Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

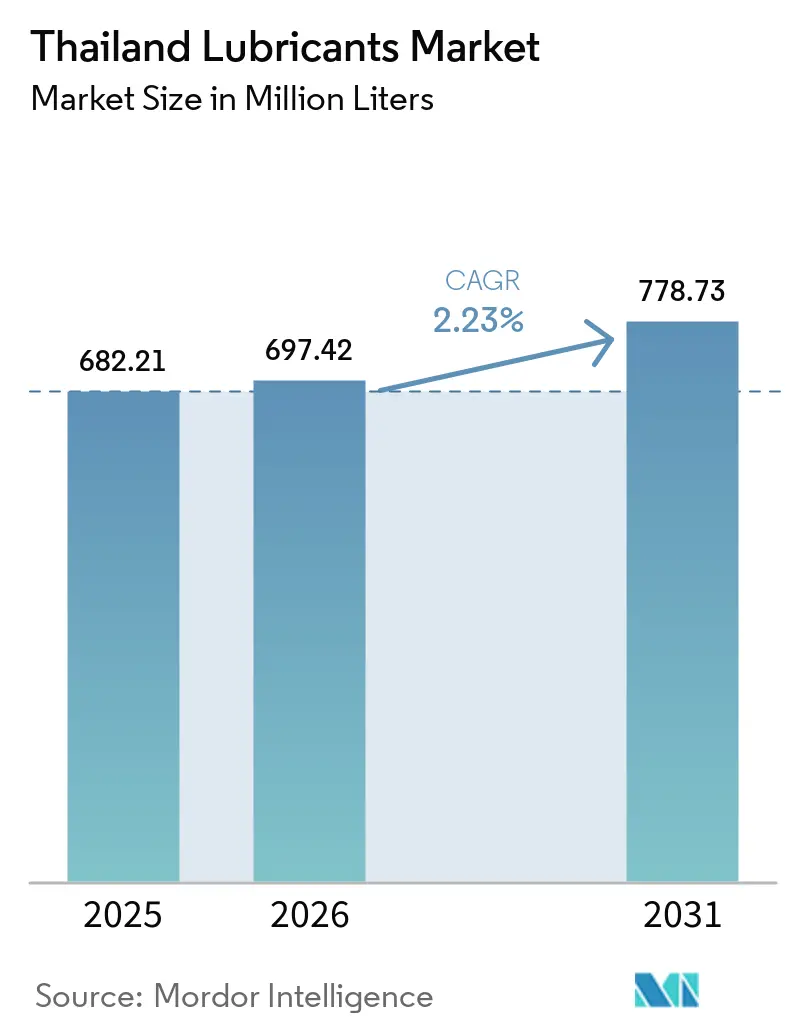

| Base Year Market Size (2025) | 682.21 Million Liters |

| Market Volume (2026) | 697.42 Million Liters |

| Market Volume (2031) | 778.73 Million Liters |

| Growth Rate (2026 - 2031) | 2.23% CAGR |

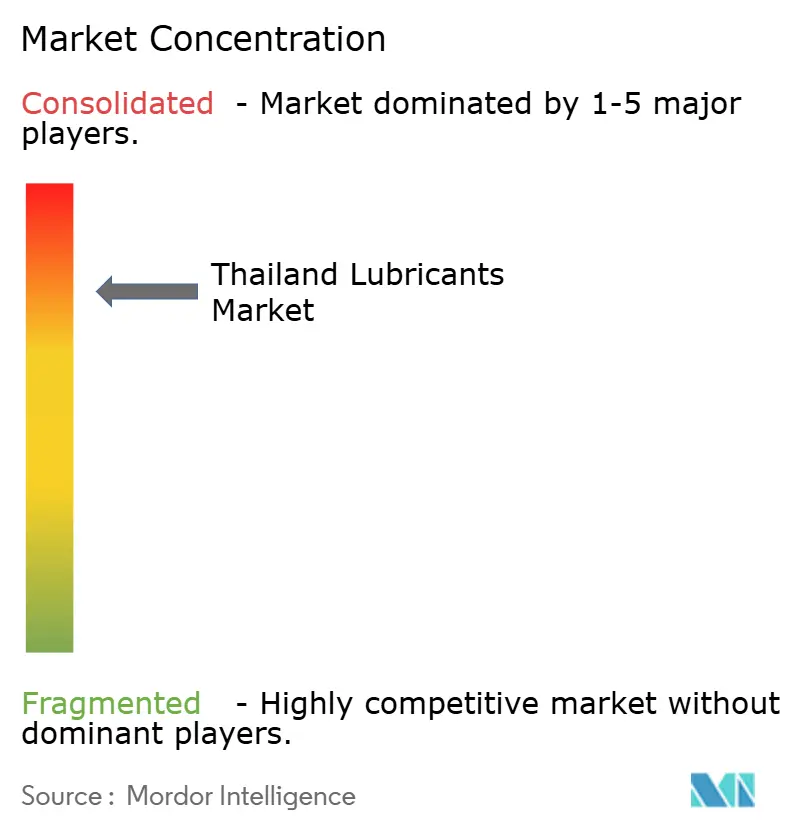

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Lubricants Market Analysis by Mordor Intelligence

The Thailand Lubricants Market size is expected to increase from 682.21 Million Liters in 2025 to 697.42 Million Liters in 2026 and reach 778.73 Million Liters by 2031, growing at a CAGR of 2.23% over 2026-2031. Headline volume growth hides a rapid quality shift driven by Euro 5 diesel standards, large-scale infrastructure spending, and the government’s 30@30 electric-vehicle roadmap. Commercial fleets are migrating to low-SAPS synthetic formulations that double drain intervals, while industrial automation is lifting demand for high-performance metalworking fluids. Parallel investments in data-center capacity and renewable power assets are expanding niches for dielectric coolants and synthetic gear oils. Together, these forces are re-balancing lubricant consumption away from mineral engine oils toward specialty synthetics, even as total liters continue to edge upward.

Key Report Takeaways

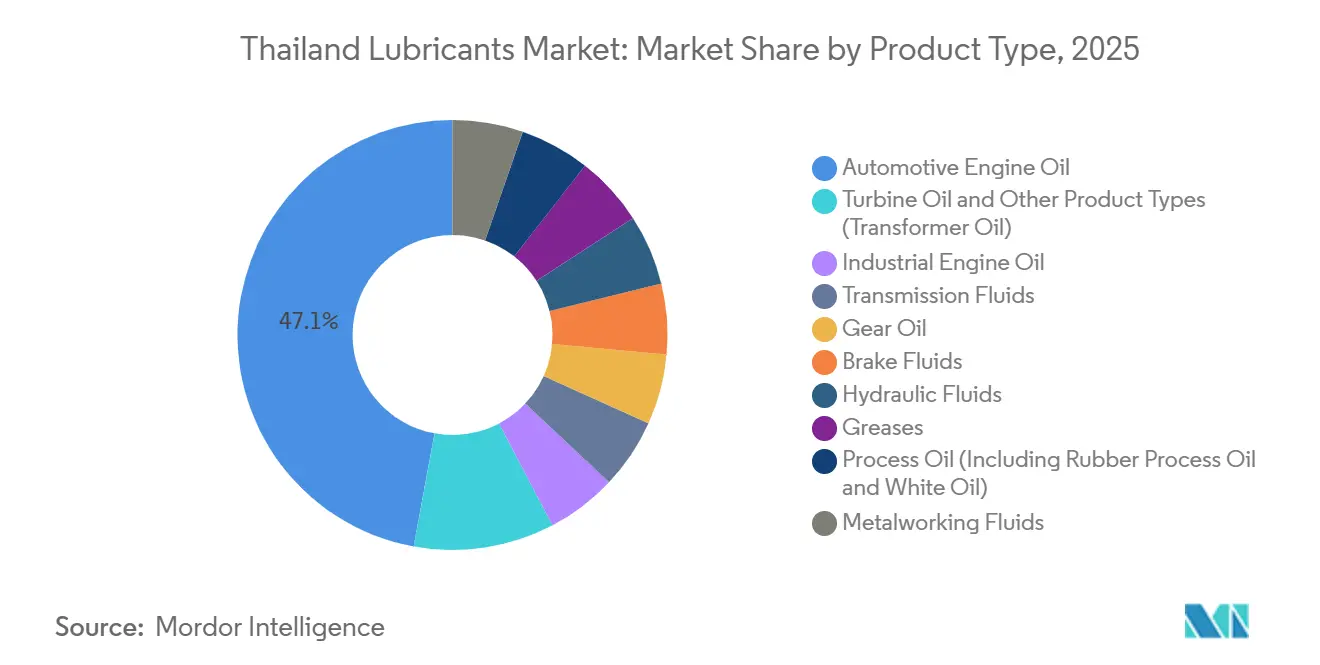

- By product type, automotive engine oil held a 47.12% share of the Thailand Lubricants market size in 2025, while greases are advancing at a 3.22% CAGR through 2031.

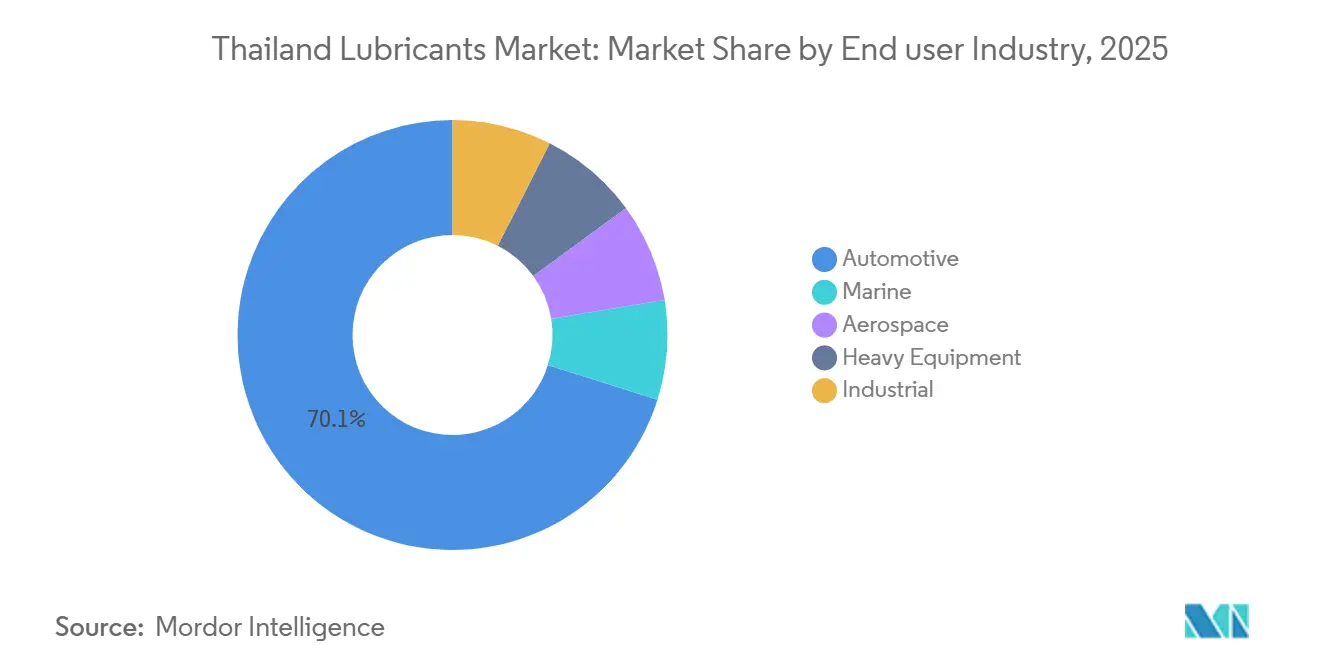

- By end-user industry, the automotive sector captured 70.13% of the Thailand Lubricants market share in 2025; the industrial sector records the fastest expansion at a 3.12% CAGR to 2031.

- By base stock type, mineral oil-based lubricants accounted for 69.66% of the market in 2025, and the demand for synthetic lubricants is expected to grow with a CAGR of 2.93% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manufacturing rebound | +0.6% | Eastern Economic Corridor, Greater Bangkok | Medium term (2-4 years) |

| Commercial-vehicle fleet growth | +0.5% | Bangkok, Chonburi, Rayong | Short term (≤2 years) |

| Industrial automation | +0.4% | Eastern Economic Corridor | Medium term (2-4 years) |

| Data-center buildouts | +0.3% | Bangkok, Chonburi | Long term (≥4 years) |

| Biodiesel B20 mandate | +0.2% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Rebound in Manufacturing and Exports

Automotive output stabilized at 1.50 million vehicles in 2025 after a pandemic dip, while motorcycle production rose to a projected 2.10 million units. Roughly 2,200 parts manufacturers, now pivoting to electric-vehicle components, generated robust export earnings that preserve baseline engine-oil demand even as lubricant intensity per vehicle declines. Farm-equipment sales worth THB 154.1 billion (USD 4.438 billion) in 2023 are adding hydraulic-fluid volumes, as 71.3% of farmers mechanize.

Expansion of Commercial-Vehicle Fleet and E-Commerce Logistics

E-commerce carriers in Bangkok and the Eastern Economic Corridor expanded fleets that must comply with Euro 5 low-SAPS lubricant specifications from January 2024. Shell’s Rimula R6 LM and Chevron’s Delo 600 ADF lengthen drain intervals to 40,000 km, lowering service events but increasing revenue per liter. Logistics firms accept higher-priced synthetics to offset diesel that exceeded THB 35 (USD 0.994) per liter in 2024[1]Shell Thailand, “Rimula R6 LM Launch Release,” shell.co.th.

Industrial Automation Boosting Demand for High-Performance Synthetics

Foreign direct investment into battery, semiconductor, and electronics plants has accelerated the adoption of CNC machining and robotic welding. These processes require thermally stable synthetic metalworking fluids that resist oxidation and extend tool life. At the same time, power-sector upgrades to meet a 37% renewables target are driving purchases of synthetic turbine and transformer oils.

Data-Center Buildouts Driving Specialty Cooling and Genset Lubricants

Hyperscale operators are selecting Bangkok and Chonburi for new server farms. Immersion-cooling systems depend on dielectric synthetic esters that maintain viscosity across wide temperature ranges, while backup gensets mandate API CK-4 oils for sporadic yet critical operation. Although small in absolute liters, these applications post double-digit growth on a low base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated EV adoption | -0.8% | Bangkok and major cities | Medium term (2-4 years) |

| Mineral-oil disposal rules | -0.3% | National | Short term (≤2 years) |

| Low-cost ASEAN imports | -0.2% | Border provinces | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerated EV Adoption Shrinking ICE Lubricant Pool

Battery electric vehicle registrations reached 89,984 units by October 2025, a trajectory that could displace roughly 150 million liters of engine oil yearly if the 30@30 target is met. BEV powertrains remove crankcase oils and conventional transmission fluids, cutting per-vehicle lubricant consumption by up to 80%[2]Electric Vehicle Association of Thailand, “EV Registration Statistics 2025,” evat.or.th.

Stricter Mineral-Oil Disposal Regulations

The Polluter-Pays Principle and the forthcoming Industrial Waste Management Act impose extended producer responsibility for used oils. Licensed transporters and certified facilities raise compliance costs, squeezing margins for small blenders and accelerating the switch to longer-life synthetics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor, Greases Gain on Infrastructure Surge

Automotive engine oil held 47.12% of Thailand Lubricants market share in 2025 on the back of a 44.8 million-unit vehicle fleet. The Thailand lubricants market size for greases is advancing at a 3.22% CAGR through 2031, as THB 980 billion (USD 29.89 billion) in infrastructure outlays deploy heavy equipment that relies on lithium-complex and polyurea greases.

Greases see tailwinds from the USD 36 billion land-bridge corridor and Laem Chabang port expansion, both of which require extreme-pressure lubrication for port cranes and earthmovers. In contrast, transmission-fluid demand softens as single-speed EV gearboxes proliferate, while metalworking fluids upgrade to synthetics because 2,200 auto-parts suppliers are installing high-precision CNC machines.

Industrial engine oils for stationary gensets remain stable, supported by 232,009 GWh of electricity generation in 2024. Hydraulic fluids dominate construction machinery, and transformer oils gain importance as EGAT expands grid assets to integrate renewable generation. Process oils serve tire and pharmaceutical factories, and brake fluids retain steady replacement demand.

By End-User Industry: Automotive Dominates, Industrial Accelerates

The automotive sector accounted for 70.13% of Thailand Lubricants market size in 2025, encompassing passenger vehicles, commercial vehicles, and two-wheelers. Passenger-car lubricant volumes will slip as BEV penetration climbs, while commercial trucks adopt low-SAPS synthetics that halve annual oil changes.

Industrial users are growing lubricant demand at a 3.12% CAGR. Power generation relies on turbine, hydraulic, and transformer oils, while metallurgy and metalworking plants consume synthetic cutting fluids that tolerate high heat and fine tolerances. Construction, mining, and agriculture segments absorb hydraulic and gear oils, and marine operators at Laem Chabang port shift to low-sulfur cylinder oils that comply with IMO 2020.

By Base Stock Type: Mineral Oils Retain Share, Synthetics Gain on Performance Mandates

Mineral oil-based lubricants held 69.66% of Thailand Lubricant market share in 2025 because of price sensitivity in passenger vehicles and agriculture. However, synthetic products are projected to expand at a 2.93% CAGR during the forecast period (2026-2031) on the strength of Euro 5 fleet adoption and industrial automation.

Semi-synthetics blend Group III base stocks with mineral oils to capture price-to-performance niches, especially in motorcycle applications. Bio-based lubricants remain below 2% share, but Bangchak’s investment in renewable feedstocks positions it for future sustainability mandates.

Geography Analysis

Bangkok Metropolitan Region, the Eastern Economic Corridor, and the Central Plains account for the majority of the national lubricant consumption due to high vehicle density and manufacturing concentration. Bangkok’s 10 million residents generate passenger-car and logistics demand, while the corridor’s automotive plants and Laem Chabang port underpin industrial and marine lubricants.

Agricultural provinces in the Central Plains rely on hydraulic and gear oils for 0.63 million tractors, whereas the northern and northeastern regions lag because of smaller fleets. Southern Thailand will gain importance as the Ranong-Chumphon land bridge adds port infrastructure that needs grease and hydraulic fluids.

Regulatory strictness varies: urban zones enforce EPR rules rigorously, stimulating sales of synthetics with longer drain intervals, whereas rural areas continue to favor lower-cost mineral oils.

Competitive Landscape

The Thailand Lubricants market is highly consolidated. Second-tier multinationals such as ExxonMobil, TotalEnergies, and ENEOS fill product gaps, while niche players like FUCHS and MOTUL focus on metalworking and food-grade oils. The pending Industrial Waste Management Act favors integrated refiners that can finance used-oil take-back schemes, pressuring small blenders. Digital oil-condition monitoring is emerging as a differentiator for fleet accounts, though adoption remains uneven.

Thailand Lubricants Industry Leaders

Chevron Corporation

PTT Public Company Limited

Shell Thailand

P.S.P. Specialties Public Company Limited

Bangchak Corporation Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Borneo Technical (Thailand) Ltd. announced a strategic partnership with Emirates National Oil Company (ENOC), a fully integrated global energy company based in Dubai, United Arab Emirates (UAE). Through this collaboration, Borneo was designated as the sole importer and exclusive official distributor of ENOC lubricants in Thailand, aiming to enhance the standards of Thailand's lubricants industry by introducing advanced solutions.

- September 2025: LIQUI MOLY expanded its production footprint beyond Germany, setting up operations in Thailand. This move was aimed at catering to the burgeoning demand in the Asian market.

Thailand Lubricants Market Report Scope

Lubricants, often oils or greases, are applied between moving surfaces to minimize friction, heat, and wear. These substances create a protective film, boosting mechanical efficiency, warding off corrosion, and prolonging machinery life. Common varieties encompass automotive engine oils, industrial lubricants, and transformer oils, all made from base oils and additives.

The Thailand Lubricants market is segmented by product type, end-user industry, and base stock type. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants.

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil & White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy & Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil & White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy & Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

How large will lubricant consumption be in Thailand by 2031?

Total demand is forecast to reach 778.73 million liters by 2031, up from 697.42 million liters in 2026.

What is driving the shift toward synthetic lubricants in Thailand?

Euro 5 diesel regulations, industrial automation, and extended drain strategies are pushing fleets and factories to adopt low-SAPS synthetic oils that offer longer service life and fuel savings.

How quickly are electric vehicles affecting lubricant demand?

BEV registrations approached 90,000 units by October 2025, and if the 30@30 goal is achieved, roughly 150 million liters of engine oil could be displaced annually.

Which geographic areas consume the most lubricants in Thailand?

Bangkok Metropolitan Region and the Eastern Economic Corridor together account for close to 70% of national lubricant volumes because of dense vehicle fleets and concentrated manufacturing.

Who are the leading suppliers of lubricants in Thailand?

PTT, Shell, Chevron, and Bangchak lead volume share, while ExxonMobil, TotalEnergies, ENEOS, FUCHS, and MOTUL compete in niche and industrial segments.

Page last updated on: