Fuel Flow Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.19 Billion |

| Market Size (2031) | USD 8.08 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

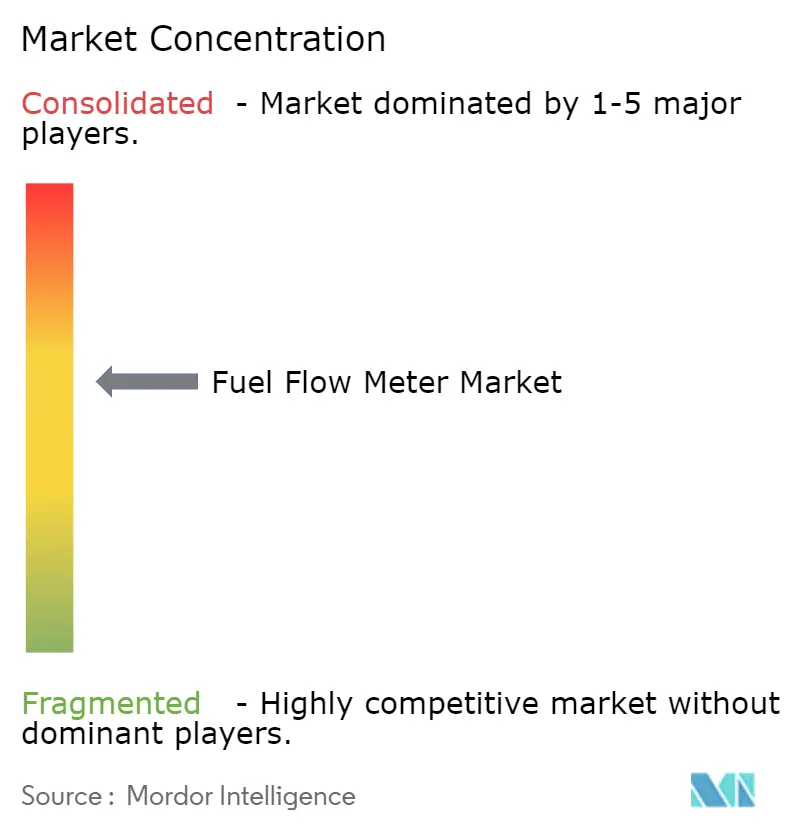

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fuel Flow Meter Market Analysis by Mordor Intelligence

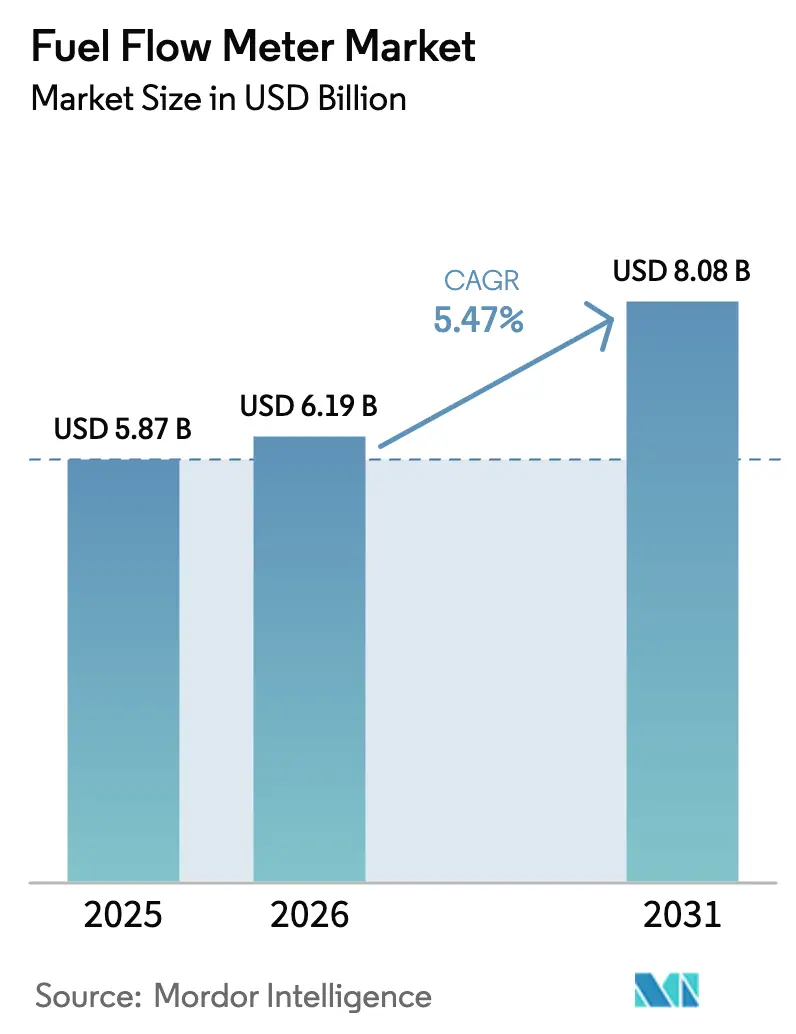

The fuel flow meter market size in 2026 is estimated at USD 6.19 billion, growing from 2025 value of USD 5.87 billion with 2031 projections showing USD 8.08 billion, growing at 5.47% CAGR over 2026-2031. Growth reflects the shift from mechanical devices to precision mass and ultrasonic solutions that satisfy stringent reporting rules and multi-fuel measurement needs.[1]Endress+Hauser, “Strategic partnership launched,” endress.com Regulatory catalysts such as the International Maritime Organization’s Data Collection System, the International Civil Aviation Organization’s net-zero milestones, and national carbon-neutrality roadmaps elevate demand for certified high-accuracy meters across marine, aviation, and industrial sectors.[2]International Maritime Organization, “MEPC 83 outcomes,” imo.org Suppliers are responding with advanced diagnostics, multi-fluid calibration, and digital connectivity that enable remote performance monitoring, fraud detection, and predictive maintenance.[3]VERIDAPT, “Masters in Fuel Management,” veridapt.com Rising LNG bunkering activity and hydrogen blending pilots further accelerate adoption of cryogen.[4]Maritime and Port Authority of Singapore, “LNG Bunkering Pilot Programme,” mpa.gov.sg

Key Report Takeaways

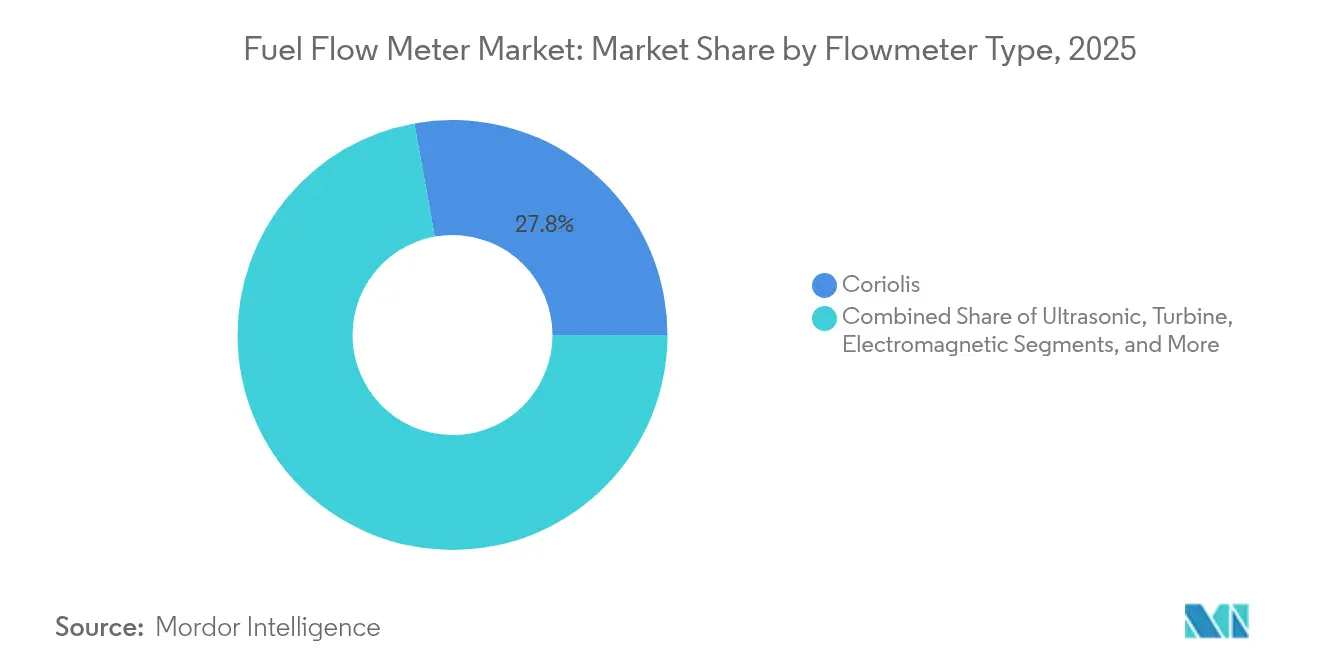

- By flowmeter type, Coriolis technology led with 27.84% of fuel flow meter market share in 2025, while ultrasonic systems are poised for a 5.65% CAGR through 2031.

- By fuel type, diesel still accounted for 56.05% share of the fuel flow meter market size in 2025; LNG and other cryogenic fuels are projected to expand at a 5.88% CAGR to 2031.

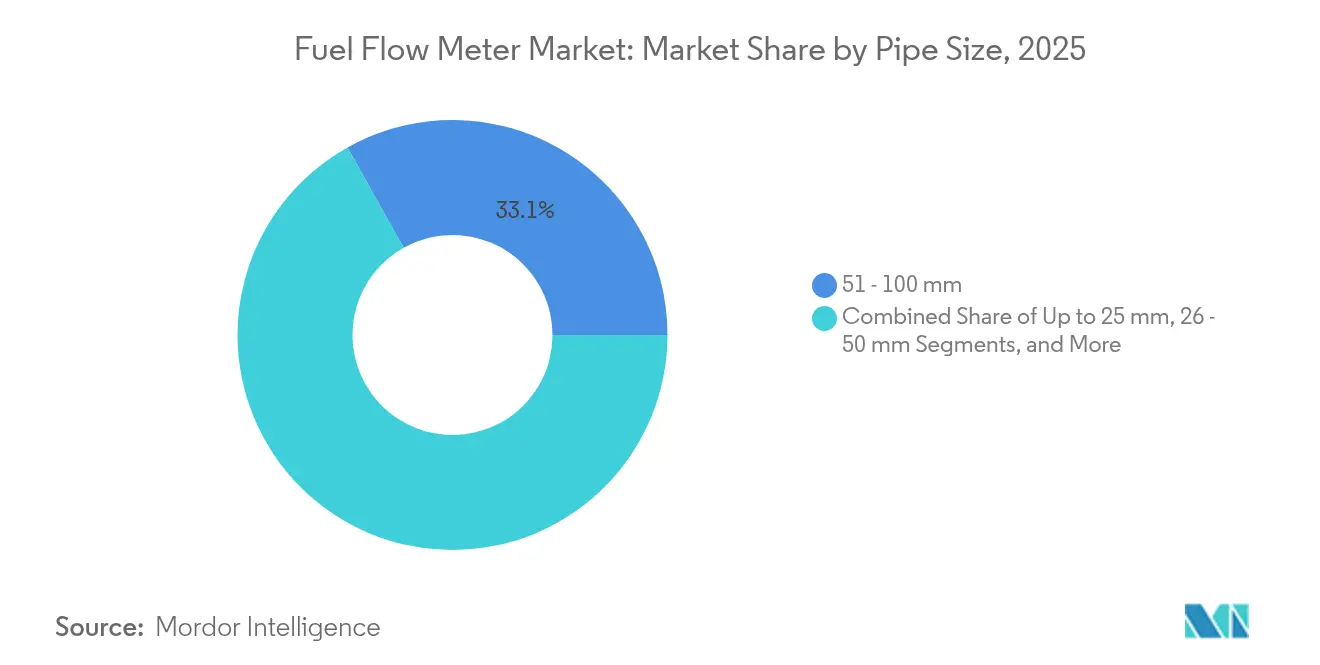

- By pipe size, 51-100 mm lines commanded 33.12% of the fuel flow meter market size in 2025, whereas pipes above 100 mm are set to grow at 5.92% annually.

- By industry vertical, oil and gas held 41.70% of the fuel flow meter market size in 2025, yet aerospace and defense is accelerating with a 6.8% CAGR through 2031.

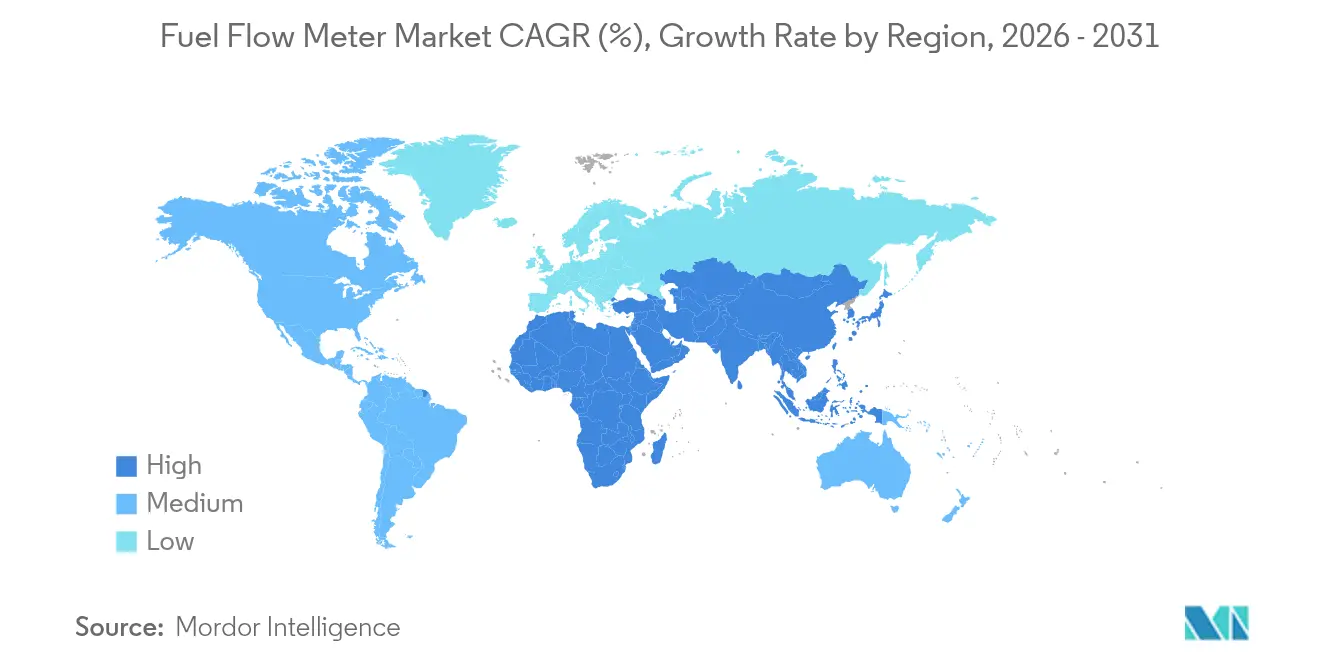

- By geography, Asia-Pacific captured 34.40% of the fuel flow meter market share in 2025; the region is expected to post the fastest 6.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fuel Flow Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent IMO DCS mandates accelerating maritime adoption | +1.2% | Global, with early adoption in EU and Asia-Pacific | Short term (≤ 2 years) |

| Real-time aviation fuel optimization systems integrating precision meters | +0.8% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| LNG bunkering expansion requiring cryogenic-capable Coriolis meters | +0.7% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Autonomous mining fleets’ need for remote diesel monitoring | +0.5% | Australia, Canada, Chile, expanding to Africa | Long term (≥ 4 years) |

| Shift to low-carbon fuels demanding multi-fluid calibration | +0.6% | Global, led by EU and California | Long term (≥ 4 years) |

| Fuel theft mitigation in emerging markets via IoT-enabled meters | +0.4% | Africa, Latin America, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent IMO DCS Mandates Accelerating Maritime Adoption

The 2024 implementation of the IMO Data Collection System obliges vessels over 5,000 GT to report actual fuel consumption, eliminating historical estimations and forcing rapid upgrades to certified meters that meet ±2.5% accuracy. About 60,000 ships now fall under this rule, creating a sizeable retrofit opportunity within the fuel flow meter market. Providers such as KROHNE bundle mass-flow hardware with automated carbon-emissions software to ensure compliance with both IMO and EU MRV frameworks. The policy impact is immediate because many fleets still operate legacy mechanical devices that lack electronic outputs for data transfer. Early adoption is strongest in European and Asian flag states where enforcement mechanisms are mature. These factors collectively add momentum to global fuel flow meter market growth.

Real-time Aviation Fuel Optimization Systems Integrating Precision Meters

Airlines integrate mass-flow sensors with flight-management computers to adjust fuel delivery in real time, trimming consumption by up to 3% per flight and supporting net-zero goals. Safran’s LiSafe and Eaton’s digital gauges reduce wiring weight while delivering ±0.1% accuracy, a level that conventional turbine meters cannot match. These upgrades improve operational performance and unlock direct savings that offset higher unit prices, strengthening the value proposition of premium meters. Certification to handle bio-jet and power-to-liquid blends future-proofs aircraft fleets. Expansion into Asia-Pacific fleets will widen the addressable fuel flow meter market as regional carriers modernize.

LNG Bunkering Expansion Requiring Cryogenic-Capable Coriolis Meters

Singapore’s 2024 bunkering standards prescribe OIML R 137 Class 1.0 meters for LNG custody transfer, elevating the technical baseline across Southeast Asian ports. Cryogenic Coriolis devices such as Chart Industries’ DynaFlow 3000 handle -162 °C liquid with proven custody accuracy, and Endress+Hauser’s FLOWSIC600-XT ultrasonic unit maintains performance even with 30% hydrogen blends. As shipowners switch to dual-fuel engines, installers prefer non-intrusive designs that minimize pressure loss and simplify maintenance. The LNG-focused driver boosts regional adoption yet also influences global fuel flow meter market specifications for future e-methanol and ammonia fuels.

Autonomous Mining Fleets’ Need for Remote Diesel Monitoring

Large open-pit mines operate around-the-clock and increasingly deploy driverless haul trucks. VERIDAPT’s AdaptFMS reduced reconciliation variance to 0.02% at Roy Hill in 2024 by linking tank sensors, mobile meters, and cloud analytics. The combination improves asset utilization and detects theft in remote locations where manual checks are impractical. Mining operators can therefore justify premium hardware by recouping losses through accurate billing and lower downtime. Digital continuity across mixed diesel and battery fleets also supports emissions accounting. This long-term driver aligns with expanding resource projects in Australia, Latin America, and Africa, lifting regional demand within the fuel flow meter market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of high-accuracy Coriolis vs mechanical meters | -0.9% | Global, particularly in price-sensitive markets | Short term (≤ 2 years) |

| Retrofitting downtime on aging offshore platforms | -0.6% | North Sea, Gulf of Mexico, offshore Brazil | Medium term (2-4 years) |

| Calibration complexity with very-low-sulfur marine fuels | -0.4% | Global maritime, concentrated in major ports | Short term (≤ 2 years) |

| Substitution by ECU-based virtual fuel flow analytics | -0.8% | Oil & gas upstream, particularly in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of High-Accuracy Coriolis vs Mechanical Meters

Coriolis units often cost three-to-five times more than turbine meters, and specialized mounting pushes installed cost even higher. The sticker shock discourages upgrades in applications where volumetric measurement suffices. Operators weighing short-term budgets against lifecycle savings may postpone purchases, trimming near-term growth of the fuel flow meter market. Yet the maintenance-free design and direct mass output still lower total cost of ownership, so the restraint is expected to ease as financing models evolve.

Substitution by ECU-Based Virtual Fuel Flow Analytics

In automotive and upstream oil fields, software derives flow rates from engine parameters, avoiding hardware and installation expenses that can exceed USD 2 million per offshore platform. Virtual metering can achieve up to 85% CAPEX savings, making it attractive for brownfield assets. Accuracy limitations, however, restrict virtual tools from custody transfer or regulatory reporting. While these systems temper hardware sales, they also open new hybrid solutions that integrate low-cost sensors with analytics, partially offsetting the restraint on the fuel flow meter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flowmeter Type: Coriolis Technology Dominates Precision Applications

Coriolis meters delivered 27.84% of fuel flow meter market share in 2025, underscoring their role in custody transfer and multi-fuel operations. Their direct mass measurement eliminates density corrections and supports hydrogen, LNG, and biofuel blends without recalibration. Adoption rises in pipe sizes above 2 inches as plant operators consolidate flow points to reduce leak paths and maintenance. Ultrasonic meters gain the momentum to post a 5.65% CAGR, primarily because clamp-on designs from newly acquired Flexim shorten shutdowns during retrofits. Turbine and positive-displacement units retain niche roles in low-viscosity or low-flow applications where budget constraints persist. Vortex and electromagnetic technologies occupy smaller shares but remain viable for steam or conductive liquids. The combined effect keeps supplier R&D focused on multi-path signal processing, self-diagnostics, and cybersecurity hardening, illustrating how technology diversity sustains expansion in the fuel flow meter market.

Across 2026-2031, Coriolis vendors aim to lift wetted-line diameters to 16 inches, enabling penetration into bulk terminals where ultrasonic meters have historically prevailed. Modular transmitters with advanced diagnostics detect entrained gas, coating, or vibration issues in real time, cutting troubleshooting labor. Integrators now bundle Coriolis meters with energy-management software to give users a single dashboard that covers rate, density, temperature, and emissions. Such ecosystem thinking embeds hardware deeper into customer workflows, reinforcing retention and recurring revenue. These factors elevate Coriolis dominance yet also spur complementary ultrasonic growth, showing that multi-technology portfolios underpin long-term resilience within the fuel flow meter market.

By Fuel Type: Diesel Dominance Challenged by Alternative Fuels

Diesel still accounts for 56.05% of the fuel flow meter market size because heavy-duty trucking, rail, and backup power remain diesel-centric. Nonetheless, LNG and other cryogens lead growth at a 5.88% CAGR as shipping and on-road fleets pivot to low-carbon fuels. Cryogenic transfers demand Class 1.0 accuracy at -162 °C, which only a limited set of Coriolis and ultrasonic designs can meet. Aviation accelerates sustainable fuel adoption, prompting meter suppliers to qualify hardware under ASTM D4054 for e-kerosene and HEFA blends. Heavy fuel oil declines as IMO sulfur caps tighten, yet it still requires viscous-service meters for auxiliary engines in short-sea corridors. Hydrogen and ammonia pilots create niche demand for low-density gas metering, commanding premium prices and raising average selling values across the fuel flow meter market.

Fuel diversity pushes vendors to develop calibration rigs that simulate wide temperature, pressure, and viscosity profiles. Multi-fluid firmware now stores up to 20 product curves in a single transmitter, letting users switch fuels without field recalibration. These capabilities lower change-over time and inventory costs. As renewable diesel blends permeate road transport, the ability to detect density and viscosity shifts becomes an operational necessity, locking in advanced meters with digital density measurement. The shift expands addressable applications and shields the fuel flow meter market from macro-fuel substitution risk.

By Pipe Size: Mid-Range Dominance with Large-Bore Growth

Lines measuring 51-100 mm held 33.12% of the fuel flow meter market size in 2025, reflecting widespread usage in industrial boilers, marine auxiliaries, and city-gate gas stations. Operators value this diameter for balancing capital cost and flow capacity. Yet pipelines above 100 mm grow fastest at 5.92% CAGR as LNG terminals, petrochemical complexes, and utility-scale hydrogen networks scale throughput. Large-bore Coriolis meters attract attention because they introduce negligible pressure loss while offering custody-level accuracy. Ultrasonic transit-time devices also thrive due to multi-path architectures that compensate for swirl, enabling accurate readings even in short upstream straight runs. Small-bore segments up to 25 mm cater to aerospace fuel lines, laboratory test rigs, and automotive calibration benches. The 26-50 mm tier supports mid-sized fleets such as regional buses and coastal vessels.

Increasing line sizes encourage suppliers to lightweight meter bodies and apply abrasion-resistant linings to protect against particulate-laden fuels like bunker blends. Electronics upgrades push diagnostic coverage beyond 95% of failure modes, supporting predictive maintenance programs. Remote configuration over secure protocols minimizes site visits, a benefit for widely distributed energy infrastructure. Together, these innovations broaden pipe-size applicability and enable the fuel flow meter market to capture large-volume growth with minimal trade-offs in accuracy.

By Industry Vertical: Oil and Gas Leadership with Aerospace Acceleration

Oil and gas commanded 41.70% of the fuel flow meter market size in 2025, spanning upstream allocation, pipeline custody transfer, and refinery blending. Stringent fiscal metering rules and carbon accounting favor high-accuracy devices. Meanwhile, aerospace and defense post a 6.8% CAGR, as mass-flow sensors integrate with digital avionics to accommodate sustainable fuels and lightweight architectures. Marine transport accelerates adoption under IMO mandates, while mining adopts IoT-enabled meters to support autonomous vehicle fleets.

Automotive telematics embed compact sensors for theft detection and eco-driving analytics, creating volume opportunities for lower-cost models. Power generation and utilities deploy large-bore devices to verify gas turbine fuel feed and allocate cost among multiple independent power producers sharing a facility. Chemical processing needs corrosion-resistant materials that withstand aggressive solvents. Agriculture requires vibration-proof designs for mobile machinery. Across sectors, the convergence of cybersecurity, cloud connectivity, and sustainability reporting drives vendors to position meters as data hubs rather than isolated instruments, sustaining expansion across the fuel flow meter market.

Geography Analysis

Asia-Pacific dominated the fuel flow meter market with a 34.40% share in 2025 and leads in growth with a 6.25% CAGR through 2031, buoyed by China’s carbon-neutrality program, Japan’s hydrogen initiatives, and India’s industrial upgrades. Singapore’s LNG bunkering protocols act as a regional reference, standardizing meter specifications across Southeast Asian ports. Local manufacturing hubs shorten lead times and reduce cost, strengthening competitiveness of Asia-based suppliers within the fuel flow meter market.

North America ranks second, propelled by shale gas custody transfer, strict EPA emissions rules, and aerospace innovation clusters. The region witnesses early trials of hydrogen transmission lines that require low-density gas calibration. Investment in digital twins and predictive analytics enhances demand for smart meters that integrate seamlessly with SCADA systems.

Europe maintains regulatory leadership, enforcing EU MRV and Fit-for-55 packages that incentivize advanced measurement on vessels and industrial boilers. The continent’s hydrogen economy roadmap drives R&D for meters handling variable-composition blends while meeting ATEX safety codes. Eastern Europe’s modernizing refineries and district heating networks also contribute incremental demand.

The Middle East and Africa benefit from large-scale oil and gas investments and mining projects, though harsh climates necessitate ruggedized enclosures and high-IP ratings. South America, led by Brazil’s offshore energy expansion and Chilean copper mines, shows growing interest in remote, cloud-enabled monitoring to cut operational costs. These regional variations ensure that technology portfolios remain diversified, safeguarding resilience in the global fuel flow meter market.

Competitive Landscape

The fuel flow meter market shows moderate consolidation. Top players expand portfolios through M&A to cover mass, ultrasonic, and clamp-on variants. Emerson’s 2024 purchase of Flexim added clamp-on ultrasonic expertise, complementing its existing Micro Motion Coriolis line and supporting a data-rich automation strategy. Endress+Hauser and SICK formed a process-automation joint venture employing 730 staff, signaling deeper specialization in gas flow analytics.

Product differentiation hinges on multi-fuel calibration, cryogenic capability, and embedded diagnostics. Baker Hughes introduced the T5MAX transducer for low-flow hydrogen measurement, enhancing its Panametrics ultrasonic portfolio. KROHNE deployed OPTIMASS 6400 meters in hydrogen pipelines, reinforcing credibility in emerging low-density applications. Siemens positions its digital water network solutions around smart flow meters that use AI leak detection to cut losses by up to 50%.

Start-ups focus on virtual metering, cloud analytics, and cybersecurity layers, providing collaboration or acquisition targets for incumbents aiming to integrate hardware and software stacks. Competitive intensity also stems from regional manufacturers that leverage cost advantages to penetrate price-sensitive markets. Overall, suppliers with wide technology coverage, strong service networks, and regulatory fluency retain an edge in capturing recurrent growth of the fuel flow meter market.

Fuel Flow Meter Industry Leaders

Emerson Electric Co.

Honeywell International Inc.

Endress+Hauser Group

Schneider Electric

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SICK and Endress+Hauser launched a strategic partnership in process automation, combining analyzer and flow-meter products to address sustainable applications.

- April 2025: MO’s MEPC 83 approved the Net-Zero Framework, tightening fuel data transparency and boosting meter demand across the commercial fleet.

- November 2024: Siemens reported EUR 75.9 billion revenue and pledged further R&D outlays in industrial software, supporting greater meter-software integration

- October 2024: KROHNE installed OPTIMASS 6400 meters for hydrogen service at MERSEN, validating Coriolis accuracy in low-density gases

Global Fuel Flow Meter Market Report Scope

The fuel flowmeter market encompasses the production, sale, and deployment of devices used to measure the flow rate and volume of fuel consumed across various industries such as automotive, aerospace, oil & gas, and manufacturing. These instruments are crucial for optimizing fuel efficiency, reducing wastage, and ensuring compliance with environmental regulations. The market includes diverse technologies such as positive displacement, turbine, ultrasonic, and smart flowmeters tailored for specific applications and fuel types.

The fuel flow meter market is segmented by type of flowmeter (positive displacement flowmeter, Coriolis flowmeter, ultrasonic flowmeter, turbine flowmeter, electromagnetic flowmeter, vortex flowmeter, and other types), industry vertical (automotive, aerospace, oil & gas, industrial (power, chemical, etc.), marine, agriculture, and other industry vertical), and Geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (usd) for all the above segments.

| Positive Displacement |

| Coriolis |

| Ultrasonic |

| Turbine |

| Electromagnetic |

| Vortex |

| Other Types |

| Diesel |

| Heavy Fuel Oil (HFO) |

| LNG/Cryogenic Fuels |

| Alternative and Biofuels (E-Methan ol, Biodiesel, SAF) |

| Upto 25 mm |

| 26 - 50 mm |

| 51 - 100 mm |

| Above 100 mm |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Marine and Shipping |

| Automotive and Commercial Fleet Management |

| Aerospace and Defense |

| Industrial Power Generation and Utilities |

| Chemicals and Process Industries |

| Agriculture and Off-Road Machinery |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Flowmeter Type | Positive Displacement | ||

| Coriolis | |||

| Ultrasonic | |||

| Turbine | |||

| Electromagnetic | |||

| Vortex | |||

| Other Types | |||

| By Fuel Type | Diesel | ||

| Heavy Fuel Oil (HFO) | |||

| LNG/Cryogenic Fuels | |||

| Alternative and Biofuels (E-Methan ol, Biodiesel, SAF) | |||

| By Pipe Size | Upto 25 mm | ||

| 26 - 50 mm | |||

| 51 - 100 mm | |||

| Above 100 mm | |||

| By Industry Vertical | Oil and Gas (Upstream, Midstream, Downstream) | ||

| Marine and Shipping | |||

| Automotive and Commercial Fleet Management | |||

| Aerospace and Defense | |||

| Industrial Power Generation and Utilities | |||

| Chemicals and Process Industries | |||

| Agriculture and Off-Road Machinery | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current fuel flow meter market size?

The fuel flow meter market size stands at USD 6.19 billion in 2026 and is projected to reach USD 8.08 billion by 2031.

Which region leads the fuel flow meter market?

Asia-Pacific led with 34.40% market share in 2025 and is also the fastest-growing region at a 6.25% CAGR through 2031.

Why are Coriolis meters popular in marine applications?

Coriolis technology meets IMO accuracy requirements, handles multi-fuel blends, and offers direct mass measurement essential for custody transfer.

What restrains rapid adoption of high-accuracy meters?

High upfront capital cost and emerging virtual flow analytics can delay purchases in price-sensitive or retrofit scenarios.

Which industry vertical is growing fastest?

Aerospace and defense is the fastest-growing vertical, advancing at 6.8% annually as sustainable aviation fuel adoption expands.

How does LNG bunkering influence meter demand?

Rising LNG bunkering mandates cryogenic-capable Class 1.0 meters, driving regional specifications that spread globally through port networks.

Page last updated on: