Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

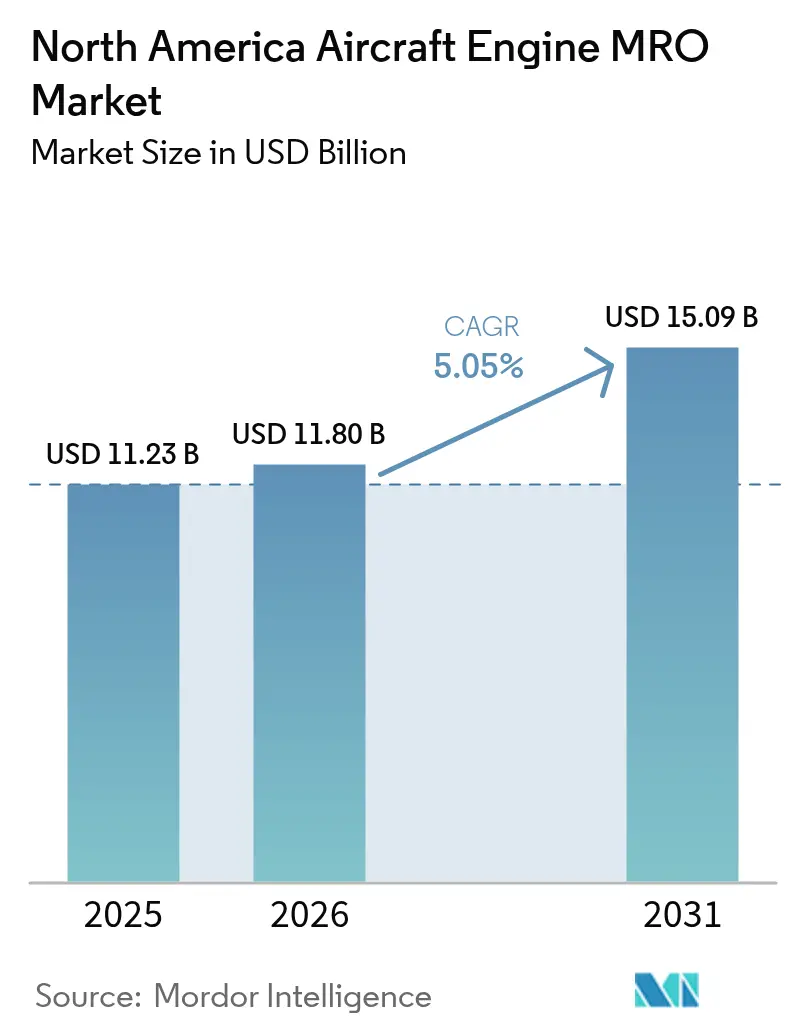

| Base Year Market Size (2025) | USD 11.23 Billion |

| Market Size (2026) | USD 11.8 Billion |

| Market Size (2031) | USD 15.09 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

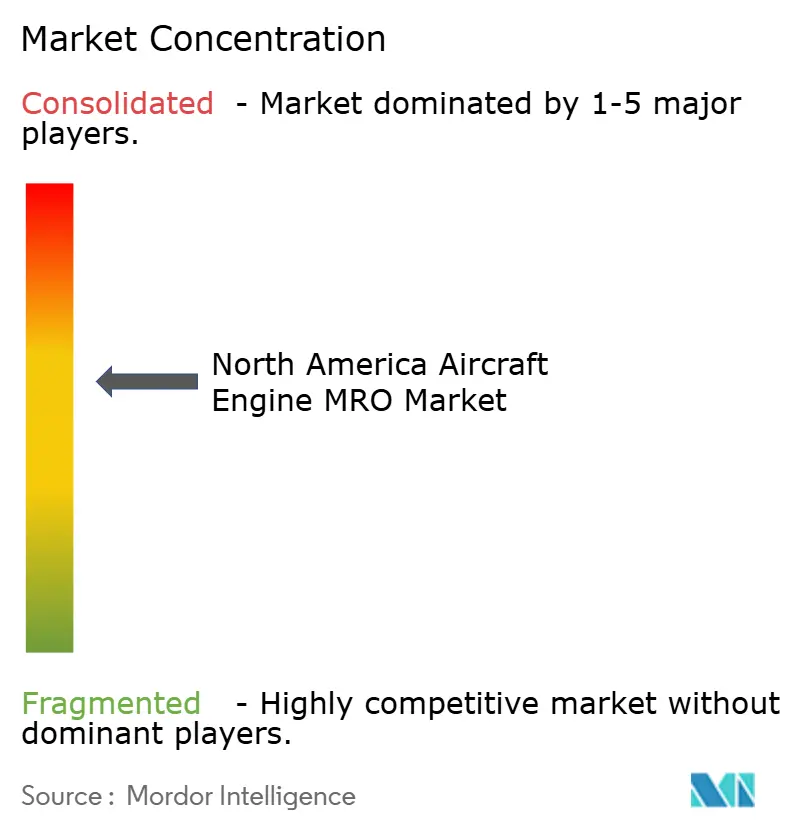

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Aircraft Engine MRO Market Analysis by Mordor Intelligence

The North America aircraft engine MRO market size was valued at USD 11.23 billion in 2025 and estimated to grow from USD 11.8 billion in 2026 to reach USD 15.09 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). Early-life durability challenges in LEAP and GTF programs, combined with heavy-maintenance cycles for aging CFM56 and V2500 fleets, and tightening FAA and ICAO emissions rules, are contributing to increased shop visit volumes. Supply chain delays for life-limited parts, however, are stretching turnaround times to 90 to 120 days, which limits capacity even as demand climbs. OEM control of proprietary data is tilting competitive power toward affiliated shops, while nearshoring trends are drawing new facilities to Mexico. Technician shortages and weather-related unscheduled inspections further complicate operational planning for airlines and MROs.

Key Report Takeaways

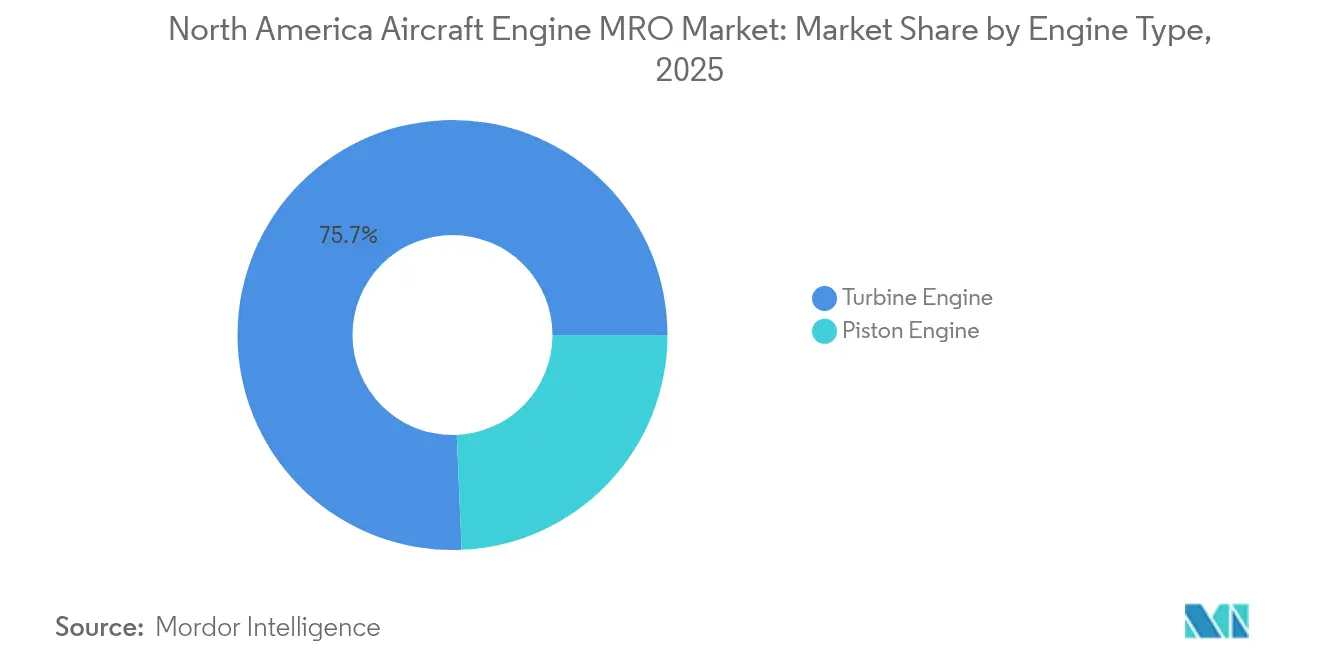

- By engine type, turbine powerplants led with 75.68% of the North America aircraft engine MRO market share in 2025, while piston-engine work remains marginal.

- By aviation segment, commercial aircraft generated 63.25% of 2025 revenue, while UAVs are forecasted to expand at a 7.3% CAGR through 2031.

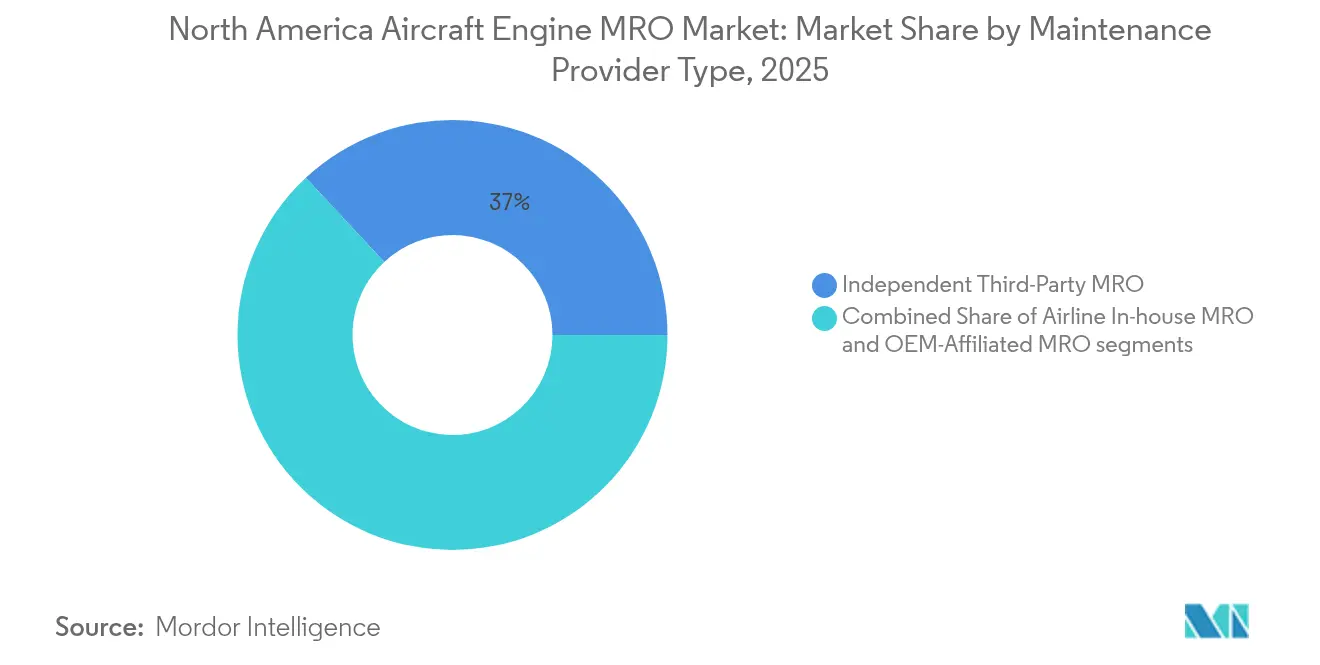

- By maintenance provider, independent third-party shops held 36.95% of 2025 revenue, and OEM-affiliated facilities are projected to grow at a 5.63% CAGR to 2031.

- By geography, the United States accounted for 85.74% of 2025 spending, while Mexico is advancing at a 6.18% CAGR, the fastest rate in the region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Aircraft Engine MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peak fleet aging driving increased heavy engine maintenance demand | +1.4% | United States, Canada | Medium term (2-4 years) |

| Expansion of OEM open-service agreements enhancing MRO shop accessibility | +0.9% | United States, Mexico | Short term (≤2 years) |

| Stricter FAA and ICAO emissions and noise regulations driving engine retrofit activity | +0.7% | United States, Canada | Long term (≥4 years) |

| Early-life reliability issues in LEAP and GTF engines increasing maintenance visits | +1.2% | United States, Canada, Mexico | Short term (≤2 years) |

| Limited availability of used serviceable material driving engine and module swap-outs | +0.6% | United States | Medium term (2-4 years) |

| Insurance-mandated post-severe weather inspections increasing unscheduled MRO events | +0.4% | US Gulf Coast, Southeast | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Peak Fleet Aging Driving Increased Heavy Engine Maintenance Demand

More than 3,200 US narrowbody aircraft delivered between 2010 and 2015 are now 12 to 15 years old, a milestone that triggers the first complete overhauls of their CFM56-7B and V2500-A5 engines. Approximately 6,400 power plants are expected to cycle through shops over the next four years, potentially crowding capacity and increasing lease-pool demand. Airlines are also postponing retirements because of OEM delivery delays, which compresses maintenance windows and lifts the strategic value of power-by-the-hour agreements. Larger, vertically integrated MROs can fund both legacy tooling and LEAP/GTF capability, widening the gap with smaller independents. Elevated shop volumes resulting from peak aging will continue to drive turbine-engine work as the main growth driver through 2028.

Expansion of OEM Open Service Agreements Enhancing MRO Shop Accessibility

Pratt & Whitney’s Certified Maintenance Provider program accepts 12 independent shops for PW1000G module work, while maintaining proprietary data control. GE Aerospace’s EngineWise analytics reduce unscheduled removals by 18 to 22%, but require airlines to share operational data that deepens OEM insight into fleet usage.[1]GE Aerospace, “EngineWise Predictive Maintenance,” geaerospace.com Safran’s modular LEAP repair option reduces the cost of single visits by up to 30% and drives more frequent, lower-value interventions that anchor long-term revenue. These selective partnerships expand geographic coverage and alleviate near-term capacity bottlenecks, directing more traffic into OEM-approved channels and accelerating vertical integration in the aftermarket.

Stricter FAA and ICAO Emissions and Noise Regulations Driving Engine Retrofit Activity

The FAA’s adoption of CORSIA metrics in 2024 requires older CFM56 and V2500 engines to undergo combustor upgrades, costing between USD 800,000 and USD 1.2 million each, to remain compliant.[2]International Civil Aviation Organization, “CORSIA Implementation Details,” icao.int New Annex 16 Chapter 14 noise rules add 180-220 labor hours per engine for acoustic-liner retrofits, further swelling shop workloads. Capital-rich network carriers are pursuing modifications to extend the life of their assets, while regional operators are accelerating fleet renewal, thereby shrinking the resale window for legacy power plants. Retrofit complexity boosts demand for engineering services with DER authority, a niche where seasoned independents can earn premium margins. Regulations, therefore, convert environmental mandates into sustained revenue in the aftermarket.

Early-Life Reliability Issues in LEAP and GTF Engines Increasing Maintenance Visits

Powder-metal contamination in PW1000G turbine disks grounded 600 to 700 engines in 2024 and shortened inspection intervals to 300 flight hours, a 70% reduction from plan. FAA directives on LEAP-1A/-1B ceramic shroud wear cut inspection cycles in half to 1,500 flights. These premature removals push spare-engine lease rates 40 to 50% higher and overwhelm shop bays, prompting airlines to pay premiums for accelerated turnarounds. Independent MROs that can mobilize rapid-response teams capture urgent business despite OEM data constraints. Moreover, the unplanned surge in visits offsets fuel-burn savings promised by new-generation propulsion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified aircraft maintenance technicians increasing turnaround times | −0.5% | Germany, UK, France | Medium term (2-4 years) |

| Supply chain delays in life-limited parts and forged components constraining MRO capacity | −0.7% | France, UK | Short term (≤ 2 years) |

| Rising weather-related engine and nacelle damage increasing maintenance complexity | −0.3% | EU | Long term (≥ 4 years) |

| OEM controlled data access limiting cost competitiveness for independent MROs | −0.4% | Germany, UK, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Aircraft Maintenance Technicians Increasing Turnaround Times

Retirements outpaced new FAA A&P certifications three-to-one in 2024, and the workforce is projected to shrink 6% by 2026.[3]U.S. Bureau of Labor Statistics, “Aircraft Mechanic Employment Outlook,” bls.gov Experienced engine specialists now command salaries of USD 85,000 to USD 110,000 in major hubs, 20 to 25% higher than in 2022, which squeezes margins for independents. Training pipelines require 18 to 30 months, so capacity cannot be ramped up quickly when demand spikes. Automation aids parts cleaning and documentation, yet core disassembly and rebuild tasks remain labor-intensive. Persistent staffing gaps lengthen shop cycles and force operators to defer non-critical work, tempering overall market growth despite robust demand.

Supply Chain Delays in Life-Limited Parts and Forged Components Constraining MRO Capacity

Lead times for titanium compressor disks and single-crystal blades doubled to 12-18 months in 2024 due to geopolitical disruptions in raw materials and foundry bottlenecks. Aging CFM56 fleets consume parts faster than reduced-rate production lines can replenish them, idling engines in “dock-awaiting-parts” status. Shops carry larger inventories, tying up working capital and risking obsolescence when fleets retire. Airlines resort to consignment pools or green-time leasing to secure availability, raising maintenance costs. Until supply chains normalize, component scarcity caps throughput, even where labor and bays are available, limiting the market’s near-term upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type Turbine Dominance Reflects Commercial Fleet Mix

Turbine engines generated 75.68% of the North America aircraft engine MRO market in 2025 and are forecasted to grow at a 5.99% CAGR to 2031. The North America aircraft engine MRO market size for turbine categories is therefore rising faster than overall expenditure, reflecting the heavy concentration of CFM56, LEAP, V2500, and PW1000G powerplants on narrowbody aircraft. High-thrust designs increase inspection frequency for advanced materials such as ceramic matrix composites, driving specialized repair demand that favors facilities with proprietary tooling and OEM data access.

Additive repair of turbine blades, as disclosed by GE Aerospace in 2024, reduces scrap rates and enables affiliated shops to increase throughput. Turboprop and turboshaft engines support regional airlines, offshore energy operations, and emergency medical services, where reliability takes precedence over cost. Piston powerplants serve flight training and general aviation; their more straightforward upkeep keeps most work at fixed-base operators rather than dedicated overhaul centers. Despite utilization gains in general aviation, piston activity accounts for a small portion of the North America aircraft engine MRO market.

By Aviation UAV Emergence Signals Propulsion Diversification

Commercial carriers commanded 63.25% of the North American aircraft engine MRO market in 2025, primarily driven by high-cycle narrowbodies that average 10 to 12 flight hours daily. Widebody engines, although fewer in number, require higher dollar outlays per visit, which balances value across fleet groups. Regional jet work is declining as airlines phase out 50-seat aircraft that no longer meet scope clause economics, trimming demand for PW1500G and CF34 engines within the forecast horizon.

UAVs are expanding at a 7.3% CAGR and represent the fastest-growing slice of the North America aircraft engine MRO market. Military reconnaissance drones currently drive the majority of the volume, but commercial logistics trials by parcel carriers promise new civil demand. MRO infrastructure remains sparse, giving early movers a competitive edge in field support and parts pooling. Military aviation remains significant due to the F-35 Pratt & Whitney F135's sustainment and Rolls-Royce AE 2100's support for C-130J transports, both of which require security-cleared facilities that OEMs typically dominate.

By Maintenance Provider OEM Affiliates Gain Ground

Independent third-party shops held 36.95% of 2025 revenue, but OEM-affiliated networks are advancing at 5.63% CAGR, overtaking independents in new long-term contracts. Control of digital engine health data enables Pratt & Whitney, GE Aerospace, and Safran to bundle analytics, parts, and labor into power-by-the-hour agreements, guaranteeing turnaround slots. Airlines favor budget certainty, even when fixed hourly rates exceed historic time-and-materials cost averages.

Independent providers defend their share by offering flexible pricing and faster slot allocation on legacy engines where data is less restricted. AAR Corp’s additive fan-blade repair, FAA-approved in 2024, shortens lead times from 90 days to 30 days. StandardAero’s August 2024 acquisition of Signature Aviation’s engine division lifted its turbofan throughput by 30%, improving economies of scale. Airline in-house MROs, such as Delta TechOps, leverage fleet proximity to minimize aircraft-on-ground days and increasingly accept third-party work to monetize capacity.

Geography Analysis

The United States accounted for 85.74% of the 2025 revenue in the North America aircraft engine MRO market. The Dallas, Atlanta, Miami, and Cincinnati anchor clusters of extensive facilities with deep supply networks. Peak fleet aging of CFM56 and V2500 engines drives shop bay utilization, while new PW1000G and LEAP reliability issues force airlines to seek rapid module-swap capability. High labor costs prompt some lower-margin work, such as light maintenance on older turboprops, to be outsourced to out-of-state or cross-border shops.

Mexico is rising fastest with a 6.18% CAGR through 2031 and is capturing turbine-component repairs for LEAP engines. Safran’s 2024 opening in Querétaro, along with GE and Pratt & Whitney satellite sites, benefits from skilled labor priced 40 to 50% below US averages. The USMCA pact eases the flow of cross-border parts, allowing Mexican shops to supply US airlines without incurring punitive duties. Universities and technical institutes, funded jointly with industry, graduate A&P-equivalent mechanics who receive bilingual training aligned with FAA Part 147 standards.

Competitive Landscape

The North America aircraft engine MRO market is moderately concentrated, wherein the top five entities, GE Aerospace (General Electric Company), Pratt & Whitney (RTX Corporation), Delta TechOps (Delta Air Lines, Inc.), Rolls-Royce Holdings plc, and StandardAero Aviation Holdings, Inc., account for the majority of the revenue. OEMs tighten their grip by bundling analytics, parts pooling, and guaranteed access to slots. Delta TechOps combines airline parentage with third-party contracts, forging a hybrid model that competes with independents and OEM affiliates alike.

Technology is the primary differentiator. GE’s EngineWise platform utilizes machine learning to identify anomaly trends and reduce unscheduled removals by 15-20%, thereby enhancing airline confidence in long-term service agreements. Pratt & Whitney’s Columbus expansion adds automated inspection cells that shave turnaround times by 20%. Rolls-Royce and Lufthansa Technik’s joint venture in Tulsa eliminates trans-Atlantic shipping costs for Trent work, thereby shortening widebody downtime.

Additive manufacturing reduces working-capital exposure. AAR Corp’s FAA-approved process lowers fan-blade repair cost by 40% and demonstrates how independents compete on innovation rather than volume. Digital capacity marketplaces reduce procurement friction, allowing smaller shops to monetize open bays when OEM centers experience overflow. Yet, technician shortages, raw material delays, and OEM data restrictions keep barriers high. The North America aircraft engine MRO market continues to reward providers that align capital with high-cycle fleet segments and invest in predictive analytics.

North America Aircraft Engine MRO Industry Leaders

Delta TechOps (Delta Air Lines, Inc.)

Pratt & Whitney (RTX Corporation)

GE Aerospace (General Electric Company)

StandardAero Aviation Holdings, Inc.

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Delta TechOps secured its first third-party LEAP-1B maintenance contract, delivering advanced engine support for Korean Air's B737 MAX fleet, marking a significant milestone in next-generation engine maintenance services.

- February 2025: WestJet and Lufthansa Technik signed a multi-billion-dollar agreement for aircraft engine maintenance, which includes a new repair facility in Calgary to enhance operational efficiency and support long-term technical services.

- February 2025: StandardAero signed a 15-year agreement with a major Middle Eastern airline to provide aftermarket services for CFM International LEAP turbofan engines. Its San Antonio, Texas, LEAP MRO facility will deliver engine and component repair, including LEAP performance restoration shop visits (PRSV) and continued time engine maintenance (CTEM), supporting the airline’s next-generation narrowbody aircraft fleet.

North America Aircraft Engine MRO Market Report Scope

Maintenance, repair, and overhaul (MRO) is one of the key activities in an aircraft's and its engines' lifecycle. The typically long operational lifetimes of aircraft necessitate performing MRO activities to maintain their longevity in the long run. Engine MRO involves the repair, servicing, or inspection of engines to ensure the safety and airworthiness of the aircraft in accordance with international standards.

The North America aircraft engine MRO market is segmented based on engine type, aviation, maintenance provider type, and geography. The market is segmented by engine type into turbine engines and piston engines. By aviation, the market is classified into commercial aviation, military aviation, general aviation, and unmanned aerial vehicles (UAVs). The scope of the study for the UAVs is limited to military applications only. By maintenance provider type, the market is categorized into airline in-house MRO, independent third-party MRO, and OEM-affiliated MRO. The report also covers the market sizes and forecasts for the North America aircraft engine MRO market in major countries in the region. For each segment, the market size is provided in terms of value (USD).

By Engine Type

| Turbine Engine | Turboprop Engine |

| Turbofan Engine | |

| Turboshaft Engine | |

| Turbojet Engine | |

| Piston Engine |

By Aviation

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Vehicles (UAVs) |

By Maintenance Provider Type

| Airline In-house MRO |

| Independent Third-Party MRO |

| OEM-Affiliated MRO |

By Geography

| United States |

| Canada |

| Mexico |

| By Engine Type | Turbine Engine | Turboprop Engine |

| Turbofan Engine | ||

| Turboshaft Engine | ||

| Turbojet Engine | ||

| Piston Engine | ||

| By Aviation | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military Aviation | Combat | |

| Transport | ||

| Special Mission | ||

| Helicopters | ||

| General Aviation | Business Jets | |

| Commercial Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| By Maintenance Provider Type | Airline In-house MRO | |

| Independent Third-Party MRO | ||

| OEM-Affiliated MRO | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America aircraft engine MRO market today?

The market is valued at USD 11.8 billion in 2026 and is projected to reach USD 15.09 billion by 2031, growing at a 5.05% CAGR.

Which engine type drives most maintenance spending?

Turbine powerplants account for 75.68% of 2025 spending and are forecast to expand further as CFM56, LEAP, and PW1000G fleets mature.

Why are OEM-affiliated MROs gaining share?

Control over diagnostic data and integrated parts supply lets OEM networks guarantee turnaround times, attracting power-by-the-hour contracts.

What is the fastest growing geographic market?

Mexico is advancing at a 6.18% CAGR due to nearshoring incentives, skilled labor, and proximity to US supply chains.

How is technician shortage affecting turnaround times?

Retirements and limited training throughput extend shop cycles to 90 to 120 days, prompting higher labor costs and deferred non-critical work.

What role do UAVs play in future MRO demand?

UAVs are the fastest growing aviation segment at a 7.3% CAGR, creating new propulsion support requirements across military and commercial operators.

Page last updated on: