Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 117.83 Billion |

| Market Size (2031) | USD 164.56 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

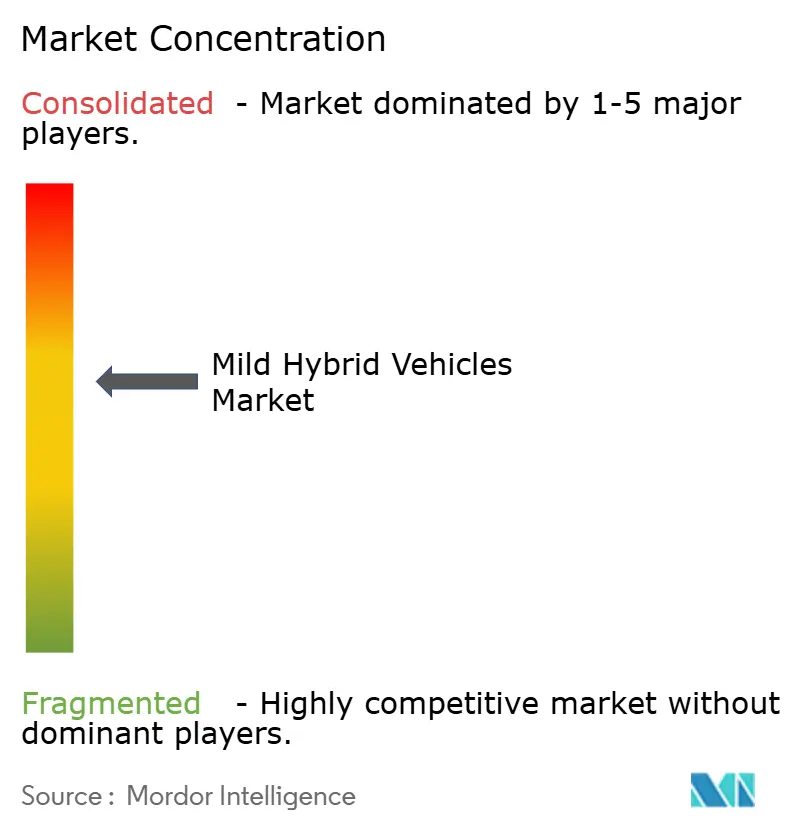

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mild Hybrid Vehicles Market Analysis by Mordor Intelligence

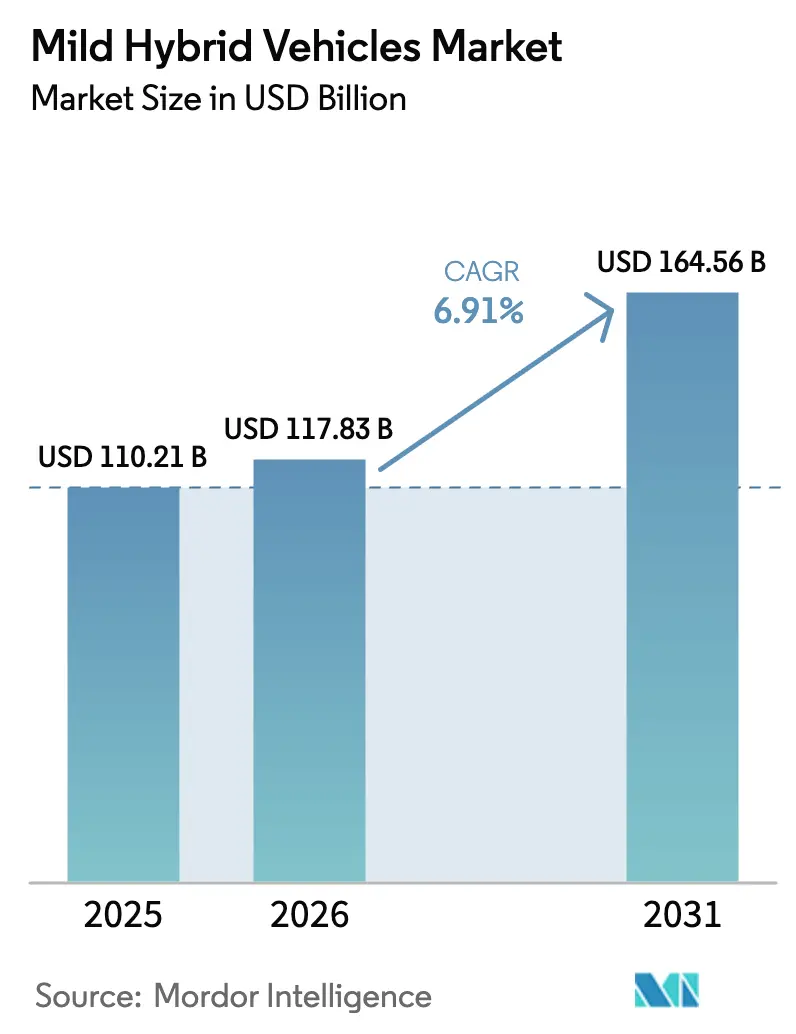

The mild hybrid vehicles market size is projected to grow from USD 110.21 billion in 2025 to USD 117.83 billion in 2026 and is forecast to reach USD 164.56 billion by 2031, growing at a CAGR of 6.91% during the forecast period (2026-2031). The near-term outlook is shaped by diesel phase-out mandates in Europe, lithium-ion price deflation, and a regulatory tilt that rewards 48V compliance solutions at a fraction of the cost of plug-in hybrid capital costs. Automakers are deploying mild hybrids to bridge tightening CO₂ rules without committing to the still-volatile economics of full battery-electric vehicles. Tier-one suppliers are redesigning powertrains around the LV148 electrical standard, aiming to monetize over-the-air features that lift lifetime revenue per vehicle. Meanwhile, the commercialization of sodium-ion batteries is lowering 48V pack costs for cost-sensitive light vans and entry-level cars, broadening the addressable market in India, Brazil, and Southeast Asia.

Key Report Takeaways

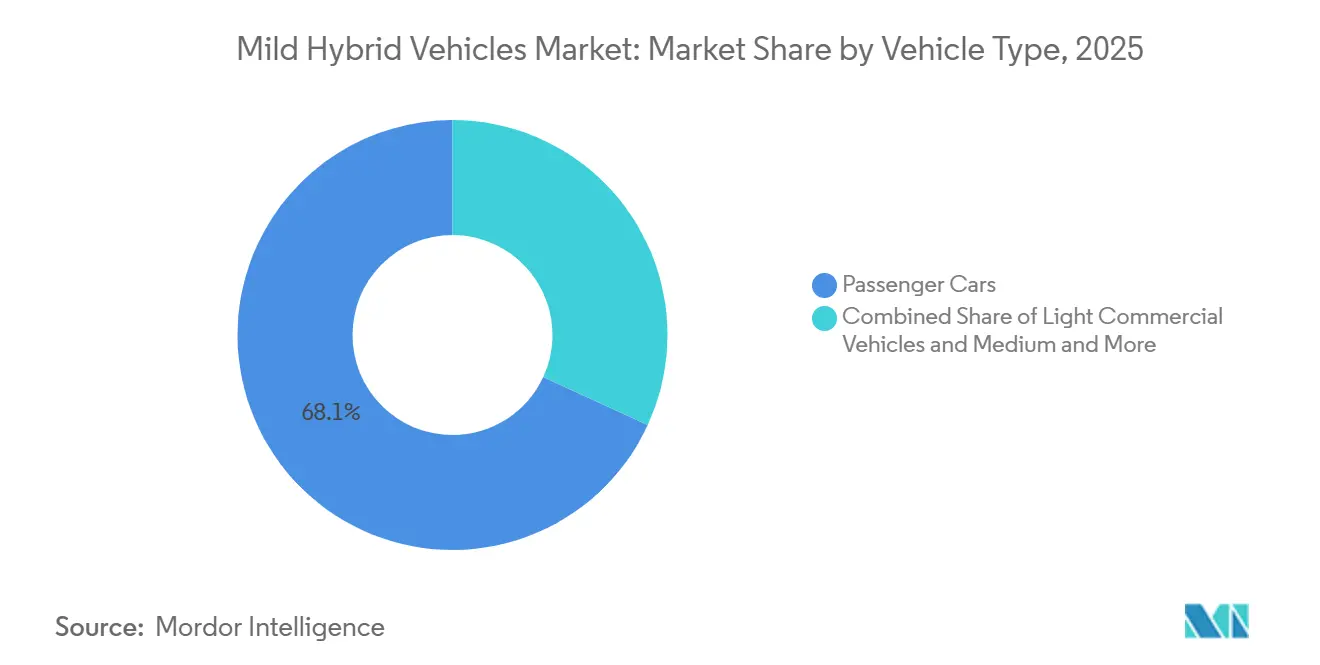

- By vehicle type, passenger cars led with 68.12% of the mild hybrid vehicles market share in 2025, while light commercial vehicles are forecast to post the fastest 8.17% CAGR through 2031.

- By hybrid system segment, the 48V architecture commanded 73.88% of the mild hybrid vehicles market share in 2025 and is projected to expand at an 8.91% CAGR between 2026 and 2031.

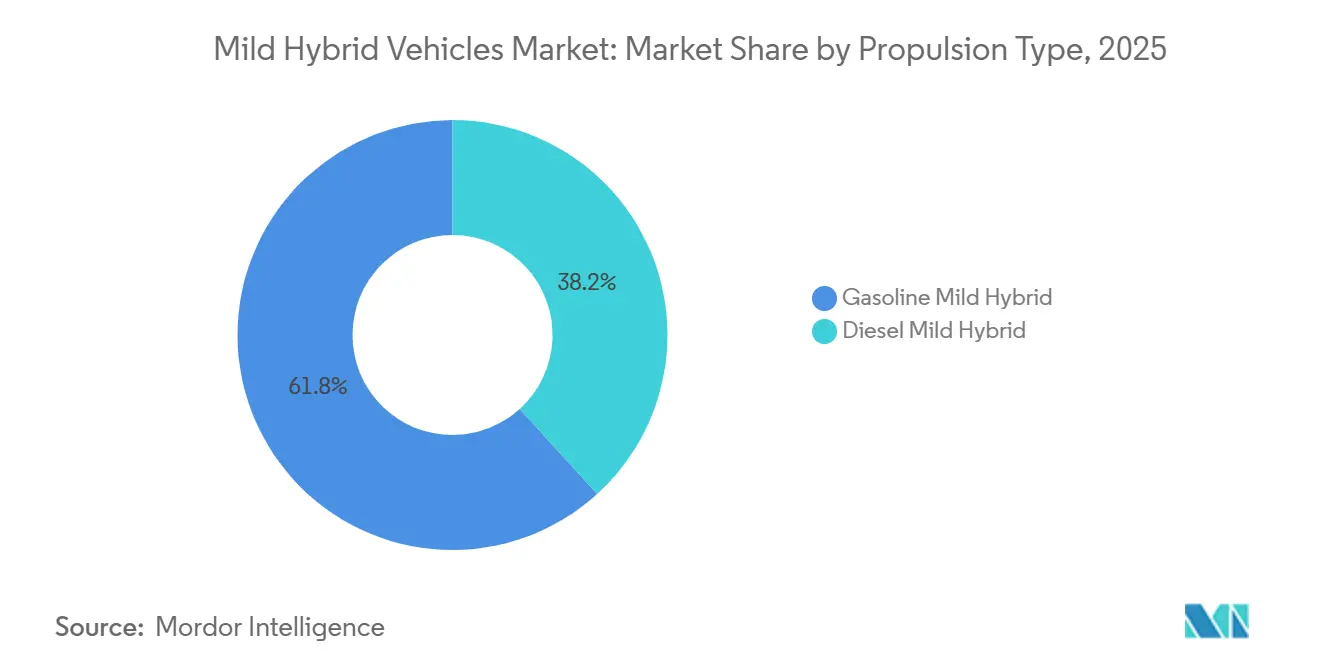

- By propulsion, gasoline mild hybrids accounted for 61.76% of the mild hybrid vehicles market share in 2025, whereas diesel mild hybrids are expected to register the highest 8.13% CAGR to 2031.

- By battery chemistry, lithium-ion held 82.22% of the mild hybrid vehicles market share in 2025, yet sodium-ion and other emerging chemistries are set to advance at a 7.16% CAGR over 2026-2031.

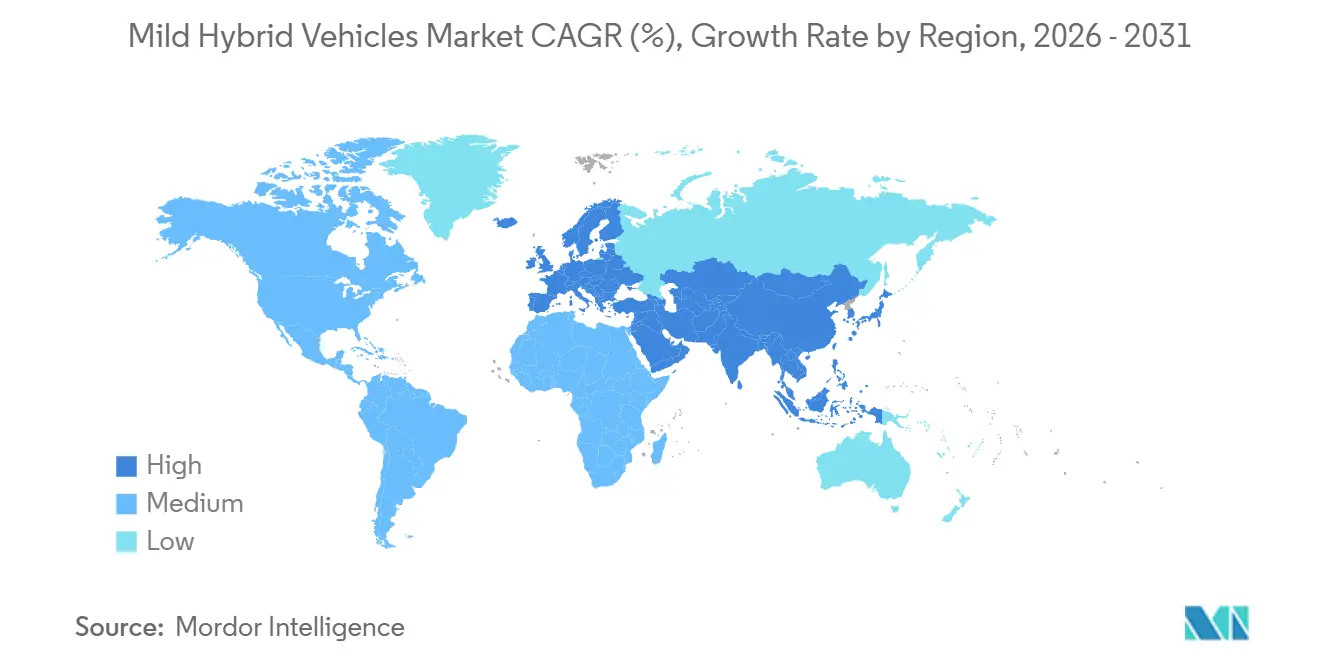

- By geography, Europe captured 48.74% of the mild hybrid vehicles market share in 2025, but Asia-Pacific is projected to be the fastest-growing region at an 8.11% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mild Hybrid Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global CO₂ and Fuel-Economy Mandates | +2.3% | Global, with peak enforcement in EU, India, China (NEV credit tightening) | Medium term (2-4 years) |

| Low-Cost 48V Architecture Drives Electrification | +1.8% | Global, strongest in Europe and China | Short term (≤2 years) |

| Falling Lithium-Ion Prices and Sodium-Ion Growth | +1.1% | Global, with China leading; CATL Naxtra 175 Wh/kg mass production Q2 2026 | Medium term (2-4 years) |

| Europe's Diesel Phase-Out Boosts OEM Rollouts | +0.9% | Europe, with spill-over to Turkey and North Africa | Short term (≤2 years) |

| Fleet Demand for Fuel-Efficient Vans | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| OTA Software Upgrades Unlock 48V Revenues | +0.2% | Global, with China leading, regulatory push | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Tightening Global CO₂ / Fuel-Economy Mandates

European fleet targets for emissions, supported by penalties for non-compliance, have positioned 48V mild hybrids as the most cost-effective compliance solution [1]“CO₂ Emission Performance Standards for Cars and Vans,” European Commission, europa.eu. These hybrids remain relevant even with the bloc's updated goals, which allow internal combustion engines to run on synthetic fuels. In India, updated regulations introduce super-credits that continue to support mild hybrids. Similarly, changes in China's plug-in rules are redirecting budgets toward 48V solutions, which benefit from reduced luxury tax bands and government incentives. The alignment of these regulatory changes is accelerating OEM decision-making processes. As a result, mild hybrids are shifting from a niche market to a mainstream option, particularly for manufacturers unable to scale battery electric vehicles competitively.

Low-Cost 48V Architecture Enabling Mass Electrification

Automakers are recognizing the advantages of a belt-starter-generator, which slightly increases build costs but significantly reduces fuel consumption, offering a quick return on investment for high-volume models. With Mercedes-Benz, BMW, and Volkswagen adopting the LV148 interface, manufacturers can now pool parts across platforms. This additional electrical capacity enables advancements such as electric turbocharging, active suspension, and steer-by-wire features. Bosch has commenced large-scale production of 48V modules in China, and industry projections indicate widespread adoption [2]“48-Volt Battery Production Milestone,” Bosch, bosch-press.com. As a result, the 48V system is becoming the preferred electrification option for cost-sensitive segments.

Declining Lithium-Ion Prices and Sodium-Ion Emergence

Global pack prices have declined and are expected to decrease further. In comparison, Chinese cells are already priced lower. CATL's sodium-ion production line has entered mass production, significantly reducing the cost of 48V batteries for light vans. Similarly, BYD is expanding its sodium-ion capacity. The use of cobalt-free chemistries and reduced material volatility strengthens supply security while improving the competitiveness of mild hybrids in emerging markets.

Diesel Phase-Out in Europe Accelerating OEM Rollouts

While diesel sales in Europe have significantly declined as a share of new-car purchases, this shift hasn't directly driven a substantial increase in battery electric vehicle (BEV) adoption. Instead, hybrids have gained a dominant share, reflecting consumer preference for diesel-gasoline combinations that alleviate concerns about range anxiety. In response, automakers like Stellantis, Audi, and BMW are improving their engines with advanced assist systems. This approach helps them comply with particle standards while avoiding the high costs associated with selective-catalytic systems. Consequently, they are extending the lifespan of their platforms and managing capital expenditures effectively.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Costs Decline, Eroding Hybrid Price Edge | -1.4% | Global, most acute in China, Western OEMs 25-40% cost disadvantage vs Chinese producers | Short term (≤2 years) |

| 48V Components Face Thermal and EMC Limits | -0.5% | Global, particularly Europe and North America | Medium term (2-4 years) |

| Tariff Fluctuations Disrupt Supply Chain | -0.4% | North America (IRA USD 7,500 consumer + USD 45/kWh production credit), EU (70% local-content proposals), impact on Asian-sourced components | Short term (≤2 years) |

| Uneven Hybrid Incentives in Emerging Markets | -0.3% | Brazil, ASEAN , India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling BEV Costs Compress Mild-Hybrid Price Advantage

Lithium-ion pack prices have declined significantly, with Chinese cell manufacturers already quoting lower costs. This trend is reducing the historical cost gap between battery-electric vehicles (BEVs) and 48V mild hybrid powertrains. Tesla and BYD have adjusted the entry-level prices of their BEVs in China to match those of comparable internal-combustion sedans. Ford has also indicated plans to introduce an affordable midsize crossover on its new platform. As the total cost of ownership for BEVs continues to decrease, consumers are comparing the fuel savings offered by mild hybrids with the zero-emission benefits and potentially higher resale values of BEVs, particularly in regulated areas. European OEMs have expressed concerns that a rapid decline in BEV prices could undermine their recent investments in 48V systems, significantly reducing the payback period. As a result, the mild hybrid vehicle market is experiencing margin pressures, especially in areas where charging infrastructure is improving, and government incentives increasingly favor full electrification.

Inconsistent Hybrid Incentives in Emerging Markets

In Brazil, Thailand, and Indonesia, policy frameworks swing between supporting battery-electric and hybrid technologies. This inconsistency poses planning risks for OEMs eyeing growth outside OECD economies. In Brazil, São Paulo's IPVA exemption applies only to hybrids produced in the state, leaving out imported mild-hybrid crossovers, which are gaining popularity in showrooms. Meanwhile, Thailand's Board of Investment has reduced excise relief for low-voltage hybrids, redirecting incentives towards fully electric models. Indonesia, on the other hand, continues to provide a luxury-tax discount for 48V systems, but revisits this rate regularly. In India, while FAME II subsidies are available for mild hybrid passenger cars, draft FAME III guidelines suggest a phase-out in the near future. Such frequent regulatory shifts not only muddle volume forecasting but also deter suppliers from investing in local content, thereby capping the potential growth of the mild hybrid vehicle market in these rapidly developing regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Dominance, Fleet Van Upside

Passenger cars accounted for 68.12% of the mild hybrid vehicles market share in 2025, as OEMs deployed 48V systems across high-volume sedans and SUVs. Light commercial vans, though smaller in absolute numbers, are forecast to expand at an 8.17% CAGR to 2031, adding incremental volume to the mild hybrid vehicle market via fleet contracts that favor quick refueling over depot charging. Dual-shift courier routes in Europe and North America illustrate why 48V vans deliver lower total cost than BEVs under present infrastructure constraints.

LCV momentum is strongest where pay-per-kilometer economics dominate procurement. Sodium-ion packs further close the cost gap, especially in India and Southeast Asia, where fuel subsidies narrow diesel economics. Medium and heavy trucks remain a niche because 48V limits peak power; those duty cycles are migrating toward hydrogen fuel cells and 800-volt traction systems.

By Hybrid System: 48V Architecture Consolidates Leadership

The 48V topology captured 73.88% of the mild hybrid vehicles market share in 2025 and is on track for an 8.91% CAGR through 2031, widening its leadership as 12V start-stop systems plateau. OEM migrations are catalyzed by the LV148 bus, which standardizes component interfaces and slashes integration time. A single P0 module yields 10-17% fuel savings at roughly 30% of full-hybrid cost, an attractive ratio for mass-market platforms.

Full-hybrid architectures remain relevant for CO₂ super-credits, yet their premium limits penetration outside Japan and select EU segments. Conversely, 24V solutions find footholds in low-speed off-highway machinery but contribute marginally to global volume. The 48V pathway is therefore expected to dominate the new mild-hybrid vehicle market share throughout the decade.

By Propulsion Type: Diesel Hybrids Regain European Momentum

Gasoline mild hybrids accounted for 61.76% of the mild hybrid vehicles market share in 2025, reflecting gasoline’s prevalence in China, India, and the United States. Yet diesel mild hybrids are predicted to record an 8.13% CAGR as European OEMs retrofit 1.6- to 3.0-liter diesels with 48V recovery and torque assist to meet Euro 7 NOx caps without heavy after-treatment.

Outside Europe, the diesel's share is minor, but the technology offers export potential to North Africa and Turkey, where diesel refueling infrastructure remains entrenched. Gasoline will nonetheless continue to dominate the mild hybrid vehicle market, as large emerging regions lack diesel passenger-car demand.

By Battery Chemistry: Lithium-Ion Dominant, Sodium-Ion Rising

Lithium-ion secured 82.22% of the mild hybrid vehicles market share in 2025 and will remain the workhorse chemistry, supported by ongoing declines in cathode costs. However, sodium-ion and other lithium-free cells are forecast to grow at a 7.16% CAGR as Chinese mass production eliminates cobalt and nickel, slashing 48V pack costs for entry-level cars and light vans.

Nickel-metal hydride remains in legacy Toyota systems but is fading quickly as energy density lags behind LFP and sodium-ion alternatives. As these affordable chemistries scale, emerging markets can accelerate penetration without the raw-material volatility linked to lithium and cobalt supply chains.

Geography Analysis

Europe captured 48.74% of 2025 volume, buoyed by stringent 93.6 g CO₂/km fleet rules and diesel-replacement demand. Germany, France, Italy, and Spain collectively generate more than two-thirds of regional registrations. Diesel-mild-hybrid variants—such as Audi’s 3.0-liter V6 and Stellantis’ upcoming 1.6-liter unit—help automakers meet Euro 7 particle metrics while avoiding selective-catalytic after-treatment complexity. Eastern European uptake lags due to lower fuel prices and slower infrastructure rollout, whereas the United Kingdom’s aggressive zero-emission mandate is compressing the local mild hybrid window[3]"Stellantis Extends Benchmark Hybrid Powertrain", Stellantis, stellantis.com.

Asia-Pacific is the fastest-growing cluster, with an 8.11% CAGR through 2031. China steers the region with PHEV credit tightening that now favors 48V packages able to slip under luxury-tax thresholds. India’s CAFE-III super-credits keep mild hybrids eligible for FAME II subsidies, and Indonesia, Thailand, and Vietnam deploy hybrid-targeted excise rebates. While Japanese manufacturers focus on full hybrids for their domestic market, they export 48V systems to budget-conscious ASEAN neighbors, highlighting the regulatory differences within the region.

North America is set to grow at a steady pace, with moderate expansion projected. In the United States, hybrid vehicle adoption has increased significantly, driven by some consumers turning back to hybrids due to charging challenges. Stellantis and Ford are updating their truck and SUV lineups, integrating belt-starter-generators as a buffer against potential BEV affordability challenges. Meanwhile, South America's automotive landscape is largely influenced by regional tax incentives. For instance, São Paulo's IPVA waiver currently gives OEMs that assemble hybrids locally an edge.

Competitive Landscape

The largest suppliers—Bosch, Continental, Valeo, ZF, and BorgWarner—dominate the mild-hybrid market, controlling a significant share of 48V revenue. While Western incumbents are restructuring to fund electrification, ZF has announced substantial layoffs and is considering spinning off its powertrain division. Continental is preparing for an Automotive IPO while reducing R&D spending as a percentage of turnover. In contrast, Asian companies are expanding aggressively. Valeo is making significant investments to increase its sales in India, targeting Mahindra’s e-axle orders. CATL and BYD are integrating sodium-ion packs to capture light commercial vehicle programs, and Huawei is promoting its DriveONE 48V drive to domestic OEMs. The competitive landscape is shifting toward companies that combine power electronics with software-driven features and maintain agile cost structures.

Key technology priorities include hairpin-wound motors for improved torque density, dual-side-cooled 48V inverters that meet the highest functional safety standards, and rare-earth-free stators to reduce dependency on magnet supplies. Increasing compliance costs related to functional safety and cybersecurity regulations are extending design timelines. This trend is driving co-development contracts between OEMs and suppliers, securing long-term business commitments.

Mild Hybrid Vehicles Industry Leaders

-

Nissan Motor Co. Ltd

-

Volkswagen AG

-

Hyundai Motor Company

-

Ford Motor Company

-

Toyota Motor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Stellantis Brazil has unveiled the next phase of its Bio-Hybrid program. The company confirmed that it will launch its inaugural flex mild-hybrid vehicle in the first half of the year. This vehicle, developed and produced at the Goiana Automotive Hub in Pernambuco, Brazil, boasts advanced 48V MHEV technology. Notably, the new model integrates a multifunctional electric machine that replaces both the alternator and starter motor. This innovative machine not only provides extra torque to the internal combustion engine but also generates energy to recharge a 48V lithium-ion battery, seamlessly working in tandem with the traditional electrical system.

- January 2026: Toyota UK unveiled the 2026 Land Cruiser Commercial, now featuring a new diesel 48V powertrain. The revamped Land Cruiser Commercial boasts a 2.8-litre turbodiesel engine, paired with an eight-speed Direct Shift automatic transmission and enhanced by a 48V mild-hybrid system.

Global Mild Hybrid Vehicles Market Report Scope

The mild hybrid vehicles market report is segmented by vehicle type (passenger cars, light commercial vehicles, medium and heavy commercial vehicles), hybrid system (12V, 24V, 48V), propulsion type (gasoline, diesel), battery type (lithium-ion, nickel-metal hydride, others including sodium-ion and LTO), and geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD) and volume (units).

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

By Hybrid System

| 12V Mild Hybrid System |

| 24V Mild Hybrid System |

| 48V Mild Hybrid System |

By Propulsion Type

| Gasoline Mild Hybrid |

| Diesel Mild Hybrid |

By Battery Type

| Lithium-Ion |

| Nickel-Metal Hydride (NiMH) |

| Others (e.g., Sodium-ion, LTO) |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| By Hybrid System | 12V Mild Hybrid System | |

| 24V Mild Hybrid System | ||

| 48V Mild Hybrid System | ||

| By Propulsion Type | Gasoline Mild Hybrid | |

| Diesel Mild Hybrid | ||

| By Battery Type | Lithium-Ion | |

| Nickel-Metal Hydride (NiMH) | ||

| Others (e.g., Sodium-ion, LTO) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the mild hybrid vehicles market expected to be by 2031?

The mild hybrid vehicles market size is forecast to reach USD 164.56 billion by 2031, expanding at a 6.91 % CAGR through 2031.

Which vehicle category is growing fastest within mild hybrids?

Light commercial vans lead growth, projected at an 8.17 % CAGR as fleet operators balance fuel savings against charging-infrastructure limits.

How are suppliers responding to shifting demand?

Western tier-ones are restructuring and forming long-term contracts, while Asian firms expand vertically into batteries and integrated 48V drives.

What role will sodium-ion batteries play?

CATL and BYD have commercialized sodium-ion technology, significantly reducing the costs of 48V packs. This cost reduction enhances the appeal of mild hybrids in markets where affordability is a primary concern.

Page last updated on: