Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 31.30 Billion |

| Market Size (2026) | USD 32.87 Billion |

| Market Size (2031) | USD 42.01 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aircraft MRO Market Analysis by Mordor Intelligence

The Europe aircraft MRO market size is expected to grow from USD 31.30 billion in 2025 to USD 32.87 billion in 2026 and is projected to reach USD 42.01 billion by 2031 at a 5.03% CAGR. Fleet demographics are tilting older across single-aisle families, which pushes more heavy checks and engine shop visits into the cycle as operators defer retirements due to OEM production backlogs. Line maintenance intensity is elevated by high-utilization models led by low-cost carriers that run tight ground schedules. Digital health monitoring platforms are scaling across European fleets, reducing unplanned events and helping providers monetize data-enabled services. Regulatory support from ReFuelEU and the EU ETS is driving increased demand for retrofit solutions, including winglet and sharklet kits, aerodynamic surface modifications, and engine performance upgrade packages. At the same time, post-Brexit certification challenges are redirecting heavy maintenance and retrofit installations to continental European facilities that comply with EASA standards.

Key Report Takeaways

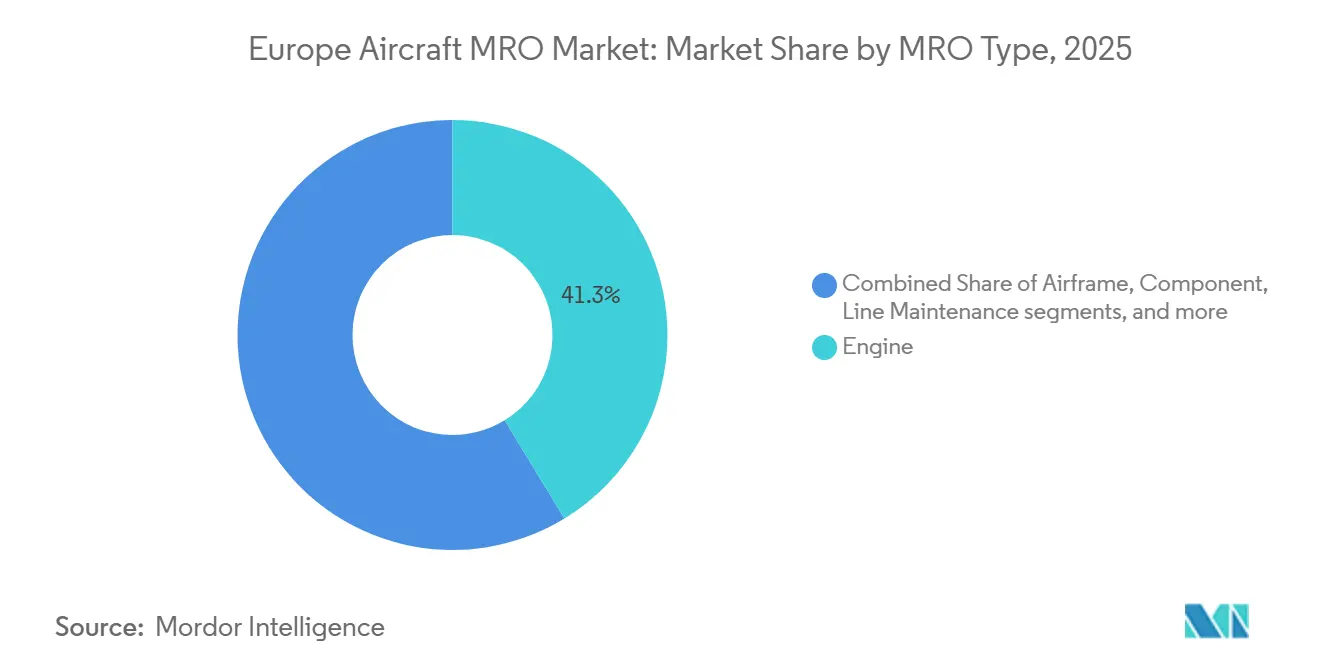

- By MRO type, engine overhaul led with a 41.28% revenue share of the Europe aircraft MRO market in 2025, and component repair and overhaul is forecast to expand at a 6.01% CAGR through 2031.

- By aircraft type, fixed-wing platforms captured a 95.45% share of the Europe aircraft MRO market in 2025, and rotary-wing MRO is projected to grow at a 5.99% CAGR through 2031.

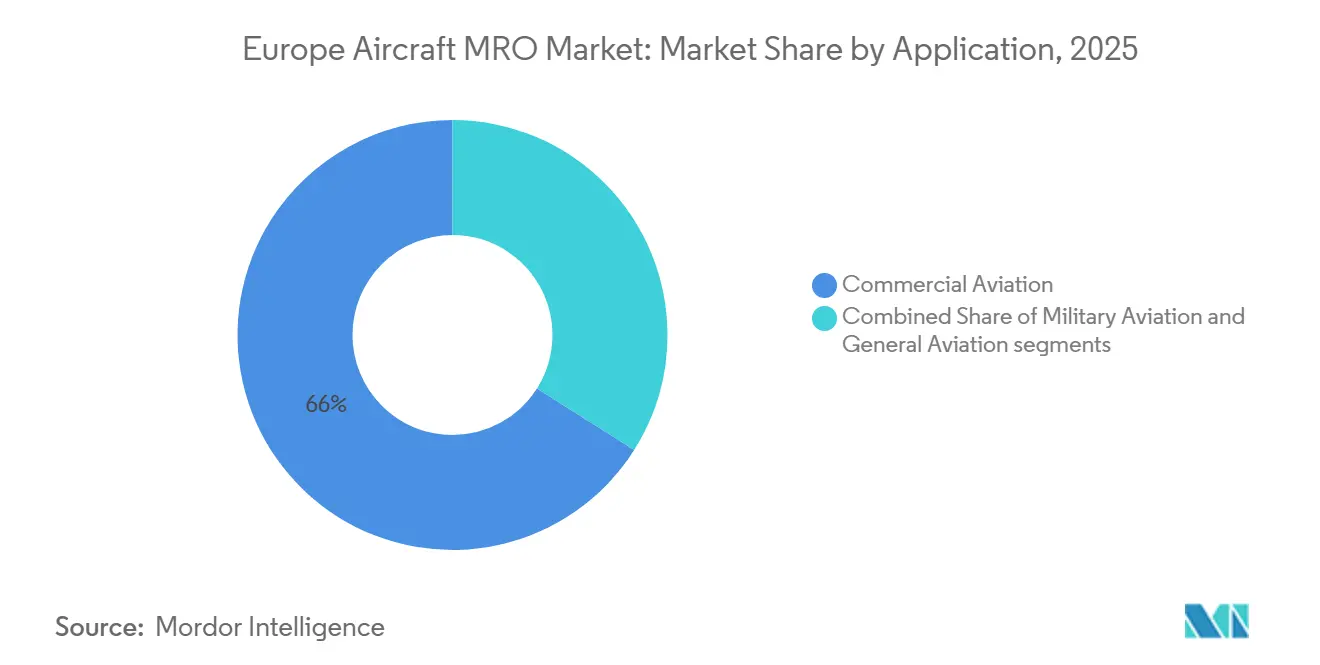

- By application, commercial aviation accounted for a 66.02% share of the Europe aircraft MRO market in 2025, and military aviation recorded the fastest expansion at a 5.83% CAGR through 2031.

- By service provider, OEM-affiliated facilities secured a 45.60% share of the Europe aircraft MRO market in 2025, and independent third-party shops are expected to grow at a 5.62% CAGR through 2031.

- By geography, Germany led with a 26.30% share of the Europe aircraft MRO market in 2025, and Italy showed the highest growth at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Aircraft MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing volume of ageing single-aisle aircraft entering heavy maintenance cycles | +0.9% | Global, with early gains in Germany, France, UK core hubs, Poland and Portugal absorbing overflow capacity | Medium term (≤ 2 years) |

| High fleet utilization rates among low-cost carriers driving service demand | +0.7% | National, concentrated in Ireland, UK, Hungary with spillovers across secondary European airports | Short term (≤ 2 years) |

| Adoption of predictive maintenance and new data monetization models | +0.5% | APAC core development with EU adoption through OEM platforms in Germany and France, concentrated in tech-advanced MROs | Long term (≥ 4 years) |

| Incentives for sustainability-driven aircraft retrofits and modifications | +0.4% | EU-wide regulatory push with early moves in France, Germany, Netherlands | Medium term (2-4 years) |

| Reallocation of heavy maintenance work within continental Europe post-Brexit | +0.3% | Regional within Europe, gains in Germany, Poland, Portugal, Estonia with reduced UK competitiveness for EU-registered fleets | Short term (≤ 2 years) |

| Expansion of multi-national military aircraft maintenance depots under EU funding programs | +0.5% | Pan-European with focus in Germany, Italy, and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Volume of Ageing Single-Aisle Aircraft Entering Heavy Maintenance Cycles

The market is entering a phase in which a significant number of older A320ceo and B737NG units require more frequent, capital-intensive heavy maintenance checks, straining base maintenance capacity during peak seasons. Backlogs at Airbus and Boeing keep operators flying older airframes, which keeps C and D checks elevated until new deliveries arrive in larger numbers later in the decade. Continental providers are expanding to absorb this peak load, illustrated by Lufthansa Technik’s multi-year build-out in Portugal to serve component and engine-related repairs for European fleets. Cross-border partnerships are also scaling engine capabilities to absorb narrowbody demand, such as the GE Aerospace and Lufthansa Technik joint venture that targets LEAP-family shop visits. The combination of older fleets and sustained utilization patterns supports high hangar occupancy across key hubs, prompting providers to invest in new lines and parts-repair capabilities to optimize turnaround.

High Fleet Utilization Rates Among Low-Cost Carriers Driving Service Demand

Low-cost carriers (LCCs) operate dense schedules that compress maintenance intervals and increase on-wing support demand at secondary airports. In 2024, Ryanair achieved exceptionally high daily utilization across its all-B737 fleet, supported by 3,500 daily flights. This operational intensity increased the frequency of line maintenance events, emphasizing the importance of mobile maintenance teams and rapid component swaps to minimize AOG risk.[1]Source: Ryanair, “Annual Report 2024,” Ryanair, investor.ryanair.com The market benefits from these operating models because distributed line operations require certified support at many outstations, which favors independents with strong regional networks. Engine-related groundings can disrupt these patterns when supply chains tighten, so carriers hedge by pooling spares and contracting AOG support that enables quick recovery. As LCCs expand capacity over the decade, line checks and light-base events should move in tandem, supporting steady staffing and parts-pooling programs among providers.

Adoption of Predictive Maintenance and New Data Monetization Models

Predictive maintenance has moved from pilots to scaled deployment on European fleets through OEM platforms and airline-developed systems. Airbus Skywise and Lufthansa Technik’s AVIATAR aggregate health data and maintenance histories to support early fault detection, reducing unplanned removals and improving shop loading.[2]Source: Airbus, “Skywise Platform,” Airbus, airbus.com Airline-affiliated providers are productizing these capabilities, offering scheduling and analytics services to external customers as software subscriptions or bundled service enhancements. As more aircraft stream data to centralized platforms, MRO providers can match parts provisioning and workcards to predicted events, reducing waste and stabilizing turnaround time. The market achieves greater structural efficiency through this shift, as providers minimize nonproductive time, airlines enhance aircraft availability, and major platforms leverage large-scale insights.

Incentives for Sustainability-Driven Aircraft Retrofits and Modifications

EU climate policy is reshaping investment pipelines, as sustainable aviation fuel blending mandates and rising carbon costs improve the payback for aerodynamic and engine-efficiency upgrades. The ReFuelEU regulation sets binding SAF blend shares that increase over the course of mid-century. By 2026, aviation's inclusion in the EU ETS will require airlines to purchase all allowances, underscoring the importance of fuel-burn reduction strategies such as retrofit kits and SAF blending. European carriers have adopted retrofit kits that reduce drag and improve time-on-wing, thereby sustaining modification lines for narrowbody and widebody aircraft. Program funding through the Clean Aviation Joint Undertaking accelerates technology development for next-generation propulsion, which, over time, will feed certification-driven retrofit projects to improve efficiency. Green finance rules under the EU taxonomy recognize qualified low-emission practices, which help providers secure better capital terms to upgrade hangars and adopt solvent-free processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of licensed maintenance technicians and rising labor costs | -0.7% | Global, with acute effects in Western Europe and rising constraints in Eastern Europe over time | Short term (≤ 2 years) |

| Persistent supply chain constraints for critical engine spare parts | -0.6% | Global, with EU-specific pressure in forgings and LEAP and CFM56 LLP supply | Medium term (2-4 years) |

| Stricter regulations on VOC emissions in aircraft painting and solvent use | -0.3% | EU-wide with outsized impact on smaller operators | Medium term (2-4 years) |

| Increased compliance costs for EASA Part-IS cybersecurity requirements | -0.5% | EASA-regulated organizations across Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Licensed Maintenance Technicians and Rising Labor Costs

Workforce availability remains the most persistent operational constraint across European line and base maintenance. Industry outlooks indicate robust global demand for new aviation maintenance technicians through 2044, with Europe accounting for a significant share.[3]Source: Boeing, “Pilot and Technician Outlook 2024–2044,” Boeing, boeing.com The training pipeline and licensing timelines slow replenishment, leaving providers with open requisitions and longer recruitment cycles for specialized engine skills. Airline-affiliated and OEM-affiliated MROs expand academy programs and apprenticeships to grow talent internally, a strategy that requires upfront investment but builds long-term capacity. Providers also deploy inspection automation and augmented guidance to improve productivity per technician while maintaining regulatory standards for sign-off authority.

Persistent Supply Chain Constraints for Critical Engine Spare Parts

Engine fleets with high utilization face delays when powder-metal or forging issues constrain the availability of life-limited parts, lengthening shop-visit cycles. Where lead times are extended, airlines and MROs rely more on pooled assets and used serviceable material, supported by teardown programs to salvage high-value components. Global industry associations have estimated multi-billion-dollar system-wide costs from knock-on effects, such as spare-engine leases, which keep turnaround times above pre-crisis norms. Engine OEMs and their networks continue to add repair routes and advanced component restoration methods, including additive processes that rebuild features on hot-section parts. Over time, the expansion of certified repair capabilities helps reduce AOG exposure and normalizes visit durations across narrowbody and widebody engines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By MRO Type: Component Work Outpaces Engine Overhaul Growth

Engine overhaul captured 41.28% of the market share in 2025, which reflects the technical depth and capital intensity of turbofan maintenance. The market benefits from engine MRO pricing power, driven by proprietary manuals and tooling. At the same time, component repair grows faster because more specialized shops serve it with multi-OEM approvals. The Europe aircraft MRO market for component repair is projected to expand at a 6.01% CAGR through 2031, which is the fastest among service types in this segmentation. Predictive analytics increases the velocity of component rotations by flagging failure risks before they trigger AOG events, which helps airlines avoid disruptions while increasing planned shop throughput. Modifications and upgrades add incremental growth as operators pursue efficiency kits, cabin improvements, and connectivity retrofits that deliver measurable returns under carbon pricing.

Airframe heavy checks constitute a significant portion of the market, as older narrowbody aircraft require extensive structural maintenance and corrosion control. Line maintenance remains essential because high-frequency operations compress intervals, which keeps distributed stations busy across Europe’s secondary and tertiary airports. Additive manufacturing standards continue to advance, enabling the quicker production of non-critical parts and reducing lead times for repairs that would otherwise wait for long-lifecycle components. Engine performance upgrades in cooperation with OEMs deliver small but meaningful fuel savings and extended time-on-wing, which are attractive amid rising carbon costs. As shops standardize digital workflows from induction to release to service, they unlock capacity that keeps turnaround predictable during peak seasons.

By Aircraft Type: Rotary-Wing Gains Traction Amid Offshore Energy Demand

Fixed-wing fleets account for around 95.45% of the market share, with single-aisle platforms underpinning most intra-European connectivity and sustaining continuous engine, airframe, and component workloads. Widebody engines and composites command higher pricing and require specialist tooling, which concentrates work in hubs with security-cleared teams and OEM-trained talent. The market for rotary-wing platforms is poised to grow faster at a 5.99% CAGR as offshore wind operations and emergency medical services expand utilization in Northern Europe and the North Sea. Helicopter programs are also integrating sustainable fuels for training and testing missions, which aligns rotary-wing operations with EU climate objectives. These patterns support a gradual increase in rotorcraft maintenance demand, even as fixed-wing remains the largest source of absolute MRO spend.

Rotorcraft maintenance introduces constraints different from those in fixed-wing work, including component obsolescence and gearbox lead times that shape fleet renewal decisions. Additive repairs and new certification pathways can ease pressure on long-lead items once standards and quality controls align with aviation-grade requirements. Search and rescue and medical operations are sensitive to aircraft availability, so predictive and condition-based programs that reduce unplanned downtime are especially valuable in this category. As wind farm construction scales in the North Sea and the Baltic, operators plan flight hours and inspection intervals, increasing demand for line and base events tied to mission profiles. The market is expected to experience steady growth in utility-driven rotorcraft, complementing the scale of single-aisle operations across the region.

By Application: Military Platforms Lead Growth Trajectory

Commercial aviation accounted for 66.02% of the market in 2025, reflecting the breadth of airline fleets and the regulatory cadence governing inspections and component replacements. Passenger carriers maintain in-house and partner networks to handle engine, airframe, and component cycles, while cargo providers extend airframe life through conversions and refurbishments. The market size benefits from commercial volume; however, engine supply constraints may lead to fluctuations in shop intake and release schedules. As low-cost carriers add capacity through the cycle, line events rise, which sustains predictable demand for outstation coverage. Predictive maintenance reduces unplanned disruptions in this segment, helping airlines increase aircraft availability and supporting stable provider utilization.

Military aviation shows the highest growth rate, with a 5.83% CAGR through 2031, driven by multi-year European security funding and coordinated platform sustainment. EU-level programs and national budgets underpin engine and avionics depot workloads for Eurofighter Typhoon, Rafale, A400M, and rotary fleets that require specialized capabilities. OEMs and primes use digital maintenance tools in defense programs, improving availability and compressing turnaround times for mission-critical assets. Long-term service arrangements provide visibility into staffing and tooling, reducing volatility compared to commercial cycles. This combination positions defense as a strategic safeguard for providers, enabling them to meet security and sovereign capability requirements.

By Service Provider: Independent Shops Retain Share Despite OEM Push

OEM-affiliated facilities held the largest share at 45.60% in 2025 as engine OEMs deepened vertical integration through captive networks and long-term service agreements. Independents are expected to post the fastest growth at a 5.62% CAGR through 2031 by leveraging multi-OEM certifications and competitive pricing across airframes and components. OEMs continue to invest in new or expanded European service centers for LEAP-family engines and other high-demand platforms, which raises in-region capacity to address long backlogs. Airline-affiliated MROs combine fleet operations knowledge with third-party work that monetizes digital tools developed for their own aircraft. This three-way dynamic supports a healthy mix of price competition, captive high-value work, and operationally tuned turnarounds in the Europe aircraft MRO market.

Independents expand footprints through targeted M&A and partnerships that add approvals, hangar slots, and access to new geographies. OEM-affiliated networks prioritize engine MRO scale due to high lifecycle economics, while independents defend share by replicating PBH-style component support, pooling, and guaranteed TAT. Airline providers position digital maintenance scheduling and predictive analytics as differentiators to win and retain external customers. Across this structure, cybersecurity and environmental compliance increase fixed costs that reward scale, which may encourage further consolidation from 2025 to 2027. As a result, the market continues to consolidate at the edges while sustaining a competitive core across engine, airframe, and component work.

Geography Analysis

Germany held a 26.30% market share in 2025 and maintained a pipeline of investments in engine and digital maintenance platforms. The country’s ecosystem includes OEM engine partners and airline-affiliated shops that deploy predictive maintenance at scale, which supports both commercial and defense workloads. Cross-border capacity expansions have been implemented to handle narrowbody engines, including a Poland-based joint venture overseen by German technical leadership. Rolls-Royce has continued to invest across European sites to support Trent-family MRO, which augments Germany’s presence in premium engine work. The combination of domestic capability and nearshore cost-optimized capacity keeps Germany central in the market.

France remains a top-tier hub, anchored by civil-engineering and landing-systems leaders and an airline-affiliated MRO that has commercialized AI-enabled scheduling. Safran has committed to a significant in-house maintenance scale-up for LEAP engines, which places France at the center of narrowbody aftermarket development and training. Integrated aerospace clusters around Toulouse deepen competencies in avionics, composites, and flight-control repair, supporting both OEM and aftermarket services. Military sustainment programs for Rafale are improving efficiency by adopting commercial practices such as predictive diagnostics and digitized spares, creating a blueprint for dual-use innovation. This concentration of industrial and airline capabilities supports premium pricing in complex work and stabilizes provider utilization in the market.

Italy posts the highest growth rate at a 6.18% CAGR through 2031 on the back of new airline activity and defense sustainment anchored by joint-strike fighter participation. The Cameri facility provides assembly and sustainment for advanced fighters, attracting allied workloads and establishing Italy as a southern European hub for security-driven maintenance. Engine repair activity across Iberia and the broader Mediterranean adds collaboration and niche turboprop MRO, complementing narrowbody work. The United Kingdom remains a premium engine and military sustainment hub despite certification friction that has shifted some EU-registered work to the continent. Spain’s engine repair capabilities continue to expand within OEM-authorized networks, supported by national champions that add training programs for gas turbine technicians. This geographic pattern supports a layered market with premium engineering hubs in Germany, France, and the UK, fast-growing southern capacity in Italy and Spain, and cost-optimized throughput in select Central and Eastern European locations.

Competitive Landscape

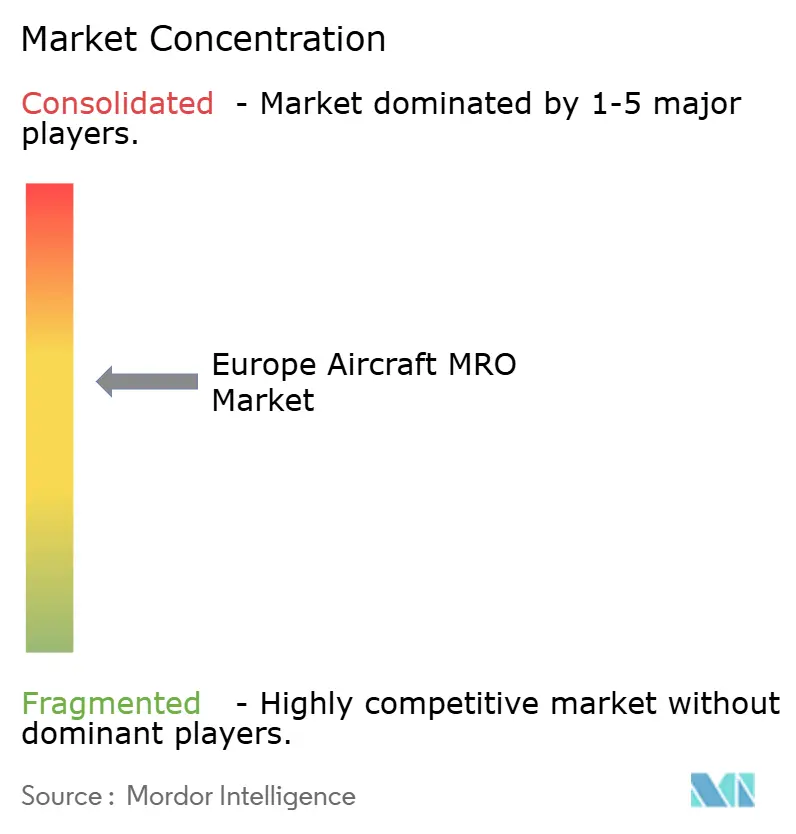

The Europe aircraft MRO market is semi-consolidated, with leading positions held by airline-affiliated providers, OEM-affiliated networks, and diversified independents. OEM strategies prioritize lifecycle economics and data-enabled agreements that tie engine performance to maintenance outcomes, which increases captive work. Airline providers combine operational knowledge with predictive and scheduling tools that create measurable efficiency for external customers. Independents lean on multi-OEM certifications, pooled spares, and price flexibility to compete in airframe and component segments where proprietary data is less controlling. This structure keeps competition active across price, turnaround, technology capability, and geographic coverage.

Strategic investments are reshaping the engine aftermarket across Europe. Safran announced a multi-year program to expand and upgrade European capacity, with a focus on LEAP-family engines that dominate narrowbody order books. GE Aerospace and Lufthansa Technik inaugurated a Poland-based joint venture to perform LEAP overhauls with technical oversight tied back to Germany. Rolls-Royce added capacity in Continental Europe to support Trent engines, which diversifies geography while retaining deep UK engineering expertise. Airline-affiliated providers also launched AI-enabled scheduling platforms that they license to external fleets, which extends digital value beyond their own aircraft. These moves point to continued scaling of engine capabilities and digital work orchestration.

Compliance and sustainability are now central to competitive differentiation. EASA’s Part-IS elevates cybersecurity baselines across maintenance and continuing airworthiness organizations, which rewards providers with mature ISMS and 24x7 monitoring. Environmental regulations on VOCs and E-participation in the US ETS provide investments in water-based paint systems, solvent recovery, and renewable power that reduce emissions and appeal to airline customers pursuing Scope 3 goals. Clean Aviation funding and EU taxonomy rules support providers that advance lower-emission processes and energy-efficient test cells. As compliance costs rise, scale benefits favor platforms with multiple sites, robust governance, and shared security and environmental reporting services. These dynamics suggest sustained consolidation at the margins and greater emphasis on digital and green capabilities within the Europe aircraft MRO market.

Europe Aircraft MRO Industry Leaders

Lufthansa Technik AG

Rolls-Royce Holdings plc

SR Technics Switzerland Ltd.

Airbus SE

Air France Industries KLM Engineering & Maintenance (Air France-KLM Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ryanair signed a Memorandum of Understanding (MoU) with CFM International for long-term material services covering 2,000 CFM56 and LEAP engines, reflecting a strategic initiative to optimize maintenance operations and reduce reliance on external providers. This agreement underscores the airline’s commitment to fleet reliability and scalability, aligning with its broader growth strategy and reinforcing its competitive edge in the aviation market.

- November 2025: Boeing's multi-year agreement with Lufthansa Technik Defense for the sustainment of the German Navy's P-8A Poseidon fleet marks a strategic collaboration in the defense aviation sector. This partnership leverages Lufthansa Technik's extensive expertise in B737 maintenance, ensuring operational efficiency for the German Navy's maritime patrol capabilities. The agreement underscores the growing demand for specialized MRO services in military aviation, highlighting the importance of robust support frameworks for advanced aircraft systems.

Europe Aircraft MRO Market Report Scope

Aircraft MRO is the process of inspecting, servicing, or restoring airframes, engines, systems, and components to keep aircraft compliant with Asia-Pacific safety and airworthiness standards. The study of the aircraft MRO market encompasses all scheduled and unscheduled line checks, heavy airframe visits, engine shop work, component repairs, and modification programs performed on fixed-wing and rotary-wing platforms across commercial, military, and general aviation fleets operating in the region. Component-level tasks, such as avionics calibration, landing gear overhauls, and cabin retrofits, are included within the market scope.

The Europe aircraft MRO market is segmented by MRO type, aircraft type, application, service provider, and geography. By MRO type, the market is segmented into engine, airframe, component, line maintenance, and modifications and upgrades. By aircraft type, the market is segmented into fixed-wing and rotary-wing aircraft. By application, the market is segmented into commercial aviation, military aviation, and general aviation. By service providers, the market is segmented into airline-affiliated MROs, independent third-party MROs, OEM-captive MROs, and military depots. The report also covers the market sizes and forecasts for five countries across the region. For each segment, the market size is provided in terms of value (USD).

By MRO Type

| Engine |

| Airframe |

| Component |

| Line Maintenance |

| Modifications and Upgrades |

By Aircraft Type

| Fixed-wing |

| Rotary-wing |

By Application

| Commercial Aviation | Passenger |

| Cargo/Freighter | |

| Military Aviation | |

| General Aviation |

By Service Provider

| Airline-Affiliated MROs |

| Independent Third-Party MROs |

| OEM-Affiliated MROs |

| Military Depots |

By Geography

| United Kingdom |

| Germany |

| Italy |

| France |

| Russia |

| Rest of Europe |

| By MRO Type | Engine | |

| Airframe | ||

| Component | ||

| Line Maintenance | ||

| Modifications and Upgrades | ||

| By Aircraft Type | Fixed-wing | |

| Rotary-wing | ||

| By Application | Commercial Aviation | Passenger |

| Cargo/Freighter | ||

| Military Aviation | ||

| General Aviation | ||

| By Service Provider | Airline-Affiliated MROs | |

| Independent Third-Party MROs | ||

| OEM-Affiliated MROs | ||

| Military Depots | ||

| By Geography | United Kingdom | |

| Germany | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe aircraft MRO market?

The Europe aircraft MRO market size is expected to grow from USD 31.30 billion in 2025 to USD 32.87 billion in 2026 and is projected to reach USD 42.01 billion by 2031 at a 5.03% CAGR.

Which service type leads and which grows the fastest in Europe?

Engine overhaul leads with 41.28% revenue share in 2025, while component repair and overhaul is the fastest-growing at a 6.01% CAGR through 2031.

How are regulations shaping Europe’s maintenance demand patterns?

ReFuelEU and the EU ETS increase the value of efficiency retrofits and maintenance upgrades, while EASA Part-IS raises cybersecurity requirements that favor scaled providers with mature ISMS.

Which countries are most influential in Europe’s MRO ecosystem?

Germany leads on share with a deep airline-OEM ecosystem, France anchors LEAP aftermarket development and digital scheduling, the UK remains strong in premium engine work, and Italy posts the fastest growth rate through 2031.

How are low-cost carriers affecting maintenance activity in Europe?

High aircraft utilization compresses check intervals and drives line maintenance at secondary airports, which sustains demand for mobile teams and pooled components to reduce AOG exposure.

What digital capabilities are most impactful for MRO providers today?

Predictive maintenance platforms such as Airbus Skywise and Lufthansa Technik’s AVIATAR help reduce unplanned events, improve turnaround predictability, and create new analytics revenues when offered to third parties.

Page last updated on: