Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 26.21 Billion |

| Market Size (2026) | USD 27.88 Billion |

| Market Size (2031) | USD 33.94 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Aircraft MRO Market Analysis by Mordor Intelligence

The North America aircraft MRO market size is expected to grow from USD 26.76 billion in 2025 to USD 27.88 billion in 2026 and is forecasted to reach USD 33.94 billion by 2031 at 4.01% CAGR over 2026-2031. This measured expansion comes as airlines and cargo operators intensify engine-shop demand just as labor and tooling capacity tighten, pushing more work to independent shops and stimulating wider use of certified used serviceable material (USM) to shorten turnaround times. Military life-extension programs for the F-16V, C-130H, UH-60 Black Hawk, and AH-64 Apache inject multi-year depot workloads into the same technician pool, resulting in wage inflation and extended lead times. OEM-captive providers are leveraging 15-year service contracts to lock in 43.21% of 2025 revenue, while independents are growing at a 5.01% CAGR by offering flexible slot access and multi-platform capabilities. Concurrently, rising avionics obsolescence, landing-gear fatigue, and auxiliary power unit overhauls on aging B737NG and A320ceo fleets fuel the fastest growth in component work.

Key Report Takeaways

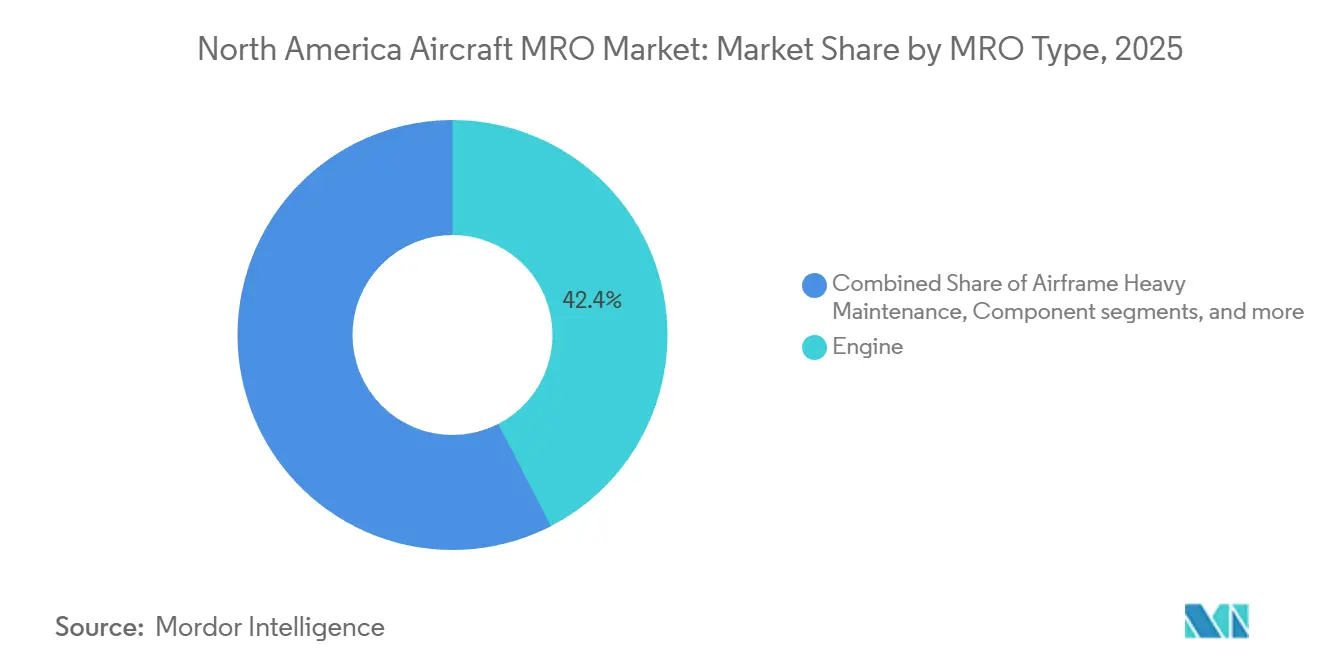

- By MRO type, engine MRO held 42.43% revenue share in 2025, whereas component repairs are forecasted to expand at a 4.25% CAGR through 2031.

- By aircraft type, fixed-wing platforms accounted for 64.22% of 2025 revenue, and rotary-wing work is advancing at a 4.87% CAGR to 2031.

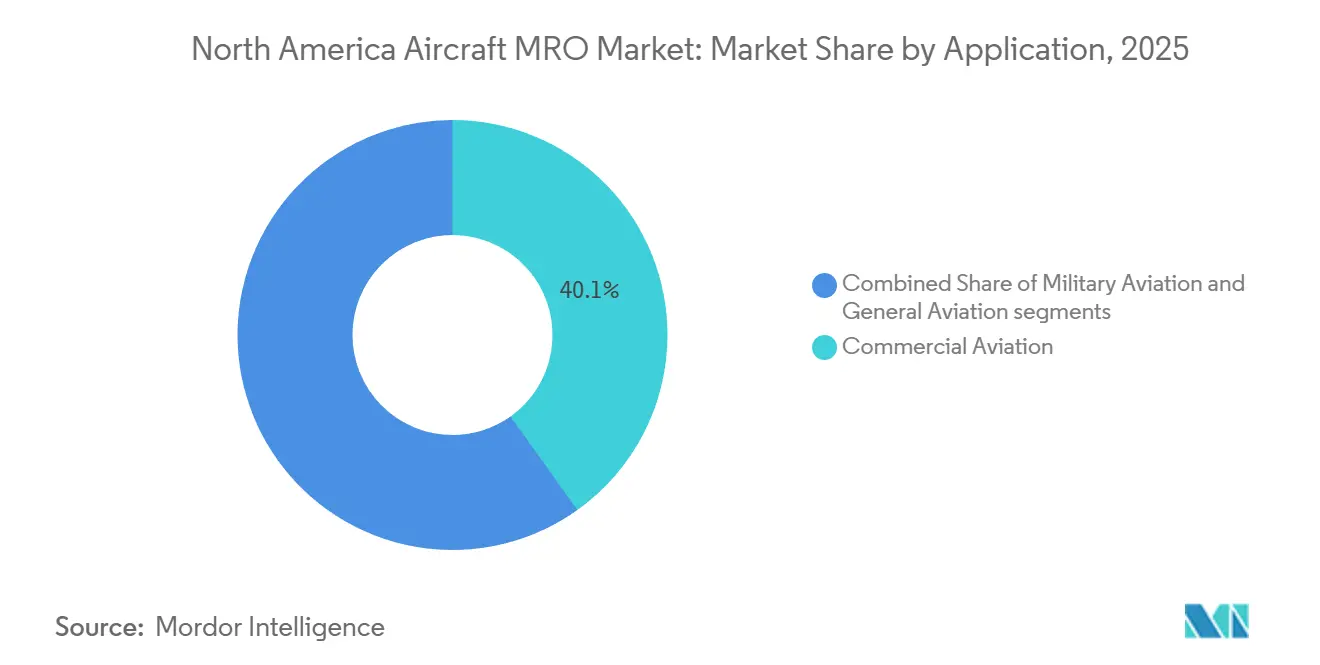

- By application, commercial aviation generated 40.14% of 2025 demand, while military programs are set to rise at a 5.72% CAGR through 2031.

- By service provider, OEM-captive networks commanded a 43.21% share in 2025, and independent third-party shops are expected to grow at a 5.01% CAGR through 2031.

- By country, the United States led with 42.67% of 2025 revenue, whereas Canada is projected to grow at a 4.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Aircraft MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging commercial fleet requiring life-extension MRO | +1.2% | United States, Canada | Long term (≥ 4 years) |

| Rebound in passenger and cargo traffic boosting flight hours | +0.9% | United States, Mexico | Medium term (2-4 years) |

| OEM long-term service agreements expanding aftermarket capture | +0.7% | United States, Canada | Long term (≥ 4 years) |

| Engine-shop capacity crunch inflating US in-region demand | +0.6% | United States | Short term (≤ 2 years) |

| Surge in Used Serviceable Material (USM) adoption to cut TAT | +0.4% | North America | Medium term (2-4 years) |

| Military life-extension programs for legacy fleets | +0.5% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Commercial Fleet Requiring Life-Extension MRO

The average age of the commercial jet fleet in the region increased to 12.8 years in 2025, with narrowbody aircraft averaging 14.1 years and widebody aircraft averaging 11.3 years.[1]Federal Aviation Administration, “Aerospace Forecast 2025-2045,” faa.gov Airlines are targeting 25- to 30-year life cycles for B737NG and A320ceo airframes, putting upward pressure on heavy D-check activity and corrosion remediation. Supplemental inspection mandates under FAA Part 26 are adding 15%-20% extra labor hours per event as cracks appear in wing root attachments and lap joints.[2]Boeing, “Commercial Fleet Data,” boeing.com OEMs increasingly bundle winglet retrofits and cabin reconfigurations with scheduled checks, locking customers into multi-year service packages that dampen price competition. These actions ensure the North America aircraft MRO market maintains a dependable structural backlog while intensifying the scramble for skilled technicians.

Rebound in Passenger and Cargo Traffic Boosting Flight Hours

Revenue departures increased 7.3% year-over-year in 2024 to 11.2 million, and total flight hours are expected to reach 28.5 million in 2026, surpassing pre-pandemic levels for the first time. A narrowbody flying 11 hours per day reaches its next engine shop visit roughly 18 months sooner than one flying 9 hours, bringing forward CFM56 and LEAP cycles. FedEx and UPS each reported double-digit block-hour growth in 2024, accelerating the overhaul of landing gear and APU. The engine overhaul turnaround has widened to 120-150 days by 2026, compared with 90 days two years earlier, forcing operators to lease spare engines and thereby inflating near-term spending. Consequently, the North America aircraft MRO market is experiencing demand peaks in line and engine services despite capacity headwinds.

OEM Long-Term Service Agreements Expanding Aftermarket Capture

CFM International enrolled 3,200 LEAP engines under 15-year flight-hour deals in 2024-2025, while Pratt & Whitney added 1,800 GTF powerplants to its EngineWise program. These agreements shift cost risk to OEMs but limit the airline's ability to shop independently, consolidating revenue within captive networks. GE Aerospace backed this strategy with a USD 1 billion capacity expansion announced in 2024 to double narrowbody engine throughput. Independent shops, therefore, pivot toward maturing platforms such as the CFM56, V2500, and CF6, where OEM focus is waning. Combined, these activities reinforce the market power of OEMs while spurring niche opportunities elsewhere in the North America aircraft MRO market.

Engine-Shop Capacity Crunch Inflating US In-Region Demand

Annual narrowbody engine shop-visit demand is expected to peak in 2026 at approximately 4,200 events, exceeding installed capacity by around 15%, according to industry estimates. The shortfall stems from accelerated LEAP repair cycles, a backlog of GTF combustor inspections, and pandemic-era under-investment in test cells. Delta TechOps opened a dedicated GTF line in May 2024, and StandardAero added LEAP-1A capability in San Antonio. Spot-market CFM56 overhaul pricing rose to USD 1.8-2.1 million in 2025, up from USD 1.5 million in 2023, as shops prioritize multi-engine commitments. These pressures keep North America aircraft MRO market participants focused on throughput and tooling investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute skilled-technician shortage | -0.8% | United States, Canada | Long term (≥ 4 years) |

| Persistent parts and supply-chain bottlenecks | -0.6% | North America | Medium term (2-4 years) |

| Tightening hazardous-chemicals and waste-disposal regulations | -0.2% | United States | Medium term (2-4 years) |

| Longer maintenance intervals on new-gen aircraft | -0.5% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Skilled-Technician Shortage

Around 30% of certificated mechanics will reach retirement eligibility within five years, while US aviation schools graduated only 3,200 technicians in 2024, against an industry demand of roughly 5,000. Starting pay at Delta TechOps reached USD 72,000 in 2025, and sign-on bonuses of USD 10,000 to USD 15,000 became common at independent shops. Throughput fell 10% to 15% in 2025 compared to 2023, as facilities struggled to staff second shifts, forcing airlines to lease additional aircraft to protect their schedules. Automation, such as robotic paint stripping and automated non-destructive testing, offers relief but requires three to five years to scale. Until then, the labor gap will continue to weigh on the North America aircraft MRO market.

Persistent Parts and Supply Chain Bottlenecks

Lead times for titanium castings and nickel-alloy forgings used in engine hot sections stretched to 12-18 months in 2025, double pre-pandemic levels.[3]National Association of Manufacturers, “2024 Aerospace Supplier Survey,” nam.org The National Association of Manufacturers found that 78% of suppliers are confronting raw-material shortages, while tariffs reinstated in 2024 add up to 25% in cost premiums. Smaller repair stations, lacking the bulk-buying power, absorb the steepest hit, which can prompt them to defer tooling upgrades or exit the field. Consequently, USM, consignment pools, and operator part cannibalization form growing elements of the North America aircraft MRO market supply response.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By MRO Type: Engine Services Dominate Amid Component Growth

Engine activity generated 42.43% of 2025 revenue, as 18,000 active commercial turbofans produced a steady cadence of first-run removals. Each overhaul averaged USD 1.8 million for narrowbody units and USD 4.5 million for widebody engines. This sub-segment anchors relationships because high-value workscopes frequently cascade into accessory, fuel-nozzle, and gearbox repairs. Component shops, however, expand at a 4.25% CAGR through 2031 as avionics mandates, landing-gear fatigue, and APU renewals rise in tandem with fleet age. Because component visits require lower capital expenditure than engine test cells, they enable independents to enter the North America aircraft MRO market rapidly.

Line-maintenance providers continue to supply a base-load of walk-around checks, minor defect rectification, and A-checks at outstations, sustaining employment across regional airports. Heavy airframe work grows more slowly due to extended structural intervals on next-generation jets. Yet, schedules remain full as operators retrofit cabin Wi-Fi, winglets, and weight-saving composite panels. Modifications and upgrades offer margin upside because engineering services add billable design hours alongside hands-on labor. Combined, these diverse service lines keep the North America aircraft MRO market resilient to cyclical swings.

By Aircraft Type: Fixed-Wing Dominance with Rotary Wing Acceleration

Fixed-wing fleets delivered 64.22% of 2025 MRO revenue, reflecting 7,800 active narrowbodies, 1,200 widebodies, and more than 15,000 business jets and turboprops registered in North America. Their high utilization and established maintenance planning documents provide predictable shop scheduling. Rotary-wing demand, although smaller in absolute value, grows at a 4.87% CAGR as military UH-60 and AH-64 upgrades and offshore oil-and-gas fleet renewals drive transmission overhaul and composite rotor-blade replacement work.

Rotary-wing MRO requires specialized tooling for dynamic components and hot-section inspections of turboshaft engines, creating entry barriers that favor niche providers. Firms such as StandardAero and ST Engineering have established rotary-wing centers of excellence, positioning them to capitalize on depot overflow and to supply composite repair know-how. Consequently, rotary-wing programs add a differentiated growth vector to the North America aircraft MRO market.

By Application: Commercial Passenger Base with Cargo Acceleration

Commercial aviation accounted for 40.14% of 2025 demand, with the freighter segment driven by e-commerce firms prioritizing same-day delivery. Boeing supplied 50 B737-800BCF conversions in 2024 and continues to ramp up B767-300BCF output, with each project involving structural reinforcements, cargo door installation, and re-certified maintenance programs. Amazon Air, FedEx, and UPS all expanded their narrowbody freighter fleets, resulting in incremental line checks, structural modifications, and engine events that are contributing to the growth of the North America aircraft MRO market for freighter operations.

Military aviation, expected to advance at a 5.72% CAGR through 2031, remains a consistent revenue source through multi-year depot contracts, although budget allocations tend to tilt toward new-platform procurement. General aviation repairs form a fragmented yet critical layer, supporting business jet reliability through cabin refurbishments, ADS-B Out upgrades, and Wi-Fi retrofits. These combined applications deliver a balanced, multi-segment demand profile for the North America aircraft MRO market.

By Service Provider: OEM Captive Leadership with Independent Growth

OEM-captive networks claimed 43.21% of 2025 revenue by bundling spares, warranties, and financing into long-term agreements that tether operators to factory facilities. Nevertheless, independents are scaling at a 5.01% CAGR as they offer multi-platform coverage, price transparency, and faster slot access, winning business from low-cost carriers and cargo operators that prioritize operating cost certainty. AAR grew MRO revenue 37.60% year on year in Q2 FY 2025 after securing new Embraer E-Jet landing-gear and Rockwell Collins avionics programs.[4]AAR Corp, “Investor Presentations,” aarcorp.com

Airline-affiliated shops, such as Delta TechOps, utilize surplus hangar capacity to serve third parties, thereby cushioning internal workload fluctuations. Digital collaboration intensifies competition, with Honeywell Forge and other analytics suites providing predictive insights that enable providers to advertise evidence-based turnaround commitments. These innovations reshape the competitive landscape within the North America aircraft MRO market.

Geography Analysis

The United States captured 42.67% of the 2025 revenue, underpinned by major hubs in Atlanta, Dallas, and Chicago, as well as Air Force and Navy depots that sustain fighter, tanker, and rotorcraft fleets. Delta TechOps’ dedicated Pratt & Whitney GTF line opened in 2024, targeting 200 annual engines by 2027, while GE Aerospace committed USD 1 billion to double LEAP capacity. The North America aircraft MRO market share, attributed to the US, benefits from a deep supplier base but must confront rising labor costs and environmental compliance obligations.

Canada is projected to grow at a 4.52% CAGR through 2031, driven by the opening of Lufthansa Technik AG and WestJet’s CAD 120 million (USD 87.13 million) LEAP-1B shop in Calgary in 2027, as well as government incentives through the Strategic Innovation Fund. StandardAero’s Winnipeg and Vancouver sites broaden engine and component capacity, while Air Canada Technical Services modernizes Montreal and Toronto facilities. Transport Canada’s bilateral approvals with the FAA and EASA enable Canadian shops to capture overflow demand, thereby strengthening their position within the broader North America aircraft MRO market.

Mexico attracts cost-sensitive projects due to labor rates averaging USD 18,000-25,000 per mechanic and tariff-free trade under USMCA. Safran’s USD 80 million LEAP center in Querétaro opens in 2026, and Viva Aerobus plans a USD 235 million base in the same state for 2027. Customs and certification procedures add two to three days to typical turnarounds, but economic advantages compensate, ensuring Mexico’s footprint within the North America aircraft MRO market continues to grow.

Competitive Landscape

The competitive landscape exhibits medium concentration. OEM groups, including GE Aerospace, RTX Corporation, Rolls-Royce plc, Safran SA, and Honeywell International Inc., collectively held more than 40% of 2025 revenue through proprietary tooling, engineering data, and flight-hour agreements. Independent majors AAR CORP., StandardAero Aviation Holdings, Inc., and Singapore Technologies Engineering Ltd. increase penetration by offering multi-platform coverage, transparent pricing, and faster shop slots for CFM56, V2500, and mature widebody engines. Airline-affiliated entities, such as Delta TechOps and Air Canada Technical Services, leverage existing infrastructure to win third-party contracts and mitigate fleet utilization cycles, thereby strengthening their contribution to the North America aircraft MRO market.

Digital capabilities now form a decisive differentiator. Honeywell Forge predicts component failures 30 days in advance across more than 1,200 aircraft, resulting in an 18% reduction in auxiliary power unit removals and a 12% reduction in landing gear overhauls. Collins Aerospace applies similar analytics to 1,200 aircraft, demonstrating consistent savings in unscheduled maintenance events. Meanwhile, USM aggregators such as AerSale achieve rapid growth by curating certified parts pools with full traceability, a capability prized amid enduring raw material shortages. Niche opportunities persist in rotary-wing, freighter conversion, and composite repair, allowing specialized firms to capture profitable pockets within the broader North America aircraft MRO market.

North America Aircraft MRO Industry Leaders

Delta TechOps (Delta Air Lines Inc.)

AAR CORP.

Lufthansa Technik AG

StandardAero Aviation Holdings, Inc.

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: AAR CORP. announced the USD 78 million acquisition of HAECO Americas from HAECO Group in an all-cash transaction. This acquisition enhances AAR's maintenance capabilities and aligns with its strategic objective to expand the Repair & Engineering segment, subject to customary adjustments and conditions.

- February 2025: Air France Industries KLM Engineering & Maintenance (AFI KLM E&M) and Air Canada signed a 10-year Component Support agreement for 58 B787 Dreamliners, establishing a new pool stock in Toronto to enhance support for Air Canada’s expanding operations.

- August 2024: StandardAero secured a USD 315.70 million contract to maintain the US Navy’s T56-A-427A engines, which support the E-2D Advanced Hawkeye.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America aircraft MRO market as the annual spending by airlines, militaries, and business-aviation operators on scheduled or unscheduled inspection, repair, overhaul, modification, and line support for fixed- and rotary-wing aircraft operating in the United States, Canada, and Mexico.

Scope exclusion: manufacture of new parts or tools and any non-aviation MRO activities are kept outside this value chain snapshot.

Segmentation Overview

- By MRO Type

- Engine

- Airframe Heavy Maintenance

- Component

- Line and Routine Checks

- Modifications and Upgrades

- By Aircraft Type

- Fixed Wing

- Rotary Wing

- By Application

- Commercial Aviation

- Passenger

- Cargo/Freighter

- Military Aviation

- General Aviation

- Commercial Aviation

- By Service Provider

- Airline-affiliated MRO

- Independent Third-party MRO

- OEM-Captive MRO

- Military Depots

- By Geography

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Our analysts gathered viewpoints through interviews with airline engineering heads, independent hangar managers, engine shop planners, and regulatory inspectors across all three countries. These discussions tested utilization rates, shop-turn bottlenecks, and average service-package prices, letting us fine-tune desk assumptions and close data gaps.

Desk Research

We began with open data from the FAA, Transport Canada, Mexico's AFAC, the Bureau of Transportation Statistics, and IATA flight-hour records, then layered insights from trade bodies such as ARSA and the Aerospace Industries Association. Market signals pulled from quarterly airline filings, OEM service bulletins, and press releases were complemented by fleet databases inside D&B Hoovers and Dow Jones Factiva.

Airworthiness directives, cross-border trade manifests, and technician wage indices helped us benchmark labor-material splits, while historic shop-visit curves provided age-cohort behavior.

The sources named here are illustrative; many additional references were tapped for validation and clarity.

Market-Sizing & Forecasting

A top-down rebuild starts with in-service fleet counts and average flight hours, which are then multiplied by typical maintenance cost per hour to derive the demand pool; selective bottom-up checks, sampled engine shop bills, parts-order volumes, and line-check frequencies keep totals grounded. Key variables modeled include fleet age, heavy-check interval drift, engine shop capacity, technician wage inflation, and freight-to-passenger traffic mix. Multivariate regression, stress-tested through scenario analysis, projects values to 2030 after aligning macro drivers such as GDP and jet-fuel trends.

Data Validation & Update Cycle

Before release, outputs pass variance scans versus historical spend, peer ratios, and independent cost trackers. Senior reviewers sign off after anomalies are resolved. We refresh the model every twelve months and reopen it sooner if fleet plans, regulation, or currency swings materially shift.

Why Mordor's North America Aircraft MRO Baseline Earns Trust

Published estimates often diverge because firms mix indirect economic output with direct maintenance spend, apply global cost curves to local wages, or freeze refresh cycles for years.

Mordor's study reports only service expenditure within North America, converts supplier quotes to constant 2025 dollars, and revalidates inputs annually; steps that temper overstatement yet avoid undue conservatism.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.96 B (2025) | Mordor Intelligence | - |

| USD 28.00 B (2025) | Global Consultancy A | Adds tooling and training outlays and applies global average labor rates |

| USD 69.00 B (2025) | Industry Association B | Tallies indirect economic output and covers only the U.S. |

In sum, our balanced, variable-driven framework delivers a transparent baseline that decision-makers can trace back to clear fleet metrics and repeat with modest resources.

Key Questions Answered in the Report

What is the current value and CAGR outlook for the North America aircraft MRO market?

The North America aircraft MRO market stands at USD 27.88 billion in 2026 and is projected to reach USD 33.94 billion by 2031, reflecting a 4.01% CAGR.

Which service line is expanding fastest within North American MRO?

Component repair and overhaul is projected to grow at about 4.25% CAGR through 2031, propelled by avionics obsolescence and landing-gear fatigue on aging narrowbody fleets.

How is the technician shortage influencing maintenance turnaround time?

A shortfall of 20,000-25,000 certificated mechanics is extending engine-shop TAT to 120-150 days and prompting airlines to lease spare engines or increase USM purchases to keep aircraft flying.

Why is Canada becoming a prominent MRO growth hub?

Government incentives and new LEAP-1B engine capacity in Calgary, plus established StandardAero and Air Canada facilities, are driving a forecast 4.52% CAGR for Canadian MRO revenue through 2031.

In what way are OEM long-term service agreements reshaping competition?

Fifteen-year, rate-per-flight-hour contracts for LEAP and GTF engines shift cost risk to manufacturers but lock airlines into captive networks, prompting independents to focus on mature engine families where OEM support is waning.

What role do long-term service agreements play in the industry?

OEM-backed agreements provide airlines with cost predictability while enabling manufacturers to secure recurring aftermarket revenue and data access.

Page last updated on: