Moving Services (Mover And Packers) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

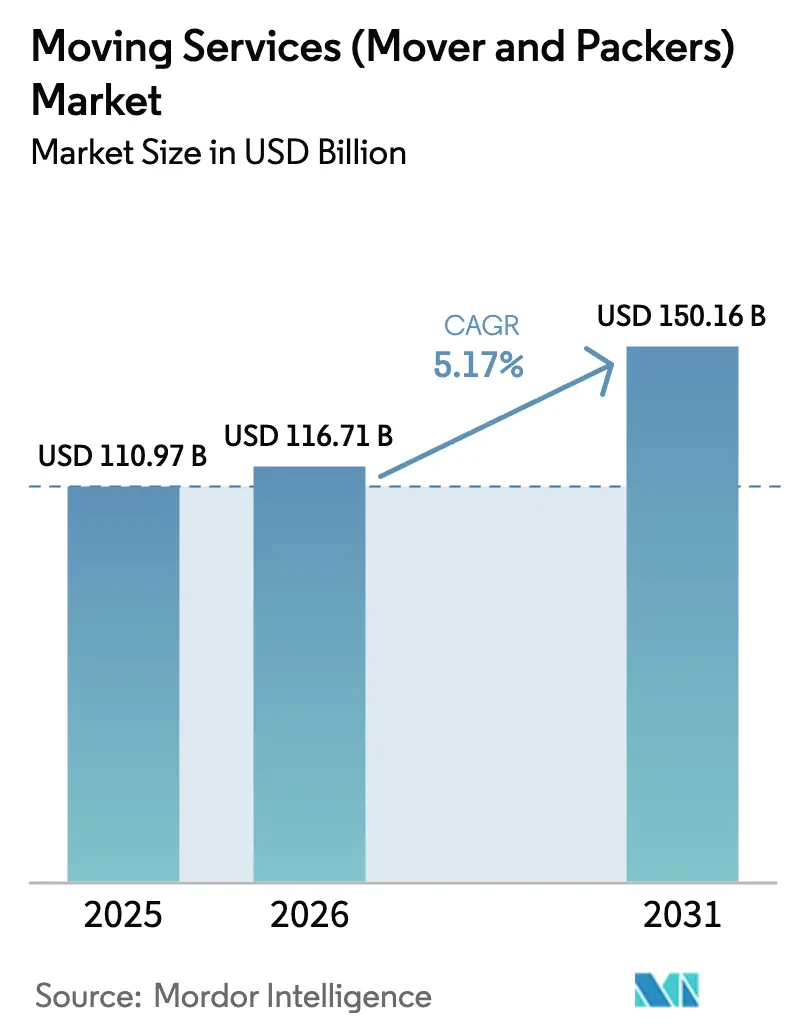

| Market Size (2026) | USD 116.71 Billion |

| Market Size (2031) | USD 150.16 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

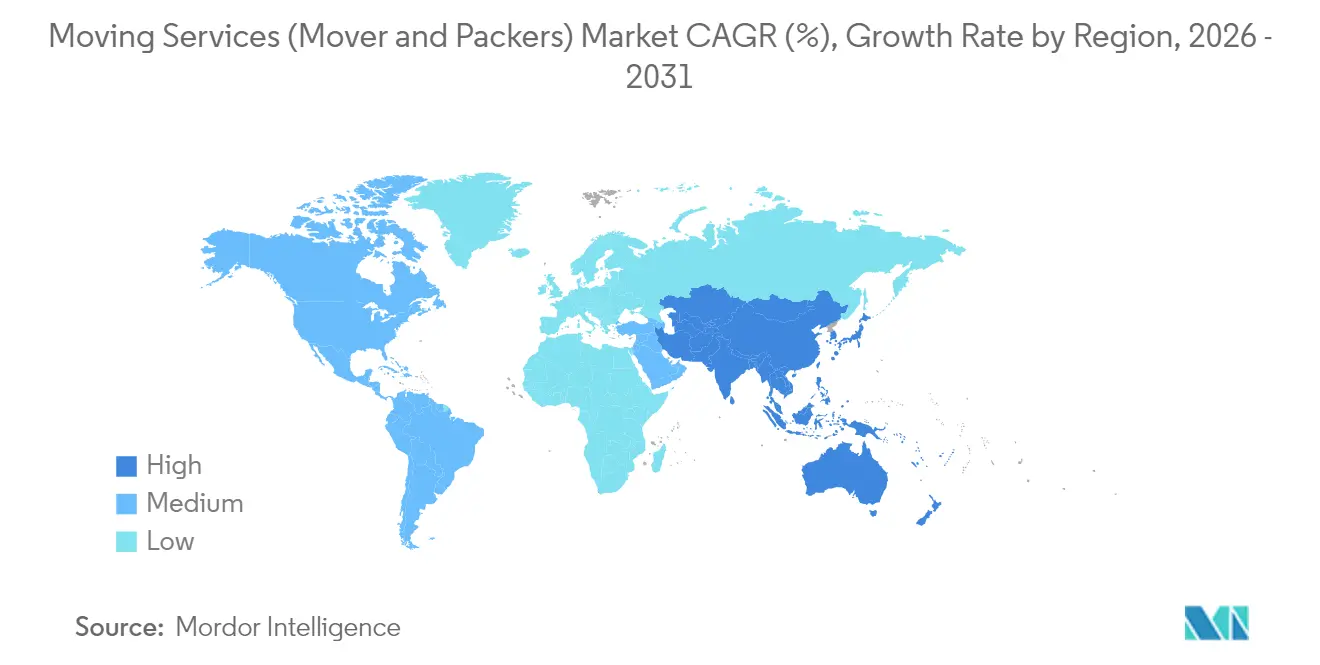

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Moving Services (Mover And Packers) Market Analysis by Mordor Intelligence

The Moving Services Market size was valued at USD 110.97 billion in 2025 and estimated to grow from USD 116.71 billion in 2026 to reach USD 150.16 billion by 2031, at a CAGR of 5.17% during the forecast period (2026-2031).

Residential demand anchored by rebounding housing activity in major metropolitan areas and corporate relocation outsourcing that turns mobility into a strategic talent lever are the central engines of growth in the moving services market. Technology investments—from AI‐powered virtual surveys to SaaS dispatch platforms—are trimming operational costs, enhancing customer experience, and allowing nimble operators to win share in the moving services market. Last-mile warehousing shifts created by e-commerce continue to spawn specialized relocation flows for racking, automation gear, and high-value equipment, further expanding the moving services market. Regionally, North America’s mature yet active housing sector sustains volume leadership, while Asia-Pacific’s rapid urbanization and cross-border trade make it the fastest-growing arena in the moving services market.

Key Report Takeaways

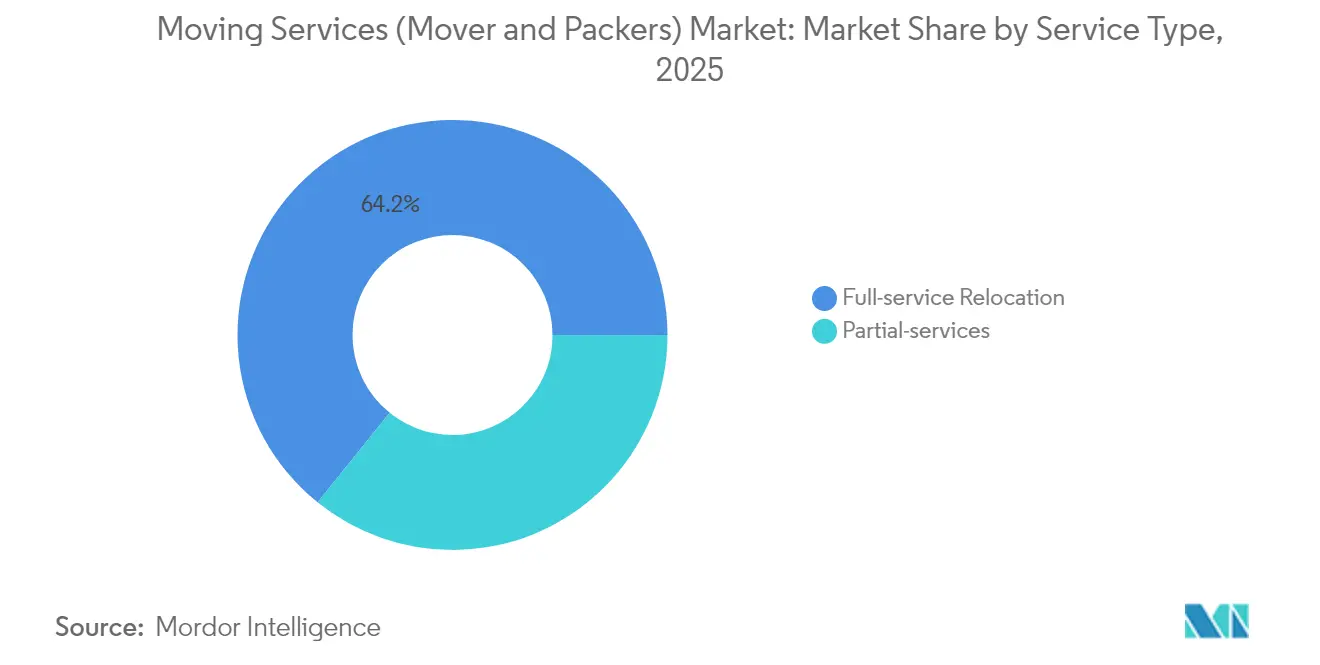

- By service type, full-service relocation held a 64.20% revenue share in 2025, while partial services are rising at a 5.32% CAGR to 2031.

- By end-user industry, the residential segment commanded 41.20% of the moving services market share in 2025; the commercial segment is advancing at a 5.18% CAGR through 2031.

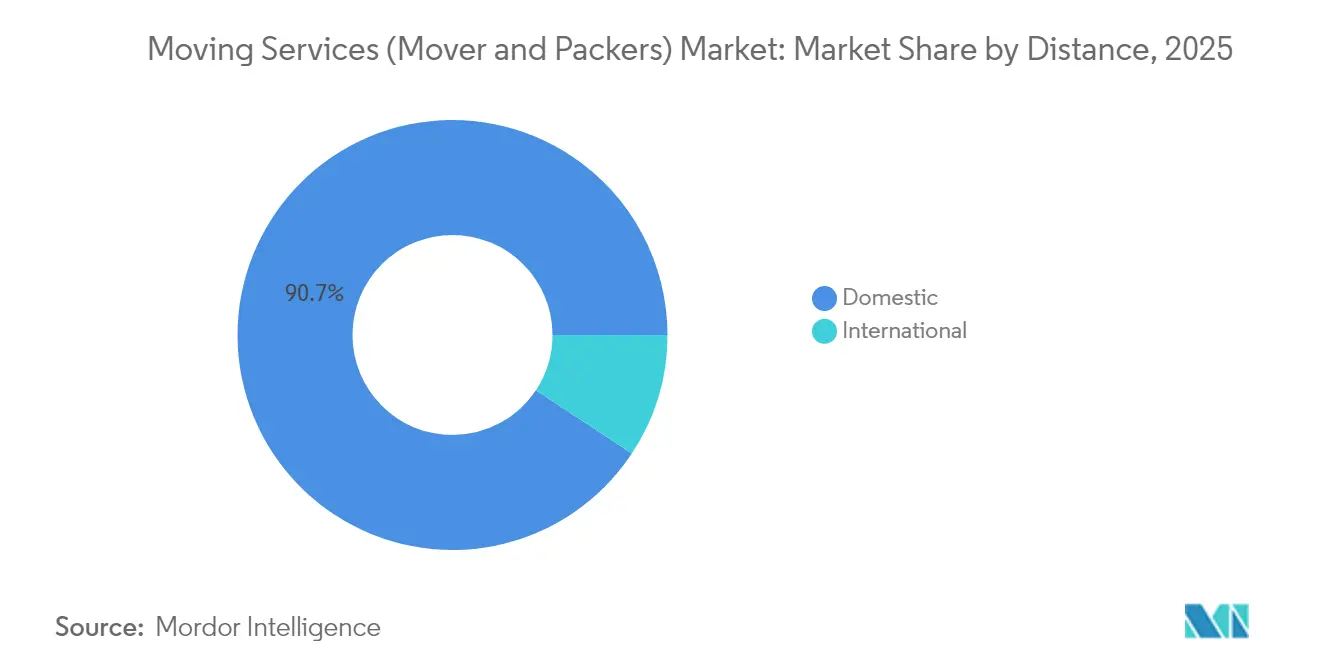

- By distance, domestic moves represented 90.70% of the moving services market size in 2025, yet international relocations are expanding at a 5.24% CAGR to 2031.

- By booking channel, offline interactions captured 63.40% share of the moving services market in 2025; online platforms are projected to post a 5.28% CAGR through 2031.

- By geography, North America led with a 32.70% share in 2025, while Asia-Pacific is on track for a 5.62% CAGR and is the fastest-growing territory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Moving Services (Mover And Packers) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing-Market Rebound in Key Metros | +1.2% | North America & Europe | Medium term (2-4 years) |

| Corporate Relocation Program Outsourcing | +0.9% | Global, concentrated in North America & Asia-Pacific | Long term (≥ 4 years) |

| E-Commerce-Fuelled Last-Mile Warehousing | +0.8% | Global, with APAC leadership | Medium term (2-4 years) |

| SaaS-Based Dispatch & Virtual Surveys | +0.7% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Labor-Scarcity Push Toward Value-Added Packing | +0.6% | North America & Europe | Medium term (2-4 years) |

| On-Demand Self-Storage Bundling | +0.5% | North America, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Housing-Market Rebound in Key Metros

Strong resale volumes and pent-up demand in gateway cities are motivating households to swap expensive urban homes for affordable secondary markets, thereby stimulating long-distance bookings in the moving services market. Real estate investors are actively repositioning portfolios, which prompts multiple property-level moves that sustain peak-season capacity utilization. Federal Motor Carrier Safety Administration oversight offers clear quality benchmarks that support premium pricing for interstate moves and protect consumer trust during high-volume periods[1]Federal Motor Carrier Safety Administration, “Protect Your Move,” fmcsa.dot.gov. The migration of skilled workers toward suburban tech hubs extends average haul lengths and yields higher revenue per job. Together, these elements add positive momentum to the moving services market.

Corporate Relocation Program Outsourcing

Multinationals have converted mobility budgets from fixed overheads to scalable third-party contracts, causing a visible shift of enterprise move volumes toward specialized suppliers[2]Keiron Greenhalgh, “AI Helps Moving Companies Boost Efficiency, Cut Costs,” Transport Topics, ttnews.com. Outsourcing firms leverage global mobility software that interfaces with human resources and finance modules, delivering real-time spend visibility and enhancing the stakeholder experience. For providers, embedding within client ERP systems cements recurring revenue, while integrated tracking data improves resource planning. Secure data exchange bolsters compliance with privacy regulations and accelerates invoice cycles. Consequently, corporate deals are lengthening contract terms, lifting average revenue per account, and adding resilience to the moving services market.

E-Commerce-Fuelled Last-Mile Warehousing Shifts

Retailers remain under pressure to position inventory near consumers for next-day delivery commitments, which generates a constant need to relocate racking, sorting machinery, and inventory between micro-fulfillment sites. Specialized moves with strict timelines and high equipment value allow premium pricing that offsets lower residential margins. Cross-border sellers entering Southeast Asian markets are relocating goods to bonded warehouses, boosting demand for international freight corridors within the moving services market[3]Asian Development Bank, “Asian Economic Integration Report 2024,” adb.org. The trend also unlocks ancillary services—such as on-site installation of automation systems—that deepen provider margins. Scalable warehousing moves are poised to stay a key revenue vein across the forecast horizon.

SaaS-Based Dispatch and Virtual Survey Adoption

Cloud platforms enable dispatchers to optimize routing against real-time traffic and fuel prices, delivering fuel cost reductions up to 30% and cutting idle time. AI-driven virtual surveys via smartphone capture produce itemized inventories with 96% accuracy, lifting estimator productivity threefold while slashing survey costs[4]Yembo, “AI Surveys,” yembo.ai. Fast quotes boost conversion rates among digital-first consumers and reduce lead loss. Integration with CRM software automates follow-up, cross-selling, packing materials, and storage bundles. Collectively, these savings and revenue multipliers give technology-forward firms a tangible edge in the moving services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing-Affordability Squeeze | -0.8% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Fuel-Price Volatility | -0.6% | Global | Short term (≤ 2 years) |

| Tight Interstate Regulatory Scrutiny | -0.4% | North America, expanding globally | Long term (≥ 4 years) |

| Rising Fraud & Fake-Review Risk | -0.3% | Global, concentrated in digital markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Housing-Affordability Squeeze

Elevated mortgage rates and persistent listing shortages hinder household formation and delay discretionary moves, dampening residential volume in the moving services market. Consumers shift toward smaller intra-city relocations or remain in place longer, undercutting revenue from high-margin long-distance jobs. Scarcity of starter homes leads to multi-generation living arrangements that reduce move frequency. Although pent-up demand could eventually unleash a rebound, near-term pressure on household mobility limits growth.

Rising Fraud & Fake-Review Risk Hurting Trust

Online marketplaces are plagued by scams ranging from hostage loads to bait-and-switch quotes, and fake reviews distort supplier selection. Legitimate firms must invest in reputation-management software and verified-review platforms, escalating marketing costs. Prolonged decision cycles hamper booking velocity, imposing working-capital strain. Consumer skepticism also raises demand for binding estimates and escrow payments, complicating cash-flow management in the moving services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Full-Service Dominance Faces Partial-Service Disruption

Full-service relocation held 64.20% of the moving services market share in 2025, reflecting a strong appetite for turnkey solutions that include packing, loading, transport, and unpacking. Partial services, however, are forecast to post a 5.32% CAGR (2026-2031), signaling a cost-sensitive cohort ready to handle packing while outsourcing heavy lifting. Labor shortages underline the premium for full-service crews trained in specialty packing, sustaining higher average ticket sizes. Meanwhile, AI-powered packing guides and inventory apps reduce the knowledge barrier for do-it-yourself segments, nudging volumes toward hybrid offerings. Digitally generated labels and QR-coded cartons expedite loading sequences, driving productivity gains for both models.

Rising disposable income in emerging economies expands the addressable base for comprehensive packages, while inflation in mature markets presses consumers to mix professional and self-service elements. Providers deploying dynamic pricing linked to crew utilization can flexibly upsell packing or unpacking at booking. The moving services market size linked to partial-service offerings is set to widen as platform intermediaries automate contractor matching and secure payments. Full-service firms defend share by integrating insurance, fine-art crating, and white-glove add-ons that raise switching costs.

By End User Industry: Commercial Acceleration Challenges Residential Leadership

Residential relocations delivered 41.20% of the moving services market size in 2025 and remain the primary volume driver due to household mobility. Commercial relocations, in contrast, are projected to accelerate at a 5.18% CAGR (2026-2031), powered by office space optimization, mergers, and global hiring. Corporate accounts favor bundled packages with temporary storage and destination services, producing longer and more predictable revenue streams. Enterprise clients mandate service-level agreements that reward on-time performance and data transparency.

Hybrid work trends accelerate office downsizing, prompting phased equipment moves and record management relocations that diversify demand. Military and government contracts supply steady baseline volumes with heightened security and compliance requirements that command premiums. Commercial operators leverage specialized heavy-lift gear and after-hours scheduling to minimize client downtime, reinforcing value in the moving services market. Data-center growth further fuels specialized high-value equipment moves, opening niche opportunities for certified teams.

By Distance: International Growth Outpaces Domestic Volume

Domestic routes accounted for 90.70% of the moving services market share in 2025, sustained by the sheer frequency of intrastate and intraregional moves. International moves, though on a smaller scale, will grow at a 5.24% CAGR (2026-2031) amid expanding expatriate assignments and cross-border e-commerce inventory repositioning. Household goods carriers certified by the International Association of Movers and FIDI adhere to stringent quality controls that assure clients navigating customs and documentation complexity. Currency hedging and consolidated freight partnerships offset cost swings and protect margins.

Emerging trade corridors under the Regional Comprehensive Economic Partnership lower tariff obstacles, improving demand for regional relocations inside the Asia-Pacific. Door-to-door tracking via IoT sensors provides peace of mind for high-value shipments, raising willingness to pay. In contrast, mature domestic markets contend with commoditization and pricing pressure, pushing operators to expand outbound international services to sustain growth in the moving services market.

By Booking Channel: Digital Transformation Accelerates Despite Offline Dominance

Offline channels—phone, branch, and field consultations—captured 63.40% of the moving services market size in 2025, buoyed by trust derived from in-person assessments and complex move planning. Online platforms will expand at a 5.28% CAGR (2026-2031), propelled by high smartphone penetration and the convenience of virtual surveys. Real-time quote generation and transparent reviews attract digitally savvy segments. Operators integrating payment gateways shorten sales cycles and reduce administrative overhead.

Hybrid models that blend virtual surveys with optional on-site verification address edge cases such as antiques or oversized machinery. Unified APIs plug into lead-generation funnels, feeding live pricing into aggregator portals. Customer dashboards with milestone alerts and digital documentation elevate engagement and reduce service calls. As trust in digital signatures and remote verification solidifies, online bookings will increasingly dent traditional channels, reshaping customer acquisition in the moving services market.

Geography Analysis

North America led the moving services market with 32.70% revenue share in 2025, underpinned by resilient housing transactions, robust corporate relocation outsourcing, and a unified regulatory framework that facilitates interstate commerce. FMCSA regulations and established insurance norms cultivate consumer trust and enable operators to price premium interstate services securely. Migration toward affordable secondary metros extends average haul lengths, lifting revenue per move and strengthening operator earnings. The region also houses the highest adoption of SaaS dispatch and virtual survey tools, which amplifies operational efficiency.

Asia-Pacific is forecast to record the fastest growth at 5.62% CAGR through 2031, driven by rapid urbanization, infrastructure projects, and a digital economy racing from USD 300 billion in 2024 toward USD 1 trillion by 2030. Cross-border trade expansions create corridors that elevate international move demand. Large-scale industrial projects and foreign direct investment trigger relocation of expatriate staff, machinery, and high-tech equipment, which yields premium contracts for certified movers. Government incentives for smart warehousing and logistics hubs further elevate the addressable pool in the moving services market.

Europe maintains steady single-digit expansion, supported by the Schengen Area’s frictionless mobility and an increasing preference for carbon-neutral transport services. Operators adopting electric vehicle fleets and biofuel blends tap differentiated pricing with eco-conscious customers. Brexit induced a temporary surge of cross-Channel relocations, yet lingering regulatory divergence continues to compel supply-chain reconfigurations and household moves. Meanwhile, South America and Middle East & Africa provide nascent upside through infrastructure development and economic diversification, although fragmented regulations and road network constraints temper growth relative to other regions.

Competitive Landscape

The moving services market remains fragmented, with a structure that empowers regional specialists to compete by leveraging local know-how and personalized service. Technology adoption now serves as a principal differentiator. Operators integrating AI dispatch, virtual surveys, and customer portals report cost reductions up to 30% and conversion improvements. As a result, early adopters are accruing outsized gains in wallet share.

Strategic maneuvers include The Armstrong Company’s 2025 acquisition of Fry-Wagner’s Kansas City branch to deepen Midwestern coverage, and Atlas Van Lines’ April 2025 partnership with Move4U to embed CrewPro software across its fleet. Franchise expansion remains a viable playbook, illustrated by Two Men and a Truck adding 31 franchises in 2024. White-space niches such as fine-art handling and data-center equipment movement are attracting investment due to high margins and certification barriers.

Consolidation efforts face cultural hurdles because small proprietors value autonomy, yet vertical integration into warehousing and last-mile services is accelerating. Tech-first aggregators aim to standardize quality and pricing, but liability exposure and regulatory licensing requirements limit pure-play intermediary growth. FMCSA and International Association of Movers standards enforce compliance costs that favor scale economies, nudging the market toward gradual concentration without immediate drastic shifts.

Moving Services (Mover And Packers) Industry Leaders

Wheaton World Wide Moving

Armstrong Relocation and Companies

UniGroup Inc. (United & Mayflower)

AGS Worldwide Movers

Arpin Van Lines

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Armstrong Company announced the acquisition of Fry-Wagner Moving and Storage’s Kansas City operations, expanding its Midwestern footprint.

- April 2025: Atlas Van Lines partnered with Move4U to roll out the CrewPro software platform, marking a key milestone in its digital transformation journey.

- January 2025: Two Men and a Truck celebrated a record-breaking 2024 with 31 franchise openings, reinforcing network coverage across new metros.

- September 2024: PODS Enterprises extended its City Service program to Atlanta, Houston, Minneapolis, Montreal, and Tampa Bay, bringing coverage to 19 urban centers in North America.

Global Moving Services (Mover And Packers) Market Report Scope

Moving services encompass any assistance associated with relocating, transporting, arranging, physically moving, or storing household items. The moving services market is segmented by type, application, and geography. By type, the market is segmented into full-service moving and partial-service moving. By application, the market is segmented into commercial, residential, and other applications (military and government). By geography, the market is segmented into Asia-Pacific, North America, Europe, South America, Middle East & Africa, and the Rest of the World. The report offers the market sizing and forecasts for the moving services market in value (USD) for all the above segments.

| Full-service Relocation |

| Partial-services |

| Residential |

| Commercial |

| Military & Government |

| Domestic |

| International |

| Online (Digital Platforms) |

| Offline (Direct / Phone & Branch) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service Type | Full-service Relocation | |

| Partial-services | ||

| By End User Industry | Residential | |

| Commercial | ||

| Military & Government | ||

| By Distance | Domestic | |

| International | ||

| By Booking Channel | Online (Digital Platforms) | |

| Offline (Direct / Phone & Branch) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

How large is the moving services market in 2026?

It is valued at USD 116.71 billion in 2026 and is projected to reach USD 150.16 billion by 2031.

What is the forecast CAGR for moving services through 2031?

The market is forecast to grow at a 5.17% CAGR over 2026-2031.

Which region is growing fastest in moving services?

Asia-Pacific is set to expand at a 5.62% CAGR through 2031 due to urbanization and cross-border trade expansion.

What segment is leading by service type?

Full-service relocation commands 64.20% revenue share, but partial-services are growing faster at 5.32% CAGR.

How dominant are online booking channels in moving services?

Online channels hold 36.60% share in 2025 and are growing at a 5.28% CAGR, driven by virtual survey adoption.

Why is corporate relocation outsourcing increasing?

Firms convert fixed relocation costs into scalable services, gaining real-time visibility and better employee experience, which drives commercial move growth.

Page last updated on: