Natural Language Generation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

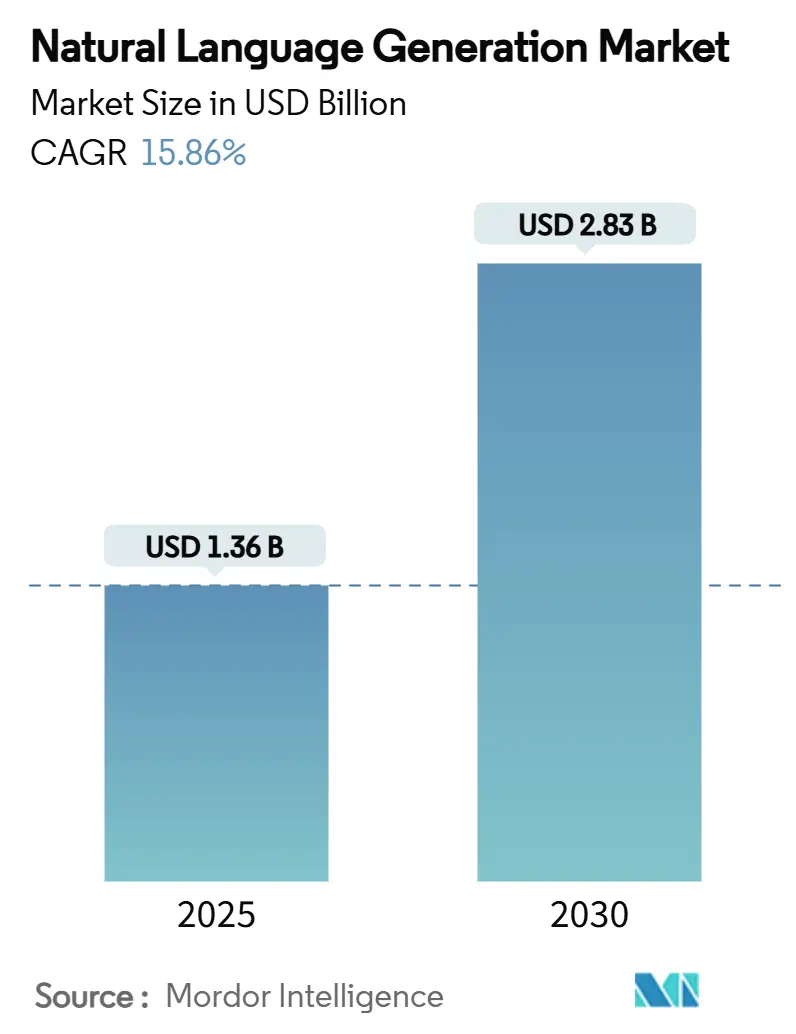

| Market Size (2025) | USD 1.36 Billion |

| Market Size (2030) | USD 2.83 Billion |

| Growth Rate (2025 - 2030) | 15.86% CAGR |

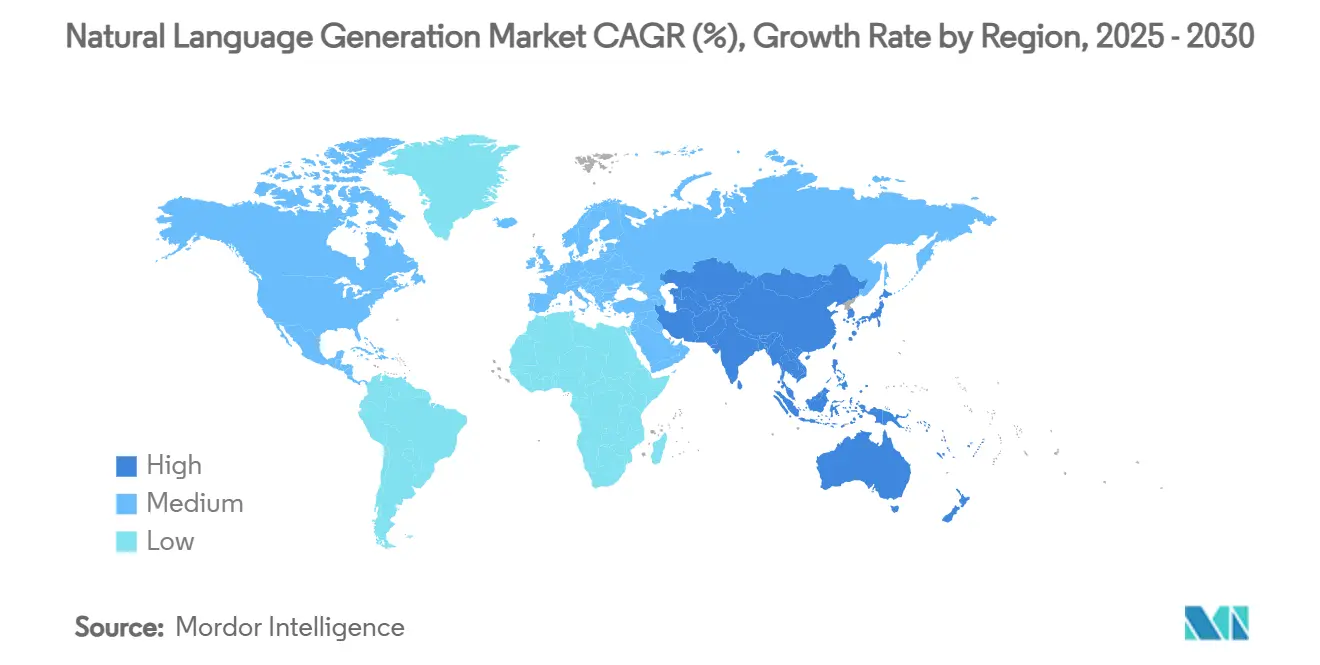

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Natural Language Generation Market Analysis by Mordor Intelligence

The natural language generation market size stands at USD 1.36 billion in 2025 and is forecast to reach USD 2.83 billion by 2030, expanding at a 15.86% CAGR. Rising enterprise demand for contextual, multilingual content, lower large-language-model inference costs, and expanding cloud-edge deployment options underpin this acceleration. Early adopters in retail, financial services, and healthcare record measurable gains from hyper-personalized content automation, while declining API pricing removes historical cost barriers for small and medium enterprises. Edge-optimised lightweight models now generate 11 tokens per second on resource-constrained devices, enabling real-time narrative generation for autonomous agents in IoT and automotive applications.[1]arXiv, “Edge-First Language Model Inference: Models, Metrics, and Trade-offs,” arxiv.org Regulatory frameworks such as the EU AI Act incentivise explainable AI, steering heavily regulated sectors toward hybrid NLG architectures that balance transparency with linguistic sophistication.

Key Report Takeaways

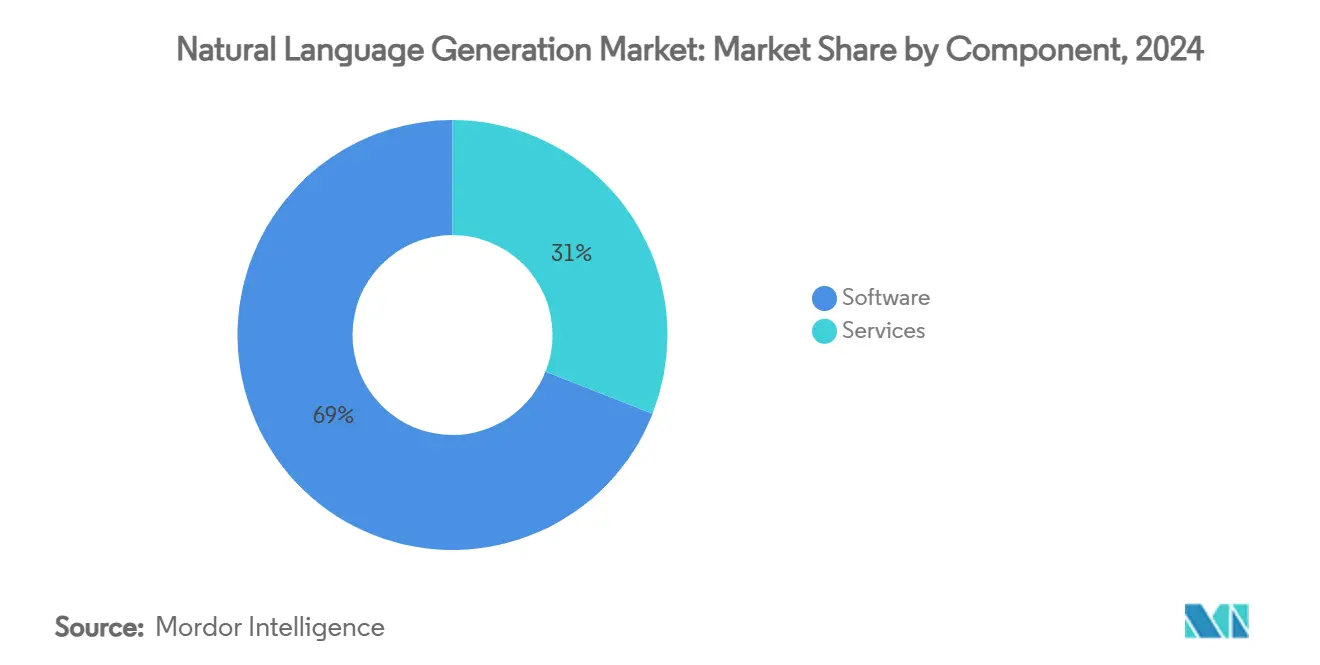

- By component, software captured 69.04% of the natural language generation market share in 2024. Services are projected to expand at a 19.35% CAGR through 2030, the fastest among all components.

- By deployment mode, cloud solutions held 62.87% of the natural language generation market size in 2024, while edge-enabled hybrid architectures are advancing at a 17.28% CAGR.

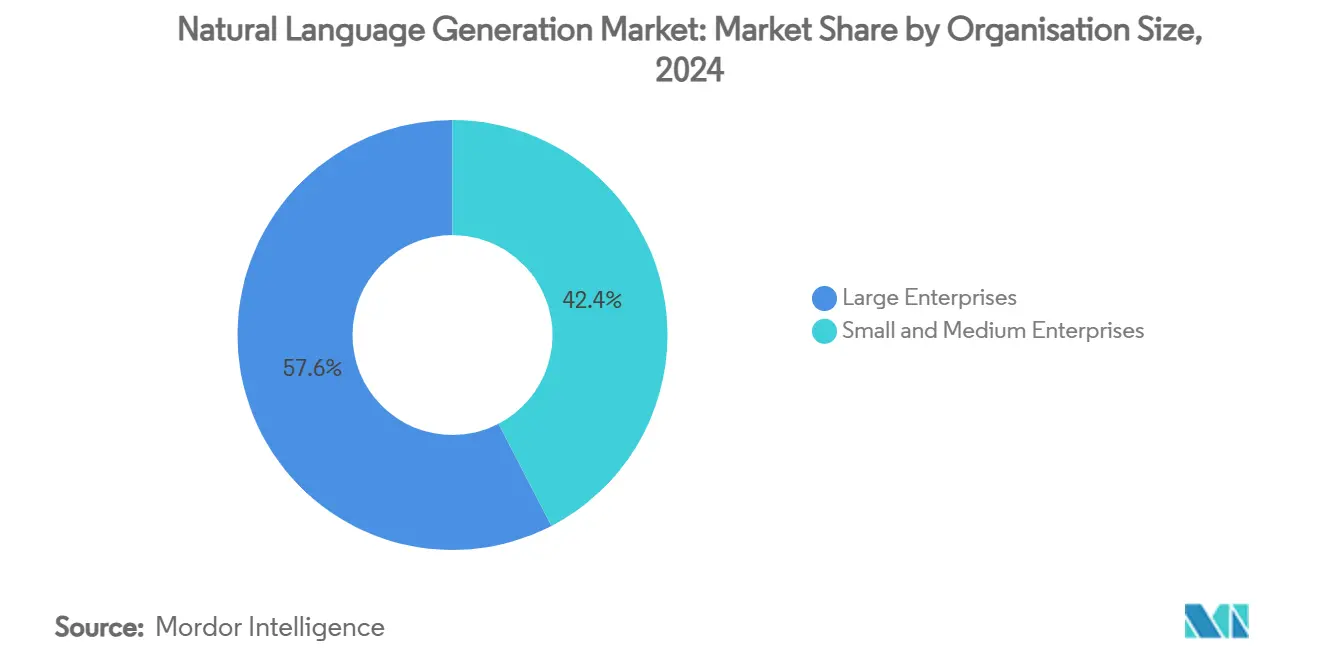

- By organisation size, large enterprises accounted for 57.61% of the natural language generation market share in 2024; small and medium enterprises are growing at a 19.05% CAGR during 2025-2030.

- By industry vertical, BFSI led with 23.47% revenue share in 2024; healthcare and life sciences are forecast to expand at an 18.62% CAGR to 2030.

- By geography, North America dominated with 38.51% revenue share in 2024, whereas Asia-Pacific is forecast to progress at a 20.09% CAGR to 2030.

Global Natural Language Generation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-personalised content at scale boosts ROI for digital-first enterprises | +3.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Real-time narrative generation required for Gen-AI copilots and autonomous agents | +4.1% | Global, early adoption in North America & APAC | Short term (≤ 2 years) |

| Rapid fall in large-language-model (LLM) inference costs widens SME adoption | +2.8% | Global, particularly impactful in APAC & emerging markets | Short term (≤ 2 years) |

| Regulatory pressure for explainable AI favours template-driven NLG in regulated sectors | +1.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Multilingual CX automation demand in emerging markets (Tier-2 languages) | +2.3% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Edge-deployment of lightweight NLG models in IoT devices and automobiles | +1.5% | Global, led by APAC manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyper-personalised content at scale boosts ROI

Enterprises deploying NLG across marketing, service, and operations have reported conversion-rate improvements of up to 25% and multi-function ROI multiples exceeding 3 times.[2]Salesforce, “Agentforce General Availability Announcement,” salesforce.com Real-time personalisation engines synthesise customer-behavior signals into dynamic product descriptions and investment summaries, preserving brand voice consistency across millions of interactions. Adoption accelerates as template design tools become accessible to non-technical staff, reducing prompt-engineering bottlenecks. Competitive differentiation increasingly hinges on the breadth of channels that a single model can address, from web and email to voice assistants. Vendors with robust content-governance controls gain preference in regulated verticals where messaging audit trails are mandatory.

Real-time narrative generation for Gen-AI copilots and autonomous agents

Sub-second latency requirements for copilots have shifted architectural priorities toward memory-efficient model quantisation and high-throughput edge inference stacks.[3]Microsoft Tech Community, “TaskWeaver: Framework for Agentic AI,” microsoft.com Customer-service agents must generate contextual explanations, action rationales, and follow-up instructions without cloud round-trips, supporting both human oversight and regulatory audit. Automotive OEMs are embedding small language models in infotainment units to deliver on-board voice guidance and vehicle-health summaries. The natural language generation market consequently sees heightened demand for toolchains that integrate code execution with narrative reporting, shortening time-to-value for agentic AI deployments.

Rapid fall in LLM inference costs widens SME adoption

API providers collectively reduced token fees by as much as 50% between 2024 and 2025, making enterprise-grade NLG affordable for resource-constrained firms. Volume discounts and pay-as-you-go tiers remove minimum-commitment hurdles, while multilingual base models cover Tier-2 languages out-of-the-box. SMEs now integrate automated product descriptions, knowledge-base articles, and customer-support scripts within weeks rather than months. This lower entry bar accelerates the natural language generation market penetration in emerging economies, where local language coverage previously demanded costly custom training.

Regulatory pressure for explainable AI favours template-driven NLG

The EU AI Act and SEC predictive-analytics rules require auditable reasoning for algorithmic outputs, motivating financial and healthcare organisations to lean on template-based or hybrid NLG systems. Rule-based scaffolding layers constrain generative outputs to predefined domains, minimising hallucination risk and simplifying compliance reporting. In clinical settings, automated discharge summaries must match structured coding standards such as ICD-10, emphasising controlled generation pipelines that pair neural fluency with symbolic validation. Vendors offering traceability dashboards and automated risk assessments differentiate in procurement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of high-quality domain-specific training data | -2.4% | Global, particularly acute in specialized industries | Medium term (2-4 years) |

| Rising concerns over AI-generated misinformation and legal liability | -1.8% | Global, with regulatory focus in North America & EU | Short term (≤ 2 years) |

| Integration complexity with legacy content-management stacks | -1.6% | Global, concentrated in large enterprises with established IT infrastructure | Medium term (2-4 years) |

| Vendor lock-in due to proprietary model ecosystems | -1.3% | Global, with particular concern in North America & EU regulated sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of high-quality domain-specific training data

Curated industry datasets remain scarce, inflating project timelines as enterprises spend up to 90% of budgets on data cleansing and annotation. Healthcare use cases encounter additional privacy hurdles under HIPAA, limiting access to clinical notes indispensable for accurate summarisation. Financial institutions invest tens of millions annually in document redaction and labeling efforts before model fine-tuning. Emerging markets face similar scarcity in local-language technical corpora, delaying deployment and dampening the natural language generation market growth trajectory.

Rising concerns over AI-generated misinformation and legal liability

Fortune 500 companies quadrupled AI-risk disclosures since 2022, reflecting rising uncertainty over content accuracy and downstream liability. Media houses worry about reputational damage from inadvertent factual errors, while insurers grapple with pricing new coverage categories for AI-related claims. Regulatory approaches diverge globally: the EU mandates stringent transparency for high-risk applications, whereas several Asia-Pacific jurisdictions adopt lighter-touch guidelines, complicating global rollouts. Enterprises respond with human-in-the-loop oversight, partially offsetting NLG productivity gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services drive implementation complexity

Software continued to dominate with 69.04% of the natural language generation market share in 2024. However, services revenue is rising at a 19.35% CAGR because enterprises require expertise in prompt engineering, workflow integration, and continuous model governance. Leading system integrators deliver outcome-based contracts covering data preparation, compliance validation, and periodic retraining. Managed service models appeal to organisations that lack in-house AI talent yet seek rapid time-to-value. This shift broadens the addressable natural language generation market, positioning consultancies alongside software vendors as primary value creators.

Services momentum also reflects escalating demand for change-management support. Line-of-business leaders need guidance on when to embed NLG engines into content-supply chains, how to redesign approval workflows, and which metrics validate success. Retainer-style optimisation packages account for a growing share of post-deployment spend, reinforcing the natural language generation industry’s pivot toward recurring revenue streams.

By Deployment Mode: Cloud dominance faces edge-computing challenge

Cloud platforms captured 62.87% of the natural language generation market size in 2024, but hybrid architectures combining cloud training with edge inference are expanding at a 17.28% CAGR. Organisations route high-complexity queries to cloud models while processing latency-sensitive tasks locally, achieving compliance with data-residency mandates. Automotive, manufacturing, and telecom firms lead adoption of on-device generation to avoid network congestion and ensure service continuity.

Edge-first strategies accelerate as GPU-equipped client hardware becomes mainstream and memory-efficient model formats lower footprint requirements. Cloud vendors respond with toolkits that compile large checkpoints into quantised runtimes targeting CPUs, NPUs, and embedded accelerators. This interplay ensures sustained cloud revenue while enabling new device-centric natural language generation market offerings.

By Organisation Size: SME adoption accelerates through API democratisation

Large enterprises commanded 57.61% of the natural language generation market share in 2024 by embedding NLG into omnichannel customer communication suites and regulatory reporting pipelines. Yet SMEs represent the fastest-growing cohort, expanding at a 19.05% CAGR on the back of low-commitment API pricing and low-code orchestration dashboards. Merchant-side e-commerce platforms auto-generate product descriptions, return policies, and multilingual FAQs, cutting content-creation cycles from days to minutes.

Funding inflows target self-service platforms that package templates, style guides, and analytics in a single pane of glass. These offerings obviate the need for data-science teams, democratising access and increasing the overall natural language generation market penetration rate among resource-constrained firms.

By Industry Vertical: Healthcare emerges as high-growth opportunity

BFSI remained the largest adopter with 23.47% revenue share in 2024, driven by regulatory reporting and personalised advisory summaries. Healthcare and life sciences are projected to grow at an 18.62% CAGR, the fastest among all verticals, as hospitals automate clinical documentation, discharge summaries, and insurance-coding narratives. Accurate terminology handling and auditability make NLG preferable to manual transcription, directly improving reimbursement accuracy.

Manufacturing uses NLG for multilingual safety data sheets and maintenance manuals, while retail focuses on dynamic product content that lifts conversion rates. Media and entertainment experiments with script-localisation and AI-assisted storyboards, highlighting the breadth of natural language generation market applications beyond back-office automation.

Geography Analysis

North America led with 38.51% natural language generation market share in 2024, supported by USD 14 billion in generative-AI venture funding and clear procurement pathways within federal agencies. Cross-industry cloud partnerships accelerate deployments, though concentration risk around a small number of foundation-model providers raises strategic supply-chain concerns. Europe prioritises sovereign AI and explainability, encouraging domestic vendors and open-source consortia. The EU AI Act sets rigorous standards that influence global product design, benefiting suppliers capable of delivering traceable outputs.

Asia-Pacific posts the highest regional CAGR at 20.09% through 2030, underpinned by China’s national funding programmes that channel billions into domestic model development. Localised language support is essential across Southeast Asia, spurring partnerships between cloud hyperscalers and regional telcos. South America, the Middle East, and Africa remain nascent but promising, backed by government digitisation agendas and improving connectivity infrastructure. Collectively, these dynamics sustain a geographically diversified demand profile for the natural language generation market.

Competitive Landscape

The natural language generation market remains moderately fragmented; no single vendor controls beyond 15% share. Technology giants compete on model performance and ecosystem breadth, while enterprise software providers differentiate via domain-tailored workflows and compliance tooling. Patent filings exceeded 14,000 families by 2023, signalling intensified intellectual-property positioning. Recent integrations of IBM Granite models into Salesforce Einstein illustrate platform convergence, giving customers integrated toolchains rather than point solutions.

Emerging challengers target under-served SME segments with template-rich, no-code interfaces, while edge-native startups optimise runtimes for hardware-constrained environments. Strategic partnerships centre on data-sharing, sovereign deployments, and joint go-to-market programmes. Ongoing regulatory scrutiny over large-scale acquisitions may slow consolidation, preserving innovation lanes for niche specialists and regional champions within the natural language generation industry.

Natural Language Generation Industry Leaders

Alphabet Inc. (Google)

Microsoft Corporation

International Business Machines Corporation (IBM)

Amazon Web Services, Inc.

Salesforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Zhipu AI secured USD 140 million from Shanghai state-backed investors to accelerate model commercialisation and prepare for IPO, reinforcing China’s sovereign-AI ambitions.

- March 2025: Salesforce launched Agentforce 2dx, adding proactive multimodal agents that embed seamlessly into enterprise workflows, signalling a shift from conversational copilots to autonomous process orchestrators.

- January 2025: OpenAI introduced ChatGPT Gov on Microsoft Azure, enabling U.S. government agencies to deploy secure NLG services within FedRAMP-authorised environments.

- October 2024: SAP enhanced its Joule copilot with collaborative agents and a knowledge-graph backbone, sharpening its value proposition for regulated European customers.

Global Natural Language Generation Market Report Scope

| Software |

| Services |

| On-Premises |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| Media and Entertainment |

| Manufacturing |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Turkey | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and eCommerce | |||

| Media and Entertainment | |||

| Manufacturing | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Turkey | |||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the natural language generation market by 2030?

The market is forecast to reach USD 2.83 billion by 2030, expanding at a 15.86% CAGR.

Which component is growing fastest in natural language generation deployments?

Professional services are expanding at a 19.35% CAGR as enterprises seek expertise in integration, compliance, and continuous optimisation.

Why are SMEs increasingly adopting natural language generation solutions?

Token-based API pricing and low-code orchestration tools remove large upfront costs, enabling SMEs to automate content creation rapidly.

Which industry vertical offers the highest growth potential for NLG vendors?

Healthcare and life sciences lead with an 18.62% CAGR due to clinical documentation automation and strict compliance needs.

How are regulatory frameworks influencing NLG technology choices?

Rules such as the EU AI Act prioritise explainability, steering financial and healthcare organisations toward template-driven or hybrid NLG systems with transparent audit trails.

What emerging deployment trend is reshaping NLG architectures?

Hybrid cloud-edge models run training in the cloud while executing latency-sensitive inference on local devices, reducing bandwidth and meeting data-sovereignty requirements.

Page last updated on: