Nigeria Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

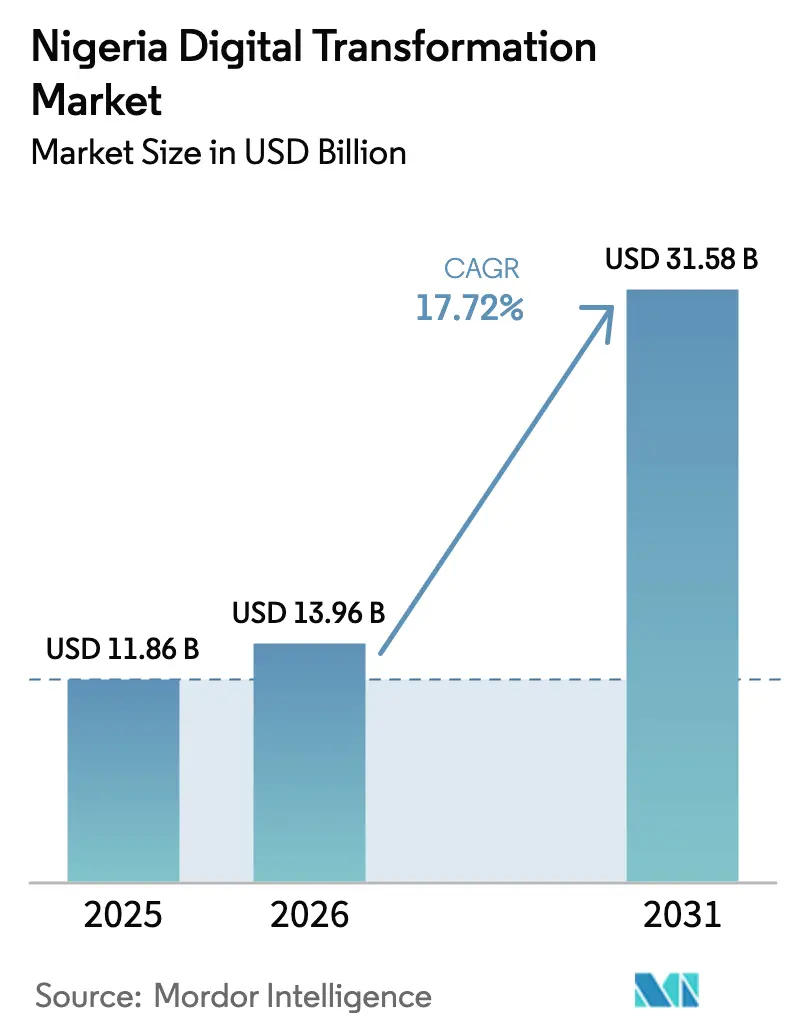

| Base Year Market Size (2025) | USD 11.86 Billion |

| Market Size (2026) | USD 13.96 Billion |

| Market Size (2031) | USD 31.58 Billion |

| Growth Rate (2026 - 2031) | 17.72% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Digital Transformation Market Analysis by Mordor Intelligence

Nigeria digital transformation market size in 2026 is estimated at USD 13.96 billion, growing from 2025 value of USD 11.86 billion with 2031 projections showing USD 31.58 billion, growing at 17.72% CAGR over 2026-2031. Rapid subsea-bandwidth additions, sovereign digital-infrastructure spending, and a fintech ecosystem that already routes NGN 600 trillion (USD 390 billion) in annual payments are reshaping enterprise technology priorities. Cloud edge-computing nodes positioned near financial hubs are closing latency gaps, while artificial-intelligence workloads tap the same infrastructure to score micro-loans and fight fraud. Rising broadband penetration, a 116% mobile-SIM density, and data-residency mandates have further pushed enterprises toward hybrid-cloud architectures. Grid unreliability, high broadband tariffs, and fragmented state regulations temper progress, yet the Nigeria digital transformation market continues to attract both global hyperscalers and indigenous innovators whose combined strategies expand service availability and lower total cost of ownership.

Key Report Takeaways

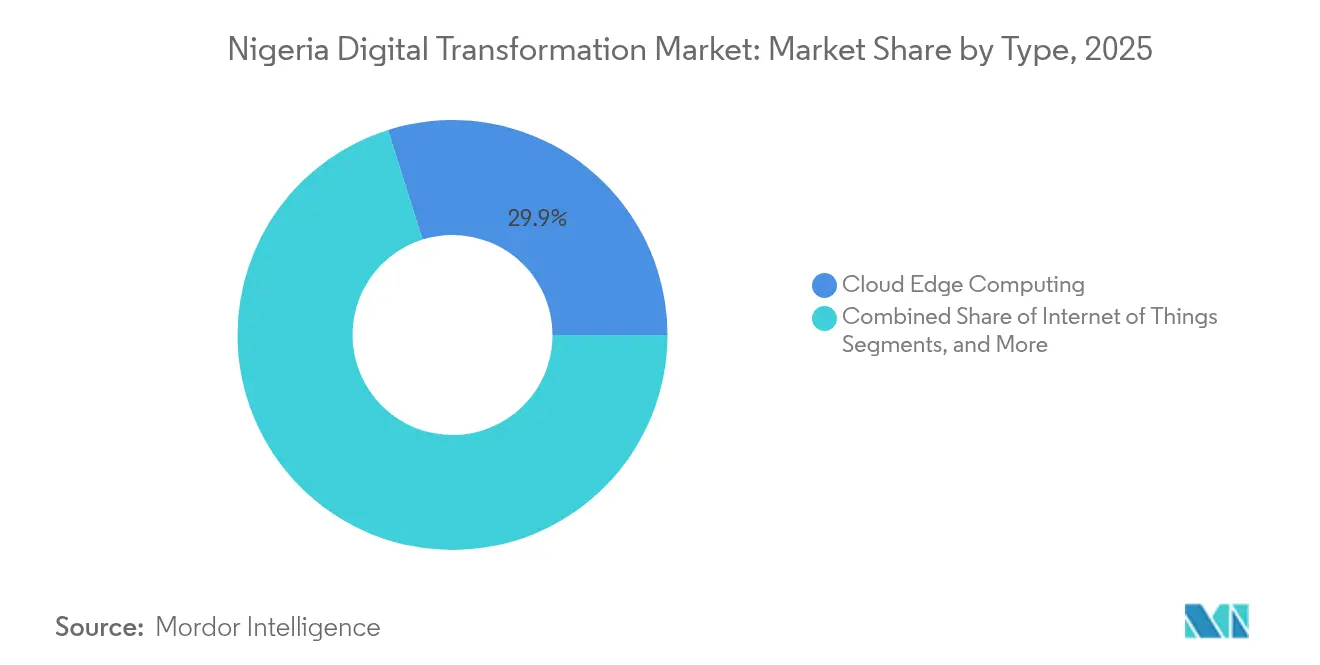

- By technology type, cloud edge computing led with a 29.85% Nigeria digital transformation market share in 2025, whereas artificial intelligence and machine learning are forecast to grow at a 22.97% CAGR to 2031.

- By end-user industry, banking, financial services, and insurance held 26.35% of the Nigeria digital transformation market size in 2025, while healthcare is expected to accelerate at a 23.9% CAGR through 2031.

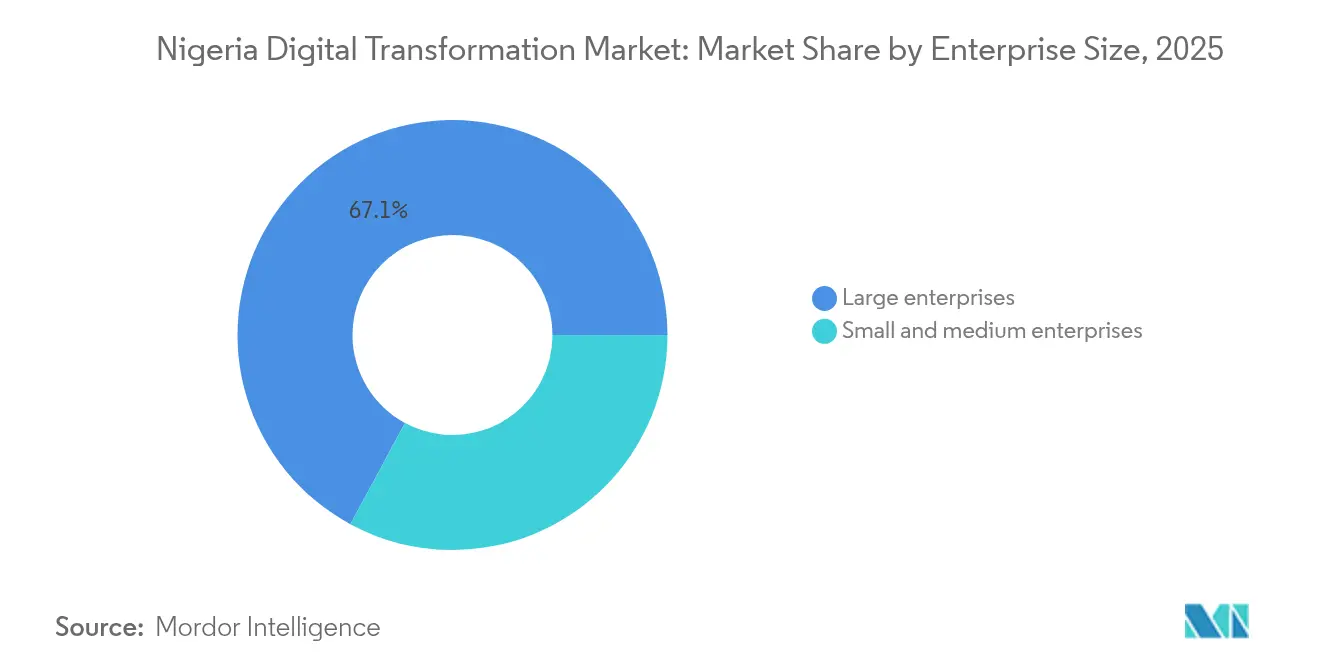

- By enterprise size, large enterprises accounted for 67.12% of spending in 2025, but small and medium enterprises are poised for a 20.12% CAGR to 2031.

- By deployment model, cloud captured 55.10% market share in 2025; hybrid architectures are projected to post a 20.5% CAGR across the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria represents one dimension of a structure that spans multiple countries, continents and economic zones. Our global digital transformation (dx) market report covers details on that full structure.

Nigeria Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing mobile and internet penetration | +3.2% | National, with urban centers in Lagos, Abuja, Port Harcourt leading adoption | Medium term (2-4 years) |

| Government investments in digital infrastructure | +4.1% | National, concentrated in South West and North Central zones | Long term (≥ 4 years) |

| Rising adoption of cloud services by enterprises | +3.8% | National, with early gains in Lagos, Abuja, and Port Harcourt metro areas | Medium term (2-4 years) |

| Growing fintech ecosystem driving digital services | +3.5% | National, strongest in South West and South South commercial hubs | Short term (≤ 2 years) |

| Surge in new subsea cable landings increasing bandwidth | +2.4% | Coastal states (Lagos, Rivers, Cross River), spillover to inland tier-2 cities | Long term (≥ 4 years) |

| Youth developer communities accelerating open-source innovation | +1.6% | National, with tech-hub concentration in Lagos, Abuja, Ibadan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Mobile and Internet Penetration

Nigeria now records 116% mobile-SIM density and 45.5% household internet adoption. The gap between device ownership and effective data use has encouraged operators to bundle low-cost smartphones with data vouchers, boosting traffic volumes and expanding the revenue base that finances 5G rollouts. Rising connectivity feeds a steady influx of subscribers to over-the-top video, e-commerce, and digital banking platforms. That momentum, in turn, raises the addressable opportunity for the Nigeria digital transformation market. Telcos have responded by accelerating radio-access-network sharing and refarming 900 MHz and 1800 MHz spectrum for LTE, further widening coverage footprints. The multiplier effect of wider access and richer applications sustains double-digit data-revenue growth even as tariffs fall, keeping capital expenditure pipelines intact and de-risking new fiber-optic and tower projects. [1]Nigerian Communications Commission, “Industry Statistics,” ncc.gov.ng

Government Investments in Digital Infrastructure

The National Information Technology Development Agency financed 90,000 kilometers of backbone fiber by 2024 and commissioned a 1.4-petabyte sovereign data center in Abuja. Parallel tower-infrastructure projects reduce site-acquisition costs for operators and extend 4G coverage to 84% of the population. Federal grants offset right-of-way fees that historically stalled fiber builds, while public-private tower leases lower per-site operating expense by 30%. Resulting improvements in bandwidth availability and transport pricing expand the Nigeria digital transformation market across education, health, and commerce use cases. Execution constraints remain at state level where right-of-way approvals vary in pace and cost, but collaborative forums are starting to harmonize fee structures

Rising Adoption of Cloud Services by Enterprises

Local cloud regions, edge locations, and hyperscaler on-ramps have cut average latency for Nigerian workloads below 20 milliseconds. Enterprises, especially in finance and oil and gas, now split workloads between domestic racks and global regions, aligning with data-residency rules while tapping elastic compute for analytics. The Central Bank’s 2024 disaster-recovery directive accelerates multi-site deployments that favor hybrid architectures. Carrier-neutral facilities, such as MTN’s 1,500-rack Lagos campus, offer direct peering to content-delivery networks, saving on international transit and improving user experience. These cost and compliance dynamics underpin the continued expansion of the Nigeria digital transformation market. [2]MTN Nigeria Communications Plc, “Annual Report 2024,” mtnonline.com

Growing Fintech Ecosystem Driving Digital Services

Payment-switch volumes reached NGN 600 trillion in 2024, reflecting deeper agency-banking penetration and QR-code uptake among small merchants. Platforms such as Interswitch, Flutterwave, and Opay have embedded credit, insurance, and savings products that depend on cloud scalability and AI-based scoring. Transaction-processing intensity forces constant infrastructure upgrades, making fintech a bellwether for the Nigeria digital transformation market. Central-bank open-banking rules taking effect in 2025 will expose additional APIs, spurring third-party innovation and driving consumption of security, integration, and monitoring tools across the ecosystem.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited electricity supply reliability | -2.8% | National, acute in North East, North West, and rural South East | Long term (≥ 4 years) |

| High broadband connectivity costs | -1.9% | National, most severe in inland states lacking fiber infrastructure | Medium term (2-4 years) |

| Shortage of local cybersecurity talent | -1.2% | National, with enterprise concentration in Lagos and Abuja | Medium term (2-4 years) |

| Fragmented digital regulations across states | -0.9% | National, compliance complexity highest for multi-state operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Electricity Supply Reliability

Grid output of 4,500 megawatts falls far short of installed capacity, resulting in daily outages averaging eight hours in tier-2 cities and up to sixteen hours in rural locations. Data-center operators earmark 40% of operating budgets for diesel, inflating colocation costs 60% above East African equivalents. Fuel price volatility further erodes margins and stifles expansion plans in zones where tariffs cannot pass through to end users. Renewable-energy pilots offer partial relief but face three-year payback periods that discourage small and medium enterprises. Until tariff reform funds grid upgrades, electricity instability will moderate the otherwise robust growth trajectory of the Nigeria digital transformation market

High Broadband Connectivity Costs

Average mobile-data tariffs stood at NGN 1,200 (USD 0.78) per gigabyte in 2024, three times the East African benchmark. High backhaul expenses, spectrum-license fees, and diesel surcharges feed an elevated cost base. Fixed-broadband penetration stagnates below 0.5%, curbing enterprise reliance on cloud and video collaboration outside major metros. The Universal Service Provision Fund subsidized backhaul to 500 unserved communities, yet annual allocations cover under 10% of the estimated investment need. Unless wholesale price compression matches subsea-capacity growth, the Nigeria digital transformation market will continue to confront affordability ceilings.[3]Universal Service Provision Fund, “Broadband Deployment Report 2024,” uspf.gov.ng

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Edge Computing Anchors Present Share, AI Drives Future Growth

Cloud edge computing held 29.85% of Nigeria digital transformation market share in 2025, reflecting banks’ latency-sensitive fraud-detection engines and content-delivery caching at carrier-neutral facilities. Processing workloads inside the country also complies with data-residency rules and shields applications from subsea-cable disruptions. Artificial-intelligence and machine-learning solutions are forecast to expand at a 22.97% CAGR, moving the Nigeria digital transformation market size for AI workloads to a materially higher base by 2031. Agri-credit platforms combine satellite imagery with mobile-money histories to underwrite smallholder loans, while state health agencies pilot AI chatbots to triage primary-care queries.

Extended-reality pilots remain concentrated in Lagos and Abuja due to limited 5G coverage yet demonstrate potential in remote equipment maintenance. Internet of Things implementations continued to scale during 2024, from smart meters to precision farming, proving sub-18-month paybacks. Industrial-robotics and additive-manufacturing projects are niche but gaining footholds in automotive assembly and affordable-housing prototypes respectively. Cybersecurity spending surged after ransomware incidents jumped 35% year on year, cementing managed detection and response as a core budget line across sectors. Digital-twin rollouts in offshore oil improved maintenance scheduling, while mobility and connectivity investments underpin every other stack layer, confirming their foundational role in the Nigeria digital transformation market.

By End-User Industry: BFSI Leads, Healthcare Accelerates

Banking, financial services, and insurance commanded 26.35% of the Nigeria digital transformation market size in 2025 as banks migrated core systems and expanded agency networks to 1.2 million field agents. Regulatory pressure to maintain cloud-based disaster-recovery sites and adopt open-API standards sustains investment momentum. Healthcare is tracking the fastest 23.9% CAGR through 2031, propelled by a digital-enrollment platform that onboarded 15 million beneficiaries and telemedicine startups that secured USD 40 million in new funding. Manufacturing remains smaller yet posts steady gains from predictive-maintenance algorithms deployed in cement and food plants.

Oil, gas, and utilities invest in digital twins and blockchain-based crude tracking to address leak-detection and theft, while retail and e-commerce channels leverage AI forecasting for inventory and last-mile routing. Logistics platforms integrate customs-clearance APIs to cut port dwell times, and telecom operators re-invest digital transformation gains into network-function virtualization. Government programs spanning identity, tax, and welfare create new public-sector workloads that anchor sovereign-cloud demand. Education, media, and environmental projects form an “other” category that benefits indirectly from these broader shifts across the Nigeria digital transformation market.

By Enterprise Size: Large Firms Dominate, SMEs Gain Momentum

Large enterprises captured 67.12% of spending in 2025, justified by hybrid-cloud migration budgets, data-protection compliance, and multinational pricing leverage. The Nigeria digital transformation market now tilts toward volume deals with global software vendors bundled under multi-year support contracts. Small and medium enterprises, however, will outpace with a 20.12% CAGR as subscription models remove upfront capital and mobile-first platforms like Moniepoint offer turnkey payments, lending, and analytics. Point-of-sale terminal deployments averaged 200,000 units per quarter in 2024, converting cash-heavy segments into digital channels.

SMEs still confront credit constraints and skills gaps, which state-backed blended-finance facilities and the 3 Million Technical Talent program aim to relieve. Micro-businesses increasingly rely on social-commerce storefronts integrated with payment links, a low-barrier entry point to the Nigeria digital transformation market. Large enterprises’ longer procurement cycles slow refresh rates yet secure higher ticket sizes, balancing the addressable revenue across firm-size cohorts. Managed-service providers bridge staffing shortages by supplying bundled infrastructure, security, and compliance monitoring to both tiers.

By Deployment: Cloud Dominates, Hybrid Gains as Compliance Tightens

Cloud services accounted for 55.10% of deployments in 2025 because pay-as-you-go pricing aligns with budget cycles and rapid growth. Regulatory restrictions on cross-border data flows motivate hybrid architectures, which are projected to post a 20.5% CAGR. Financial institutions must retain encryption keys domestically, creating demand for split-stack configurations where sensitive data resides on-premise while analytics burst to external regions. The Nigeria digital transformation market therefore revolves around orchestration tools that unify compliance, networking, and governance across heterogeneous environments.

On-premise stacks persist in defense and critical-infrastructure verticals, but even these sectors install private-cloud layers for agility. Multi-cloud strategies gained traction in 2024 as 40% of surveyed corporations ran workloads across at least two hyperscalers, hedging against vendor lock-in and price shocks. Skilled personnel shortages add complexity, prompting systems integrators to offer turnkey managed hybrids that accelerate adoption without sacrificing control.

Geography Analysis

The South West zone, led by Lagos, attracted 44.30% of Nigeria digital transformation market spending in 2025, owing to 11 internet exchange points, eight submarine-cable landings, and near-ubiquitous 4G coverage. Lagos also hosts the headquarters of major telcos and fintech unicorns, forming a dense demand and supply cluster. South South states benefit from oil-sector budgets and Port Harcourt’s cable landing but must internalize higher diesel costs because outages average 12 hours daily, limiting data-center profitability. South East entrepreneurial hubs such as Aba embrace mobile-money at scale yet suffer fixed-broadband penetration below 0.3%, restricting access to cloud enterprise applications. North Central, anchored by Abuja, leverages federal IT budgets and a sovereign data center but remains constrained by microwave backhaul to tier-2 cities. North West and North East lag on every metric 4G coverage below 60%, electricity access under 40% in rural districts, and limited cybersecurity response capacity cementing a digital divide. The Universal Service Provision Fund extended connectivity to 500 underserved communities, but annual funds cover less than a tenth of required outlays, prolonging geographic disparities in the Nigeria digital transformation market

Federal infrastructure-sharing rules require tower companies to lease space to competitors within 90 days, yet implementation proves uneven amid pricing disputes. Tax incentives seek to lure data-center builds outside Lagos and Abuja, though no hyperscaler has committed to a northern facility. Talent clusters also bias the South West, where 60% of national software-developer jobs reside, creating a virtuous cycle of startup formation and venture funding. Northern states offer lower real-estate and labor costs, but inadequate connectivity and grid reliability continue to deter large-scale investments.

Mordor Intelligence tracks the digital transformation (dx) market across other major regions such as Africa, Latin America, and Asia, with additional country-level coverage spanning Colombia, Indonesia, France, Oman, Italy, and Canada, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Competition features global hyperscalers—Microsoft, Oracle, SAP—vying with domestic integrators such as CWG, Sidmach Technologies, and Wragby Business Solutions for enterprise workloads. Edge-computing capabilities differentiate offers because local processing cuts latency and satisfies data-residency mandates. Microsoft’s nearest Azure regions in South Africa deliver sub-20-millisecond latency, while Oracle partners with MainOne to host database services inside Lagos colocation facilities, merging global platforms with local compliance.

Fintech remains the fiercest battleground, as Flutterwave, Interswitch, and Opay compete on transaction costs and platform extensibility. Opay’s USD 12 billion monthly volume underscores the scale stakes, forcing rivals to adopt AI-driven fraud prevention and dynamic pricing. Carrier-neutral data-center operators including MTN’s Lagos hub create new value chains where enterprises peer directly with content-delivery networks, while infrastructure-sharing mandates commoditize tower assets, shifting differentiation to software-defined networking. Indigenous startups such as Moniepoint demonstrate how mobile-first models leapfrog legacy IT by bundling payments, lending, and analytics for two million merchants. The Nigeria digital transformation market is therefore a mosaic of global scale, local nuance, and vertical specialization.

Nigeria Digital Transformation Industry Leaders

IBM Corporation

Microsoft Corporation

Oracle Corporation

Schneider Electric group

Alphabet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: MTN Nigeria announced the expansion of its 5G network to 25 cities, up from 15 cities at the start of the year, with population coverage reaching 18.5%. The operator disclosed plans to invest an additional USD 200 million in edge-computing infrastructure by end-2025, targeting financial institutions and content-delivery networks requiring sub-10-millisecond latency. This expansion positions MTN as the dominant 5G provider in Nigeria and enables enterprise use cases in autonomous systems and real-time analytics.

- August 2025: The Central Bank of Nigeria mandated all commercial banks to complete core-banking system modernization by December 2025, requiring migration to cloud-native architectures with API-first design principles. The directive compels 22 deposit-money banks to replace legacy systems that average 15 years in age, creating a USD 500 million opportunity for Oracle, SAP, and indigenous integrators. Banks failing to comply face restrictions on new branch licenses and digital-banking approvals.

- July 2025: Google Cloud formally opened its Lagos edge location, offering compute and storage services with direct interconnection to the Equiano subsea cable. The facility provides Nigerian enterprises with a local alternative to South African cloud regions, reducing latency by 60% and enabling compliance with the Nigeria Data Protection Commission's data-residency requirements. Initial customers include fintech platforms, e-commerce operators, and government agencies migrating from on-premise infrastructure.

- June 2025: Airtel Africa completed construction of its second Lagos data center, a 2,000-rack facility offering carrier-neutral colocation and direct cloud on-ramps to AWS, Microsoft Azure, and Google Cloud. The investment totaled USD 80 million and targets financial institutions requiring disaster-recovery sites at least 100 kilometers from primary data centers, as mandated by Central Bank of Nigeria regulations. The facility features N+2 power redundancy and 100% renewable-energy sourcing through solar arrays and battery storage.

Nigeria Digital Transformation Market Report Scope

The Digital transformation market refers to the global ecosystem of technologies, platforms, services, and solutions that enable organizations to modernize their operations, customer experiences, business models, and internal processes through the adoption of digital technologies.

The Nigeria Digital Transformation Market Report is Segmented by Type (Artificial Intelligence and Machine Learning, Extended Reality, Internet of Things, Industrial Robotics, Blockchain, Additive Manufacturing, Cybersecurity, Cloud Edge Computing, Digital Twin, Mobility and Connectivity), End-User Industry (Manufacturing, Oil and Gas and Utilities, Retail and E-commerce, Transportation and Logistics, Healthcare, Banking and Financial Services and Insurance, Telecom and IT, Government and Public Sector, Other End-User Industry), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Deployment (On-Premise, Cloud, and Hybrid). The Market Forecasts are Provided in Terms of Value (USD).

| Artificial Intelligence and Machine Learning |

| Extended Reality (VR and AR) |

| Internet of Things |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing / 3D Printing |

| Cybersecurity |

| Cloud Edge Computing |

| Digital Twin |

| Mobility and Connectivity |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| Banking, Financial Services and Insurance |

| Telecom and IT |

| Government and Public Sector |

| Other Industries (Education, Media and Environment) |

| Large enterprises |

| Small and medium enterprises |

| On-premise |

| Cloud |

| Hybrid |

| By Type | Artificial Intelligence and Machine Learning |

| Extended Reality (VR and AR) | |

| Internet of Things | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing / 3D Printing | |

| Cybersecurity | |

| Cloud Edge Computing | |

| Digital Twin | |

| Mobility and Connectivity | |

| By End-user Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| Banking, Financial Services and Insurance | |

| Telecom and IT | |

| Government and Public Sector | |

| Other Industries (Education, Media and Environment) | |

| By Enterprise Size | Large enterprises |

| Small and medium enterprises | |

| By Deployment | On-premise |

| Cloud | |

| Hybrid |

Key Questions Answered in the Report

How large is the Nigeria digital transformation market in 2026?

It is valued at USD 13.96 billion and is forecast to grow to USD 31.58 billion by 2031, reflecting an 17.72% CAGR.

Which enterprise segment contributes most to spending?

Large enterprises account for 67.12% of 2025 expenditure, driven by hybrid-cloud migration and compliance requirements.

What is the fastest-growing technology within this space?

Artificial-intelligence and machine-learning workloads are expected to post a 22.97% CAGR through 2031.

Which geographic zone captures the highest investment?

The South West zone, anchored by Lagos, attracted about 44.30% of 2025 spending due to its dense submarine-cable and data-center footprint.

What are the main barriers to wider adoption?

Limited grid reliability and above-benchmark broadband tariffs remain the two strongest restraints on market growth.

Page last updated on: