Power Generation NDT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

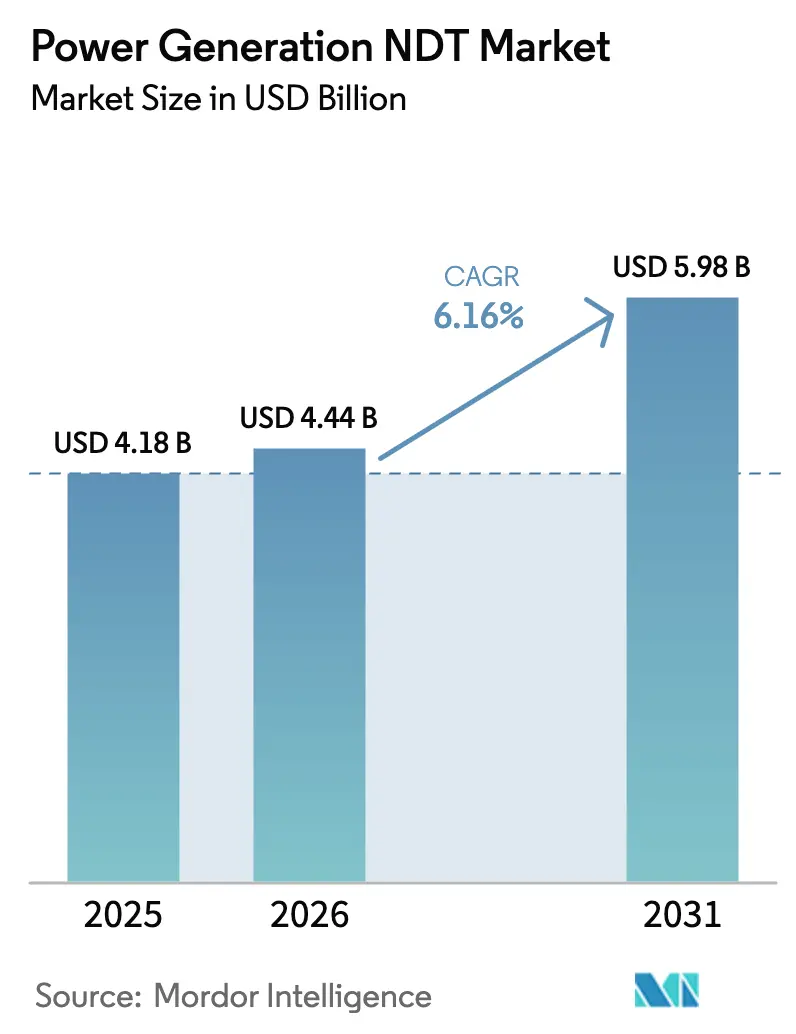

| Market Size (2026) | USD 4.44 Billion |

| Market Size (2031) | USD 5.98 Billion |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

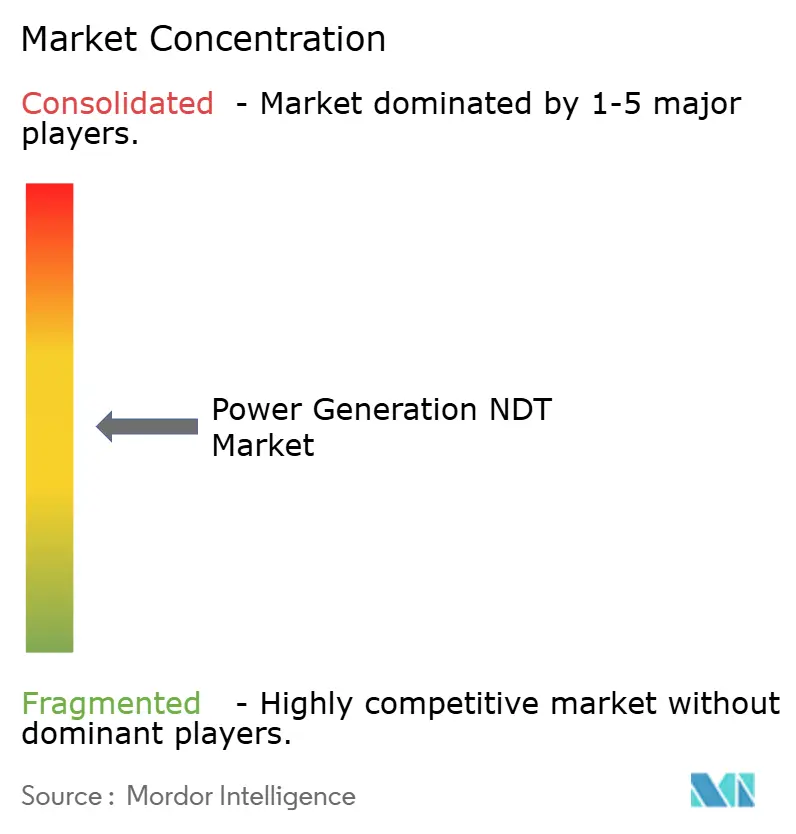

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Generation NDT Market Analysis by Mordor Intelligence

The power generation NDT market size is expected to grow from USD 4.18 billion in 2025 to USD 4.44 billion in 2026 and is forecast to reach USD 5.98 billion by 2031 at 6.16% CAGR over 2026-2031. Rising inspection workloads for aging coal- and gas-fired plants, nuclear license renewal programs, and the shift toward predictive maintenance platforms are steering procurement budgets toward advanced ultrasonic, radiographic, and computed tomography systems. Large utilities are standardizing inspection data formats to feed digital twins, which is encouraging bundled hardware-software deals and shortening replacement cycles. At the same time, tariff-driven localization of sensor supply chains is improving lead times for smaller operators, while the persistent shortage of certified ISO 9712 and ASNT Level III technicians continues to inflate labor costs. Service providers that can combine automated scanners, AI-assisted defect recognition, and cloud analytics are capturing multi-year framework agreements that lock in recurring revenue.

Key Report Takeaways

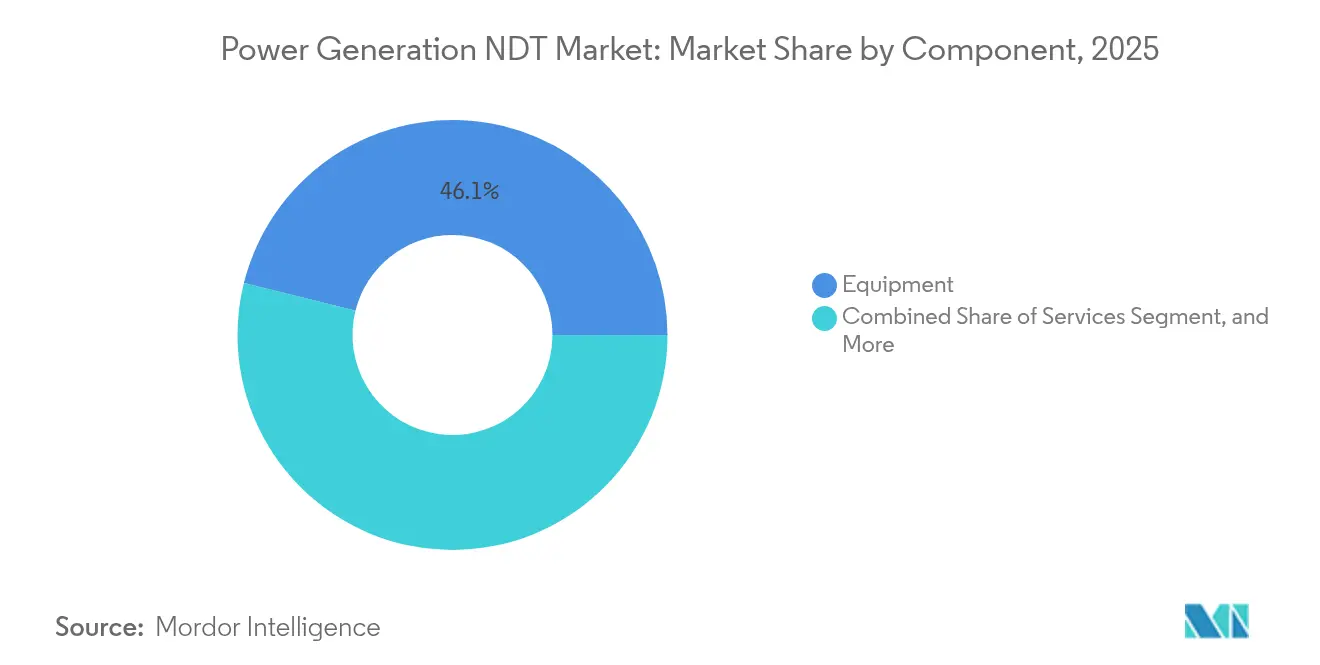

- By component, equipment led with a 46.12% share of the power generation NDT market in 2025; software is expected to advance at a 7.01% CAGR through 2031.

- By testing method, ultrasonic testing accounted for 34.15% of the power generation NDT market size in 2025, whereas computed tomography is projected to expand at an 7.62% CAGR to 2031.

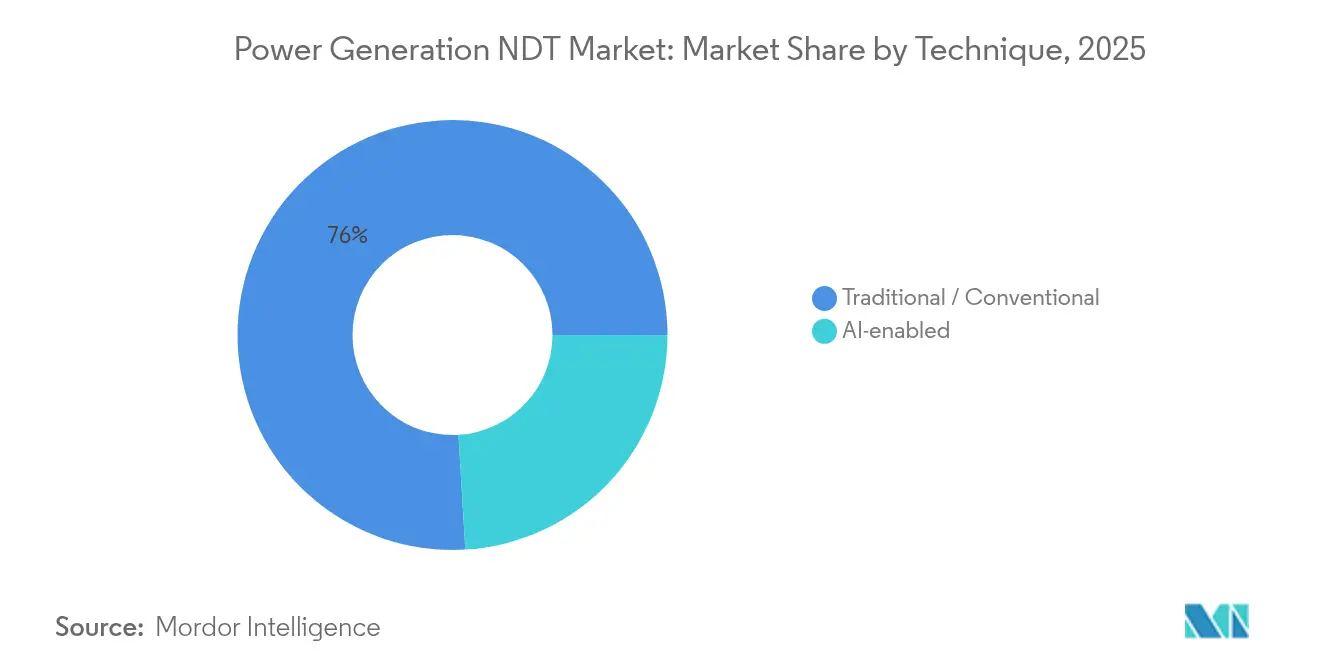

- By technique, traditional approaches held 75.95% of the power generation NDT market share in 2025, while AI-enabled methods are projected to grow at a 6.68% CAGR through 2031.

- By geography, North America accounted for 38.22% of the power generation NDT market size in 2025; the Asia-Pacific region is forecasted to grow at a 6.74% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Power Generation NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging thermal-fossil power fleet reaching end-of-life inspection cycles | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Nuclear life-extension mandates (ASME XI, IAEA periodic safety review) | +1.5% | North America, Europe, Asia-Pacific nuclear markets | Long term (≥ 4 years) |

| Predictive-maintenance programs integrating digital twins and NDT data lakes | +1.2% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Renewables boom driving blade-composite NDT protocols for on-shore/off-shore wind | +0.9% | Global, with emphasis on Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Laser-ultrasonic adoption enabling in-service, non-contact boiler inspection | +0.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Tariff-driven regionalization of sensor supply chains improving local availability | +0.4% | Regional impact across all major markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Thermal-Fossil Power Fleet Reaching End-of-Life Inspection Cycles

Plant owners in North America and Europe are extending the lives of coal and gas units beyond their original design, which amplifies demand for phased-array ultrasonics and computed tomography to detect creep and fatigue in boiler tubes, steam headers, and turbine casings.[1]U.S. Energy Information Administration, “Electric Power Monthly Report,” eia.gov Inspection intensity peaks during the final operating years, resulting in increased per-facility spending and accelerated equipment replacement. Utilities are opting for automated scanners that reduce outage durations and improve repeatability. Service providers with mobile CT capabilities are winning short-notice call-outs as regulators tighten safety audits. The power generation NDT market benefits because each incremental year of operation mandates deeper and more frequent examinations.

Nuclear Life-Extension Mandates

Regulators require license-renewal applicants to verify the integrity of their vessels, the condition of their steam generator tubes, and the health of their primary piping under ASME XI and IAEA periodic review rules.[2]International Atomic Energy Agency, “Periodic Safety Review for Nuclear Power Plants,” iaea.org ENIQ-qualified procedures cost USD 0.5–2 million each, which entrenches incumbent vendors that already possess validated techniques. Utilities allocate multiyear budgets for outage-specific ultrasonic, eddy-current, and acoustic-emission campaigns, sustaining a predictable revenue stream for certified suppliers. The nuclear segment, therefore, acts as a stability anchor for the power generation NDT market, cushioning cyclical swings in fossil-fired spending. Vendors that combine field robotics with AI-aided interpretation are shortening inspection windows and lowering collective radiation exposure.

Predictive-Maintenance Programs Integrating Digital Twins

Digital twins fuse physics-based models with real-time sensor feeds and historical NDT data, enabling condition-based maintenance plans that defer unnecessary inspections. Data lakes store high-resolution ultrasonic and radiographic files that machine-learning models use to identify degradation patterns, thereby improving failure predictions and spare-parts logistics. Software-as-a-service (SaaS) pricing is gaining traction, transforming one-time equipment sales into recurring revenue streams. Buyers are prioritizing open APIs so that inspection data flows seamlessly into plant information management systems. As early success stories spread, the power generation NDT market is shifting toward outcome-based contracts that reward uptime rather than the number of hours spent on site.

Renewables Boom Driving Blade-Composite NDT Protocols

Wind expansion is spawning a specialized demand niche for composite-blade inspection using drones, thermography, and advanced ultrasonics that can map internal delamination. Offshore wind farms magnify the challenge due to access constraints and harsh marine environments, pushing developers to pre-install robotic crawler tracks that support remote inspections. Seasonal maintenance windows concentrate service demand, prompting asset-light providers to adopt mobile teams equipped with ruggedized phased-array sets. Standards such as IEC 61400-1 are harmonizing inspection practices, encouraging multinational utilities to consolidate vendor panels. Consequently, the power generation NDT market is seeing fresh entrants that focus exclusively on rotor-blade health monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified ISO 9712 / ASNT Level III power-sector technicians | -1.4% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| High capex for phased-array, automated and CT systems | -0.8% | Global, affecting smaller service providers disproportionately | Medium term (2-4 years) |

| Data-overload bottlenecks for high-resolution inspection files | -0.6% | Global, concentrated in advanced NDT adopters | Short term (≤ 2 years) |

| Trade-tariff shocks on specialty piezo / opto components | -0.4% | Global supply chains, regional impact variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified ISO 9712 / ASNT Level III Technicians

A retiree wave and stringent certification timelines have created a 25–30% talent gap that inflates wages and extends project lead times.[3]American Society for Nondestructive Testing, “NDT Personnel Shortage Report 2024,” asnt.org Nuclear projects feel the pinch most acutely because regulators cap crew overtime and mandate dual review of critical scans. Service companies are investing in virtual-reality training modules and AI-driven preliminary screening to ease interpreter workloads, yet field deployment still hinges on scarce senior personnel. Utilities are bundling multi-plant contracts to reserve technician rosters in advance, reducing flexibility for unscheduled outages. This constraint tempers growth in the power generation NDT market by limiting the volume of simultaneous campaigns that can be staffed.

High Capex for Phased-Array, Automated and CT Systems

State-of-the-art phased-array sets cost up to USD 1 million, while fully automated scanners with robotics and analytics software can double that figure. Smaller service providers often face balance-sheet pressure, resorting to rental pools or leasing arrangements that erode their margins. Equipment OEMs are countering with pay-per-scan models that bundle hardware, software, and maintenance under a single subscription, thereby shifting capital expenses to operating expenses. Nonetheless, the sticker shock remains a barrier for new entrants, reinforcing the moderate concentration that characterizes the power generation NDT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Equipment Sets the Baseline for Integrated Solutions

Equipment captured 46.12% of the 2025 power generation NDT market share thanks to strong demand for phased-array ultrasonic racks, automated scanners, and high-energy CT gantries. Nuclear license renewals and fossil-plant life-extension projects require multi-modality toolkits that include ultrasonic, eddy-current, and radiographic capabilities. As utilities adopt predictive maintenance, software revenues are climbing at a 7.01% CAGR through 2031, outpacing hardware but still building on a hardware foundation. Cloud-hosted analytics platforms monetize inspection data via subscription, reshaping vendor economics.

Consumables such as couplants, penetrants, and radiographic films deliver recurring revenue that locks customers into OEM ecosystems. Services remain a vital layer because complex codes and qualification regimes push plant operators to outsource rather than maintain in-house crews. The power generation NDT market size for services is projected to swell steadily as personnel shortages intensify. Vendors that bundle equipment leasing with long-term service contracts are achieving double-digit renewal rates. Internal rate-of-return models now weigh lifetime data analytics fees alongside hardware depreciation, refining price-discovery mechanisms.

By Testing Method: Ultrasonic Retains Primacy While CT Accelerates

Ultrasonic testing accounted for 34.15% of the power generation NDT market size in 2025, reflecting its versatility across various materials, including metals, composites, and welds. Phased-array configurations increase scan coverage without repositioning, improving outage productivity. Computed tomography, although niche, is advancing at an 7.62% CAGR as blade composites, additive-manufactured parts, and complex castings require volumetric visualization.

Radiographic testing remains mandated for certain pressure-part welds, particularly in nuclear primary circuits. Eddy-current arrays dominate steam generator tube inspections, where stress corrosion cracking often lurks beneath the inner diameters. Acoustic emission monitoring is gaining adoption as a real-time technique for monitoring rotating machinery, complementing periodic ultrasonic inspections. Thermography extends beyond motor control centers to mechanical insulation surveys, which pinpoint heat-loss hotspots. As workloads diversify, mixed-method work scopes are becoming the norm, encouraging OEMs to offer modular platforms. Cross-calibration routines accelerate job mobilization and reduce data-fusion errors, thereby strengthening the power generation NDT market proposition.

By Technique: AI-Enabled Approaches Transform Interpretation Workflows

Traditional methods still accounted for 75.95% of 2025 revenue, as regulators and insurers continue to cling to proven practices. Yet, AI-enabled workflows are projected to post a 6.68% CAGR through 2031, as deep-learning algorithms surpass human interpreters in repeatability and low-contrast defect recognition. Early use cases focus on automated weld assessment, where models trained on thousands of image slices can classify porosity, lack of fusion, and slag inclusions within seconds.

In blade composites, convolutional networks flag delamination zones that manifest only subtle phase shifts. OEMs embed accelerators directly in portable instruments, enabling edge inference without cloud latency. Validation remains the gating factor: utilities demand statistical evidence of false-alarm rates that align with code requirements. Hybrid reporting formats, where AI pre-labels indications and certified inspectors sign off, are emerging as the acceptable compromise. Over time, accumulated training data will shrink the confidence interval, driving deeper AI penetration and reshaping the cost curve of the power generation NDT market.

Geography Analysis

North America accounted for 38.22% of 2025 revenue in the power generation NDT market, driven by over 90 U.S. reactor license renewals and a backlog of coal-plant end-of-life inspections. Canada’s CANDU refurbishments and Mexico’s grid-modernization projects add further momentum. Well-defined regulatory frameworks ease equipment qualification, while deep service supply chains enable multi-crew deployments during condensed outage windows.

The Asia-Pacific region is the fastest-growing region, with a 6.74% CAGR to 2031, driven by Chinese reactor buildouts, Indian coal fleet modernization, and Southeast Asian renewable energy targets. Local OEMs are scaling phased-array production, compressing lead times and lowering acquisition costs. Regional governments offer tax credits for AI-enabled inspection systems, accelerating digital adoption. Training academies in China and Singapore are expanding ISO 9712 capacity, gradually narrowing the technician gap.

Europe maintains steady growth, underpinned by stringent nuclear directives from ENSREG that require periodic safety reviews encompassing ultrasonic, radiographic, and eddy-current methods. Germany’s nuclear phase-out still needs intensive decommissioning scans, while France’s fleet life-extension hinges on ENIQ-qualified procedures. Offshore wind expansion across the North Sea is spawning specialized composite-blade inspection demand. Harmonized EN ISO standards encourage cross-border service contracts, making Europe a competitive yet accessible arena within the wider power generation NDT market.

Competitive Landscape

The power generation NDT market exhibits moderate concentration, as validated nuclear procedures, global service hubs, and proprietary analytics platforms create defensible moats. Baker Hughes’ Waygate Technologies division anchors its leadership through a cradle-to-grave equipment line, field robotics, and AI libraries tuned for reactor environments. Olympus, rebranded as Evident, continues to command a significant share of the ultrasonic system market despite divesting non-core assets, leveraging ergonomic, portable sets that reduce technician fatigue.[4]Olympus Corporation, “Consolidated Financial Results FY 2025,” olympus-global.com

MISTRAS Group posted USD 36.5 million in 2024 power-sector revenue, pairing asset-light ultrasonic crews with cloud dashboards that benchmark wall-thickness trends across fleets. Eddyfi Technologies is scaling through targeted acquisitions that add composite expertise for wind applications, while Screening Eagle Technologies utilizes fresh venture funding to accelerate the development of inspection robotics. Competition increasingly hinges on data analytics sophistication rather than probe sensitivity alone.

OEMs and service firms are forming joint ventures to create integrated teams that can bid on turnkey scopes encompassing equipment rental, data acquisition, and analytics. Framework agreements spanning multiple plants are common, locking in vendor panels for five-year horizons. Across the board, investment priorities center on AI model validation, automated scanner mobility, and secure data pipelines that comply with nuclear cybersecurity mandates. These moves collectively intensify rivalry but also expand the addressable power generation NDT market.

Power Generation NDT Industry Leaders

Baker Hughes Company

Mistras Group Inc.

SGS S.A.

Intertek Group plc

Applus Services S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MISTRAS Group reported full-year 2024 revenue of USD 729.6 million, with the power generation and transmission segment contributing USD 36.5 million, representing 5.0% growth year-over-year.

- February 2025: Baker Hughes expanded its Waygate Technologies line with AI-enabled ultrasonic systems qualified for ASME XI reactor vessel inspection.

- January 2025: Eddyfi Technologies acquired European wind-blade inspection assets, adding proprietary composite techniques and certified offshore crews.

- December 2024: Screening Eagle Technologies has raised USD 15 million in Series B funding to develop inspection robotics and cloud analytics for power-sector clients.

Global Power Generation NDT Market Report Scope

Non-destructive testing (NDT) instruments are used to scan, inspect, and quantify flaws, corrosions, and other material conditions without permanently damaging or altering the examined product or part. NDT equipment encompasses a broad set of equipment, such as flaw detectors, thickness gages, material condition testers, visual inspection devices, acoustic emission testers, and eddy current instruments, along with devices that measure resistivity, conductivity, and corrosion. The study is segmented by technologies, such as radiography testing equipment, ultrasonic testing equipment, and visual testing equipment, among others, in different geographies. Further, the study covers a comprehensive analysis of the impact of COVID-19 on the market studied.

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Equipment | |

| Software | ||

| Services | ||

| Consumables | ||

| By Testing Method | Ultrasonic Testing | |

| Radiographic Testing | ||

| Magnetic Particle Testing | ||

| Liquid Penetrant Testing | ||

| Visual Inspection Testing | ||

| Eddy-Current Testing | ||

| Acoustic Emission Testing | ||

| Thermography / Infrared Testing | ||

| Computed Tomography Testing | ||

| By Technique | Traditional / Conventional | |

| AI-enabled | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the power generation NDT market in 2026?

The power generation NDT market size is USD 4.44 billion in 2026 and is projected to grow to USD 5.98 billion by 2031 at a 6.16% CAGR.

Which component segment is growing fastest?

Software is the fastest-expanding component, posting a 7.01% CAGR as AI-enabled analytics platforms gain traction among utilities.

What factor drives the strongest near-term demand?

Aging coal and gas units undergoing end-of-life assessments are triggering intensive ultrasonic and CT inspection campaigns, especially in North America and Europe.

Why is ultrasonic testing still dominant?

Ultrasonic testing balances depth penetration, portability, and regulatory acceptance, allowing it to handle thick steel sections in reactors and turbines while meeting code requirements.

How are digital twins influencing NDT purchasing?

Digital twins need structured inspection data, prompting buyers to select integrated hardware-software suites that automatically feed cloud analytics and enable condition-based maintenance.

What is constraining market growth?

A global shortage of certified ISO 9712 and ASNT Level III technicians limits the number of concurrent projects that can be staffed, slowing service rollout despite strong demand.

Page last updated on: