Nasopharyngeal Cancer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nasopharyngeal Cancer Market Analysis by Mordor Intelligence

The nasopharyngeal cancer market size is expected to grow from USD 1.14 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 1.68 billion by 2031 at 6.66% CAGR over 2026-2031. The market’s ascent mirrors rapid clinical adoption of PD-1/PD-L1 checkpoint inhibitors, which have shifted the therapeutic focus from exclusive reliance on platinum-based chemotherapy toward durable immunologic control of recurrent and metastatic disease [1]National Cancer Institute, “Checkpoint Inhibitors in Head and Neck Cancer,” cancer.gov . Rising reimbursement for precision diagnostics, broader inclusion of endemic populations in global trials, and regional manufacturing of immunotherapy biologics further accelerate growth momentum. Competitive dynamics now hinge on combination-therapy life-cycle strategies, while hospital systems increasingly standardize EBV DNA screening to triage patients into risk-stratified care pathways. In parallel, artificial-intelligence tools that automate IMRT contouring reduce clinician workload and raise throughput, reinforcing radiotherapy as a complementary pillar rather than a displaced modality.

Key Report Takeaways

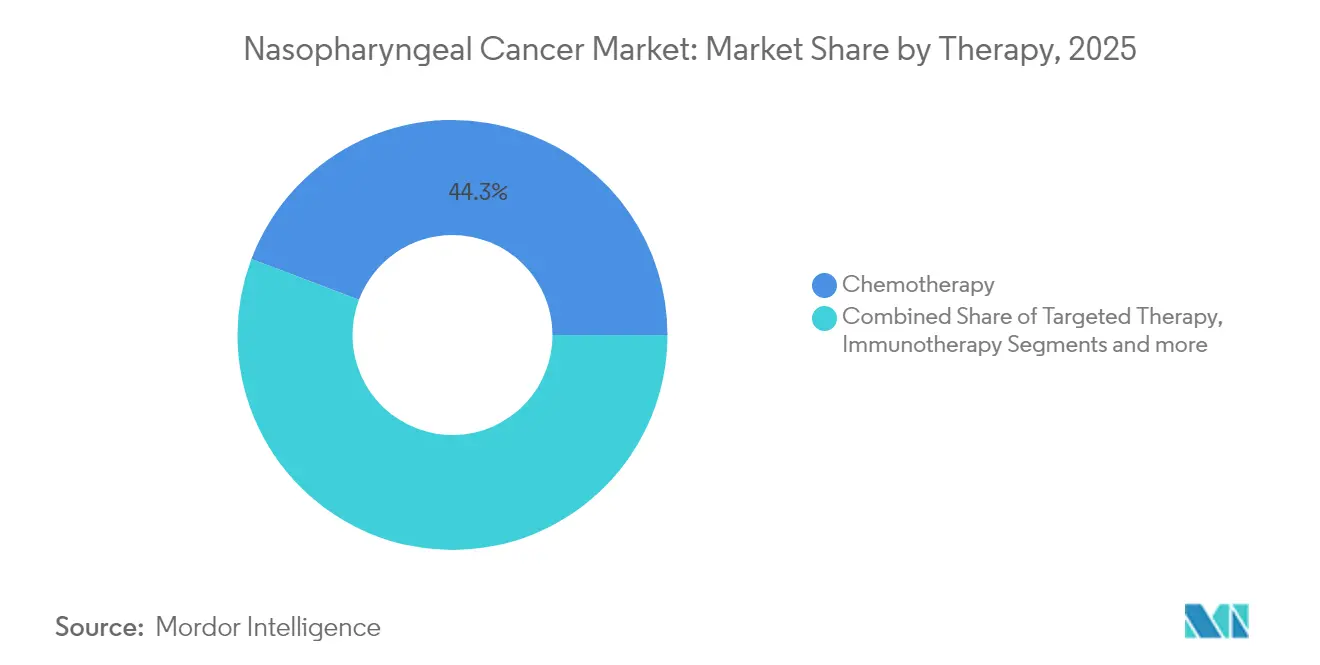

- By therapy, chemotherapy retained 44.25% share of the nasopharyngeal cancer market size in 2025, whereas immunotherapy is projected to post the fastest 7.48% CAGR through 2031.

- By end-user, hospitals and specialty clinics commanded 67.10% revenue share in 2025, while ambulatory surgery centers are set to grow at 7.33% CAGR to 2031.

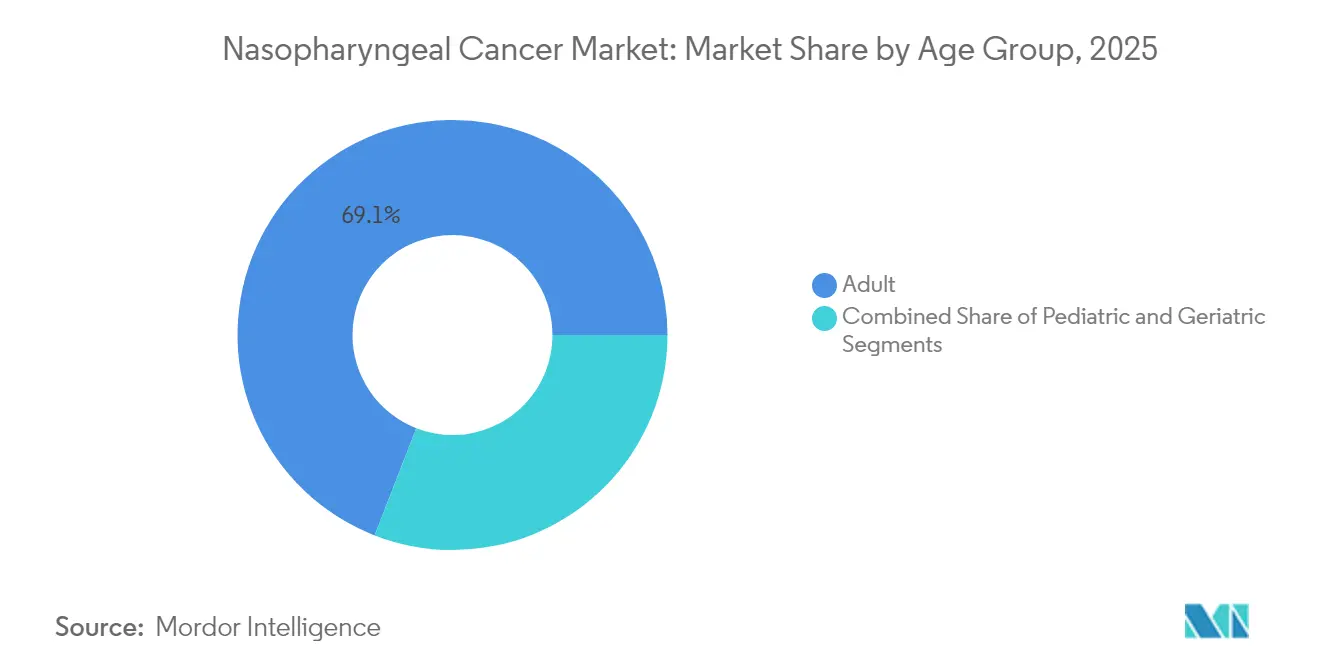

- By age group, adults accounted for 69.10% of the nasopharyngeal cancer market size in 2025, while the geriatric segment is on track for a 7.44% CAGR during 2026-2031.

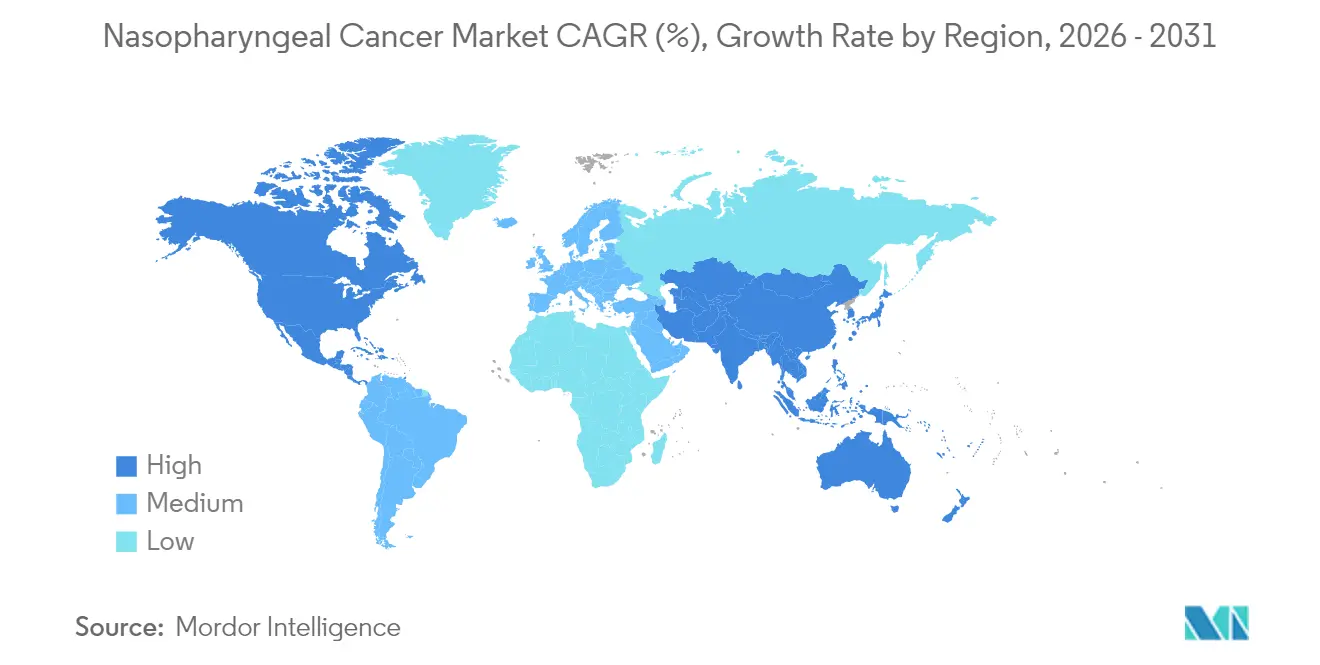

- By geography, Asia-Pacific led with 41.20% nasopharyngeal cancer market share in 2025 and is forecast to expand at a 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Nasopharyngeal Cancer Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence in endemic East & South-East Asia | +2.1% | Asia-Pacific core, spill-over to global diaspora populations | Medium term (2-4 years) |

| Regulatory orphan-drug & fast-track incentives | +1.8% | Global, with early gains in US, EU, Asia-Pacific | Short term (≤ 2 years) |

| Breakthrough results of PD-1/PD-L1 checkpoint inhibitors | +2.3% | Global | Short term (≤ 2 years) |

| Plasma EBV-DNA guided precision medicine protocols | +1.4% | Global, concentrated in endemic regions | Medium term (2-4 years) |

| AI-enabled IMRT planning & automated MRI segmentation | +1.2% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Accelerating EBV/HPV prophylactic vaccine pipelines | +0.9% | Global, prioritized in endemic regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Breakthrough Results of PD-1/PD-L1 Checkpoint Inhibitors

PD-1 antibodies such as toripalimab and penpulimab have produced clinically meaningful extensions in progression-free survival when combined with platinum-based chemotherapy, underscoring their emergence as first-line standards for recurrent or metastatic disease. Phase III evidence documented median PFS of 21.4 months for toripalimab–chemotherapy versus 8.2 months for placebo–chemotherapy in the JUPITER-02 study. The FDA then granted penpulimab breakthrough, orphan, and fast-track statuses, culminating in its April 2025 approval that shortened development timelines by nearly 18 months [2]U.S. Food and Drug Administration, “FDA Approves Penpulimab Combination for Nasopharyngeal Carcinoma,” fda.gov . Modelling shows that delayed progression lowers cumulative hospitalization spend and raises quality-adjusted life years, reinforcing payer willingness to reimburse immunotherapy in endemic markets. Molecular insights reveal that EBV-driven viral antigens promote a highly inflamed tumor microenvironment, making nasopharyngeal tumors intrinsically sensitive to PD-1 blockade. The resulting paradigm shift places immunotherapy at the center of long-term disease control strategies and injects competitive urgency among developers of next-generation checkpoint modulators.

Rising Incidence in Endemic East & South-East Asia

Global case counts are projected to climb from 133,354 in 2020 to 179,476 by 2040, with Eastern Asia expected to carry 70% of that burden despite comprising only one-fifth of the world’s population. Cantonese communities in Guangdong Province post incidence rates 50-100 times higher than Western averages because of gene–environment interactions that include salted-fish consumption and family clustering. Urbanization has improved diagnostic access and stimulated government-funded screening using EBV DNA assays, thereby enlarging the identified patient pool entering guideline-directed therapy. Multinational oncology sponsors are scaling Asia-based pivotal trials to capture these concentrated patient cohorts, accelerating dossier submissions to Chinese and ASEAN regulators. In parallel, local contract-development organizations streamline biologics manufacturing, driving down unit prices and broadening access for lower-income segments.

Regulatory Orphan-Drug & Fast-Track Incentives

The FDA’s orphan-drug construct grants seven-year exclusivity, tax credits, and exemption from user fees, collectively de-risking nasopharyngeal therapeutic pipelines. Penpulimab-kcqx capitalized on this framework, securing accelerated evaluation that shaved nearly one-and-a-half years off the traditional pathway and unlocked rapid US reimbursement. Comparable expedited review mechanisms are operational in the European Union and China, heightening the strategic importance of rare-disease status for asset valuation. Public data indicate that 27 companies now explore actinium-225 radiopharmaceuticals across multiple rare tumors, with 13 candidates reaching human testing and several earmarked for the nasopharyngeal indication [3]Richard Zimmermann, "Is Actinium Really Happening?," JNM, jnm.snmjournals.org. Regulatory goodwill thus drives a virtuous loop in which commercial exclusivity encourages risk-taking in precision radiotherapy, diverse antibody platforms, and EBV-targeted vaccines.

Plasma EBV-DNA Guided Precision Medicine Protocols

Circulating EBV DNA quantification has redefined early detection and treatment monitoring paradigms. A landmark population trial of 20,174 asymptomatic adults recorded 97.1% sensitivity and 98.6% specificity, enabling stage I–II detection in 71% of screen-positive cases compared with only 20% historically. Early intervention reduces per-patient treatment expenditure by USD 50,000–70,000 through avoidance of advanced-stage multimodality regimens. Post-therapy surveillance using the same assay stratifies relapse risk; undetectable EBV DNA at week 26 correlates with 95% five-year disease-free survival. In endemic jurisdictions such as Hong Kong, policymakers integrate EBV DNA testing into routine health checks, driving reagent consumption and lab-service revenues. The diagnostic tailwind complements therapeutic expansion, reinforcing a cohesive value proposition across the nasopharyngeal cancer market.

Restraints Impact Analysis of Nasopharyngeal Cancer Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of immuno-oncology combinations | -1.9% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Limited radiotherapy infrastructure in low-income nations | -1.6% | Sub-Saharan Africa, parts of Asia, Latin America | Medium term (2-4 years) |

| Supply constraints in α-emitter radio-isotopes | -0.8% | Global | Medium term (2-4 years) |

| Lack of harmonised EBV-DNA testing standards | -0.7% | Global, concentrated in endemic regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Immuno-Oncology Combinations

Adding PD-1 antibodies to platinum doublets lifts drug-treatment invoices to USD 78,860 per Malaysian patient, roughly six-fold above conventional regimens. The incremental cost-effectiveness ratio of USD 15,103 per QALY exceeds affordability thresholds in several ASEAN economies, leading to unequal access between public and private sectors. Manufacturers are experimenting with tiered-pricing schemes, but international reference pricing and parallel importation constrain flexibility. Philanthropic partnerships and domestic biosimilar development may alleviate sticker-shock over time, yet near-term demand will underperform clinical potential in low-income geographies, tempering the global nasopharyngeal cancer market trajectory.

Limited Radiotherapy Infrastructure in Low-Income Nations

Over 50% of patients in low- and middle-income countries lack radiotherapy access, with the shortfall exceeding 90% in the poorest economies. Sub-Saharan Africa hosts just 9% of the world’s machines, while Nigeria maintains only eight functional linear accelerators for more than 200 million residents. Bridging this gap requires 9,169 additional units and 43,200 trained professionals by 2032, translating to a USD 15-20 billion capital requirement. Infrastructure scarcity delays curative intent therapy for locoregionally advanced disease, limiting demand for concurrent chemoradiation drugs and capping revenue growth in high-burden zones of the nasopharyngeal cancer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Nasopharyngeal Cancer Market Segment Analysis

By Therapy:

Immunotherapy Reshapes Treatment ParadigmsImmunotherapy’s advent has disrupted entrenched chemotherapy primacy, yet chemotherapy still held the largest 44.25% share of the nasopharyngeal cancer market in 2025. Median overall survival now surpasses 33 months when PD-1 inhibitors are layered onto platinum-based backbones, dwarfing the 12-15-month benchmarks of chemotherapy alone and fuelling a 7.48% CAGR for the immunotherapy segment. The nasopharyngeal cancer market size for immunotherapy applications is anticipated to widen in absolute terms as earlier-line use becomes guideline standard. Targeted therapy remains a smaller but strategically pivotal segment; integration of EGFR inhibitors and anti-angiogenic agents aligns with the EBV-driven molecular landscape and may yield future combination approvals.

Demand for radiation therapy persists given its curative efficacy in stage II–III disease; IMRT achieves 5-year overall survival of 86.5%, outperforming older two-dimensional techniques. AI-enabled auto-contouring and adaptive planning keep radiation competitive by reducing toxicity and resource intensity. Experimental α-emitter constructs, while nascent, carry disruptive potential once isotope supply chains stabilize and late-phase evidence matures, positioning them as prospective wildcards within the broader nasopharyngeal cancer market.

By End-User:

Ambulatory Care Gains MomentumHospitals and specialty clinics dominated distribution channels with 67.10% revenue capture in 2025, anchored by integrated radiotherapy suites and multidisciplinary tumor boards. Yet outpatient-friendly PD-1 infusion protocols and streamlined EBV DNA monitoring underpin a 7.33% CAGR for ambulatory surgery centers between 2026 and 2031. The nasopharyngeal cancer market size serviced by ambulatory settings is projected to expand steadily as payers reward site-of-care cost differentials and patients prefer shorter stays.

Community oncology networks are installing modular infusion units and leveraging telehealth to supervise immune-related adverse events, further decentralizing care. Academic medical centers and comprehensive cancer institutes continue to lead investigational therapy delivery and complex salvage radiotherapy, maintaining share stability even as routine regimens migrate to lower-cost venues.

By Age Group:

Geriatric Segment Drives GrowthAdults aged 18-64 years constituted 69.10% of 2025 treatment volume, mirroring the typical mid-life onset profile of EBV-associated malignancy. However, demographic aging in endemic regions pushes the geriatric cohort toward a 7.44% CAGR, the fastest among all age bands. The nasopharyngeal cancer market share for patients over 65 tightens as longevity rises and screening detects early-stage disease amenable to combined-modality treatment.

Clinicians adapt dosing and schedule modifications to balance efficacy with comorbidity constraints, especially when deploying immune checkpoint therapy that can provoke autoimmune toxicities. Pediatric and young adult cases, though numerically smaller, retain strategic importance for protocol refinement that minimizes long-term functional sequelae; trials such as the University of Florida’s nivolumab combination seek to curtail cumulative radiation exposure while safeguarding survival outcomes.

Geography Analysis

North America Nasopharyngeal Cancer Market

North America captured 41.20% of 2025 revenues even though nasopharyngeal incidence remains below 1 per 100,000, a reflection of premium biologic pricing and insurance mechanisms that absorb high drug costs. Robust clinical-trial infrastructure sustains early adoption of investigational combinations, but limited patient growth moderates regional CAGR compared with emerging Asia.

APAC Nasopharyngeal Cancer Market

Asia-Pacific anchors both volume and momentum, holding a matching 41.20% share while propelling a 7.86% CAGR that leads all regions. The nasopharyngeal cancer market size in China, Hong Kong, Singapore, and Malaysia rises in tandem with reimbursement expansion and domestic PD-1 approvals that price well below imported analogues. Government-backed EBV DNA screening further enlarges the treated population and solidifies therapy pipelines adapted to local genetic profiles.

EMEA Nasopharyngeal Cancer Market

Europe maintains a mature but slower-growing landscape characterized by consistent access via national health systems and active participation in multi-center trials. Price-volume agreements constrain biologic spending yet secure equitable patient access. The nasopharyngeal cancer market in Middle East & Africa remains nascent; however, accelerating oncology infrastructure and heightened disease awareness lay the foundation for double-digit growth pockets once radiotherapy capacity improves.

Competitive Landscape

The nasopharyngeal cancer market exhibits moderate concentration, with top Western incumbents leveraging established PD-1 franchises while Chinese biotechs press competitive price points and ethnicity-specific data. Merck & Co. and Bristol Myers Squibb continue to harvest volume from pembrolizumab and nivolumab via off-label regimens while engineering pipeline breadth through acquisitions such as Merck’s 2024 buyout of Harpoon Therapeutics. Combination trials that integrate antibody-drug conjugates, bispecifics, and radioligands underscore a portfolio-level shift toward multi-mechanistic control.

Chinese innovators BeiGene, Junshi Biosciences, and Innovent Biologics deploy regional regulatory efficiencies to secure early domestic approvals for tislelizumab, toripalimab, and sintilimab. Subsequent alliances with Coherus BioSciences and other Western partners extend commercial reach into Europe and North America, intensifying global price competition. Cross-border technology transfer agreements permit localized biologic manufacturing that shortens supply chains and trims costs.

Smaller players focus on EBV-targeted modalities, from therapeutic vaccines to T-cell receptor therapies, aiming to exploit the virus’s universal presence within tumor cells. Radiopharmaceutical entrants seek differentiation through alpha-emitting payloads that deliver high-linear-energy transfer with controlled collateral damage, though isotope supply constraints presently gate large-scale rollout. Collectively, these dynamics reinforce a market where success pivots on combination readiness, regional pricing agility, and access to biomarker-aligned patient pools.

Nasopharyngeal Cancer Industry Leaders

-

Bristol Myers Squibb

-

Eli Lilly and Company

-

Merck & Co., Inc.

-

Novartis AG

-

GlaxoSmithKline (GSK) PLC

- *Disclaimer: Major Players sorted in no particular order

Nasopharyngeal Cancer Market Companies Covered in this Report

- Merck

- Bristol-Myers Squibb

- Novartis

- Roche

- Pfizer

- AstraZeneca

- GlaxoSmithKline

- Sanofi

- Eli Lilly and Company

- Innovent Biologics

- Junshi Biosciences

- BeiGene

- Hutchmed

- Theravectys

- Cyclacel Pharma

- Biocon

- CSPC ZhongQi

- Qilu Pharma

- ONO Pharma

- Astellas Pharma

Recent Industry Developments in Nasopharyngeal Cancer Market

- July 2025: The European Commission approved Tevimbra (tislelizumab) plus gemcitabine–cisplatin for first-line treatment of metastatic or recurrent nasopharyngeal carcinoma unamenable to curative surgery or radiotherapy.

- April 2025: The FDA cleared penpulimab-kcqx in combination with platinum-gemcitabine as the second FDA-authorized immunotherapy for nasopharyngeal carcinoma, under breakthrough, orphan, and fast-track designations.

- October 2024: Toripalimab obtained regulatory approvals in India and Hong Kong for recurrent or metastatic disease, broadening PD-1 access across high-incidence markets.

- June 2024: A Singapore–Japan scientific collaboration uncovered epigenetic mechanisms by which EBV accelerates oncogenesis, prompting multiple pharmaceutical development partnerships.

Global Nasopharyngeal Cancer Market Report Scope

As per the scope of the report, nasopharyngeal cancer is a disease in which cancer cells form in the tissues of the nasopharynx (the upper part of the throat behind the nose). The risk of nasopharyngeal cancer can be affected by many things, including one's race and whether or not they have been exposed to the Epstein-Barr virus. Therapy (Chemotherapy, Immunotherapy, Radiation Therapy, and Others), End User (Hospitals and Clinics, Ambulatory Surgery Centers, and Other End Users), and Geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America) are the segments of the Nasopharyngeal Cancer Market. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

Segmentation Overview

| Chemotherapy |

| Targeted Therapy |

| Immunotherapy |

| Radiation Therapy |

| Other Therapies |

| Hospitals and Spcialty Clinics |

| Ambulatory Surgery Centres |

| Other End-Users |

| Adult |

| Pediatric |

| Geriatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy | Chemotherapy | |

| Targeted Therapy | ||

| Immunotherapy | ||

| Radiation Therapy | ||

| Other Therapies | ||

| By End-User | Hospitals and Spcialty Clinics | |

| Ambulatory Surgery Centres | ||

| Other End-Users | ||

| By Age Group | Adult | |

| Pediatric | ||

| Geriatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the nasopharyngeal cancer market?

The nasopharyngeal cancer market size reached USD 1.22 billion in 2026 and is forecast to climb to USD 1.68 billion by 2031.

Which region leads the nasopharyngeal cancer market?

Asia-Pacific holds the largest revenue share at 41.20% thanks to its high disease incidence and rapid adoption of locally manufactured immunotherapies.

What therapy segment is growing fastest?

Immunotherapy is projected to expand at a 7.48% CAGR, outpacing all other modalities as PD-1/PD-L1 agents move into first-line combinations.

Why are ambulatory surgery centers gaining share?

Checkpoint inhibitors can be administered safely in outpatient settings, allowing payers to capture cost savings while maintaining clinical oversight.

How does EBV DNA testing influence market growth?

High-accuracy plasma EBV DNA assays detect early-stage disease and guide post-treatment monitoring, increasing the addressable patient pool for curative and maintenance therapies.

What is the main barrier to treatment in low-income regions?

Severe shortages of radiotherapy infrastructure and trained clinicians limit access to standard curative regimens, suppressing demand in high-burden geographies.

Page last updated on: