Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

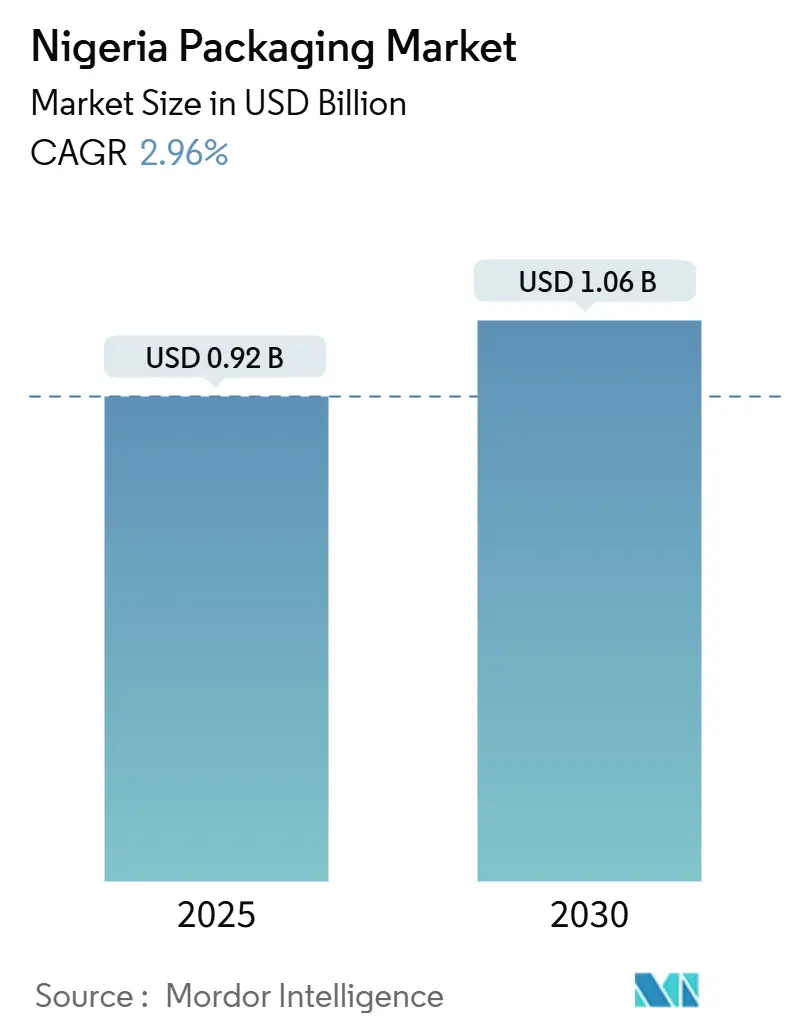

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.06 Billion |

| Growth Rate (2025 - 2030) | 2.96% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nigeria Packaging Market Analysis by Mordor Intelligence

The Nigeria packaging market size reached USD 0.92 billion in 2025 and is forecast to climb to USD 1.06 billion by 2030, reflecting a 2.96% CAGR over the period. Demographic momentum, accelerating urbanization and local-content policies continue to anchor demand even as foreign-exchange pressures challenge raw-material procurement. Plastic remains the dominant substrate because of cost advantages and established filling lines, but sustainability mandates and e-commerce logistics are shifting growth toward paper and flexible formats. Domestic resin supply from the new Dangote polypropylene complex is set to curb import exposure, while tighter monetary rules are pushing converters to deepen local sourcing. Investors that align with recycling infrastructure, barrier solutions for agro-exports and anti-counterfeit closures are best positioned to capture long-term value in the Nigeria packaging market.

Key Report Takeaways

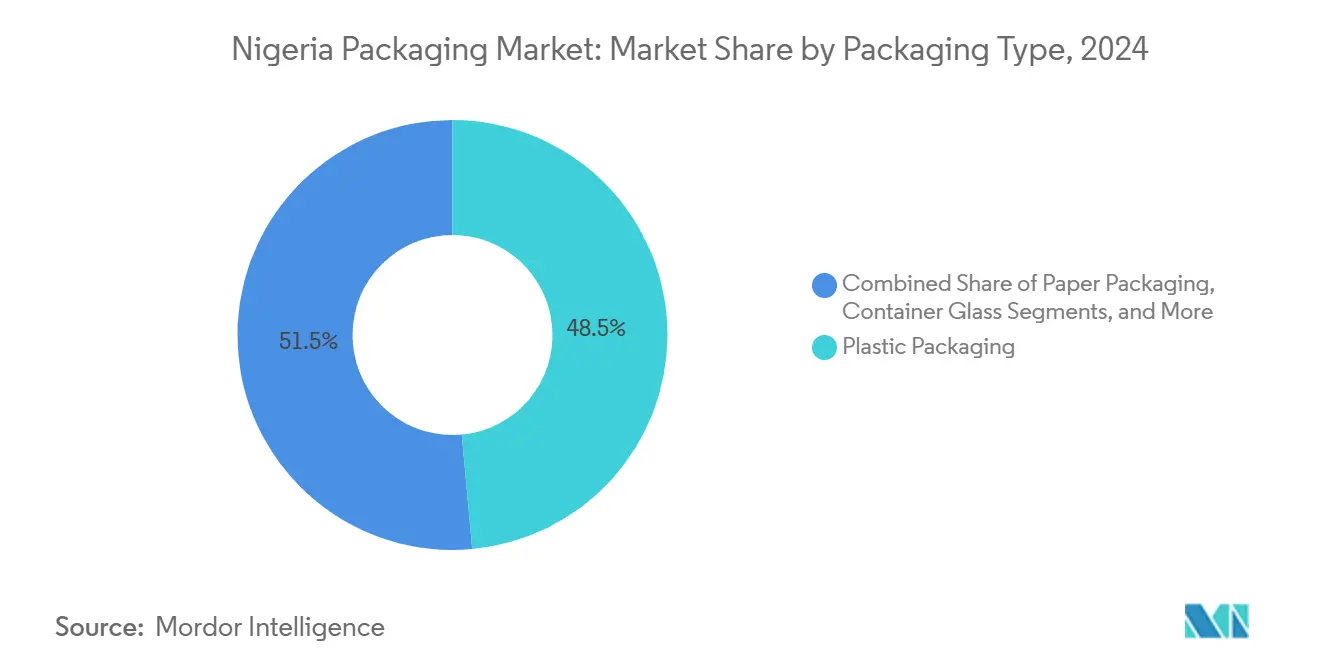

- By packaging type, plastic captured 48.54% of Nigeria's packaging market share in 2024, while paper leads growth at a 4.21% CAGR through 2030.

- By packaging format, flexible formats accounted for 54.86% of the Nigerian packaging market size in 2024 and are expected to expand at a 3.75% CAGR up to 2030.

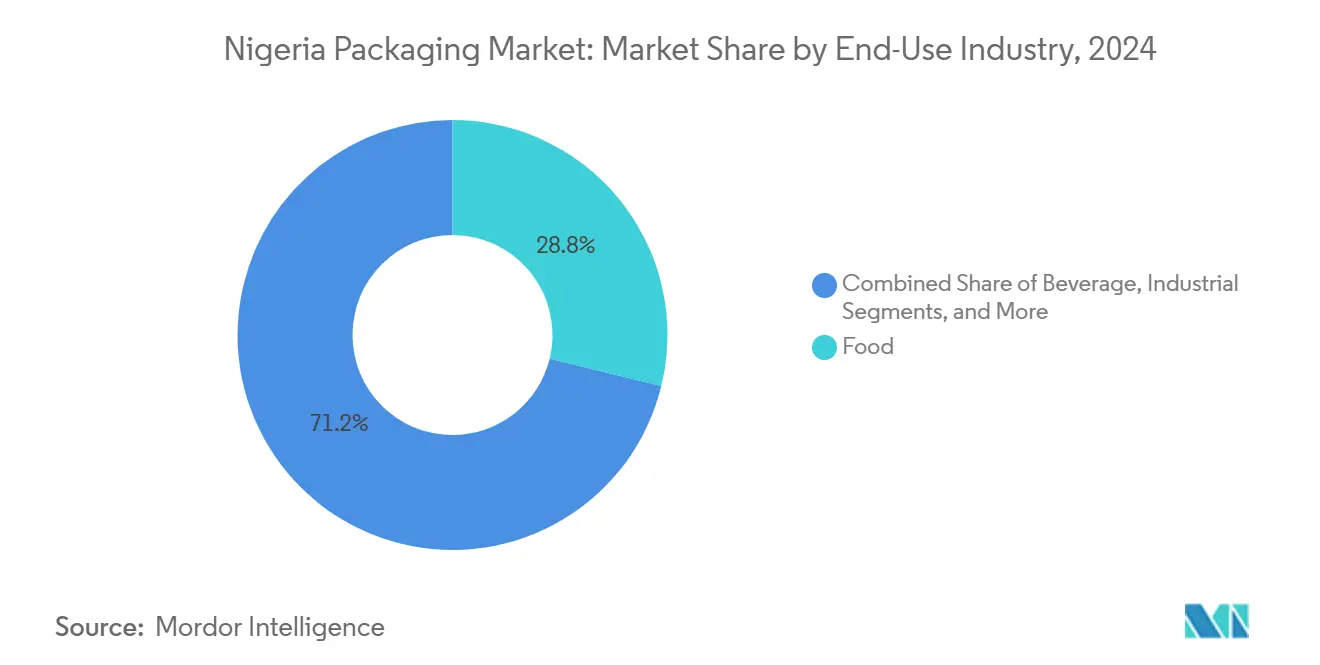

- By end-use industry, food applications commanded a 28.82% share of the Nigeria packaging market size in 2024, whereas e-commerce packaging is projected to advance at a 4.64% CAGR through 2030.

Nigeria Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in beverage demand | +0.8% | Lagos, Kano, Kaduna | Medium term (2-4 years) |

| Rising e-commerce and last-mile delivery | +0.6% | Lagos, Abuja, Port Harcourt | Short term (≤ 2 years) |

| Urban middle-class convenience culture | +0.5% | Lagos, Abuja, Ibadan | Long term (≥ 4 years) |

| On-shore converting capacity investments | +0.4% | Lagos, Ogun, Rivers | Medium term (2-4 years) |

| Local-content push for FMCG packs | +0.3% | National | Long term (≥ 4 years) |

| Export-oriented agri chains need barrier | +0.2% | Ondo, Cross River, Benue, Jigawa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Beverage Demand

Nigeria’s beverage producers are scaling filling lines and secondary packaging to serve a consumer base exceeding 230 million. Nigerian Bottling Company alone operates nine plants and 36 distribution points, driving sustained PET, glass, and aluminum orders. Coca-Cola’s Apapa collection hub, inaugurated in 2025, processes 13,000 t of PET annually and underpins a target of 35-40% recycled content by 2035. The trend toward larger pack sizes, typified by 60 cl carbonated drinks, lifts absolute material consumption per unit sold. Breweries such as Guinness Nigeria, now under Tolaram ownership, are likewise pursuing volume strategies that reinforce demand for caps, labels, and cartons in the Nigeria packaging market. Sustained beverage volume growth is therefore set to add around 0.8 percentage points to the market CAGR through 2030.

Growing Penetration of E-Commerce and Last-Mile Delivery

Digital-commerce spending is accelerating on the back of smartphone uptake and improved payment rails. Urban merchants increasingly specify tamper-evident, brandable mailers, and low-minimum flexible pouches offered by firms like Pack Hub meet this need. Logistics enablers such as Terminal Africa are expanding export documentation services, broadening addressable demand for protective transit packaging. E-commerce buyers value damage-free delivery and unboxing aesthetics, propelling corrugated mailers, void fills and laminated film demand within the Nigeria packaging market. The segment’s growth adds roughly 0.6% to the forecast CAGR and rewards converters capable of rapid customization and short print runs.

Urban Middle-Class Expansion and Convenience Culture

An urban middle class estimated near 50 million consumers is influencing portion sizes, premium finishes and resealability. Nestlé Nigeria’s 50% rPET Pure Life bottles and Cerelac bag-in-box formats show how global brands adapt packs for modern retail. Supermarket footprints grew 24% in 2023, raising shelf-ready packaging needs and labeling clarity demands. Sachet formats remain prevalent as inflation weighs on spending power, yet environmental scrutiny is nudging brands toward multilayer monomaterial pouches that retain affordability while improving recyclability. Over the long term this demographic driver is expected to contribute 0.5 percentage points to the Nigeria packaging market CAGR.

Government Local-Content Push for FMCG Packs

The Central Bank’s foreign-exchange eligibility list discourages imports of cartons, glass, and cellophane, compelling FMCG firms to procure locally.[1]Nigeria Customs Service, “Industrial Incentives,” customs.gov.ng Manufacture-in-Bond and Export Expansion Grants further tilt incentives toward domestic sourcing and regional export. As compliance thresholds tighten, packaging converters that meet food-grade and traceability norms gain procurement preference, adding an estimated 0.3% to long-range market growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict environmental and recycling mandates | -0.4% | Lagos leading enforcement | Medium term (2-4 years) |

| FX volatility inflating polymer and paper | -0.6% | National | Short term (≤ 2 years) |

| Weak logistics infrastructure | -0.3% | Rural and northern regions | Long term (≥ 4 years) |

| Import restrictions on filling machinery | -0.2% | Lagos, Ogun, Rivers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Environmental and Recycling Mandates

NESREA’s Extended Producer Responsibility rules require producers to finance take-back schemes and recycled-content thresholds, increasing compliance costs. Lagos State’s enforcement of waste regulations sets the benchmark, and the federal Climate Change Act compels companies with 50+ employees to publish carbon plans. The first government-approved e-waste facility, inaugurated in 2024, demonstrates regulators’ intent to expand circular-economy principles. Converters must redesign packs for recyclability or biodegradable performance, raising near-term capex and shaving 0.4% from the Nigeria packaging market CAGR.

FX Volatility Inflating Polymer and Paper Costs

Persistent naira depreciation forces importers to source currency at premiums of 20-30% on the parallel market. Corrugated sheets, specialty films, and filling equipment on the CBN’s restriction list face additional hurdles.[2]Export.gov, “Nigeria – Prohibited and Restricted Imports,” export.govThe Dangote polypropylene complex mitigates some polymer risk, but food-grade certification and distribution ramp-up take time. Elevated input prices curb specification upgrades and squeeze converter margins, dampening the market by 0.6% CAGR points in the short term.

Segment Analysis

By Packaging Type: Plastic Remains Dominant but Paper Accelerates

Plastic retained a 48.54% share of the Nigeria packaging market in 2024, benefiting from ingrained filling lines across drinks, personal care, and industrial goods. The March 2025 start-up of Dangote’s 900,000 tpa polypropylene plant ensures a steady resin supply that shields converters from currency swings. Rigid PET bottles and HDPE closures particularly gain from localized feedstock. Flexible polyolefin pouches, offered in minimum runs of 50 units by Hazken Digital, cater to SMEs seeking colorful, laminated prints. Nonetheless, ESG pressure and retail e-commerce lifting corrugated demand push paperboard to a 4.21% CAGR, the highest among major substrates.

Converters are diversifying into coated-paper wraps and molded-fiber trays to secure procurement from multinational FMCG firms committed to reducing virgin plastic. Coca-Cola’s PET collection hub illustrates value-chain investments aimed at integrating recycled resin streams. Mohinani Group’s PET recycling plants are expected to supplement recycled feedstock volumes regionally. Although biodegradable film suppliers like Bonniebio are piloting starch-based bags, adoption remains niche because of a 30-40% cost premium. Metal cans face aluminum price volatility, whereas container glass benefits from import bans on bottles above 150 ml that shield Beta Glass from Asian competition.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Format: Flexible Solutions Extend Leadership

Flexible formats comprised 54.86% of Nigeria's packaging market share in 2024 and are forecast at a 3.75% CAGR through 2030. Roll-to-roll efficiency uses up to 70% less material than rigid packs, lowering freight and storage expenses for online sellers. Accuxel Prints delivers custom chip pouches within seven days, illustrating quick-turn capability valued by emerging snack brands. Sachet water and condiments sustain high-volume demand even as regulators eye single-use waste, prompting converters to explore thin-gauge mono-material laminates.

Rigid packaging upholds critical roles in premium positioning and tamper resistance. Guala Closures’ 5,000 m² Lagos plant will supply aluminum-steel closures with engraving and NFC tags that deter counterfeiting. Pharma vials and HDPE containers remain mandatory under NAFDAC rules, and Tetra Pak’s West Africa headquarters relocation underscores commitment to aseptic carton growth. Smart packaging pilots-incorporating temperature indicators and RFID-emerge in dairy and vaccine lines, but scale is limited by equipment costs and fragmented cold chains.

By End-Use Industry: Food Leads; E-Commerce Surges

Food processing led with 28.82% Nigeria packaging market share in 2024, underpinned by population growth and government's drive for import substitution. Nestlé Nigeria invested NGN 61.25 billion (USD 134 million) in plant upgrades and achieved 100% plastics neutrality, reinforcing demand for rPET preforms and laminated foil sachets. Export-grade cocoa and sesame shipments are adopting hermetic liners and bulk sacks as processors chase higher margins abroad.

The fastest growth, however, stems from e-commerce packaging, projected at 4.64% CAGR to 2030. Online merchants source kraft mailers and corrugated shipping boxes from Pack Hub at basket prices ranging from NGN 5,400–100,000, widening the addressable base for transit-optimized formats. Beverage remains robust on the back of capacity additions by Coca-Cola and Guinness Nigeria, while pharmaceuticals demand blister films and child-resistant closures in step with a national market expected to hit USD 5.3 billion by 2024. Industrial drums and IBCs support petrochemical and agrochemical flows, and personal-care exports leverage premium jars and tubes made with indigenous shea and cocoa butters.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Lagos-Ogun corridor accounts for an estimated 60% of Nigeria packaging market output, hosting Quantum Packaging’s carton plant, Flex Films’ BOPET line and multiple Nigerian Bottling Company facilities. Proximity to Apapa and Tin Can ports facilitates resin and machinery imports as well as finished-goods exports, while LASEPA’s stricter waste codes spur early adoption of recycled-content mandates. The Lagos Free Zone is emerging as a magnet for foreign direct investment, evidenced by Guala Closures’ new factory erected in just 22 weeks.

Northern centers such as Kano and Kaduna serve agricultural processors and textile makers, respectively, with carton converters setting up satellite plants to cut haulage distances. Port Harcourt supports oilfield chemical packaging, relying on steel drums and composite IBCs. Although rural belts remain underserved by modern distribution, ECOWAS trade corridors offer growth runways as AfCFTA protocols simplify customs. Infrastructure gaps-variable power, patchy roads-inflate logistics costs and shape design for durability and stackability.

Federal initiatives under the Economic Recovery and Growth Plan prioritize power reliability and road rehabilitation, which could slash wastage rates and widen cold-chain penetration. Converters seeking pan-Nigeria reach often adopt hub-and-spoke networks, placing filling satellites closer to consumption clusters while centralizing graphics and extrusion at coastal megaplants.

Competitive Landscape

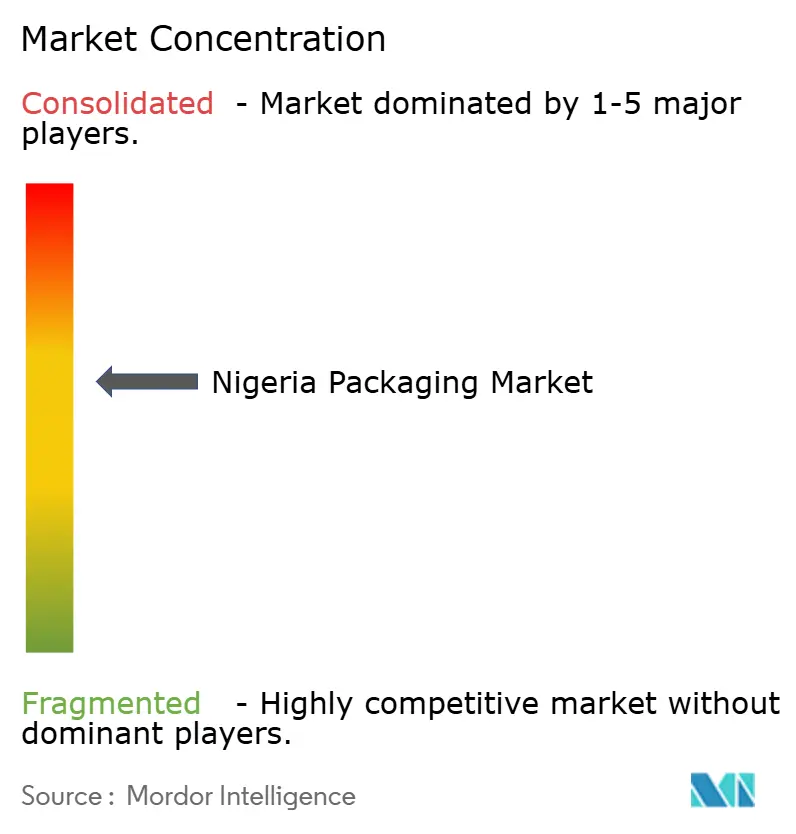

The Nigeria packaging market is moderately fragmented, with the top five players estimated to generate roughly 48% combined revenue. Beverage converters exhibit higher consolidation due to capital intensity and franchise contracts; Nigerian Bottling Company and Strong Pack dominate the PET bottle supply. Flexible and industrial segments remain populated by dozens of SMEs, though FX scarcity and environmental compliance are accelerating attrition of under-capitalized firms.

Vertical integration is a defining strategy. Dangote’s upstream polypropylene provides resin security for affiliated molders, while Nestlé’s closed-loop plastics neutrality guarantees tolling volumes for recyclers. Technology adoption differentiates premium converters: Quantum Packaging’s Koenig & Bauer Rapida press supports seven-color water-based inks, enabling export-grade print fidelity.[3]Quantum Packaging Nigeria, “Mono Carton Manufacturing,” quantumpackagingnig.com Smart-closure specialist Guala leverages engraving and NFC features to protect spirits in a market plagued by counterfeits. White-space opportunities persist in compostable films, barrier sacks for agro-exports, and digital print-on-demand services aligned with social-commerce sellers.

Regulatory capability is increasingly critical. NESREA audits, NAFDAC serialization rules, and SON packaging standards require documentation and testing infrastructure that small converters struggle to maintain. Partnerships with OEMs offering credit-linked equipment packages or managed-service recycling hubs are emerging pathways for capability uplift.

Nigeria Packaging Industry Leaders

-

Avon Crowncaps & Containers Nigeria Limited

-

Beta Glass Plc

-

Nampak Ltd

-

Greif, Inc.

-

Twinstar Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Guala Closures inaugurated a 5,000 m² plant in Lagos Free Zone to supply anti-counterfeiting closures across West Africa.

- March 2025: Dangote Group commenced 900,000 tpa polypropylene output, expected to displace USD 268 million of annual polymer imports.

- February 2025: Coca-Cola System commissioned a 13,000 t plastic collection hub in Apapa, reinforcing its 35–40% recycled-content ambition.

- February 2025: Mohinani Group announced PET recycling expansions in Nigeria and Ghana to bolster regional rPET supply.

Nigeria Packaging Market Report Scope

The packaging industry in Nigeria is tracked based on packaging materials, products, and end-user industries. This provides a detailed assessment of all types of packaging based on factors related to the different packaging products' demand and supply. The consumption volume and revenue accrued from the sales of packaging products offered by various vendors operating in the studied market are considered.

The packaging industry in Nigeria is Segmented by material (plastic, paper and paperboard, glass, and metal), product type (bottles, bags and pouches, corrugated boxes, and metal cans), and end-user industry (beverage, food, pharmaceutical and healthcare, and cosmetics and toiletries and household chemicals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Packaging Type

| Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | ||||

| Polyethylene Terephthalate (PET) | ||||

| Polyvinyl Chloride (PVC) | ||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | ||||

| Other Material Types | ||||

| By Product Type | Bottles and Jars | |||

| Caps and Closures | ||||

| Trays and Containers | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industry | ||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | ||

| Biaxially Oriented Polypropylene (BOPP) | ||||

| Cast Polypropylene (CPP) | ||||

| Other Material Types | ||||

| By Product Type | Pouches and Bags | |||

| Films and Wraps | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industry | ||||

| By Product Type | Bottles and Jars | |||

| Pouches and Bags | ||||

| Bulk-Grade Products | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| Cosmetics and Personal Care | ||||

| Pharamceuticals | ||||

| Industrial | ||||

| Other End-use Industry | ||||

| Paper Packaging | By Product Type | Folding Carton | ||

| Corrugated Boxes | ||||

| Liquid Paperboard | ||||

| Other Product Type | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| E-commerce | ||||

| Other End-use Industry | ||||

| Container Glass | By Color | Green | ||

| Amber | ||||

| Flint | ||||

| Other Colors | ||||

| By End-use Industry | Food | |||

| Alcoholic | ||||

| Non-Alcoholic | ||||

| Personal Care and Cosmetics | ||||

| Pharmaceuticals (excluding Vials and Ampoules) | ||||

| Perfumery | ||||

| Metal Cans and Containers | By Material Type | Steel | ||

| Aluminum | ||||

| By Product Type | Cans | |||

| Drums and Barrels | ||||

| Caps and Closures | ||||

| Other Product Type | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Chemicals and Petroleum | ||||

| Industrial | ||||

| Paints and coatings | ||||

| Other End-use Industry | ||||

By Packaging Format

| Flexible |

| Rigid |

By End-use Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Industrial |

| E-commerce |

| Other End-use Industry |

| By Packaging Type | Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |||||

| Polyethylene Terephthalate (PET) | |||||

| Polyvinyl Chloride (PVC) | |||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | |||||

| Other Material Types | |||||

| By Product Type | Bottles and Jars | ||||

| Caps and Closures | |||||

| Trays and Containers | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industry | |||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | |||

| Biaxially Oriented Polypropylene (BOPP) | |||||

| Cast Polypropylene (CPP) | |||||

| Other Material Types | |||||

| By Product Type | Pouches and Bags | ||||

| Films and Wraps | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industry | |||||

| By Product Type | Bottles and Jars | ||||

| Pouches and Bags | |||||

| Bulk-Grade Products | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| Cosmetics and Personal Care | |||||

| Pharamceuticals | |||||

| Industrial | |||||

| Other End-use Industry | |||||

| Paper Packaging | By Product Type | Folding Carton | |||

| Corrugated Boxes | |||||

| Liquid Paperboard | |||||

| Other Product Type | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| E-commerce | |||||

| Other End-use Industry | |||||

| Container Glass | By Color | Green | |||

| Amber | |||||

| Flint | |||||

| Other Colors | |||||

| By End-use Industry | Food | ||||

| Alcoholic | |||||

| Non-Alcoholic | |||||

| Personal Care and Cosmetics | |||||

| Pharmaceuticals (excluding Vials and Ampoules) | |||||

| Perfumery | |||||

| Metal Cans and Containers | By Material Type | Steel | |||

| Aluminum | |||||

| By Product Type | Cans | ||||

| Drums and Barrels | |||||

| Caps and Closures | |||||

| Other Product Type | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Chemicals and Petroleum | |||||

| Industrial | |||||

| Paints and coatings | |||||

| Other End-use Industry | |||||

| By Packaging Format | Flexible | ||||

| Rigid | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceuticals and Healthcare | |||||

| Personal Care and Cosmetics | |||||

| Industrial | |||||

| E-commerce | |||||

| Other End-use Industry | |||||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Nigeria packaging market in 2025?

The market stands at USD 0.92 billion in 2025 and is projected to reach USD 1.06 billion by 2030.

Which substrate holds the largest share in Nigeria?

Plastic retains 48.54% share, led by PET bottles and flexible polyolefin films.

What is the fastest-growing packaging format?

Flexible packaging is advancing at a 3.75% CAGR on the back of e-commerce logistics and material efficiency.

How will local polypropylene output influence converters?

The 900,000 tpa Dangote resin plant reduces FX exposure for bottle and film manufacturers and should stabilize feedstock pricing.

Which end-use sector is growing quickest?

E-commerce packaging is forecast to expand at a 4.64% CAGR through 2030 as online retail volumes rise.

What role do environmental mandates play?

NESREA’s Extended Producer Responsibility rules are increasing recycled-content requirements, raising short-term costs but opening opportunities in circular solutions.

Page last updated on: