Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

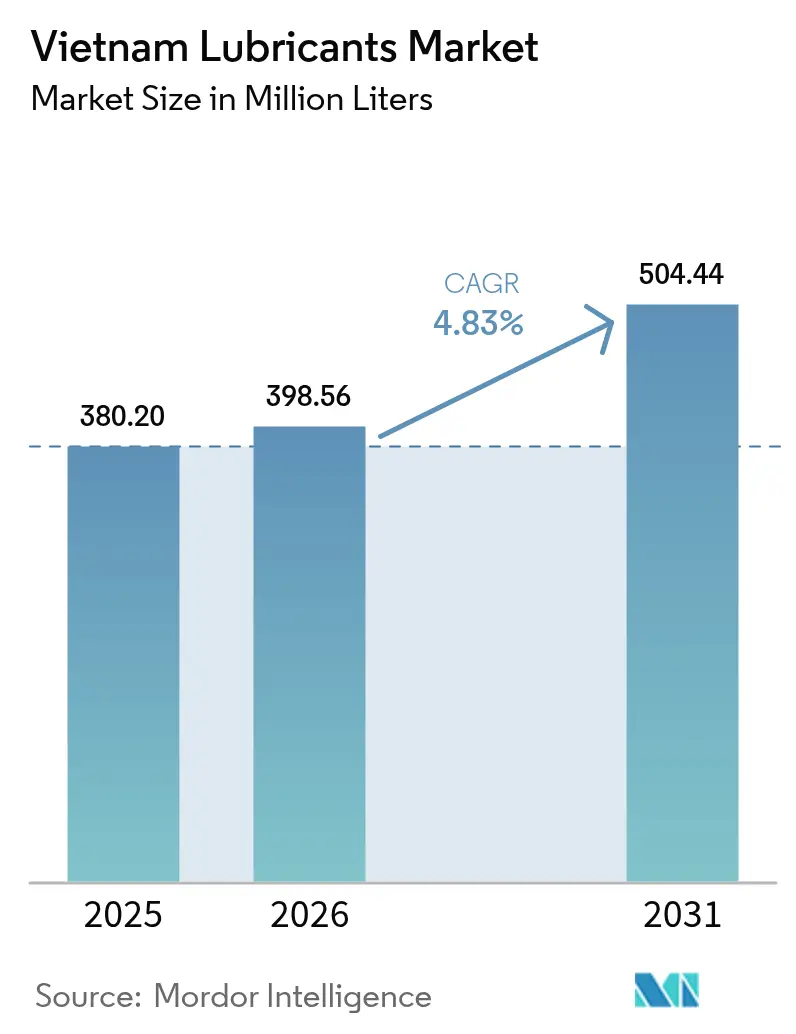

| Base Year Market Size (2025) | 380.20 Million liters |

| Market Volume (2026) | 398.56 Million liters |

| Market Volume (2031) | 504.44 Million liters |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Lubricants Market Analysis by Mordor Intelligence

Vietnam Lubricants Market size in 2026 is estimated at 398.56 million liters, growing from 2025 value of 380.20 million liters with 2031 projections showing 504.44 million liters, growing at 4.83% CAGR over 2026-2031. This growth persists even as electrification advances, because two-wheelers continue to dominate mobility, and new manufacturing investments keep industrial activity rising. An expanding vehicle parc sustains momentum, a shift toward higher-performance formulations, and steady foreign direct investment that lifts machinery demand across industrial zones. Market participants emphasize premium drain-interval products, broad distribution, and localized blending to protect margins against base-oil cost fluctuations. At the same time, looming environmental taxes and Extended Producer Responsibility (EPR) rules are steering producers toward synthetic and bio-based lines that command higher price points yet trim lifecycle emissions. These intersecting trends frame a resilient near-term outlook for the Vietnam lubricants market even as electric vehicles (EVs) gradually erode conventional engine oil volumes.

Key Report Takeaways

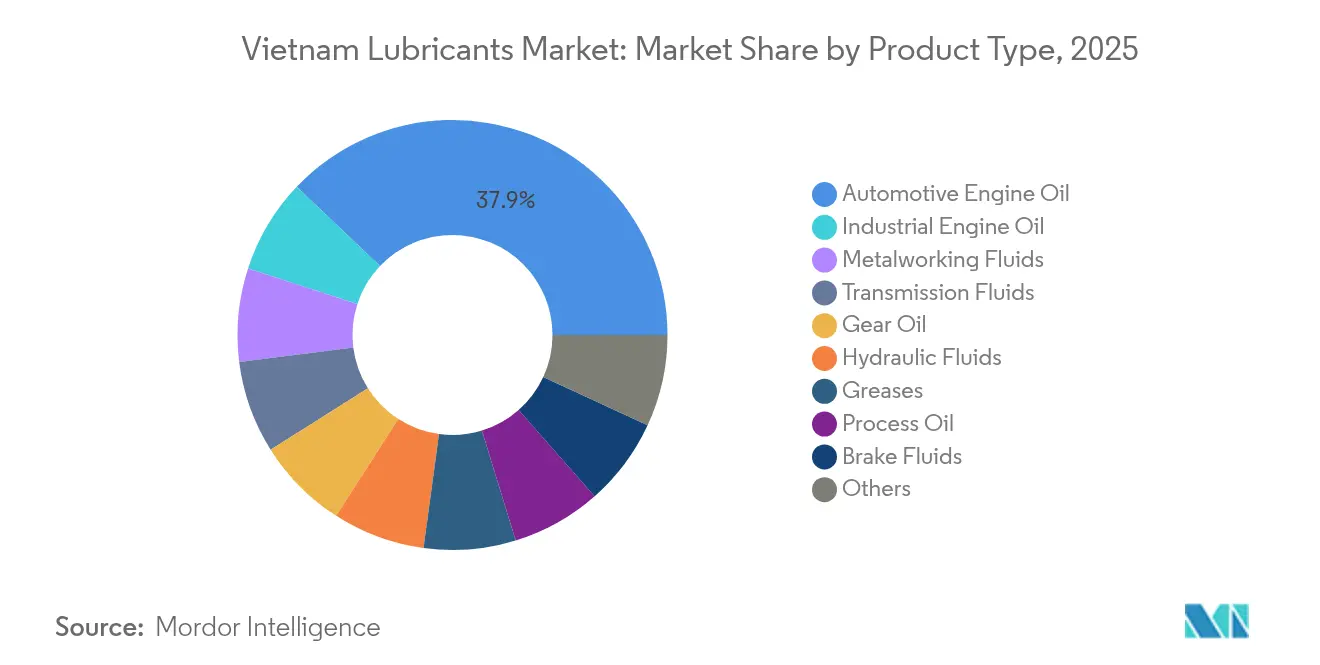

- By product type, automotive engine oil led with 37.90% revenue in 2025, while industrial engine oil is projected to advance at a 5.22% CAGR through 2031.

- By end-user industry, automotive applications accounted for 70.05% of the Vietnam lubricants market share in 2025; however, industrial users are projected to expand at a 5.08% CAGR through 2031.

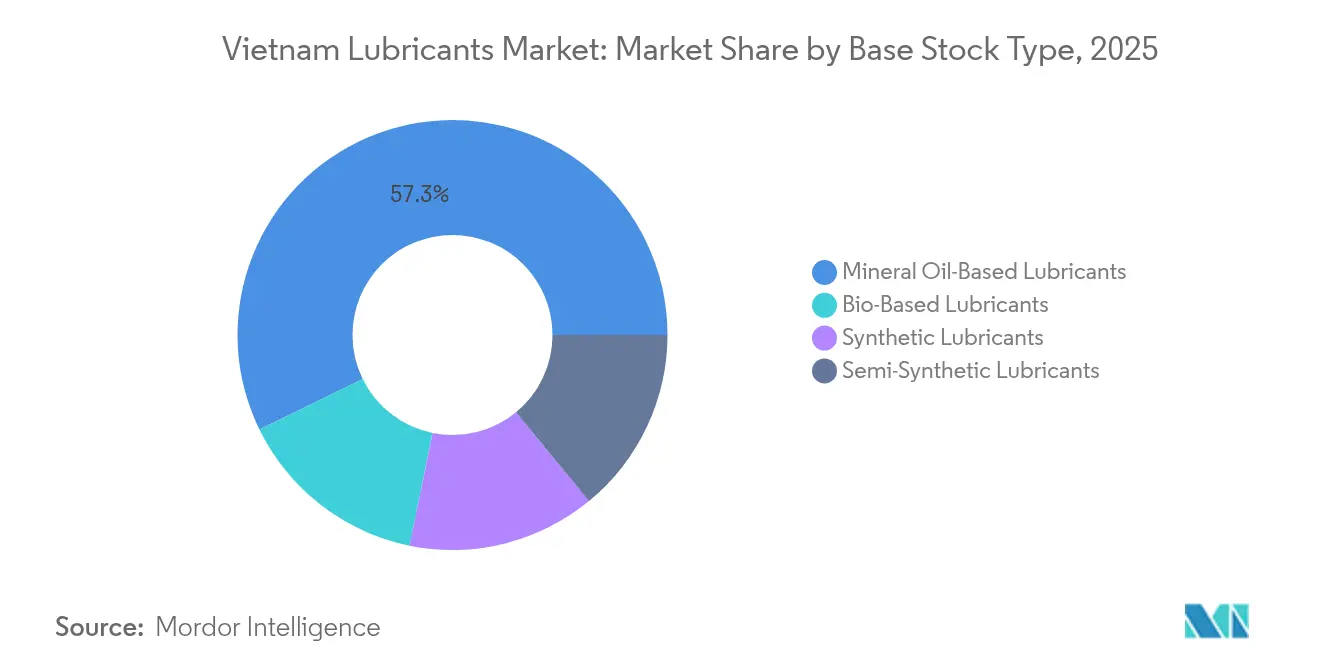

- By base stock, mineral-oil formulations retained 57.25% of the Vietnam lubricants market size in 2025; bio-based alternatives recorded the fastest 5.52% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle parc and two-wheeler dominance | +1.8% | Ho Chi Minh City, Hanoi | Medium term (2-4 years) |

| Accelerating industrialization and FDI manufacturing growth | +1.2% | Northern and southern industrial zones | Long term (≥ 4 years) |

| Shift toward synthetic/higher-performance lubricants | +0.9% | Urban centers | Medium term (2-4 years) |

| Growth of foreign-invested auto-component plants | +0.6% | Thai Binh, Hai Duong clusters | Long term (≥ 4 years) |

| Expansion of cross-border e-commerce logistics fleets | +0.4% | Border provinces, logistics corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Two-Wheeler Dominance

Vietnam’s industrial policy aims to achieve annual passenger-car and two-wheeler sales of approximately 1.0–1.1 million units by 2030. Two-wheelers still account for the majority of the vehicle fleet, preserving a large base of internal-combustion engines that require frequent oil changes. Although electric motorcycles accounted for a significant portion of new two-wheeler registrations in 2024, range anxiety outside urban cores continues to underpin sustained demand for mineral oil and semi-synthetic products. Regular maintenance cycles associated with motorcycles, combined with rising disposable incomes, continue to anchor volume growth for engine oils and transmission fluids[1]International Energy Agency, “Global EV Outlook 2024,” iea.org.

Accelerating Industrialization and FDI Manufacturing Growth

Manufacturing FDI reached USD 15.2 billion in the first six months of 2024, with processing and electronics plants accounting for more than two-thirds of the inflows. These capital injections translate into machinery installations that demand hydraulic, gear, and metalworking fluids engineered for longer drain intervals and lower downtime. Industrial parks in Hai Phong, Bac Ninh, and Dong Nai require OEM-approved lubricants that comply with global supply-chain audit standards. The resulting pull for synthetic and bio-based lubricants helps lift overall premium-product penetration through the forecast window.

Shift Toward Synthetic and Higher-Performance Lubricants

Emission regulations aligned with Euro 5 standards came into effect in 2025, accelerating customer migration from straight-grade mineral oils to low-SAPS synthetics that protect exhaust after-treatment systems. International brands introduced re-refined and bio-based ranges, such as Motul’s NGEN line, catering to fleet operators focused on reducing the total cost of ownership. Industrial users are also shifting toward poly-alpha-olefin-based hydraulic oils that can withstand elevated operating temperatures, thereby extending service intervals and reducing unplanned downtime in high-output factories.

Growth of Foreign-Invested Auto-Component Plants

Automotive component localization targets of 55–60% domestic value-add by 2030 are prompting Japanese and Korean OEMs to establish engine, transmission, and drivetrain facilities in Thai Binh and Hai Duong. These factories require specialized cutting fluids and stamping oils that meet stringent cleanliness benchmarks. They also create demand for dielectric and thermal-management fluids used in EV battery modules and inverter assemblies, which represent nascent but high-value lubricant niches.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Base-oil import price volatility | -0.8% | Nationwide | Short term (≤ 2 years) |

| Rapid rise of electric motorcycles | -1.1% | Hanoi, Ho Chi Minh City | Medium term (2-4 years) |

| Stricter used-oil disposal rules | -0.3% | Industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Base-Oil Import Price Volatility

Vietnam imports the majority of its base-oil requirement, exposing local blenders to global crude swings. A spike in Group II base-oil spot prices in 2024 compressed margins and led to retail price hikes across most viscosity grades. Independent blenders with limited inventory credit struggled to pass on costs, risking volume losses to heavily promoted international brands. As a result, some distributors trimmed rural stock levels, causing sporadic shortages in tier-3 cities until supply contracts normalized.

Rapid Rise of Electric Motorcycles

The share of electric two-wheelers in new sales increased in 2024, driven by government incentives and the development of urban charging networks. Each electrified motorcycle reduces annual engine oil demand by approximately 2–3 liters, directly eroding volume growth in densely populated cities. Battery-swapping ecosystems pioneered by VinFast also reduce friction for rural adoption, accelerating the displacement curve of lubricants in secondary towns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Engine Oil Drives Premium Growth

In 2025, automotive engine oil commands a 37.90% share of the market, underscoring Vietnam's transportation landscape, which is heavily skewed towards motorcycles. Here, both 2-stroke and 4-stroke engine oils cater to a staggering 77 million registered two-wheelers. Industrial engine oil is the fastest-growing product category, expanding at a 5.22% CAGR through 2031, driven by new gas-fired and renewable power projects. The demand is driven by OEM requirements for low-ash formulations that enable longer maintenance intervals. Transmission fluids are expected to benefit from increased automatic-transmission penetration in passenger cars, while gear oil demand is expected to align with the expansion of light-commercial and logistics fleets.

Metalworking fluids escalate in tandem with precision-machining investments by Samsung and Foxconn suppliers, and Master Fluid Solutions’ localized distribution underscores this trend. Turbine and transformer oils are experiencing steady growth as Vietnam’s Power Development Plan targets a 29% renewable capacity by 2030, creating specialty-fluid opportunities that offer attractive margins. Overall, the product mix is tilting toward higher-performance synthetics that accommodate high-load, high-temperature operating conditions in modern equipment.

By End-User Industry: Manufacturing Industrialization Accelerates Demand

Automotive applications still accounted for 70.05% of the Vietnam lubricants market share in 2025, anchored by the sizeable two-wheeler parc. Yet, industrial consumption is scaling faster, growing at a 5.08% CAGR amid sustained FDI inflows. Factories producing electronics, textiles, and metal components require ISO-grade hydraulic and gear oils that maintain viscosity stability over extended operating shifts.

Power generation growth, both conventional and renewable, adds steady volume for turbine, transformer, and compressor oils. The marine sector is benefiting from increased port capacity and cargo throughput, which is spurring demand for trunk-piston engine oils and environmentally friendly greases supplied by TotalEnergies at key harbors. Aerospace lubricant volumes remain minimal but show promise as maintenance, repair, and overhaul (MRO) facilities in Da Nang look to capture Southeast Asian airline contracts.

By Base Stock Type: Bio-Based Alternatives Gain Environmental Traction

Mineral-oil formulations accounted for 57.25% of total consumption in 2025, as price sensitivity remains high among motorcycle users and small workshops. Nonetheless, synthetics and semi-synthetics are gaining ground in urban centers where emission standards and fleet efficiency considerations override upfront costs. The Vietnam lubricants market's demand for synthetic grades is growing, reflecting a shift toward Group III and poly-alpha-olefin blends that extend drain intervals.

Bio-based and re-refined options, although starting from a small base, post the highest 5.52% CAGR. MOTUL’s NGEN range demonstrates commercial feasibility for re-refined base oils, while domestic blenders explore palm-oil esters derived from local agricultural feedstocks. Government tax incentives tied to lower carbon footprints further enhance the value proposition for these greener options.

Geography Analysis

Ho Chi Minh City, Binh Duong, and Dong Nai collectively accounted for a significant portion of national lubricant demand in 2025, due to the dense vehicle ownership and heavy industrialization in the southern growth corridor. Continuous infrastructure upgrades, including ring-road expansions and metro line construction, support the use of off-highway lubricants for excavators and concrete pumps in the region.

Northern provinces such as Hai Phong, Bac Ninh, and Thai Binh are emerging as the fastest-growing cluster, thanks to new electronics and automotive component plants that demand high-grade metalworking and hydraulic fluids. Hai Phong’s deep-water port upgrades, coupled with PETEC’s storage-capacity expansion, streamline lubricant logistics for both export and domestic distribution.

Central Vietnam, centered on Da Nang, experiences moderate growth driven by tourism and expanding maritime services. The Mekong Delta maintains resilient demand for agricultural-equipment oils, while border provinces capture incremental volumes from rising cross-border freight with China and Cambodia. Altogether, spatial consumption patterns reflect Vietnam’s broader economic rebalancing, as the northern and central regions narrow the historical gap with the south.

Regulatory Landscape

Vietnam regulates lubricants through a combination of product quality standards, chemical controls, and trading conditions that shape how producers, importers, and distributors operate. For internal-combustion engine oils, national technical regulation QCVN 14:2018/BKHCN (and subsequent consolidations) sets minimum quality and testing requirements, typically requiring certification and a declaration of conformity before products are placed on the market.

From January 1, 2026, the Law on Chemicals No. 69/2025/QH15 introduced a tighter compliance environment for chemical substances used in lubricant additive packages and related preparations, supported by implementing decrees that took effect from January 17, 2026. This shift adds procedural requirements for imports and handling of controlled chemicals. Distribution access also continues to be shaped by Vietnam's rules on trading rights for foreign-invested enterprises under Decree 09/2018/ND-CP, reinforcing the need for compliant local manufacturing and distributor partnerships for route-to-market.

Value Chain Analysis

Vietnam's lubricant value chain starts with reliance on imported base oils and additives, followed by local blending and packaging, then multi-tier distribution through national oil companies, independent distributors, workshops, and industrial procurement channels. Because Vietnam lacks domestic base stock production capacity, import logistics, customs procedures, and base-oil price swings are central to blending economics, inventory strategies, and retail pricing. Recent moves, such as ExxonMobil Asia Pacific appointing VietSea Chemicals as an exclusive distributor for EHC Group II base stocks in Vietnam, underscore how specialized import and distribution partners help stabilize upstream supply.

Downstream, route-to-market is strongly shaped by licensing and trading-right conditions that limit foreign-invested enterprises in retail distribution and narrow wholesale pathways. This increases the value of established domestic networks and localized production footprints. Compliance also extends into end-of-life management, with EPR rules under Decree No. 110/2026/ND-CP (effective May 25, 2026) increasing the role of used-oil collection, licensed recyclers, and re-refining within the extended value chain for engine oils and other lubricants.

Competitive Landscape

The Vietnam lubricants market is moderately consolidated. International majors utilize sophisticated brand marketing, OEM partnerships, and multi-grade synthetic portfolios to target premium segments. Domestic champions capture the national market share through their extensive state-affiliated distribution network and competitive pricing. Mid-tier players pursue white-space opportunities in specialty synthetics and EV-thermal fluids. Players are investing in localized research and development to tailor formulations for Vietnam’s hot-humid climate and variable fuel quality. Market success is increasingly dependent on technical service capabilities, inventory agility, and compliance with tightening EPR and emission regulations.

Vietnam Lubricants Industry Leaders

BP p.l.c.

Petrolimex (PLX)

Shell plc

TotalEnergies

Mekong Petrochemical JSC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is developing around compliance-driven circularity, where Decree No. 110/2026/ND-CP made EPR obligations for lubricants operational from May 25, 2026. That change requires brand owners and importers to secure used-oil collection and recycling capacity, creating room for licensed waste-oil collectors, re-refiners, and lubricant marketers that can bundle take-back programs with fleet service contracts, particularly in industrial zones and logistics corridors where maintenance volumes are concentrated.

Local manufacturing and technical service capabilities are also becoming a practical differentiator as Vietnam's industrial base expands and customers demand OEM-aligned fluids and documentation. Capacity and capability investments point to this direction, including NPOil's second blending plant in Tay Ninh (18,000 tonnes per year) and Motul Asia Pacific's Vilube factory expansion with a new R&D and customer experience center (groundbreaking in July 2026). At the same time, tighter chemical controls from the Law on Chemicals (effective January 1, 2026) and product-quality enforcement under QCVN 14:2018/BKHCN favor suppliers with strong formulation governance, compliant additive sourcing, and the ability to support audits for foreign-invested manufacturers operating in Vietnam.

Recent Industry Developments

- July 2026: Motul Asia Pacific held the groundbreaking ceremony for the expansion of its Vilube factory in Vietnam, adding a Research & Development and Customer Experience Centre as part of the site upgrade. The investment strengthens local formulation and testing capacity, supporting higher-performance synthetic, re-refined, and specialty lines demanded by industrial users and premium two-wheeler segments. The expanded footprint also improves supply responsiveness versus fully imported finished lubricants.

- August 2025: TotalEnergies announced completion of a rooftop solar PV and battery energy storage system at its lubricants plant in Go Dau, Dong Nai province, enabling the facility to cover up to 60% of its electricity needs with renewable power. The project lowers the operational carbon intensity of local blending and packaging, aligning plant operations with customer and partner decarbonization requirements. It also supports supply continuity by reducing exposure to grid variability for a key domestic production site.

- February 2025: Petrolimex signed a comprehensive cooperation agreement with Vinachem and VNPT focused on resource optimization, ecosystem expansion, and accelerated digital transformation. The partnership supports more integrated procurement, logistics coordination, and data-enabled selling across Petrolimex's downstream footprint, which is material for lubricant distribution reach. Greater digitalization can improve product traceability and service coverage for workshops and fleets as compliance and quality requirements tighten.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Vietnam lubricants market covers finished lubricants consumed within Vietnam across automotive and industrial uses, measured at the point of domestic sales into end-use demand and converted into market value using observed pricing levels.

Scope exclusions: This market sizing excludes base oils and additives sold as raw materials, as well as lubricants that are re-exported without being consumed domestically.

Segmentation Overview

- By Product Type

- Automotive Engine Oil

- Industrial Engine Oil

- Transmission Fluids

- Gear Oil

- Brake Fluids

- Hydraulic Fluids

- Greases

- Process Oil (Including Rubber Process Oil and White Oil)

- Metalworking Fluids

- Turbine Oil

- Transformer Oil

- Other Product Types

- By End-user Industry

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Marine

- Aerospace

- Heavy Equipment

- Construction

- Mining

- Agriculture

- Industrial

- Power Generation

- Metallurgy and Metalworking

- Textiles

- Oil and Gas

- Other End-Use Industries

- Automotive

- By Base Stock Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-Based Lubricants

Data Sources, Market Sizing, and Validation

Desk Research

We started with public statistics and technical references that help build the demand picture and cross-check trends. Common inputs included Vietnam vehicle registrations and fleet indicators from official transport agencies, macro and industry series from the General Statistics Office of Vietnam, and energy and industrial output context from sources such as the International Energy Agency.

To keep the model grounded in lubricant usage, we also reviewed trade and customs releases for finished lubricants and base oil movements, plus standards and technical notes from groups such as API and SAE that influence drain intervals and viscosity preferences. On top of that, company annual reports, investor presentations, and credible press were used to understand plant expansions, blending activity, channel shifts, and pricing behavior, with paid subscriptions for company financials, patent checks, and shipment-level import export validation where needed. This list is illustrative, and many other public and paid references were used for data collection, validation, and clarification during the analysis.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with lubricant blenders, distributors, workshops, fleet operators, and industrial maintenance teams so that desk assumptions could be corrected with real purchase behavior. We also spoke with trade participants involved in import distribution and with sector specialists in manufacturing hubs to validate product mix shifts, channel margins, and typical service intervals that drive consumption in liters.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 13% | |

| Mid tier: 40% | Functional/Unit leaders: 35% | |

| Smaller Players: 21% | Managers: 52% |

Market-Sizing & Forecasting

Sizing followed a top-down and bottom-up mix, with the main build anchored on a Vietnam demand pool in liters that is reconstructed from the in-use vehicle parc, industrial activity intensity, and typical lubricant change cycles. Once that consumption volume was established, it was translated into value by applying segment-level average selling prices that reflect observed pack sizes, base oil type mix, and channel markups.

Key inputs used in the model included the two-wheeler and passenger car population, commercial vehicle and off-highway activity proxies, manufacturing output indicators, average drain intervals (which differ by vehicle type and service quality), and the split between automotive and industrial usage. Because public data can be uneven by end-use, gaps were handled through conservative proxying, such as mapping industrial lubricant demand to sector output and then testing the implied liters per unit of activity through interviews.

Forecasting relied on scenario analysis supported by a simple multivariate regression layer, where lubricant volume growth is linked to fleet growth and industrial output expectations, and prices are adjusted using base oil cost direction and local inflation signals. Final totals were checked with selective bottom-up approximations like sampled SKU price points times estimated volumes by channel, followed by adjustments when the implied mix did not match field feedback.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, and then reviewed for anomalies that could come from unit conversion errors, extreme price assumptions, or sudden mix shifts. We also compare results against observable checkpoints such as lubricant import patterns, manufacturing activity changes, and workshop service trends to see if the implied market movement makes sense.

Before sign-off, a second analyst reviews key assumptions and the logic chain, and follow-up calls are triggered when a major variance is spotted by segment or year. Reports are refreshed annually, and interim updates are made when material events occur such as tax changes, plant additions, or sharp base oil price swings. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Vietnam Lubricants Market Size Compared With Other Published Estimates

Published market sizes for Vietnam lubricants can look far apart because the scope and measurement unit are not always aligned, and because price and mix assumptions move the value result quickly. Even when everyone talks about the same country, differences show up in whether the estimate is built from liters consumed, from sales revenues, or from a blend of both.

Import and customs checks for finished lubricants, along with fleet and workshop service signals, are the evidence used to keep Mordor Intelligence's estimate tied to liters actually consumed in-country, which are then converted into value using pricing levels that match the same time period. The biggest gaps usually come from including base oils and additives in the total, using aggressive price progression without validating pack mix, and mixing shipment value with consumption value without adjusting for inventory swings or currency timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.40 B (2026) | |

| Trade Journal A | USD 0.57 B (2024) | This figure is value-led and appears to depend heavily on revenue assumptions, where lubricant price and premium mix can be projected forward without being anchored to a liters-based demand build. |

| Industry Commentary B | USD 0.32 B (2024) | This estimate is reported in volume terms and can understate value when converted with a single average price, especially if it does not adjust for pack sizes, industrial product mix, and channel margins. |

Taken together, the spread is mostly explained by unit choice (liters versus USD) and by how prices are applied across the product mix. Our approach stays repeatable by starting from measurable consumption drivers, then layering pricing assumptions that are cross-checked through channel interviews and observable market signals.

Key Questions Answered in the Report

How large is the Vietnam lubricants market in 2026?

The volume reached 398.56 million liters in 2026, and the Vietnam lubricants market size is projected to grow at a 4.83% CAGR through 2031.

Which segment grows fastest through 2031?

Industrial engine oil is expected to record the highest 5.22% CAGR as new power plants and factories demand long-drain, high-performance formulations.

What drives the adoption of bio-based lubricants in Vietnam?

EPR recycling mandates and environmental-protection taxes, effective from 2026, encourage blenders to introduce palm-oil-based and re-refined products that qualify for lower levies.

How is electrification affecting lubricant demand?

Electric motorcycles account for a significant portion of new two-wheeler sales, reducing engine oil volumes in large cities but leaving industrial and commercial-vehicle demand largely intact for now.

Page last updated on: