Market Overview

| Study Period | 2020 - 2031 |

|---|---|

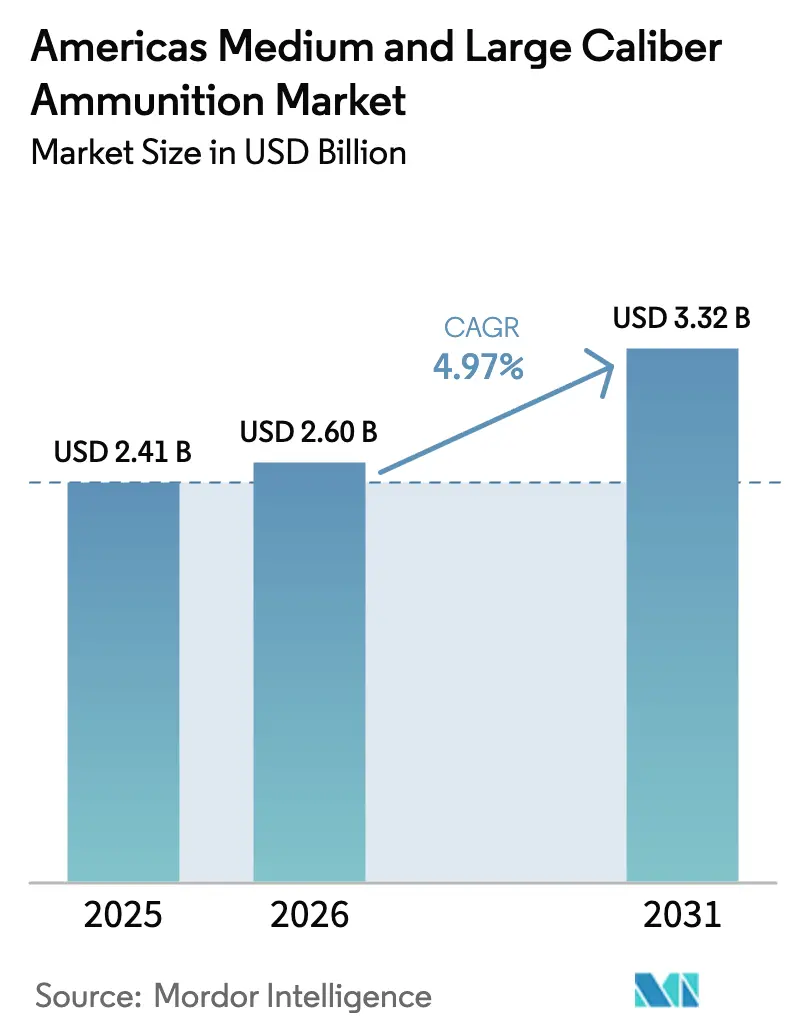

| Base Year Market Size (2025) | USD 2.41 Billion |

| Market Size (2026) | USD 2.60 Billion |

| Market Size (2031) | USD 3.32 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Medium And Large Caliber Ammunition Market Analysis by Mordor Intelligence

The Americas medium and large caliber ammunition market size is expected to grow from USD 2.41 billion in 2025 to USD 2.6 billion in 2026 and is forecasted to reach USD 3.32 billion by 2031 at a 4.97% CAGR over 2026-2031. The market is currently absorbing most of the new production capacity from facilities in the US, Brazil, and Mexico, helping producers mitigate the effects of raw material inflation and occasional delays in congressional budgets. Modernization initiatives for armored vehicles, frigates, and expeditionary artillery are expanding the customer base, while border security operations are driving ammunition consumption to levels not seen since combat rotations. The adoption of guided projectiles is increasing the average selling price per round; however, unguided munitions are expected to account for 80% of 2026 deliveries, as suppression fire and live-fire training requirements cannot be met with shells costing USD 8,000. Suppliers capable of incorporating insensitive and lead-free chemistries without compromising range or lethality are likely to gain a competitive edge as green-ammunition mandates extend beyond California to the US Department of Defense (DoD).

Key Report Takeaways

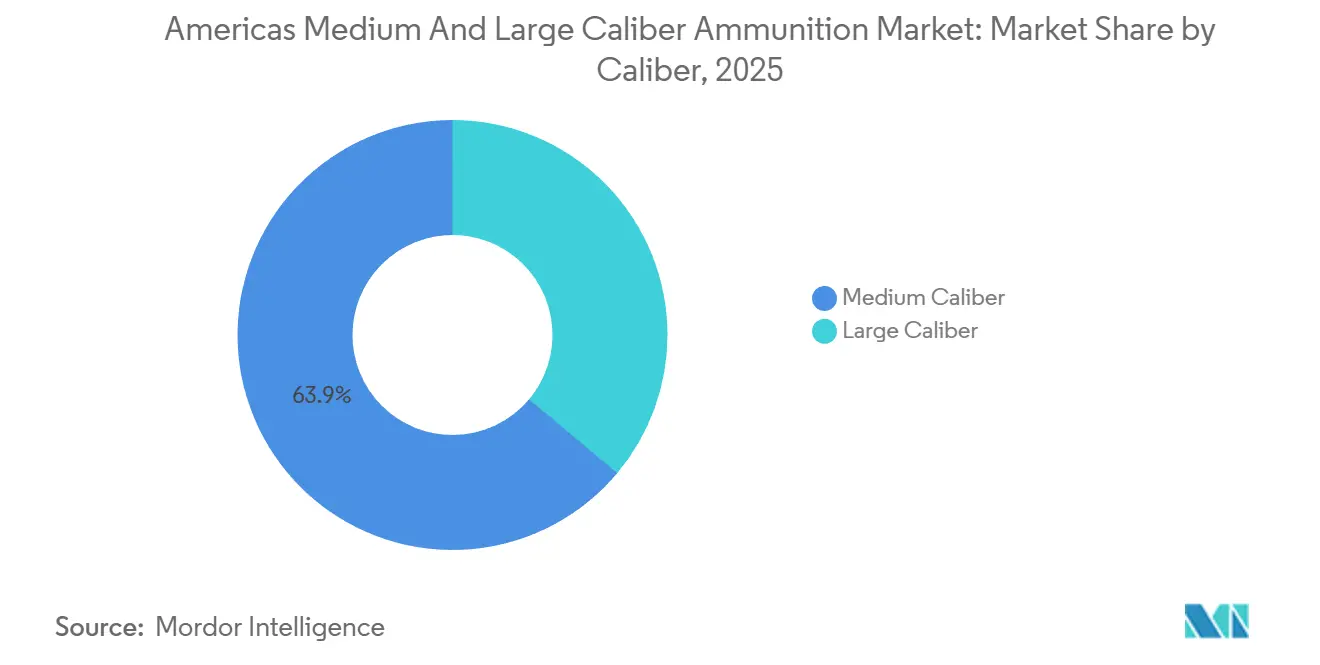

- By caliber, medium rounds led with 63.89% of the Americas medium and large caliber ammunition market share in 2025; large-caliber ammunition is forecasted to expand at a 5.21% CAGR through 2031.

- By product, artillery shells and mortars captured 53.41% of 2025 revenue, while aerial bombs and grenades are on track to grow at a 6.34% CAGR to 2031.

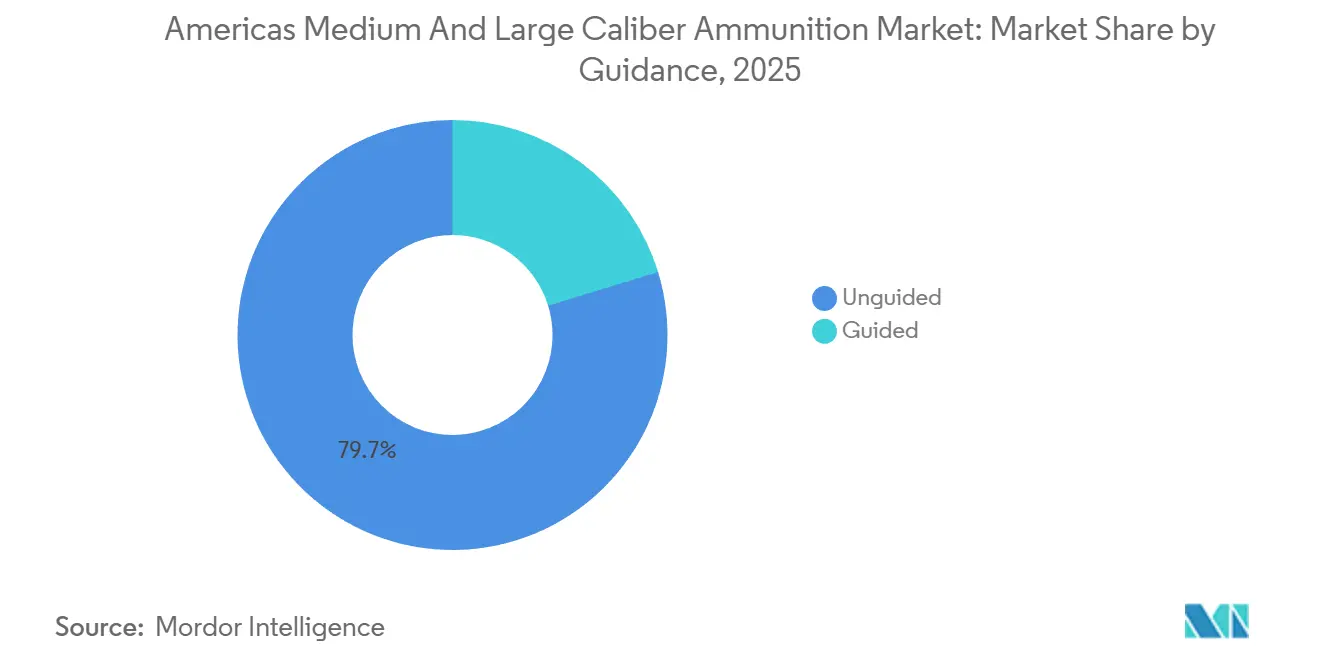

- By guidance, unguided munitions held a 79.73% share in 2025, whereas guided rounds are expected to rise at an 8.43% CAGR through 2031.

- By end-user, the military segment dominated with a 89.84% share in 2025; law enforcement demand is advancing at a 5.67% CAGR to 2031.

- By platform, land systems commanded a 68.75% share in 2025, and naval programs are forecasted to record a 5.84% CAGR through 2031.

- By geography, North America dominated with 73.82% of regional spending in 2025, whereas South America is the fastest-growing market, with a 5.19% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Americas Medium And Large Caliber Ammunition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense budgets across the Americas | +1.20% | North America, with spillover to Brazil and Chile | Medium term (2-4 years) |

| Modernization of armored and artillery platforms | +1.40% | United States, Canada, Brazil | Long term (≥ 4 years) |

| Geopolitical tensions and border-security operations | +0.90% | United States-Mexico border, Colombia-Venezuela frontier | Short term (≤ 2 years) |

| Replacement of aging ammunition stockpiles | +0.80% | United States, Canada, legacy Cold War inventories in South America | Medium term (2-4 years) |

| Surge in joint hemispheric training exercises | +0.50% | Global, concentrated in Pacific and Caribbean theaters | Short term (≤ 2 years) |

| Growth of local ammunition manufacturing in South America | +0.60% | Brazil, Mexico, Colombia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Budgets Across the Americas

Defense budgets across the Americas reached USD 912 billion in 2025, with a significant focus on ammunition allocations. The US increased its ammunition budget to USD 2.1 billion, emphasizing multi-year contracts to support industry investments in tooling and production stability. Canada allocated CAD 553 million (USD 398.18 million), enabling bulk purchases of 155mm and 50mm rounds for Arctic operations.[1]Government of Canada, “Strong, Secure, Engaged,” canada.ca Brazil’s BRL 137 billion (USD 25.58 billion) defense budget included funding for insensitive-munition conversions, providing IMBEL with a stable multi-year revenue stream. Mexico allocated MXN 178 billion (approximately USD 9.90 billion) to bolster National Guard inventories, demonstrating the influence of homeland-security agencies on the medium- and large-caliber ammunition market, particularly when conventional military budgets face constraints. Chile maintained its overall defense budget but redirected 18% of procurement funds to consumables, with a particular focus on ammunition as a critical component for operational readiness.

Modernization of Armored and Artillery Platforms

Modernization programs for armored and artillery platforms are driving diversification in demand for calibers. The US Army’s M109A7 Paladin now uses insensitive 155mm rounds requiring thicker-walled cases, while Canada’s LAV III upgrade to the XM913 50mm cannon has established a new caliber standard. Brazil’s Guarani APC and Mexico’s DN-XI IFV adopted 40mm and 30mm weapons, respectively, shifting away from the previously dominant 25mm calibers. The US Marine Corps’ ACV-30 employs MK 310 programmable ammunition, which doubles the annual consumption per vehicle. The US Army’s ERCA gun extends the 155mm range to 70 kilometers, necessitating stricter controls on steel grain structure. These modernization efforts are expected to continuously refresh SKU lists in the Americas medium and large caliber ammunition market through 2031, with retrofits impacting the entire supply chain.

Geopolitical Tensions and Border-Security Operations

Geopolitical tensions and border-security operations have intensified, leading to increased ammunition demand. Along the Rio Grande, US Customs and Border Protection (CBP) reported a 19% rise in incidents requiring small-unit direct fire, prompting a USD 47 million increase in its FY 2026 ammunition request. Mexico’s National Guard consumed training stocks three times faster than usual, forcing SEDENA to expedite procurement processes by utilizing military reserves. Colombia experienced a 34% increase in 105mm and 155mm shell usage during operations near Cúcuta, while Chile’s 25mm ammunition consumption rose by 27% in anti-smuggling patrols. These surges have shortened lead times in the Americas medium and large caliber ammunition market, requiring manufacturers to operate additional shifts to meet urgent replenishment demands.

Replacement of Aging Ammunition Stockpiles

The replacement of aging ammunition stockpiles is becoming a priority due to rising demilitarization costs. The US Army identified 22% of its 155mm inventory as exceeding the 30-year safety limit, incurring disposal costs before new rounds can be procured. Canada reported 14,000 tons of obsolete Cold War-era ammunition, while Brazil disclosed that 38% of its 105mm stocks failed insensitive-munition standards. Mexico revealed that 60% of its 120mm tank ammunition dates back to pre-1995 production, posing safety and performance risks. Chile’s transition to Rheinmetall DM121 shells reflects a broader trend across the continent: replacement spending is focused on structural turnover rather than consumption growth, ensuring baseline demand in the Americas medium and large caliber ammunition market through the decade.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent export control and ITAR compliance costs | -0.70% | United States exports to non-NATO LATAM buyers | Medium term (2-4 years) |

| Volatility in raw-material prices (copper, steel, propellants) | -0.90% | Global, acute in North America and Brazil | Short term (≤ 2 years) |

| Environmental regulations on lead and energetic materials | -0.40% | United States (California, federal lands), Canada | Long term (≥ 4 years) |

| Shift toward precision-strike alternatives (loitering munitions) | -0.30% | United States, Canada, limited LATAM adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Export Control and ITAR Compliance Costs

Export controls and ITAR compliance are imposing high costs on ammunition exports. ITAR filings add USD 1,200–1,800 per line item, extend approval timelines, and increase shipment costs by 12–15%. The average wait time of 127 days deters smaller US suppliers from pursuing quick-turn orders.[2]Government Accountability Office, “Defense Export Controls,” gao.gov Mexico incurred USD 2.3 million in compliance costs for a USD 21 million grenade purchase, leading to a preference for non-ITAR suppliers from South Korea and Israel. Brazil’s IMBEL faced a nine-month delay in ramping up 155mm production due to US propellant ingredient waivers. At the same time, Colombia canceled a US joint venture over projected compliance costs of USD 4.8 million. These regulatory challenges benefit European and South American manufacturers, reducing the market share available to US exporters in the Americas medium and large caliber ammunition market.

Volatility in Raw-Material Prices (Copper, Steel, Propellants)

Fluctuations in raw material prices are impacting ammunition production costs. Copper prices remained at USD 4.20 per pound in December 2025, an 18% increase from 2024, while steel coil prices rose by 14%. A fire at the Radford plant disrupted US nitrocellulose production, forcing General Dynamics and Northrop to import from Europe at a 19% premium. CBC Global reported a 3.2-point margin reduction, and IMBEL faced a 21% increase in steel-billet costs as Vale prioritized exports. Larger manufacturers are mitigating risks through five-year take-or-pay contracts. Still, smaller South American firms lack the financial leverage to hedge their risks effectively, thereby increasing their vulnerability to consolidation. This raw-material volatility limits profit margins and discourages capacity expansions dependent on stable input costs, constraining growth in the Americas medium and large caliber ammunition market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Caliber: Medium Strength Prevails, Large Accelerates

Medium rounds led the Americas medium and large caliber ammunition market in 2025, accounting for a 63.89% share. This dominance is attributed to the widespread use of 20–40mm guns on infantry vehicles, close-in weapon systems (CIWS), and attack helicopters. However, demand for large-caliber ammunition is expected to grow at a CAGR of 5.21%, driven by programs such as the ERCA initiative and Brazil’s ASTROS rocket-artillery expansion, both of which emphasize 155mm shells. The market size for large-caliber projectiles is projected to increase from approximately USD 1 billion in 2026 to USD 1.3 billion by 2031. Notable contracts, such as General Dynamics’ USD 465 million agreement in July 2025 for 120mm M1002 training rounds, highlight sustained demand from the Abrams fleet, while Northrop’s Bushmaster contract supports medium-caliber production through 2028.

The market faces a strategic balance between volume and lethality. Medium calibers are cost-effective and support rapid-fire tactics essential for border patrol, naval interdiction, and urban defense. In contrast, large calibers offer higher payloads, extended range, and superior performance in peer warfare scenarios. Innovations like Textron’s XM204 120mm top-attack round, priced at USD 12,000 and capable of defeating active-protection systems, blur the distinction between shells and missiles. However, logistical challenges persist, as seen in Canada’s adoption of a 50mm cannon for its LAV III, which necessitated funding a standalone ammunition line due to limited allied stockpiles. These divergences complicate efforts to standardize SKUs, increasing inventory costs for coalition planners.

By Product: Artillery Dominance, Aerial Momentum

Artillery shells and mortars accounted for 53.41% of revenue in 2025, solidifying their position as the cornerstone of the Americas medium and large caliber ammunition market. US monthly production targets of 70,000 155mm shells could generate approximately USD 1.7 billion in annual revenue by 2031, assuming unit prices for unguided variants remain near USD 1,050. Aerial bombs and grenades are expected to grow at a CAGR of 6.34%, supported by the AH-1Z Viper and A-10 fleets, which utilize programmable fuzes that increase average selling prices without significantly raising material costs. The USD 819 million Amtec training-grenade contract demonstrated the potential for economies of scale in this previously fragmented sub-sector, creating a strategic revenue stream for suppliers adept at producing low-cost composite casings.

Mortar ammunition, once considered a niche product, has seen renewed interest as light-infantry units shift from relying on heavy artillery to adopting mobile firepower. For instance, Orbital ATK’s M821A3 insensitive 81mm round completed fielding with the Marine Corps in June 2025, establishing a baseline reorder rate that mitigates potential declines in 120mm tank ammunition consumption. Brazil’s ASTROS system, which integrates 127mm rockets and tube artillery, has attracted new electronics suppliers to the value chain, as these hybrid systems require GPS, data links, and fuse setters traditionally absent from conventional shell production.

By Guidance: Unguided Mass, Guided Upswing

Unguided ammunition accounted for 79.73% of shipments in 2025 and is projected to maintain nearly two-thirds of the market share by 2031. This dominance reflects the cost-effectiveness and simplicity of unguided rounds, which remain a staple for many military operations. However, guided ammunition is expected to grow at a CAGR of 8.43%, capturing over one-quarter of the total market value by the end of the forecast horizon. Growth in the guided segment is supported by products like XM1113 RAP shells and Elbit’s SIGMA family, which aim for ranges of up to 70 kilometers.

Despite advancements, challenges remain, such as GPS jamming at the US National Training Center, which reduced Excalibur hit rates to 68% and prompted the Army to procure SPIKE NLOS man-portable missiles as a contingency. Cost remains a barrier, with precision 155mm rounds priced at seven times the cost of unguided variants. In South America, armies continue to rely on unguided ammunition until local licensing of seeker assemblies by US or Korean suppliers reduces costs below USD 3,000, enabling broader adoption. The gradual shift toward guided ammunition reflects a broader trend of increasing precision and technological integration in modern warfare, although cost and logistical challenges remain significant hurdles to overcome.

By End-User: Military Core, Law-Enforcement Lift

Military forces accounted for 89.84% of the market revenue in 2025; however, law enforcement is emerging as a growing segment with a CAGR of 5.67%. Notable examples include the US Customs and Border Protection’s USD 47 million ammunition order and Brazil’s Federal Police procurement of 800,000 12.7mm rounds. These developments highlight the increasing role of internal security forces in driving demand for specialized ammunition.

Urban operations favor medium calibers with low-fragmentation profiles, creating opportunities for product specialization. This shift enables smaller firms producing non-lethal 40mm grenades to scale up production, a market previously dominated by military contracts. The growing involvement of law enforcement agencies in the ammunition market highlights the expanding scope of applications for medium and large-caliber ammunition, thereby further diversifying the customer base and driving innovation in product design and manufacturing processes.

By Platform: Land Weight, Naval Upside

Land systems accounted for 68.75% of the market share in 2025, providing a stable baseline for tonnage through 2031. These systems remain critical for ground-based operations, providing a consistent demand for medium- and large-caliber ammunition. However, the naval segment is expected to grow at a CAGR of 5.84%, driven by the introduction of new frigates and destroyer upgrades equipped with Mk 45 Mod 4 guns, each consuming approximately 1,200 rounds annually.

Airborne demand, however, faces challenges. The retirement of the A-10 fleet will eliminate the need for approximately 1.8 million annual 30mm training rounds. While AH-64E and AC-130 fleets will partially offset this decline, overall airborne ammunition consumption may decrease by 18% by 2031 unless unmanned gunships enter production. The evolving dynamics across land, naval, and airborne platforms highlight the diverse and shifting demands within the Americas medium and large caliber ammunition market, emphasizing the need for adaptability and innovation among suppliers.

Geography Analysis

North America continues to lead the Americas medium and large caliber ammunition market, although its internal market dynamics are evolving. The US, with a 66.54% market share in 2025, is prioritizing rebuilding strategic reserves through fixed-price contracts that mitigate supplier capital-expenditure risks. In Canada, a one-time CAD 553 million (USD 398.18 million) replenishment is expected to drive a spike in volumes during 2025-2026. Still, orders are projected to decline once backfilling for Ukraine is completed. Meanwhile, Mexico, with a 5.15% CAGR, is emerging as the region's growth driver, supported by National Guard deployments and the DN-XI program, which consumes 180,000 30mm rounds annually. This varied pace of growth across the region necessitates differentiated pricing strategies: long-term US contracts favor discount structures, Canadian spot purchases require surge capacity, and Mexican agreements depend on regulatory flexibility.

South America accounted for 25.50% of the market's revenue and is actively reshaping trade flows. Brazil's IMBEL facility is adding 120,000 155mm shells to the regional supply, reducing reliance on US exports, which are constrained by ITAR regulations.[3] Janes, “Brazil Defense Budget 2025,” janes.com Chile has increased ammunition spending to 18% of its procurement budget, while Colombia turned to Poongsan Corporation for emergency shell supplies when inventories fell below training requirements.

Despite budgetary challenges, Argentina allocated 22% of its procurement budget to 105mm ammunition, recognizing the critical role of consumables in maintaining readiness. Peru's riverine programs have tripled the use of 20mm rounds, exposing inventory shortages that regional manufacturers, such as FAMAE and Indumil, aim to address through brokerage. Local production capacity is growing at an annual rate of 12-15%, offering a viable alternative for neighboring countries and reducing delivery times from 12 months to under six months.

Brazil's export initiatives, supported by agreements to supply Paraguay, Uruguay, and Ecuador, indicate that South-South trade channels could reduce US export dominance by up to 22% by 2030. Technology transfer agreements are enabling Chile and Colombia to license-produce specialized ammunition, providing a safeguard against supply disruptions. For manufacturers, this shift places downward pressure on margins unless offset by innovations such as insensitive munitions or embedded proximity fuzes. The evolving market landscape marks a change from a US-centric export model to a decentralized ecosystem, where flexibility in capacity and compliance is increasingly prioritized over sheer scale.

Competitive Landscape

The industry concentration is moderate. General Dynamics, Northrop Grumman, and BAE Systems accounted for 48% of the North American market value in 2025, supported by long-term contracts that ensure production line rates will continue until at least 2028. General Dynamics’ Mesquite plant achieved a production output of 30,000 shells per month. Combined with the vertical integration of propellant production at the Radford facility, the company is positioned to internalize margins across the supply chain. Northrop Grumman’s December 2025 contract, valued at USD 200 million for XM1211 laser-guided rounds, highlights its capabilities in electronic integration. BAE Systems maintains a strong presence in naval segments with the Mk 45 Mod 4 gun and supplies insensitive 155mm rounds for the M109A7, leveraging its expertise across multiple domains. RTX continues to hold significant intellectual property in proximity fuzes but has lagged in securing recent artillery contracts.

Regional competitors are gaining traction. IMBEL’s heavy-munition production line has secured both domestic Brazilian and export orders. CBC Global’s Oklahoma facility is targeting contracts from the National Guard and Mexican buyers, while Chile’s FAMAE and Colombia’s Indumil are addressing sub-regional demand with shorter lead times. These emerging players focus on lower-volume tenders that are less attractive to major industry incumbents, gradually eroding the market share of established firms in the Americas medium and large-caliber ammunition market. Regulatory flexibility has become a key competitive advantage. Compliance with EPA and DoD green standards, along with strategies to navigate ITAR restrictions, allows bidders to reduce effective prices by 8-10%. Smaller US operators, such as American Ordnance, leverage government-owned, contractor-operated facilities to minimize capital expenditures. However, their limited product catalogs restrict their export potential. As a result, the competitive focus is shifting from manufacturing scale to a combination of portfolio diversity and regulatory expertise.

Americas Medium And Large Caliber Ammunition Industry Leaders

General Dynamics Corporation

Northrop Grumman Corporation

BAE Systems plc

RTX Corporation

Indústria de Material Bélico do Brasil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The US Army awarded Northrop Grumman Corporation a contract exceeding USD 200 million to produce the XM1211 High Explosive Proximity (HEP) fuzed round of medium-caliber ammunition. This contract represents a key milestone in advancing next-generation munitions for short-range air defense against small Unmanned Aerial Systems (UAS). The XM1211 is a 30x113mm round equipped with a proximity sensor that detonates upon detecting a target within range, releasing fragmentation to neutralize the threat.

- July 2025: The Department of the Army’s Joint Munitions Command awarded General Dynamics Ordnance and Tactical Systems a contract worth up to USD 464.60 million for the production of 120mm M865A1 tank training ammunition.

Americas Medium And Large Caliber Ammunition Market Report Scope

Medium and large caliber ammunition includes cartridge-based, artillery, and aerial ordnance, ranging from 20mm rounds to 155mm projectiles, which support land, naval, and airborne weapon systems across the Americas. This study examines all stages of the value chain, including new manufacturing, depot-level refurbishment, and insensitive munitions upgrades, covering cartridge cases, projectiles, propellants, fuzes, and related components procured by military and law enforcement agencies in the region. Small-arms ammunition below 20mm caliber and missile warheads are excluded from this analysis.

The Americas medium and large caliber ammunition market is segmented by caliber, product type, guidance technology, end user, platform, and geography. By caliber, the market is categorized into medium caliber and large caliber. By product type, the market is divided into rounds, artillery shells and mortars, and aerial bombs and grenades. Based on guidance technology, the market is segmented into guided and unguided ammunition. By end user, it is classified into military and law enforcement. By platform, it is segmented into land, naval, and airborne weapon systems. The report also covers the market sizes and forecasts for the Americas medium and large caliber ammunition market in major countries across the regions. For each segment, the market size is provided in terms of value (USD).

By Caliber

| Medium Caliber |

| Large Caliber |

By Product

| Rounds |

| Artillery Shells and Mortars |

| Aerial Bombs and Grenades |

By Guidance

| Guided |

| Unguided |

By End-User

| Military |

| Law Enforcement |

By Platform

| Land |

| Naval |

| Airborne |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America |

| By Caliber | Medium Caliber | |

| Large Caliber | ||

| By Product | Rounds | |

| Artillery Shells and Mortars | ||

| Aerial Bombs and Grenades | ||

| By Guidance | Guided | |

| Unguided | ||

| By End-User | Military | |

| Law Enforcement | ||

| By Platform | Land | |

| Naval | ||

| Airborne | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Americas medium and large caliber ammunition market by 2031?

The Americas medium and large caliber ammunition market is expected to reach USD 3.32 billion by 2031, reflecting sustained demand across military and security agencies.

Which platform category is set for the fastest growth?

Naval guns, supported by new frigate classes and destroyer overhauls, are forecasted to grow at a 5.84% CAGR through 2031.

Why are large-caliber rounds gaining traction despite higher costs?

Programs like ERCA and continued Abrams training requirements need extended-range, high-lethality shells that medium calibers cannot provide.

How are environmental regulations influencing procurement?

Mandates for lead-free and insensitive munitions add up to USD 1.20 per round but open new contract channels for compliant suppliers.

Which Latin American country is emerging as a regional exporter?

Brazil, via IMBEL’s new plant capable of producing 120,000 155mm shells annually for domestic use and neighboring countries.

How significant is guided ammunition adoption in value terms?

Guided rounds could account for more than 25% of Americas medium and large caliber ammunition market value by 2031, even while remaining a minority in volume.

Page last updated on: