Middle East Satellite Communications Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

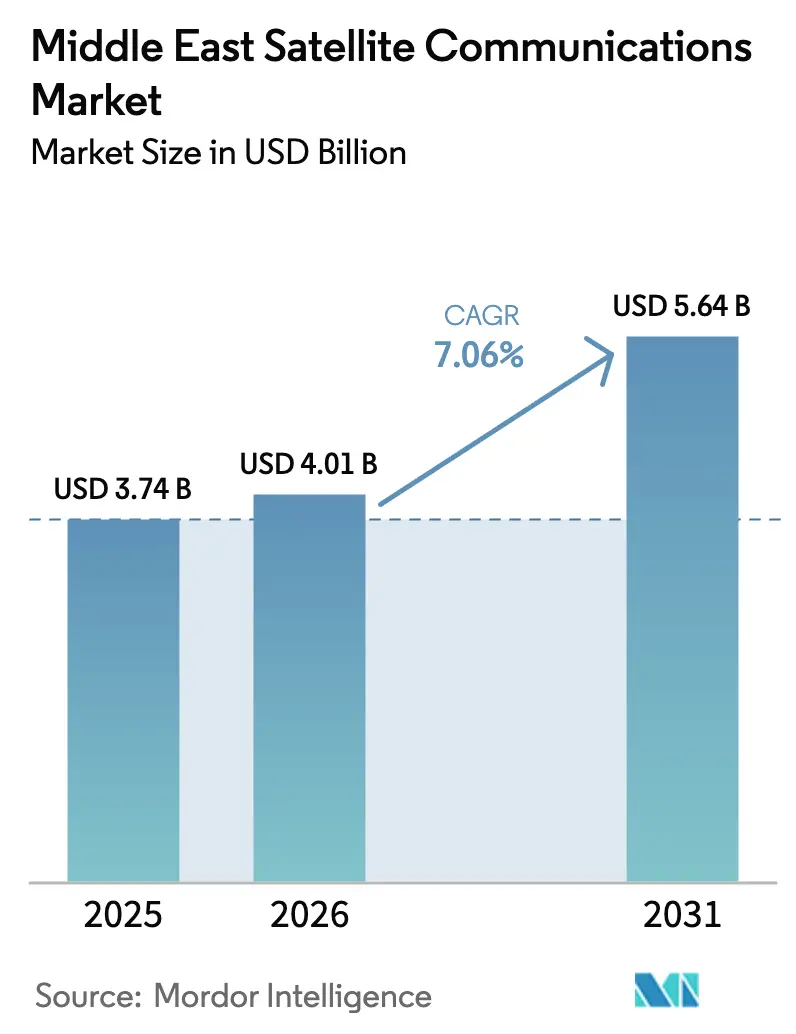

| Base Year Market Size (2025) | USD 3.74 Billion |

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 7.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Satellite Communications Market Analysis by Mordor Intelligence

The Middle East satellite communications market size is projected to expand from USD 3.74 billion in 2025 and USD 4.01 billion in 2026 to USD 5.64 billion by 2031, registering a CAGR of 7.06% between 2026 to 2031. Ongoing universal-broadband programs, rising IoT adoption in remote oilfields, and aggressive low-Earth-orbit (LEO) rollouts are accelerating revenue streams across services, equipment, and platforms. Operators are shifting capital toward multi-orbit networks to reduce latency while leveraging geostationary resilience, a strategy reinforced by Saudi Arabia’s and the UAE’s fast-track licensing regimes. Maritime and aviation connectivity demand, plus methane-monitoring mandates, are broadening the addressable base for data and remote-sensing payloads, while software-defined satellites such as Eutelsat Quantum shorten time-to-market for new applications. At the same time, spectrum congestion along the 57°E-64°E arc and lingering shortages of radiation-hardened chips continue to weigh on deployment schedules.

Key Report Takeaways

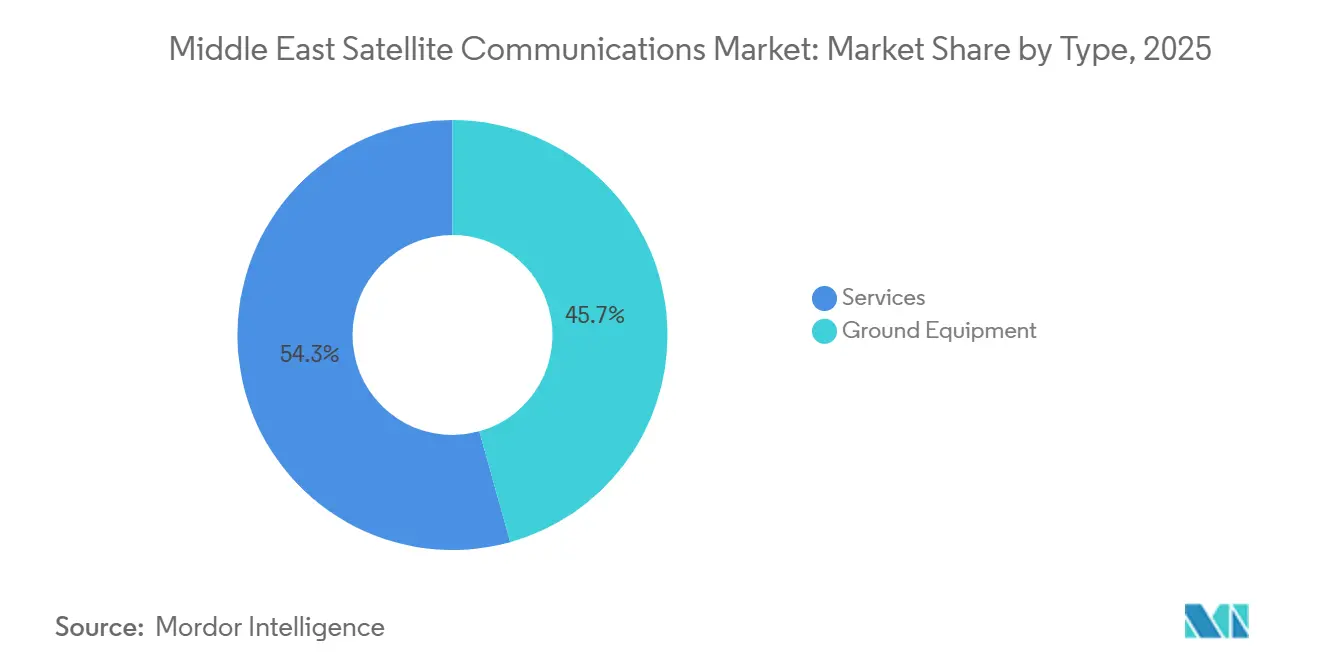

- By type, services led with 54.32% of the Middle East satellite communications market share in 2025, while services revenue is forecast to rise at a 7.52% CAGR to 2031.

- By platform, maritime platforms accounted for 32.11% of revenue in 2025, whereas airborne platform is projected to advance at the fastest 7.81% CAGR over 2026-2031.

- By frequency band, Ku-band retained 41.71% share of the Middle East satellite communications market size in 2025, yet Ka-band is poised for a 7.96% CAGR through 2031.

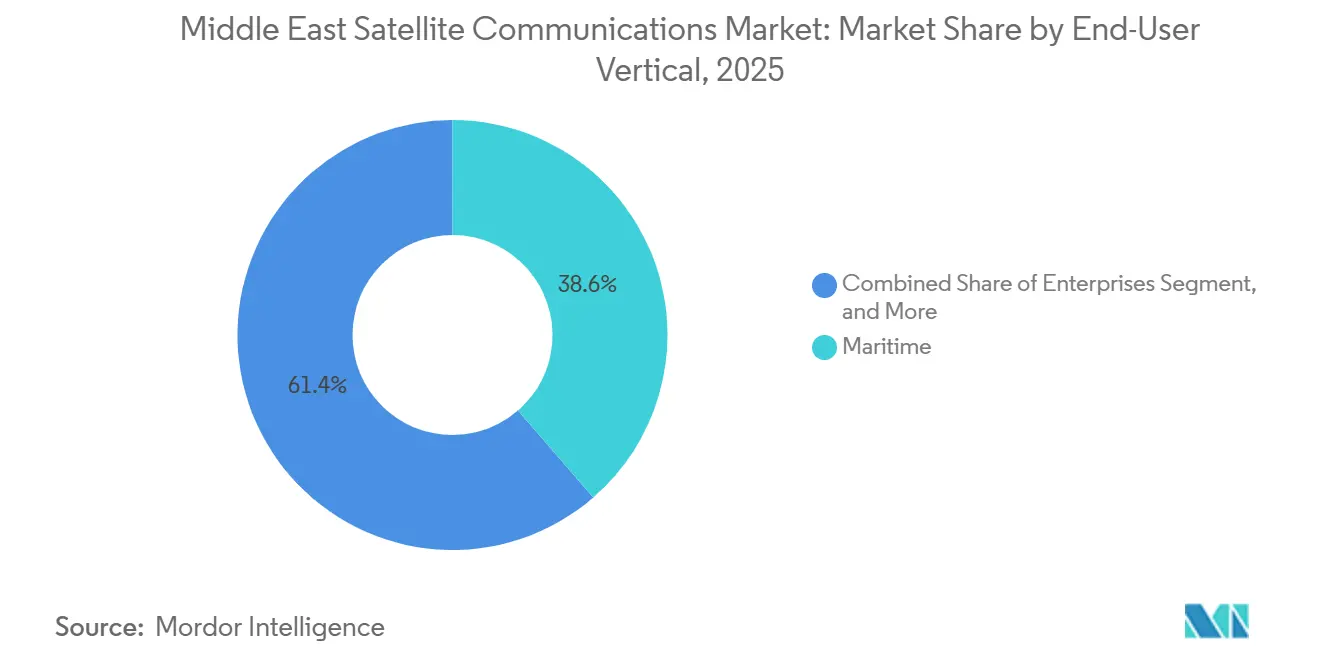

- By end-user, maritime users held 38.63% share in 2025, while enterprises is expected to post the strongest 8.12% CAGR to 2031.

- By application, data communications represented 47.92% of revenue in 2025, whereas remote sensing is forecast to grow at a 7.78% CAGR during 2026-2031.

- By country, Saudi Arabia captured 29.63% of revenue in 2025, and the United Arab Emirates is set to expand the fastest at an 8.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Satellite Communications Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Uptake of IoT-Enabled Oilfield Equipment | +1.2% | Saudi Arabia, UAE, Oman, Qatar | Medium term (2-4 years) |

| Rapid Adoption of VSAT-Based Maritime Connectivity | +1.5% | Gulf shipping lanes, Red Sea, Arabian Sea | Short term (≤ 2 years) |

| Government Programs for Universal Broadband | +1.8% | Saudi Arabia and UAE | Medium term (2-4 years) |

| Growth of Private Inter-Satellite Relay Networks | +0.9% | GCC consortium ground nodes | Long term (≥ 4 years) |

| Rising Demand for Satellite Back-Haul of 5G Private Networks | +1.3% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Expansion of Cooperative Deep-Space Missions | +0.4% | UAE lead, regional partners | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Uptake of IoT-Enabled Oilfield Equipment

Saudi Aramco’s decision to blanket drilling assets with OneWeb LEO backhaul in 2024 signaled a pivot from intermittent VSAT links to always-on sensor connectivity, enabling real-time monitoring of pressure, temperature, and methane leakage.[1]Saudi Aramco, “Aramco and OneWeb Partner to Advance Satellite Connectivity,” aramco.com Saudi Telecom Company’s S-band mobile-satellite launch in 2024 lets upstream operators integrate satellite traffic into core cellular networks, trimming capital outlay by up to 40%. Venture funding for specialist providers, exemplified by OQ Technology’s USD 13 million raise, is lowering device costs below USD 50 per terminal. Methane-monitoring satellites from GHGSat began commercial service for Aramco in September 2024, turning emissions compliance into a recurring connectivity revenue stream. Finally, the ITU’s new L- and S-band allocations for machine-type communications have removed a spectrum bottleneck, allowing Middle East operators to scale IoT links without interference.[2]International Telecommunication Union, “WRC-23 Outcomes,” itu.int

Rapid Adoption of VSAT-Based Maritime Connectivity

Flat-rate LEO packages from Starlink cut per-megabyte costs by nearly 70% versus traditional GEO tariffs, propelling non-geostationary systems to a projected 98% capacity share on vessels by 2034. Viasat’s post-merger Fleet Xpress still secures multi-year Gulf shipping contracts, yet clients now demand hybrid GEO-plus-LEO redundancy to satisfy International Maritime Organization safety mandates. Zamil Offshore’s 2024 fleet-wide VSAT rollout underlines that workboats act as digital nodes, relaying drilling telemetry to shore control centers. UAE regulators issued Starlink maritime licenses in November 2024, setting a technology-neutral precedent that speeds competition and compresses pricing. Technical blueprints from the 5G-ROUTES ferry trials, which proved seamless Ku- and Ka-band handovers, are now being adapted for Red Sea and Arabian Gulf routes.[3]IEEE, “5G-ROUTES Maritime Connectivity Trials,” ieeexplore.ieee.org

Government Programs for Universal Broadband

Saudi Arabia’s Non-Terrestrial Networks roadmap mandates 95% landmass broadband coverage by 2030, reserving fresh Ka- and Q/V-band channels and pushing operators to install multi-gigabit gateways. The UAE’s Space Services Policy slashes satellite-licensing fees by 40% and fast-tracks approvals for LEO firms that invest in local teleports, a move that has already drawn Eutelsat and Starlink ground nodes to Dubai. Saudi Telecom Company prepaid USD 175 million for AST SpaceMobile capacity, underscoring how policy targets convert into large-ticket contracts that de-risk constellation rollouts. The first GCC Space Cooperation Workshop forged a draft plan for shared ground stations and reciprocal spectrum, promising 20-30% savings on infrastructure cost. These measures collectively expand the Middle East satellite communications market by opening underserved interiors and offshore zones.

Rising Demand for Satellite Back-Haul of 5G Private Networks

Energy majors and smart-city developers are installing private 5G cores at refineries, ports, and mines; satellite backhaul lets them bypass fiber gaps and roam across national borders. Saudi Arabia, the UAE, and Qatar are front-running deployments, with early pilots showing 400-600 Mbps downlink speeds via Ka-band gateways. 3GPP Release 17 non-terrestrial standards, adopted regionally in 2024, allow seamless mobility between cell towers and LEO links, cutting integration complexity. Hardware suppliers have responded with ruggedized user terminals rated for 55°C desert heat, enabling year-round outdoor use. As network slices proliferate, operators expect satellite to carry ultra-reliable low-latency traffic for autonomous drones and pipeline robots, further enlarging addressable revenue pools within the Middle East satellite communications market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum Congestion and Cross-Border Frequency Disputes | -1.1% | GCC arc 57°E-64°E | Medium term (2-4 years) |

| High CAPEX of High-Throughput Satellite Upgrades | -0.8% | Global, hits Yahsat and Arabsat | Medium term (2-4 years) |

| Geopolitical Launch-Service Restrictions | -0.3% | Iran, Syria spillovers | Short term (≤ 2 years) |

| Shortage of Radiation-Hardened Chips | -0.5% | Global supply chain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion and Cross-Border Frequency Disputes

The 57°E-64°E arc hosts Yahsat, Intelsat, and SES birds operating dense Ka- and Ku-band beams, leaving little room for new filings without bilateral coordination. Operators now face 12-24-month delays as neighbors negotiate interference clauses, a hurdle that slows new capacity for the Middle East satellite communications market. UAE regulators concede that Q/V-band could relieve pressure, but heavy Gulf humidity forces costly power margins. Starlink’s rapid terminal rollout sparked calls for Saudi price floors, highlighting policy fragmentation. A gap persists with European Q/V-band harmonization, complicating procurement and insurance for regional fleets.

High CAPEX of High-Throughput Satellite Upgrades

Radiation-hardened processors carry 300-500% price premiums, pushing full GEO payload replacement costs well above USD 250 million and stretching upgrade cycles beyond eight years. Launch vehicles remain in short supply, and insurance underwriters insist on mature parts lists. Arabsat’s BADR-8 used optical waveguides to sidestep some component constraints, yet the technology is not field-proven for every transponder class. Accelerated burn-in tests add nine months to lead times, locking in older chipsets and limiting agility. Until regional foundries qualify space-grade lines, capex burdens will temper fleet expansion, moderating overall growth in the Middle East satellite communications market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Outpace Equipment as Recurring Revenue Models Gain Traction

Services contributed 54.32% to the Middle East satellite communications market share in 2025, and the segment is tracking a 7.52% CAGR through 2031. The emergence of non-terrestrial direct-to-device offers, validated by Saudi Telecom Company’s USD 175 million prepayment to AST SpaceMobile, is broadening the addressable base beyond maritime and aviation niches. Earth-observation subscriptions tied to emissions monitoring are another fast-moving pocket, supported by GHGSat’s imaging contracts. Ground equipment held 45.68% share, yet the proliferation of software-defined user terminals is extending replacement cycles, curbing hardware revenue growth. Chinese vendors pricing Ku- and Ka-band kits 40-50% below Western incumbents are forcing local suppliers to pivot toward managed services, reinforcing the region’s shift toward recurring revenue within the Middle East satellite communications market.

Equipment demand remains solid in the near term for high-throughput VSATs used on offshore support vessels and remote drill sites. However, operators now co-locate network operation centers with public clouds in Riyadh and Dubai to shave latency for enterprise workloads, a trend that limits further capex on standalone facilities. As LEO fleets mature, terminal standardization is expected to trim unit prices below USD 300, further tilting the value stack toward bandwidth and software.

By Platform: Airborne Momentum Builds on Defense and In-Flight Connectivity

Maritime platforms owned 32.11% of 2025 revenue, anchored by tanker traffic and offshore rigs, but airborne connectivity is projected to post a 7.81% CAGR to 2031. Gulf carriers such as Emirates and Qatar Airways are refitting wide-body fleets with Ka-band antennas delivering 100 Mbps per passenger, positioning aviation as a showcase for high-capacity LEO trunking. L3Harris’s USD 843 million Golden Dome satellite program underscores regional defense appetite for beyond-line-of-sight links on fighter, UAV, and AEW platforms. Land terminals serving oil refineries and rural sites grow more slowly as fiber creeps deeper into the desert. Portable manpacks, though niche, command premiums because Thuraya-4’s 3GPP compliance lets a single handset provide voice and broadband data.

Commercial operators now test beam-steering antennas that move seamlessly between GEO, MEO, and LEO birds, eliminating window-seat blockage on aircraft and enhancing failover resilience. Maritime incumbents hedge against Starlink by pairing GEO for safety services with LEO for crew welfare, creating hybrid contracts that preserve share yet pressure margin within the Middle East satellite communications market.

By Frequency Band: Ka-Band Emerges as Preferred Growth Engine

Ku-band systems maintained 41.71% share of the Middle East satellite communications market in 2025, thanks to mature hardware and wide installed bases. Yet Ka-band is on track for a 7.96% CAGR into 2031 as operators chase higher spectral efficiency and 16-fold frequency reuse. SES and Intelsat concede Ku-band congestion pushes new inflight projects toward Ka-band, despite heavier rain attenuation in humid coastal belts. L-band, underpinned by Thuraya-4, retains utility for handheld voice, IoT, and safety-of-life services. C-band continues sliding because broadcasters migrate to fiber and OTT distribution. Regulators evaluating Q/V-band feeder links could unlock terabit-class gateway throughput, but equipment ecosystems remain nascent.

Cost-per-bit metrics increasingly favor Ka-band, falling below USD 200 per megabit per second on next-generation birds. Rain fade mitigation via adaptive coding and site diversity is narrowing performance gaps, positioning Ka-band as the de-facto choice for new broadband payloads that will underpin future expansions of the Middle East satellite communications market size.

By End-User Vertical: Enterprises Lead Growth Curve on Private 5G Backhaul

Maritime users held 38.63% revenue share in 2025, reflecting the Gulf’s vessel density, yet the enterprise segment is forecast to accelerate at an 8.12% CAGR through 2031. Energy companies integrate satellite links into private 5G cores for drilling, maintenance drones, and real-time analytics. Defense ministries remain a solid second, financing resilient command loops extending from Yemen to the Horn of Africa. Media contribution is contracting as streaming dominates distribution, forcing operators like Arabsat to redeploy transponders for data and government channels. Agricultural pilots in Qatar and Oman use sub-meter satellite imagery and narrowband IoT sensors to optimize irrigation, offering an early glimpse of diversified demand pools that will sustain expansion of the Middle East satellite communications market.

Corporate CIOs increasingly evaluate satellite connectivity against cloud latency budgets rather than raw megabits. That shift favors low-latency LEO paths bundled with managed security, opening white spaces for integrators skilled in SD-WAN and zero-trust overlays. As spectrum rules harmonize, cross-border enterprise VPNs are likely to become the largest incremental source of bandwidth orders.

By Application: Remote Sensing Climbs on Emissions Compliance

Data communications contributed 47.92% of 2025 revenue, spanning broadband, IoT backhaul, and enterprise VPNs. Remote sensing, however, is projected to clock a 7.78% CAGR, propelled by mandatory methane tracking and precision-agriculture programs. Voice communications remain vital for maritime distress and military coordination, with Thuraya-4 enabling seamless satellite-cellular handoff. Broadcasting continues its structural retreat but still fills rain-fade-resistant C-band beams for disaster recovery. Low-rate IoT packets move over L- and S-band, while video and cloud traffic chase high-throughput Ka-band and LEO pipes.

Commercial regulators now tie flare-gas permits to continuous satellite-based methane reporting, locking in demand for remote-sensing downlinks. Meanwhile, enterprise cloud migrations sustain data-communications volume, ensuring that both application classes jointly underpin growth in the Middle East satellite communications market.

Geography Analysis

Saudi Arabia controlled 29.63% of 2025 revenue, enabled by Vision 2030 subsidies, S-band allocations for non-terrestrial broadband, and Saudi Telecom Company’s large-value LEO commitments. The country’s move to colocate satellite gateways with Riyadh and Jeddah internet exchanges reduces latency to under 50 milliseconds, supporting hyperscale cloud adoption. Universal-service targets require coverage of sparsely populated interiors, guaranteeing a steady stream of capacity purchases that should lift Saudi contributions to the Middle East satellite communications market size through 2031.

The United Arab Emirates is forecast to grow fastest at an 8.02% CAGR, buoyed by TDRA’s licensing reforms and e&’s early adoption of software-defined satellites. Dubai’s free-zone incentives have attracted satellite operations centers from Eutelsat, Starlink, and OneWeb. Deep-space missions such as the Emirates Asteroid Belt probe expand national R&D talent, cross-feeding commercial SatCom projects.

Qatar leverages Es’hailSat’s Doha teleport to anchor regional broadcast and enterprise traffic. Ooredoo’s 4G/5G-ready offshore network trials prove that LEO backhaul can integrate with Ericsson terrestrial gear, demonstrating templates for Oman and Kuwait. Turkey’s growing satellite manufacturing base promises regional supply-chain resiliency but faces procurement barriers in GCC tenders. The rest of the Middle East Jordan, Iraq, Lebanon, Yemen relies heavily on humanitarian VSAT deployments led by UN agencies, creating stable though modest demand pockets.

Competitive Landscape

Incumbent GEO operators Yahsat, Arabsat, and Thuraya accounted for major share of regional revenue in 2025, yet face mounting competition from LEO entrants Starlink, OneWeb, and AST SpaceMobile. Defensive plays include Arabsat’s talks to lease Telesat Lightspeed capacity and Space42’s optical link integration on Thuraya-4. GEO safety channels layered with LEO broadband to meet latency and redundancy benchmarks.

Chinese terminal vendors undercut Western equipment by up to 50%, pushing Cobham and L3Harris to bundle managed services. Software-defined satellites such as Eutelsat Quantum let operators reposition beams overnight, shortening provisioning cycles from months to hours. Optical inter-satellite links, validated by ESA terabit demonstrations, now feature in regional procurement specs, while 3GPP compliance unlocks direct connections into mobile cores without separate gateways. Regulatory fast-tracks in Saudi Arabia and the UAE amplify churn by lowering entry costs, though export controls on radiation-hardened parts still advantage incumbents with established supply-chain relationships.

Growth niches span direct-to-device broadband, IoT-as-a-service for oil producers, and shared optical relay networks. Early-mover alliances such as stc’s USD 175 million AST SpaceMobile deal confirm commercial appetite for smartphone-grade satellite links. Market consolidation is possible as GEO incumbents vie for LEO partnerships to preserve share in the expanding Middle East satellite communications market.

Middle East Satellite Communications Industry Leaders

Al Yah Satellite Communications Company PJSC (Yahsat)

Inmarsat Global Limited (now Viasat Inc.)

Arab Satellite Communications Organization

Intelsat S.A.

Eutelsat Communications S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: MBRSC signed a cooperation MoU with Colombian agencies, expanding the UAE’s global partnerships.

- January 2026: Es’hailSat showcased teleport capabilities at IBC 2025 to court broadcasters and enterprises.

- December 2025: Space42 and Cobham Satcom released a full Thuraya-4 terminal suite compliant with 3GPP non-terrestrial standards.

- November 2025: Space42 activated Thuraya-4, the first L-band satellite with optical inter-satellite links serving Europe, Africa, and the Middle East.

Middle East Satellite Communications Market Report Scope

Satellite communication is the transfer of data and information via satellites orbiting the Earth. It enables long-distance communication by relaying signals between ground stations and satellite receivers in orbit, enabling television broadcasts, internet access, and phone calls.

The Middle East Satellite Communications Market Report is Segmented by Type (Ground Equipment including Satellite Gateway, VSAT Equipment, Network Operation Center, Satellite News Gathering Equipment; Services including Mobile Satellite Services, Earth Observation Services), Platform (Portable, Land, Maritime, Airborne), Frequency Band (L-Band, C-Band, Ku-Band, Ka-Band), End-User Vertical (Maritime, Defense and Government, Enterprises, Media and Entertainment, Oil and Gas, Other End-User Verticals), Application (Voice Communications, Data Communications, Broadcasting, Remote Sensing), and Country (Saudi Arabia, United Arab Emirates, Qatar, Oman, Kuwait, Turkey, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

| Ground Equipment | Satellite Gateway |

| VSAT Equipment | |

| Network Operation Center (NOC) | |

| Satellite News Gathering (SNG) Equipment | |

| Services | Mobile Satellite Services (MSS) |

| Earth Observation Services |

| Portable |

| Land |

| Maritime |

| Airborne |

| L-Band |

| C-Band |

| Ku-Band |

| Ka-Band |

| Maritime |

| Defense and Government |

| Enterprises |

| Media and Entertainment |

| Oil and Gas |

| Other End-User Verticals |

| Voice Communications |

| Data Communications |

| Broadcasting |

| Remote Sensing |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Turkey |

| Rest of Middle East |

| By Type | Ground Equipment | Satellite Gateway |

| VSAT Equipment | ||

| Network Operation Center (NOC) | ||

| Satellite News Gathering (SNG) Equipment | ||

| Services | Mobile Satellite Services (MSS) | |

| Earth Observation Services | ||

| By Platform | Portable | |

| Land | ||

| Maritime | ||

| Airborne | ||

| By Frequency Band | L-Band | |

| C-Band | ||

| Ku-Band | ||

| Ka-Band | ||

| By End-User Vertical | Maritime | |

| Defense and Government | ||

| Enterprises | ||

| Media and Entertainment | ||

| Oil and Gas | ||

| Other End-User Verticals | ||

| By Application | Voice Communications | |

| Data Communications | ||

| Broadcasting | ||

| Remote Sensing | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Turkey | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the current value of the Middle East satellite communications market?

The market is valued at USD 4.01 billion in 2026 and is on course to reach USD 5.64 billion by 2031.

Which platform segment is growing the fastest in the region?

Airborne connectivity is forecast to expand at a 7.81% CAGR, driven by inflight Wi-Fi upgrades and defense procurements.

Why is Ka-band gaining traction over Ku-band?

Ka-band offers wider bandwidth and higher frequency-reuse factors, enabling lower cost-per-bit even though it requires rain-fade mitigation.

How are universal-broadband mandates influencing demand?

Saudi Arabia and the UAE tie national broadband targets to satellite capacity contracts, guaranteeing traffic for both GEO and LEO operators.

What role do private 5G networks play in market growth?

Enterprises deploy private 5G cores at remote sites and rely on satellite backhaul for coverage continuity, propelling the fastest-growing end-user segment.

Which country is expected to lead market growth through 2031?

The United Arab Emirates is projected to record the highest CAGR at 8.02% as policy reforms attract multi-orbit operators and ground-segment investors.

Page last updated on: