Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

| Market Size (2026) | USD 10.55 Billion |

| Market Size (2031) | USD 13.35 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Aircraft MRO Market Analysis by Mordor Intelligence

The Middle East aircraft MRO market size stands at USD 10.55 billion in 2026 and is projected to reach USD 13.35 billion by 2031, reflecting a 4.82% CAGR over the forecast period. The acceleration of fleet expansion by GCC flag carriers, ongoing airport privatization programs, and the rapid induction of CFM LEAP and Pratt & Whitney GTF engines underpin a positive growth outlook for the Middle East aircraft MRO market. Independent third-party shops are scaling their capacity at a faster pace than airline-affiliated facilities, aided by policy reforms that unlock on-airport land and lower capital-cost structures. Digital-twin platforms are reducing turnaround times by up to 20%, enabling shops to process more airframes per bay each year. Meanwhile, modular component-repair strategies limit aircraft-on-ground days and redistribute budgets from rotable inventory to repair labor. Engine-shop concentration, skilled-technician shortages, and geopolitical uncertainty in the Levant temper growth but do not outweigh the structural demand drivers that keep the Middle East aircraft MRO market on a steady upward trajectory.

Key Report Takeaways

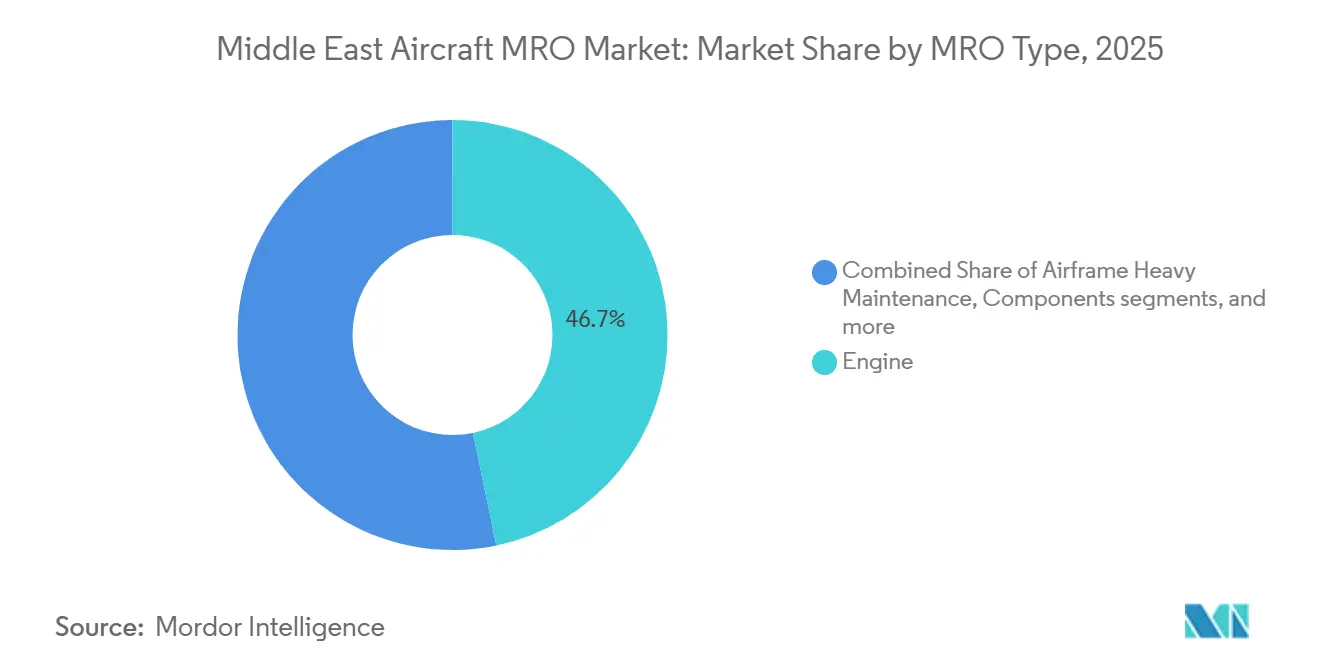

- By MRO type, engine maintenance led with 46.73% of 2025 revenue, while component repair is forecasted to expand at a 5.38% CAGR through 2031.

- By aircraft class, fixed-wing platforms held 91.14% of 2025 spending, yet rotary-wing work is advancing at a 6.65% CAGR to 2031.

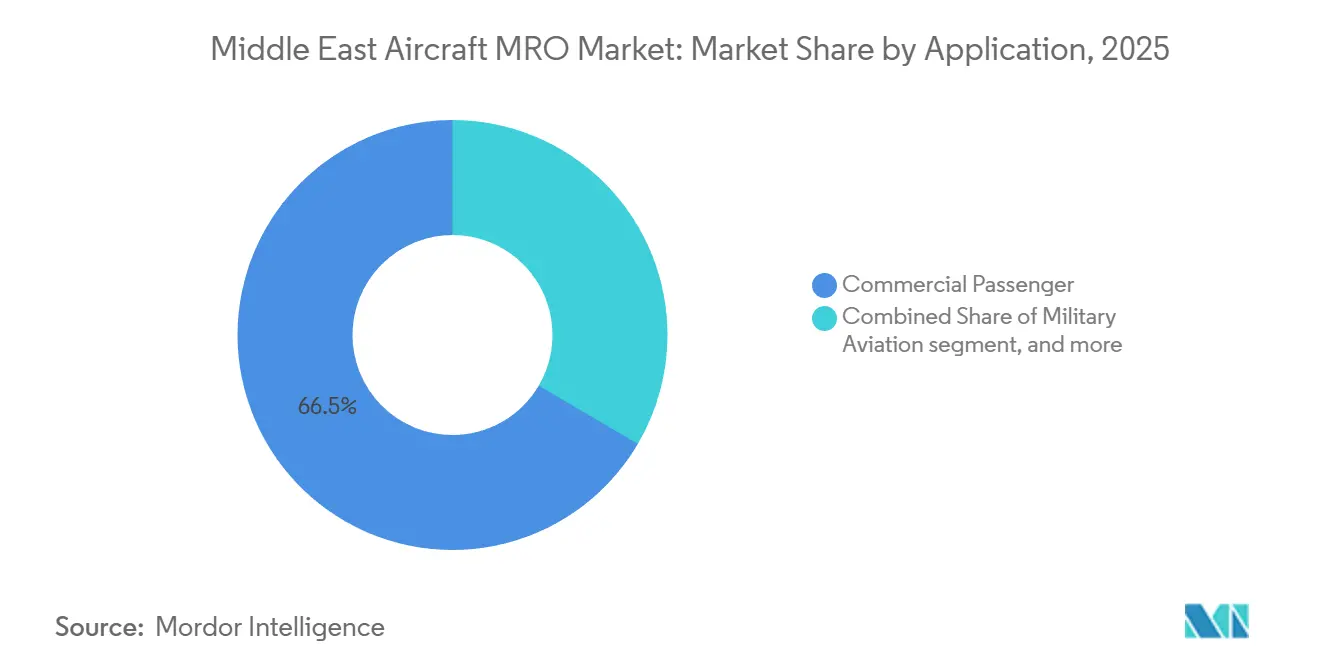

- By application, commercial passenger operations accounted for 66.54% of 2025 demand, and cargo freighter activity is growing at a 5.19% CAGR through 2031.

- By service provider, airline-affiliated shops captured 50.17% of the 2025 spending, but independent third-party facilities are projected to rise at a 6.58% CAGR through 2031.

- By geography, Turkey secured 33.25% of the 2025 revenue, whereas Saudi Arabia is the fastest-growing market, with a 4.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Aircraft MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National-carrier fleet expansion programs in GCC boosting heavy-check demand | +1.2% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Privatization of Saudi and UAE airports creating third-party MRO opportunities | +0.9% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Ramp-up of LEAP and GTF engine fleets necessitating new engine shops | +1.1% | GCC core, Turkey, Egypt | Medium term (2-4 years) |

| Digital twin adoption reducing turnaround time and increasing shop-visit volume | +0.7% | UAE, Saudi Arabia, Turkey | Short term (≤ 2 years) |

| Emergence of LCCs driving line-maintenance outsourcing | +0.5% | Saudi Arabia, UAE, Kuwait | Short term (≤ 2 years) |

| Military offset policies pushing OEMs to localize component repair | +0.6% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National-Carrier Fleet Expansion Programs in GCC Boosting Heavy-Check Demand

Saudia ordered 105 A320-family aircraft in 2024 and 39 B787-9s in 2025, aiming for a 200-unit fleet by 2030; these deliveries compress heavy-check intervals and inject an estimated 120 additional airframe checks per year into the Middle East aircraft MRO market. Emirates’ record order for 90 B777-8 freighters in 2024 will require two dedicated widebody bays at a USD 950 million complex coming online at Dubai World Central in 2027. Qatar Airways adjusted the C-check frequency for its A350-1000s and B777-9s from 18 months to 14 months in 2025 and awarded overflow contracts to Turkish Technic and Joramco, thereby expanding regional third-party opportunities. Etihad Engineering’s Al Massar program aims to double revenue by integrating newly acquired Abu Dhabi Aviation line stations, which collectively increase widebody throughput by 25%.

Privatization of Saudi and UAE Airports Creating Third-Party MRO Opportunities

Saudi Arabia’s General Authority of Civil Aviation framework now permits long-term land leases for independent hangars, ending the historic monopoly of Saudia Technic and reallocating roughly 15% of heavy-check volume toward non-airline shops by 2030. The Public Investment Fund’s USD 1.5 billion infusion into Jeddah’s MRO Village extends 10 new bays to third-party operators scheduled for completion in 2027. In the UAE, Mubadala’s Sanad logged AED 2.3 billion (USD 626.28 million) revenue in H1 2024 after onboarding Asiana Airlines and European lessors under an expanded engine-maintenance contract. Dubai Airports Authority has allocated 1.2 million square feet at Dubai South to IER MRO Industries, whose USD 1.3 billion facility is expected to feature twin LEAP-capable test cells by 2027.[1]Ali Mansoor, “Dubai Airport Land Opens to Private MROs,” arabianbusiness.com

Ramp-Up of LEAP and GTF Engine Fleets Necessitating New Engine Shops

CFM LEAP-1A/1B and Pratt & Whitney GTF powerplants will propel roughly 60% of narrowbody deliveries across the region by 2028, pushing the installed base beyond 1,200 engines and concentrating engine work among Sanad, Emirates Engineering, and Turkish Technic.[2]Ben Sammut, “LEAP Engines Push Capacity Limits,” aviationweek.com Sanad inducted 160 LEAP engines during 2024 and activated a fourth test cell calibrated for 32,000 lbf thrust ratings. GE invested USD 10 million to upgrade tooling in Dubai and Doha service centers, cutting on-wing time for LEAP fan-blade exchanges by 12%. Turkish Technic’s January 2025 contract with IndiGo covers 150 LEAP engines and positions Istanbul as a South Asia and Middle East hub.

Digital Twin Adoption Reducing Turnaround Time and Increasing Shop-Visit Volume

Emirates Engineering’s collaboration with Boeing introduced fleet-wide digital twins in 2024, which predict component failures 30 days in advance with 85% accuracy, reducing the average C-check turnaround time to 38 days and increasing annual bay utilization by 18%. Etihad Engineering integrated Airbus Skywise data into its workflows, resulting in a 22% increase in shop-visit throughput in 2025. Qatar Airways Technic equipped 120 aircraft with predictive-maintenance sensors, cutting unscheduled removals by 18%. Lufthansa Technik Middle East applied similar analytics to Saudia’s component-support contracts, deferring 12% of shop visits through condition-based monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-technician shortage elevating labor costs in Dubai and Riyadh | -0.8% | UAE, Saudi Arabia | Short term (≤ 2 years) |

| Prolonged redelivery delays at OEM shops limiting aftermarket share | -0.6% | GCC core, Turkey | Medium term (2-4 years) |

| Political instability in the Levant impacting widebody utilization rates | -0.3% | Jordan, Lebanon | Medium term (2-4 years) |

| High capex for engine test cells deterring independent entrants | -0.5% | Regional, Saudi Arabia, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Technician Shortage Elevating Labor Costs in Dubai and Riyadh

Vacancy rates for EASA B1/B2 mechanics reached 22% in Dubai in 2025, pushing monthly wages above USD 7,000 and squeezing independent shop margins by 200 basis points.[3] Etihad Engineering’s tri-party academy with GE and Lufthansa Technik will graduate its first 200 Emirati technicians in 2027, leaving a near-term supply gap. Saudi training programs enroll 150 students annually, yet fewer than 40% secure GCAA licenses within two years, compounding wage inflation. Military rotary-wing specialists in the UAE command a monthly salary of USD 7,400, reflecting the scarcity of their expertise.

Prolonged Redelivery Delays at OEM Shops Limiting Aftermarket Share

Pratt & Whitney GTF overhaul times exceeded 300 days in early 2025 due to turbine-blade shortages, obliging lessors to extend leases and defer shop visits. CFM admitted to a 15% capacity shortfall for LEAP maintenance in its 2024 annual report, resulting in the prioritization of airline-owned engines over third-party jobs and a reduction in independent revenue potential. Rolls-Royce Trent programs averaged a 180-day turnaround in 2025, twice the target, leading Emirates Engineering to strike a deal for in-house A380 Trent 900 capability and bypass OEM queues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By MRO Type: Component Repair Outpaces Engine Dominance

Component maintenance will grow at a 5.38% CAGR through 2031, the fastest among MRO types, as operators adopt modular repair strategies to cut aircraft-on-ground durations. Engine work held 46.73% of 2025 revenue within the Middle East aircraft MRO market, a share tied to LEAP and GTF overhauls that can exceed USD 8 million per shop visit. Prolonged OEM redelivery cycles shift incremental spend toward landing gear, avionics, and APU overhaul, where Etihad Engineering’s five-year component-support deal with Lufthansa Technik generates USD 120 million in annual revenue. Emirates’ Aviation Supply Centre stocks 12,000 line-replaceable units (LRUs) and offers 24-hour turnaround, attracting contracts from Qatar Airways and Turkish Airlines.

Airframe heavy checks and line maintenance together account for 35% of the 2025 spend, with widebody work concentrated in Istanbul, Jeddah, and Dubai hangars that handle 30,000 to 50,000 labor-hour events. Passenger-to-freighter (P2F) conversions and cabin retrofits form a fast-growing niche; Israel Aerospace Industries completed 18 P2F projects in 2024 for Middle East carriers, each adding USD 8 million to USD 12 million in revenue. Line-maintenance outsourcing by LCCs redistributes USD 200 million annually toward independent stations, accelerating the shift in the Middle East aircraft MRO market.

By Aircraft Class: Rotary-Wing Gains Traction Amid Fixed-Wing Dominance

Fixed-wing platforms controlled 91.14% of 2025 revenue, while rotary-wing work is projected to grow at a 6.65% CAGR through 2031, as Saudi Arabia and the UAE expand their military and offshore-energy helicopter fleets. Saudi contracts for 60 UH-60M Black Hawks include 10 years of sustainment worth USD 400 million to local shops, while Abu Dhabi Aviation operates a dedicated rotary-wing center servicing AW139, S-92, and H225 fleets. Narrowbody jets continue to dominate fixed-wing spending, driven by LCC growth, whereas widebody heavy checks cluster at Turkish Technic’s Istanbul base, which inducted 22 units in Q1 2025.

Regional jets and turboprops account for less than 5% of the spend, reflecting retirements in favor of larger narrowbody aircraft on intra-GCC routes. Rotary-wing demand relies on specialized tooling and OEM partnerships, limiting provider participation and concentrating share among a handful of shops, which positions the Middle East aircraft MRO market for higher margins in this niche.

By Application: Cargo Freighters Accelerate as Passenger Ops Hold Share

Commercial passenger fleets generated 66.54% of 2025 demand across the Middle East aircraft MRO market, underpinned by Emirates’ 260 aircraft, Qatar Airways’ 250 units, and Saudia’s planned 200-aircraft fleet by 2030. Cargo and freighter work, however, is expanding at a 5.19% CAGR thanks to record 777-8 freighter orders and sustained e-commerce growth. Emirates’ USD 950 million facility at Dubai World Central allocates two bays exclusively to B777-8 freighters from 2027.

Military aviation accounts for 15% of 2025 spending, driven by the F-15SA, Mirage 2000, and F-16 sustainment. General aviation remains below 10%, though ExecuJet and Jetex are enlarging FBO footprints to serve Gulf business-jet owners. Passenger operations remain the volume anchor, but cargo growth diversifies revenue streams within the Middle East aircraft MRO market.

By Service Provider: Independent Third-Party Shops Gain Ground

Independent third-party providers are forecast to grow at a 6.58% CAGR, chipping away at the 50.17% share held by airline-affiliated facilities in 2025. Joramco’s USD 100 million seventh hangar in Amman features 22 parallel maintenance lines, catering to European and Asian carriers seeking cost relief from rates in the UAE and Turkey. FL Technics’ Dubai station has secured contracts with flydubai and Fly Vaayu, targeting a USD 25 million revenue by 2027. Gulf Aircraft & Engineering Services broke ground at Bahrain International in 2025, addressing demand from Gulf Air and regional LCCs.

Airline-affiliated giants, such as Emirates Engineering, Etihad Engineering, Saudia Technic, and Turkish Technic, enjoy captive demand and OEM licenses; however, capacity constraints during peak seasons drive overflow to independents, altering the competitive dynamics within the Middle East aircraft MRO market.

Geography Analysis

Turkey secured 33.25% of the 2025 MRO revenue, leveraging Turkish Technic’s 1.2 million square feet of facilities, which resulted in complex and labor costs roughly 20% below the UAE benchmarks. The 10-year IndiGo LEAP contract for 150 engines further solidifies Istanbul as a hub for South Asia and the Gulf. Saudi Arabia, powered by USD 1.5 billion in PIF funding for the Jeddah MRO Village, is the fastest-growing geography, with a 4.87% CAGR through 2031.[4]Nada Al-Tamimi, “PIF Funds Jeddah MRO Village,” arabianbusiness.com The UAE accounts for approximately 30% of 2025 spending and maintains a stronghold in engines and components through Sanad, which posted a 22% revenue increase in the first half of 2024.

Qatar focuses on captive maintenance in its 1 million square feet facility, limiting the potential for third-party revenue. Jordan’s Joramco expanded hangar capacity but contends with Levant instability that restrains widebody utilization. Egypt, Kuwait, Bahrain, and Oman collectively account for less than 15% of the spend, with EgyptAir Maintenance & Engineering holding EASA and FAA approvals yet struggling to attract Gulf carriers amid currency volatility.

Competitive Landscape

Airline-affiliated giants hold captive demand and OEM licenses, but independent entrants, such as Joramco and FL Technics, leverage cost advantages and faster turnarounds to win overflow work. OEM-captive centers operated by GE, Safran, and Rolls-Royce dominate proprietary engine and component segments, maintaining technological barriers that restrict third-party participation.

Digital-twin adoption by Emirates and Etihad reduces turnaround times by 15-20%, allowing for higher annual throughput without proportional bay expansion, a scale efficiency that strengthens their competitive edge. IER MRO Industries plans a USD 1.30 billion Dubai South complex with dual test cells, signaling fresh competition in engine overhaul once financing closes. Safran Electrical & Power’s Dubai wiring-repair center exemplifies OEM compliance with offset rules that drive local capability build-out.[5]Safran Group, “Dubai Wiring Systems Shop Opens,” safran-group.com Smaller specialists, such as Wallan Aviation, focus on rotary-wing components, a niche that is buffered from commercial aviation cycles.

Middle East Aircraft MRO Industry Leaders

Lufthansa Technik AG

General Electric Company

Safran SA

Emirates Engineering (Emirates Group)

Turkish Technic Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Pratt & Whitney (RTX Corporation) added Sanad Group to its GTF MRO network, creating the region’s first PW1100G-JM, PW1500G, and PW1900G facility.

- February 2025: Tawazun Council and Mubadala Investment Company established an aircraft engine MRO facility in Al Ain. This collaboration aligns with the UAE's objectives to strengthen its aerospace capabilities and enhance its efforts at economic diversification.

- December 2024: Saudia, the country's national flag carrier, signed a Memorandum of Understanding (MoU) with Air France-KLM to expand and localize its MRO operations. The agreement includes provisions for Saudi Arabia to conduct module assembly and disassembly of GE90 engines, which power the B777 aircraft.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Middle East aircraft MRO market as all scheduled and unscheduled maintenance, repair, and overhaul services carried out on fixed-wing and rotary-wing civil and military aircraft that are registered, based, or routinely serviced within the region. This includes engine shop visits, heavy airframe checks, line maintenance, component overhaul, and modification programs undertaken by airline-affiliated, independent, or OEM-captive facilities.

Scope exclusion: component distributors that only trade spare parts without performing repair work are outside our coverage.

Segmentation Overview

- By MRO Type

- Airframe Heavy Maintenance

- Engine

- Components

- Line and Routine Checks

- Modifications and Upgrades

- By Aircraft Class

- Fixed Wing

- Rotary Wing

- By Application

- Commercial Passenger

- Commercial Cargo/Freighter

- Military Aviation

- General Aviation

- By Service Provider

- Airline-affiliated MRO

- Independent Third-party MRO

- OEM-Captive MRO

- Military Depots

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Bahrain

- Oman

- Jordan

- Turkey

- Egypt

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with airline engineering heads, independent hangar managers, and regional regulators provided real-time views on labor rates, fleet retirement plans, and shop capacity utilization across the Gulf, Levant, and Turkey. These conversations filled data gaps around gray-market component flows and helped us adjust escalation factors for engine work scopes.

Desk Research

We began by pulling foundational statistics on fleet size, average daily flight cycles, and shop visit intervals from free sources such as ICAO traffic databases, IATA Fleet & Forecast Fact Sheets, and national civil aviation authorities in Saudi Arabia, the UAE, and Turkiye. Public annual reports, Form 20-F filings, and analyst presentations from major Gulf carriers then helped us benchmark labor hour consumption and average spend per shop visit. To contextualize cost structures, our analysts accessed Aviation Week Intelligence Network articles, GCAA directives, and airframe OEM service bulletins archived in Dow Jones Factiva. D&B Hoovers delivered revenue splits for over 60 regional MRO firms, allowing us to cross-check segment shares. The sources listed are illustrative; a wider body of trade journals, customs data, and flight tracking records was also reviewed for validation.

Market-Sizing & Forecasting

We constructed a top-down model that starts with in-service fleet counts by aircraft class, multiplies them by standard maintenance event frequencies, and converts labor hours into value using blended average selling prices reported in interviews. Select bottom-up checks, such as engine overhaul volumes reported by five large depots, were then overlaid to reconcile totals. Key variables include flight cycles per frame, mean time between overhauls, regional technician wage inflation, OEM-mandated work scope escalations, and passenger traffic growth patterns. Five-year forecasts employ multivariate regression with GDP per capita, Brent crude prices, and seat kilometer expansion as predictors, followed by ARIMA smoothing to absorb pandemic-era outliers.

Data Validation & Update Cycle

Before sign-off, our team compares outputs with AWIN engine shop forecasts, IATA billing indices, and audited financials of listed MRO firms; anomalies trigger re-checks with original respondents. Models refresh annually, and any fleet grounding or regulatory shock prompts an interim update so clients always receive the most current baseline.

Why Our Middle East Aircraft MRO Baseline Commands Reliability

Published values often diverge because firms adopt different geographic scopes, service inclusions, and forecast cadences.

Key gap drivers in this market include whether military heavy checks are counted, if Africa is blended with the Gulf states, the choice of currency conversion year, and the depth of engine work scope escalation applied beyond OEM minimums.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.06 B (2025) | Mordor Intelligence | - |

| USD 6.18 B (2025) | Global Consultancy A | Excludes military fleets and counts only airframe and line work, lowering total spend. |

| USD 12.45 B (2024) | Trade Journal B | Combines Africa with Middle East and includes parts distribution revenue, inflating addressable value. |

| USD 9.50 B (2024) | Research Publisher C | Mixes civil and select defense work but omits OEM-captive shops in Turkey, trimming totals. |

These comparisons show that Mordor analysts anchor the baseline to a clearly defined fleet universe, transparent work scope logic, and annual refresh cycle, giving decision-makers a balanced and repeatable reference point grounded in real regional operating data.

Key Questions Answered in the Report

What is the current value of the Middle East aircraft MRO market and its expected growth rate?

The Middle East aircraft MRO market is valued at USD 10.55 billion in 2026 and is forecasted to reach USD 13.35 billion by 2031 at a 4.82% CAGR.

Which MRO type is growing the fastest in the region?

Component repair is expanding at a 5.38% CAGR through 2031, outpacing engine, airframe, and line-maintenance segments.

Why is Saudi Arabia considered the fastest-growing geography?

Saudi Arabia benefits from a USD 1.5 billion investment in Jeddah MRO Village and Saudia’s plan to double its fleet, which together generate a 4.87% CAGR to 2031.

How are digital twins influencing maintenance turnarounds?

Digital-twin platforms adopted by Emirates and Etihad cut turnaround times by up to 20% and raise annual bay utilization by nearly the same percentage.

What factors are limiting new entrants in engine overhaul?

LEAP- and GTF-rated test cells cost more than USD 50 million and require lengthy certification, creating high capital barriers that deter smaller providers.

Which service-provider category is gaining market share?

Independent third-party shops are growing at a 6.58% CAGR as airport privatization and LCC outsourcing redirect work away from airline-affiliated facilities.

Page last updated on: