owners and vice versa, improving residual values and underpinning financing rates.

Mexico is the fastest-growing geography at a 7.74% CAGR and hosts new manufacturing investments that reshape continental supply chains. Kawasaki’s Nuevo León plant targets 30,000 units annually, complemented by Can-Am’s Juarez facilities producing Rotax engines for regional assembly lines. Domestic demand climbs on rising disposable income and government subsidies promoting mechanized agriculture in Sinaloa and Jalisco. Mexico’s tourism secretariat also funds eco-park developments that rent UTVs for guided dune and jungle excursions, creating a dual domestic-export justification for OEM capacity. Cross-border logistics benefit from USMCA duty exemptions on finished vehicles meeting regional content thresholds, ensuring the North America ATV and UTV market retains production resiliency against global shipping disruptions.

Competitive Landscape

The industry exhibits oligopolistic characteristics as Polaris, BRP (Can-Am), Honda, Yamaha, and Kawasaki collectively control most of the market share. Polaris leans on its defense backlog and the battery-electric Pro XD Kinetic to shore up margins after Q3 2024 retail decline. BRP leverages vertical integration with Rotax powertrains to maintain supply stability amid chip shortages. Honda’s North Carolina consolidation creates an exclusive North American ATV hub that lowers freight costs by 8%. Kawasaki’s forthcoming 2026 Teryx H2 introduces supercharged performance features derived from its street-motorcycle heritage, signaling continued platform borrowing across product lines.

Strategic moves in 2025 include Arctic Cat’s acquisition by an Argo-led consortium, targeting a brand revitalization focused on recreational snow-to-dirt crossover models. Kandi Technologies scales U.S. knock-down kit assembly in Texas to dodge import tariffs and carving out budget electric niches. Technology alliances proliferate: Overland AI partners with Polaris to retrofit lidar perception stacks on Sportsman chassis for autonomous route clearance missions, while Fox Factory collaborates with Yamaha to embed predictive damping algorithms harnessing cloud-logged telemetry.

Supply chain priorities center on battery cell localization, composite-panel molding, and semiconductor redundancy. OEMs hedge geopolitical risk by dual-sourcing motor controllers from U.S. and Taiwanese vendors. Dealers diversify income streams through subscription diagnostics and extended warranty bundles that capture aftermarket value as unit sales growth moderates. Collectively, these strategic vectors reinforce competitive differentiation while elevating switching costs for fleet managers participating in the North America ATV and UTV market.

North America ATV And UTV Industry Leaders

American Honda Motor Co. Inc.

Yamaha Motor Co. Ltd

Arctic Cat Inc.

Polaris Industries Inc.

BRP Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kawasaki unveiled the 2026 Teryx H2 featuring FOX 3.0 Live Valve bypass shocks with 23.2-inch front and 24.0-inch rear travel to target the premium multi-passenger UTV segment.

- July 2025: Polaris celebrated the 40th anniversary of Polaris ATVs by launching its 2026 model family across recreational and utility lines, introducing enhanced battery-compatible chassis.

- April 2025: Argo and an investment group completed the acquisition of Arctic Cat from Textron, signaling a renewed focus on brand-specific innovation and dealer engagement.

North America ATV And UTV Market Report Scope

ATVs (all-terrain vehicles) are primarily used for recreational activities. They are designed for a single rider. UTVs (utility task vehicles) include side-by-side car-like control, along with steering wheels. UTVs are used to transport small freight loads on off-roads.

The North American ATV and UTV market is segmented by vehicle type, application type, fuel type, and country. By vehicle type, the market is segmented into sport ATVs and utility terrain vehicles (UTVs). By application type, the market is segmented into sports, agriculture, and other applications. By fuel type, the market is segmented into gasoline-powered and electric-powered. By country, the market is segmented into the United States, Canada, and the Rest of North America. For each segment, the market sizing and forecast have been done based on the value (USD).

| All-Terrain Vehicles (ATVs) | Sport ATVs |

| Utility/Work ATVs | |

| Utility Terrain Vehicles (UTVs/Side-by-Sides) | Sport UTVs |

| Multi-purpose UTVs |

| Gasoline |

| Diesel |

| Electric |

| Hybrid |

| Recreation & Sports |

| Agriculture & Forestry |

| Industrial & Construction |

| Military & Government |

| Search, Rescue & Emergency Services |

| Single-seat |

| 2 – 3 seat |

| 4 – 6 seat |

| 2-Wheel Drive |

| 4-Wheel Drive |

| All-Wheel Drive |

| United States |

| Canada |

| Rest of North America |

| By Vehicle Type | All-Terrain Vehicles (ATVs) | Sport ATVs |

| Utility/Work ATVs | ||

| Utility Terrain Vehicles (UTVs/Side-by-Sides) | Sport UTVs | |

| Multi-purpose UTVs | ||

| By Propulsion/Fuel Type | Gasoline | |

| Diesel | ||

| Electric | ||

| By End-use Industry | Hybrid | |

| Recreation & Sports | ||

| Agriculture & Forestry | ||

| Industrial & Construction | ||

| Military & Government | ||

| Search, Rescue & Emergency Services | ||

| By Seating/Capacity | Single-seat | |

| 2 – 3 seat | ||

| 4 – 6 seat | ||

| By Drive Type | 2-Wheel Drive | |

| 4-Wheel Drive | ||

| All-Wheel Drive | ||

| By Country | United States | |

| Canada | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current value of the North America ATV UTV market and its projected CAGR to 2031?

The segment is valued at USD 11.79 billion in 2026 and is forecast to expand to USD 16.95 billion by 2031 on a 7.55% CAGR trajectory.

Which vehicle type holds the largest share in North America ATV UTV sales for 2025?

Utility terrain vehicles led with 71.18% of 2025 revenue, reflecting their versatility across recreational, agricultural, and public-sector applications.

How fast are electric ATV and UTV volumes expected to grow in North America?

Electrified units represent the fastest propulsion category, advancing at a 7.62% CAGR through 2031 as adoption widens in noise-sensitive and fleet segments.

Which end-use segment shows the highest growth momentum in this space?

Military and government procurement is rising at a 7.6% CAGR, driven by autonomous mobility initiatives and stealth requirements.

Why is Mexico viewed as the regional growth engine for these vehicles?

New OEM plants and expanding domestic demand support a growth at 7.74% CAGR, the highest among North American countries, while leveraging USMCA trade advantages.

Who are the leading manufacturers dominating North America ATV UTV shipments?

Polaris, BRP (Can-Am), Honda, Yamaha, and Kawasaki collectively account for significant regional revenue, underscoring an oligopolistic landscape.

Page last updated on: