Military Radars Market Size

Market Overview

| Study Period | 2019 - 2030 |

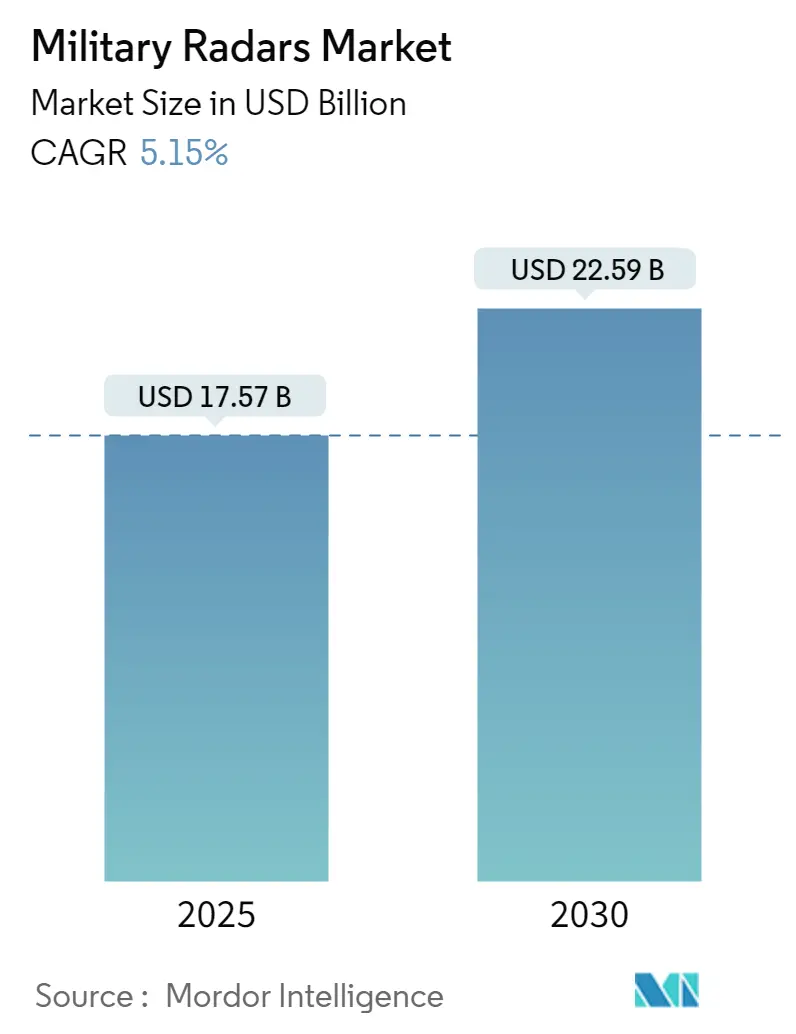

| Market Size (2025) | USD 17.57 Billion |

| Market Size (2030) | USD 22.59 Billion |

| Growth Rate (2025 - 2030) | 5.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Military Radars Market Analysis

The Military Radars Market size is estimated at USD 17.57 billion in 2025, and is expected to reach USD 22.59 billion by 2030, at a CAGR of 5.15% during the forecast period (2025-2030).

The military radar industry continues to evolve amid escalating global security challenges and technological advancements. The nature of warfare has fundamentally transformed with the emergence of more lethal, agile, and untraceable threats with autonomous capabilities, compelling nations to enhance their military radar systems as the first line of defense. Major defense exporters like the United States, Russia, and Israel are increasingly focusing on the Asia-Pacific region as a high-growth area, driven by growing territorial disputes and the need for enhanced surveillance systems. The U.S. Department of Defense's 2024 budget allocation includes significant investments in radar technology, with over USD 147 million dedicated to sea-based X-band radar systems and USD 133.5 million for anti-radar missile improvements.

Technological innovation is reshaping the radar landscape, with artificial intelligence and machine learning integration becoming paramount for enhanced threat detection and analysis. The industry is witnessing a significant shift toward Active Electronically Scanned Array (AESA) radar systems, offering superior performance and reliability compared to traditional mechanical scanning radars. In 2023, several breakthrough developments emerged, including Israel Aerospace Industries' completion of installing advanced MF-STAR (Magen Adir) radar systems on new Sa'ar 6 corvette warships, featuring four staring radar panels that provide 360-degree hemispherical coverage around vessels.

Strategic partnerships and industry consolidation are becoming increasingly prevalent as companies seek to strengthen their technological capabilities and market presence. In July 2023, Hensoldt partnered with Israel Aerospace Industries to deliver advanced radar systems worth approximately EUR 200 million to the German military, demonstrating the growing trend of cross-border collaboration in radar technology development. These partnerships are particularly focused on developing multi-mission radar systems capable of detecting and tracking various threats, from conventional aircraft to hypersonic missiles and small drones.

The emergence of new threats, particularly in the domain of unmanned aerial systems and hypersonic weapons, is driving innovation in radar technology. Modern radar systems are being developed with enhanced capabilities to detect and track small unmanned aerial vehicles (UAVs) while effectively screening radar clutters. In a significant development in 2023, the Defense Advanced Research Projects Agency (DARPA) announced plans to develop a prototype line of cost-effective reconnaissance satellites with advanced radar capabilities as part of the "Blackjack" program, aiming to integrate reconnaissance and communications payloads into standard commercial satellites to accelerate constellation formation.

Military Radars Market Trends

Growing Defense Expenditure and Military Modernization Programs

The substantial increase in global defense spending has become a primary driver for the military radars market, with worldwide military expenditure reaching USD 2,440 billion in 2023, representing a significant 9% growth from 2022. This unprecedented level of defense spending has enabled countries to invest heavily in modernizing their military capabilities, particularly in advanced military radar systems. Major defense powers are launching comprehensive modernization programs to replace aging radar systems with more sophisticated variants. For instance, in October 2023, the US Air Force announced plans to construct homeland-defense radars specifically designed to detect next-generation Russian cruise missiles, demonstrating the direct correlation between increased defense budgets and radar system procurement.

The modernization initiatives are further exemplified by multinational collaboration programs focused on developing advanced military capabilities. A prime example is the agreement between France, Germany, and Spain to proceed with the next phase of the Future Combat Air System program, with project costs exceeding USD 103.4 billion. Similarly, the United Kingdom's partnership with Japan and Italy to develop next-generation stealth fighters under the future combat air program highlights how increased defense spending is driving innovation in military radar technologies. These collaborative efforts are creating sustained demand for advanced radar systems that can support modern warfare requirements, including enhanced detection capabilities and improved target tracking precision.

Rising Demand for Enhanced Surveillance and Reconnaissance Capabilities

The increasing emphasis on intelligence, surveillance, and reconnaissance (ISR) capabilities has emerged as a crucial driver for the airborne radar market, particularly in the context of evolving security threats and territorial disputes. Military forces worldwide are investing in sophisticated radar systems to enhance their situational awareness and early warning capabilities. This trend is evidenced by recent procurement decisions, such as India's contract with Israel Aerospace Industries Ltd in November 2023 for six additional Hermes 900 unmanned drones, specifically aimed at strengthening surveillance capabilities. The integration of advanced radar systems in these platforms demonstrates the growing importance of comprehensive surveillance capabilities in modern military operations.

The demand for enhanced surveillance capabilities is further reinforced by the development of multi-mission radar systems that can perform various surveillance tasks simultaneously. Military organizations are increasingly seeking radar systems that can provide comprehensive coverage across different operational domains—air, land, and sea. This is exemplified by RTX's development of the Lower Tier Air and Missile Defense Sensor system, which successfully demonstrated its capability to intercept cruise missiles in November 2023. The system's ability to neutralize threats from all directions while maintaining continuous surveillance represents the evolution of radar technology in response to complex security requirements. This trend is driving innovation in radar system design, particularly in areas such as electronic scanning capabilities and advanced signal processing.

Technological Advancements in Radar Systems

The continuous evolution of radar technology has become a significant market driver, with developments in areas such as electronic scanning radars, synthetic aperture radar, and solid-state radars creating new opportunities for military applications. Modern military radar systems are incorporating advanced features such as automated target recognition, improved signal processing, and enhanced detection capabilities. These technological improvements are particularly evident in the development of quantum radars, which use subatomic particles instead of traditional radio waves, making them highly effective against stealth technology and conventional radar-jamming tactics. The integration of artificial intelligence and machine learning algorithms in radar systems is further enhancing their capabilities in target identification and threat assessment.

The push for more sophisticated radar technologies is also driven by the need to counter emerging threats such as hypersonic weapons and stealth aircraft. Military forces are investing in radar systems that can provide faster scanning speeds, higher resolution, and improved target discrimination capabilities. This is exemplified by the development of multi-function radar systems that can simultaneously perform air surveillance, fire control, and missile guidance functions. The trend toward automation in radar systems has led to significant reductions in operator workload, with some systems achieving up to a 50% reduction in manual operations, allowing operators to focus more on mission-critical tasks rather than system operation. These technological advancements are creating a new generation of radar systems that offer superior performance and operational efficiency, contributing to the growth of the air and missile defense radar market and the naval radar market.

Segment Analysis: Platform

Ground-based Segment in Military Radars Market

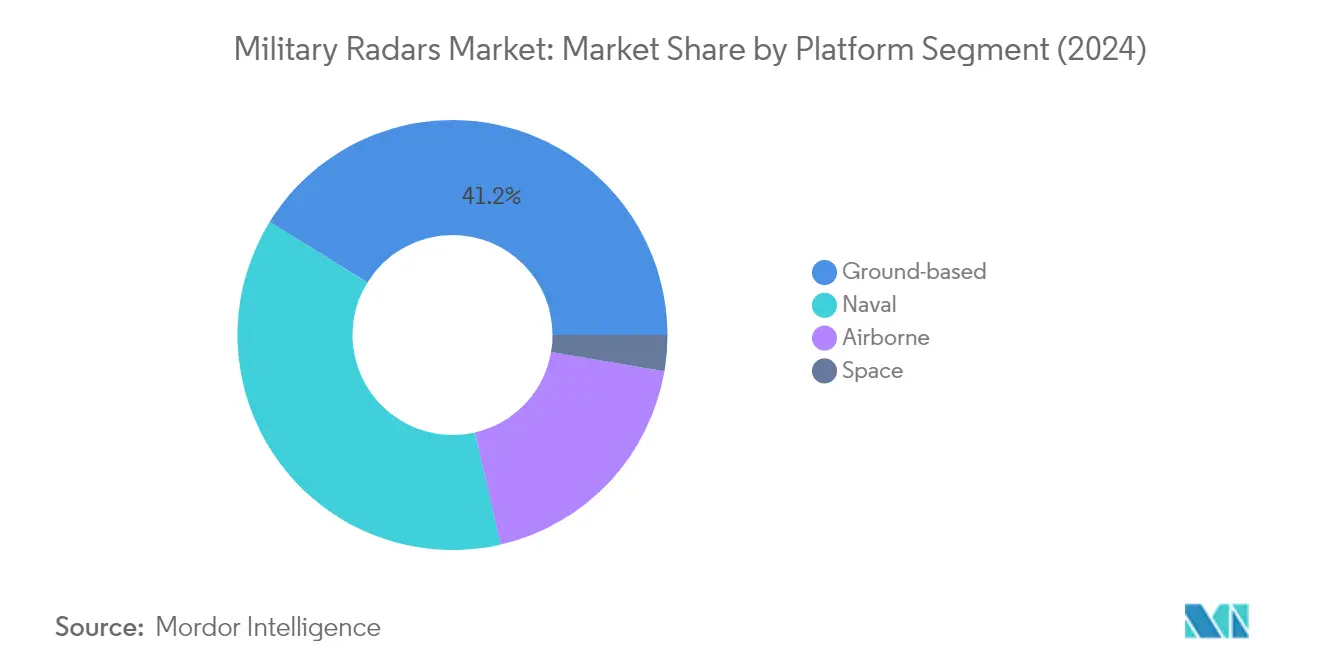

The ground-based segment dominates the military radar systems market, accounting for approximately 41% of the total market share in 2024. Ground-based military radar systems serve multiple critical functions, including ground surveillance, missile control, fire control, air traffic control (ATC), moving target indication (MTI), weapons location, and vehicle search capabilities. Modern ground-based radar systems offer enhanced mobility, with many being transportable by personnel and vehicles. Ground-penetrating radars mounted on military vehicles are particularly valuable for detecting improvised explosive devices (IEDs). The versatility and effectiveness of these systems have led to their widespread adoption by global military forces, resulting in sustained demand and numerous procurement contracts.

Airborne Segment in Military Radars Market

The airborne radars market is projected to witness the highest growth rate of approximately 6% during the forecast period 2024-2029. This growth is driven by increasing investments in airborne surveillance capabilities and the rising demand for advanced fighter aircraft equipped with sophisticated radar systems. The segment's expansion is further supported by the growing adoption of unmanned aerial vehicles (UAVs) for reconnaissance missions and the integration of advanced radar technologies like synthetic aperture radar (SAR) and active electronically scanned array (AESA) systems. Military forces worldwide are increasingly recognizing the strategic importance of airborne radar systems in modern warfare scenarios, particularly for intelligence, surveillance, and reconnaissance (ISR) operations.

Remaining Segments in Platform Segmentation

The naval and space segments complete the military radar systems market platform segmentation. Naval radars play a crucial role in maritime security, offering capabilities for surface surveillance, threat detection, and target identification at sea. These systems are essential for modern naval vessels, providing enhanced situational awareness and supporting weapon engagement through automatic tracking and fire control solutions. The space segment, while smaller in market share, represents an emerging frontier in military radar technology, particularly in the domain of space situational awareness and satellite-based surveillance systems. Both segments contribute significantly to the overall military radar ecosystem, offering unique capabilities for their respective operational environments.

Segment Analysis: Application

Air and Missile Defense Segment in Military Radars Market

The air defense radar market continues to dominate the military radars market, accounting for approximately 41% of the total market share in 2024. This significant market position is driven by the increasing focus on integrated air defense systems and the growing need to counter evolving aerial threats, including ballistic missiles, cruise missiles, and unmanned aerial vehicles. The segment's prominence is further reinforced by major defense modernization programs across various nations, particularly in regions like North America, Europe, and Asia-Pacific. Modern air defense radar systems now incorporate advanced technologies like active electronically scanned arrays (AESA), gallium nitride (GaN) components, and enhanced digital signal processing capabilities, enabling better detection and tracking of multiple threats simultaneously. The deployment of sophisticated multi-mission radar systems that can perform both surveillance and fire control functions has also contributed to this segment's market leadership.

Space Situational Awareness Segment in Military Radars Market

The Space Situational Awareness (SSA) segment is emerging as the fastest-growing segment in the military radars market, with a projected growth rate of approximately 6% during 2024-2029. This accelerated growth is primarily driven by increasing concerns about space debris, growing satellite constellations, and the need to protect space-based assets from potential threats. The segment is witnessing substantial technological advancements in radar systems designed specifically for tracking objects in low Earth orbit (LEO) and beyond. Military organizations worldwide are investing heavily in ground-based radar systems capable of detecting, tracking, and characterizing space objects with enhanced precision. The integration of artificial intelligence and machine learning capabilities in these radar systems is further augmenting their ability to identify and classify space objects, contributing to the segment's rapid growth trajectory.

Remaining Segments in Military Radars Market Application

The Intelligence, Surveillance, and Reconnaissance (ISR), Navigation and Weapon Guidance, and Other Applications segments continue to play vital roles in shaping the military radars market. The ISR segment maintains its strong position through the deployment of advanced surveillance radars in maritime patrol aircraft, airborne early warning systems, and ground-based reconnaissance platforms. Navigation and Weapon Guidance applications are crucial for modern precision-guided munitions and tactical weapons systems, incorporating sophisticated radar guidance technologies. The Other Applications segment encompasses specialized uses such as counter-drone systems, weather monitoring, and battlefield surveillance, contributing to the overall market diversity and technological advancement in military radar applications.

Military Radars Market Geography Segment Analysis

Military Radars Market in North America

North America represents a dominant force in the military radars market, driven by substantial defense budgets and continuous technological advancements. The United States and Canada are the key contributors to the regional market, with both countries focusing on modernizing their radar capabilities across air, naval, and ground-based platforms. The region's market is characterized by significant investments in research and development of advanced radar technologies, including AESA radars and multi-function radar systems. The presence of major defense contractors and ongoing military modernization programs further strengthens North America's position in the global radar market.

Military Radars Market in United States

The United States maintains its position as the largest market for military radars in North America, accounting for approximately 89% of the regional market share in 2024. The country's dominance is supported by its extensive military infrastructure and comprehensive defense modernization initiatives. The US military continues to invest heavily in advanced radar systems for various applications, including air and missile defense, surveillance, and reconnaissance. The country's robust defense industrial base, featuring major contractors like Raytheon, Lockheed Martin, and Northrop Grumman, contributes significantly to radar technology development and production capabilities.

Military Radars Market Growth Dynamics in United States

The United States is projected to maintain the highest growth rate in North America, with an expected CAGR of approximately 5% during 2024-2029. This growth is driven by ongoing military modernization programs and an increasing focus on developing next-generation radar systems. The US military's emphasis on maintaining technological superiority through advanced radar capabilities, particularly in areas like space surveillance and hypersonic missile detection, continues to drive market expansion. The country's investment in research and development of innovative radar technologies, including quantum radar systems and AI-integrated solutions, further supports this growth trajectory.

Military Radars Market in Europe

Europe represents a significant market for military radars, characterized by diverse requirements and capabilities across different countries. The region's market is driven by increasing defense cooperation among European nations and ongoing modernization efforts of military forces. Key countries including Russia, the United Kingdom, France, and Germany are actively investing in advanced radar technologies and systems. The European market is particularly focused on developing indigenous radar capabilities while maintaining strategic partnerships for technology sharing and joint development programs.

Military Radars Market in Russia

Russia emerges as the largest market for military radars in Europe, commanding approximately 23% of the regional market share in 2024. The country's strong position is underpinned by its extensive military modernization programs and indigenous radar development capabilities. Russia continues to invest in advanced radar systems for various applications, including air defense, maritime surveillance, and space monitoring. The country's focus on developing sophisticated radar technologies, particularly in counter-stealth and long-range detection capabilities, reinforces its market leadership.

Military Radars Market Growth Dynamics in France

France demonstrates the highest growth potential in the European market, with an anticipated CAGR of approximately 6% from 2024-2029. The country's growth is driven by its commitment to military modernization and an increasing focus on developing advanced radar capabilities. France's strategic investments in naval radar systems, airborne early warning capabilities, and ground-based air defense radars contribute to this growth trajectory. The country's strong aerospace and defense industrial base, coupled with active participation in European defense cooperation initiatives, supports sustained market expansion.

Military Radars Market in Asia-Pacific

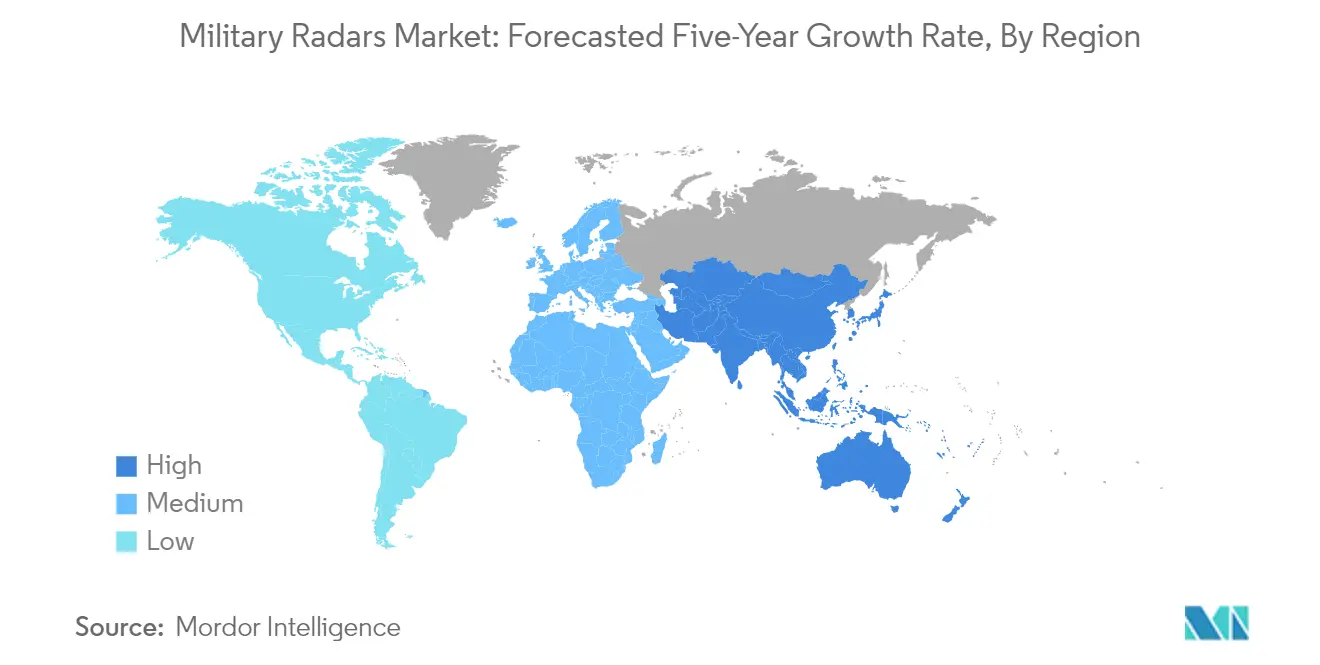

The Asia-Pacific region represents a rapidly evolving market for military radars, driven by increasing defense modernization initiatives and growing regional security concerns. Countries like China, India, Japan, and South Korea are making significant investments in enhancing their radar capabilities across all domains. The region is characterized by a mix of indigenous development programs and strategic partnerships with international defense contractors. The increasing focus on maritime security and air defense capabilities is driving the demand for advanced radar systems throughout the region.

Military Radars Market in China

China maintains its position as the dominant force in the Asia-Pacific military radars market. The country's leadership is supported by its extensive military modernization programs and growing indigenous capabilities in radar technology development. China's focus on developing advanced radar systems spans across airborne, naval, and ground-based applications, with particular emphasis on long-range surveillance and air defense systems. The country's investments in research and development of new radar technologies, including quantum radar systems and AI-integrated solutions, further strengthen its market position.

Military Radars Market Growth Dynamics in India

India emerges as the fastest-growing market for military radars in the Asia-Pacific region. The country's growth is driven by its ambitious military modernization programs and an increasing focus on indigenous radar development capabilities. India's strategic partnerships with international defense contractors, coupled with its growing domestic defense industrial base, contribute to market expansion. The country's emphasis on enhancing its surveillance and reconnaissance capabilities, particularly in response to regional security challenges, continues to drive investments in advanced radar systems.

Military Radars Market in Latin America

The Latin American military radars market is characterized by modernization efforts and an increasing focus on border surveillance capabilities. Brazil emerges as both the largest and fastest-growing market in the region, leading regional procurement and development initiatives. The region's market is driven by requirements for maritime surveillance, air defense, and border monitoring systems. Countries in the region are increasingly focusing on acquiring modern radar systems to enhance their territorial surveillance capabilities and modernize their armed forces.

Military Radars Market in Middle East & Africa

The Middle East & Africa region demonstrates significant potential in the military radars market, driven by ongoing regional security concerns and military modernization programs. Saudi Arabia emerges as the largest market, while the United Arab Emirates shows the fastest growth potential. The region's market is characterized by substantial investments in air defense systems and border surveillance capabilities. Countries in the region are actively pursuing acquisitions of advanced radar systems to enhance their defense capabilities and maintain regional security.

Military Radars Industry Overview

Top Companies in Military Radars Market

The military radar market features prominent players like Lockheed Martin, Northrop Grumman, IAI, Leonardo, SAAB, Raytheon Technologies, and Thales Group leading technological innovation and market development. Companies are heavily investing in next-generation radar technologies, including 3D radar systems, dual-band capabilities, and advanced materials like gallium nitride for improved performance. Operational agility is demonstrated through the vertical integration of manufacturing operations and the development of in-house expertise in critical component technologies. Strategic partnerships with stealth materials manufacturers and designing OEMs are becoming crucial for technological breakthroughs. Market leaders are expanding their global footprint through the establishment of a local presence, industrial partnerships, and a focus on emerging markets, particularly in the Asia-Pacific and Middle East regions.

Fragmented Market with Strong Regional Players

The military radars market exhibits a highly fragmented structure with numerous local and international players providing various radar systems and services. While global defense conglomerates dominate the high-end military radar segment through their extensive R&D capabilities and established relationships with defense forces, regional specialists maintain significant market share in their respective territories through a deep understanding of local requirements and strong government relationships. The market features a mix of state-owned enterprises and private companies, with some players focusing exclusively on radar technologies while others operate as part of larger defense and aerospace conglomerates.

Market consolidation is primarily driven by technology acquisition and regional market access, with companies actively pursuing strategic acquisitions to strengthen their technological capabilities and expand their geographical presence. The industry witnesses significant collaboration between prime contractors and subcontractors, with many players operating in both roles depending on the project scope and requirements. Joint ventures and technology partnerships are common, particularly for developing next-generation radar systems that require diverse expertise and substantial investment.

Innovation and Adaptability Drive Market Success

Success in the military radars market increasingly depends on companies' ability to innovate in areas like stealth detection, hypersonic tracking capabilities, and quantum radar technologies. Incumbents are focusing on modernizing their existing infrastructure, investing in research and development of newer generation radar systems, and developing cost-effective solutions to maintain their market position. Companies are also emphasizing the development of multi-mission capabilities, automated systems, and the integration of artificial intelligence to address evolving military requirements and maintain a competitive advantage.

For contenders looking to gain market share, key success factors include developing specialized expertise in emerging technologies, forming strategic partnerships with established players, and focusing on niche applications or regional markets. The high concentration of end-users in government and defense sectors necessitates building strong relationships with defense procurement agencies and understanding complex regulatory requirements. While substitution risk remains low due to the unique capabilities of radar systems, companies must continuously innovate to address emerging threats and maintain technological superiority. Regulatory compliance, particularly regarding export controls and defense procurement policies, continues to shape market dynamics and influence company strategies.

Military Radars Market Leaders

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Leonardo S.p.A.

-

RTX Corporation

-

Israel Aerospace Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Military Radars Market News

March 2024: South Korea’s DAPA announced that it plans to invest USD 2.9 billion to enhance the radar systems and long-range mission capabilities of its F-15K Eagle fleet. Under the program, the aircraft is expected to be equipped with the AN/APG-82 electronic scanning radar, BAE Systems' AN/ALQ-250 Eagle Passive Active Warning Survivability System, and a new large-area display in the cockpit to enhance situational awareness.

December 2023: The Royal Malaysia Air Force (RMAF) awarded THALES a contract to deliver the new GM400α long-range radar. The GM400α allows Malaysia’s armed forces to detect all types of threats early for decision-making and action.

Military Radars Industry Segmentation

Armed forces use military radars for surveillance, locating targets, tracking their movements, and directing other weapons or countermeasures against them. Military radars are also used for navigation and tracking weather changes. The study includes radars used by the navy (coastal radars and ship-based radars), air force (weather navigation radar, airborne radar, and precision approach radar), and army (perimeter surveillance radars, long-range surveillance radars, and fixed and movable land radars), as well as in space applications. The other applications include IED detection, airspace monitoring, traffic management, and weather monitoring.

The military radar systems market is segmented by platform, application, components, and geography. By platform, it is segmented into ground-based, naval, airborne, and space. By application, the market is classified into air and missile defense, intelligence, surveillance, and reconnaissance (ISR), navigation and weapon guidance, space situational awareness, and other applications. Based on components, the market is segmented into antennas, transmitters, receivers, power amplifiers, duplexers, digital signal processors, stabilization systems, and graphical user interfaces. The report also covers the market sizes and forecasts for the military radar systems market in major countries across different regions. For each segment, the market size and forecast are provided in terms of value (USD).

| Platform | Ground-based | ||

| Naval | |||

| Airborne | |||

| Space | |||

| Application | Air and Missile Defense | ||

| Intelligence, Surveillance, and Reconnaissance (ISR) | |||

| Navigation and Weapon Guidance | |||

| Space Situational Awareness | |||

| Other Applications | |||

| Component | Antennas | ||

| Transmitters | |||

| Receivers | |||

| Power Amplifiers | |||

| Duplexers | |||

| Digital Signal Processors | |||

| Stabilization Systems | |||

| Graphical User Interfaces | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Rest of Latin America | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Egypt | |||

| Rest of Middle East and Africa | |||

| Ground-based |

| Naval |

| Airborne |

| Space |

| Air and Missile Defense |

| Intelligence, Surveillance, and Reconnaissance (ISR) |

| Navigation and Weapon Guidance |

| Space Situational Awareness |

| Other Applications |

| Antennas |

| Transmitters |

| Receivers |

| Power Amplifiers |

| Duplexers |

| Digital Signal Processors |

| Stabilization Systems |

| Graphical User Interfaces |

| North America | United States |

| Canada | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Rest of Latin America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| Rest of Middle East and Africa |

Military Radar Market Research FAQs

How big is the Military Radars Market?

The Military Radars Market size is expected to reach USD 17.57 billion in 2025 and grow at a CAGR of 5.15% to reach USD 22.59 billion by 2030.

What is the current Military Radars Market size?

In 2025, the Military Radars Market size is expected to reach USD 17.57 billion.

Who are the key players in Military Radars Market?

Lockheed Martin Corporation, Northrop Grumman Corporation, Leonardo S.p.A., RTX Corporation and Israel Aerospace Industries Ltd. are the major companies operating in the Military Radars Market.

Which is the fastest growing region in Military Radars Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Military Radars Market?

In 2025, the North America accounts for the largest market share in Military Radars Market.

What years does this Military Radars Market cover, and what was the market size in 2024?

In 2024, the Military Radars Market size was estimated at USD 16.67 billion. The report covers the Military Radars Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Military Radars Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: June 16, 2024