Military Vehicle Electrification Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 4.53 Billion |

| Market Size (2031) | USD 9.35 Billion |

| Growth Rate (2026 - 2031) | 15.59% CAGR |

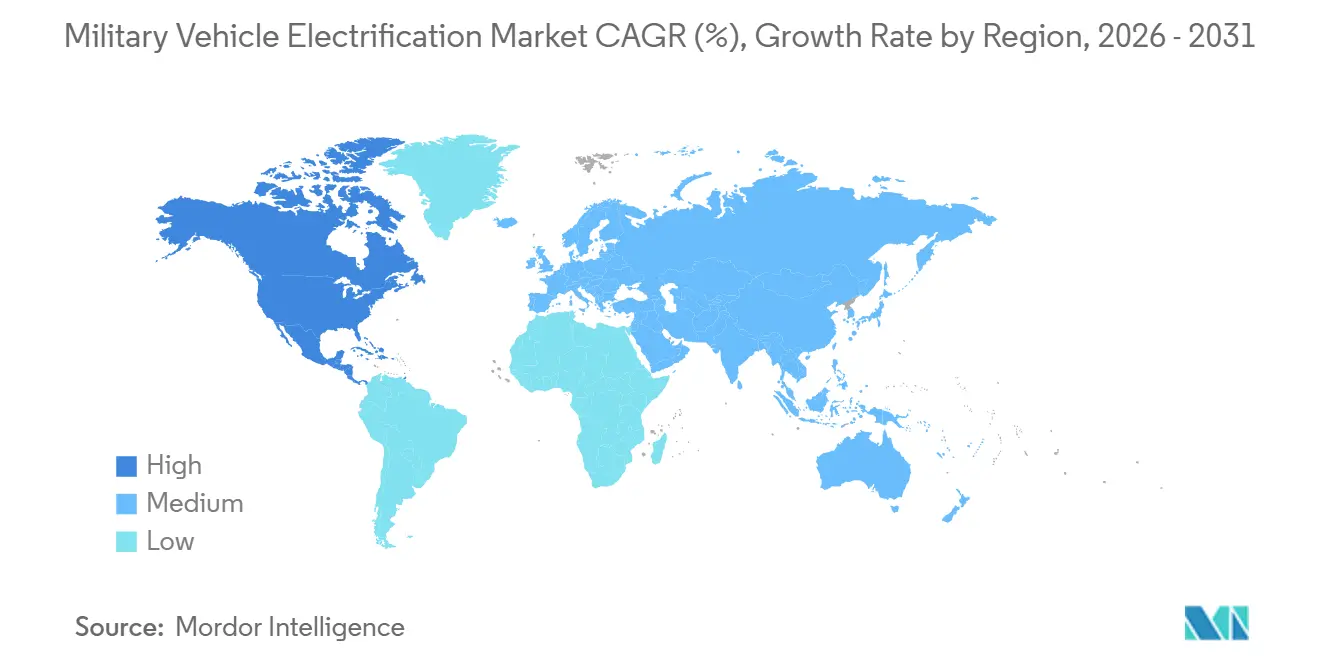

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Vehicle Electrification Market Analysis by Mordor Intelligence

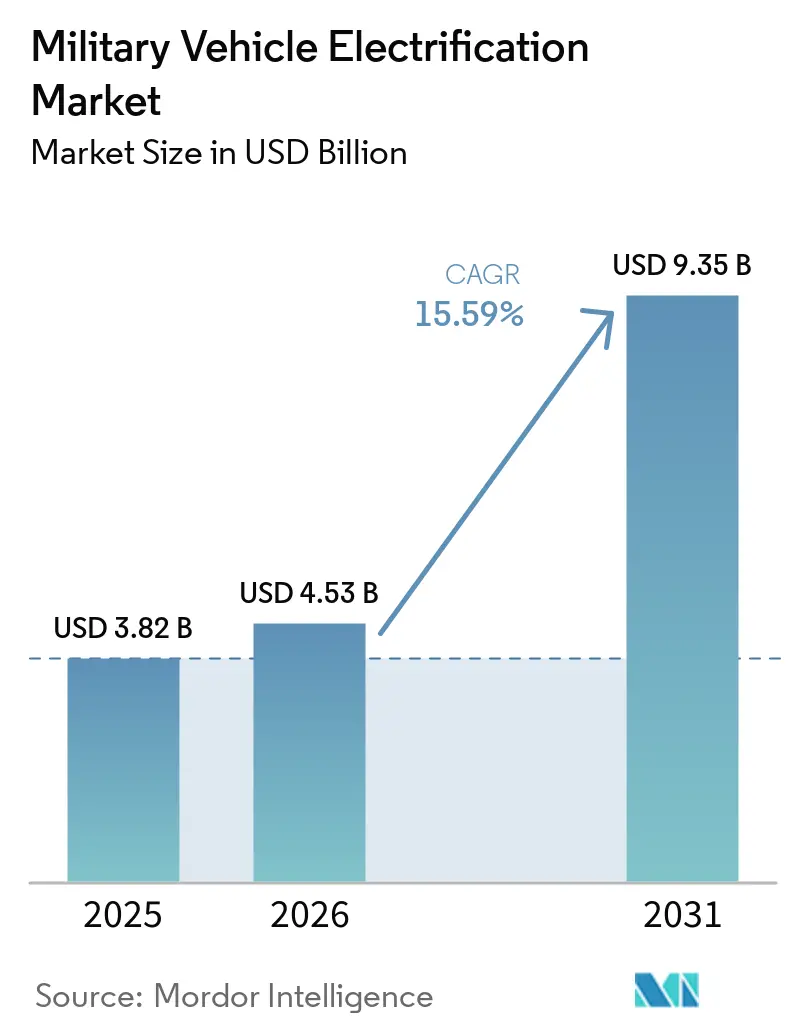

The military vehicle electrification market was valued at USD 3.82 billion in 2025, and is projected to grow from USD 4.53 billion in 2026 to reach USD 9.35 billion by 2031, at a 15.59% CAGR over 2026-2031. Intensive modernization budgets, tightening energy security mandates, and the tactical value of silent propulsion are driving the military vehicle electrification market toward mainstream deployment. Hybrid platforms give defense forces an immediate path to lower fuel logistics, while fast-maturing solid-state batteries shorten the time horizon for fully electric combat vehicles. Stealth mobility, exportable onboard power, and reduced maintenance downtime collectively strengthen commanders’ operational flexibility, resulting in a procurement environment that increasingly rewards suppliers able to integrate advanced energy storage, high-voltage power distribution, and robust thermal management. Consolidation among prime contractors underscores the strategic importance of vertical integration around battery technology and critical-mineral sourcing, signaling that supply-chain control is now a core differentiator in the military vehicle electrification market.

Key Report Takeaways

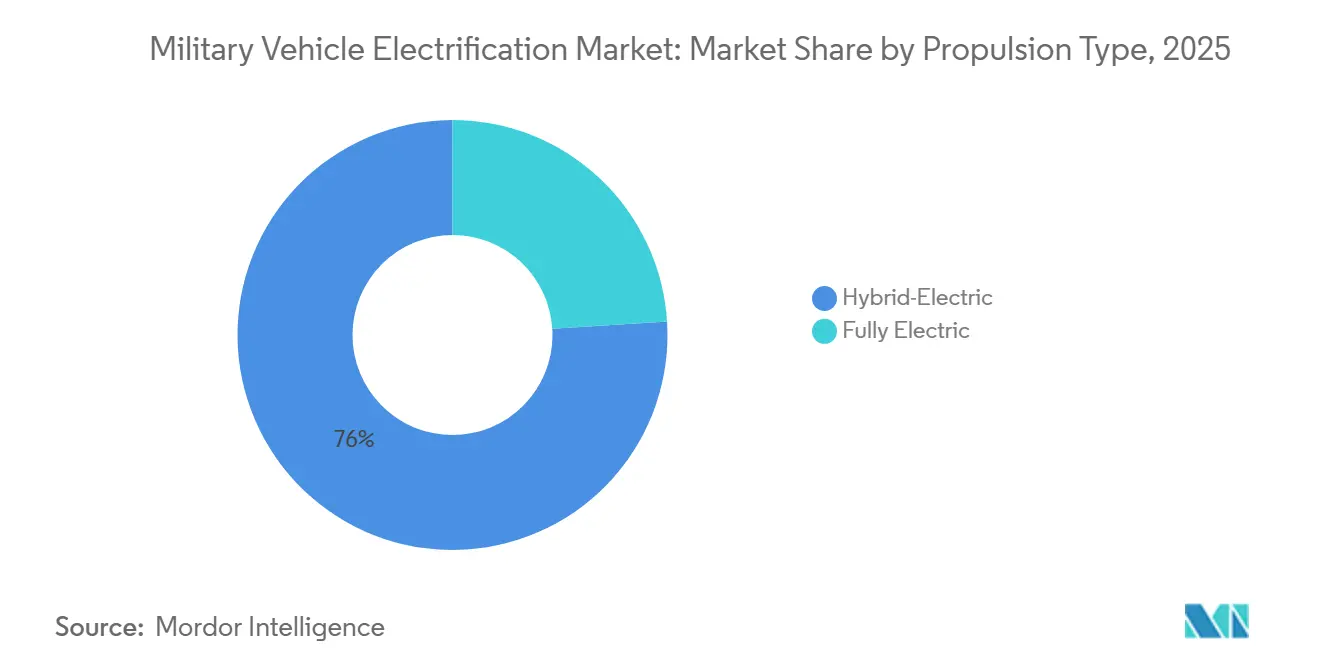

- By propulsion type, hybrid-electric systems led the military vehicle electrification market with a 76.00% revenue share in 2025, while fully electric platforms are forecast to grow at a 19.88% CAGR through 2031.

- By platform, combat vehicles commanded 48.97% of the military vehicle electrification market share in 2025; support vehicles are projected to expand at a 17.81% CAGR between 2026 and 2031.

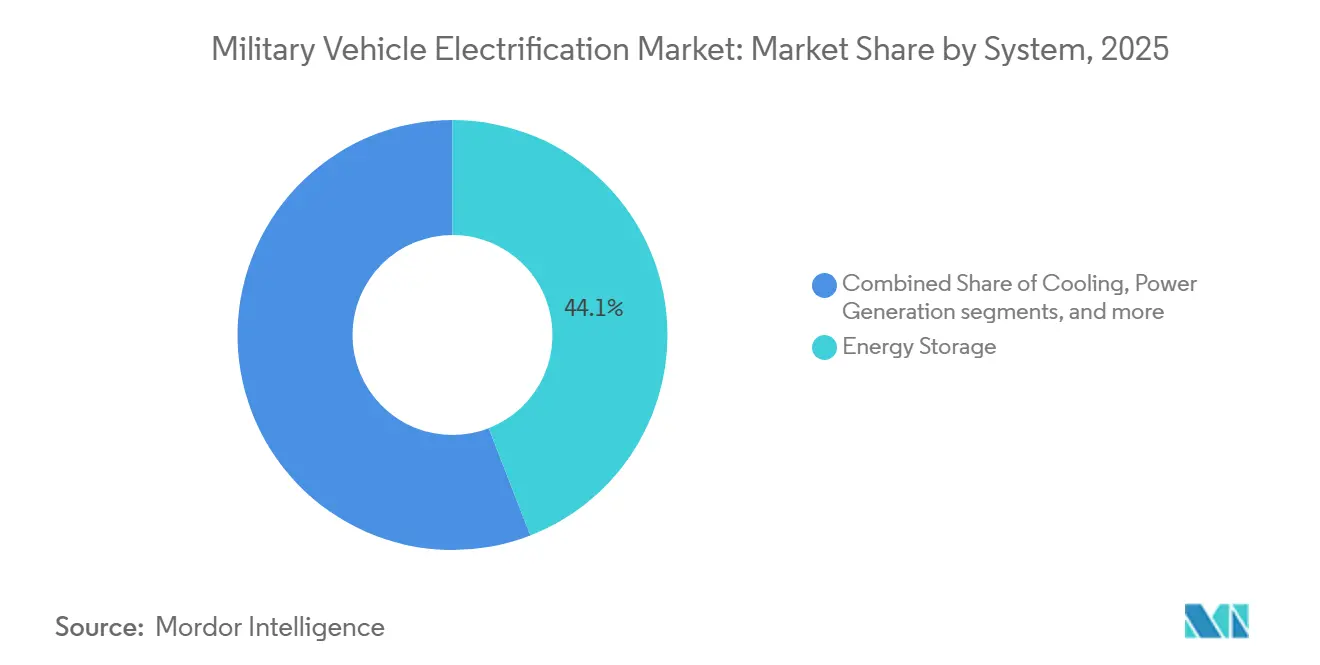

- By system, energy storage accounted for 44.10% of the market in 2025 and is forecast to grow at a 16.36% CAGR through 2031.

- By voltage class, medium-voltage architectures (50 V to 600 V) held 46.60% market share in 2025 and are projected to grow at a 17.02% CAGR through 2031.

- By geography, North America accounted for 51.62% in 2025 and is forecast to grow at a 16.30% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Military Vehicle Electrification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in high-energy-density lithium and solid-state batteries | +4.1% | Global | Medium term (2-4 years) |

| Rising onboard power requirements for directed-energy and C4ISR systems | +3.7% | Global | Medium term (2-4 years) |

| Increased defense funding for ground vehicle modernization programs | +3.2% | North America, Europe | Medium term (2-4 years) |

| Operational savings from reduced fuel logistics and supply chain dependencies | +2.8% | Global | Short term (≤ 2 years) |

| Tactical benefits of silent mobility for ISR and electronic warfare operations | +2.4% | Global | Short term (≤ 2 years) |

| Global emissions and fuel efficiency standards influencing defense fleets | +2.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Defense Funding for Ground Vehicle Modernization Programs

Accelerated appropriations are channeling unprecedented sums into electrification. The US Army’s climate strategy pursues an all-electric non-tactical fleet by 2027 and hybridized tactical platforms beginning with the M1E3 Abrams program, which integrates an advanced battery pack derived from GM Defense’s Ultium technology. In parallel, the European Union earmarked EUR 150 billion (USD 175.83 billion) within its ReArm Europe framework to seed next-generation powertrains, positioning electrification as a force multiplier for readiness.[1]European Commission, “Member States’ Defence Budgets,” europa.eu Such funding pools de-risk supplier investment in solid-state chemistry, cooling subsystems, and power electronics, accelerating the global adoption curve of the military vehicle electrification market.

Global Emissions and Fuel-Efficiency Standards Influencing Defense Fleets

Federal Executive Orders 14008 and 14057 require US government agencies to transition to zero-emission vehicles on aggressive timelines, a mandate that affects the Department of Defense’s (DoD's) vast tactical inventory. NATO members embed similar sustainability metrics into the 2% of GDP defense-spending guideline, compelling procurement offices to favor hybrid and electric variants. These policies codify stealth, reduced thermal signature, and lower maintenance overhead as co-benefits, reinforcing the long-run growth trajectory of the military vehicle electrification market.

Technological Advancements in High-Energy-Density Lithium and Solid-State Batteries

Breakthroughs regularly exceed 480 Wh/kg, as demonstrated by University of Texas at Dallas researchers who optimized space-charge layers under the DoD BEACONS initiative. Complementary work by US Army scientists produced a patent for a zinc-battery treatment that improves cycle life without compromising safety. With Amprius’ silicon-anode wearable packs doubling energy density for infantry applications, these advances sharply improve range and silent-watch duration, dissolving legacy barriers to widespread fielding of electric combat vehicles and propelling the military vehicle electrification market forward.

Operational Savings from Reduced Fuel Logistics and Supply-Chain Dependencies

Historically, fuel convoys expose up to 70% of the supply chain's vulnerability in expeditionary operations. The Secure Tactical Advanced Mobile Power (STAMP) program demonstrated a 25% fuel reduction by exporting 100 kW of vehicle-generated electricity to microgrids, thereby reducing reliance on generators and convoy frequency.[2]US Army, “STAMP: Advanced Power Distribution as a Force Multiplier,” army.mil Lower maintenance costs follow the elimination of complex transmissions, trimming lifecycle expenditures, and shortening acquisition payback periods. These quantifiable savings strengthen the business case for defense ministries weighing up-front electrification costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain vulnerabilities in critical minerals under defense procurement policies | -3.4% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Insufficient tactical charging and battlefield refueling infrastructure | -2.7% | Global | Medium term (2-4 years) |

| High initial costs for procurement and retrofitting of electric platforms | -2.3% | Global | Short term (≤ 2 years) |

| Thermal signature risks associated with large-capacity battery systems | -1.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Insufficient Tactical Charging and Battlefield Refueling Infrastructure

Pilot installations of Level-3 chargers on US bases underscore progress, yet expeditionary forces lack ruggedized, grid-independent solutions. DoD microgrid tests using solar-generator hybrids and modular lithium packs indicate feasibility, but large-scale deployment awaits MIL-spec certification and doctrinal integration. Until portable high-capacity chargers are ready, range anxiety will temper adoption rates in the military vehicle electrification market.

High Initial Costs for Procurement and Retrofitting of Electric Platforms

Advanced batteries, cooling loops, and power electronics raise acquisition costs above those of diesel equivalents. Budget planners often choose new-build hybrids over retrofits because legacy hulls require extensive driveline re-engineering. While lifecycle savings are material, the payback window can exceed five years, pressuring nations with constrained capital to defer large-scale commitments despite strategic interest in the military vehicle electrification industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Hybrid Leadership with Pure-Electric Momentum

Hybrid-electric systems generated 76.00% of 2025 revenue, leveraging regenerative braking, on-the-move power export, and compatibility with existing refueling doctrine. This portion of the military vehicle electrification market supports near-term fleet upgrades without demanding radical infrastructure overhaul. Though smaller today, fully electric platforms are posting an 19.88% CAGR and benefit from advances in cell chemistry that enable armored vehicles to travel mission-relevant distances on a single charge.

By Platform: Combat Vehicle Dominance, Support Vehicles Acceleration

Combat platforms accounted for 48.97% of 2025 demand, propelled by marquee programs such as the M1E3 Abrams and the Boxer hybridization effort. The requirement for exportable electrical power to new sensor suites and laser countermeasures aligns naturally with electrified drivelines, keeping combat vehicles central to growth in the military vehicle electrification market.

Support and logistics vehicles are the fastest-growing segment, with a 17.81% CAGR through 2031, as they increasingly integrate modular battery pods and auxiliary inverters, creating rolling microgrids capable of powering field hospitals and radar stations. This secondary demand stream further diversifies revenue opportunities and cushions suppliers against the cyclicality of big-ticket combat vehicle awards.

By System: Energy Storage as the Anchor of Electrification

Energy storage subsystems captured 44.10% of the market in 2025 and are projected to grow further with a CAGR of 16.36% through 2031, as defense forces prioritize extended silent watch and reduced reliance on generators. Growth rests on improvements in cell safety, intelligent battery-management software, and solid-state commercialization timelines. Power generation and conversion units follow closely; the Army’s STAMP architecture, capable of exporting 100 kW, exemplifies how vehicles now serve as mobile power hubs, displacing standalone diesel generators.

Thermal management and transmission components are also evolving. Meggitt Defense Systems has delivered over 2,400 advanced cooling units designed for high-voltage applications, demonstrating supplier readiness to meet the next wave of heat-rejection challenges within the military vehicle electrification market.[3]Meggitt Defense Systems, “Thermal Systems,” meggitt.com

By Voltage Class: Medium-Voltage Prevalence with High-Voltage Upswing

Medium-voltage systems, which held a 46.60% share in 2025, are projected to expand at a CAGR of 17.02% from 2026 to 2031. This growth is attributed to their backward compatibility with 28V accessories and manageable insulation requirements. In contrast, high-voltage systems (those exceeding 600V) are making strides, offering fast charging and facilitating directed-energy integration. High-voltage systems are poised for healthy growth, buoyed by the swift commercialization of wide-bandgap semiconductors and ruggedized DC/DC converters.

Geography Analysis

North America, which accounted for 51.62% of 2025 revenue, is projected to grow at a 16.30% CAGR through 2031. This growth trajectory mirrors the DoD's investments, spanning from battery standardization to supply-chain onshoring. Notable programs like the Next-Generation Tactical Vehicle-Hybrid and the hybridized Abrams underscore the confidence in scalable electrification. Furthermore, Canada's modernization initiatives, prioritizing cold-weather and silent mobility, highlight how regional climate factors influence specifications in the military vehicle electrification arena.

In South Korea, Japan, and Australia, large-scale modernization efforts are fueling growth in the Asia-Pacific region, with each nation pursuing energy independence and aiming to minimize logistics footprints. Demonstrating its commitment, the region has showcased government-funded trials of hydrogen-powered armored vehicles and high-voltage support trucks. Such initiatives are set to diversify the technological landscape of the military vehicle electrification sector.

Europe's trajectory is guided by funding for the Common Security and Defence Policy and by tightened sustainability mandates. The EUR 1.7 billion (USD 1.99 billion) integration of Iveco Defence into Leonardo cements Italy's position as a European land-systems powerhouse and accelerates the continent's closed-loop supply of electrified drivetrains. Interoperability requirements under NATO rail-carriage dimensions and cross-country mobility standards further harmonize demand across member states, elevating the collective bargaining power of the European defense bloc within the military vehicle electrification market.

Competitive Landscape

Consolidation continues as prime contractors secure battery expertise and critical-mineral access. Leonardo’s acquisition of Iveco Defense positions the combined entity to provide end-to-end hybrid and electric solutions across NATO fleets, from chassis to battery logistics, highlighting vertical integration advantages in the military vehicle electrification market. Rheinmetall’s purchase of Loc Performance Products strengthens its US industrial base. It complements partnerships with General Dynamics Land Systems to co-develop the XM30 hybrid infantry fighting vehicle, ensuring that drivetrain and power-management IP remain under one corporate roof.[4]Rheinmetall AG, “Rheinmetall Completes Strategic Acquisition of Loc Performance Products,” rheinmetall.com

QinetiQ and Texelis are advancing in-wheel hub motors that simplify powertrain layouts and free cabin volume for mission systems. At the same time, GM Defense collaborates with Middle Eastern partners to localize the production of hybrid tactical trucks, underscoring the strategic value of regional manufacturing for export-controlled components. Battery-technology innovators such as Amprius and SandboxAQ are courting defense contracts with promises of double the energy density and AI-driven predictive-maintenance platforms, injecting competitive pressure on legacy suppliers to upgrade their chemistry roadmaps. The clustering of prime contractors around battery intellectual property and thermal-management know-how suggests that the military vehicle electrification market is coalescing into an oligopoly of integrated system houses.

Military Vehicle Electrification Industry Leaders

BAE Systems plc

Oshkosh Corporation

General Dynamics Corporation

Rheinmetall AG

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Rheinmetall AG signed an agreement to acquire a majority stake in DOK-ING, strengthening its capabilities in unmanned and autonomous ground systems, including electrified and robotic vehicle technologies.

- March 2026: Rolls-Royce Power Systems and ZF were awarded a contract by Germany’s BAAINBw to develop the world’s first parallel-hybrid drive for heavy tracked vehicles (MGCS), delivering >1,400 kW system output to support rising electrical loads.

- February 2026: ST Engineering unveiled the Terrex S5 HED eight-wheeled armored vehicle at the Singapore Airshow. This variant, with a gross weight of 35 tons and a payload capacity of 13 tons, features a hybrid-electric drive system.

Global Military Vehicle Electrification Market Report Scope

Defense vehicles are increasingly adopting electric systems and propulsion technologies, replacing or supplementing their traditional mechanical and hydraulic counterparts. Military vehicle electrification integrates electric power technologies into ground vehicles to enhance performance, efficiency, survivability, and energy management.

The military vehicle electrification market is segmented by propulsion type, platform, system, voltage class, and geography. By propulsion type, the market is segmented into hybrid-electric and fully electric. By platform, the market is segmented into combat vehicles, support vehicles, and unmanned ground vehicles. By system, the market is segmented into power generation, cooling, energy storage, traction drive, power conversion, and transmission. By voltage class, the market is segmented into low, medium, and high. The report also covers the market sizes and forecasts for the military vehicle electrification market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Hybrid-Electric |

| Fully Electric |

| Combat Vehicles |

| Support Vehicles |

| Unmanned Ground Vehicles (UGVs) |

| Power Generation |

| Cooling |

| Energy Storage |

| Traction Drive |

| Power Conversion |

| Transmission |

| Low (Less than 50 V) |

| Medium (50 V to 600 V) |

| High (Greater than 600 V) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Propulsion Type | Hybrid-Electric | ||

| Fully Electric | |||

| By Platform | Combat Vehicles | ||

| Support Vehicles | |||

| Unmanned Ground Vehicles (UGVs) | |||

| By System | Power Generation | ||

| Cooling | |||

| Energy Storage | |||

| Traction Drive | |||

| Power Conversion | |||

| Transmission | |||

| By Voltage Class | Low (Less than 50 V) | ||

| Medium (50 V to 600 V) | |||

| High (Greater than 600 V) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the military vehicle electrification market in 2031?

The military vehicle electrification market indicate USD 9.35 billion by 2031, reflecting a 15.59% CAGR from 2026.

Which propulsion type currently leads defense adoption?

Hybrid-electric systems held 76.00% of 2025 revenue due to immediate fuel-saving and silent-mobility benefits.

Why are high-voltage architectures gaining popularity?

Directed-energy weapons and advanced C4ISR suites require more than 600V power pulses that only high-voltage systems can deliver efficiently.

Which region is growing fastest in vehicle electrification?

North America is set to log a 16.30% CAGR through 2031 on the back of major modernization programs.

How do electric combat vehicles affect logistics costs?

Programs such as STAMP have demonstrated 25% fuel-logistics savings by replacing generator trailers with vehicle-exported power.

What challenges restrict rapid adoption?

Inadequate tactical charging, high upfront costs and critical-mineral supply vulnerability remain primary headwinds to broader fielding.

Page last updated on: