Myanmar Used Car Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

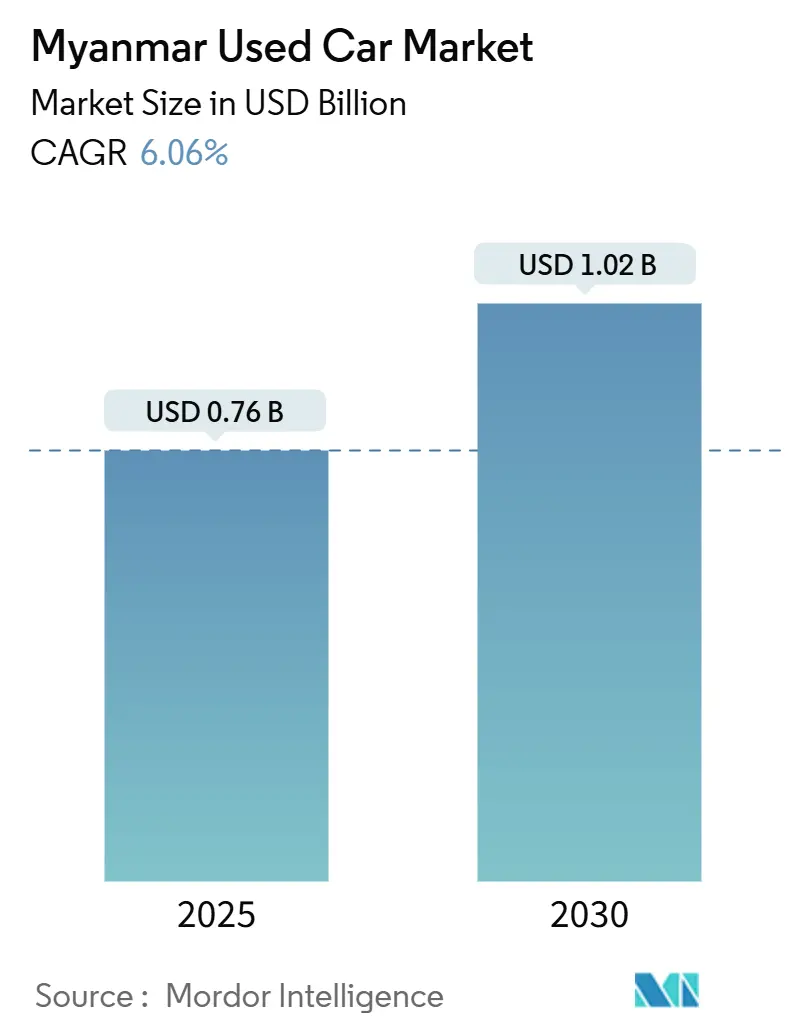

| Market Size (2025) | USD 0.76 Billion |

| Market Size (2030) | USD 1.02 Billion |

| Growth Rate (2025 - 2030) | 6.06% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myanmar Used Car Market Analysis by Mordor Intelligence

The Myanmar used car market is valued at USD 0.76 billion in 2025 and is forecast to reach USD 1.02 billion by 2030, advancing at a 6.06% CAGR. Steady growth continues despite political turbulence, currency swings, and import controls. Digital retail now dominates transactions, electric-vehicle incentives are shifting fuel preferences, and a gradual easing of licence caps is widening the supply base. Demand also benefits from migrant remittances, rising new-car prices, and the convenience of fintech-enabled loans, while organised dealers gain ground by offering verified histories and warranties. These factors are reshaping a once-informal trading arena into a more regulated and technology-enabled ecosystem.

Key Report Takeaways

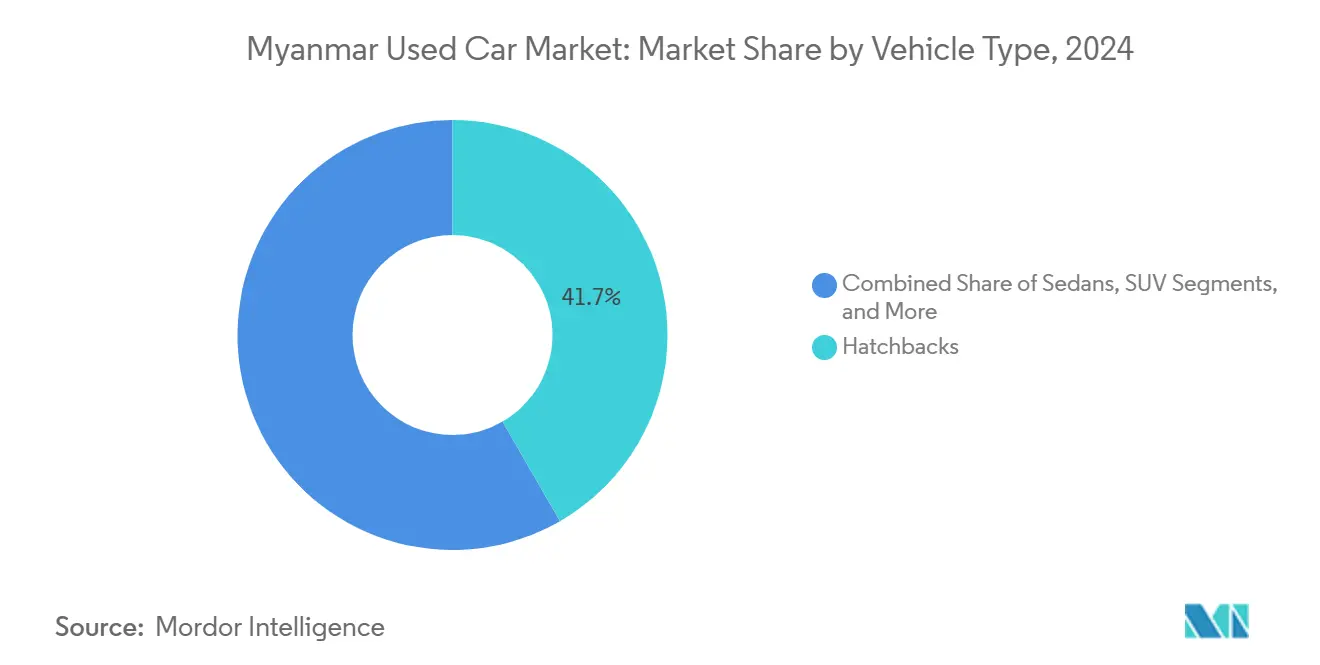

- By vehicle type, hatchbacks contributed a 41.67% share in the Myanmar Used Car Market in 2024; SUVs are projected to post the highest 9.76% CAGR.

- By vendor type, unorganised sellers held 68.39% share in the Myanmar Used Car Market in 2024; organised dealers are advancing at a 10.84% CAGR.

- By fuel type, petrol models dominated the Myanmar Used Car Market in 2024, with a 77.86% share; battery-electric vehicles will grow at a 16.24% CAGR.

- By vehicle age, 3-5-year units accounted for 34.54% revenue share in the Myanmar Used Car Market in 2024; 0-2-year vehicles are set to climb at an 11.22% CAGR.

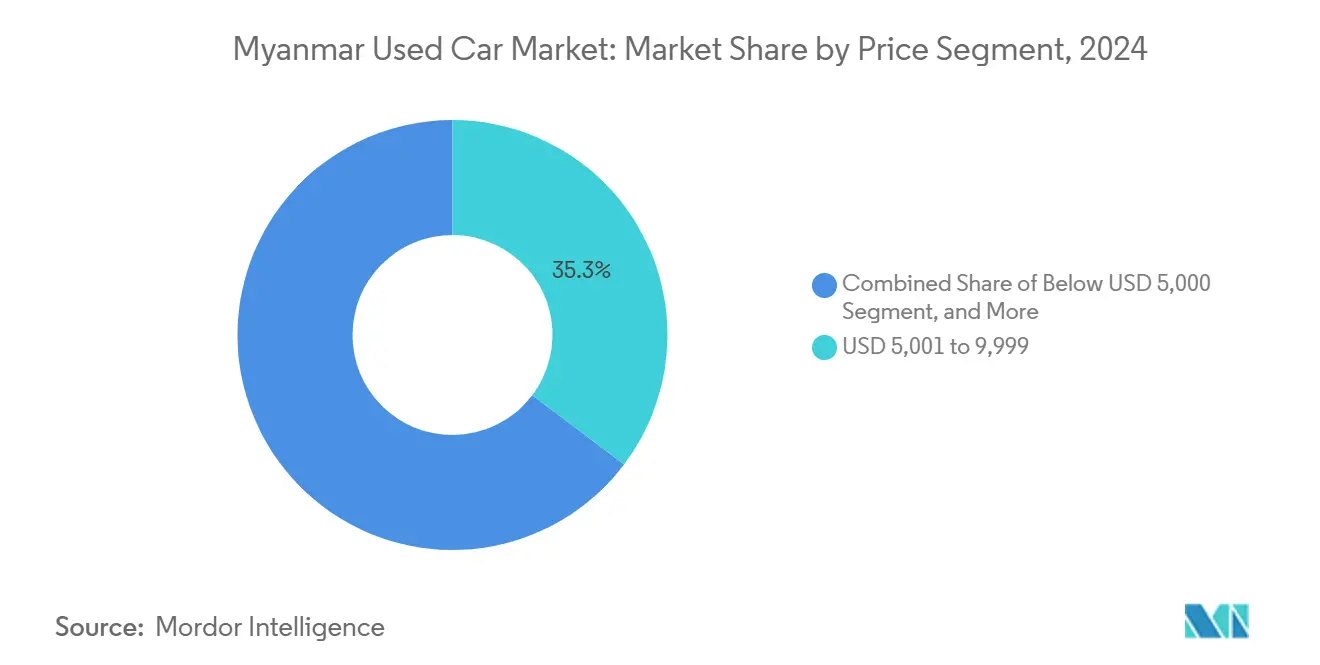

- By price band, the USD 5,001-9,999 tier captured 35.29% share in the Myanmar Used Car Market in 2024; the above-USD 30,000 tier is expected to rise at a 10.41% CAGR.

- By sales channel, online platforms led with 70.34% revenue share in the Myanmar Used Car Market in 2024; offline OEM-franchised outlets are projected to expand at an 8.37% CAGR through 2030.

- By ownership, multi-owner cars represented 64.18% share in the Myanmar Used Car Market in 2024; first-owner resales are forecast to increase at a 13.17% CAGR through 2030.

- By region, Yangon commanded 53.25% of market revenue in the Myanmar Used Car Market in 2024; Mandalay is forecast to grow fastest at an 11.62% CAGR to 2030.

Myanmar operates as part of an interconnected international environment rather than as a self-contained country level unit. The used car market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Myanmar Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Price of New Cars | +1.8% | Yangon and Mandalay | Medium term (2-4 years) |

| Growth of Digital Classifieds and Auto-Loans | +1.5% | Urban hubs, spreading to secondary cities | Short term (≤ 2 years) |

| Gradual Easing of Post-Coup Import Caps | +1.2% | National, early gains in border states | Long term (≥ 4 years) |

| Migrant-Remittance Demand in Border States | +0.8% | Shan, Kachin and other border regions | Medium term (2-4 years) |

| Tax Rebate for EV Imports | +0.9% | Major cities | Short term (≤ 2 years) |

| OEM-Certified Pre-Owned Programmes | +0.7% | Primarily Yangon | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Price of New Cars

Local assembly disruption and Kyat depreciation have lifted showroom prices, steering budget-conscious households toward used vehicles. Used units priced between USD 5,001 and USD 9,999 satisfy the affordability gap and form the single largest price band. Currency weakness inflates imported parts costs, magnifying the total cost of ownership of new vehicles. Organised dealers respond by stockpiling popular Japanese imports that align with prevailing budgets.

Growth of Digital Classifieds and Fintech-Enabled Auto-Loans

Smartphone penetration pushes shoppers toward mobile marketplaces where listings, price comparisons, and chat functions shorten decision cycles. Carsome Myanmar reports that more than seven out of ten transactions in 2024 originated online, confirming the seismic channel shift. Embedded loan approvals de-risk purchases for first-time buyers who lack a formal credit history. Digital records also enhance transparency, building confidence in odometer readings and accident histories. Secondary cities now see similar adoption as bandwidth improves and handset prices fall.

Gradual Easing of Post-Coup Import Licence Caps

The Commerce Ministry has started to loosen approvals for select categories, allowing more supply to enter via licensed distributors. Border checkpoints still see tight inspection, yet compliant importers secure an advantage over informal traders. Organised dealers, therefore, accelerate share gains because they can manage documentation demands. Easing constraints will aid larger lots entering Mandalay’s yards, supporting the region’s double-digit growth outlook. Long-term, a broader vehicle mix is set to improve replacement cycles across the Myanmar used car market[1]“Automobile Import Licensing Updates,” Ministry of Commerce, moc.gov.mm.

Tax Rebate for EV Imports

The military government waives duties on electric models to curb fuel import bills. BEVs consequently register the fastest-rising share of the Myanmar used car market, supported by Chinese brands such as BYD and Neta. Operating cost savings resonate with ride-hail drivers navigating daily petrol shortages. Charging networks remain sparse, yet urban pilots in Yangon are expanding with municipal support. The policy signals longer-term alignment with regional electrification trends.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Volatility Inflating Landed-Costs | -2.1% | National, with severe impact on import-dependent regions | Short term (≤ 2 years) |

| Trust and Odometer-Fraud Concerns | -1.4% | National, particularly affecting online transactions | Medium term (2-4 years) |

| Political Instability Disrupting Logistics | -1.3% | National, with severe impact on border states and rural areas | Long term (≥ 4 years) |

| FX-Driven Ad-Hoc Import Bans | -1.0% | National, with concentrated impact on border trade routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Inflating Landed Costs

Sharp currency swings raise the USD value of customs duties and bank guarantees, compressing importer margins. Inflation at 34.1% in 2025 further erodes household purchasing power, tightening discretionary budgets. Spare parts prices spike in tandem, elevating maintenance expenses for older cars. The March 2025 earthquake added USD 11 billion in damage costs, diverting capital away from vehicle upgrades. As a result, many buyers delay replacement cycles, limiting upside in premium segments through 2026[2]“Inflation and Exchange Rate Trends,” World Bank, worldbank.org.

Trust and Odometer-Fraud Concerns

Buyers remain wary of tampered mileage and forged import papers. Enforcement capacity at the Myanmar Road Transport Administration Department is improving, yet grey-market loopholes persist. Fraud worries slow online checkout rates, forcing many shoppers to insist on physical inspection before payment[3]“Vehicle Registration Procedures,” Myanmar Road Transport Administration Department, roadtransport.gov.mm. Organised dealers invest in Japanese auction reports and blockchain logs to verify vehicle histories, using these tools as selling points. OEM-backed certification programmes aim to raise confidence, though their reach is still small relative to the national fleet.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Hatchbacks Hold Lead While SUVs Accelerate

Hatchbacks retained a 41.67% share of the Myanmar used car market in 2024, reflecting their fuel efficiency and affordability. Daily commuters in Yangon value compact dimensions that suit congested streets. The Myanmar used car market size for SUVs is projected to expand at a 9.76% CAGR, supported by border-state demand for higher ground clearance. Rising disposable incomes and remittance inflows also lift preference for versatile lifestyle SUVs.

Fuel savings and low parts costs underpin hatchback popularity in lower-income households. SUV growth benefits from new BEV incentives, with electric crossovers entering at competitive landed prices. Improved rural roadworks open fresh routes, further boosting SUV appeal. Sedans and MPVs remain secondary options, while niche sports and luxury cars signal emerging affluent clusters in Yangon and Mandalay.

By Vendor Type: Organized Dealers Close the Gap

Unorganized sellers controlled 68.39% of transactions in 2024, yet organized dealers are growing at 10.84% CAGR through 2030. Price-driven shoppers still flock to informal bazaars in Hlaing Thar Yar township, but warranty seekers migrate toward certified lots. Documentation confidence is a chief pull, because organised dealers streamline import licences and loan processing. Their digital storefronts also mirror offline inventory, easing discovery.

The Myanmar used car market size captured by organised players is supported by banking alliances that bundle instalment plans and insurance. Compliance costs weigh on small roadside traders, squeezing their margins. Government registration crackdowns accelerate the shake-out, because fines for incomplete papers hurt thinly capitalised vendors. Over the forecast horizon, consolidation is set to tilt volume toward multi-branch networks with central reconditioning hubs.

By Fuel Type: Petrol Dominance Faces Electric Momentum

Petrol models commanded 77.86% of 2024 volume, yet battery-electric units are forecast to log a 16.24% CAGR as tariff relief endures. Price parity improves rapidly once fuel savings overtake upfront differentials. The Myanmar used car market share for diesel remains moderate, serving trucking and rural haulage where torque needs outweigh electrification readiness.

Hybrid options bridge the gap for buyers seeking economy without charging anxiety, though higher sticker prices still limit mass uptake. Chinese EV brands gain mindshare through aggressive after-sales support and battery warranties that calm durability fears. Pilot charging corridors on the Yangon–Mandalay expressway give early adopters range confidence. LPG and CNG conversions form a niche, mainly among taxi cooperatives.

By Vehicle Age: Newer Stock Commands Growing Premium

Cars aged 3-5 held a 34.54% share in 2024, offering a compromise between price and reliability. However, 0-2-year inventory is forecast to post an 11.22% CAGR as incomes rise and financing availability widens. Buyers target fresher models to access safety technology like airbags and anti-lock brakes, which older imports often lack. OEM-certified schemes concentrate on lease returns under three years, deepening this supply.

Older 6-8-year and 9-12-year brackets continue to serve budget-bound households. Rural workshops specialize in maintaining these units with imported, reconditioned parts. Vehicles above 12 years remain prevalent in agricultural zones where simple engines ease roadside fixes. Tightening emission rules in Yangon could eventually curtail entry for the oldest stock, nudging demand up the age ladder.

By Price Segment: Mid-Range Still Rules, Premium Rising

The USD 5,001-9,999 band captured 35.29% of revenue in 2024, anchored by Japanese hatchbacks and compact MPVs. Mid-tier affordability aligns with average urban household earnings. The above-USD 30,000 tier, though small, is projected to grow at 10.41% CAGR as affluent professionals and business owners reward themselves with late-model SUVs and luxury sedans. Currency hedging via hard-asset purchases also drives high-end interest.

The below-USD 5,000 stock satisfies rural mobility needs where installment products are scarce. The USD 10,000-19,999 range houses hybrid sedans and high-spec MPVs for family buyers seeking comfort upgrades. The USD 20,000-29,999 tier forms a bridge to luxury, featuring lightly used German nameplates and premium Japanese SUVs. Dealers tailor financing campaigns to stretch middle-class budgets into higher brackets.

By Sales Channel: Online Reaches Scale While Offline Re-Tools

Online channels accounted for a 70.34% share in the Myanmar used car market in 2024, powered by mobile-first behavior and pandemic-era safety concerns. Listing portals offer transparent comparisons and chat-based negotiations that suit private sellers and professional dealers. The online channel integrates logistics and inspection at doorstep handover, cutting buyers' travel time. Meanwhile, the Myanmar used car market size handled through offline OEM showrooms will expand at 8.37% CAGR because certified units and tailored finance require physical handovers.

Offline channels, such as auction houses, preserve relevance for wholesale trade, supplying yards in Mandalay and border towns with bulk consignments. Multi-brand independents offline channels adapt by adopting hybrid models in which online reservations lead to offline test drives. IDOM and BE FORWARD jointly syndicate inventory across their global platforms, increasing choice for local consumers and raising transparency standards

By Ownership: Multi-Owner Units Remain Mainstream

Multi-owner cars represented 64.18% of 2024 transactions, a testament to budget constraints and long vehicle life cycles. Flexible pricing makes these units attractive despite patchy maintenance histories. First-owner resales are forecast to grow at 13.17% CAGR, reflecting rising willingness to pay for provenance. Organized dealers cultivate this niche by tapping off-lease fleets from Japan and neighboring markets.

Clear title and odometer certainties reduce post-purchase surprises, appealing to risk-averse millennials engaging online. Annual registration renewal rules also favor first-owner vehicles because paperwork is more straightforward. Over time, improved access to credit will reinforce the shift toward lower-owner-count inventory across the Myanmar used car market.

Geography Analysis

Yangon remained the primary hub with a 53.25% share in 2024, driven by a dense population, higher incomes, and established logistics. Importers funnel most stock through Thilawa Port, then distribute to suburban yards. Traffic congestion steers preferences toward compact hatchbacks and, increasingly, small electric cars that qualify for parking incentives. Luxury boutiques cluster along Kabar Aye Pagoda Road, underscoring the city’s role as the chief premium locus.

Mandalay is forecast to post 11.62% CAGR as it capitalizes on China–Myanmar trade corridors. Chan Mya Tharsi township dealers benefit from continuous inflows of reconditioned right-hand-drive units crossing Muse and other northern checkpoints. Improved expressway links shorten delivery times to Upper Myanmar, encouraging organized networks to open satellite showrooms. Provincial authorities prioritize road widening, enabling larger SUVs to gain popularity.

Naypyitaw and the central corridor account for a smaller slice yet showcase distinct demand patterns shaped by government fleet renewal and diplomatic procurement. Border states such as Shan and Kachin exhibit volatile volumes because insurgency outbreaks and customs crackdowns intermittently impact supply. Nevertheless, remittance-fuelled purchases in these areas sustain a demand baseline for versatile pickups. Ongoing security improvements and infrastructure investments could unlock latent growth, adding geographic diversity to the Myanmar used car market.

The used car market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Africa, along with detailed country-level analysis for South Korea, Bangladesh, Ethiopia, Belgium, Nigeria, Kenya, Brazil, and Kuwait.

Competitive Landscape

Competition remains moderately fragmented. Unorganized yards dominate rural and low-ticket trades, but organized groups such as CarsDB and Carsome strengthen their presence through data-driven pricing and warranty offers. Digital convenience helps them court younger buyers who value time and transparent histories. Partnerships with banks and insurers further differentiate these platforms.

Japanese import specialists retain an edge on quality perception, supported by auction-grade reports that verify condition. IDOM’s alliance with BE FORWARD opens a wider pipeline of late-model hybrids and electric cars suited to government incentives. Chinese brands, including BYD and Neta, exploit duty exemptions to seed affordable EV options, eroding petrol supremacy in urban showrooms. Local distributors invest in spare parts warehouses and technician training to ensure after-sales support.

Regulatory hurdles act as a moat for incumbents who master documentation processes. The Road Transport Administration Department mandates detailed ownership records, which organized dealers integrate into digital ledgers. Smaller traders lack the capital to meet these standards, nudging consolidation. Over the next five years, a dual structure is expected to persist, with tech-enabled chains scaling in cities while informal lots continue to serve price-focused buyers in outlying areas.

Myanmar Used Car Industry Leaders

Toyota Aye and Sons

CarsDB

Capital Diamond Star Group Limited

Prestige Automobiles

SBT Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IDOM and BE FORWARD announced a strategic partnership to integrate vehicle inventory across cross-border e-commerce platforms, enhancing Japanese used car availability in Myanmar and other Southeast Asian markets.

- April 2024: Myanmar's regulatory framework for used car imports strikes a balance between ensuring affordable transportation and modernizing its vehicle fleet. The policy permits the import of only left-hand-drive vehicles and imposes specific production year restrictions on passenger and commercial vehicles.

Myanmar Used Car Market Report Scope

A used car is a pre-owned vehicle that has previously had one or more retail owners. These cars are sold through a variety of outlets through independent dealers, online sales channels, and others.

The Myanmar used car market is segmented into vehicle type, vendor type, and fuel type. Based on the vehicle type, the market is segmented into hatchbacks, sedans, sports utility vehicles, and multi-purpose vehicles. Based on the vendor type, the market is segmented into organized and unorganized. Based on the fuel type, the market is segmented into gasoline, diesel, electric, and other fuel types.

For each segment, the market sizing and forecasts have been done based on the value (USD).

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Organised |

| Unorganised |

| Petrol |

| Diesel |

| Hybrid (HEV & PHEV) |

| Battery-Electric (BEV) |

| Others |

| 0 - 2 Years |

| 3 - 5 Years |

| 6 - 8 Years |

| 9 - 12 Years |

| Above 12 Years |

| Below 5,000 |

| 5,000 - 9,999 |

| 10,000 - 14,999 |

| 15,000 - 19,999 |

| 20,000 - 29,999 |

| Above 30 000 |

| Online |

| Offline |

| First-owner Resale |

| Multi-owner |

| Yangon | Mandalay |

| Naypyitaw & Central Corridor | |

| Border States (Shan, Kachin, others) |

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| Sport-Utility Vehicles (SUVs) | ||

| Multi-Purpose Vehicles (MPVs) | ||

| By Vendor Type | Organised | |

| Unorganised | ||

| By Fuel Type | Petrol | |

| Diesel | ||

| Hybrid (HEV & PHEV) | ||

| Battery-Electric (BEV) | ||

| Others | ||

| By Vehicle Age | 0 - 2 Years | |

| 3 - 5 Years | ||

| 6 - 8 Years | ||

| 9 - 12 Years | ||

| Above 12 Years | ||

| By Price Segment (USD) | Below 5,000 | |

| 5,000 - 9,999 | ||

| 10,000 - 14,999 | ||

| 15,000 - 19,999 | ||

| 20,000 - 29,999 | ||

| Above 30 000 | ||

| By Sales Channel | Online | |

| Offline | ||

| By Ownership | First-owner Resale | |

| Multi-owner | ||

| By Region (Myanmar) | Yangon | Mandalay |

| Naypyitaw & Central Corridor | ||

| Border States (Shan, Kachin, others) | ||

Key Questions Answered in the Report

What is the current value of the Myanmar used car market?

The market stands at USD 0.76 billion in 2025 and is projected to reach USD 1.02 billion by 2030.

Which sales channel is most important in Myanmar’s used car space?

Online platforms dominate with a 70.34% share and continue to outpace traditional channels in reach and convenience.

Why are electric cars gaining traction in Myanmar?

Duty exemptions, lower running costs, and Chinese brand entry have pushed battery-electric vehicles to the fastest CAGR of 16.24% in the forecast period.

What is the main challenge slowing market growth?

Currency volatility raises import costs and squeezes consumer purchasing power, reducing appetite for higher-priced segments.

How are organized dealers gaining share?

They provide verified documentation, warranty coverage, and aligned fintech partnerships, which address buyer trust issues and support a 10.84% CAGR through 2030.

Page last updated on: